Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 22.44 Billion |

| Market Size (2026) | USD 23.13 Billion |

| Market Size (2031) | USD 26.89 Billion |

| Growth Rate (2026 - 2031) | 3.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Plastic Packaging Market Analysis by Mordor Intelligence

The India plastic packaging market size was valued at USD 22.44 billion in 2025 and estimated to grow from USD 23.13 billion in 2026 to reach USD 26.89 billion by 2031, at a CAGR of 3.06% during the forecast period (2026-2031).[1]Ministry of Environment, Forest and Climate Change, “Extended Producer Responsibility Guidelines,” moef.gov.in Demand pivots from pure volume to value-added formats as Extended Producer Responsibility (EPR) rules enacted in 2024 place the onus of post-consumer waste on brand owners, pushing converters toward recycled-content resins and higher-margin barrier technologies. E-commerce parcel volumes surged 40% in 2024, triggering a parallel spike in secondary packaging that favors tamper-evident pouches, low-gauge stretch films, and moisture-barrier liners. The sector also benefits from pharmaceuticals shifting to single-dose packs that suit rural health outreach programs, while food and beverage multinationals localize production to serve rapid-delivery channels and comply with food-contact material rules. Regional plastic parks in Maharashtra, Gujarat, and Tamil Nadu compress supply chains, reduce logistics cost, and enable just-in-time inventory for both virgin and recycled feedstocks.

Key Report Takeaways

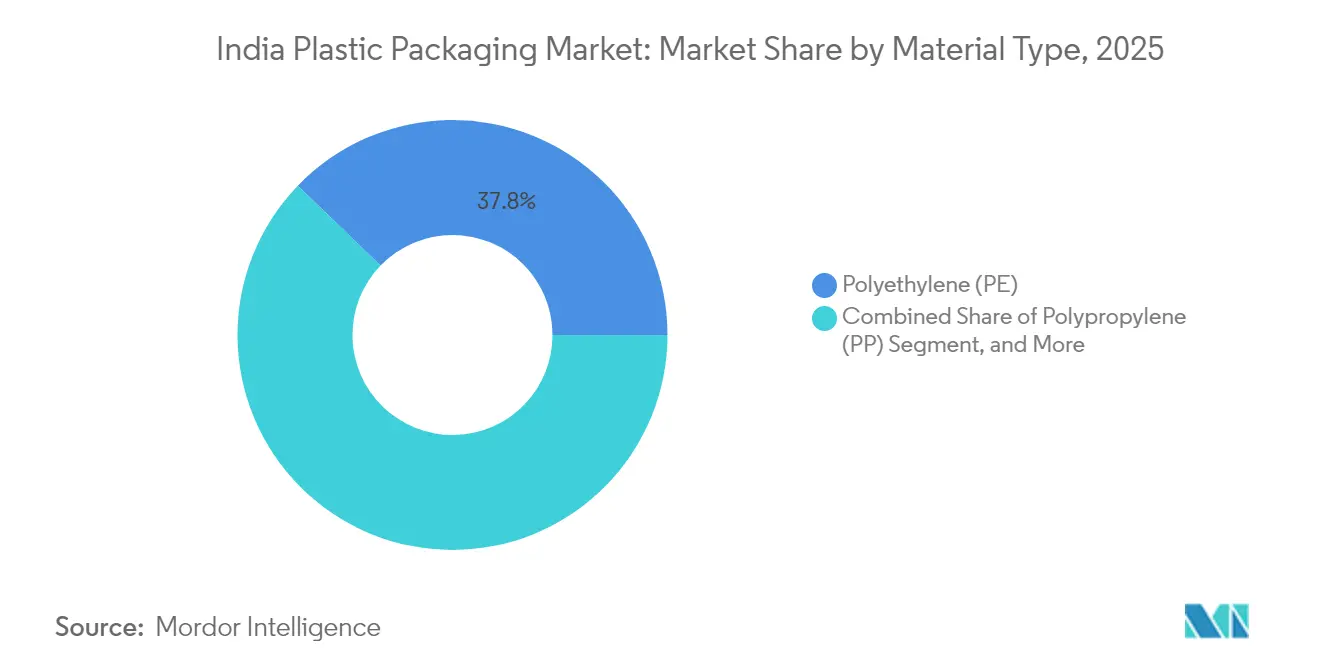

- By material type, polyethylene held 37.78% of the India plastic packaging market share in 2025, and polyethylene terephthalate is projected to advance at a 4.18% CAGR through 2031.

- By packaging type, flexible solutions accounted for 54.05% share of the India plastic packaging market size in 2025, and forecast to expand at a 4.6% CAGR through 2031.

- By product form, pouches and sachets led with 31.85% revenue share in 2025, and Films and wraps are advancing at a 4.78% CAGR through 2031.

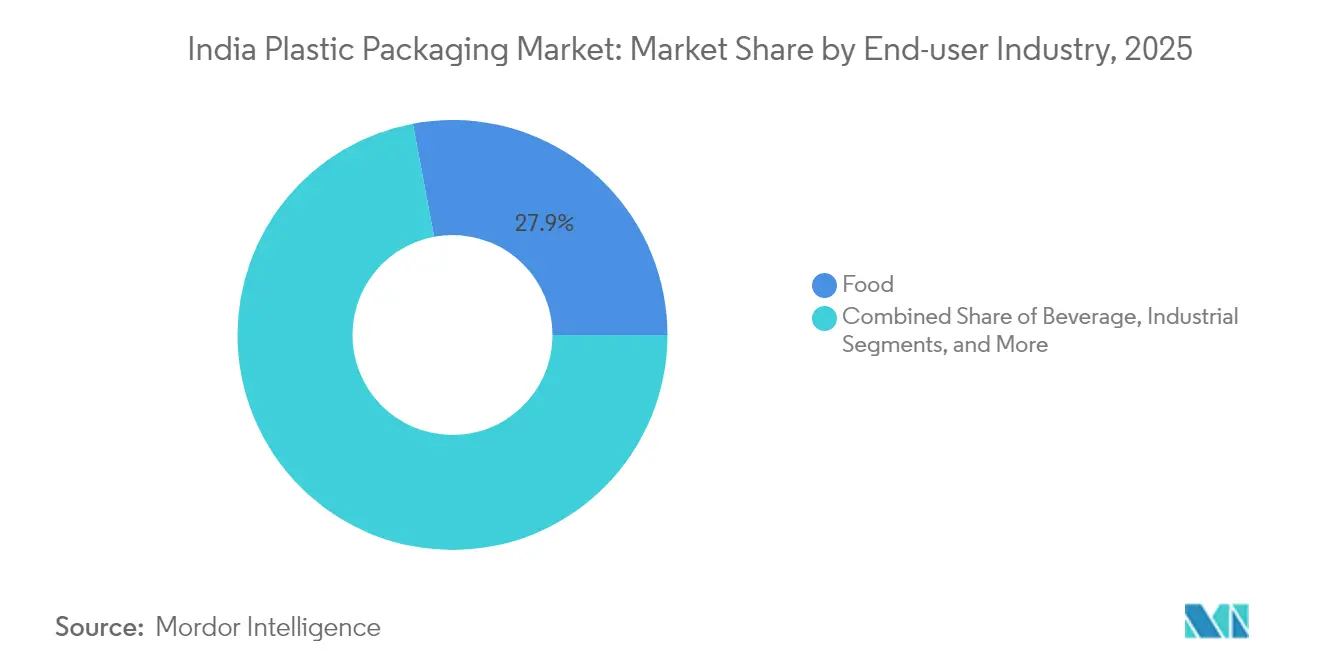

- By end-user industry, food maintained a 27.95% share of the India plastic packaging market size in 2025, and cosmetics and personal care are expected to grow at a 4.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing e-commerce and quick-commerce logistics boom | +0.8% | National, with early gains in Mumbai, Delhi, Bengaluru | Short term (≤ 2 years) |

| Demand for lightweight flexible formats | +1.2% | Global, concentrated in Maharashtra, Gujarat, Tamil Nadu | Medium term (2-4 years) |

| Uptake of recycled-content plastics | +0.7% | National, spill-over to neighboring countries | Long term (≥ 4 years) |

| EPR-linked rPET/rHDPE localization push | +0.9% | National, with early adoption in industrial states | Medium term (2-4 years) |

| AI-enabled converting lines for SMEs | +0.6% | Regional clusters in Maharashtra, Gujarat, Karnataka | Long term (≥ 4 years) |

| Single-dose pharma pouch surge | +0.4% | National, rural healthcare expansion focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing e-commerce and quick-commerce logistics boom

Package volumes from 15-minute delivery platforms grew 300% in major metros during 2024, requiring tamper-proof pouches that preserve integrity across multiple handling points. Converters that deploy automated pouch lines achieve cycle times near 200 packs per minute, shortening lead times for grocery aggregators that refresh inventory thrice daily. FMCG majors have responded by relocating filling operations closer to demand centers; for example, a leading beverage maker commissioned a plant in Assam in 2025, trimming average transit distance to 450 km and cutting secondary packaging spend by 14%. This shift concentrates demand for low-gauge stretch films that withstand vibration and thermal fluctuations common in last-mile two-wheeler delivery. Regional warehousing networks now specify moisture-barrier films with WVTR below 10 g / m² / day to avoid condensation damage during the monsoon. The India plastic packaging market, therefore, receives a rapid influx of orders for small-format, high-barrier solutions that command price premiums over legacy SKUs without eroding fill-rate economics.

Demand for lightweight flexible formats

Logistics providers levy fuel-surcharge pass-throughs that incentivize weight reduction, steering brands away from rigid packs toward mono-material laminates that are 40% lighter yet meet drop-test thresholds. Barrier-coated substrates now achieve oxygen transmission rates below 1 cc / m² / day, allowing shelf-stable food to travel farther without a cold chain. As flexible pouches replace composite cans in powdered beverage mixes, converters save up to 30% resin weight per 100 g serving, easing EPR fee liabilities that scale with grammage. Thermoforming lines that once served dairy tubs now pivot to form-fill-seal cup lidding, capturing an outsized share of premium yogurt launches. The India plastic packaging market also witnesses bi-axially oriented PE films gaining traction because they allow all-PE laminates that qualify for single-material recycling streams. Capital outlay for retrofitting lamination equipment averages USD 2 million per line; SMEs mitigate risk by forming cooperatives that share finishing assets inside government-backed plastic parks.

Uptake of recycled-content plastics

A nationwide mandate requires 30% recycled content in PET beverage bottles by 2025, spurring investments in food-grade wash lines with FDA-equivalent certification. Integrated players with captive recycling assets sell certified rPET at a 20-25% premium over virgin resin due to limited compliant capacity, currently only 15% of national recycling throughput. The India plastic packaging market thus experiences vertical mergers; resin producers acquire downstream converters to guarantee offtake for recycled flakes. Financial closure for a USD 165 million depolymerization plant announced in 2024 demonstrates investor confidence that chemical recycling will meet upcoming quality thresholds for direct food contact. Equipment suppliers report 18-month lead times for solid-state polycondensation units, compelling early movers to place orders ahead of surging demand. EPR credits now trade on emerging exchanges, with rPET certificates averaging USD 55 per tonne in Q1 2025, offering additional revenue streams for recyclers who exceed legal targets.

EPR-linked rPET / rHDPE localization push

Brand owners finance take-back systems, catalyzing regional collection hubs that feed into polymer parks where recyclers pelletize waste within 48 hours, preserving IV levels for high-end applications. Domestic supply has become strategic after 2024 geopolitical tensions disrupted 30% of specialty film imports. A leading multinational converter doubled planned Panipat capacity to 168,000 MTPA of post-consumer PET chips, ensuring consistent input for its barrier film lines. State incentives such as electricity rebates up to INR 2 / kWh for recycling plants shorten payback to under five years. Cross-industry tie-ups-beverage bottlers co-funding grocery chains’ reverse-vending machines-further anchor the India plastic packaging market in a localized circular economy model. Parallel standardization by the Bureau of Indian Standards (BIS) sets testing protocols for recycled resins, averting performance variability that previously deterred converters from large-scale adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resin price volatility | -0.5% | Global impact, concentrated in import-dependent regions | Short term (≤ 2 years) |

| Single-use-plastic regulatory bans | -0.3% | National, with state-level variations | Medium term (2-4 years) |

| Scarce food-grade PCR infrastructure | -0.4% | National, concentrated in Maharashtra, Gujarat, Tamil Nadu | Long term (≥ 4 years) |

| Import-dependent hi-end film machinery CAPEX | -0.6% | National, affecting specialized converters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Resin price volatility

Crude swings drove PE and PP contract prices up to 30% during 2024, yet converters locked into six-month supply agreements could only reprice quarterly, compressing EBITDA margins by nearly 4 percentage points. Flexible converters carry inventory covering just 20 production days on average; sudden price hikes strain working capital facilities that already carry 11% interest. Hedging via polymer futures remains nascent, with low liquidity restricting meaningful coverage beyond 5% of monthly volume. The India plastic packaging market, therefore, sees cooperatives negotiating pooled contracts to gain bulk discounts while sharing storage depots adjacent to refinery tank farms. Government plans for a Production-Linked Incentive (PLI) scheme in petrochemicals promise duty waivers, but capacity additions will not materialize until 2028, leaving the near-term outlook vulnerable to global feedstock volatility.

Single-use-plastic regulatory bans

State rules vary: Maharashtra bans carry bags below 50 micron thickness, while Tamil Nadu targets cutlery and straws, forcing firms with national footprints to juggle 10+ SKU codes per product line.[2]Maharashtra Pollution Control Board, “Single-Use Plastic Ban Notifications,” mpcb.gov.in Compliance redesign costs average 9% of affected SKUs’ annual revenue, including tooling and artwork changes. Biodegradable PLA substitutes remain 54% costlier than PE, limiting immediate switch viability for mass-market sachets, though a landmark 80,000-tonne PLA plant breaking ground in February 2025 aims to narrow the gap within three years. The India plastic packaging market consequently experiences an order backlog as converters await clarity on potential central harmonization of bans. Meanwhile, retailers shift to thicker reusable bags that carry a refundable deposit, slightly cushioning volume loss in banned segments but adding reverse-logistics complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: PE Dominance Faces PET Innovation

Polyethylene commands the highest 37.78% share of the India plastic packaging market in 2025, underpinned by competitive resin pricing and compatibility with blown-film and injection-molding lines already installed nationwide. Its role in high-volume SKUs such as shopping bags, agricultural sheets, and detergent pouches sustains throughput that keeps average operating rates above 80% in major plants. PE also benefits from the flexible feedstock slate of domestic crackers, which maintains a steady monomer supply even during global disruptions, giving local converters stable price benchmarks against imported parity levels. However, polyethylene terephthalate is projected to grow at a 4.18% CAGR through 2031 as brands seek clarity, gloss, and superior barrier credentials for ready-to-drink beverages and condiments. PET’s recyclability advantage dovetails with EPR targets, and multiple bottle-to-bottle projects under implementation aim to lift the India plastic packaging market size for food-grade rPET flakes to more than 1 million TPA by 2027.

In spite of its growth, PET faces melt-filtration bottlenecks that raise capital intensity; integrated PET lines cost 20-25% more than equivalent PE lines due to solid-state polycondensation and higher-pressure injection stretches. Polypropylene fills specialized slots where rigidity and heat resistance matter, such as microwaveable trays and pharma caps, but supply remains tight because domestic PP capacities favor fiber and automotive grades. Polystyrene and EPS gradually decline owing to state bans on foamed tableware, though niche demand persists in appliance liners where cushioning outweighs recyclability concerns. Emerging bioplastics like PLA, backed by a USD 342 million greenfield project in Uttar Pradesh, hold potential in compostable snack packs but remain contingent on municipal composting infrastructure scaling beyond pilot units. As regulators publish draft norms to equate recycled-content thresholds across polymers, converters anticipate a multi-material portfolio balancing cost, performance, and recycle-content quotas, reshaping the India plastic packaging industry over the next decade.

By Packaging Type: Flexible Solutions Drive Innovation

Flexible formats account for 54.05% share of the India plastic packaging market size in 2025, demonstrating the clear economic edge of film-based systems that deliver 30% lower transportation cost per unit of packed weight than rigid alternatives. Multi-layer laminates engineered with EVOH or AlOx coatings extend aroma barrier life, enabling rural distribution without refrigerated trucks. Brand owners pursuing carbon-footprint disclosures favor flexible pouches because life-cycle-assessment models credit them with 60% fewer greenhouse-gas emissions per liter of beverage compared with glass bottles. Flexible packaging is forecast to expand at a 4.6% CAGR through 2031 as quick-commerce spurts heighten demand for single-serve sachets that meet impulse-buy price points. Flexible’s dominance also stems from rapid line changeovers; digital solventless lamination cures in under two hours, allowing converters to manage SKU proliferation from regional flavor launches.

Rigid plastic packaging retains relevance in cosmetics where shelf presence and tactile cues command premium price points. Extrusion-blow-molded HDPE bottles for personal-care products now feature near-infrared sortable masterbatches that ease downstream recycling, aligning rigid formats with circularity goals. Injection-stretch-blown PET jars gain share in nutraceuticals because 38-mm neck finishes accommodate induction-seal liners, preserving volatile ingredients. However, cap-and-closure resin consumption plateaus as tethered-cap EU requirements influence design globally, prompting material light-weighting of hinge bridges. The India plastic packaging market thus exhibits a nuanced co-existence: flexible growth rides on e-commerce cycles, while rigid solutions maintain foothold in premium niches that value aesthetics and reusability.

By Product Form: Pouches Lead While Films Accelerate

Pouches and sachets secure 31.85% of 2025 revenue, reflecting consumers’ affinity for portion-controlled packs priced at INR 5-10 that align with daily cash-flow patterns. Ultrasonic-sealed spouted pouches consolidate baby-food launches, reducing energy consumption by 70% compared with thermal sealing, and improving recyclability via all-PE mono-structures. Stick packs in electrolyte beverages capitalize on rural electrification programs that expand cold-chain reach but still rely on sachet convenience for on-the-go hydration. On the other hand, films and wraps are advancing at a 4.78% CAGR through 2031, buoyed by stretch-hood applications in warehouse palletization and silage films for agrarian export hubs. Specialty shrink films with anti-fog additives penetrate fresh-produce exports, where rejection rates fell to 4% in 2024 from 9% in 2023 due to improved condensation control.

Bottle and jar volumes grow moderately as rPET mandates boost collection schemes that loop clear flake back into beverage chains, with deposit-return pilots in three states retrieving 78% of bottles sold in Q2 2025. Trays and containers ride on the convenience-foods wave, using barrier-coated PP to achieve 180-day ambient shelf life for ready-to-eat curries, reducing cold storage energy load by 22 GWh annually. Bags and sacks remain integral for fertilizers and cement, but average grammage drops by 12% thanks to high-tenacity PE wovens. The “other forms” category features collapsible tubes and thermoformed clamshells incorporating up to 50% recycled PETG, widening repertoire for cosmetics aimed at eco-conscious millennials. Such diversification reinforces the India plastic packaging market as a test-bed for high-barrier yet affordable innovations.

By End-User Industry: Food Sector Stability Meets Cosmetics Growth

Food applications held 27.95% of the India plastic packaging market size in 2025, sustained by rising processed-food penetration and stricter cold-chain logistics under FSSAI guidelines that specify migration limits for multilayer structures. Retort pouches for ready-to-eat meals elevate shelf stability to 18 months, enabling military and disaster-relief tenders that demand field-ready nutrition without frozen storage. Dairy brands adopt transparent barrier cups, allowing consumers to inspect texture, increasing perceived quality and boosting repeat purchases by 7%, according to brand audits. Meanwhile, single-serve condiment sachets ride on quick-service-restaurant expansion, where hygiene concerns prohibit communal dip bowls after the pandemic. The India plastic packaging market thus sees steady base-load volume from food, anchoring factory utilization even during broader economic dips.

Cosmetics and personal care are projected to post a 4.86% CAGR through 2031, driven by premiumization as disposable income climbs among urban households. Airless pump bottles made of recyclable mono-material PP replace multi-component acrylic assemblies, marrying sustainability with upscale touchpoints. Digital-printed shrink sleeves enable limited-edition runs for influencer-led campaigns, shortening concept-to-shelf cycles to under six weeks. Beverage packaging entwines with recycled content targets; rPET bottle adoption soars as soft-drink giants pledge 50% recycled content by 2027, stimulating flake imports until domestic capacity scales. Pharmaceuticals expand unit-dose pouches for antibiotic stewardship programs, as smaller pack sizes curb misuse. Industrial packaging wrestles with resin price swings, turning toward returnable PP crates in automotive supply chains to mitigate single-use tax levies in select states. Together, these dynamics diversify demand streams, cushioning the India plastic packaging industry against shocks in any one vertical.

By Manufacturing Process: Extrusion Scale Versus Thermoforming Innovation

Extrusion processes captured 28.12% of the India plastic packaging market share in 2025, thanks to their versatility across blown film, sheet, and profile applications. Leading converters operate up-gauged three-layer co-extruders equipped with inline MDO units that impart stiffness, allowing 12-micron films to replace traditional 18-micron gauges without compromising tensile strength. Energy-recovery systems on high-output lines cut specific energy consumption to 0.36 kWh / kg, delivering cost savings that absorb resin-price shocks. Co-extrusion enables n-layer tubes with decorative barrier layers, opening export opportunities for oral-care products subject to European recycling criteria. The India plastic packaging market benefits from export-backed extruders achieving 85% capacity utilization even in domestic downturns.

Thermoforming, forecast to grow at a 5.04% CAGR through 2031, leverages precision plug-assist technology to mold thin-wall trays at denesting strengths exceeding 20 N, supporting mechanized filling lines in snacks and confectionery. High-clarity APET sheets, now containing up to 30% internal regrind, meet aesthetic demands while meeting EFSA-equivalent migration limits. Mini-batch thermoformers empower SMEs to serve regional dairy brands without investing in large molds, bolstering capacity in Tier-2 clusters. Injection molding retains niche leadership in caps, closures, and thick-wall jars, while blow molding evolves through multilayer co-ex heads that embed recycled core layers between virgin skins, satisfying food-contact rules yet delivering 25% recycled content. “Other processes,” such as digital direct-to-shape printing, emerge, enabling SKUs as small as 2,000 units for hyper-local runs. Each method addresses distinct value pools, collectively reinforcing the technological depth of the India plastic packaging market.

Geography Analysis

Manufacturing clusters in Maharashtra, Gujarat, and Tamil Nadu account for roughly 60% of organized plastic-packaging capacity, leveraging proximity to refineries, ports, and end-market consumption. Maharashtra’s complexes near Mumbai capitalize on twin-port access at Nhava Sheva and Pipavav, cutting transit times for export cartons to 14 days versus the 21-day national average. Gujarat’s plastic parks at Dahej and Dholera receive polymer directly from on-site crackers, trimming raw-material freight by 6 c / kg and allowing converters to offer price locks despite volatile crude benchmarks. Tamil Nadu’s 239-acre Polymer Industries Park in Thiruvallur, backed by INR 216 crore state funding, draws SMEs into plug-and-play plots where shared utilities shave 12% off capex for extrusion lines. These agglomerations amplify the India plastic packaging market’s regional competitiveness by clustering suppliers, toolmakers, and testing labs within a 50 km radius.

Northern states such as Uttar Pradesh, Haryana, and Punjab serve agricultural film and fertilizer sack demand, boosted by cold-chain expansion along the Delhi-Mumbai Industrial Corridor. Uttar Pradesh offers capital subsidies up to 25% for new packaging units in backward districts, encouraging decentralization from overloaded western hubs. Haryana benefits from the Kundli-Manesar-Palwal expressway that connects converters to Delhi warehouses in under two hours, accelerating just-in-time shipments for e-commerce fulfillment centers. Eastern India remains under-scaled but poised for acceleration as the National Industrial Corridor Programme earmarks multimodal hubs in Odisha and West Bengal, supplying petrochemical feedstock via Paradip and Dhamra ports. Local governments court foreign investors with land-lease holidays and SGST reimbursements aimed at diversifying the India plastic packaging market’s geographic footprint.

Raw-material logistics shape cost structures: Gujarat’s adjacency to refineries shields converters from rail bottlenecks that occasionally plague northern plants relying on distant resin shipments. Tamil Nadu’s coastal sites import high-barrier EVOH and adhesive resins within 15 days from Japan, reducing inventory-financing needs. Meanwhile, states with fragmented bans on single-use plastics compel multi-plant companies to tailor packaging specs by destination, raising tooling duplication but mitigating last-mile compliance risk. Government flagship PM GatiShakti infrastructure upgrades promise synchronized planning of highways, rail, and dry ports, expected to slice average domestic freight cost from 14% to below 10% of delivered value by 2028. As connectivity tightens, the India plastic packaging market anticipates increased intra-regional competition, rewarding plants that combine cost efficiency with regulatory agility.

Competitive Landscape

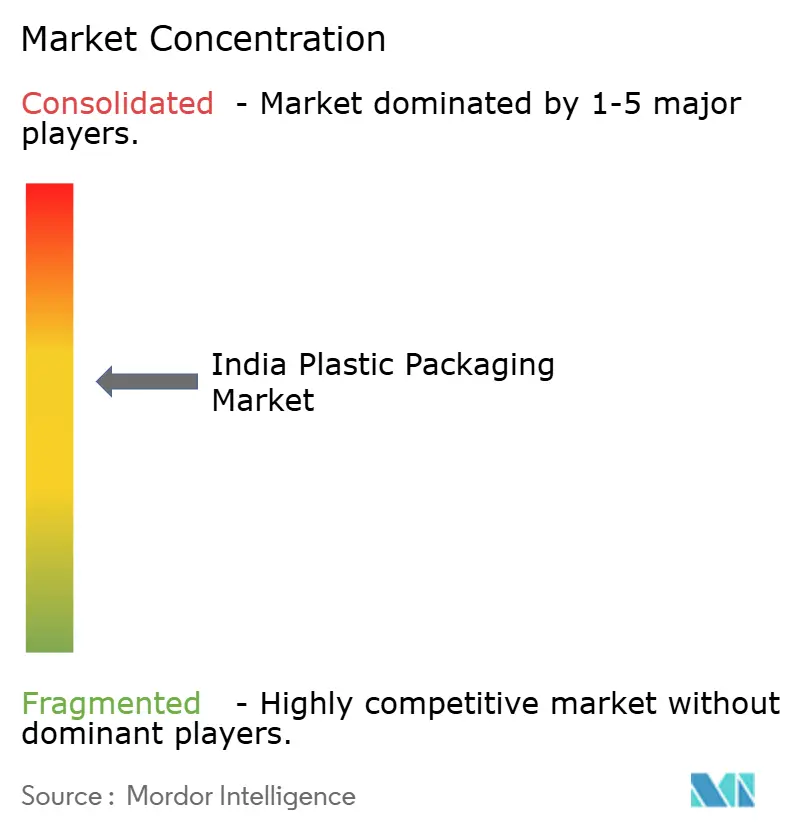

Roughly 200 organized firms operate across films, laminates, and rigid containers, yet the top 10 players control around 35% of sales, indicating moderate concentration that still leaves room for regional specialists. The November 2024 acquisition of Manjushree Technopack by PAG for nearly USD 1 billion underscores growing private-equity appetite for scalable assets in the India plastic packaging market. Consolidators prioritize vertical integration; UFlex’s 168,000 MTPA rPET chip plant in Panipat secures feedstock for its CPP and BOPET film lines, insulating margins against virgin-resin volatility. Foreign entrants like ALPLA raise competition by pledging to double domestic recycling capacity to 700,000 tonnes by 2030, leveraging global know-how and capital depth.

Technology adoption differentiates leaders. AI-enabled vision systems slash defect rates below 0.3%, boosting acceptance for high-speed sachet lines that fill 1,500 ppm in condiment plants. Patent filings around mono-material barrier structures rise 18% YoY, with Indian innovators collaborating with academic labs on plasma-coating breakthroughs that enable PE-only flexible packs to match EVOH barrier levels. Smaller firms cluster in plastic parks to share R&D and testing, pooling resources to attain BIS certification across diversified material families. Export orientation strengthens as supply-chain re-shoring in the West prompts global brands to dual-source from India; converter audits now emphasize traceability of recycled content, prompting investments in blockchain-enabled material passports. Overall, strategic plays pivot on sustainability, cost leadership, and automation, shaping a dynamic India plastic packaging market poised for selective consolidation.

India Plastic Packaging Industry Leaders

Amcor plc

UFlex Limited

Jindal Poly Films Limited

Cosmo First Limited

Polyplex Corporation Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: SIG opened an aseptic carton plant in Ahmedabad, Gujarat, with EUR 90 million (USD 106.10 million) investment and capacity for up to 4 billion packs annually, generating over 300 jobs.

- February 2025: Balrampur Chini Mills laid the foundation for an INR 2,850 crore PLA bioplastic facility in Uttar Pradesh, slated to begin operations by October 2026.

- January 2025: Canpac Trends acquired Saptagiri Packagings, adding rigid-box capacity in Hyderabad and NCR to serve FMCG customers.

- December 2024: Loop Industries and Ester Industries formed a USD 165 million recycling joint venture aiming to commercialize depolymerized DMT and MEG by early 2027.

India Plastic Packaging Market Report Scope

Plastic packaging provides a protective and informative covering while protecting the product during material handling, storage, and movement, as well as providing information about the package's content. The study tracks the demand for plastic packaging through the revenue derived from selling plastic packaging, both rigid and flexible. The study also follows the effects of regulations and market drivers on growth and factors hindering its growth.

The Indian plastic packaging market is segmented by packaging type (rigid plastic and flexible plastic), end-user (food, beverage, healthcare, personal care and household, and other end-user types), and products (bottles and jars, trays and containers, pouches, bags, films and wraps, and other product types). The market sizes and forecasts are provided in value (USD) for all the above segments.

By Material Type

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Polystyrene and EPS |

| Other Material Types |

By Packaging Type

| Flexible Plastic Packaging |

| Rigid Plastic Packaging |

By Product Form

| Bottles and Jars |

| Trays and Containers |

| Pouches and Sachets |

| Bags and Sacks |

| Films and Wraps |

| Other Product Forms |

By End-User Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

By Manufacturing Process

| Extrusion |

| Injection Molding |

| Blow Molding |

| Thermoforming |

| Other Manufacturing Processes |

| By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polystyrene and EPS | |

| Other Material Types | |

| By Packaging Type | Flexible Plastic Packaging |

| Rigid Plastic Packaging | |

| By Product Form | Bottles and Jars |

| Trays and Containers | |

| Pouches and Sachets | |

| Bags and Sacks | |

| Films and Wraps | |

| Other Product Forms | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceuticals and Healthcare | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-user Industries | |

| By Manufacturing Process | Extrusion |

| Injection Molding | |

| Blow Molding | |

| Thermoforming | |

| Other Manufacturing Processes |

Key Questions Answered in the Report

What is the current value of the India plastic packaging market?

The market is worth USD 23.13 billion in 2026 and is projected to reach USD 26.89 billion by 2031 at a 3.06% CAGR.

Which segment holds the highest share in Indian plastic packaging by material?

Polyethylene leads with 37.78% share, reflecting its cost and processing advantages.

How are EPR rules influencing packaging formats?

EPR mandates are steering converters toward recycled-content resins and creating captive demand for food-grade rPET and rHDPE.

Which region is emerging fastest for new packaging plants?

Tamil Nadu, backed by a state-funded polymer park, is attracting SMEs with plug-and-play plots and tax incentives.

What technology trend is improving production efficiency?

AI-enabled vision systems and predictive maintenance are lifting overall equipment effectiveness above 85% in leading plants.

Which end-use industry is growing quickest?

Cosmetics and personal care packaging is forecast to grow at a 4.86% CAGR through 2031 due to premiumization and sustainable-pack adoption.

Page last updated on: