Household Refrigerators And Freezers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

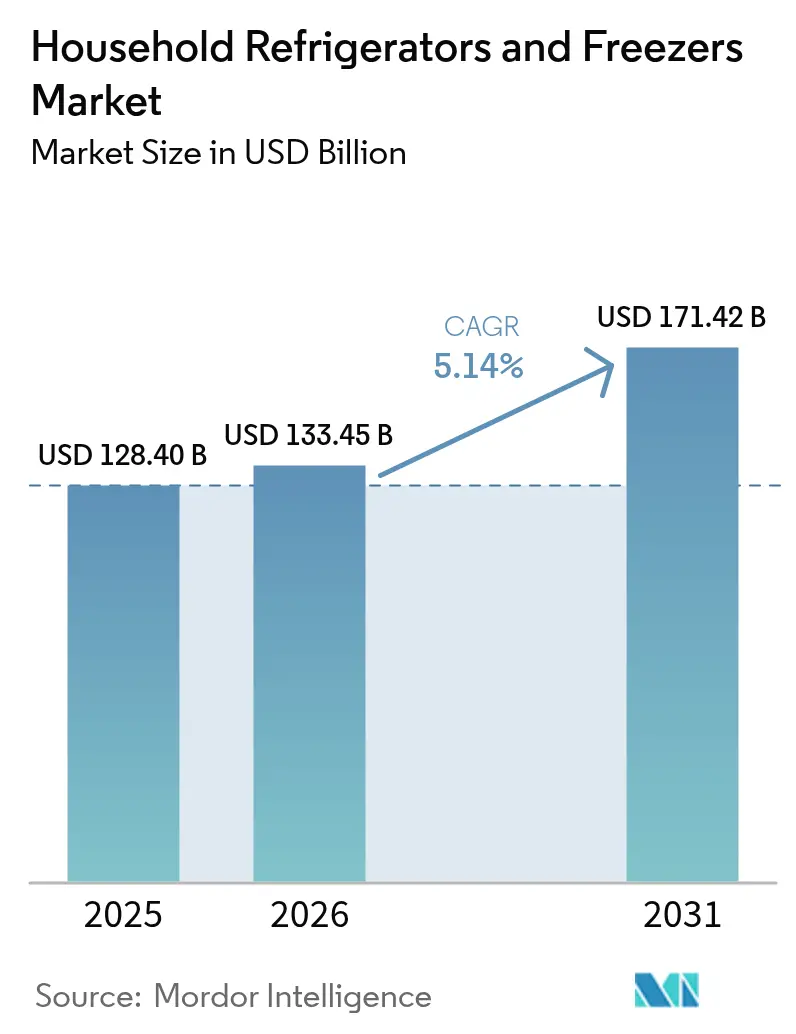

| Market Size (2026) | USD 133.45 Billion |

| Market Size (2031) | USD 171.42 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Household Refrigerators And Freezers Market Analysis by Mordor Intelligence

The household refrigerators and freezers market size was USD 128.40 billion in 2025, is set to reach USD 133.45 billion in 2026, and is forecast to rise to USD 171.42 billion by 2031, reflecting a 5.14% CAGR during 2026-2031. The global household refrigerators and freezers market is driven by rising urbanization, increasing disposable incomes, and growing demand for energy-efficient appliances. Changing lifestyles, nuclear families, and higher consumption of processed and frozen foods further boost demand, while technological advancements such as smart and connected refrigeration enhance product adoption globally. Regulatory momentum on energy efficiency and refrigerant transitions, combined with wider adoption of the Matter standard and faster online channel penetration, is reshaping product roadmaps and retail strategies within a compressed timeframe. China’s 2024 appliance trade-in push showed that targeted incentives can lift sell-through even in saturated categories, a pattern that favors policy-aware planning in the household refrigerators and freezers market[1]. The most resilient growth positions are mid-capacity formats tuned to price-sensitive urban households in Asia-Pacific, supported by e-commerce financing and omnichannel fulfillment expansions in key cities.

Key Report Takeaways

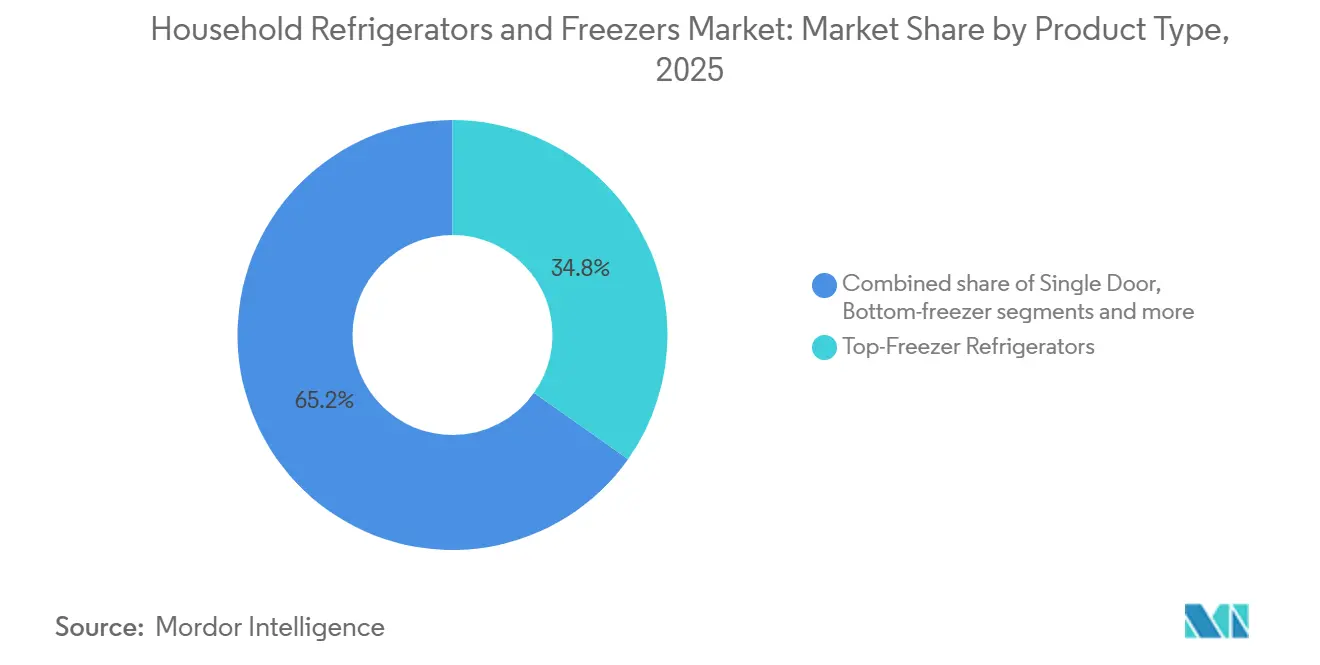

- By product type, top-freezer refrigerators held 34.81% of the household refrigerators and freezers market share in 2025, and French-door units are forecast to expand at 6.75% CAGR through 2031, the fastest among product types.

- By capacity, the 19-22.9 cubic foot bracket accounted for 31.64% of the household refrigerators and freezers market share in 2025, and units at or above 23 cubic feet are projected to grow at a 5.68% CAGR to 2031.

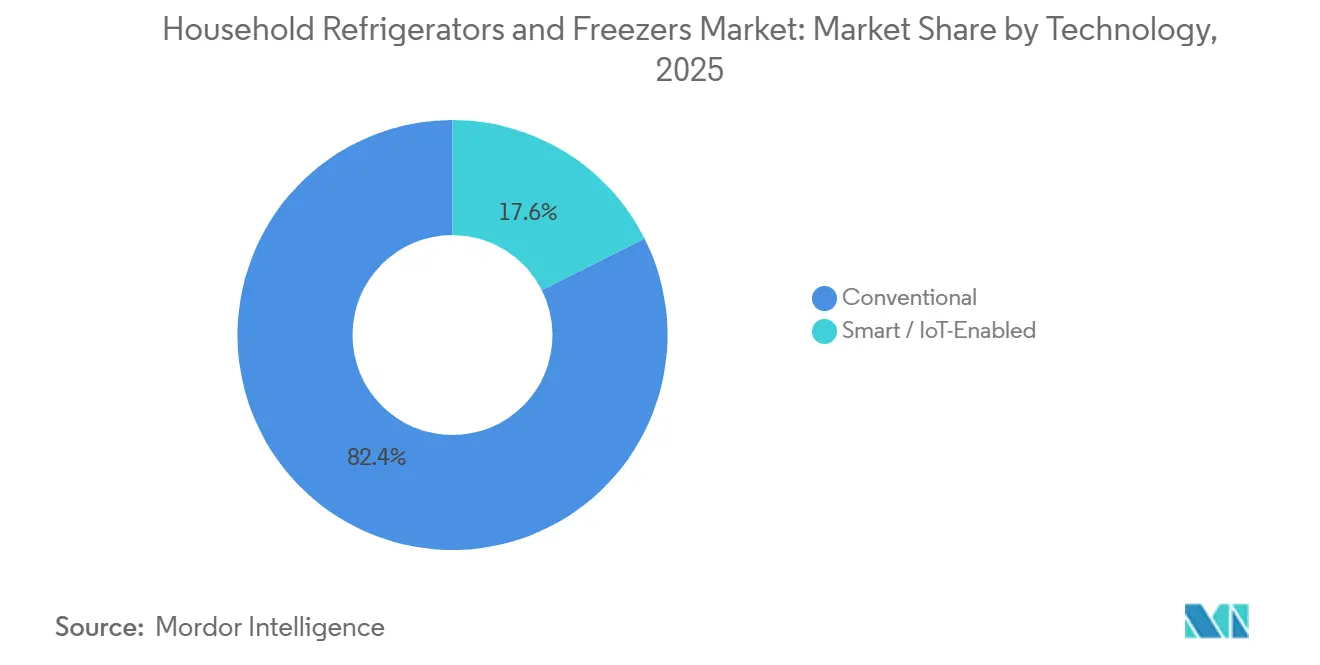

- By technology, conventional models represented 82.41% of the household refrigerators and freezers market share in 2025 sales, and smart/IoT-enabled variants are expected to grow at a 6.65% CAGR through 2031.

- By distribution channel, multi-brand stores led with 46.20% of the household refrigerators and freezers market share in 2025, and online channels are set to expand at 8.14% CAGR over the forecast period.

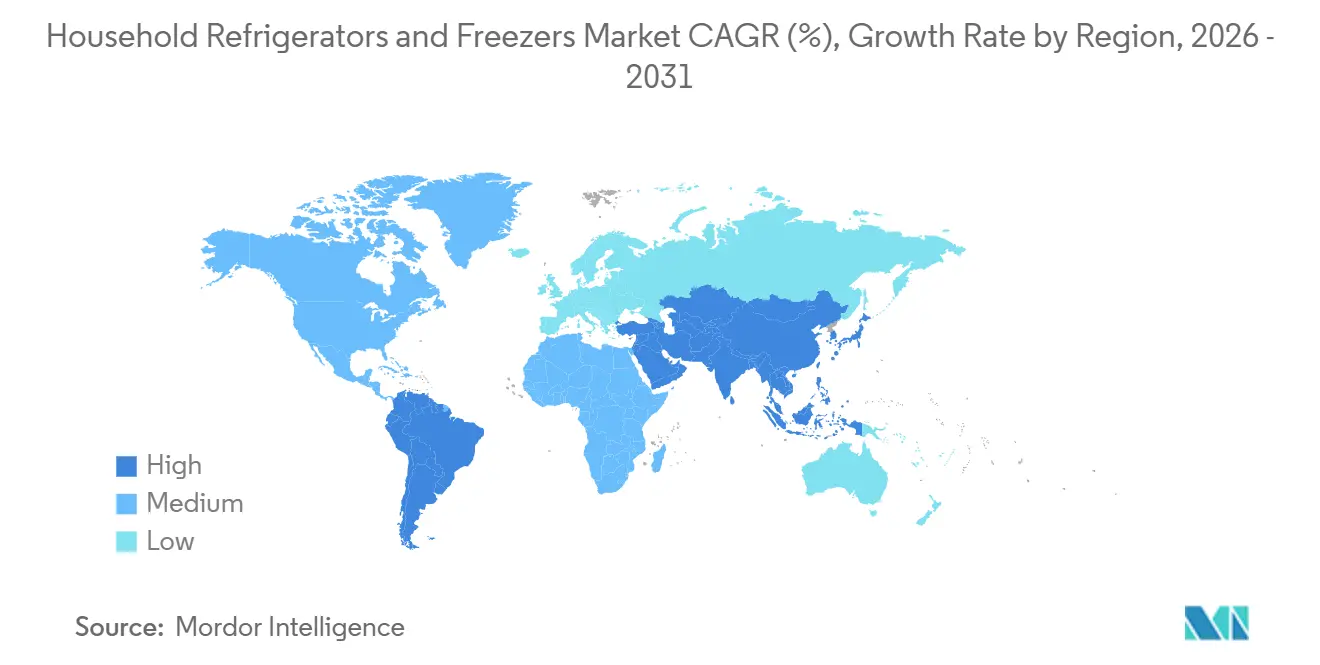

- By geography, North America led with 39.30% of the household refrigerators and freezers market share in 2025, while Asia-Pacific is projected to record the fastest growth at 5.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Household Refrigerators And Freezers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening energy-efficiency standards | +1.2% | Global, led by the United States, the Europe, China, and India | Medium term (2-4 years) |

| Urbanization and income growth in Asia-Pacific | +1.8% | Asia-Pacific core with spill-over to South Asia | Long term (≥ 4 years) |

| E-commerce and omnichannel expansion | +0.7% | Global, strongest in India, Southeast Asia, and Latin America | Short term (≤ 2 years) |

| Smart-home adoption for connected units | +0.9% | North America, Western Europe, and urban China | Medium term (2-4 years) |

| HFC phasedown and refrigerant transitions | +0.6% | Global, compliance-led in the United States, Europe, faster in China, Brazil | Long term (≥ 4 years) |

| Utility rebates and demand response | +0.4% | United States and select Europe markets, emerging in Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening Energy-Efficiency Standards Spur Replacement and Premiumization

The United States Department of Energy’s final rule for refrigerators, refrigerator-freezers, and freezers, effective for products manufactured in 2029-2030, targets an average 11% energy reduction versus current units, with projected lifetime savings for consumers and significant national energy benefits that reinforce replacement timing for older products. Complementary voluntary programs like ENERGY STAR Most Efficient 2025 set performance thresholds that require advanced insulation and high-efficiency compression, tightening the bar for top-tier labels that influence premium assortments in the household refrigerators and freezers market[2]ENERGY STAR Program Office, “Consumer Refrigeration Products ENERGY STAR Most Efficient 2025 Criteria,” U.S. Environmental Protection Agency and U.S. Department of Energy, energystar.gov . China has updated its minimum energy performance standards for consumer refrigeration, with enforcement planned from mid-2026, which pulls forward redesign plans and procurement changes for multinational brands active in the region. Indonesia’s 2024 update to MEPS and labeling for refrigerators raises the compliance bar for entry-tier products, shaping the feature mix that manufacturers can profitably maintain at low price points. Over the next two to four years, these requirements will push inverter compressors, improved foams, and adaptive cooling across broader mid-tier lineups, which, over time, narrows differentiation based only on headline energy ratings in the household refrigerators and freezers market.

Urbanization and Income Growth in Asia-Pacific Accelerate First-Time Ownership

Asia-Pacific’s urbanization momentum and income growth patterns continue to expand the first-purchase cohort for major appliances, with China’s permanent urban population rising by 10.83 million in 2024 and the urbanization rate reaching 67.00%, setting a durable foundation for broader ownership in the household refrigerators and freezers market. Urban wage gains and narrowing rural-urban income gaps in China improve affordability for larger capacities and more efficient units over the forecast horizon. Penetration remains well below saturation in populous South and Southeast Asian markets, so demand concentrates in mid-capacity, value-priced products that fit smaller kitchens and tighter monthly budgets. As distributor footprints spread, financing and installation ecosystems mature, and localized content guides purchasing, the household refrigerators and freezers market sees conversion of latent demand in second-tier cities where electrification and incomes have already improved. Over the long term, this intake will offset softness in saturated regions and rebalance production footprints toward platforms optimized for 15-22.9 cubic foot formats.

E-Commerce and Omnichannel Expansion Boosts Appliance Access and Choice

Online channels expand selection and reduce friction for large-format deliveries, while omnichannel models improve last-mile reliability for time-sensitive replacements in the household refrigerators and freezers market. In mature markets, buy-online-pickup-in-store has strengthened attachment of installation and haul-away services while protecting store traffic, a pattern consistent with observed consumer preferences in omnichannel studies. In growth markets, embedded financing at checkout lowers the upfront barrier for first-time buyers and expands eligibility for larger capacities than cash-only purchases would allow. Live and social commerce formats are also reshaping consideration by demonstrating features in real time, which supports faster decisions for mid-tier SKUs that prioritize features-per-dollar. Rapid fulfillment at scale further reduces the advantage of immediate in-store availability, as major marketplaces lift same-day and next-day delivery coverage across metros, which accelerates the online share shift in the household refrigerators and freezers market.

Smart-Home Adoption Lifts Demand for Connected Refrigerators

Connected refrigerators gain traction as platforms standardize and use cases mature beyond novelty features, with the smart refrigerator segment demonstrating a faster growth profile than conventional units within the household refrigerators and freezers market. The arrival of Matter-certified refrigerators marks a meaningful change for cross-platform interoperability, led by BSH’s early 2025 release of a Matter-enabled French door bottom-mount model[3]Bosch Home Appliances U.S. Press Office, “BSH Drives Matter Connectivity Standard Forward for Home Appliances at CES 2025,” BSH, us.bosch-press.com . AI-driven features are moving from flagship to broader lineups, as shown by Samsung’s integration of AI Vision and Google Gemini, designed to improve food recognition and in-home assistance, which will raise the perceived utility of connected units through 2028. GE Appliances’ Kitchen Assistant, announced for April 2026 availability, layers barcode scanning and interior cameras to streamline grocery management and lift engagement with smart features at the point of daily use. As interoperability improves and AI use cases add measurable convenience, connectivity will contribute a larger share of revenue growth even as conventional formats continue to dominate units through the mid-term in the household refrigerators and freezers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturation and long replacement cycles | -1.5% | North America, Western Europe, Japan, Australia | Long term (≥ 4 years) |

| Housing softness and inflation | -1.1% | Global, acute in the United States, United Kingdom, select European markets | Medium term (2-4 years) |

| Input cost and logistics volatility | -0.8% | Global, supply-chain-dependent manufacturers | Short term (≤ 2 years) |

| Right-to-repair policies extend lifetimes | -0.5% | Europe and select United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Saturation and Long Replacement Cycles in Developed Markets

In North America, Western Europe, Japan, and Australia, near-universal penetration means demand relies on replacements, remodels, and product upgrades rather than new ownership, which naturally slows unit growth in the household refrigerators and freezers market. Replacement timing is long, so efficiency and feature upgrades must be compelling to trigger earlier purchases, especially when operating-cost savings alone are modest relative to total product price. Premiumization strategies lift average selling prices, yet they do not necessarily shorten lifespans, which limits the impact of step-up features on overall unit volumes in saturated regions. Regulatory actions can change this pattern during transition windows when new standards apply, but the effect is usually localized and time-bound. As a result, the household refrigerators and freezers market leans more on policy timing and targeted incentives for near-term bumps in mature economies than on organic ownership gains.

Housing Softness and Inflation Dampen Big-Ticket Purchases

When housing activity cools and financing costs remain elevated, big-ticket discretionary purchases pause or shift down the price ladder, which restrains short-term momentum in the household refrigerators and freezers market. Lower transaction volumes in new construction reduce bundled appliance sales and can move buyers toward repair rather than replacement for legacy units during budget pressure periods. Retailers tend to lean on promotional financing to smooth demand, but these offers mainly shift timing within the next few quarters rather than drive structural growth. The result is a lagged response where appliance volumes recover only after housing stabilizes, and price expectations reset, keeping the channel mix and product mix in flux during the adjustment. This dynamic reinforces the case for emerging-market exposure, where first-purchase demand is less correlated with mortgage cycles and interest rate movements.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: French-Door Units Drive Premiumization as Top-Freezers Retain Volume Leadership

Top-freezer refrigerators accounted for 34.81% of 2025 revenue, anchoring unit leadership in price-sensitive markets, while French-door models are projected to post a 6.75% CAGR through 2031, the fastest among product types in the household refrigerators and freezers market. The product mix aligns with kitchen dimensions and budget realities in emerging markets, which favor single-door and top-freezer formats at retail price points that fit first-time buyers. In the premium tier, French-door adoption rises as builders and remodelers standardize wider openings, drawing in shoppers who value ease of access and multi-zone storage. Brands are also solving fit challenges for compact apartments, as seen in Samsung’s zero-clearance Bespoke AI 3-door variants that cut side clearances and door depths to improve installation flexibility. Feature-led launches at the top end, such as GE Appliances’ Kitchen Assistant with exterior barcode scanning and interior camera intelligence, push smart readiness deeper into the category and increase the feature spread versus conventional offerings.

At the same time, bottom-freezer and side-by-side formats retain stable shares in regions where ergonomics or aesthetics drive preferences, and compact refrigerators continue to serve dorm, office, and secondary-cooling needs within developed markets. The premium tier is also advancing on efficiency, exemplified by LG’s French-door lineup achieving Europe's rare “A” energy rating at IFA 2025, which reduces the historical efficiency gap with simpler configurations[4]LG Global Press Office, “LG Presents New Space- and Energy-Efficient Refrigerator Lineup at IFA 2025,” LG, lg.com . As brands balance profit pools that lean toward premium configurations with volume platforms that sustain scale, development roadmaps are split between high-ticket innovation and cost-optimized refreshes in the household refrigerators and freezers industry. Over the forecast period, revenue mix will tilt further toward French-door and four-door variants because of higher average selling prices, even as top-freezers continue to dominate unit counts. This dual-track strategy keeps manufacturing footprints flexible while retailers adjust floor plans and online catalog depth to match local demand in the household refrigerators and freezers market.

Note: Segment shares of all individual segments available upon report purchase

By Capacity: 19-22.9 Cubic Feet Dominates as Larger Formats Gain Share

The 19-22.9 cubic foot band held 31.64% of 2025 revenue, confirming continued optimization around four-person households and common kitchen widths, while capacities at or above 23 cubic feet are forecast to grow at a 5.68% CAGR through 2031 in the household refrigerators and freezers market. Larger formats capture shoppers who prioritize fewer trips, bulk purchases, and more flexible zone management, especially in suburban settings and multi-generational homes. Innovation that adds usable space within existing footprints, such as Samsung’s AI Hybrid Cooling approach that increases loadable volume with deeper shelves and targeted cooling assist, supports capacity migration without major layout changes. Smaller bands under 15 cubic feet remain important in compact-living and entry-tier contexts, where constraints on space and utility budgets direct buyers to simpler, efficient formats. Mid-size bands at 15-18.9 cubic feet hold steady in dense urban housing, where cabinet alignment and door-swing clearance are decisive factors.

Efficiency improvements now stretch across size classes, as seen in Europe-rated models that bring top-tier energy labels to larger capacities, which historically had to accept a performance penalty at the upper end. Over time, operating-cost differences between mid and large capacities have narrowed when measured per liter of storage, which helps higher-capacity units defend their share in markets with elevated electricity prices. The household refrigerators and freezers market size for ≥23 cubic foot configurations is projected to expand at a 5.68% CAGR through 2031 as supply chains optimize insulation, airflow, and compressor modulation for larger enclosures. In parallel, the 19-22.9 cubic foot band remains the global volume anchor because it balances capacity, energy use, and fit across a wide range of kitchens in both mature and growth markets. These shifts guide SKU planning toward a tighter set of high-velocity sizes that align with local cabinetry norms and retail price bands in the household refrigerators and freezers market.

By Technology: Conventional Models Sustain Volume Leadership as Smart Segment Compounds Rapidly

Conventional refrigerators represented 82.41% of 2025 sales, confirming the price-sensitivity that defines unit leadership, while the smart/IoT-enabled segment is expected to grow at 6.65% CAGR through 2031 as standards harmonize and features add daily utility in the household refrigerators and freezers market. Momentum for connectivity has strengthened with the first Matter-certified refrigerators entering the market, enabling broader cross-platform compatibility that reduces setup friction for mainstream users. AI-enabled experiences are widening, including Samsung’s integration of AI Vision with Google Gemini to improve recognition and assistance, which improves engagement after installation. GE Appliances is also advancing hands-on use cases through Kitchen Assistant’s barcode scanning and in-fridge cameras, which can reduce manual steps in meal planning and replenishment. These advances support a larger revenue share for connected models even as conventional formats remain the bulk of unit sales through the medium term in the household refrigerators and freezers market.

Within connectivity, Wi-Fi remains the base layer for most smart refrigerators, and voice-assistant integrations are improving as vendors update firmware and cloud services on rolling schedules. Energy-management modes from leading brands now tune compressor cycles and temperatures based on usage patterns, helping households lower consumption without changing routines. The household refrigerators and freezers market size for connected models is lifted by these features because they contribute to clear value narratives at the point of sale, especially when utilities promote smart-readiness and demand response. Over the forecast period, higher attach rates for connectivity in mid-tier and premium SKUs will expand buyer choice and move smart features into the mainstream. This shift requires careful price-band management so connectivity adds perceived value without overextending entry-tier shoppers in the household refrigerators and freezers market.

By Distribution Channel: Multi-Brand Stores Face Margin Compression as Online Accelerates

Multi-brand stores held 46.20% of 2025 revenue, reflecting the continued value of in-person comparisons, immediate availability for urgent replacements, and bundled installation offers that many shoppers still prefer in the household refrigerators and freezers market. Online channels are the fastest-growing route to market at 8.14% CAGR through 2031, with different regional mechanisms such as buy-online-pickup-in-store in mature markets and embedded financing in growth markets. Omnichannel models increase store visits and preserve service attach rates while online marketplaces refine last-mile options for large appliances, supporting steady share gains for digital and hybrid journeys. As rapid delivery expands, the speed advantage of physical inventory narrows, which allows more urgent replacements to shift online without sacrificing installation quality or timeline. The household refrigerators and freezers market continues to reflect a strong offline base even as online share grows, which keeps merchandising, logistics, and service coordination central to retailer competitiveness.

Exclusive brand outlets remain important in premium urban locations for experiential selling of French-door and connected models, while independent retailers and builder-direct channels continue to serve local preferences and project timelines. Region-specific innovations in live commerce and social-led demos also lift consideration for mid-tier brands competing on features-per-dollar. The household refrigerators and freezers market share advantage of multi-brand stores faces gradual erosion as digital journeys normalize configuration comparisons and price transparency, pushing stores to focus on service, delivery, and premium experiences. Over the forecast period, channel strategies that fuse financing, fast fulfillment, and clear installation propositions will capture the most durable gains across regions. Retailers that align with utility programs and smart-readiness messaging can also differentiate in markets where energy incentives are available.

Geography Analysis

North America held 39.30% of global revenue in 2025, supported by near-universal ownership and steady replacement cycles anchored in kitchen remodels and product updates within the household refrigerators and freezers market. The region’s projected 2.30% CAGR through 2031 trails the global average because unit volume growth depends on upgrades rather than first-time purchases. The United States-based manufacturing footprints mitigate some logistics volatility and tariffs for brands that maintain significant domestic capacity. New federal efficiency standards set for products made in 2029-2030 will require portfolio refreshes that ripple through design, procurement, and labeling across the next product cycles. Over the medium term, the household refrigerators and freezers market will rely on premiumization, connectivity, and targeted incentives to lift revenue in the United States and Canada, while Mexico supports additional unit growth through urban household formation.

Asia-Pacific is set to lead growth at a 5.34% CAGR through 2031 as urbanization, rising incomes, and channel expansion improve access and affordability for first-time buyers in the household refrigerators and freezers market. China’s 2024 data reported 10.83 million more permanent urban residents and a 67.00% urbanization rate, and retailing programs that encouraged trade-ins for efficient appliances boosted household appliance retail sales, underscoring the power of policy in accelerating replacement cycles. China’s updated refrigerator MEPS entering into force from mid-2026 will push higher-efficiency baselines into the market and sharpen competition among multinational and local brands. Across South and Southeast Asia, the category expands fastest in mid-capacity, value-led SKUs as online storefronts, financing, and service networks reach second-tier cities. Over the forecast period, Asia-Pacific’s mix shift will continue to favor cost-effective designs and durable components while premium segments rise with the region’s middle-class expansion in the household refrigerators and freezers market.

Europe is a mature region with stable replacement-led demand and a regulatory environment that emphasizes higher efficiency, clearer consumer information, and improved repairability for home refrigeration. Category growth is modest and centers on premium formats, built-in designs, and top energy labels, as reflected in flagship product lines that have earned the EU’s rare “A” rating for large-format French-door and bottom-freezer designs. Natural refrigerants and advanced insulation are key to meeting label goals while preserving capacity and convenience features. Over the period to 2031, the household refrigerators and freezers market in Europe will reflect incremental unit growth with a higher revenue mix from premium and connected models, paced by ongoing policy consultations and label updates. This path underscores the importance of compliance-ready platforms for global brands that operate across multiple policy regimes.

Competitive Landscape

Global competition remains moderately fragmented in units and more concentrated at premium price points, where innovation, connectivity, and brand ecosystems shape purchasing in the household refrigerators and freezers market. Haier Smart Home maintained global leadership by volume for another year, supported by a multi-brand portfolio and strong positions in both China and the United States through GE Appliances. Samsung has deepened its IoT leadership with consistent Family Hub innovation and a new AI Vision and Google Gemini integration timed for CES 2026. BSH set the early benchmark for Matter-certified refrigerators, which strengthens the case for shared standards across platforms. LG has targeted efficiency leadership in premium configurations with EU “A” label achievements for French-door and bottom-freezer lines. These moves define the premium tier while mid-tier portfolios focus on capacity, durability, and features-per-dollar positioning in the household refrigerators and freezers market.

Local manufacturing footprints and component integration help some firms cushion logistics volatility and speed compliance updates, as seen in brands emphasizing domestic capacity within their largest end markets. Midea has accelerated retail expansion in Southeast Asia with new branded stores, which support multi-channel coverage and demonstrate how vertically integrated producers can scale quickly in growth corridors. GE Appliances introduced Kitchen Assistant with barcode scanning and interior cameras to simplify food management, signaling deeper software roadmaps for premium models. Samsung’s new zero-clearance French-door options address retrofit constraints in dense housing, supporting broader adoption of premium configurations in Europe and Asia-Pacific. As standards and incentives evolve, interoperability, energy savings, and service integration are becoming more influential vectors of competition in the household refrigerators and freezers market.

The strategic focus now spans three arcs, each with different levers for advantage in the household refrigerators and freezers market. First, compliance-ready platforms with scalable refrigerant and insulation choices reduce redesign risks and time-to-market when policy timelines shift. Second, connected ecosystems that deliver practical utility, like AI-supported recognition and automated grocery workflows, can raise engagement and increase brand lock-in across appliances. Third, channel strategies that balance service quality with rapid fulfillment capture near-term share gains as more urgent replacements move online. Together, these themes suggest continued differentiation in premium segments while value-led formats anchor volume and defend share in fast-growing urban markets.

Household Refrigerators And Freezers Industry Leaders

Haier Smart Home Co., Ltd.

LG Electronics Inc.

Samsung Electronics Co., Ltd.

Whirlpool Corporation

Electrolux AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: GE Appliances unveiled the GE Profile Smart French-Door Refrigerator with Kitchen Assistant, launching April 2026 at USD 4,899, featuring a patented exterior barcode scanner recognizing 4+ million products and FridgeFocus AI-powered interior cameras for crisper-drawer inventory tracking. This represents a significant advancement in reducing manual grocery-list creation friction that limited earlier smart-refrigerator adoption.

- January 2026: Samsung announced integration of AI Vision with Google Gemini in its Bespoke AI Family Hub refrigerators at CES 2026, expanding food recognition to include processed foods and user-labeled items without manual registration, alongside a Bespoke AI Wine Cellar with top camera tracking wine labels and SmartThings AI Wine Manager for pairing suggestions. Samsung also launched zero-clearance 3-Door French Door models with 4mm side gaps and reduced door depth, addressing space constraints in European and Asian apartments.

- December 2025: Midea simultaneously launched 18 Midea brand stores across Malaysia on December 3, setting a Malaysia Book of Records milestone and targeting USD 142.8 million in 2025 sales with projected 20% growth in 2026. The company plans to upgrade 50+ stores over the next two years, signaling aggressive retail expansion in Asia-Pacific.

- October 2025: Samsung released the Family Hub 2025 update, expanding AI Vision Inside to recognize more food items, introducing Bixby Voice ID for personalized account switching, and extending Knox Matrix security to 2024 Wi‑Fi-compatible Samsung refrigerators, washers, and dryers. The update demonstrates ongoing software value-add that extends the useful life of installed hardware.

Global Household Refrigerators And Freezers Market Report Scope

A household refrigerator is primarily used for food storage and protecting food from contamination. The Household Refrigerators and Freezers Market is segmented by product type, capacity, technology, distribution channel, and geography. By product type, the market is divided into single-door, top-freezer, bottom-freezer, side-by-side, French-door, and compact & mini refrigerators. By capacity, the market is categorized into less than 15 cu. ft., 15–18.9 cu. ft., 19–22.9 cu. ft., and 23 cu. ft. and above. By technology, the market is segmented into conventional and smart/IoT-enabled refrigerators. By distribution channel, the market is divided into multi-brand stores, exclusive brand outlets, online, and other channels. Geographically, the market analysis covers North America, South America, Europe, Asia-Pacific, and the Middle East & Africa. The report provides market size and forecasts for the household refrigerators and freezers market in value (USD) across all the above segments.

| Single Door Refrigerators |

| Top-Freezer Refrigerators |

| Bottom-Freezer Refrigerators |

| Side-by-Side Refrigerators |

| French-Door Refrigerators |

| Compact & Mini Refrigerators |

| Less than 15 |

| 15 – 18.9 |

| 19 – 22.9 |

| More than or equal to 23 |

| Conventional |

| Smart / IoT-Enabled |

| Multi-brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Single Door Refrigerators | |

| Top-Freezer Refrigerators | ||

| Bottom-Freezer Refrigerators | ||

| Side-by-Side Refrigerators | ||

| French-Door Refrigerators | ||

| Compact & Mini Refrigerators | ||

| By Capacity (cu. ft.) | Less than 15 | |

| 15 – 18.9 | ||

| 19 – 22.9 | ||

| More than or equal to 23 | ||

| By Technology | Conventional | |

| Smart / IoT-Enabled | ||

| By Distribution Channel | Multi-brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Region | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the household refrigerators and freezers market?

The household refrigerators and freezers market size is expected to increase from USD 128.40 billion in 2025 to USD 133.45 billion in 2026 and reach USD 171.42 billion by 2031, at a 5.14% CAGR over 2026-2031.

Which region leads and which grows fastest within this category?

North America led with 39.30% revenue in 2025, while Asia-Pacific is projected to be the fastest-growing region at 5.34% CAGR through 2031.

Which product types are most significant for growth?

Top-freezers led with 34.81% in 2025, and French-door units are forecast to grow the fastest at 6.75% CAGR to 2031 as premium adoption rises.

How is connectivity changing buyer choices?

Interoperable standards and AI-enabled features are lifting engagement, highlighted by BSH’s first Matter-enabled refrigerator and Samsung’s AI Vision with Google Gemini, which enhance utility and reduce setup friction.

What channels will gain the most share through 2031?

Online channels are projected to be the fastest-growing route at 8.14% CAGR, while multi-brand stores continue to play a central role for comparisons, installation, and urgent replacements.

Which policy or regulatory shifts matter most over the next product cycles?

United States energy conservation standards effective for 2029-2030 production and regional policy updates on labeling and refrigerants will drive redesigns and portfolio refreshes across markets.