Japan Private Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

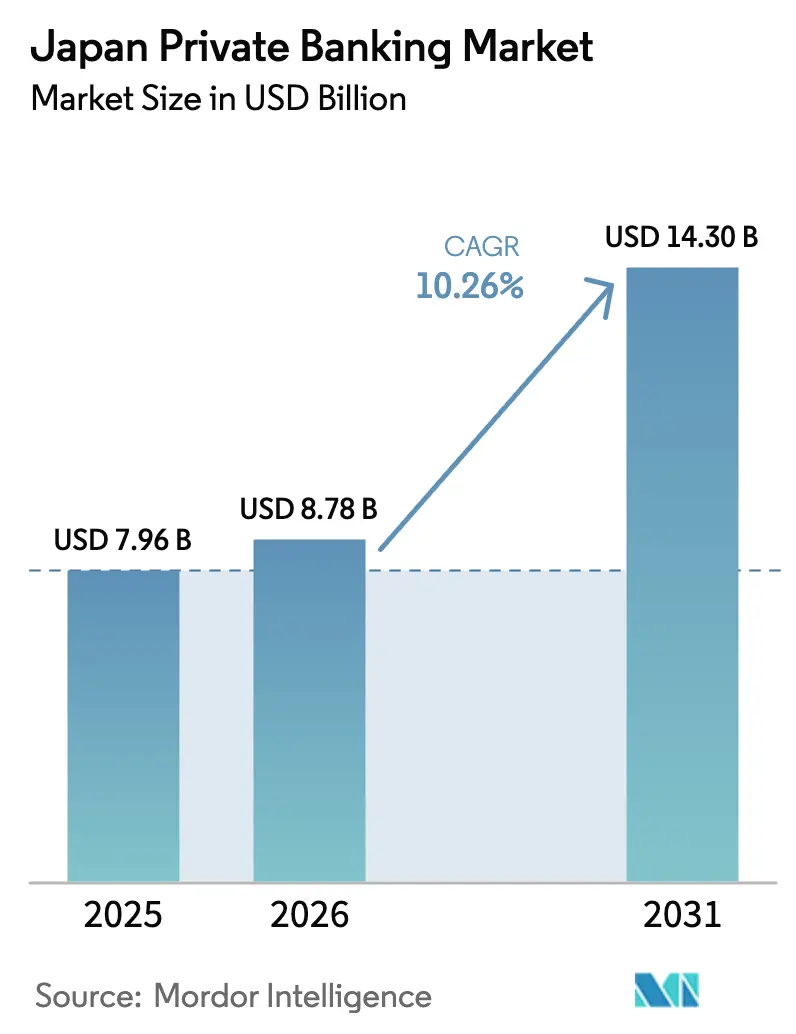

| Base Year Market Size (2025) | USD 7.96 Billion |

| Market Size (2026) | USD 8.78 Billion |

| Market Size (2031) | USD 14.3 Billion |

| Growth Rate (2026 - 2031) | 10.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Private Banking Market Analysis by Mordor Intelligence

The Japan private banking market size is expected to grow from USD 7.96 billion in 2025 to USD 8.78 billion in 2026 and is forecast to reach USD 14.3 billion by 2031 at 10.26% CAGR over 2026-2031. This expansion is fueled by the country’s unprecedented inter-generational wealth transfer, incremental deregulation of fiduciary services, intensifying digital innovation, and rising equity valuations that swell investable assets. Scale advantages held by the largest domestic trust banks, rising demand for holistic succession solutions, and the rapid emergence of API-enabled advisory platforms are amplifying competitive intensity. Simultaneously, foreign houses are enlarging on-shore desks to serve ultra-high-net-worth (UHNW) clients who seek cross-border diversification, while domestic banks deepen fee-based revenue streams to offset margin pressure. Structural opportunities remain concentrated in wealth succession, discretionary mandates, and digital advisory tools that broaden access to specialist products.

Key Report Takeaways

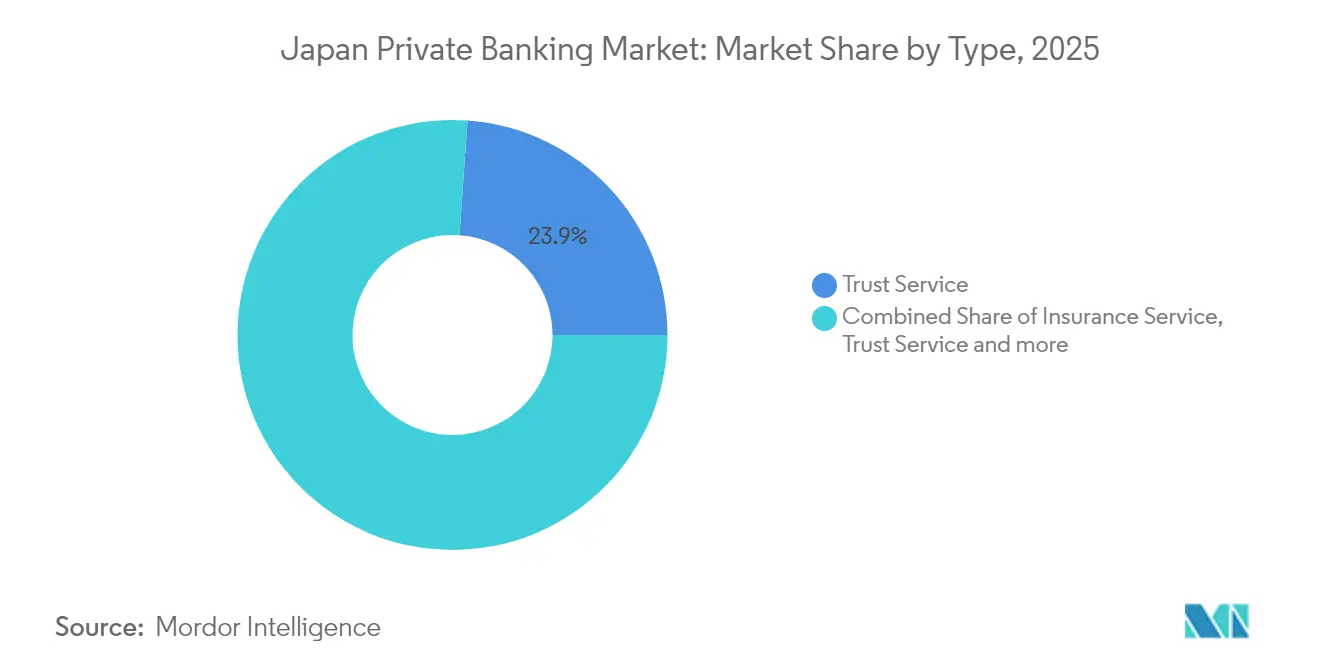

- By type, trust service held a 23.89% of the Japan private banking market share in 2025, while real estate consulting is forecast to advance at an 8.22% CAGR through 2031.

- By application, the personal segment controlled 30.45% of the Japan private banking market share in 2025 and is progressing at a 5.75% CAGR to 2031.

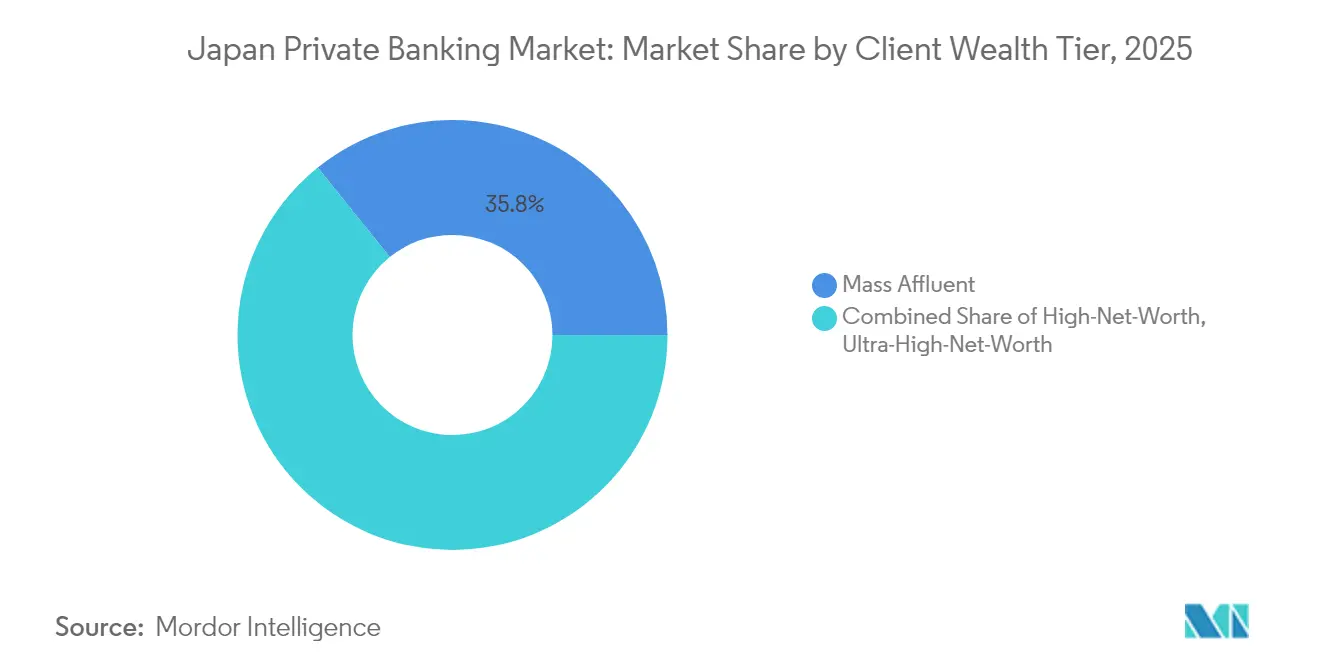

- By client wealth tier, mass affluent clients represented 35.78% of the Japan private banking market share in 2025, whereas high-net-worth clients are set to expand at a 6.95% CAGR.

- By geography, Kansai commanded 25.35% of the Japan private banking market share in 2025; Kanto is poised for a 6.05% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Private Banking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population driving inter-generational wealth transfer | +3.2% | National, concentrated in Kanto and Kansai | Long term (≥ 4 years) |

| Deregulation of fiduciary services under Japan's Stewardship Code | +2.1% | National, early adoption in Tokyo metropolitan | Medium term (2-4 years) |

| Digital transformation of wealth platforms (APIs, robo-advisory) | +1.8% | National, urban centers leading | Short term (≤ 2 years) |

| Rising stock-market valuation spurring affluent asset growth | +1.4% | National, Kanto region primary beneficiary | Medium term (2-4 years) |

| Corporate-governance reforms triggering executive liquidity events | +1.0% | National, Tokyo Stock Exchange listed companies | Medium term (2-4 years) |

| Tokyo metropolitan real-estate tokenization enabling new PB products | +0.8% | Kanto region, spillover to major urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population Wealth Transfer

Japan's demographic transition is creating the world's largest intergenerational wealth transfer event, with USD 2.21 trillion (Yen330 trillion) in assets expected to change hands by 2030 as baby boomers pass wealth to younger generations. This transfer represents approximately 60% of Japan's GDP and is concentrated among households with investable assets exceeding USD 670,000 (Yen100 million), creating a natural client base for private banking services. The complexity of Japan's inheritance tax system, which imposes rates up to 55% on estates exceeding USD 4.02 million (Yen600 million), is driving demand for sophisticated tax planning and trust structures. Recent legislative changes extending the inheritance tax clawback period from 3 to 7 years for overseas residents further amplifies the need for professional wealth structuring services. Cultural shifts are equally significant, with Nomura Research Institute data showing that 64.6% of business heirs have no intention of taking over family enterprises, necessitating alternative succession strategies through private banking channels.

Deregulation of Fiduciary Services Under Japan's Stewardship Code

The Financial Services Agency's 2024 amendments to Japan's Stewardship Code are dismantling traditional barriers between asset management and advisory services, enabling private banks to offer more integrated wealth solutions. These reforms allow institutions to provide discretionary investment management alongside traditional banking services, creating new revenue streams and improving client outcomes through holistic portfolio management[1]Source: Financial Services Agency, “Japan’s Stewardship Code and Fiduciary Services Reform,” fsa.go.jp. The deregulation particularly benefits trust banks like Sumitomo Mitsui Trust, which can now leverage their fiduciary expertise across broader client segments without regulatory constraints. Early adoption metrics show discretionary mandate growth of 23% year-over-year among major private banks in 2024, with average fee compression of 15 basis points as competition intensifies. This regulatory evolution aligns Japan with global best practices in wealth management while maintaining robust investor protection standards through enhanced disclosure requirements.

Digital Transformation of Wealth Platforms (APIs, Robo-Advisory)

Technology adoption in Japan's private banking sector accelerated dramatically following MUFG's USD 660 million acquisition of WealthNavi in 2024, validating the robo-advisory model for affluent Japanese investors. WealthNavi's flagship ROBOPRO Fund reached USD 670 million (Yen100 billion) in assets under management within 18 months of launch, delivering 39% returns and demonstrating strong client acceptance of algorithm-driven investment strategies[2]Source: WealthNavi, “ROBOPRO Fund Surpasses Yen100 Billion in AUM,” wealthnavi.com. This success is spurring broader digital transformation initiatives across the industry, with traditional institutions investing heavily in API-enabled platforms that integrate banking, investment, and advisory services. SBI Shinsei Bank's partnership with DeCurret and Partior to offer tokenized deposits represents another frontier, enabling real-time settlement and cross-border wealth transfers through blockchain infrastructure. The digital evolution is particularly resonating with younger affluent clients, who represent 34% of new private banking relationships in 2024 compared to 18% in 2020, according to internal metrics from major institutions.

Rising Stock-Market Valuation Spurring Affluent Asset Growth

Japan's equity markets reached multi-decade highs in 2024, with the Nikkei 225 surpassing 40,000 points and creating substantial wealth effects among affluent investors. This rally increased investable assets among high-net-worth individuals by an estimated 28% year-over-year, expanding the addressable market for private banking services. Corporate governance reforms mandating improved shareholder returns are sustaining this trend, with Tokyo Stock Exchange companies increasing dividend payouts by 15% annually since 2022. The wealth creation is particularly concentrated among executives and entrepreneurs holding equity stakes in listed companies, driving demand for liquidity management and tax-efficient monetization strategies. Private banks are responding with specialized equity collar products and structured derivatives that allow clients to hedge concentrated positions while maintaining upside participation, generating fee income of 75-125 basis points annually on structured exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently low interest-rate environment compressing NIMs | -1.9% | National, affecting all deposit-taking institutions | Long term (≥ 4 years) |

| Stricter Basel III capital requirements limiting risk appetite | -1.2% | National, major banks primarily affected | Medium term (2-4 years) |

| Intensifying competition from foreign private banks | -0.8% | Kanto and Kansai regions, UHNW segment focus | Short term (≤ 2 years) |

| Cultural hesitancy among SMEs to outsource succession planning | -0.6% | National, rural and traditional industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Interest-Rate Environment

The Bank of Japan’s March 2024 policy lift to 0.1% concluded an era of negative rates, yet margins remain historically compressed[3]Source: Bank of Japan, “Statement on Monetary Policy,” boj.or.jp. This environment particularly challenges smaller regional private banks that lack scale in advisory services, with average NIMs declining to 0.85% in 2024 from 1.2% in 2019 across the sector. The constraint is driving strategic pivots toward wealth management fees, with leading institutions targeting fee income ratios of 35-40% by 2030 compared to the current 25% average. Regulatory compliance factors under the Financial Instruments and Exchange Act require enhanced disclosure of fee structures, creating transparency that benefits clients but pressures institutional margins during the transition period.

Basel III Capital Requirements

Enhanced Basel III capital requirements, fully implemented in Japan by 2024, are constraining private banks' ability to extend credit facilities and structured products to wealthy clients. The Total Loss-Absorbing Capacity (TLAC) framework requires systemically important banks to maintain capital ratios of 18% or higher, reducing available capital for discretionary lending activities. This regulatory pressure particularly affects credit-intensive private banking products such as securities-backed lending and real estate financing, where risk-weighted asset calculations limit portfolio growth. Major institutions are responding by partnering with non-bank lenders and insurance companies to provide credit solutions while maintaining regulatory compliance, though these arrangements typically reduce fee capture by 25-35% compared to direct lending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Trust Services Sustain Leadership Amid Real-Estate Innovation

Trust Service held 23.89% of the Japan private banking market in 2025, underpinned by the nation’s complex inheritance taxes and a legal culture that favors trust structures for asset continuity. Integration of portfolio management with trust administration has improved relationship depth and share-of-wallet among multi-generational families. Real Estate Consulting, while accounting for a smaller base, is projected to register the fastest 8.22% CAGR as tokenization of metropolitan properties and REIT-linked offerings democratize access to prime assets. The Japan private banking market size for real-estate-focused mandates is accelerating as blockchain platforms open fractional ownership opportunities to mass affluent investors. Insurance Service, backed by bancassurance tie-ups, commands 17.62% revenue through capital-protected wrappers popular among risk-averse seniors. Tax Consulting expands at 8.05% CAGR, driven by cross-border financial complexity as affluent households diversify overseas portfolios.

Digitalization permeates each service line. API bridges now feed trust-account data into portfolio dashboards, giving clients a single view of assets. High-volume advisory processes are automated, releasing capacity for bankers to focus on complex structures. The regulatory backdrop remains supportive: the Financial Services Agency streamlines trust-bank licensing, while property-token guidelines released in 2024 clarify custodial responsibilities. As a result, the Japan private banking market continues to migrate from transactional product silos toward holistic, digitally enabled service bundles.

By Application: Personal Mandates Preserve Dominance

Personal mandates represented 30.45% of Japan private banking market share in 2025, manifesting Japan’s relationship-centric culture in which families prefer bespoke advisory over institutional pooling. Growth at 5.75% CAGR is driven by rising demand for family office-like services portfolio aggregation, philanthropy planning, and next-generation financial education. Enterprise mandates, while smaller at roughly 7.85% share, post a quicker 6.05% CAGR as listed companies outsource executive compensation management and employee stock ownership program (ESOP) administration. Digital account-opening reforms enacted in 2024 simplify enterprise onboarding, fostering new corporate-linked wealth flows. Meanwhile, hybrid models emerge employee-ownership platforms that facilitate leveraged buyouts allow departing founders to exit while employees accumulate wealth, widening the advisory remit.

Customization remains the competitive battleground in personal mandates. Banks deploy AI-assisted goals-based planning to translate life events education, retirement, philanthropy into portfolio glide paths. For the enterprise segment, regulatory filings such as insider-trading reports and tax withholding obligations create compliance complexity that private banks monetize through specialized administrative services. Ultimately, the Japan private banking industry converges around integrated offerings that bridge personal and corporate wealth, blurring historic segmentation lines yet preserving individualized service.

By Client Wealth Tier: Mass Affluent Scale Meets High-Net-Worth Velocity

Mass Affluent households accounted for 35.78% of the Japan private banking market in 2025. Standardized discretionary portfolios and robo-advisory tools keep servicing costs low, enabling scalability and stable recurring revenue. Conversely, High-Net-Worth clients expand at a faster 6.95% CAGR as equity-market liquidity events and business successions swell their investable assets. The Japan private banking market size for UHNW services remains smaller but revenue-rich, driven by complex private-equity access, co-investment opportunities, and bespoke credit. Compliance frameworks under the Anti-Money-Laundering Act mandate enhanced due diligence for UHNW accounts, reinforcing the need for robust KYC systems that large providers already possess.

Banks adopt tier-differentiated engagement: digital-first workflows serve mass affluent segments, while dedicated relationship managers handle top-tier clients whose multidimensional needs span philanthropy, art finance, and global estate planning. Cross-selling deepens life policies backed by trust wrappers protect overseas property, and securities-backed loans finance tax liabilities without liquidating assets. Overall, wealth-tier segmentation evolves toward experience levels rather than asset thresholds, with digital literacy now a key stratifier.

Geography Analysis

Kansai maintained a 25.35% share of the Japan private banking market in 2025, anchored by longstanding conglomerates and affluent manufacturing dynasties in Osaka and Kobe. Trust-bank branches historically embedded in keiretsu supply chains continue to channel corporate founder wealth into private-banking divisions. Growth, however, is shifting eastward. Kanto is expected to secure a 6.05% CAGR through 2031 on the back of Tokyo’s status as Asia’s second-largest financial hub and its concentration of technology IPOs. Unicorn founder liquidity events and stock-option exercises translate into incremental private-bank relationships, especially among younger clients who favor API-enabled advisory models.

Chubu, supported by Nagoya’s automotive ecosystem, contributes steady 13.85% revenue, with exporters turning to hedging and offshore diversification amid currency volatility. Northern regions Hokkaido & Tohoku benefit from digital onboarding that eliminates branch dependency; remote clients can now execute sophisticated trust deeds via e-signatures validated under the 2024 Digital Procedures Act. Chugoku & Shikoku retain niche high-margin agribusiness succession mandates, yet market depth is thin. Kyushu & Okinawa posts the fastest 7.72% CAGR thanks to government incentives for semiconductor fabs around Kumamoto and Fukuoka’s startup scene that spawns new wealth. Regional banks collaborate with megabanks to white-label private-bank platforms, marrying local relationship capital with product scale.

Competitive Landscape

The Japan private banking market is characterized by an oligopolistic structure, with the top five firms dominating overall revenues. Mitsubishi UFJ Morgan Stanley Private Banking holds the leading position, benefiting from its dual-brand strategy that combines international product access with strong domestic deposit funding. Sumitomo Mitsui Trust comes next, capitalizing on its extensive trust operations and long-standing reputation for fiduciary expertise. Mizuho Private Wealth follows with a comprehensive service model that integrates investment banking and wealth management. Beneath these megabanks, regional firms like Nomura and Daiwa are crafting multi-family office models, while international banks such as UBS, HSBC, and Credit Suisse expand their Tokyo operations to serve ultra-wealthy clients seeking global diversification.

Strategic differentiation in Japan’s private banking landscape increasingly hinges on digital innovation and intergenerational wealth planning. MUFG’s acquisition of WealthNavi represents a deliberate choice to accelerate digital capabilities through acquisition rather than internal development. Sumitomo Mitsui Trust is piloting AI-powered tools to simulate estate tax scenarios, deepening relationships with clients across generations. UBS, meanwhile, takes advantage of its global open-architecture platform to distribute alternative investments not easily accessible through domestic providers. Domestic institutions are also expanding ESG-focused portfolios and philanthropic advisory services to align with the values of younger heirs, aiming to retain family wealth across generations.

While foreign banks continue to grow their presence, competition remains focused on the ultra-high-net-worth segment, where cross-border needs are more pronounced. In the broader mass affluent space, cultural familiarity and language fluency still give local banks a competitive edge. However, the rise of open-banking APIs is beginning to break down traditional distribution channels, empowering fintech platforms to compete on pricing transparency and accessibility. Over the coming years, operational scale, regulatory readiness, and data-driven client engagement will separate leaders from laggards. Firms that fail to evolve risk declining profit margins and eventual client attrition in an increasingly competitive landscape.

Japan Private Banking Industry Leaders

Mitsubishi UFJ Morgan Stanley PB

Sumitomo Mitsui Trust Bank

Mizuho Private Wealth Management

Nomura Holdings

Daiwa Securities Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Prudential and Dai-ichi Life Insurance announced a strategic partnership to develop integrated wealth management and insurance solutions for high-net-worth clients, combining Prudential's international expertise with Dai-ichi's domestic market knowledge to create comprehensive financial planning services.

- February 2025: State Street Corporation completed its acquisition of Mizuho Bank's global custody business for an undisclosed amount, taking over USD 580 billion in assets under custody and strengthening foreign institutional access to Japanese private banking clients.

- July 2025: Nikko Asset Management, rebranding as Amova, established a strategic partnership with Singapore-based Chocolate Finance to develop AI-powered wealth management solutions targeting affluent millennials across Asia Pacific markets.

- September 2025: SBI Shinsei Bank launched Japan's first tokenized deposit service in partnership with DeCurret and Partior, enabling real-time cross-border settlements for private banking clients with international investment portfolios.

Japan Private Banking Market Report Scope

Private banking is defined as the financial activity orientated to wealthy customers to manage their wealth in the long-term period according to the objectives and needs of the clients. Private Banking is a team of professionals that deliver private banking and wealth management services to high net-worth individuals and families, from banking and cash management to lending, investment strategies, and trust and wealth advisory services. Private banking services have been targeted by many large banks because of the growing wealth of individuals and the relative profitability of private banking businesses. The report provides more details about industry trends and the latest updates. Private Banking Market in Japan is segmented by type (Asset Management Service, Insurance Service, Trust Service, Tax Consulting, and Real Estate Consulting) and by application (Personal and Enterprise). The report offers market size and forecasts for the private banking market in Japan in value (USD Million) for all the above segments.

| Asset Management Service |

| Insurance Service |

| Trust Service |

| Tax Consulting |

| Real Estate Consulting |

| Personal |

| Enterprise |

| Mass Affluent |

| High-Net-Worth |

| Ultra-High-Net-Worth |

| Kanto |

| Kansai |

| Chubu |

| Hokkaido & Tohoku |

| Chugoku & Shikoku |

| Kyushu & Okinawa |

| By Type | Asset Management Service |

| Insurance Service | |

| Trust Service | |

| Tax Consulting | |

| Real Estate Consulting | |

| By Application | Personal |

| Enterprise | |

| By Client Wealth Tier | Mass Affluent |

| High-Net-Worth | |

| Ultra-High-Net-Worth | |

| By Region | Kanto |

| Kansai | |

| Chubu | |

| Hokkaido & Tohoku | |

| Chugoku & Shikoku | |

| Kyushu & Okinawa |

Key Questions Answered in the Report

How large is Japan’s private banking market in 2026?

The Japan private banking market size stands at USD 8.78 billion in 2026 and is forecast to grow at 10.26% CAGR to USD 14.3 billion by 2031.

Which service type currently leads private banking revenue?

Trust Service leads with 23.89% share in 2025, sustained by demand for inheritance and fiduciary structures.

Which client wealth tier is expanding fastest?

High-Net-Worth clients show the highest growth, projected at a 6.95% CAGR through 2031 as equity liquidity events rise.

Which region is expected to deliver the strongest growth?

The Kanto region is projected to record a 6.05% CAGR thanks to Tokyo’s tech-driven wealth creation and financial-services density.

How are banks countering low interest margins?

Institutions pivot toward fee-based income discretionary mandates, real-estate advisory, and digital asset services to offset compressed net interest margins.

What digital trends are shaping private banking in Japan?

API-enabled aggregation, robo-advisory portfolios, and tokenized deposits are redefining client experience and broadening access to sophisticated products.

Page last updated on: