Smart Refrigerator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

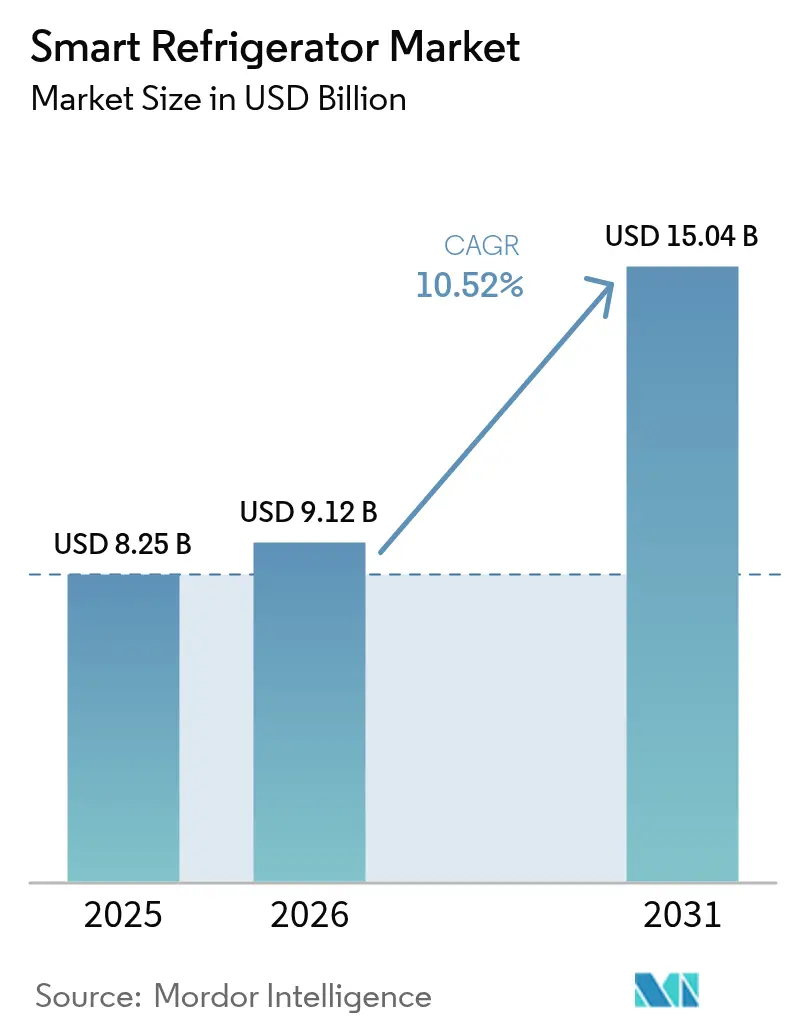

| Market Size (2026) | USD 9.12 Billion |

| Market Size (2031) | USD 15.04 Billion |

| Growth Rate (2026 - 2031) | 10.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Refrigerator Market Analysis by Mordor Intelligence

The smart refrigerator market size is expected to grow from USD 8.25 billion in 2025 to USD 9.12 billion in 2026 and is forecast to reach USD 15.04 billion by 2031 at 10.52% CAGR over 2026-2031. The current expansion reflects the mainstreaming of IoT connectivity, maturing artificial-intelligence (AI) capabilities, and regulatory pressure for higher energy efficiency [1]Samsung Electronics, “Bespoke AI Refrigerator Launch Highlights,” news.samsung.com. Sensor prices keep falling, Matter 1.3 has removed many interoperability obstacles, and utilities now promote connected appliances through dynamic-tariff programs, all of which reinforce the demand upswing. Manufacturers are also reallocating R&D budgets toward natural-refrigerant platforms to comply with the EU F-Gas Regulation 2024/573 and parallel U.S. Environmental Protection Agency rules, thereby refreshing model line-ups faster than historic replacement cycles. Competitive traction remains strongest in premium kitchen remodels, but mid-market traction is improving because AI Vision features are cascading, opening the smart refrigerator market to a wider income band.

Key Report Takeaways

- By product category, double-door units commanded 29.40% of the smart refrigerator market share in 2025, while French-door models are projected to post a 11.96% CAGR through 2031.

- By connectivity, Wi-Fi-enabled lines held 44.30% share of the smart refrigerator market size in 2025; Voice-Assistant & AI-integrated variants are set to grow the fastest at an 11.12% CAGR.

- By capacity, the 300-500 L segment accounted for 39.20% of the smart refrigerator market size in 2025, yet units above 700 L are advancing at an 11.55% CAGR.

- By end-user, the residential segment retained a 69.10% share in 2025, whereas commercial applications are rising at an 8.62% CAGR.

- By distribution channel, B2C/Retail captured 82.30% sales in 2025; the B2B channel is forecast to expand at an 8.25% CAGR.

- By geography, North America led with a 29.60% share in 2025, while Asia-Pacific is projected to be the fastest-growing region at a 9.95% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Refrigerator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of smart-home ecosystems | +2.8% | Global (North America & EU lead) | Medium term (2-4 years) |

| Stringent energy-efficiency regulations | +2.1% | Global, strongest in the EU & North America | Short term (≤2 years) |

| Declining IoT module and sensor costs | +1.9% | Global, fastest in Asia-Pacific hubs | Short term (≤2 years) |

| Manufacturer-integrated AI for predictive maintenance | +1.5% | Premium segments in North America & the EU | Medium term (2-4 years) |

| Retailer telemetry monetization | +1.2% | North America is expanding to the EU | Long term (≥4 years) |

| Home-health medication storage | +0.8% | Aging demographics worldwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Smart-Home Ecosystems

Matter 1.3, launched in May 2024, officially certified refrigerators for cross-platform control and reduced set-up friction between Apple Home, Google Home, and Amazon Alexa environments. BSH introduced Matter-enabled refrigerators in early 2025, signaling that interoperability is now table stakes in the smart refrigerator market. Households adopting multiple connected devices display a higher propensity to upgrade additional appliances to gain unified voice control, calendar integration, and energy scheduling. Premium models strengthen this dynamic through 9-inch AI Home displays that place recipe suggestions, family calendars, and energy dashboards at eye level.

Stringent Energy-Efficiency Regulations Driving Replacements

The U.S. Department of Energy tightened refrigerator efficiency standards in December 2024 and mandated certification submissions starting May 2025. New York State’s standards forecast USD 264 million in yearly consumer savings by 2035 and specifically reward connected units that prove demand-response compatibility [2]New York State Energy Research and Development Authority, “Appliance and Equipment Efficiency Standards,” nyserda.ny.gov. In April 2025, the UK began requiring smart readiness so that appliances can automatically shift load to off-peak periods. Canada’s Amendment 18 will harmonize with U.S. rules from 2026, giving manufacturers an incentive to design uniform North American portfolios. These measures accelerate natural replacement by making legacy units comparatively expensive to operate, thereby uplifting the smart refrigerator market.

Declining IoT Module and Sensor Costs

A Jabil survey in 2023 among 202 smart-home executives found that 63% now consider reliable connectivity affordable at scale, even though 68% of brands still struggle with embedded software complexity. China’s refrigerator production capacity added more than 15 million units between 2022-2024, boosting economies of scale that directly lower camera and sensor costs. Low-cost parts from the smartphone supply chain—such as temperature and humidity sensors or tiny cameras—let fridge makers add food-recognition features without pushing up the sticker price. As 5G networks spread, connectivity chips cost less yet move data fast enough for predictive maintenance and remote troubleshooting. By blending several low-cost sensors in one unit, brands now offer smart functions that once demanded pricey custom hardware, so even mid-priced models can carry advanced features.

Manufacturer-Integrated AI for Predictive Maintenance

Samsung’s AI Vision Inside identifies 37 staples and creates Instacart shopping lists so owners rarely find empty shelves. GE Appliances’ SmartHQ platform now covers coffee, laundry, and refrigeration, training a centralized model on cross-appliance telemetry. Predictive maintenance models analyze compressor amperage, cycle frequency, and ambient deviation to pre-empt failures, cutting warranty costs and reinforcing brand loyalty. Samsung reports that its AI Energy Mode trims fridge power draw by up to 15% during peak tariffs without compromising food safety. Continuous over-the-air (OTA) firmware updates deliver incremental algorithm gains, which, in turn, extend usable product life and generate subscription revenue for premium diagnostics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront price premium vs conventional models | -1.8% | Global, most pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Cybersecurity and data privacy vulnerabilities | -1.2% | Global, heightened in privacy-conscious regions | Medium term (2 - 4 years) |

| Fragmented interoperability despite the Matter rollout | -0.9% | Global, concentrated in multi-brand households | Medium term (2 - 4 years) |

| Right-to-repair and embedded-carbon scrutiny | -0.7% | EU & North America, expanding worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Price Premium Versus Conventional Models

Smart refrigerators still carry a hefty price tag, which puts off buyers who watch their budgets, especially in countries where price is the first filter. The extra cost is mainly acceptable to well-off households, and North American families are the most willing to pay for connected features. That leaves manufacturers stuck between loading in new tech and keeping the final price within reach of a wider audience. Ongoing inflation and economic jitters make matters worse because many people delay replacing an old fridge until it stops working. On top of that, shoppers often have trouble seeing how lower energy bills or predictive maintenance justify the bigger upfront spend, so brands need clearer, numbers-based stories that show the payback in real terms.

Cyber-Security and Data-Privacy Vulnerabilities

Internet-enabled fridges create another possible doorway for hackers, and that makes privacy-minded households and businesses nervous. The Connectivity Standards Alliance released its IoT Device Security Specification and “Product Security Verified” Mark in March 2024 to improve buyer confidence. Yet high-profile hacks of smart TVs and thermostats keep privacy concerns in headlines, and refrigerators with cameras can feel intrusive. Regulatory frameworks such as GDPR and a growing patchwork of U.S. state privacy acts require explicit consent and data-handling transparency, which elevates compliance costs. Even with stronger security rules coming into place, these worries can still give potential buyers pause.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Premium French-Door Models Outpace Legacy Formats

The double-door format retained the largest slot with a 29.40% smart refrigerator market share in 2025 because buyers still equate the layout with reliable cold air circulation. The segment also benefits from incremental upgrades, such as Wi-Fi boards and touch displays, that can be added without retooling cabinet designs. French-door units, however, are charting the fastest 11.96% CAGR on the back of premium kitchen remodels, additional door-within-door storage, and wider shelves that accommodate meal-prepping containers. Samsung’s latest AI Hybrid Cooling model boosts interior volume by 25 L without expanding external dimensions, underscoring how premium engineering solves real-world space constraints.

The growing popularity of French-door configurations positions the format as the principal innovation sandbox where OEMs debut high-resolution cameras, recipe recommendation engines, and AI-powered freshness algorithms. Because the layout places refrigerated foods at eye level, vision modules can capture clearer images for machine learning, increasing recognition accuracy. As production scales, BOM reductions should feed back into lower Street prices, enabling further substitution of legacy double-door units and reinforcing the expansion of the smart refrigerator market.

By Connectivity: Voice-First Interaction Gains Momentum

Wi-Fi connectivity became a baseline expectation, constituting 44.30% of shipments in 2025 and anchoring the smart refrigerator market size for entry-level SKUs. Manufacturers preload apps that issue firmware updates, energy-usage dashboards, and diagnostic codes via standardized over-the-air protocols. Voice-assistant and AI-integrated models are growing at an 11.12% CAGR because they enable hands-free grocery management and recipe planning. Integration with Alexa, Google Assistant, and Samsung Bixby is the main pull, but LG’s ThinQ and GE’s SmartHQ are expanding their natural language libraries.

Multi-protocol chips now embed Wi-Fi, Thread, and Bluetooth LE on a single die, cutting module cost, which in turn smooths Matter 1.3 certification. That convergence reduces consumer setup friction, driving higher attach rates of voice-assistant SKUs to broader smart-home deployments. OEMs view natural language as the sticky interface that anchors their wider appliance ecosystems. Consequently, voice-first control is expected to become the de facto standard during the forecast window, amplifying replacement demand in the smart refrigerator market.

By Capacity: Demand Shifts Toward Larger, High-End Formats

Units in the 300-500 L bracket commanded 39.20% of the smart refrigerator market size in 2025, balancing storage and floor-space constraints typical of three-member households. Nonetheless, refrigerators exceeding 700 L are clocking an 11.55% CAGR as affluent homeowners build chef-grade kitchens and small food-service operators migrate to premium residential-style equipment. Capacity growth dovetails with macro trends such as bulk shopping at warehouse clubs and weekend meal prep, both of which favor high-volume storage.

Energy-efficiency improvements mitigate the operating-cost penalty traditionally associated with larger cabinets. OEM test data show that a 700 L model equipped with inverter compressors and vacuum-insulated panels can consume less annual electricity than a 2019-era 400 L unit, assuaging sustainability worries. Smart Vision algorithms further streamline organizations so that perishables are no longer lost at the back of cavernous shelves, directly addressing a top pain point cited in customer reviews. The heightened utility underpins continued premiumization, reinforcing growth momentum within the smart refrigerator market.

By End-User: Commercial Applications Accelerate ROI-Driven Adoption

Residential buyers still represented 69.10% of 2025 shipments because product roadmaps and marketing budgets historically targeted the consumer segment. Restaurants, hotels, and convenience chains now form an emerging demand cluster, however, with a projected 8.62% CAGR as they quantify the dollar value of predictive maintenance and inventory analytics.

Haier’s USD 775 million acquisition of Carrier Commercial Refrigeration provided immediate entry into B2B channels, adding brands that already meet stringent food-safety logging requirements. Connected sensors send temperature and door-open frequency data to cloud dashboards, triggering maintenance before failures cascade. Energy-optimization algorithms also reduce peak-time utility load, which yields a measurable ROI that justifies premium pricing. As software-as-a-service packages mature, OEMs will transition from hardware sales to recurring revenue, deepening stickiness in the smart refrigerator industry’s commercial slice.

By Distribution Channel: B2B Direct Sales Gain Ground as Retail Holds Scale

B2C retail formats retained 82.30% of 2025 shipments, with multi-brand stores securing half of the total thanks to live showroom demonstrations and bundled installation services that simplify large-appliance purchases. Exclusive brand outlets continued to reinforce premium positioning through curated displays and in-house finance plans, while online storefronts logged the fastest CAGR inside retail, supported by same-day delivery windows and real-time price matching that appeal to digitally-native buyers. Home-improvement chains and warehouse clubs rounded out the channel mix by attracting value-driven households with seasonal rebates and bulk-buy discounts, a dynamic that kept them relevant despite thin margins. Collectively, these touchpoints preserved the largest slice of the smart refrigerator market share in 2025 and kept average selling prices resilient by maintaining service-led differentiation.

Direct B2B sales from manufacturers are expanding at an 8.25% CAGR through 2031 as restaurants, hotels, and institutional kitchens demand tailored configurations, bulk purchasing agreements, and integrated service contracts that bypass traditional retail mark-ups. Haier’s USD 775 million acquisition of Carrier Commercial Refrigeration in 2024 illustrates the strategic push toward deeper commercial pipelines that feed recurring maintenance revenue and lock in high-value clients. As manufacturers leverage direct relationships to bundle predictive-maintenance subscriptions and rapid-spare-parts fulfillment, the smart refrigerator market size flowing through B2B channels is set to climb steadily, easing reliance on margin-squeezed retail networks while enhancing lifetime customer value.

Geography Analysis

North America preserved a 29.60% share of the smart refrigerator market in 2025 due to early smart-home adoption, high disposable income, and a well-developed installer network. Utility rebate programs covering connected appliances further shift purchasing toward ENERGY STAR Most Efficient models that embed real-time tracking . Brand trust indices place Bosch, Whirlpool and LG above newcomers, illustrating the latent brand-equity moat that cushions incumbents. Premium kitchen remodels continue to substitute working but feature-poor refrigerators, extending a robust upgrade cycle that favors advanced AI Vision capabilities compatible with third-party grocery platforms.

Asia-Pacific, led by China, is closing the gap at a forecast 9.95% CAGR through 2031. Middle-class income expansion in urban China, India, and Southeast Asia is driving the uptake of premium SKUs that incorporate voice control and AI freshness monitoring. Chinese OEMs such as Haier and Hisense translate local manufacturing scale into aggressive global pricing, further democratizing access. Regional policy incentives aimed at smart-home infrastructure and carbon-neutral living support long-run momentum in the smart refrigerator market.

Europe remains a technologically mature yet regulation-driven arena. The EU F-Gas Regulation and the Ecodesign for Sustainable Products Regulation press manufacturers to adopt natural refrigerants and design for durability ec.europa.eu. Consumers prioritize energy scorecards and cradle-to-cradle recyclability over flashy add-ons, steering the competitive battle toward efficiency algorithms and modular repairability. BSH’s Matter-enabled releases and LG’s Q1 2025 AI-ready refrigerators both respond to these preferences by coupling low global-warming-potential refrigerants with open-protocol interoperability. Regulatory convergence across the continent harmonizes product requirements, effectively enlarging the addressable smart refrigerator market.

Competitive Landscape

The competitive field exhibits moderate concentration. Samsung, LG, Whirlpool, Haier, and BSH collectively leverage century-old brand recognition and nationwide service footprints. Samsung differentiates through AI Vision Inside that recognizes 37 categories of food and automates Instacart list creation, raising the service stickiness of its Bespoke platform. LG is pushing aggressively into U.S. B2B channels, bundling commercial smart refrigerators into larger building automation packages.

Haier’s takeover of Carrier Commercial Refrigeration extends reach into supermarket and pharmaceutical cold-chain verticals, aligning hardware with industrial IoT dashboards that prove ROI. Whirlpool pools R&D with Arçelik in Beko Europe, targeting cost-competitive but Matter-certified models optimized for EU efficiency mandates. Technology convergence around Matter potentially levels the connectivity playing field, so OEMs differentiate via AI-enabled services, predictive maintenance subscriptions, and branded food-shopping ecosystems. As recurring software revenue grows, the smart refrigerator market will increasingly reward end-to-end platform control rather than simple hardware scale.

White-space competition is intensifying in data monetization. Retailers seek aggregated, anonymized fridge-stock insights to refine just-in-time inventory, and OEMs weigh whether to sell that data or keep it as an exclusive value-add. Start-ups offering cloud-agnostic AI retrofits face high customer-acquisition costs in a market where incumbents bundle connectivity free of charge. Given these forces, incumbents’ brand equity and service footprints remain pivotal advantages inside the smart refrigerator industry.

Smart Refrigerator Industry Leaders

Samsung Electronics Co. Ltd.

LG Electronics Inc.

Whirlpool Corporation

BSH Hausgeräte GmbH

Haier Smart Home Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Samsung Electronics introduced enhanced AI Vision Inside refrigerators featuring 9-inch AI Home screens and larger Family Hub displays, reinforcing its “Screens Everywhere” roadmap.

- February 2025: GE Appliances upgraded its SmartHQ platform to suggest recipes from photographed fridge contents and rolled out appliance-specific AI assistants.

- December 2024: LG Electronics showcased a 36-inch Smart InstaView French-Door model with customizable panels and efficiency gains at CES 2025.

- December 2024: Samsung previewed AI Hybrid Cooling refrigerators that marry compressors and Peltier modules to reach 900 L capacity while seeking ENERGY STAR Most Efficient status.

Global Smart Refrigerator Market Report Scope

A smart refrigerator is a device that is connected to the cloud. These refrigerators are programmed to sense what kind of products are being stored inside. Depending on the configuration, it allows the use of smartphones to monitor and control the refrigerator. Apart from this, it also allows sending and receiving notes and calendar entries that appear on the refrigerator screen.

The smart refrigerator market is segmented by types, end-users, and geography. By types, the market is sub-segmented into French doors, side-by-side doors, triple doors, double doors, and single doors. By end-user, the market is sub-segmented into residential and commercial. By geography, the market is sub-segmented into North America, South America, Asia Pacific, Europe, and the Middle East and Africa.

The report offers market size and forecasts for the smart refrigerator market in terms of volume (number of products) and value (USD) for all the above segments.

| Single-Door Refrigerator | |

| Double-Door Refrigerator | Top Freezer |

| Bottom Freezer | |

| Side-By-Side Door Refrigerator | |

| French-Door Refrigerator | |

| Other Refrigerators |

| Wi-Fi Enabled (App-Controlled) |

| Voice-Assistant & AI-Integrated (e.g., Family-Hub) |

| Bluetooth / Zigbee / Thread |

| Screen-Based Smart Fridges |

| Less than 300 L |

| 300 – 500 L |

| 501 – 700 L |

| Greater than 700 L |

| Residential |

| Commercial |

| B2C / Retail | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly From The Manufacturers |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest Of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, And Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, And Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, And Sweden) | |

| Rest Of Europe | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest Of Middle East And Africa |

| By Product | Single-Door Refrigerator | |

| Double-Door Refrigerator | Top Freezer | |

| Bottom Freezer | ||

| Side-By-Side Door Refrigerator | ||

| French-Door Refrigerator | ||

| Other Refrigerators | ||

| By Connectivity | Wi-Fi Enabled (App-Controlled) | |

| Voice-Assistant & AI-Integrated (e.g., Family-Hub) | ||

| Bluetooth / Zigbee / Thread | ||

| Screen-Based Smart Fridges | ||

| By Capacity (Liters) | Less than 300 L | |

| 300 – 500 L | ||

| 501 – 700 L | ||

| Greater than 700 L | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Multi-Brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly From The Manufacturers | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest Of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, And Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, And Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, And Sweden) | ||

| Rest Of Europe | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest Of Middle East And Africa | ||

Key Questions Answered in the Report

What is the smart refrigerator market expected to be worth by 2031?

Forecasts place the smart refrigerator market size at USD 15.04 billion by 2031, reflecting a 10.52% CAGR over 2026-2031.

Which product format is growing the fastest?

French-door models are projected to expand at a 11.96% CAGR, outpacing all other configurations during the forecast horizon.

Why is Asia-Pacific the fastest-growing region?

Manufacturing scale, falling IoT component costs, and an expanding middle class combine to produce a regional CAGR of about 9.95%, the strongest globally.

How do energy-efficiency rules influence adoption?

Tighter U.S., Canadian, and EU regulations accelerate the replacement of legacy units, benefiting models with built-in monitoring that simplify compliance and reduce utility bills.

What role does AI play in new models?

Integrated vision and predictive-maintenance algorithms cut food waste, schedule service before failures, and optimize power draw, enhancing consumer value and OEM service revenue.

Are commercial buyers adopting smart refrigerators?

Yes, restaurants and convenience stores are moving quickly because predictive maintenance and energy optimization deliver measurable ROI that justifies premium pricing.

Page last updated on: