India Home Loan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

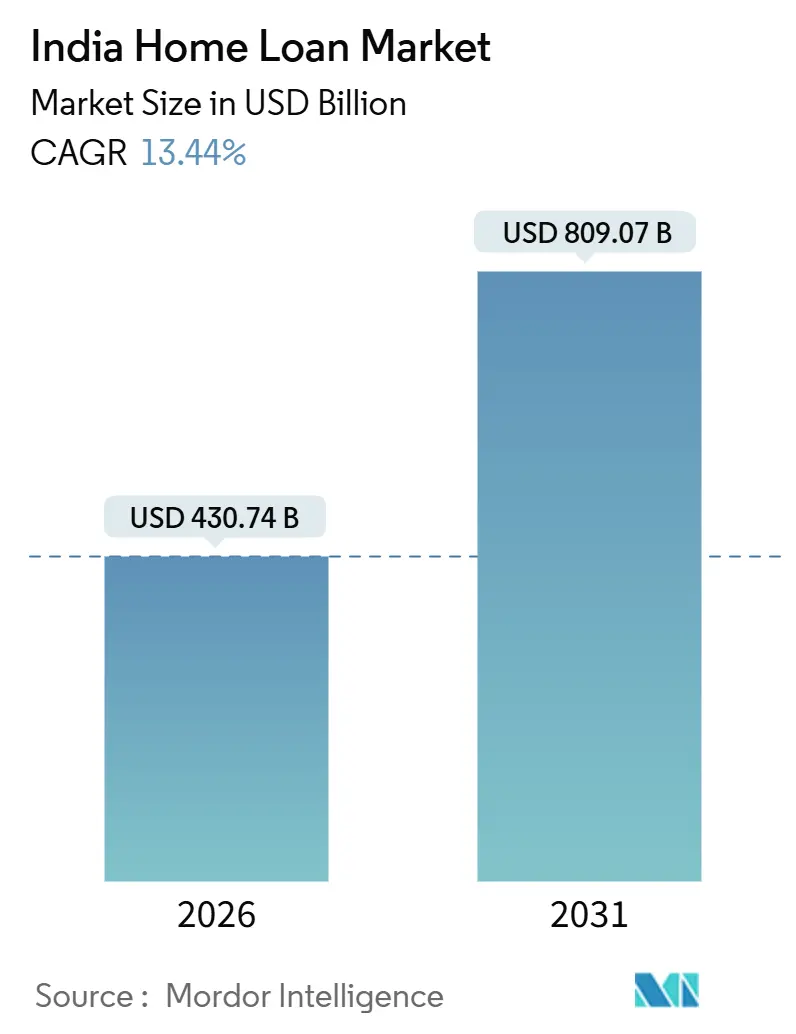

| Market Size (2026) | USD 430.74 Billion |

| Market Size (2031) | USD 809.07 Billion |

| Growth Rate (2026 - 2031) | 13.44% CAGR |

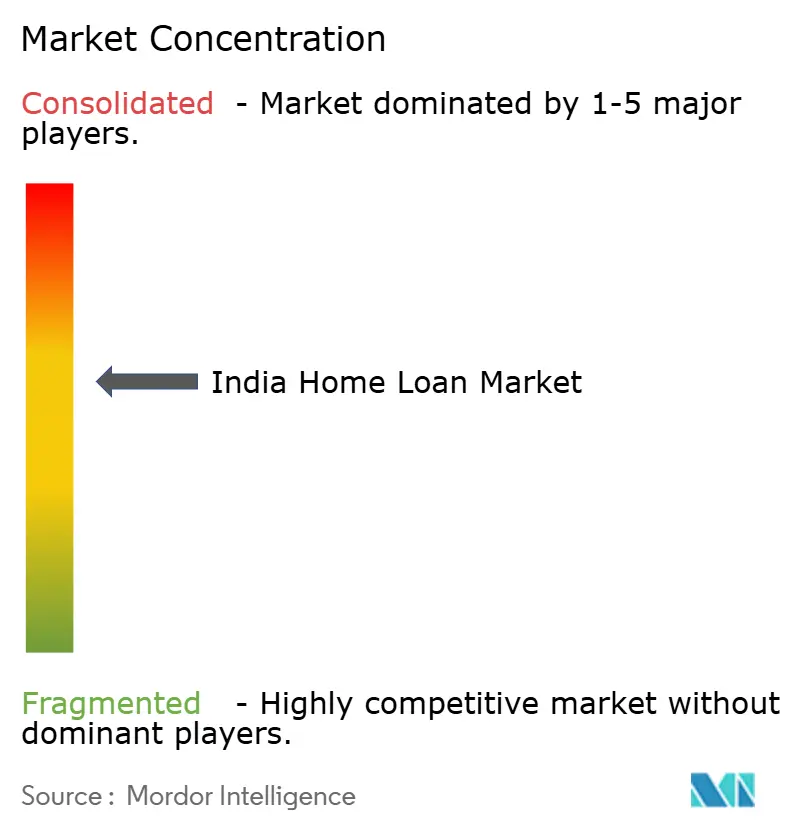

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Home Loan Market Analysis by Mordor Intelligence

The India home loan market size stood at USD 430.74 billion in 2026 and is projected to reach USD 809.07 billion by 2031 at a 13.44% CAGR. The India home loan market is riding on rapid urbanization and housing formation that now extends well beyond the metros into Tier-2 and Tier-3 cities as employment centers diffuse and transport, water, and sanitation networks expand. Monetary easing through 2025 restored affordability for prime borrowers as the policy repo fell to 5.25% by December 2025, and muted retail inflation created a supportive credit window after a prolonged tight cycle[1]Source: Reserve Bank of India, “Monetary Policy Statements and Press Releases,” Reserve Bank of India, rbi.org.in.. Competitive intensity in the India home loan market has escalated as public-sector banks transmit rate cuts quickly through external benchmark linkages while private banks and NBFCs push digital onboarding and underwriting speed. The India home loan market is consolidating technology gains from embedded-finance flows and algorithmic credit assessment, which pull new-to-credit and self-employed borrowers into formal mortgages.

Key Report Takeaways

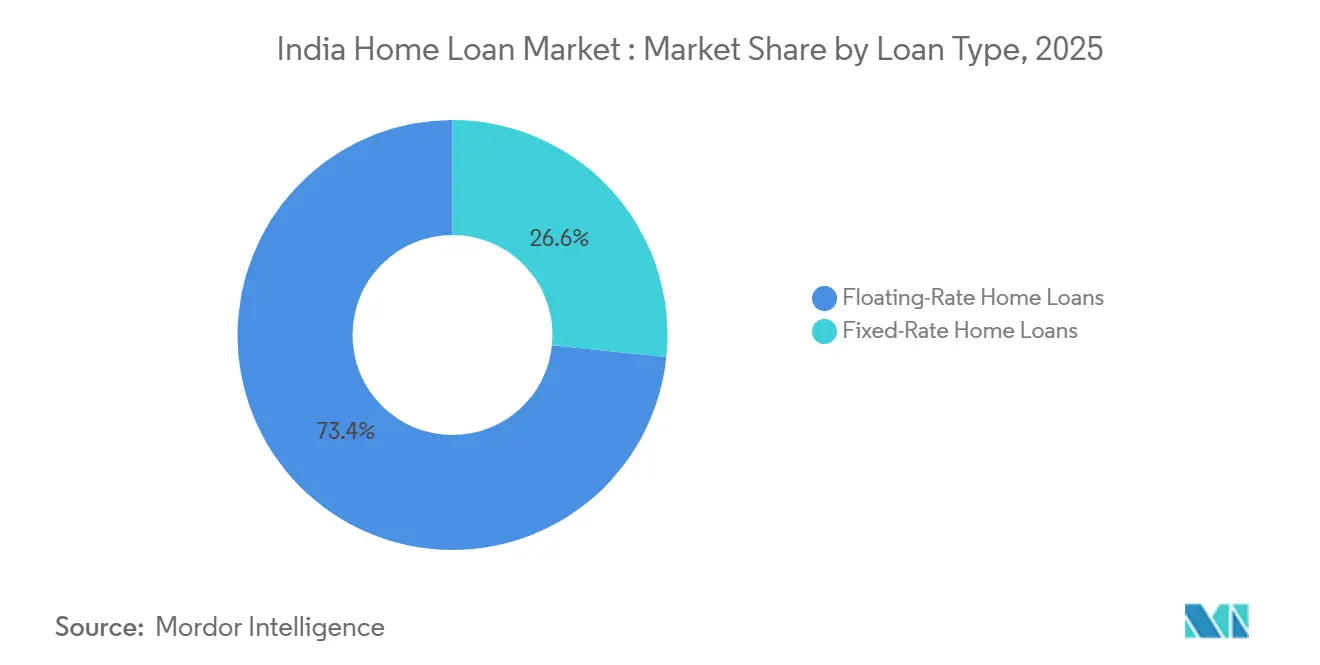

- By loan type, floating-rate loans led with 73.37% of the India home loan market share in 2025, while fixed-rate products are projected to grow the fastest at 17.24% CAGR through 2031.

- By provider type, public-sector banks held 47.33% of the India home loan market share in 2025, while NBFCs recorded the highest growth trajectory at 18.38% through 2031.

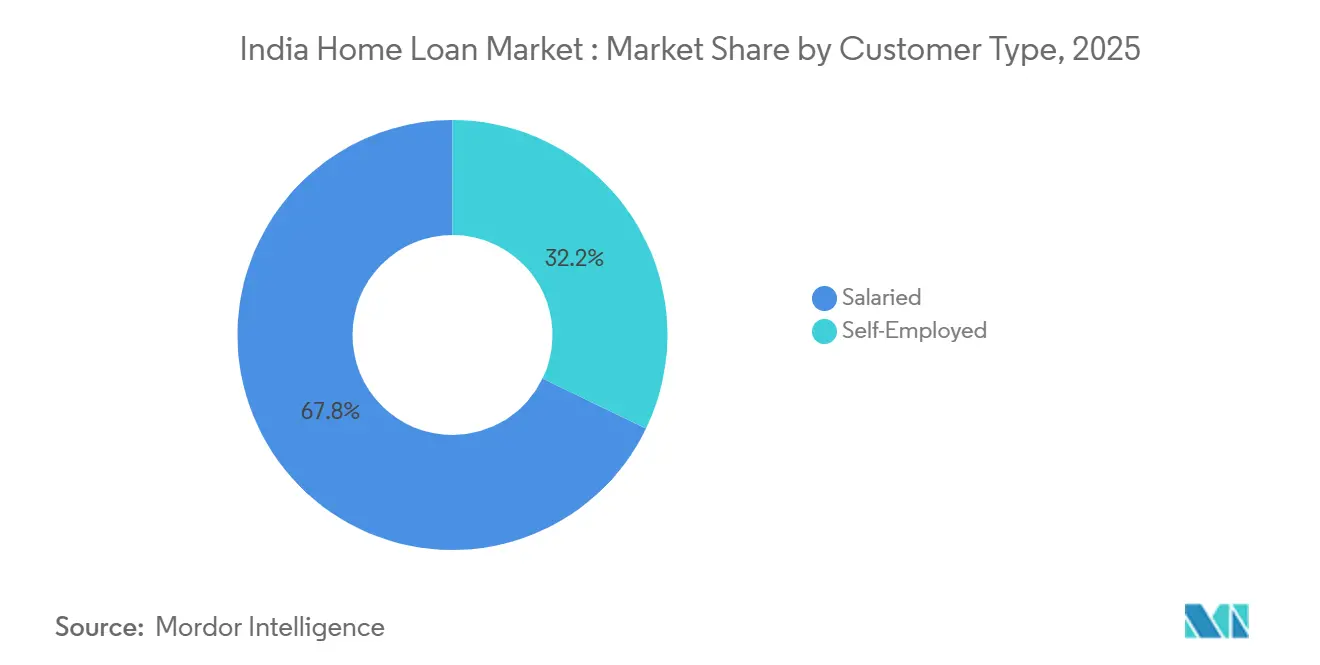

- By customer type, salaried borrowers accounted for 67.84% of the India home loan market share in 2025, while self-employed borrowers are projected to grow at 17.38% through 2031.

- By interest-subsidy participation, non-subsidized loans held 71.37% of the India home loan market share in 2025, while PMAY-CLSS beneficiaries are set to expand at 16.44% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India contributes to a system defined not by any single country or region but by the interaction of many. The global home loan market data by Mordor Intelligence represents that combined structure.

India Home Loan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated urban migration into Tier-2 & Tier-3 cities | +2.7% | Pan-India, with concentration in UP, Bihar, MP, Rajasthan | Medium term (2-4 years) |

| Surge in women-centric tax incentives & preferential rates | +0.9% | Maharashtra, Delhi, Haryana, UP | Short term (≤ 2 years) |

| Increasing formal-sector employment & payroll digitization | +3.1% | Urban hubs such as Bengaluru, Hyderabad, Pune, NCR | Long term (≥ 4 years) |

| PMAY subsidies extended through 2027 | +3.5% | All statutory towns with focus on EWS/LIG/MIG | Short to medium term (≤ 3 years) |

| Embedded-finance distribution via prop-tech platforms | +1.4% | Metro and Tier-1 with spillover to Tier-2 | Medium term (2-4 years) |

| Satellite-based property-valuation data reducing collateral risk | +0.8% | Pan-India urban clusters with NBFC pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Urban Migration Into Tier-2 & Tier-3 Cities

Migration is building a durable housing pipeline outside the big metros as smaller cities benefit from lower land prices and rising employment nodes. The India home loan market is increasingly shaped by mid-sized cities where capex under the Smart Cities Mission and AMRUT 2.0 is improving civic services and supporting new home formation at accessible price points. The India home loan market is seeing faster traction in affordable ticket sizes, sustained by digital onboarding that streamlines KYC and income checks even for self-employed borrowers with limited documentation. Lenders and platforms using UPI transaction histories and bank statement aggregation reduce friction for entrepreneurial households in Tier-3 clusters, thereby lifting conversion rates for low and mid-ticket mortgages.

PMAY Subsidies Extended Through 2027

Policy support through PMAY-Urban 2.0 is widening the affordable mortgage funnel as states implement reforms on stamp duty, FAR, and approvals to accelerate supply. By December 2025, sanction traction under the new guidelines had taken hold, and states were aligning with conditional reforms designed to lower build costs and increase unit throughput for EWS, LIG, and MIG segments[2]Source: Pradhan Mantri Awas Yojana Urban, “PMAY-U 2.0 Operational Guidelines,” Ministry of Housing and Urban Affairs, pmay-urban.gov.in. The India home loan market is benefiting from a streamlined path-to-credit as NHB expanded the lender network and enabled quicker subsidy pass-through to borrowers via primary lending partners. Spillover from PMAY-Gramin adds a pipeline effect when migrants transition to urban housing, reinforcing entry-level demand in peripheral city markets.

Increasing Formal-Sector Employment & Payroll Digitization

Formal job creation and income verification infrastructure are lifting mortgage eligibility at scale, especially for salaried workers in urban centers. EPFO net additions in FY25, along with payroll digitization and e-KYC rails, have supported faster credit decisioning for salaried cohorts who typically secure lower spreads relative to self-employed peers. Average monthly earnings for regular wage workers were higher by Q2 FY25, which improved debt servicing capacity and acceptance rates for prime profiles. The home loan market in India also benefits from an expanding services base in IT, finance, and professional services hubs where steady payrolls anchor stable repayment behavior in mortgage books. Parallel advances in underwriting for self-employed borrowers, including models that rely on cash-flow proxies and digital trails, are closing the rate gap and unlocking new originations.

Embedded-Finance Distribution Via Prop-Tech Platforms

Property portals have integrated financing journeys that let buyers check eligibility, compare rates, and receive pre-approvals within a single interface. The India housing loan market is seeing meaningful origination from embedded channels as multi-lender marketplaces place offers from banks and housing finance companies at the point of property discovery. Prop-tech players apply automated valuation tools and bank-grade credit checks to shorten time-to-approval and to route borrowers to the most suitable lender products. Regulators have bolstered safe adoption by requiring that digital lending apps work only with regulated entities and by advancing interoperability for credit portability. These steps improve transparency, contain misconduct risk, and anchor customer trust, which supports sustained digital-led growth in the India home loan market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continued policy-rate volatility | -1.8% | Pan-India with transmission lag in MCLR-linked portfolios | Short term (≤ 2 years) |

| Rising developer insolvencies delaying possession | -2.1% | NCR, Mumbai Metropolitan Region, Bengaluru, Hyderabad | Medium term (2-4 years) |

| Unaddressed land-title ambiguities in peri-urban India | -0.9% | Peri-urban belts of Tier-2/3 cities with fragmented holdings | Long term (≥ 4 years) |

| Climate-risk exclusions for flood-prone districts | -0.6% | Coastal and riverine belts in Karnataka, Kerala, Bengal, Assam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continued Policy-Rate Volatility

The rate cycle delivered relief in 2025 as the policy repo reached 5.25% by December, yet the near-term outlook features two-sided risks that can unsettle borrower expectations. The India home loan market faces uneven pass-through across legacy books since MCLR-linked loans adjust with a lag compared to repo-linked products that reprice faster. Refinancing has risen as borrowers shift to external benchmarks for quicker benefits, which creates churn and margin pressure across lenders. Fixed-rate products offer EMI certainty but have carried a premium, which moderates uptake when the forward rate path is unclear for households with tight budgets. Lender repricing and spread resets continue to evolve with regulatory guidance, which helps improve transparency for the India home loan market while transmission gaps take time to close.

Rising Developer Insolvencies Delaying Possession

A high share of real estate cases under insolvency remains unresolved beyond statutory timelines, which extends the wait for possession and raises borrower stress. Homebuyers can face simultaneous rent and EMI, and lenders must provision for stress where project execution is uncertain. Judicial bodies have highlighted severe delays in marquee cases, and courts have intervened to safeguard assets while resolution proceeds. Process improvements now require early reporting on development rights and involve regulators more closely in committee proceedings, which improves oversight of project viability. Escrow norms under the Real Estate Act are designed to reduce fund diversion and protect project completion, though enforcement strength varies across legacy and state contexts, which the India home loan market must factor into underwriting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Type: Fixed-Rate Products Gain Momentum

Floating-rate products dominated with 73.37% of the India home loan market share in 2025 as borrowers favored transparent and quick repo transmission. Fixed-rate loans are the fastest-growing option at 17.24% projected CAGR through 2031 as many households seek near-term EMI certainty after wide rate swings. The India home loan market has broadened hybrid variants that hold the rate for initial years and then reset to a floating benchmark to blend predictability and potential future savings. Pricing spreads on fixed loans remain higher to reflect duration and repricing risk, yet demand persists among profiles with rigid cash flow budgets. Bajaj Housing Finance has offered a 3-year fixed product that targets this need for stability at the start of the tenure.

Fixed-rate offers typically convert to floating after a fixed window, which makes clear reset mechanics critical to customer outcomes. The home loan market in India is also seeing improved disclosures on rate resets and spread revisions, which reduces customer confusion at the switch point. The fixed segment appeals to salaried borrowers who anchor household budgets on predictable monthly outflows across long amortization periods. Floating-rate loans remain a strong default choice for borrowers who expect benign policy rates or who want faster pass-through of any easing. Together these choices allow households to align mortgage risk with their income visibility, which supports a more resilient India housing loan market through the cycle.

By Provider Type: NBFCs capture self-employed share as PSBs dominate salaried flow

Public-sector banks retained 47.33% in 2025, which reflects rapid transmission of repo-linked pricing and the ability to serve salaried demand at scale. The India home loan market has also seen strong growth from NBFCs that specialize in self-employed underwriting and flexible documentation with a corresponding rate premium. SBI guided its home-loan book to cross INR 10 trillion (USD 120.5 billion) in FY26, with strong asset quality metrics that support continued share defense. Private banks remain active in prime and near-prime segments using fast digital onboarding and decisioning to speed up disbursals. The provider landscape therefore anchors a balanced flow of salaried and self-employed demand within the India home loan market.

NBFCs are positioned to outgrow the system where underwriting must interpret irregular incomes through transaction analytics and field assessment. Specialized HFCs have deepened their presence in sub-INR 25 lakh tickets, which align well with the entry-level buyer in smaller cities and peri-urban belts. The India home loan market benefits from liquidity initiatives such as NHB refinance and securitization conduits that lower the funding cost of compliant pools. Governance and disclosure norms under RERA improve comparability across lenders, though capital cost structures differ across bank and NBFC models. This diversity of provider strengths supports better segment fit for borrowers, which is positive for long-run penetration in the India home loan market.

By Customer Type: Self-employed CAGR triples salaried growth on fintech-enabled underwriting

Salaried borrowers accounted for 67.84% of accounts in 2025 as automated income verification and e-KYC rails compress approval time for mainstream profiles. The India home loan market size allocation to salaried borrowers remains large because payroll records and employer documentation reduce perceived risk in underwriting. Self-employed borrowers are projected to grow at 17.38% through 2031, which is roughly triple the pace of salaried growth given advances in data-led credit modeling. EPFO additions and higher average monthly earnings of INR 21,103 (USD 254.3) in Q2 FY25 improved affordability headroom for many salaried families. The India home loan market is also seeing self-employed rate differentials narrow at some lenders that use cash-flow proxies and device analytics to underwrite volatile income streams.

Platforms and lenders are offering payment flexibility that better matches the income cadence of freelancers and micro-entrepreneurs. This shift encourages formalization and moves borrowers from informal credit toward secure, amortizing products within the India home loan market. NBFCs with strong field verification and local sourcing capabilities are particularly effective in this segment. Improved documentation through GST data and bank statement aggregation has reduced rejection rates for viable self-employed profiles. These improvements are expanding inclusion and raising the addressable base without compromising on compliance in the India home loan market.

By Interest-Subsidy Scheme Participation: PMAY 2.0 relaunch propels subsidized-loan CAGR to 16.44%

Non-subsidized loans held 71.37% in 2025 while PMAY-CLSS beneficiaries accounted for 28.63% of accounts and are projected to expand at 16.44% through 2031. The home loan market size in India linked to eligible subsidy cohorts benefits from the INR 2.50 trillion (USD 30.1 billion) PMAY-Urban 2.0 allocation and the interest subsidy design that reduces early-tenor burden for lower and middle-income families. NHB signed MOUs with a large base of lenders and disbursed subsidy in the scheme’s early months after relaunch, signaling execution momentum. States have adopted stamp-duty and FAR reforms to align incentives, which lowers project break-even thresholds and creates more compliant, mortgageable supply. PMAY-Gramin assistance of up to INR 2.2 lakh (USD 2.7 thousand) per unit in select states supports rural housing that can feed eventual urban migration and formal mortgage demand.

The India home loan market sees concentrated PMAY uptake in MIG-I and EWS/LIG bands where the EMI relief is most meaningful to household budgets. Ticket sizes in these cohorts tend to be modest and align with the availability of units in peripheral micro-markets where land and infrastructure costs are lower. Stronger tracking through geo-tagging and digital monitoring increases subsidy integrity and reduces leakage. Continued budgetary support and capacity building in the primary lending partner network remain important to sustain the projected growth path. These elements together underpin a durable affordability channel within the India home loan market.

Geography Analysis

Public-sector banks have a strong footprint in the Hindi-speaking North with significant branch density in Uttar Pradesh, Bihar, Madhya Pradesh, and Rajasthan, which aligns with the current wave of Tier-2 and Tier-3 urbanization. Uttar Pradesh moved to resolve legacy title bottlenecks through the regularization of millions of parcels, which broadens mortgage eligibility for previously excluded households. PMAY-Urban sanctions continue to gather pace in northern states, supporting new supply in statutory towns and aiding first-time ownership. The India home loan market is therefore seeing a more even geographic contribution from growth corridors beyond the top metros as programs and title reforms expand the pool of bankable borrowers.

Maharashtra, Karnataka, and Tamil Nadu sustain large pools of salaried applicants in major cities with technology, manufacturing, and service sector anchors. The India home loan market benefits from stable payroll formation in Bengaluru, Hyderabad, Pune, and Mumbai, which helps keep delinquencies low as labor markets remain robust. Stamp-duty and title regularization in peri-urban belts improved transaction confidence and unlocked latent supply in these states. In Mumbai, housing registrations reached a new high in 2025 with greater activity in the lower ticket bands that suit first-time buyers, even as a small share of luxury transactions also grew. The India home loan market continues to integrate satellite-based valuation and remote diligence in these dense urban clusters to accelerate underwriting without compromising risk controls.

Coastal and flood-prone states such as Karnataka, Kerala, and Assam reflect higher climate risk in underwriting through stricter property and insurance checks. Lenders calibrate loan-to-value caps and documentation rigor for climate-exposed districts to protect collateral quality in the India home loan market. Title digitization under programs like SVAMITVA and urban mapping projects like NAKSHA help lenders verify assets and limit delays during diligence. Regional policy forums and lender conclaves have focused on North-East inclusion and infrastructure-led connectivity to extend formal housing finance deeper into under-penetrated areas. These efforts help align risk, access, and infrastructure in a way that supports long-term regional diversification in the India home loan market.

The home loan market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for China, United States, and Brazil, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The India home loan market shows moderate concentration, with large public and private banks and established housing finance companies together holding a majority of outstanding mortgages. SBI remains the system leader with a home-loan portfolio guided to exceed INR 10 trillion (USD 120.5 billion) in FY26 and asset quality that supports continued scale[3]Source: State Bank of India, “Home Loan Portfolio and Guidance,” State Bank of India, sbi.co.in. The combined HDFC Bank franchise, following its merger with HDFC Ltd, broadened distribution and cross-sell potential across a large retail customer base. The India home loan market is also competitive at the point of property discovery, with embedded-finance partners steering borrowers to multi-lender marketplaces for pre-approval and rate comparison. Lenders continue to differentiate on speed, simplicity, and digital transparency to contest market share in priority micro-markets.

Technology-driven underwriting has moved from pilots to scaled adoption across the value chain. Automated valuation models use satellite and aerial imagery to accelerate collateral checks and reduce fraud exposure, which helps lower turnaround time in busy urban markets. The India home loan market also benefits from securitization and refinance initiatives that deepen liquidity for originators who maintain strong servicing and compliance. Newer players have launched AI-enabled origination assistants and expanded into under-served segments with tailored documentation norms. Together these investments in data, mapping, and process automation raise consistency in underwriting outcomes across borrower profiles.

Strategic moves continue across incumbents and challengers. Bajaj Housing Finance’s 2024 public listing raised USD 781 million and showcased investor appetite for well-capitalized originators with digital delivery strengths[4]Source: Bajaj Housing Finance, “Fixed Rate Home Loan Product Features,” Bajaj Housing Finance, bajajhousingfinance.in. The RMBS Development Company set up by NHB completed a first mortgage-backed issuance and listing that can help standardize deal structures and funding access. These steps support broader participation and funding diversity in the India home loan market while maintaining regulatory guardrails.

India Home Loan Industry Leaders

State Bank of India

HDFC Ltd / HDFC Bank

LIC Housing Finance

ICICI Bank

Axis Bank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: PMAY-U 2.0 sanctioned an additional 1.41 lakh houses across 14 states with a focus on women, SC, and OBC households under the INR 2.50 trillion (USD 30.1 billion) allocation.

- September 2025: Bajaj Housing Finance raised USD 781 million in India’s largest 2024 IPO with strong subscription and plans to expand affordable lending capacity.

- May 2025: Warburg Pincus acquired 100% of Shriram Housing Finance for INR 4,757 crore (USD 0.6 billion) to scale affordable-focused housing credit.

- December 2025: SBI guided its home-loan portfolio to cross INR 10 trillion (USD 120.5 billion) in FY26, supported by strong growth and stable asset quality.

India Home Loan Market Report Scope

The home loan market is the financial sector where lenders provide loans to purchase or construct residential properties. It involves borrowing and lending funds to individuals or households seeking financial assistance to buy a house, apartment, or land for residential purposes. India's Home Loan Market is segmented By Customer Type (Salaried, Self-Employed), By Source (Bank and Housing Finance Companies), By Interest Rate (Fixed Rate and Floating Rate), and By Tenure (up to 5 Years, 6 - 10 Years, 11 - 24 Years, and 25 - 30 Years). The report offers market size and forecasts in value (USD) for all the above segments.

| Fixed-Rate Home Loans |

| Floating-Rate Home Loans |

| Public Sector Banks |

| Private Sector Banks |

| Housing Finance Companies (HFCs) |

| Non-Banking Financial Companies (NBFCs) |

| Salaried |

| Self-Employed |

| PMAY-CLSS Beneficiaries |

| Non-Subsidized Loans |

| By Loan Type (Value) | Fixed-Rate Home Loans |

| Floating-Rate Home Loans | |

| By Provider Type (Value) | Public Sector Banks |

| Private Sector Banks | |

| Housing Finance Companies (HFCs) | |

| Non-Banking Financial Companies (NBFCs) | |

| By Customer Type | Salaried |

| Self-Employed | |

| By Interest-Subsidy Scheme Participation (Value) | PMAY-CLSS Beneficiaries |

| Non-Subsidized Loans |

Key Questions Answered in the Report

What is the current size and growth outlook for the India home loan market?

The India home loan market size is USD 430.74 billion in 2026 and is forecast to reach USD 809.07 billion by 2031 at a 13.44% CAGR.

Which loan type is growing the fastest in the India home loan market?

Fixed-rate mortgages are projected to grow the fastest at 17.24% through 2031, even as floating-rate products remain the largest by share in 2025.

How do government subsidies influence demand in the India home loan market?

PMAY-Urban 2.0 lowers EMIs for eligible borrowers with interest subsidy up to INR 1.80 lakh, and the CLSS segment is expected to expand at 16.44% through 2031.

Which provider groups lead the India home loan market and why?

Public-sector banks held 47.33% in 2025 due to rapid rate transmission, while NBFCs are growing faster by specializing in self-employed underwriting.

What policy continues to boost affordable housing demand?

The Pradhan Mantri Awas Yojana subsidy program, extended through 2027, offers interest subventions up to 6.5%, enhancing affordability.

What are the main risks to growth in the India home loan market?

Policy-rate volatility and developer insolvency delays remain the most prominent risks, with regulatory measures improving transparency and pass-through over time.

Page last updated on: