Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

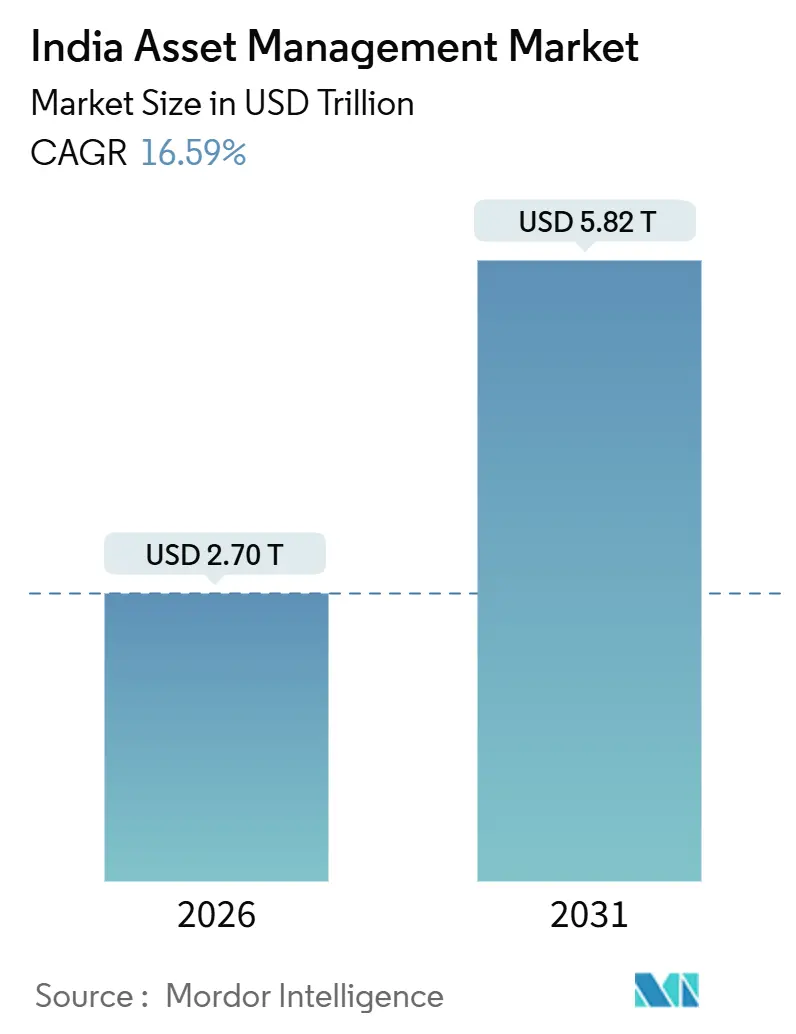

| Market Size (2026) | USD 2.70 Trillion |

| Market Size (2031) | USD 5.82 Trillion |

| Growth Rate (2026 - 2031) | 16.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Asset Management Market Analysis by Mordor Intelligence

The India asset management market size stands at USD 2.70 trillion in 2026 and is projected to reach USD 5.82 trillion by 2031, reflecting a 16.59% CAGR over 2026-2031. The growth outlook is supported by the formalization of household savings, steady pension reforms that improve flexibility and choice, and policy-led digitization that has reduced investor onboarding from weeks to minutes. A broader shift toward financialization is evident as systematic investing deepens and retirement assets scale, reinforcing a long-term savings funnel. Regulatory infrastructure continues to emphasize risk-based supervision alongside clear product rules, which promotes innovation while maintaining investor protection. Cross-border pathways through GIFT City complement onshore platforms by channeling compliant foreign capital into domestic assets.

Key Report Takeaways

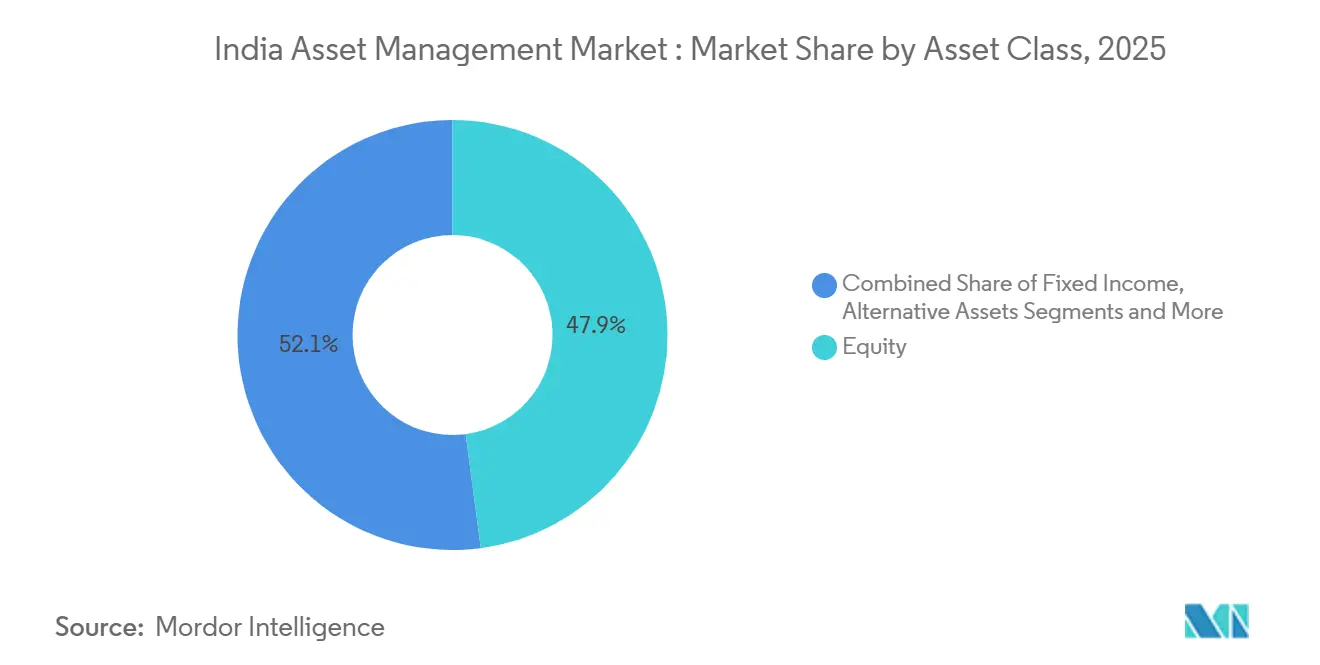

- By asset class, equity-oriented assets held 47.9% of India asset management market share in 2025, while alternatives are projected to record the fastest growth with a 16.85% CAGR through 2031.

- By firm type, banks held 56.5% market share in 2025, and wealth advisory firms and RIAs are projected to expand at a 17.27% CAGR to 2031.

- By mode of advisory, human advisory retained 92.6% share in 2025, and robo-advisory is projected to grow at a 22.43% CAGR through 2031.

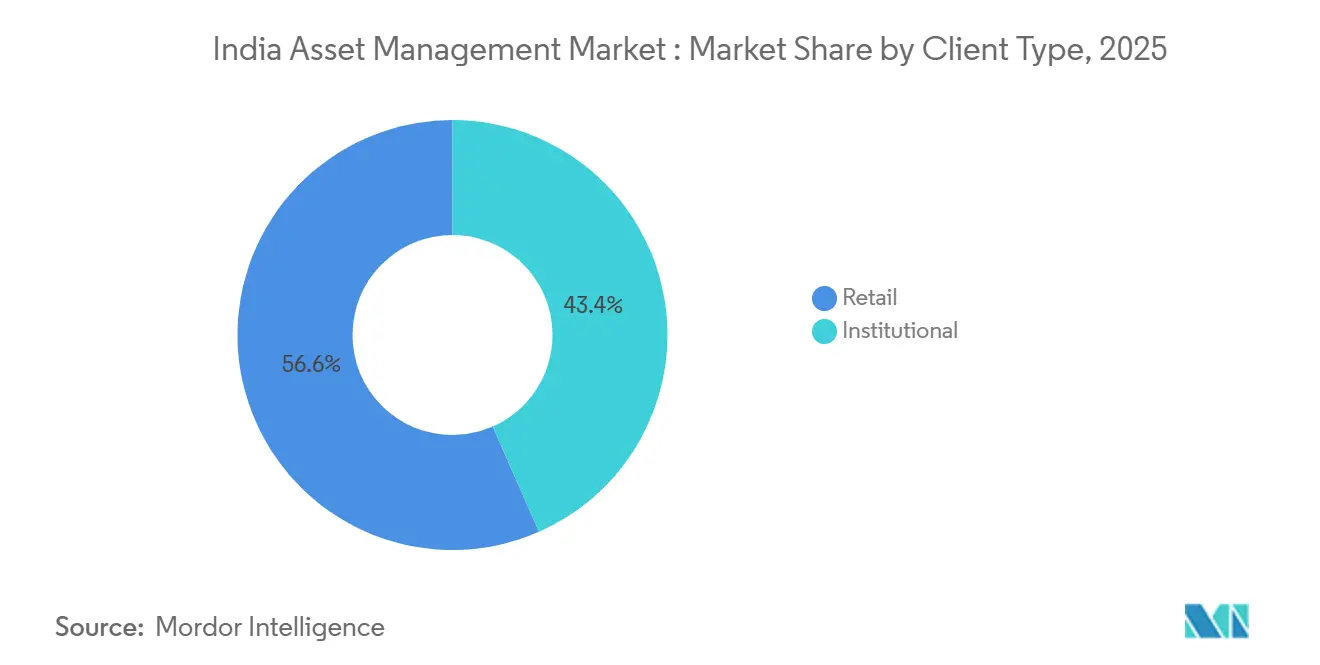

- By client type, retail investors held 56.6% share in 2025, while the institutional segment is projected to grow at a 16.19% CAGR to 2031.

- By management source, the onshore-managed segment retained 87.2% share in 2025, and offshore-delegated mandates are projected to expand at an 18.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retail SIP boom & digital onboarding | +4.2% | National, with early gains in Tier-I cities expanding to Tier-II/III via fintech penetration | Short term (≤ 2 years) |

| Surge in Alternatives (AIF & PMS) | +3.8% | Pan-India, concentrated in metros for HNI and institutional mandates; expanding via GIFT City for cross-border capital | Medium term (2-4 years) |

| Pension reforms driving NPS inflows | +2.9% | National for government employees, accelerating in corporate and all-citizen categories | Long term (≥ 4 years) |

| GIFT City cross-border fund passporting | +2.1% | GIFT City with spillover to national managers seeking offshore LP capital | Medium term (2-4 years) |

| Tokenized funds and DLT-enabled operations | +1.3% | GIFT City sandbox with pilots in select AMCs for blockchain-based units and settlements | Long term (≥ 4 years) |

| SEBI risk-based supervision lowers compliance costs | +1.1% | National, aiding mid-tier AMCs through optimized inspection cycles | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Retail SIP Boom & Digital Onboarding

Monthly systematic investing has created persistent retail participation that supports diversified flows across market cycles. AMFI data and monthly market commentary show sustained investor additions and consistent inflows through 2025, which anchors disciplined allocation patterns even during episodes of volatility[1]Association of Mutual Funds in India, “AMFI Annual Report Fiscal 2025,” AMFI, amfiindia.com. Digital onboarding has compressed account-opening times through SEBI’s video-based customer identification procedures and e-KYC, which reduces paper dependence and improves reach beyond top-tier cities. The MITRA platform that helps investors trace and recover inactive folios increases transparency and supports long-term investor confidence in mutual funds. NPS has paired UPI-enabled D-Remit and BBPS channels with simplified operations, which enable friction-light voluntary contributions for gig workers and the informal sector[2]National Pension System Trust, “PFRDA Circulars,” NPSCRA, npscra.proteantech.in. SEBI’s 2025 incentive framework that targets beyond-top-30 cities and women investors supports first-time participation and broader geographic reach for the India asset management market.

Surge in Alternatives (AIF & PMS)

AIFs and PMS have scaled as differentiated mandates for high net worth, family office, and institutional investors who seek concentrated, bespoke strategies and access to private markets. SEBI’s ongoing disclosure, valuation, and risk-based supervision standards for AIFs and portfolio managers have increased transparency, which supports sustained fundraising and portfolio deployment in private equity, credit, and real assets. As of 2025, SEBI records show a large registered base of AIFs and an expanding PMS industry footprint, which together broaden the product shelf beyond traditional mutual funds for the India asset management market. RBI has limited interconnectedness risks through exposure caps on regulated entities’ investments in AIFs and has imposed provisioning for certain downstream exposures, which addresses systemic concerns while preserving the growth runway for private credit and special situations[3]https://www.rbi.org.in/. . SEBI has also tightened product-level guardrails such as restrictions on unlisted equity exposure in open-ended mutual funds, which keeps liquidity architecture aligned with daily redemption obligations and avoids structural mismatches. Together, these measures underpin a steady shift toward alternatives, while onshore and IFSC vehicles provide flexible structuring paths for domestic and cross-border limited partners.

Pension Reforms Driving NPS Inflows

Reforms across exit rules and asset allocation flexibility have improved NPS’s appeal for non-government subscribers and corporates. In December 2025, PFRDA increased the lump-sum withdrawal limit to 80% of accumulated pension wealth for non-government subscribers and reduced the mandatory annuity requirement, which improved autonomy and retirement planning choices. The Multiple Scheme Framework allows non-government subscribers up to 100% equity allocation and diversified choices across pension fund managers, which raises the potential for long-term wealth creation within the regulatory envelope for the India asset management market. PFRDA has also simplified operations through same-day investment for eligible contributions and expanded distribution via pension agents and Points of Presence, which streamlines access to retirement products. Portfolio diversification permissions now include gold and silver ETFs and broader domestic capital market exposures, which reduce concentration in government securities and corporate debt alone.

GIFT City Cross-Border Fund Passporting

The IFSC framework at GIFT City is supporting India-focused fund management with global investor access under a clear regulatory architecture. By mid-2025, 177 fund management entities had launched 272 schemes with cumulative commitments of USD 22.11 billion, with most of the capital allocated back into India[4]https://ifsca.gov.in/CommonDirect/ViewFile?id=21626bde60601ef44a0ed022016f9fa2&fileName=Fund_Management_ecosystem_at_GIFT_IFSC_records_robust_growth_amid_IFSCA%E2%80%99s_progressive_regulatory_reforms_20250807_0623.pdf. The IFSCA Fund Management Regulations detail permissible investments across IFSC, India, and eligible foreign jurisdictions, enabling managers to run global mandates from an India base. A tax-neutral relocation framework allows offshore funds to move into IFSC before March 2030 without triggering capital gains for the fund or investors, which reduces friction for redomiciling vehicles and for setting up parallel structures. SEBI and IFSCA have also enabled participation by NRIs, OCIs, and resident individuals in eligible IFSC-based FPIs, which unlocks compliant diaspora and domestic capital into India strategies through IFSC channels. Over time, third-party fund management permissions within IFSC lower entry barriers for global managers who seek India exposure with local regulatory certainty and tax efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee compression from passives | -2.8% | National, across all AMC categories as passive AUM share rises | Short term (≤ 2 years) |

| Volatility and rich equity valuations | -2.4% | National equity markets with spillover to hybrid allocations | Short term (≤ 2 years) |

| Analytics and AI talent shortage | -1.6% | Metro hubs hosting GCCs and AMC tech teams | Medium term (2-4 years) |

| Liquidity mismatch in privately placed alternatives | -1.3% | Category II AIFs, unlisted PMS portfolios, and private credit | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fee Compression from Passives

SEBI has moved from a Total Expense Ratio to a Base Expense Ratio regime and lowered fee caps for passively managed funds, which reduces investor costs and compresses management margins for passive products, effective April 2026. Brokerage caps for cash and derivatives transactions were also reduced within the same package, improving end-investor efficiency and reinforcing a scale-led model for passive asset gathering. AMFI data through 2025 shows steady inflows into index funds and ETFs, reflecting a persistent shift toward low-cost beta exposure within the India asset management market. The new fee architecture unbundles levies from core management fees and standardizes disclosures, which strengthens transparency and comparability across product types. Active managers face higher thresholds for sustained alpha net of fees, which intensifies the focus on clear differentiation in process, risk management, and capacity discipline within the India asset management market.

Volatility and Rich Equity Valuations

India’s risk environment is sensitive to global liquidity cycles and periodic earnings resets, which raises the risk of intermittent corrections that test investor discipline and fund liquidity. SEBI’s ongoing surveillance and targeted product rules, including restrictions on pre-IPO placements for open-ended schemes, are designed to align liquidity profiles with daily redemption obligations during stress. Periods of heightened volatility tend to produce a barbell in flows, with disciplined SIPs continuing and tactical reallocations between debt, equity, and hybrid funds, which underscores the role of asset allocation in balancing risk. Market-wide oversight through SEBI’s risk-based supervision supports priority monitoring of larger or higher-risk entities so that systemic channels are contained if selloffs broaden. On valuation, investor communications from public institutions have highlighted episodes where price-to-earnings metrics and market capitalization-to-GDP ratios have stayed elevated relative to long-term ranges, which suggests tempered forward returns if earnings disappoint, though the long-run household savings shift remains intact for the India asset management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Equity schemes anchor retail flows while alternatives surge

Equity-oriented assets accounted for 47.9% of the India asset management market share in 2025, propelled by consistent SIP participation and positive mark-to-market gains through the year. AMFI disclosures confirm sustained monthly equity contributions and expanding investor bases, which strengthen the core retail foundation of equity schemes in the India asset management market. Balanced and hybrid products complement equity exposure by providing downside buffers through debt and gold allocations, which improve portfolio resiliency during risk-off episodes. On the retirement side, NPS has improved elective equity exposure for non-government subscribers under the Multiple Scheme Framework, which aligns asset allocation with longer working horizons. SEBI’s product rules on liquidity and diversification cap illiquid and unlisted exposures for open-ended funds, which protects redemption architecture and reduces cross-asset spillovers for the India asset management market.

Fixed income remains a core allocation channel for institutions and conservative retail investors, with money market and liquid funds providing transaction efficiency for treasury and corporate liquidity needs. AMFI reports show robust fixed income categories through mid-2025 and stable adoption of short-duration products, which smooths reinvestment risk during policy transitions. Gold ETFs have acted as a tactical hedge during bouts of currency and rates volatility, and their integration into pension allocation menus broadens their use beyond tactical retail positioning. Alternatives continue to scale with AIFs and PMS serving different needs across private equity, credit, and specialist strategies, supported by evolving disclosure and valuation standards for the India asset management market. Overall, the multi-asset mix is deepening, with equity as an anchor, high-quality credit as ballast, and alternatives for incremental alpha or diversification premia.

By Firm Type: Banks dominate distribution, yet wealth advisors scale rapidly

Banks held 56.5% share in 2025, reflecting the combined influence of branch distribution, captive customer bases, and regulatory permissions to sponsor select pension vehicles that meet prudential criteria. PFRDA’s 2026 guidelines allow eligible scheduled commercial banks that satisfy market capitalization, asset base, profitability, and asset quality thresholds to sponsor pension funds, which broadens the field of institutional managers serving NPS mandates. SEBI’s framework for distributor incentives in beyond-top-30 cities and for women investors adds inclusion-oriented funding for outreach, which particularly benefits banking networks and larger distributors in the India asset management market. AMFI has documented the steady rise of direct plans and the continued breadth of folio growth, which together signal the coexistence of both advice-led and direct channels as investors mature.

Wealth advisory firms and RIAs are projected to grow at a 17.27% CAGR through 2031 as higher net worth segments seek fee-only advice, estate planning, and curated access to alternatives. SEBI’s Master Circular for Investment Advisers and ongoing administrative oversight have strengthened suitability, disclosure, and fiduciary plumbing for advice relationships in the India asset management industry. The growth of fee-based advisory reflects investor demand for transparent cost structures, while banks and broker-dealers continue to anchor scale distribution models that suit mainstream retail adoption. Over time, hybrid advice that blends human guidance with automated tools is likely to expand, while the core role of banks remains intact for mass-market reach in the India asset management market.

By Mode of Advisory: Human advisors anchor trust while robo-advisory scales automation

Human advisory retained 92.6% share in 2025, supported by comprehensive mandates that span portfolio construction, tax planning, and behavioral coaching across wider product sets. SEBI’s Master Circular for Portfolio Managers codifies quarterly reporting, prudential exposure thresholds, and governance standards that reinforce trust in discretionary and non-discretionary mandates for the India asset management market. SEBI’s risk-based supervision approach for mutual funds and principle-based monitoring of advisers allows higher-touch oversight where systemic impact is larger, while enabling streamlined inspection cycles for lower-risk entities. This layered regulation supports the depth of human advice across complex client needs in the India asset management industry.

Robo-advisory, at 7.4% share, is projected to grow at a 22.43% CAGR through 2031 as digital natives favor low-cost, rules-based portfolios. SEBI requires robust risk profiling, suitability processes, and audit trails even for automated models, which protects consumers and improves comparability across platforms. The product shelf for goal-based plans is strongest in standardized building blocks such as equity index funds, short-duration debt, and gold ETFs, which simplifies automation and periodic rebalancing. As hybrid arrangements scale, algorithms handle tactical allocation while human advisers manage complex planning and risk scenarios for the India asset management market.

By Client Type: Retail SIP momentum sustains equity while institutional rebalances

Retail investors held 56.6% share in 2025, anchored by systematic investment plans and digitized onboarding that reduces friction. AMFI recorded a steady rise in folios to more than 26 crore by late 2025, with retail investors forming the backbone of equity funds through persistent SIP discipline in the India asset management market. SEBI’s inclusion-focused incentive framework for distributors in beyond-top-30 cities and for women investors extends reach into new investor cohorts. PFRDA-supported rails such as BBPS and UPI-enabled contributions further extend access for voluntary retirement savings, which supports long-term participation.

Institutions, at 43.4% share, are projected to expand at a 16.19% CAGR through 2031 as insurers, provident funds, and corporate treasuries recalibrate public and private market allocations. PMS and AIF structures offer policy-compliant mandates with concentration and liquidity parameters aligned to liability needs, while onshore mutual funds remain core for daily-liquidity strategies in the India asset management market. Institutions also utilize fixed income categories for liquidity and balance-sheet efficiency, supporting a diverse demand base across credit tenors and risk grades . During year-end or policy transitions, institutions adjust exposures tactically, while steady retail SIPs cushion overall industry flows for the India asset management market.

By Management Source: Onshore managers anchor domestic savings, offshore mandates tap global capital

Onshore-managed assets accounted for 87.2% of total assets in 2025, reflecting the combined scale of SEBI-registered mutual funds, portfolio managers, and AIFs under daily NAV, custody, and disclosure standards. AMFI’s industry updates show high and rising industry AUM with a wide investor base, which underlines the onshore anchor for Indian household financialization. SEBI’s risk-based supervision concentrates oversight on entities with higher scale or impact, which supports market integrity without duplicative compliance burdens for smaller participants. The India asset management industry benefits from stable and transparent rules across mutual funds, AIFs, and PMS, which maintains investor confidence.

Offshore-delegated assets are projected to grow at an 18.56% CAGR through 2031, anchored by IFSC fund management permissions that allow India-focused and global mandates within a tax-efficient, regulatorily ring-fenced zone. IFSCA reports 177 registered fund management entities and USD 22.11 billion of cumulative commitments as of mid-2025, with most of the capital channeled into India opportunities. Tax-neutral relocation, third-party fund management, and permission for eligible Indian and diaspora investors to participate in IFSC-based FPIs reduce structural frictions and expand the addressable LP universe for the India asset management market. Over time, dual-shore capabilities are likely to differentiate managers who can serve domestic retail and offshore institutional pools with product and compliance specialization.

Geography Analysis

India’s asset management activity concentrates in Tier-I hubs that house exchanges, regulators, and the largest talent pools, while distribution and folio growth are broadening across Tier-II and beyond-top-30 cities. AMFI data through 2025 highlight a widening investor base and steady folio expansion, with direct plans and systematic investing rising in tandem in the India asset management market. Inclusion-led incentives that target new-to-industry segments and women investors aim to accelerate adoption outside metros, which aligns with the continued rollout of digital rails. Pension reforms and operational enablers such as same-day investment and broader PoP networks are designed to extend retirement coverage into semi-urban and rural segments.

Tier-II hiring hubs are expanding as financial firms build technology, analytics, and operations teams in lower-cost cities, which supports distribution and advisory capacity outside metros. National digital public infrastructure and interoperable payment and identity rails reduce onboarding friction, which helps mobilize flows into mutual funds and NPS products beyond legacy centers in the India asset management market. AMFI’s data on passive and hybrid adoption through 2025 also reflect broader product familiarity, aided by app-based education, standardized disclosures, and transparent cost frameworks. These developments indicate a more even geographic footprint for distribution and service delivery over the forecast period.

GIFT City adds a cross-border dimension to the geographic picture by anchoring international capital under Indian regulation. IFSCA has documented a growing roster of fund management entities, redomiciled schemes, and global investor participation, which positions IFSC as a gateway for inbound allocations to Indian assets within the India asset management market . As onshore and IFSC regimes advance in parallel, managers can tailor legal structures and distribution to investor domicile and tax needs, while maintaining consistent product governance standards. Over time, this combination supports a more diversified, resilient, and geographically balanced growth path for the India asset management market.

Competitive Landscape

Industry concentration is moderate, with large mutual fund houses leading by AUM and deep retail penetration, while PMS and AIF segments remain more fragmented due to niche strategies and sponsor-driven differentiation. AMFI’s industry reporting underscores the scale of the mutual fund complex and the breadth of folio participation, which provides durable operating leverage for the largest managers in the India asset management market. Mid-tier managers benefit from SEBI’s risk-based supervision that calibrates inspection intensity to scale and governance factors, allowing more resources to flow into product innovation and distribution. The result is a landscape where scale, brand trust, and compliant innovation determine durable share gains.

Two strategic vectors are shaping competition. First, cost and process reforms continue to influence product design and pricing, with SEBI’s Base Expense Ratio regime and tighter brokerage caps reinforcing a low-cost spine for passive offerings in the India asset management market. Second, cross-border structuring via IFSC allows managers to serve global limited partners under Indian oversight while running onshore retail and advisory mandates in parallel. These shifts favor managers who can operate dual-shore platforms and execute clear product architectures across equity, fixed income, and alternatives while maintaining consistent compliance.

Examples of recent strategic moves illustrate these vectors. Managers have invested in direct-to-investor platforms and portfolio reporting tools that improve transparency, reduce servicing costs, and support direct plan adoption within the India asset management market. IFSC permissions for third-party fund management and diaspora participation in eligible IFSC-based FPIs expand the scope for India-focused strategies to attract global capital under a common regulatory perimeter. On the operations side, PFRDA’s same-day investment and broader asset eligibility in NPS modernize the retirement product experience, aligning with investor expectations shaped by instant settlement and digital service standards.

India Asset Management Industry Leaders

SBI Mutual Fund

ICICI Prudential AMC

HDFC AMC

Nippon India AMC

Axis AMC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: PFRDA constituted a 15-member expert committee chaired by M.S. Sahoo to develop a regulatory framework for assured payout options under NPS, focusing on lock-ins, withdrawal limits, pricing mechanisms, and consumer protection standards.

- December 2025: SEBI approved a shift to Base Expense Ratio and reduced brokerage caps for mutual funds, effective April 1, 2026, enhancing transparency and lowering investor costs for passives.

- November 2025: SEBI introduced additional incentives for distributors onboarding new investors from beyond-top-30 cities and for women investors, with commission caps and product exclusions for alignment.

- September 2025: MeitY launched the National Blockchain Framework and the Vishvasya Blockchain Stack, expanding the national backbone for permissioned DLT pilots.

India Asset Management Market Report Scope

By Asset Class

| Equity |

| Fixed Income |

| Alternative Assets |

| Other Asset Classes |

By Firm Type

| Broker-Dealers |

| Banks |

| Wealth Advisory Firms |

| Other Firm Types |

By Mode of Advisory

| Human Advisory |

| Robo-Advisory |

By Client Type

| Retail |

| Institutional |

By Management Source

| Offshore |

| Onshore |

| By Asset Class | Equity |

| Fixed Income | |

| Alternative Assets | |

| Other Asset Classes | |

| By Firm Type | Broker-Dealers |

| Banks | |

| Wealth Advisory Firms | |

| Other Firm Types | |

| By Mode of Advisory | Human Advisory |

| Robo-Advisory | |

| By Client Type | Retail |

| Institutional | |

| By Management Source | Offshore |

| Onshore |

Key Questions Answered in the Report

What is the size and growth outlook for the India asset management market to 2031?

The India asset management market size is USD 2.70 trillion in 2026 and is projected to reach USD 5.82 trillion by 2031 at a 16.59% CAGR.

Which segments lead and which are growing fastest in the India asset management market?

Equity-oriented assets lead by share, while alternatives are projected to be the fastest-growing asset class; banks lead by firm type, while wealth advisory firms and RIAs grow fastest; human advisory dominates by share, and robo-advisory grows fastest.

How do policy and regulation support the India asset management market today?

SEBI’s risk-based supervision, expense ratio reforms, and product guardrails, along with PFRDA’s flexibility in NPS exits and allocations and IFSCA’s fund passporting, support transparent growth and broader access.

What role does GIFT City play in the India asset management market?

GIFT City’s IFSC enables managers to domicile India-focused and global strategies under a tax-efficient regime, attracting international capital with USD 22.11 billion in commitments as of mid-2025.

How are digital rails changing access to the India asset management market?

Video KYC, e-KYC, BBPS, and UPI-enabled contributions reduce onboarding friction and enable disciplined investing through SIPs and NPS contributions across geographies.

What risks could slow growth in the India asset management market?

Fee compression from passives, valuation and volatility cycles, AI and analytics talent shortages, and liquidity mismatches in privately-placed alternatives are the key near to medium-term risks that managers are addressing through product and process design SEBI.GOV.IN.

Page last updated on: