India Auto Loan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

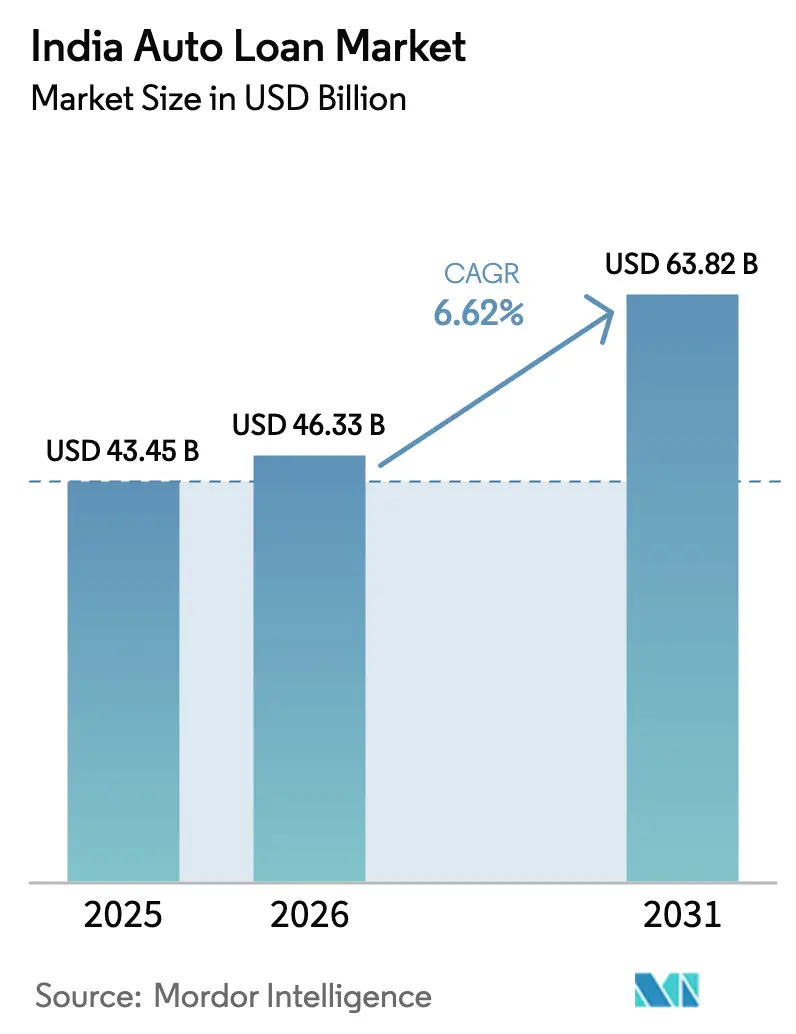

| Base Year Market Size (2025) | USD 43.45 Billion |

| Market Size (2026) | USD 46.33 Billion |

| Market Size (2031) | USD 63.82 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

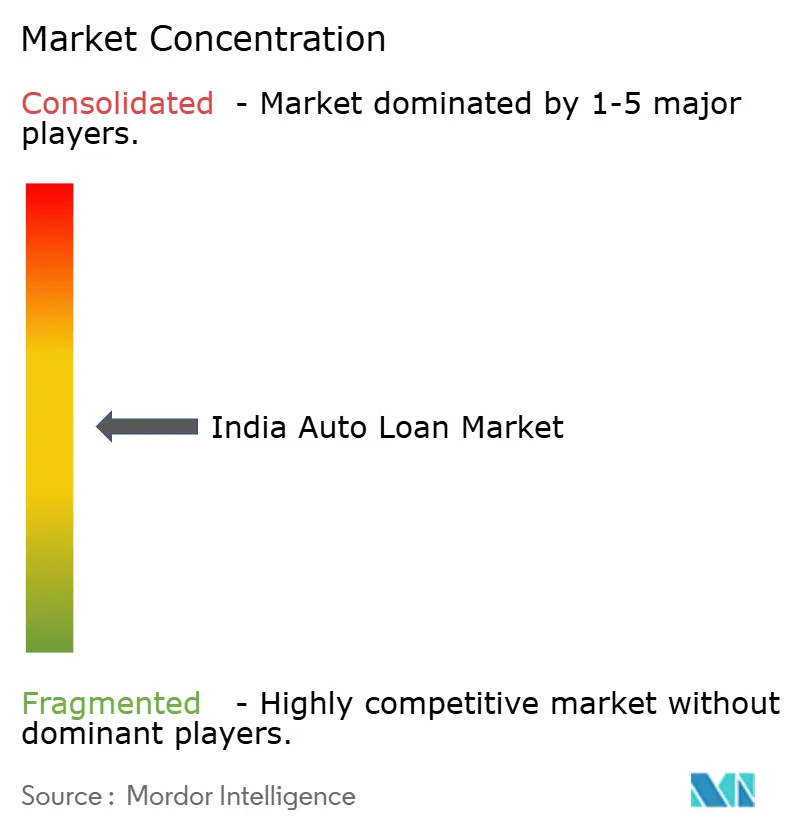

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Auto Loan Market Analysis by Mordor Intelligence

The India auto loan market size was valued at USD 43.45 billion in 2025 and estimated to grow from USD 46.33 billion in 2026 to reach USD 63.82 billion by 2031, at a CAGR of 6.62% during the forecast period (2026-2031). Robust urbanization, rising disposable incomes, and expanding digital credit rails collectively underpin this trajectory. Demand is also buoyed by the government’s electric-mobility agenda, which stimulates fresh lending niches as lenders craft battery-subscription and subsidy-linked products. At the same time, the maturing Account Aggregator data-sharing layer compresses approval cycles and broadens borrower inclusion, allowing the India auto loan market to pull previously thin-file households into formal finance. Competitive pressures intensify as NBFCs leverage agile operations to win share from incumbent banks, even as captive finance arms of OEMs deploy embedded-finance platforms to lock in customers.

Key Report Takeaways

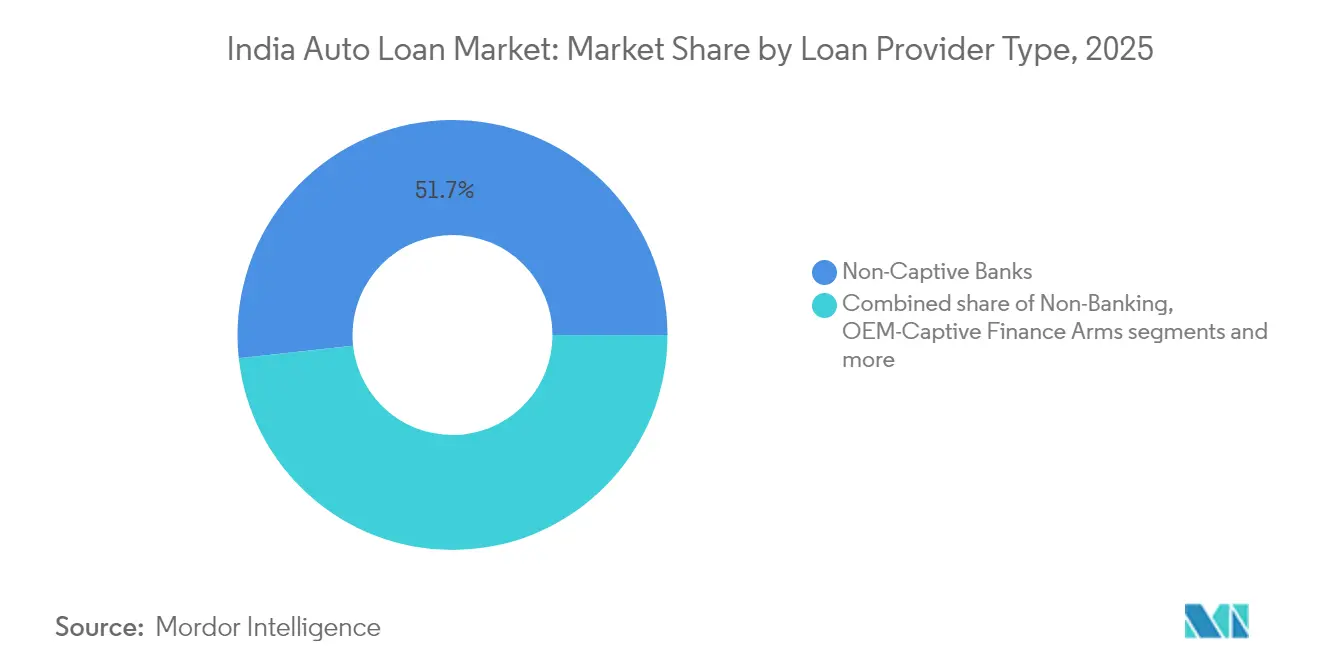

- By loan provider type, non-captive banks held 51.72% of the India auto loan market share in 2025, while NBFCs are expanding at a 7.34% CAGR through 2031.

- By vehicle type, passenger vehicles accounted for 71.55% of the India auto loan market in 2025; commercial-vehicle credit is forecast to grow at a 7.69% CAGR through 2031.

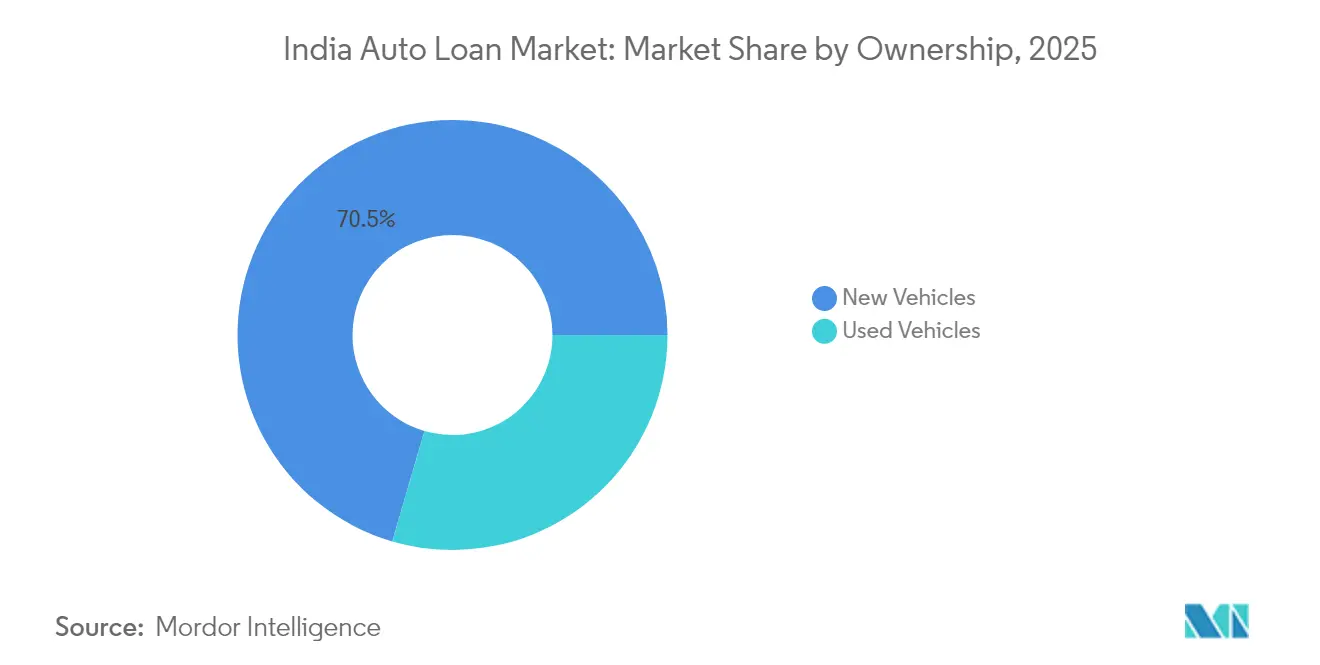

- By ownership, new-vehicle loans represented 70.48% of the India auto loan market in 2025, whereas used-vehicle financing is set to climb at an 8.39% CAGR during 2026-2031.

- By distribution channel, dealership point-of-sale retained 67.58% share in 2025, but online direct lending is advancing at an 8.78% CAGR on the back of e-KYC and instant-approval workflows.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India contributes to a system defined not by any single country or region but by the interaction of many. The global auto loan market data by Mordor Intelligence represents that combined structure.

India Auto Loan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle-ownership aspirations & GDP growth | +1.8% | Nationwide; strongest in tier-2/3 cities | Long term (≥ 4 years) |

| Increasing penetration of used-car financing | +0.9% | Metro and tier-1 catchments | Medium term (2-4 years) |

| Expanding digital lending & e-KYC adoption | +1.2% | Urban centers; scaling into semi-urban belts | Short term (≤ 2 years) |

| RBI Account-Aggregator enabling alternative data scoring | +0.7% | Early traction in Karnataka, Maharashtra, Delhi | Medium term (2-4 years) |

| Captive EV-finance subsidy programs by OEMs | +0.6% | EV hubs such as Bengaluru, Pune, Delhi NCR | Medium term (2-4 years) |

| Co-lending model unlocking tier-3/4 distribution | +0.4% | Rural and semi-urban pockets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle-Ownership Aspirations & GDP Growth

A steady elevation in per-capita GDP fortifies consumer confidence, encouraging first-time buyers to migrate from two-wheelers to entry-segment cars or from cars to utility vehicles. Tier-2 and tier-3 agglomerations post the fastest credit off-take as road-network upgrades make private mobility more practical. Micro-enterprise owners also pivot toward small commercial vans, harnessing credit for last-mile logistics contracts that mushroom amid e-commerce penetration. Lenders respond with longer tenors and step-up EMIs, enabling alignment between monthly obligations and anticipated income growth. These trends ensure resilient origination volumes within the India auto loan market even during fuel-price volatility.

RBI Account-Aggregator Enabling Alternative Data Scoring

The consent-based model gives lenders real-time visibility into current-account cash flows, mutual-fund SIPs, and insurance premiums. Thin-file borrowers in semi-urban areas who lacked bureau depth now qualify through cash-surplus analytics. Banks deploying the framework observe double-digit improvements in underwriting accuracy, translating to lower provisional buffers. Early adoption in Karnataka and Maharashtra demonstrates that integrating GST-return feeds further enriches SME credit models, particularly for commercial-vehicle loans. The architecture is poised to become the default underwriting backbone, elevating data granularity across the India auto loan market[1]Reserve Bank of India, “Master Direction on Account Aggregator Framework,” rbi.org.in.

Captive EV-Finance Subsidy Programs by OEMs

OEM finance arms bundle factory incentives with state-level subsidies, slicing net EMIs below comparable internal-combustion options for select city-commute segments. Battery-subscription schemes decouple battery ownership from chassis, mitigating residual-value ambiguity that traditionally deterred lenders. Pilot programs with cab-aggregator fleets in Delhi NCR show near-zero early-delinquency trends, emboldening lenders to stretch tenors for EV products. As charging-infrastructure density improves, captive arms expect EV penetration in their loan books to triple by 2027, amplifying credit growth vectors inside the India auto loan market[2]Press Information Bureau, “PM E-DRIVE Scheme for Electric Vehicle Promotion,” pib.gov.in.

Co-lending Model Unlocking Tier-3/4 Distribution

Revised guidelines permit banks to fund up to 80% of each co-originated auto loan while NBFCs service the customer, preserving local touch points. Early pilots in Rajasthan and Odisha recorded 35% higher disbursal velocity versus standalone NBFC operations. Embedded API rails enable real-time risk-grading and blended-rate discovery, reducing turnaround times to under 24 hours even in remote geos. The model lowers effective borrower rates by 150–200 basis points, catalyzing demand in aspirational segments and extending the geographic footprint of the India auto loan market[3]Reserve Bank of India, “Master Direction on Co-lending Model,” rbi.org.in.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle prices pressuring affordability | −1.1% | Nationwide; most acute in tier-2/3 clusters | Short term (≤ 2 years) |

| Asset-quality concerns among NBFCs | −0.8% | NBFC-heavy southern and western corridors | Medium term (2-4 years) |

| Scarcity of reliable EV-battery residual-value data | −0.6% | Metro EV adoption precincts | Medium term (2-4 years) |

| Possible tightening of bank risk-weights on NBFC exposure | −0.4% | System-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Prices Pressuring Affordability

Between 2024 and 2025, ex-showroom prices rose by 15–18%, driven by supply-chain disruptions and regulatory safety mandates, significantly outpacing median wage growth. In several states, monthly EMIs for entry-level hatchbacks have crossed INR 10,000 (USD 120), discouraging first-time buyers. Lenders are extending loan tenors to seven years as a countermeasure. However, this approach results in a higher total interest payout and amplifies residual-value risk. Additionally, users of shared mobility are postponing their purchases, leading to a decline in incremental demand and hindering the short-term growth of India's auto loan market.

Asset-Quality Concerns Among NBFCs

RBI's July 2025 Financial Stability Report reveals that several mid-tier NBFCs are grappling with vehicle-loan GNPA ratios exceeding 6%, a stark contrast to the sub-2% figures reported by leading private banks[4]Reserve Bank of India, “Financial Stability Report – NBFC Asset Quality Trends,” rbi.org.in. These heightened delinquencies can be traced back to aggressive forays into informal-income sectors, where the recovery from the pandemic has been inconsistent. Investors are demanding risk premiums, which has widened the spread between funding costs and bank rates, squeezing net interest margins. The tightening liquidity environment is forcing NBFCs to reassess their underwriting standards. This shift is slowing their previously rapid growth and tempering the overall expansion of India's auto loan market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Provider Type: NBFCs Reshape Competitive Balance

Non-captive banks retained dominance with a 51.72% India auto loan market share in 2025, yet NBFC disbursements are compounding at a 7.34% CAGR, signaling a redistribution of power. OEM-captive finance arms exploit manufacturer insights to innovate bespoke schemes such as battery subscriptions, while fintech aggregators orchestrate digital co-lending pools. NBFC outreach in tier-3/4 locations capitalizes on informal income assessment and flexible repayment calendars, extending credit inclusion beyond traditional footprints.

The India auto loan market benefits from symbiotic bank–NBFC ties: banks supply low-cost capital and regulatory credibility, whereas NBFCs deliver origination throughput and nuanced borrower vetting. Co-lending APIs synchronize underwriting in real time, lowering operational friction. A more granular risk-pricing regime emerges, rewarding data-rich NBFCs with superior cost-of-funds and elevating competitive benchmarks across the India auto loan industry.

By Vehicle Type: Commercial Vehicles Gain Speed

In 2025, passenger cars dominated the Indian auto loan market, holding a significant 71.55% share. However, commercial vehicle (CV) loans are growing at a faster rate, with a 7.69% CAGR. This growth is driven by the increasing demand for e-commerce deliveries and the ongoing expansion of highways across the country. To manage risks, CV lenders are using telematics systems to monitor vehicle usage and ensure repayments are tied to how the vehicles are utilized. This strategy helps reduce the impact of fluctuating freight rates, which can otherwise lead to higher default risks.

Electrification of vehicle fleets is opening up new opportunities in the market. Light commercial electric vehicles (EVs) used for urban deliveries follow predictable schedules, making them suitable for overnight charging at depots. This predictability lowers operating costs and makes these vehicles more affordable in the long run. Lenders are also testing tools to monitor battery health, which helps them better predict potential defaults. These advancements are making CV loans more attractive and strengthening their position in the Indian auto loan market over time.

By Ownership: Used-Vehicle Credit Accelerates

New-vehicle loans dominate India's auto loan market, holding 70.48% of the market share in 2025, but used-vehicle financing is growing steadily at an 8.39% CAGR. Certification platforms are reducing information gaps, encouraging lenders who were previously cautious due to odometer fraud. Digital auction platforms are helping determine fair prices, increasing trust in the resale value of vehicles. Rising costs are pushing buyers toward three-year-old models, which have lower depreciation. This shift is making used-vehicle financing a key growth area in the auto loan market.

Risk-based pricing, which offers better interest rates for certified vehicles, is attracting more borrowers to the used-vehicle segment. Certified inventories are seen as lower risk, which helps lenders offer competitive rates. Buyers are drawn to these options as they provide affordability without compromising quality. This trend is expanding the auto loan market without significantly increasing risk. As a result, the used-vehicle segment is becoming an important part of India's auto loan landscape.

By Distribution Channel: Online Direct Lending Advances

Dealership financing holds a strong 67.58% share of India's auto loan market in 2025 due to its built-in sales momentum. Online direct lending, however, is growing at a notable 8.78% CAGR. Mobile apps with pre-approved limits are speeding up loan decisions to just minutes, giving digital lenders an edge. Payment apps are helping lenders find new customers at a low cost through cross-selling. This shift is gradually changing how loans are offered in the market.

Marketplace brokers are simplifying complex loans, such as co-signature loans for families. They combine digital KYC processes with doorstep document collection for convenience. New rules requiring clear fee disclosures, set to take effect in August 2025, aim to build borrower trust. These regulations are expected to create fair competition among lenders. As a result, the digital lending space in India's auto loan market is likely to grow further.

Geography Analysis

The India auto loan market highlights varying growth patterns across regions. Northern and western states, including Delhi, Mumbai, and Pune, dominate the market with their strong presence of auto OEM plants and extensive dealer networks. These regions contribute approximately 44.63% of the total loan disbursements in the country. The average loan size in these areas is 12% higher than the national average, driven by a higher demand for SUVs. The early adoption of Account Aggregators has significantly reduced loan approval times to under two hours. This efficiency has provided lenders with a competitive edge in these regions.

Southern states such as Karnataka, Tamil Nadu, and Andhra Pradesh are experiencing the fastest growth in the auto loan market, with a CAGR exceeding 8.06%. State-level EV subsidies, combined with central government incentives, have boosted the share of EV loans in Bengaluru to 11%, which is double the national average. The IT workforce in these states has embraced digital platforms, making loan applications more efficient. In Chennai, over 70% of loan applications are submitted through mobile apps, reflecting the growing reliance on technology. This digital-first approach is driving the expansion of the auto loan market in southern India.

The eastern and northeastern regions of India remain less developed in terms of auto loan penetration but offer significant growth potential. Non-Banking Financial Companies (NBFCs) are using local languages to explain loan products and improve credit awareness among customers. In Assam, co-lending programs are helping streamline funding for commercial vehicles used in tea estate operations. As infrastructure improves, particularly highway connectivity, these regions are expected to see double-digit growth in commercial vehicle loans. This growth is likely to diversify the revenue streams for lenders in the auto loan market. The focus on these regions is gradually increasing as lenders recognize their untapped potential.

The auto loan market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe. This is complemented by country-specific insights for South Korea, China, Russia, France, Brazil, United Kingdom, Germany, and Japan, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The India auto loan market features moderate concentration: the top five lenders own slightly above half of the outstanding balances. HDFC Bank, ICICI Bank, and SBI Card leverage retail deposit bases to price aggressively, yet NBFCs like Bajaj Finance and Shriram Finance counter with risk-tiered products and localized servicing. OEM-captive arms, notably Maruti Suzuki Smart Finance and Hyundai Motor Finance, embed approval workflows inside dealer CRM platforms, lifting loan-attachment rates at the point of vehicle booking.

Recent industry developments sharpened these dynamics. The September 2025 festival-season blitz saw NBFCs pair zero-processing-fee offers with e-Mandate EMI debits, capturing incremental wallet share from banks that lacked similar agility. March 2025 co-lending clarifications prompted private banks to ramp allocations for NBFC-originated assets, mitigating portfolio-concentration risk. OEM captives seized March 2024 EV-partnership windows to underwrite battery-subscription pilots, converting subsidy support into competitive differentiation within the India auto loan market.

Technology investment defines future positioning. Leading banks deploy AI-driven fraud analytics trained on cross-bureau datasets, curbing first-payment default rates. NBFCs integrate telematics telemetry into dynamic pricing algorithms for commercial-vehicle fleets, rewarding high utilization with interest rebates. Fintech aggregators ingest GST e-invoice streams to offer pre-qualified credit lines, attacking friction in working-capital cycles. Collectively, these initiatives elevate customer choice and compress spread arbitrage, heralding an era where data proficiency and ecosystem partnerships supersede balance-sheet sheer size in steering the India auto loan market’s competitive calculus.

India Auto Loan Industry Leaders

State Bank of India

HDFC Bank

ICICI Bank

Axis Bank

Kotak Mahindra Bank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Multiple automotive manufacturers and financial institutions launched comprehensive festival-season financing campaigns, signaling strategic alignment with seasonal demand peaks and boosting disbursement velocity in the India auto loan market.

- August 2025: RBI rolled out enhanced digital-lending guidelines mandating granular fee transparency and cooling-off windows, reinforcing consumer protection and sustaining confidence in app-based auto lending

- July 2025: Leading NBFCs reported stabilization in vehicle-loan GNPA ratios, reflecting prudent underwriting post-pandemic and supporting healthier margin outlooks for the India auto loan market.

- March 2025: Reserve Bank of India issued updated co-lending guidelines stipulating minimum retention norms and blended-rate disclosure, catalyzing bank–NBFC deal flow and expanding credit supply.

India Auto Loan Market Report Scope

An automobile loan allows a user to borrow money from a lender and use it to purchase different forms of vehicles, which include Passenger and commercial vehicles. The loan is paid back to the issuer in the form of installments over a period of time with an agreed amount of interest payment.

India's auto loan market is segmented by vehicle type (passenger vehicles, commercial vehicles), by ownership (new vehicles, used vehicles), end user (individual, enterprise), and by loan provider (banks, OEMs, credit unions, other loan providers).

The report offers market sizes and forecasts for the Indian auto loan market in value (USD) for all the above segments.

| Non-Captive Banks |

| Non-Banking Financial Companies (NBFCs) |

| OEM-Captive Finance Arms |

| Other Providers (Co-lending & FinTech Platforms) |

| Passenger Vehicles |

| Commercial Vehicles |

| New Vehicles |

| Used Vehicles |

| Dealership Point-of-Sale |

| Online Direct Lending |

| Brokers & Marketplaces |

| By Loan Provider Type | Non-Captive Banks |

| Non-Banking Financial Companies (NBFCs) | |

| OEM-Captive Finance Arms | |

| Other Providers (Co-lending & FinTech Platforms) | |

| By Vehicle Type | Passenger Vehicles |

| Commercial Vehicles | |

| By Ownership | New Vehicles |

| Used Vehicles | |

| By Distribution Channel | Dealership Point-of-Sale |

| Online Direct Lending | |

| Brokers & Marketplaces |

Key Questions Answered in the Report

How large is the India auto loan market in 2026?

The India auto loan market size is USD 46.33 billion in 2026.

What growth rate is forecast for auto-loan credit through 2031?

Aggregate disbursements are projected to expand at a 6.62% CAGR between 2026 and 2031.

Which provider segment is growing fastest?

NBFCs lead with a 7.34% CAGR, driven by agile underwriting and tier-3/4 reach.

How quickly is used-vehicle financing expanding?

Used-vehicle loans are forecast to climb at an 8.39% CAGR during 2026-2031 as organized platforms professionalize the segment.

What role does the Account Aggregator framework play in auto lending?

It enables real-time data sharing, shortening approval times and improving risk segmentation across the India auto loan market.

Why are EV-finance products gaining traction?

OEM subsidy alignment and battery-subscription models cut upfront costs, encouraging more borrowers to choose electric vehicles.

Page last updated on: