Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

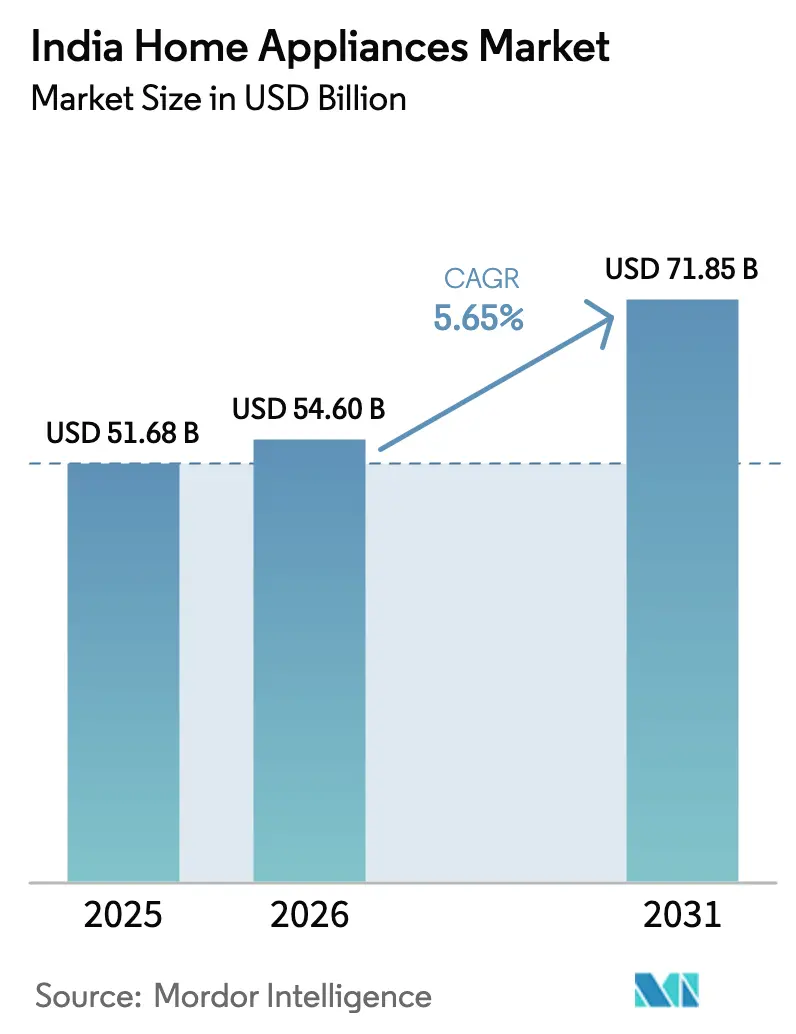

| Base Year Market Size (2025) | USD 51.68 Billion |

| Market Size (2026) | USD 54.60 Billion |

| Market Size (2031) | USD 71.85 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Home Appliances Market Analysis by Mordor Intelligence

The India home appliances market size is expected to grow from USD 51.68 billion in 2025 to USD 54.6 billion in 2026 and is forecast to reach USD 71.85 billion by 2031 at a 5.65% CAGR over 2026–2030. Steady income growth, faster urbanization, and rising aspirations are driving consumer spending and expanding market opportunities. The Production Linked Incentive PLI scheme for white goods, including air conditioner components and LED lights, has attracted committed investments totaling several thousand crore rupees, about INR 4,121 crore (USD 48 million) from the third round and more than INR 6,962 crore (USD 81 million) from selected beneficiaries, reflecting substantial manufacturing expansion under the programme.[1]Source: “PLI Scheme for White Goods,” Press Information Bureau, pib.gov.in The growth of the India home appliances market is being fueled by rising household incomes and the increasing prevalence of nuclear families, which are driving higher demand for modern appliances. Urbanization and changing lifestyles are driving consumers to adopt energy-efficient, smart appliances that offer greater convenience and long-term savings. Government policies and initiatives supporting local manufacturing are boosting production capacity and making appliances more widely accessible nationwide. The rapid expansion of online channels and rental platforms is improving reach and flexibility, particularly in smaller cities and among young professionals.

Key Report Takeaways

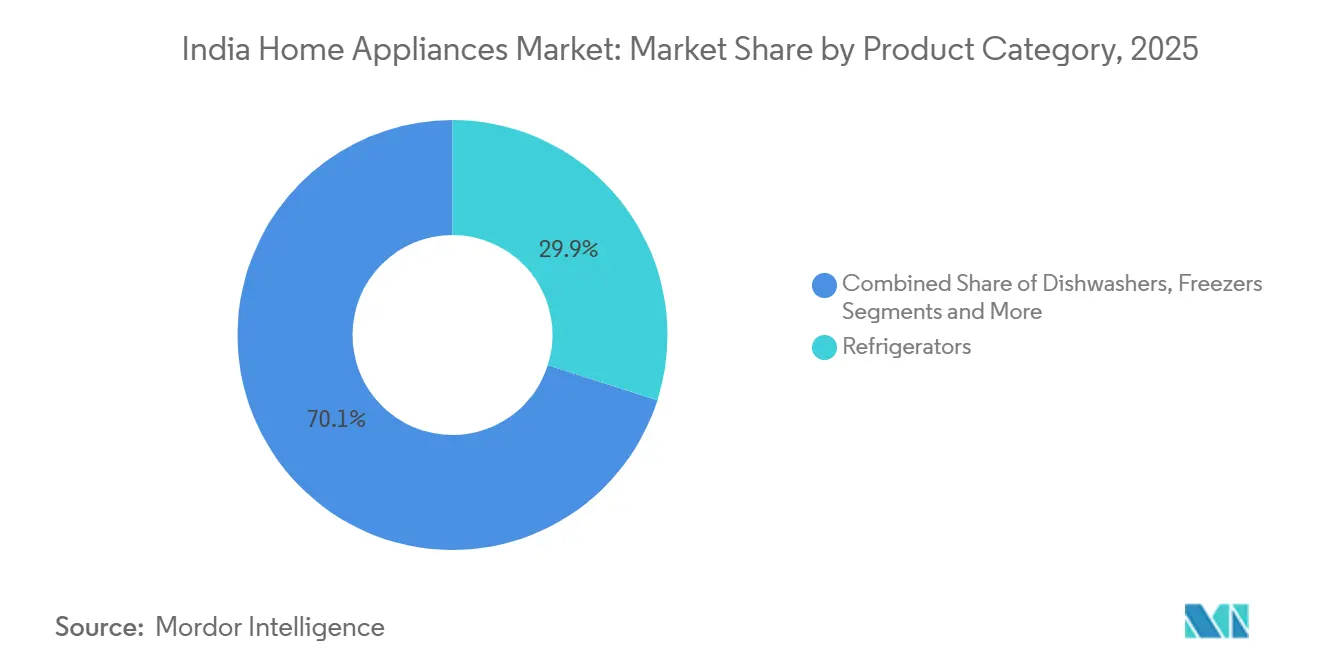

- By product category, refrigerators led with 29.90% of the India home appliances market size in 2025, while air conditioners are projected to expand at a 17.5% CAGR to 2031.

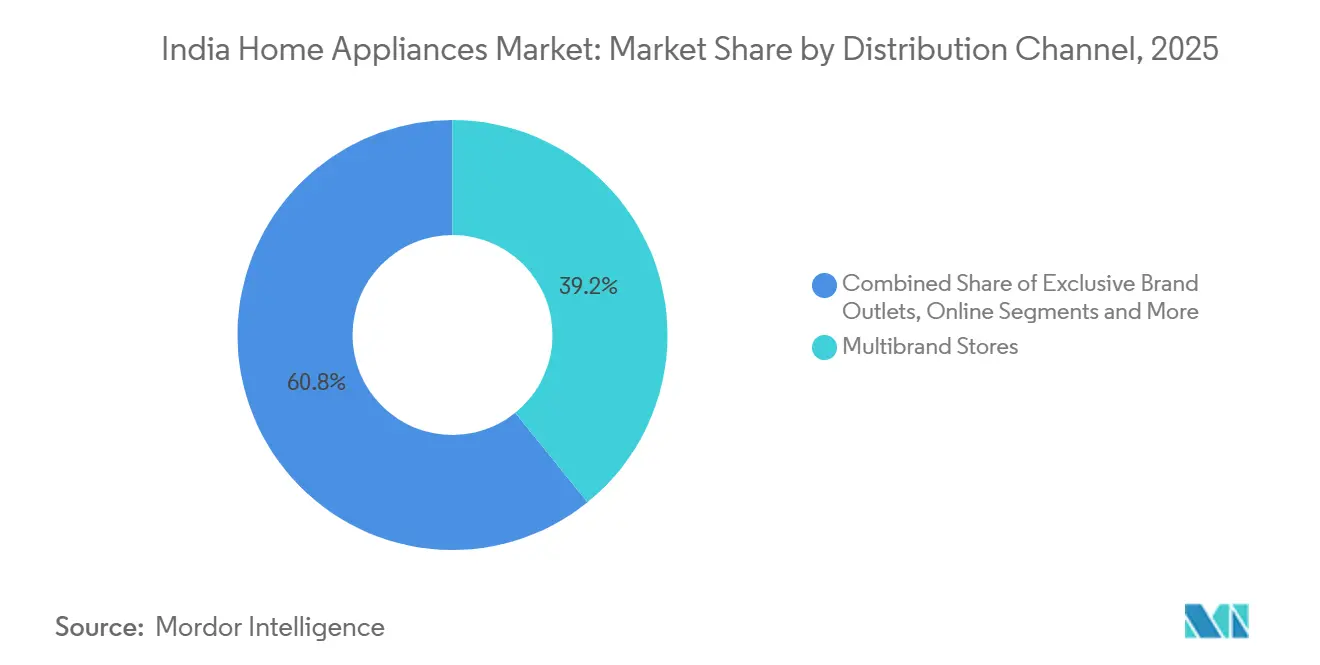

- By distribution channel, multibrand store formats accounted for 39.2% of the India home appliances market size in 2025; online is expected to grow at a 16.9% CAGR through 2031.

- By geography, North India captured 33.20% of the India home appliances market share in 2025; South India is forecast to rise at a 14.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income & Aspirational Spending | +1.30% | National, early gains in North and West metros | Medium term (2–4 years) |

| Rapid Urbanisation & Growth of Nuclear Families | +1.10% | National, tier-1 and tier-2 cities | Long term (≥ 4 years) |

| PLI & Make-In-India Incentives Boosting Local Manufacturing | +0.90% | Manufacturing hubs in Gujarat, Tamil Nadu, and Uttar Pradesh | Medium term (2–4 years) |

| Strong Growth In E-Commerce & Quick-Commerce Channels | +0.80% | Faster uptake in the South and West | Short term (≤ 2 years) |

| Increasing Adoption of Inverter-Grade, Energy-Efficient Appliances | +0.70% | Led by South India and urban centers | Medium term (2–4 years) |

| Emergence of Pay-Per-Use & Rental Appliance Platforms | +0.30% | Concentrated in Bangalore, Pune, Hyderabad, and NCR | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Aspirational Spending

Rising disposable incomes and shrinking urban household sizes are driving higher spending on home appliances, as smaller households have more discretionary budgets for products that reflect upward mobility. This trend is especially pronounced in tier-2 cities, where first-time buyers of refrigerators and washing machines now account for a significant share of sales, compared to replacement-driven purchases in metros. Premium appliances, including French-door refrigerators, inverter front-load washers, and IoT-enabled air conditioners, are witnessing faster growth, reflecting consumers’ willingness to pay for advanced features. Air conditioners, despite being owned by only 8% of India’s 300 million households, are experiencing unprecedented demand, with sales projected to grow 60% this summer compared to the usual 25–30%, highlighting India as the world’s fastest-growing AC market [2]Air conditioner sales surge amid India heatwave,” BBC News, bbc.com. Financing options such as zero-interest EMIs and buy-now-pay-later schemes are reducing the effective entry price, enabling earlier adoption, while aspirational spending among higher-income households continues to accelerate purchases.

Rapid Urbanisation & Growth of Nuclear Families

Rapid urbanization and the rise of nuclear families are driving significant growth in the India home appliances market. With the urban population projected to reach 600 million by 2031 and nuclear households now making up about half of all families, smaller living spaces are increasing demand for compact, multi-function appliances such as combi microwaves, 2-in-1 washer-dryers, and slim-profile refrigerators. Infrastructure improvements under the Smart Cities Mission have enhanced electricity reliability, enabling continuous power supply in most urban wards, which is a key enabler for appliance adoption. Nuclear households also exhibit higher per-capita appliance ownership, prioritizing convenience over shared resources, with air-conditioner penetration significantly higher than in joint families. This trend is self-reinforcing, as young professionals migrating to cities form nuclear households that adopt appliances rapidly, compressing the adoption cycle from decades to just a few years.

PLI & Make-In-India Incentives Boosting Local Manufacturing

The Indian government’s Production Linked Incentive (PLI) scheme and Make-in-India initiatives are driving significant domestic manufacturing growth, particularly in steel and home appliances. The PLI scheme for white goods, with a total outlay of approximately USD 75 million (INR 6,238 crore), has sanctioned 84 companies and drawn committed investments of around USD 126 million (INR 10,478 crore), encouraging domestic manufacturing over imports [4]Source: “Press Information Bureau (Press Release ID 2094465), Government of India,” pib.gov.in. . Major companies like LG Electronics and Haier are expanding capacities in India, targeting millions of additional ACs and refrigerators, with components such as compressors, motors, and PCBs required to be sourced domestically. Compliance with BIS certifications ensures energy efficiency and quality standards, reducing substandard imports and strengthening India’s home appliance market.

Growth In E-Commerce & Quick-Commerce Channels

E-commerce platforms like Amazon and Flipkart are now offering same-day delivery for small appliances such as juicers, kettles, and rice cookers, across 15 metro cities, reducing purchase cycles and targeting impulse buyers. Brands are optimizing inventory by stocking products in dark stores within 5 km of high-demand areas, enabling deliveries in 2–4 hours and lowering return rates by 10–15% through immediate product inspection. Multi-brand retailers like Croma and Reliance Digital have embraced omnichannel models, allowing customers to browse online, reserve items, and pick them up in-store within 30 minutes, combining digital convenience with physical verification. The Consumer Affairs Ministry’s 2024 e-commerce warranty guidelines ensure that manufacturer warranties are honoured from the date of installation, improving consumer confidence. Quick-commerce has been particularly effective for small appliances priced under INR 5,000 (USD 60), encouraging trial purchases and experimentation that traditional retail channels struggle to support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Sensitivity & Large Informal Grey Market | -0.50% | Tier-3 cities and rural areas nationwide | Short term (≤ 2 years) |

| Volatile Input Costs & Frequent Supply-Chain Disruptions | -0.40% | Manufacturing hubs exposed to commodity swings | Medium term (2–4 years) |

| Fragmented After-Sales Service Network | -0.30% | Acute in tier-2 and tier-3 cities | Medium term (2–4 years) |

| Growing Compliance Costs From E-Waste Regulations | -0.20% | Higher burden on smaller manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity & Large Informal Grey Market

Price sensitivity in India’s home appliance market remains high, particularly in smaller cities, with many buyers prioritizing upfront cost over long-term value. Many consumers prioritize the initial cost over long-term value, creating opportunities for unbranded and grey-market products. These products often offer lower prices but compromise on safety and quality standards. The grey market includes items from unregistered assemblers, refurbished imports, and products without valid warranties, which can erode consumer trust when they fail. Additionally, heavy discounts from e-commerce platforms have intensified competition, forcing some authorized dealers to turn to grey-market sourcing to stay competitive. Warranty enforcement is a significant issue, as many buyers of unofficial products only realize the lack of support when problems arise, limiting adoption in certain areas. To address these challenges, the government has introduced measures like mandatory QR codes linking to certification and manufacturing details. However, enforcement remains weak, particularly in rural and semi-urban regions.

Volatile Input Costs & Frequent Supply-Chain Disruptions

In the Indian home appliances market, prices of key raw materials like steel, copper, and plastics have fluctuated significantly in recent years due to global commodity trends and domestic policy changes. Higher steel and copper prices have especially increased costs for products like refrigerators, washing machines, and motor-based appliances such as mixers and vacuum cleaners. Additionally, rising crude oil prices have driven up plastic costs, affecting parts like housings and control panels. While manufacturers use forward contracts to handle these price changes, smaller companies are more exposed to sudden market shifts. Supply chain issues, including shipping delays and import restrictions, have forced brands to use costlier alternatives, reducing their profit margins. Efforts to reduce reliance on China for components like PCBs and sensors have also added operational challenges and increased lead times for manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Refrigerators Anchor Share, Air Conditioners Accelerate

In 2025, refrigerators accounted for 29.90% of the home appliances market share in India, backed by 85% urban penetration and steady upgrade cycles. Frost-free inverter designs are displacing direct-cool models as electricity costs become central to purchase criteria. Rural demand, once held back by intermittent power, is ticking post-Saubhagya rural electrification upward, widening the total addressable base. Parallelly, air conditioners are forecast to expand at a 17.50% CAGR through 2031 as climate stress intensifies and inverter regulations narrow the price delta with fixed-speed units. The India home appliances market size for compressors and refrigerant components is therefore scaling faster than the broader industry, encouraging further localization of critical parts.

Washing machines continue to migrate from semi-automatic to fully automatic formats, especially front-loaders that use up to 50% less water per cycle, an edge in drought-prone cities such as Bangalore and Chennai. Dishwashers and combo ovens remain low-penetration but are rising in affluent dual-income households that value labor-saving over cultural dishwashing norms. Small domestic appliances, led by air fryers and food processors, outpaced major appliances with 29% value growth in H1 2024, signaling that convenience-centric categories can swing overall demand even as ticket sizes remain modest. Premiumization is visible in high-wattage motors and stainless-steel builds, drawing margins upward across the India home appliances market.

By Distribution Channel: Multibrand Still Dominant, Online Races Ahead

Multibrand stores retained 39.2% share of the India home appliances market size in 2025 as shoppers still seek tactile validation for bulky, high-value items. Multi-brand chains offer side-by-side comparisons and installation support, while exclusive brand outlets stage live demos that justify premium pricing. Yet online channels are on a 16.90% CAGR trajectory because quick-commerce platforms deliver sub-INR 5,000 appliances within two hours and e-commerce giants harness direct-to-consumer economics to trim prices by up to 15%. Omnichannel hybrids, Reserve & Collect at Croma or same-day delivery via Reliance Digital, blend the strengths of both worlds and are becoming table-stakes.

For brands, dark-store inventory positioning and real-time stock visibility demand advanced demand-forecasting models backed by AI. Builders pre-installing appliances in premium projects account for a small but high-value slice that is growing 6–8% annually. Corporate bulk orders from co-living operators and hospitality groups add further diversity to the channel mix, cushioning cyclicality and reinforcing the India home appliances market’s steady growth path.

Geography Analysis

In 2025, North India held 33.20% of the home appliances market size in India, due to prosperous clusters in NCR, Punjab, and Haryana, where extreme summer temperatures push cooling adoption. Refrigerator- and washing-machine volumes benefit from a cultural preference for bulk grocery buying and laundering efficiency. Power-supply reliability in Delhi and adjoining cities reduces operational anxiety, further underpinning purchases.

South India will be the fastest-growing territory at a 14.80% CAGR to 2031, already home to 40% of installed air-conditioner stock thanks to early inverter uptake and IT-sector wealth in Bangalore, Hyderabad, and Chennai. State rebates on 5-star appliances accelerate replacement, and widespread broadband penetration fuels smart-appliance adoption. Coastal humidity also drives demand for dryers and dehumidifiers that are niche elsewhere.

West India, led by Maharashtra and Gujarat, leans on Mumbai’s high disposable income and Ahmedabad’s manufacturing strength to push premium French-door refrigerators, IoT-enabled washing machines, and large-capacity microwaves. Smart City upgrades in Pune and Surat have improved grid reliability, unlocking wider appliance ownership. East and Central India lag in per-capita income but are catching up as rural electrification reaches near-universal coverage, setting the stage for future first-time purchases in the India home appliances market. The North-East remains the smallest by value, yet improved road links and growing student migration into Guwahati and Shillong are stimulating demand for rental and compact appliances.

Regulatory Landscape

India home appliances are governed by safety and quality requirements led by the Bureau of Indian Standards (BIS), alongside policy instruments that prioritize domestic manufacturing. A key recent step is the Department for Promotion of Industry and Internal Trade (DPIIT) notification of the Safety of Household, Commercial and Similar Electrical Appliances (Quality Control) Order, 2026 (S.O. 1739(E)) dated April 6, 2026, which designates BIS as the certifying and enforcing authority for covered appliances.

Under the QCO 2026, covered electrical appliances must conform to IS 302 (Part 1): 2024 (aligned with IEC 60335-1:2020) and carry the BIS Standard Mark. The implementation timeline runs from October 1, 2026 (general enterprises), January 1, 2027 (small enterprises), and April 1, 2027 (micro enterprises). Alongside BIS-led conformity requirements, the compliance burden is rising for manufacturers and importers across multiple appliance categories, reinforcing a shift toward certified supply chains and more formalized after-sales and warranty practices.

Value Chain Analysis

The India home appliances value chain starts with raw materials (steel, copper, plastics) and high-value sub-systems (compressors, motors, PCBs, sensors), then moves through component manufacturing and final assembly by OEMs and ODMs. From there, products reach consumers through distribution channels such as multi-brand retail chains, exclusive brand outlets, and faster-growing e-commerce and quick-commerce platforms. Government manufacturing programs are reshaping upstream participation through the PLI scheme for white goods (2021-2029), which targets higher domestic value addition. Selections under successive PLI rounds have also included beneficiaries focused on components and sub-assemblies, strengthening the local supplier base beyond final assembly.

The tightest bottlenecks are concentrated in imported high-value parts and compliance-linked sourcing. Industry dependence on imported compressors, motors, and PCBs, together with BIS factory certification requirements for suppliers, has periodically constrained component availability and pushed up lead times. Brands have therefore moved to localize critical parts and qualify alternate suppliers. In May 2026, a DPIIT order that linked permissible compressor imports (referenced to FY25 volumes) further increases the strategic importance of domestic compressor and motor ecosystems. On the distribution side, differentiation increasingly depends on installation capability, service coverage, and reverse logistics to reduce returns and protect brand experience in online-led sales.

Competitive Landscape

The India home appliances market is moderately concentrated, with leading multinational and domestic players such as LG, Samsung, Whirlpool, Godrej, and Voltas accounting for a significant share of total market revenues. Their strong presence is built on extensive distribution networks, brand recall, and after-sales service infrastructure across urban and semi-urban regions. However, this concentration still leaves meaningful whitespace for regional manufacturers and digital-first challengers, particularly in niche categories and price-sensitive segments. While multinational corporations leverage global scale and brand equity, domestic players benefit from localized market understanding, enabling them to compete effectively on customization and affordability. As a result, competition remains dynamic, with innovation, pricing, and reach acting as key differentiators. The coexistence of global giants and agile domestic firms continues to shape a competitive yet fragmented landscape.

Multinational companies operating in India increasingly leverage their global R&D capabilities to introduce advanced features such as AI-enabled diagnostics, smart sensors, and voice-controlled interfaces, targeting premium and upper-middle-income consumers. At the same time, domestic brands emphasize India-specific product designs, value pricing, and robust performance tailored to local usage conditions such as voltage fluctuations and water quality variations. Government-led initiatives, particularly the Production Linked Incentive (PLI) scheme, have encouraged capacity expansions by players such as LG and Haier, supporting localized manufacturing and reducing reliance on imports. These investments are improving supply-chain resilience, shortening product development cycles, and enabling faster rollout of new models. Additionally, extended warranties on critical components, such as compressors and motors, are becoming common, strengthening customer trust and enhancing brand loyalty. Together, these factors are elevating competitive intensity across both premium and mass-market segments.

Technology adoption increasingly segments the Indian home appliances market, with premium consumers gravitating toward smart, app-connected, and digitally integrated appliances, while value-conscious buyers prioritize durability, energy efficiency, and long-term operating costs. Emerging startups such as Atomberg and Livpure are leveraging e-commerce and direct-to-consumer channels to reach younger, tech-savvy consumers, often combining smart functionality with competitive pricing. These challengers benefit from asset-light models and strong digital marketing, allowing them to scale quickly without traditional retail dependencies. However, upcoming Bureau of Indian Standards (BIS) energy-efficiency revisions may raise compliance costs and technical entry barriers, potentially favoring incumbents with in-house R&D and manufacturing capabilities. As regulatory standards tighten, market consolidation is likely to increase, strengthening the position of established brands while testing the scalability of smaller players. Overall, the competitive landscape is evolving toward higher technological sophistication and regulatory-driven differentiation.

India Home Appliances Industry Leaders

LG Electronics

Whirlpool Corporation

Samsung India Electronics

Godrej Appliances

IFB Industries

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A program-led opportunity is emerging around electrification of cooking and large-scale procurement of efficient small appliances. In May 2026, the Government of India moved to ramp up domestic induction cooktop production, with procurement plans of 6 to 8 million units via EESL over about 18 months. This creates a tender-driven demand pool that can accelerate scale for Indian manufacturers and component suppliers, including heating elements, power electronics, plastics, and control boards. The channel favors firms that can meet compliance requirements, deliver consistent quality, and support warranty and service at volume.

On the competitive and manufacturing side, new investments and portfolio repositioning are widening addressable segments and deepening localization. BSH Home Appliances entered India’s mass-market segment in June 2026 with a large model refresh and a lower entry price architecture, intensifying competition in high-volume categories and expanding consumer choice beyond premium-only positioning. Capacity and component localization initiatives also point to where demand is building for both major and small appliances as online and quick-commerce shorten purchase cycles. EPACK Durable’s approved INR 1,084.31 crore investment package in Andhra Pradesh (July 2026) for air conditioners, washing machines, and components, along with Versuni’s manufacturing upgrades in Chennai (including an air fryer motor line), highlight whitespace in motors, sub-assemblies, and ODM-led production.

Recent Industry Developments

- July 2026: Samsung launched new Bespoke AI air conditioners in India targeted at monsoon humidity management. The rollout extends AI-led differentiation from summer cooling into a seasonality-driven use case, supporting premiumization and higher feature adoption in room air conditioners.

- October 2025: LG Electronics India launched its Essential Series of home appliances for Indian households, spanning a refrigerator, washing machine, room AC, and convertible oven. Designed using insights from over 1,200 Indian families, the lineup supports faster replacement and first-time adoption by aligning feature sets to local usage and value thresholds.

- September 2024: Godrej Appliances invested INR 100 crore to add a new production facility at Shirwal, Pune, focused on AI-technology-powered front-load washing machines. The added capacity strengthens local manufacturing depth in laundry appliances and supports shorter lead times and better control over quality and service outcomes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the India home appliances market is the value of household appliance sales in India across major and small appliances, counted at the point of sale into the country market in USD.

Scope exclusions: We exclude non-household industrial equipment, replacement parts sold separately, and installation-only service revenue when it is billed outside the appliance sale.

Segmentation Overview

- By Product

- Major Home Appliances

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances

- Small Home Appliances

- Coffee Makers

- Food Processors

- Grills & Roasters

- Electric Kettles

- Juicers & Blenders

- Air Fryers

- Vacuum Cleaners

- Electric Rice Cookers

- Toasters

- Countertop Ovens

- Other Small Home Appliances

- Major Home Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- North India

- South India

- West India

- East India

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping the category structure for home appliances in India and then aligning it with measurable signals for demand and supply. Public references were used to anchor the model, such as India's Ministry of Commerce and Industry trade statistics, the National Statistical Office (MOSPI) household consumption series, the Bureau of Energy Efficiency label and standards updates, and the Reserve Bank of India macro indicators that influence household spending.

To sharpen assumptions that are hard to observe directly, we also reviewed company annual reports and investor presentations, product specification sheets, and reputable press coverage on pricing and channel shifts. Where it helped, we used paid subscriptions for company financials and intelligence, shipment-level import and export records, and patent databases to validate product activity and timing. These sources are illustrative, and many other public and paid references were checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were used to pressure-test the desk assumptions on category splits, channel mix, and realistic pricing moves across India. We covered stakeholders across manufacturing, distribution, and retail, and we also spoke with industry experts who track demand across North, South, East, and West India so gaps from published sources could be closed before final sign-off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | |

| Mid tier: 49% | Functional/Unit leaders: 27% | |

| Smaller Players: 14% | Managers: 60% |

Market-Sizing & Forecasting

The sizing is built using a top-down demand pool approach, where household formation, urbanization, electrification, and appliance penetration levels are translated into category volumes before values are derived through realistic average selling prices. Since many appliances are imported as finished goods or as key components, trade flows and tariff changes were also checked to make sure the implied supply picture did not conflict with the demand build.

To keep the totals grounded, we then corroborated the outputs with selective bottom-up approximations, including sampled price tracking across channels, distributor feedback on mix shifts, and a roll-up of reported category revenue where it could be cleanly attributed to India. Inputs that mattered most in practice included room air conditioner seasonality, energy label driven product replacement cycles, e-commerce share gains versus multi-brand outlets, and the pace of premiumization in refrigerators, washing machines, and small kitchen appliances. For forecasting, scenario analysis was used around income growth and summer intensity, and then it was tied back to interview-led expectations for penetration and price progression. Where direct volume indicators were thin for niche appliances, gaps were handled by using proxy adoption rates from comparable appliance categories and then re-tested with channel checks.

Data Validation & Update Cycle

Validation happens in layers so the final number does not depend on one data stream. Model results are compared against independent signals like import trends, category price movements, and visible retail expansion, and then variances are investigated until the drivers are clear. If a step change is seen, such as a sudden price drop, a channel disruption, or a policy move affecting imports or energy standards, we re-contact sources to confirm what changed.

Before release, the work goes through analyst cross-checks on formulas, units, currency timing, and year-on-year continuity, followed by a final review that focuses on outliers by category and region. Reports are refreshed annually, and interim updates are made when material events could shift demand or pricing meaningfully, which helps clients receive a current view.

Mordor Intelligence's India Home Appliances Market Market Size Versus Other Published Estimates

Published market sizes for India home appliances can look far apart, even when the topic sounds identical, because the category list, channel treatment, and pricing assumptions are not consistent across publishers. Differences also show up when one estimate leans on manufacturer value versus retail value, or when the base year and currency conversion timing are not aligned.

The main gap comes from whether adjacent electronics and consumer devices are bundled into home appliances, and how major and small appliances are counted across retail and online channels, a scope choice that Mordor Intelligence applies by keeping the definition tied to household appliances sold in India and by separating appliance value from add-on service billing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 54.60 B (2026) | |

| Global Consultancy A | USD 81.21 B (2025) | Uses a different base year and tends to apply a broader household scope, which can pull in adjacent categories and a higher retail value capture, thereby lifting the total versus a stricter appliance-only build. |

| Industry Publisher B | USD 69.02 B (2025) | Runs a longer forecast horizon and often applies a wider channel and product mapping, where the treatment of premiumization and price progression can raise the 2025 value versus an ASP path that is validated with channel checks. |

Looking at the spread, the biggest drivers are definition choices, base year alignment, and how pricing is moved forward across categories with very different replacement and seasonality patterns. Our approach keeps each step traceable to simple signals like penetration, channel mix, and price ranges, which makes the final number easier to reproduce and explain.

Key Questions Answered in the Report

How large is the India home appliances market in 2026?

It stands at USD 54.60 billion and is forecast to reach USD 71.85 billion by 2031, reflecting a 5.65% CAGR.

Which product class grows fastest through 2031?

Air conditioners, expanding at a 17.50% CAGR as inverter regulations cut energy costs and climate conditions intensify.

What share do online channels hold?

Online formats account for 31.60% of 2025 sales and are projected to grow at a 16.90% CAGR on the strength of quick-commerce delivery.

Why is South India the growth hot spot?

The region already hosts 40% of installed AC units and combines higher IT-sector incomes with state rebates on 5-star appliances, supporting a 14.80% CAGR.

How do PLI incentives change the competitive landscape?

They channel subsidies to local production, encouraging multinationals and domestic firms to expand capacity and deepen component localization.

Page last updated on: