Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

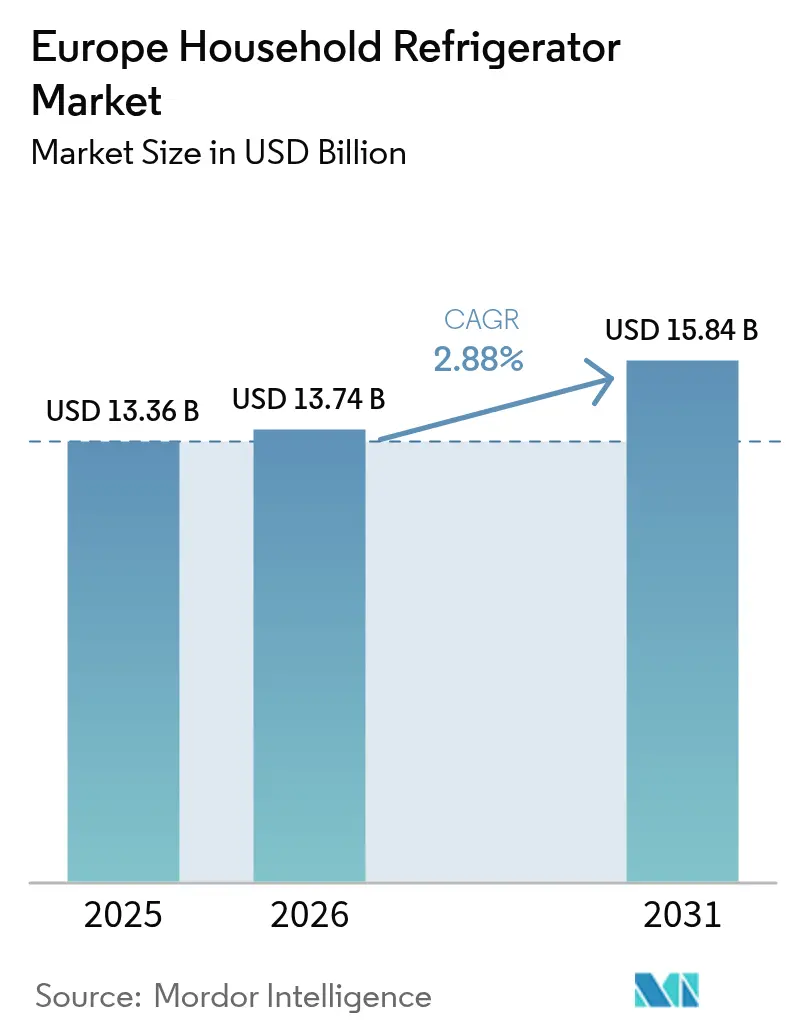

| Base Year Market Size (2025) | USD 13.36 Billion |

| Market Size (2026) | USD 13.74 Billion |

| Market Size (2031) | USD 15.84 Billion |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

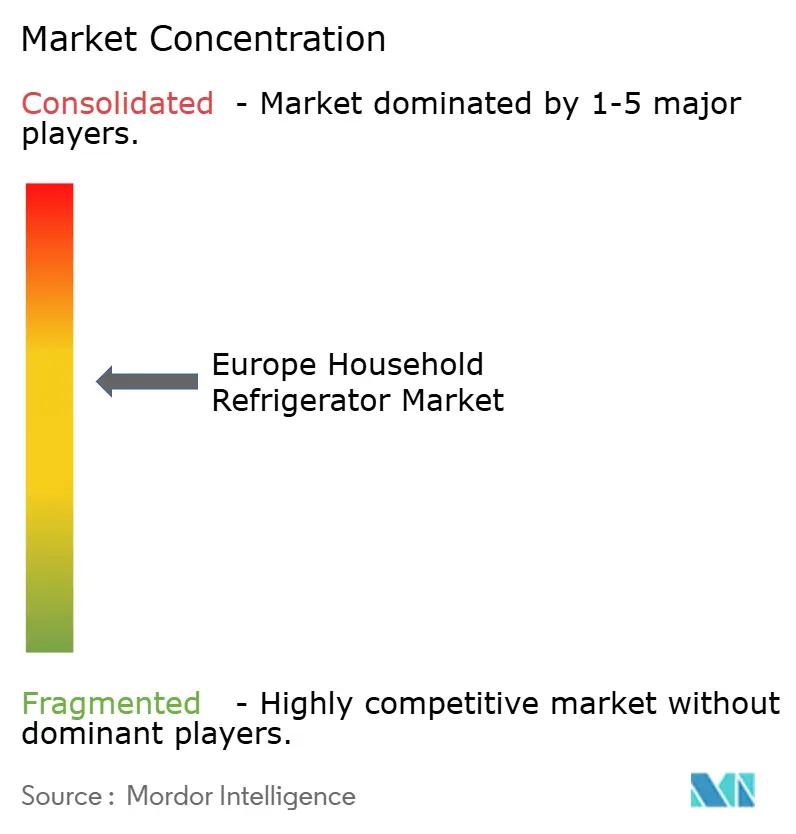

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Household Refrigerator Market Analysis by Mordor Intelligence

The Europe household refrigerator market size is expected to grow from USD 13.36 billion in 2025 to USD 13.74 billion in 2026 and is forecast to reach USD 15.84 billion by 2031 at 2.88% CAGR over 2026-2031. The measured expansion reflects a maturing replacement-driven environment where EU energy labels, now recognized by 93% of consumers, push households toward higher-efficiency models[1]European Commission, “Energy Labelling and Ecodesign,” europa.eu. Regulatory moves such as the Right to Repair directive compel brands to hold spare parts for seven years, extending product lifecycles while still catalyzing upgrades when older units fail to meet new standards. Elevated electricity tariffs significantly higher than US averages—amplify consumer sensitivity to running costs, accelerating demand for A-class appliances. On the supply side, the F-gas regulation inflates prices for legacy refrigerants by up to 1,000%, nudging manufacturers toward propane and CO₂ systems that remain competitively priced at EUR 5-15 per kg. Within this policy-shaped arena, the European household refrigerator market experiences resilient volume even as value growth hinges on premium features, smart connectivity, and circular-economy compliance.

Key Report Takeaways

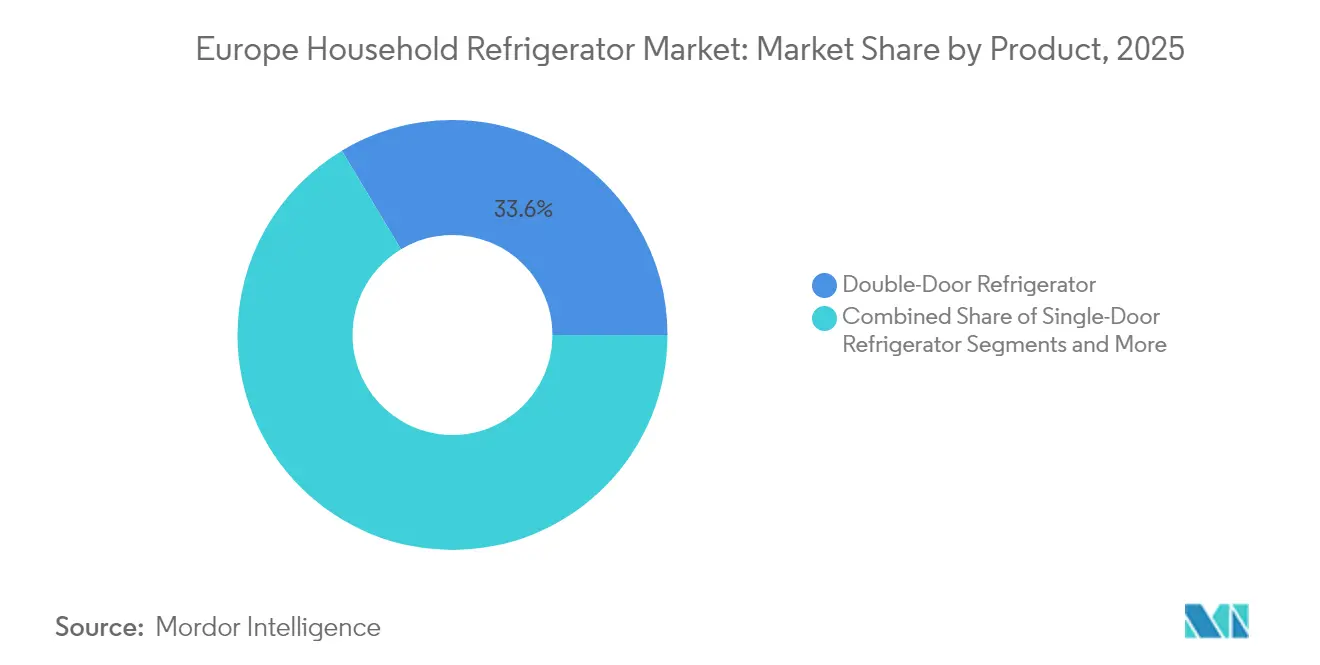

- By product, double-door refrigerators led with 33.60% revenue share of the Europe household refrigerator market in 2025, while French-door models are projected to post a 5.35% CAGR through 2031.

- By structure, freestanding units retained 67.40% share in 2025; built-in models hold the fastest trajectory at 5.70% CAGR to 2031.

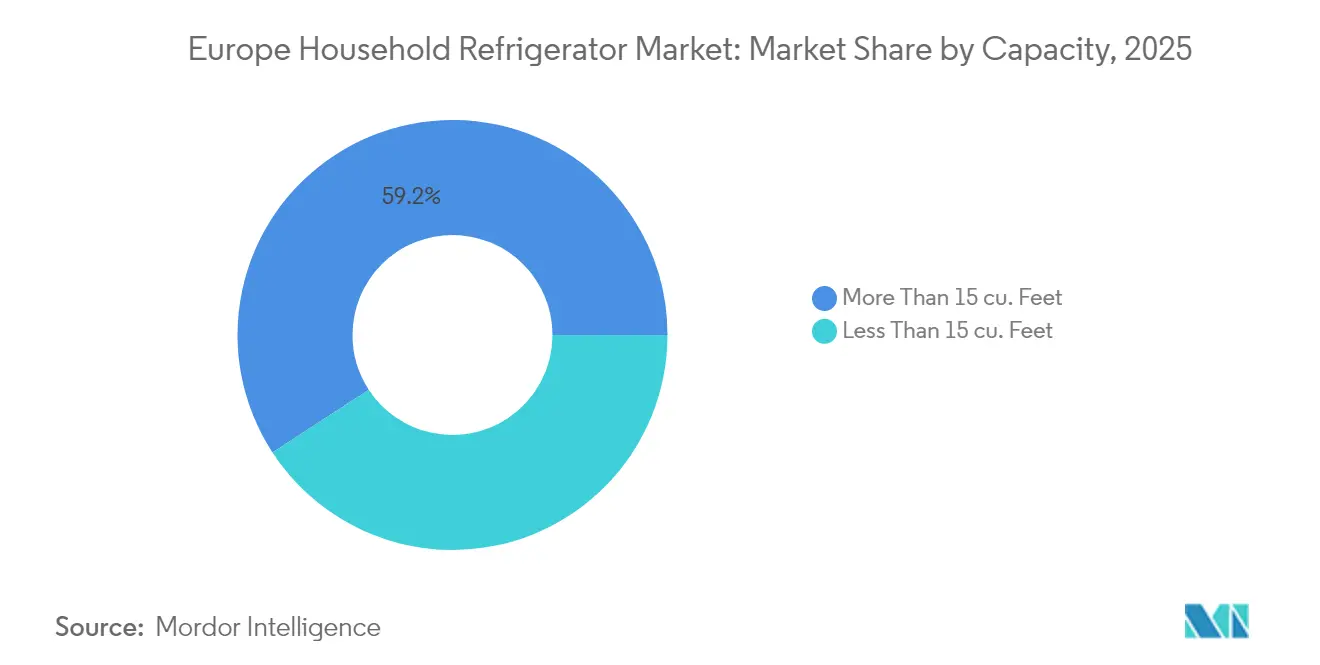

- By capacity, models exceeding 15 cu ft accounted for 59.20% of the Europe household refrigerator market size in 2025 and are expected to grow at a 4.65% CAGR.

- By distribution channel, multi-brand stores dominated with a 44.30% share in 2025, yet online sales will expand at a 6.45% CAGR to 2031.

- By geography, Germany contributed 16.80% of 2025 revenue, whereas BENELUX is set to advance at 5.05% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Household Refrigerator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Energy-Efficiency Regulations and Incentives | 0.80% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Rapid Smart-Appliance Penetration and IoT Interoperability | 0.60% | BENELUX, NORDICS, Germany | Long term (≥ 4 years) |

| High Replacement Demand from Ageing Installed Base | 0.70% | Germany, UK, France | Short term (≤ 2 years) |

| Expansion of Organised Retail and Last-Mile Cold-Chain Logistics | 0.30% | Germany, France, UK urban centers | Medium term (2-4 years) |

| VPP-Ready Refrigerators Enabling Demand-Response Revenues | 0.40% | NORDICS, Germany, Netherlands | | Long term (≥ 4 years) |

| Circular-Economy Subsidies for Refurbishment and Repair Schemes | 0.20% | France, Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Energy-Efficiency Regulations and Incentives

The European Commission’s new Ecodesign for Sustainable Products Regulation is giving appliance makers an extra push. Under its 2025–2030 agenda, household devices take top billing, and manufacturers must now build products that last longer, can be repaired more easily, and carry clear labels showing their carbon footprint. The Ecodesign for Sustainable Products Regulation accelerates replacement cycles by requiring durability, repairability, and carbon disclosure across household refrigeration lines. Moving to a clear A-G energy scale eliminates label confusion while digital product passports allow authorities to trace registered models, phasing out non-compliant stock. Consumer savings reached EUR 90 billion in 2022 and are projected at EUR 150 billion by 2030, anchoring a policy-led runway for the European household refrigerator market.

Rapid Smart-Appliance Penetration and IoT Interoperability

The EU Code of Conduct for energy-smart appliances, launched in April 2024, harmonizes protocols so refrigerators seamlessly join demand-side flexibility programs[2]Joint Research Centre, “EU Code of Conduct on Energy-Smart Appliances,” jrc.ec.europa.eu. Commitments from Arçelik, Daikin, and Electrolux ensure compliant models within a year. LG’s 80% stake in Dutch platform Athom attaches Homey Pro’s 50,000-device ecosystem to its white-goods portfolio, affirming that connected features now justify premium pricing. Academic trials show home-energy management can cut household consumption by 57%, translating connectivity into measurable savings.

High Replacement Demand from Ageing Installed Base

Refrigerators bought before 2010 approach end-of-life just as newer rules tighten, igniting a replacement wave that shields volumes from macro-slowdowns. Average lifespans of 10-15 years mean non-A-class units incur high operating costs, propelling trade-ups despite inflation. BSH Hausgeräte sustained European share during a contracting 2024 market, illustrating how replacements underpin the European household refrigerator market. EU labels have already slashed average per-unit energy draw by 60% since 1994.

Expansion of Organised Retail and Last-Mile Cold-Chain Logistics

Wider coverage of specialist retailers and rapid-delivery services simplifies bulky-goods fulfilment, removing friction for online conversions. Urban hubs in Germany, France, and the UK lead turnkey installation offerings that speed adoption of larger, feature-rich models. Retailers exploit omnichannel data to target households nearing end-of-life cycles, raising replacement capture rates and supporting the European household refrigerator market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile steel and compressor input costs | -0.50% | Germany, Italy production hubs | Short term (≤ 2 years) |

| Intensifying price competition from Chinese OEM imports | -0.30% | All EU markets | Medium term (2-4 years) |

| Consumer confusion over new EU energy labels | -0.20% | EU-wide | Short term (≤ 2 years) |

| Delivery delays from ADR rules on refrigerant or battery shipping | -0.10% | BENELUX, Germany corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Steel and Compressor Input Costs

European manufacturers operate 130 plants that absorb wide swings in steel and compressor pricing, eroding margins just as energy costs run 2-3 times US levels[3]APPLiA, “Home Appliance Industry Economic Report,” applia-europe.eu. The new F-gas regime further inflates high-GWP refrigerant costs, forcing swift conversion to natural alternatives. BSH’s EUR 850 million R&D outlay in 2023 underscores the capex required to counter cost spikes via design efficiency.

Intensifying Price Competition from Chinese OEM Imports

Chinese shipments of 4.48 billion household appliances in 2024 place sustained deflationary pressure on mid-range segments. Cixi City alone exported RMB 2.41 billion worth of refrigerators, demonstrating persistent capacity buildup aimed at the European household refrigerator market. European players, therefore, lean into premium differentiation—energy savings, smart features, and robust after-sales—to safeguard pricing power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: French-Door Innovation Drives Premium Migration

Double-door formats anchored 33.60% of 2025 shipments, thriving on familiarity and mid-price positioning. French-door units, though still a minority, will sprint at 5.35% CAGR between 2026-2031, outpacing the European household refrigerator market’s overall rhythm. Yet rising urban affluence calls for wider shelf space and discreet vegetable drawers, propelling French-door adoption. The broader cabinet allows manufacturers to bundle multi-zone cooling, touchscreens, and camera-based inventory tracking that meet EU smart-appliance interoperability codes.Growth feeds off replacement demand: households with ageing double-door models weigh operating costs against the energy savings achievable with fresh A-class French-door offerings. BSH dedicates 5.5% of turnover to R&D, channelling funds into premium models that integrate Home Connect platforms for predictive maintenance. This reinforces brand stickiness and cushions margins amid Chinese pricing pressure, underlining why French-door innovation is pivotal for the European household refrigerator market.

By Structure: Built-In Segment Accelerates Despite Freestanding Dominance

Freestanding designs accounted for 67.40% of 2025 shipments, favored by renters and value-seekers who prize easy relocation. Built-in appliances, however, are poised for a 5.70% CAGR as renovation cycles in dense European cities emphasize seamless cabinetry. Energy-label reforms further encourage integrated units because owners anticipate keeping them for longer, diluting the upfront cost premium across an extended lifespan.Manufacturers respond with telescopic installation kits and slimmer compressor housings that reclaim cabinet depth without reducing capacity. The EU’s durability criteria, embedded in the Ecodesign regulation, align with built-in quality, ensuring lower failure rates and fewer service calls over 15-plus years. As kitchens evolve into open-plan social spaces, built-in formats satisfy aesthetic demands while helping brands capture high-margin upgrades in the Europe household refrigerator market.

By Capacity: Large-Format Units Dominate Growth Trajectory

Refrigerators above 15 cu ft captured 59.20% of 2025 demand and will expand 4.65% annually, buoyed by bulk-shopping trends arising from hybrid work lifestyles. Enhanced compressor and insulation technologies let bigger cabinets achieve the same A-class ratings once exclusive to compact models, neutralizing energy-cost objections. The Europe household refrigerator market size for >15 cu ft units is projected to widen faster than any smaller category through 2031.Feature bundling intensifies in this size band: variable-speed compressors, humidity-controlled produce drawers, and door-within-door beverage zones make large units a canvas for upselling. Natural-refrigerant adoption is also simplest at scale because interior volume offsets any cost delta, strengthening compliance with tight F-gas quotas. Households thus view upsizing as both an energy and lifestyle upgrade, sustaining the capacity-led growth story.

By Distribution Channel: Digital Transformation Reshapes Retail Landscape

Traditional multi-brand outlets still secure 44.30% of 2025 turnover, offering live demos and turnkey installation, critical for bulky goods. Online channels nevertheless clock 6.45% CAGR as logistics firms master two-man delivery, reverse pickup of old units, and on-site connection of water dispensers or home-hub networks. Covid-era comfort with high-ticket e-purchases persists, pushing brands to fine-tune web configurators that calculate lifetime energy savings—an argument compelling enough for cost-sensitive households facing elevated power tariffs.Exclusive brand stores extend the omnichannel spectrum, letting manufacturers retain margin and gather first-party usage data via IoT enrolment. Such telemetry supports personalized upsell campaigns and predictive maintenance alerts, locking customers into the European household refrigerator market’s premium ecosystem and limiting churn toward budget imports.

Geography Analysis

By geography, Germany contributed 16.80% of 2025 revenue, whereas BENELUX is set to advance at 5.05% CAGR between 2026-2031. Germany remains the anchor for the European household refrigerator market, combining a large population with stringent efficiency norms that compel timely replacements. Local buyers gravitate toward premium German-made brands, rewarding firms that align with emerging VPP services and offering ample headroom for connected, A-class French-door units. Domestic retailers benefit from well-funded financing programs that soften upfront costs, helping manufacturers defend price positioning even against import pressure.BENELUX adds high-margin momentum. Compact city apartments favor built-in formats, and household broadband penetration above 95% streamlines smart-appliance adoption. National grid operators in the Netherlands are among the first to issue dynamic-tariff contracts that pay consumers for flexible load shifting, catalyzing VPP-ready refrigerator sales. Belgium’s warranty-backed circular-economy subsidies further stimulate uptake of durable, repairable models, reinforcing compliance-value messaging.Elsewhere, France’s repairability index informs purchase decisions, while Spain and Italy pivot on tourism-driven second-home refurbishment that boosts medium-capacity demand. Nordic nations top per-capita spending on refrigeration and lead natural-refrigerant penetration, setting design standards envied by the wider Europe household refrigerator market. Collectively, these distinct trajectories create a pan-European tapestry that allows manufacturers to spread risk and tailor innovation strategies by region.

Competitive Landscape

European refrigeration remains moderately concentrated. BSH Hausgeräte, Whirlpool (now Beko Europe), and Electrolux together controlled a significant share of shipments in 2024, each bulwarked by scale manufacturing, proprietary IoT ecosystems, and deep regulatory engagement. BSH’s EUR 850 million R&D commitment advances energy-efficient compressors and modular interiors attuned to EU durability mandates.

Tech acquisition underpins differentiation. LG’s purchase of Athom gives it the Homey Pro platform, instantly widening native compatibility and letting its refrigerators speak to 50,000 third-party devices—an edge in interoperability-driven Europe. Meanwhile, Midea’s acquisition of Küppersbusch’s parent provides a local flag for Chinese entry into premium niches, sidestepping quotas and offering German-heritage branding to counter skittish consumers.

Chinese OEMs nonetheless squeeze margins on value-led SKUs, flooding the channel with competitively priced freestanding models. European incumbents retaliate by accentuating after-sales reliability, natural-refrigerant leadership, and EU-compliant repair networks—advantages harder for importers to replicate. The next battleground lies in VPP-ready features, where early compliance with demand-response security protocols may cement first-mover preference across the Europe household refrigerator market.

Europe Household Refrigerator Industry Leaders

BSH Hausgeräte GmbH (Bosch-Siemens)

Whirlpool Corp.

Samsung Electronics Co. Ltd.

LG Electronics Inc.

Haier Smart Home Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: European Commission ratified the 2025-2030 Ecodesign working plan, raising durability and carbon-footprint disclosure standards for refrigerators.

- April 2025: Midea acquired Küppersbusch's parent company, Teka Group, deepening its penetration of Europe’s premium appliance niches.

- January 2025: BSH Hausgeräte posted a EUR 15.3 billion 2024 turnover while investing 5.5% of sales in R&D to reinforce innovation leadership.

- September 2024: The European Commission adopted revised F-gas rules effective in 2025, tightening refrigerant quota and labeling requirements.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the household refrigerator market as all new, electrically powered cold-storage units sold for residential food preservation across Europe, covering single-door, double-door, side-by-side, French-door, and built-in formats. Values reflect factory-gate revenue plus standard channel margins, expressed in constant 2024 USD.

Scope Exclusions: Chest freezers, wine coolers, and any equipment intended primarily for commercial kitchens are outside scope.

Segmentation Overview

- By Product

- Single-Door Refrigerator

- Double-Door Refrigerator

- Top Freezer

- Bottom Freezer

- Side-By-Side Door Refrigerator

- French-Door Refrigerator

- Other Refrigerators

- By Structure

- Built-In

- Freestanding

- By Capacity

- Less Than 15 cu. Feet

- More Than 15 cu. Feet

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed appliance retailers, category buyers, energy-label consultants, and after-sales technicians across Germany, Italy, France, the Nordics, and the U.K. Their insights on sell-out volumes, average selling prices, replacement cycles, and regulatory pinch points filled data gaps and validated model assumptions.

Desk Research

We started with Eurostat production indices, UN Comtrade trade flows for HS 8418, and APPLiA shipment releases; these sources outline unit flows and average export prices. Energy-efficiency updates from the European Commission Eco-design database, household expenditure tables from Eurostat, and national statistics offices (e.g., Destatis, INSEE) helped anchor demand patterns. Company filings captured through D&B Hoovers, complemented by news archives on Dow Jones Factiva, supplied pricing and mix shifts. This list is illustrative; many additional open datasets informed our desk work.

A second pass checked patent activity on Questel and promotional claims in retailer circulars to gauge smart-feature adoption, while electricity price series from Eurostat framed running-cost sensitivity. Together, these strands provided the factual spine against which later estimates were tested.

Market-Sizing & Forecasting

A top-down supply-pool build was constructed from European production plus net imports, then priced using blended ex-factory ASPs gathered above and checked against sampled retailer shelf prices. Select bottom-up benchmarks, vendor revenue roll-ups and e-commerce channel checks, tempered totals. Key variables feeding the model include household formation, electricity price index, EU A-to-G energy-label penetration, average replacement cycle length, and online share of major-appliance sales. Forecasts to 2030 rely on multivariate regression linked to these drivers, with scenario analysis covering energy-price shocks.

Data Validation & Update Cycle

Outputs pass variance and outlier checks before senior analyst sign-off. We refresh every twelve months, triggering interim updates for material events such as tariff changes or major regulation, so clients receive the most current view.

Why Mordor's Europe Household Refrigerator Baseline Holds Firm

Published estimates often diverge because firms apply different product scopes, pricing layers, and refresh cadences.

According to Mordor Intelligence, our disciplined scope and annual refresh limit drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.36 billion (2025) | Mordor Intelligence | |

| USD 17.06 billion (2024) | Global Consultancy A | Freezers and small commercial units included, broader scope |

| USD 15.90 billion (2024) | Data-Analytics Firm B | Consumption-value method, fixed 2023 EUR-USD rate, limited online sales capture |

| USD 15.20 billion (2023) | Research Outlet C | Older base year carried forward at flat CAGR, no premium ASP adjustment |

Taken together, the comparison shows that Mordor's clear scope choices, transparent variables, and yearly re-validation yield a balanced, decision-ready baseline clients can trace and replicate.

Key Questions Answered in the Report

What is the current value of the Europe household refrigerator market?

The market is valued at USD 13.74 billion in 2026 and is projected to reach USD 15.84 billion by 2031 at a 2.88% CAGR.

Which product segment is growing fastest?

French-door refrigerators are advancing at 5.35% CAGR, outpacing all other formats due to premium features and larger capacities.

How significant are online sales for refrigerators in Europe?

Online channels account for a smaller base today but are expected to expand at 6.45% CAGR, eroding the 44.30% share still held by multi-brand stores.

Why are natural refrigerants gaining traction?

High-GWP refrigerants face cost inflation up to 1,000% under EU F-gas rules, while propane and CO₂ remain stable, driving manufacturers toward low-impact alternatives.

What role do smart capabilities play in purchasing decisions?

EU interoperability standards and demand-response incentives make connected refrigerators more attractive, with studies showing up to 57% household energy savings when integrated into energy-management platforms.

How does the Right to Repair directive influence replacement cycles?

Although it mandates seven-year spare-parts availability, consumers often choose new A-class models because energy savings outweigh repair costs on ageing, less-efficient units, sustaining the replacement-driven Europe household refrigerator market.

Page last updated on: