India Car Loan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

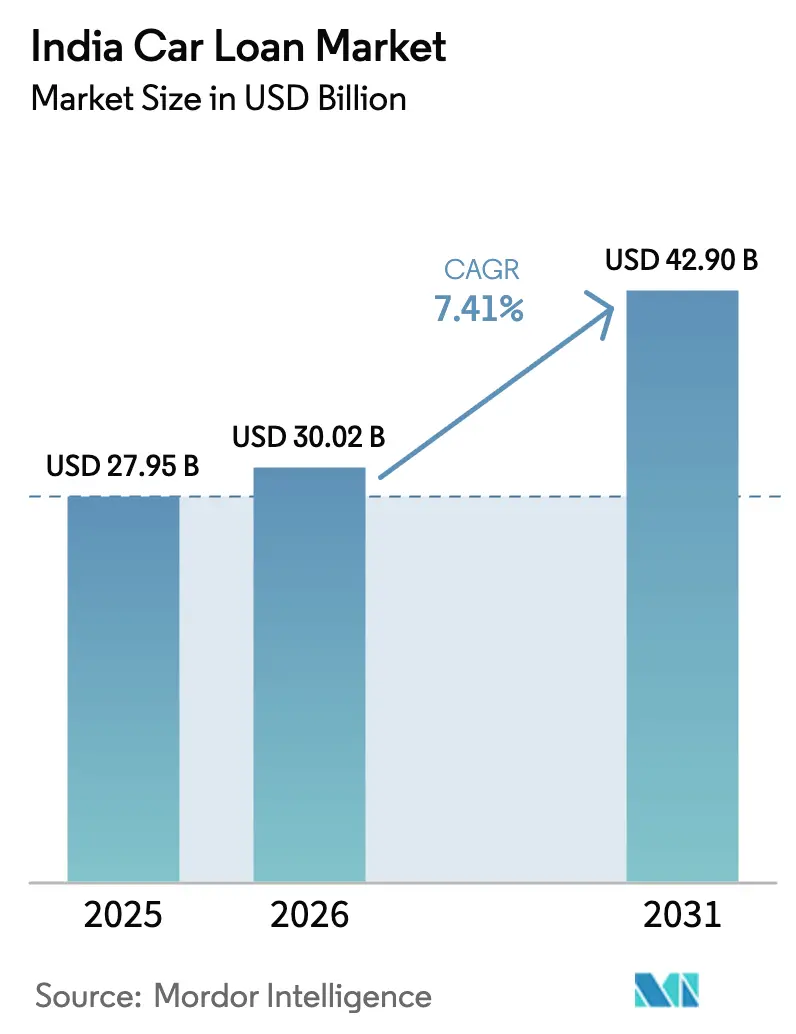

| Base Year Market Size (2025) | USD 27.95 Billion |

| Market Size (2026) | USD 30.02 Billion |

| Market Size (2031) | USD 42.90 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

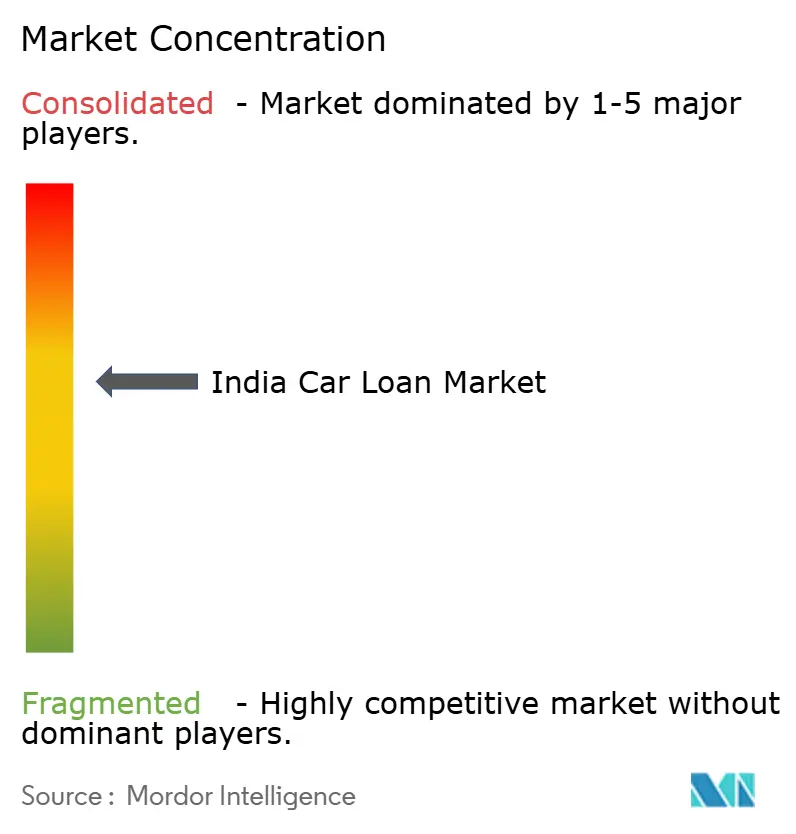

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Car Loan Market Analysis by Mordor Intelligence

The India Car Loan Market size is projected to be USD 27.95 billion in 2025, USD 30.02 billion in 2026, and reach USD 42.90 billion by 2031, growing at a CAGR of 7.41% from 2026 to 2031.

Favorable monetary policy, faster digital onboarding, and expanding alternative data sources combine to widen access to formal vehicle financing and push the India car loan market toward structurally higher growth levels. Competitive pricing by banks, growing securitization appetite, and manufacturer-subsidized electric-vehicle (EV) loans are compressing borrowing costs and lifting loan eligibility for new cohorts of consumers. Digital KYC and e-mandate rails now cut average turnaround time to under 30 minutes, improving customer experience and supporting volume growth in metro as well as tier-2 and tier-3 cities. Simultaneously, co-lending arrangements and Account Aggregator data flows diversify funding and underwriting models, ensuring that the addressable borrower pool for the India car loan market continues to expand even in risk-averse credit cycles[1]Reserve Bank of India, “Monetary Policy Statement February 2025,” rbi.org.in.

Key Report Takeaways

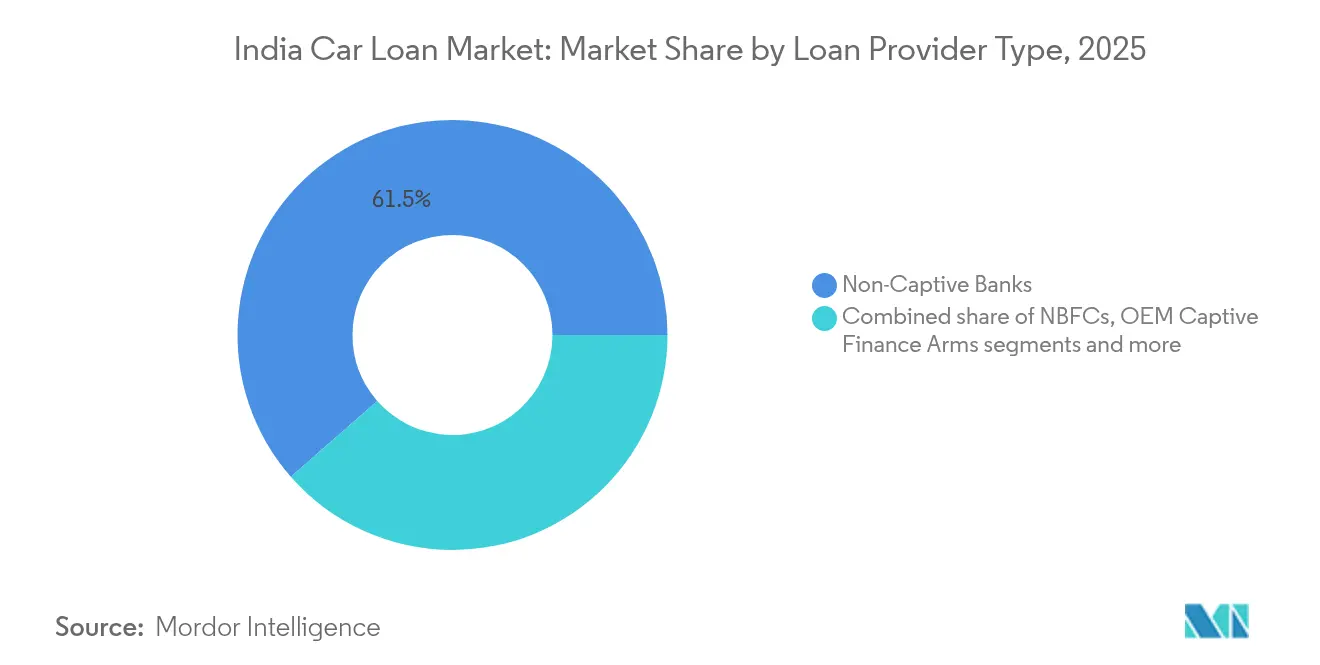

- By loan-provider type, non-captive banks held a 61.45% share of the India car loan market in 2025, while non-banking financial companies recorded the fastest 7.82% CAGR through 2031.

- By vehicle type, new cars commanded 71.35% of the India car loan market share in 2025, whereas used-car financing is advancing at an 7.96% CAGR to 2031.

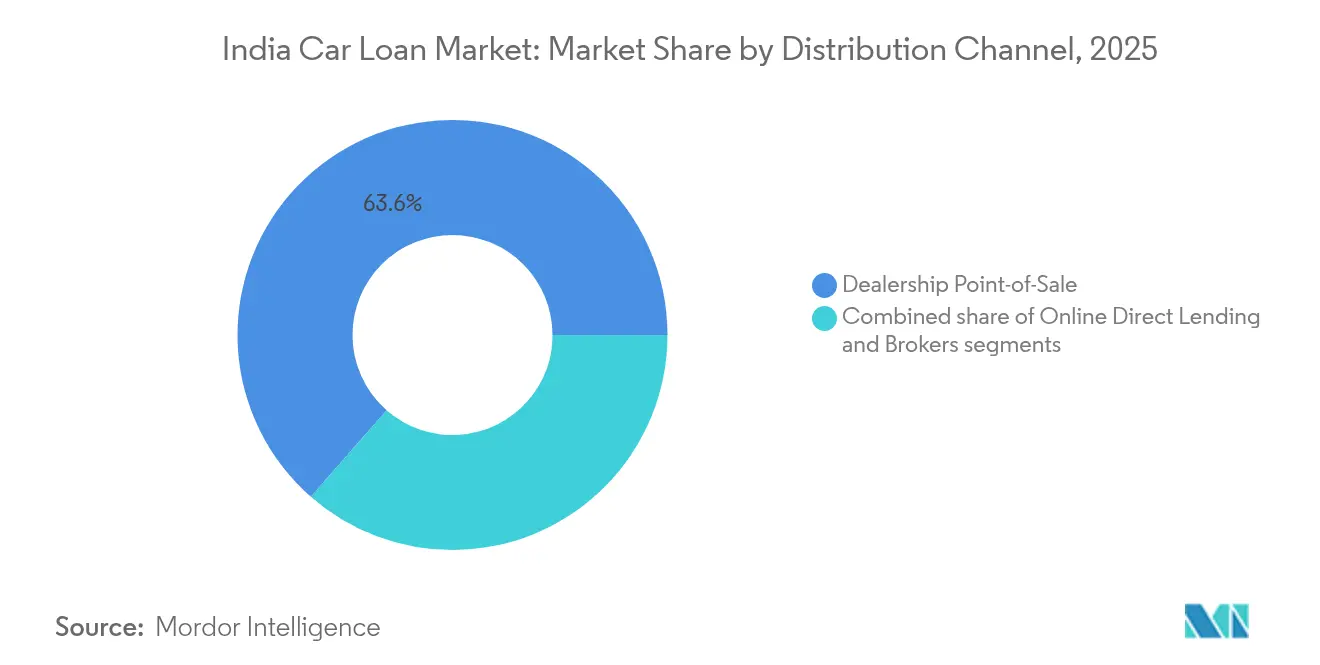

- By distribution channel, dealership point-of-sale captured 63.55% of the India car loan market in 2025; online direct lending, however, is forecast to grow at 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Figures recorded within India feed into a worldwide estimate while studying the global industry. Mordor Intelligence's car loan market size captures this aggregation.

India Car Loan Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural fall in repo/MCLR spreads boosts affordability | +1.2% | National, stronger in metro and tier-1 cities | Short term (≤ 2 years) |

| OEM-subsidized green-car loans accelerate EV adoption | +0.8% | National, early gains in Delhi, Mumbai, Bangalore, Hyderabad | Medium term (2-4 years) |

| Rapid digitization of KYC and e-mandate processes | +1.5% | National, higher uptake in urban centers | Short term (≤ 2 years) |

| Tier-2 and tier-3 income growth widens borrower base | +2.1% | Tier-2/3 cities nationwide | Long term (≥ 4 years) |

| Account-Aggregator data enables thin-file underwriting | +0.9% | National, stronger in under-banked regions | Medium term (2-4 years) |

| Rising securitization appetite lowers lender funding cost | +0.7% | National, concentrated among large NBFCs and banks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Structural Fall in Repo/MCLR Rate Spreads Boosts Affordability

RBI reduced the policy repo rate from 6.5% to 6% in five calibrated cuts during 2025, prompting a broad-based drop in retail vehicle-loan rates within 30-60 days of each announcement. Banks such as Bank of India and Punjab National Bank trimmed car-loan rates by 25 basis points, lowering equated monthly installments for a five-year INR 500,000 loan by INR 150-200. Lower monthly payments improve debt-to-income ratios and enlarge the eligible borrower pool by close to one-fifth, supporting incremental loan originations in both metro and tier-2 clusters. Competitive rate transmission also intensifies price-based rivalry among lenders, forcing traditionally conservative players to adopt dynamic repricing strategies. The India car loan market, therefore, enjoys a durable affordability tailwind as monetary policy remains growth-supportive in the short term.

OEM-Subsidized Green-Car Loans Accelerate EV Adoption

Auto manufacturers cooperate with captive finance arms and third-party banks to offer 0.05%-0.50% rate concessions on EV loans, narrowing the total-cost-of-ownership gap with internal-combustion models[2]Tata Motors, “Annual Integrated Report 2025,” tatamotors.com. State Bank of India’s Green Car Loan facility prices EV credit at 8.85%-9.90%, while Bank of India provides an additional 0.50% markdown for battery-electric purchases. Layered onto central and state EV incentives, these concessions improve affordability and stimulate early-stage demand in pollution-conscious metro markets. Captive financiers from Toyota and Hyundai reinforce dealer relationships by bundling finance with warranty extensions and charging-station support. As charging infrastructure scales, the India car loan market captures incremental EV volumes and fortifies its medium-term growth outlook.

Rapid Digitization of KYC & E-Mandate Processes Cuts TAT to Under 30 Minutes

RBI Digital Lending Directions 2025 require standardized onboarding while permitting full e-KYC and e-mandate journeys that slash approval time to below 30 minutes[3]National Payments Corporation of India, “e-NACH Adoption Report 2025,” npci.org.in. Large banks deploy optical-character-recognition engines and AI-driven income analytics, trimming manual checks and boosting straight-through-processing ratios above 80%. Instant mandate creation on the NCPI e-NACH platform removes the need for paper forms and branch visits, elevating customer satisfaction and referral volumes. Account-Aggregator connectivity supplies consent-based transaction data that replaces multiple bank-statement uploads and accelerates underwriting for self-employed borrowers. Speed and simplicity become decisive selection criteria, strengthening the competitive position of tech-forward lenders in the India car loan market.

Tier-2/3 Income Growth & Formalization Widen Borrower Base

Vision IAS forecasts India’s GDP to quadruple to USD 40 trillion by 2047, with smaller cities driving 60% of new output and generating verifiable income trails through GST and digital payments. Rising disposable income, organized retail expansion, and formal payroll adoption enlarge the population of credit-worthy but previously underserved consumers. Banks establish satellite branches and mobile-based loan officers to harness local knowledge, while NBFCs exploit dense on-ground networks in towns such as Coimbatore, Indore, and Guwahati. Aspirational car ownership gains momentum as first-time buyers shift from two-wheelers to compact cars, lifting penetration in lower-tier markets. The India car loan market leverages this demographic dividend to secure a long-tail growth engine beyond metro centers.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Used-car collateral valuation volatility raises NPA risk | -0.9% | National, more acute in tier-2/3 cities | Medium term (2-4 years) |

| RBI’s higher retail-unsecured risk weight tightens credit | -0.6% | National, heavier impact on NBFCs | Short term (≤ 2 years) |

| EV residual-value uncertainty curbs lender LTV ratios | -0.4% | National, concentrated in major EV hubs | Long term (≥ 4 years) |

| Rising cyber-fraud in digital channels inflates cost-to-serve | -0.5% | National, acute for digital-first lenders | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Used-Car Collateral Valuation Volatility Raises NPA Risk

Price discovery in India’s fragmented used-car ecosystem remains inconsistent because unorganized dealers dominate retail supply, and centralized valuation databases are nascent[4]Maruti Suzuki India, “True Value Certified Pre-Owned Program Overview 2025,” marutisuzuki.com. Lenders therefore face collateral markdowns when market demand softens, pushing loan-to-value ratios above realizable resale proceeds during stress scenarios. Regional demand swings, rapid model obsolescence, and limited uniform vehicle-inspection standards further complicate recovery prospects after default. To mitigate the risk, financiers lower LTV thresholds on used-car loans and integrate third-party inspection APIs that standardize condition reports, although these measures raise processing costs. The India car loan market must balance the growth opportunity in used vehicles with disciplined collateral management to prevent asset-quality deterioration.

RBI’s Higher Retail-Unsecured Risk Weight Tightens Credit

In November 2023, the central bank raised risk weights on unsecured personal loans, prompting a supervisory spill-over into secured retail books as lenders reassessed aggregate borrower leverage. Although February 2025 relaxations restored some capital relief, many NBFCs still encounter elevated wholesale-funding spreads that restrain aggressive expansion. Banks apply stricter debt-service-ratio cut-offs and higher documentation thresholds, excluding thin-file applicants and slowing disbursal run-rates during cyclical upswings. Co-lending agreements now require 10% minimum retention by originators, reshaping risk-transfer economics between banks and NBFC partners. The India car loan market will continue to manage growth-quality trade-offs as regulatory oversight prioritizes systemic stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Provider Type: NBFCs Challenge Bank Dominance

Non-captive banks commanded a 61.45% share of the India car loan market size in 2025, leveraging low funding costs and entrenched branch relationships to serve prime borrowers nationwide. NBFCs, however, are expanding at a 7.82% CAGR to 2031 by targeting self-employed customers, thin-file applicants, and tier-2/3 geographies where traditional banks remain under-penetrated. Regulatory clarity on co-lending permits NBFCs to loop in bank funds while retaining origination control, creating blended models that share risk capital yet accelerate disbursals. Captive finance arms of OEMs strengthen dealer throughput by bundling promotional rates with brand-specific warranty extensions, thereby defending niche pockets of the India car loan market. Competitive signaling through faster approvals, flexible repayment schedules, and digital dashboards redefines value propositions and keeps market-share shifts fluid.

Banks reinforce their primacy by cross-selling bundled savings accounts, credit cards, and insurance, turning vehicle loans into relationship footholds that broaden lifetime value. Meanwhile, fintech-enabled NBFCs adopt alternative data, telematics feeds, and psychometric scoring to deep-mine credit-invisible segments at scale. Regulatory guardrails around digital lending drive investments in governance tech, favoring well-capitalized providers with mature compliance frameworks. OEM captives increasingly partner with fintechs to embed finance at the point of vehicle configuration, meeting customer expectations for frictionless checkout. Thus, provider-type dynamics in the India car loan market remain balanced, with innovation and cost-of-funds acting as twin axes of competitive advantage.

By Vehicle Type: Used Cars Accelerate Despite New-Car Dominance

New vehicles accounted for 71.35% of the India car loan market share in 2025 because organized dealer networks, predictable residual values, and OEM incentive schemes simplify credit risk management. Pre-owned cars, however, register an 7.96% CAGR through 2031 as digital inspection platforms, AI-based pricing tools, and warranty add-ons reduce information asymmetry and boost lender confidence. Organized retailers such as Maruti Suzuki True Value and Cars24 integrate real-time valuation APIs that lenders can query at origination to verify collateral quality. Rapid urbanization and aspirational ownership among first-time buyers in tier-2 cities drive demand for affordable used cars, expanding addressable volumes. Consequently, segmental diversification lowers portfolio concentration and supports counter-cyclical stability in the India car loan market.

Electric models introduce fresh complexities in both new and used segments owing to battery-health uncertainty, yet they also create opportunities for specialized finance products that bundle residual-value guarantees. Rising penetration of connected-car telematics delivers usage data that insurers and lenders use to refine risk-based pricing. Depreciation curves differ by fuel type, model generation, and regional demand, compelling lenders to adopt differentiated LTV matrices. Enhanced refurbishment standards at organized used-car outlets further de-risk collateral by ensuring mechanical quality and predictable resale timelines. As these ecosystem improvements gain traction, the India car loan market size for used vehicles is poised to rise rapidly without materially elevating non-performing assets.

By Distribution Channel: Digital Channels Disrupt Traditional Models

Dealership point-of-sale retained a 63.55% share of the India car loan market in 2025 because it synchronizes vehicle selection, financing, and delivery within a single visit. Nevertheless, online direct lending is forecast to expand at 8.78% CAGR through 2031 as consumers increasingly prefer anytime access, rate transparency, and app-based approval. Fintech marketplaces aggregate multiple lenders, enabling customers to compare pre-qualified offers and choose lower EMI structures in minutes. Account-Aggregator integration accelerates income verification while e-NACH simplifies mandate creation, compressing origination costs and improving margins for digital-first providers. These advantages allow online channels to penetrate beyond metros into smaller towns where branch networks are sparse, yet smartphone adoption is high, thereby enlarging the India car loan market.

Dealers respond by embedding lender APIs into showroom systems, offering hybrid journeys where customers initiate applications in person but complete documentation digitally. Captive finance companies exploit physical-digital convergence to pre-approve repeat buyers and arrange delivery within 24 hours, sustaining loyalty. Brokers and aggregators monetize data generated from price comparisons by supplying lenders with propensity-to-buy scores, raising conversion efficiency. RBI’s Digital Lending Directions mandate transparent rate disclosures and secure consent flows, encouraging responsible innovation while reducing mis-selling. Over time, channel boundaries blur, but speed, personalization, and regulatory compliance remain the critical success factors in distribution share battles across the India car loan market.

Geography Analysis

Metro and tier-1 cities contributed roughly 69.20% of disbursed value to the India car loan market in 2025, reflecting higher per-capita incomes, dense dealer networks, and mature banking infrastructure. Northern and western regions, home to industrial hubs such as Delhi-NCR, Mumbai, and Pune, hold the largest absolute market, while the south, led by Chennai and Bangalore, records robust adoption of digital loan journeys. Tier-2 and tier-3 cities like Lucknow, Coimbatore, and Jaipur are clocking double-digit loan growth as formal payroll penetration improves and organized retail expands footprints. Lenders tailor underwriting to local income mixes, incorporating agricultural cash-flow seasonality in semi-rural belts surrounding smaller cities. As highway construction under Bharatmala and state road upgrades link peripheral towns, latent mobility demand converts into financed car purchases that add breadth to the India car loan market.

Regional variations in road-tax rebates, vehicle-registration fees, and EV subsidies influence borrowing costs and repayment preferences, prompting lenders to customize EMI tenure options and seasonal moratoriums. In the east, Kolkata and Bhubaneshwar are witnessing an uptick in compact-SUV loans linked to mining and infrastructure employment, whereas the west shows higher penetration of premium sedans financed through salary-linked products. Bangladesh and Nepal border trade corridors encourage cross-state used-car flows, necessitating vigilant collateral tracking to prevent asset leakage. Digital channels enable lenders to underwrite customers in districts where physical branches are absent, and field-verification partners handle ground-truthing for high-ticket loans. Consequently, geography-specific strategies become indispensable for sustained share gains in the India car loan market.

State governments increasingly integrate Vahan and Sarathi transport databases, enhancing lien noting and ownership-transfer processes that lower fraud risks and speed repossession in default cases. Lenders employ geo-analytics to calibrate dealer recruitment, optimize collection routes, and allocate risk-adjusted capital by pin code clusters. Government-backed industrial corridors spur ancillary auto-component manufacturing clusters, bringing new employment families into the formal credit grid. Public-charging infrastructure rollouts in Delhi, Maharashtra, and Karnataka gradually normalize EV financing outside metros, diversifying geographic risk. Together, e r these trends underscore that a nuanced, region-aware playbook is critical for scaling operations while preserving portfolio hygiene in the India car loan market.

Mordor Intelligence evaluates the car loan market across all key regional markets, including Europe and Asia, with deeper country-level insights covering India, South Korea, France, Russia, China, Japan, and United Kingdom.

Competitive Landscape

The India car loan market remains moderately concentrated, with the five largest lenders accounting major market share of outstanding balances, indicating space for agile challengers to capture niche segments. Large banks exploit inexpensive deposits and multi-product relationships to price loans competitively, yet NBFCs narrow the gap by harnessing securitization to recycle capital and maintain growth velocity. Fintech entrants differentiate via AI-driven underwriting and personalized in-app experiences that appeal to digitally native millennials, encroaching on the prime salaried customer base traditionally owned by banks. Co-lending partnerships allow banks to ride on NBFC origination strengths in smaller towns while sharing risk on a pro-rata basis, creating hybrid models that blur organizational boundaries. Against this backdrop, continual tech investment, regulatory compliance, and customer-centric innovation define competitive success factors in the India car loan market.

Strategic moves include HDFC Bank’s INR 90.6 billion securitization of auto loans to access cheaper market funding and free up capital for fresh disbursals. Axis Bank initiated a strategic review of Axis Finance in February 2025, exploring a potential majority stake sale valued at up to USD 1 billion to sharpen focus on core banking operations and optimize capital. Fintech marketplace CarDekho Rupyy partnered with multiple NBFCs to launch instant approval journeys that reduce dealer dependency and cut acquisition cost per file by 30%. Shriram Finance expanded telematics-based repayment tracking for commercial-use vehicles, enhancing early-warning signals and lowering Gross NPA ratios in its vehicle book. As players experiment with product innovation and inorganic moves, the India car loan market continues to evolve into a technology-augmented credit ecosystem.

Regulatory oversight under RBI Digital Lending Directions compels all providers to establish Board-approved product governance frameworks, strengthening consumer protection and data security. Market leaders allocate double-digit percentages of operating budgets to tech modernization, risk-model recalibration, and cyber-resilience programs. Consolidation pressures build as scale benefits in data, capital, and distribution become more pronounced, leading mid-sized NBFCs to seek mergers or strategic alliances. OEMs court fintech partners to embed financing at the vehicle-configuration stage, aiming to lock in buyers before they approach banks. In this environment, the India car loan market rewards institutions that can harmonize compliance rigor with user-centric digital journeys and razor-thin turnaround times.

India Car Loan Industry Leaders

State Bank of India

HDFC Bank

ICICI Bank

Axis Bank

Kotak Mahindra Bank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Axis Bank began a strategic review of wholly owned NBFC subsidiary Axis Finance, evaluating a majority stake sale that could value the unit at USD 900 million-USD 1 billion.

- October 2024: IDFC First Bank completed its merger with IDFC Limited following NCLT clearance, thereby injecting INR 600 crore cash into the merged entity and eliminating the holding-company structure.

- May 2024: Piramal Enterprises announced the merger of Piramal Capital & Housing Finance with the listed parent to meet RBI scale-based supervision norms and sidestep a separate IPO.

- May 2024: Aditya Birla Finance entered talks to merge with Aditya Birla Capital within a 12-month window, aiming to satisfy RBI’s mandatory public-listing requirement for upper-layer NBFCs by September 2025.

India Car Loan Market Report Scope

A car loan is the funds that one borrows from a lender for the sole purpose of purchasing a car. Lenders like banks and non-banking financial companies (NBFCs) offer auto finance to consumers in the form of new and used car loans.

India's car loan market is segmented by type, car type, provider type, percentage of amount sanctioned, type of city, and tenure. By type, the market is segmented by new cars and used cars. By car type, the market is segmented by SUVs, hatchbacks, and sedans. By provider type, the market is segmented by OEM (original equipment manufacturer), bank, and non-banking financial companies. By tenure, the market is segmented into less than 3 years, 3 to 5 years, and more than 5 years.

The report offers market size and forecasts for the Indian car loan market in value (USD) for all the above segments.

| Non-Captive Banks |

| Non-Banking Financial Companies (NBFCs) |

| OEM Captive Finance Arms |

| Other Providers (Co-lending, FinTech platforms) |

| New Car |

| Used Car |

| Dealership Point-of-Sale |

| Online Direct Lending |

| Brokers & Marketplaces |

| By Loan Provider Type | Non-Captive Banks |

| Non-Banking Financial Companies (NBFCs) | |

| OEM Captive Finance Arms | |

| Other Providers (Co-lending, FinTech platforms) | |

| By Vehicle Type | New Car |

| Used Car | |

| By Distribution Channel | Dealership Point-of-Sale |

| Online Direct Lending | |

| Brokers & Marketplaces |

Key Questions Answered in the Report

What is the projected value of the India car loan market by 2031?

The India car loan market is forecast to reach USD 42.9 billion by 2031, reflecting a 7.41% CAGR over 2026-2031.

Which loan-provider segment is growing fastest?

Non-banking financial companies are expanding at a 7.82% CAGR through 2031 by targeting underserved customer segments in tier-2 and tier-3 cities.

How large is the new-versus-used vehicle split?

New cars held a 71.35% share in 2025, while used-car financing is rising quickly with an 7.96% CAGR projected through 2031.

Why are online lending channels gaining traction?

Online direct lending offers rate transparency, instant approvals, and lower acquisition costs, enabling the channel to grow at an expected 8.78% CAGR over 2026-2031.

What regulatory changes are shaping digital car loans?

RBI Digital Lending Directions 2025 mandate standardized e-KYC, transparent pricing, and secure consent flows, reinforcing consumer protection while supporting innovation.

How does EV financing differ from conventional vehicle loans?

Electric-vehicle loans often feature OEM-subsidized rate concessions yet carry lower LTVs due to residual-value uncertainty, requiring specialized risk management frameworks.

Page last updated on: