India Legal Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

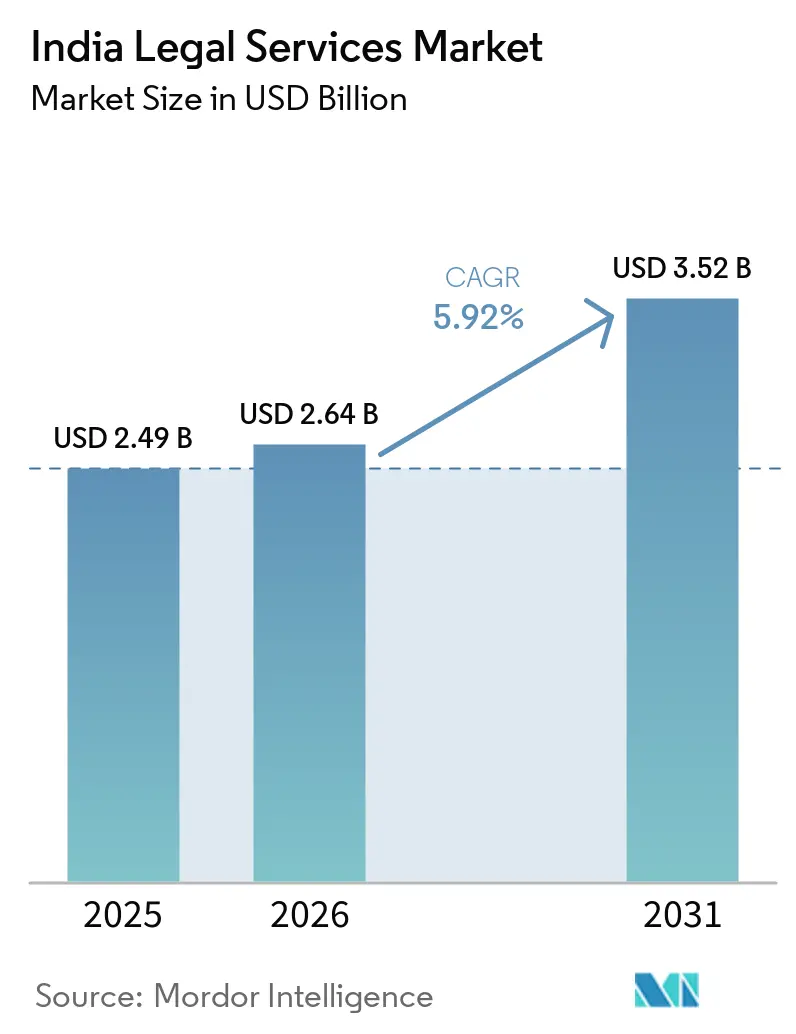

| Base Year Market Size (2025) | USD 2.49 Billion |

| Market Size (2026) | USD 2.64 Billion |

| Market Size (2031) | USD 3.52 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Legal Services Market Analysis by Mordor Intelligence

The India legal services market size was valued at USD 2.49 billion in 2025 and estimated to grow from USD 2.64 billion in 2026 to reach USD 3.52 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031). Robust FDI inflows, sweeping digital-economy regulations, and mandatory ESG disclosures are broadening the range of matters that require highly specialized counsel. Liberalized rules that allow foreign lawyers to advise on foreign law in arbitration and to appear in India-seated arbitral proceedings are expected to elevate cross-border work and bring fresh competitive pressures. At the same time, alternative legal service providers (ALSPs) and legal-technology platforms are driving new expectations around efficiency even as they open advisory niches in AI governance and process redesign. Finally, massive court backlogs are nudging corporate clients toward mediation and institutional arbitration, reinforcing demand for pre-emptive compliance guidance and sophisticated dispute-avoidance strategies.

Key Report Takeaways

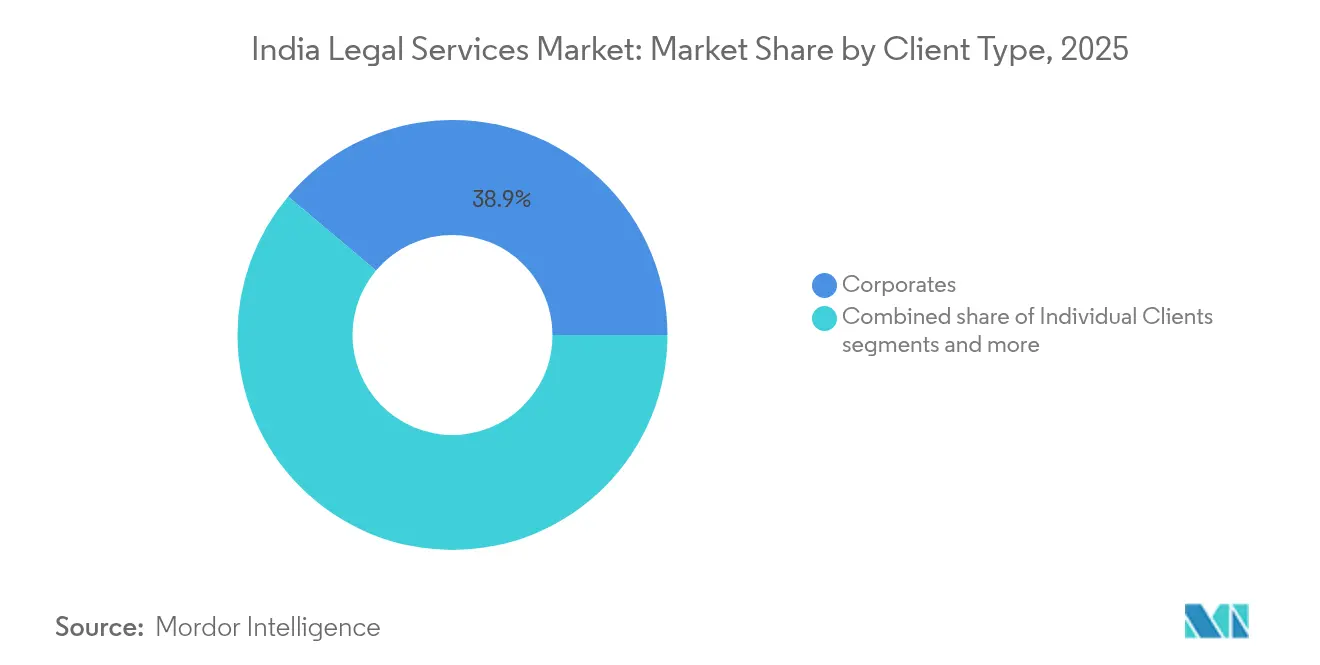

- By client type, corporates led with 38.85% of India's legal services market share in 2025, while small and medium enterprises (SMEs) are on track for the fastest 11.94% CAGR through 2031.

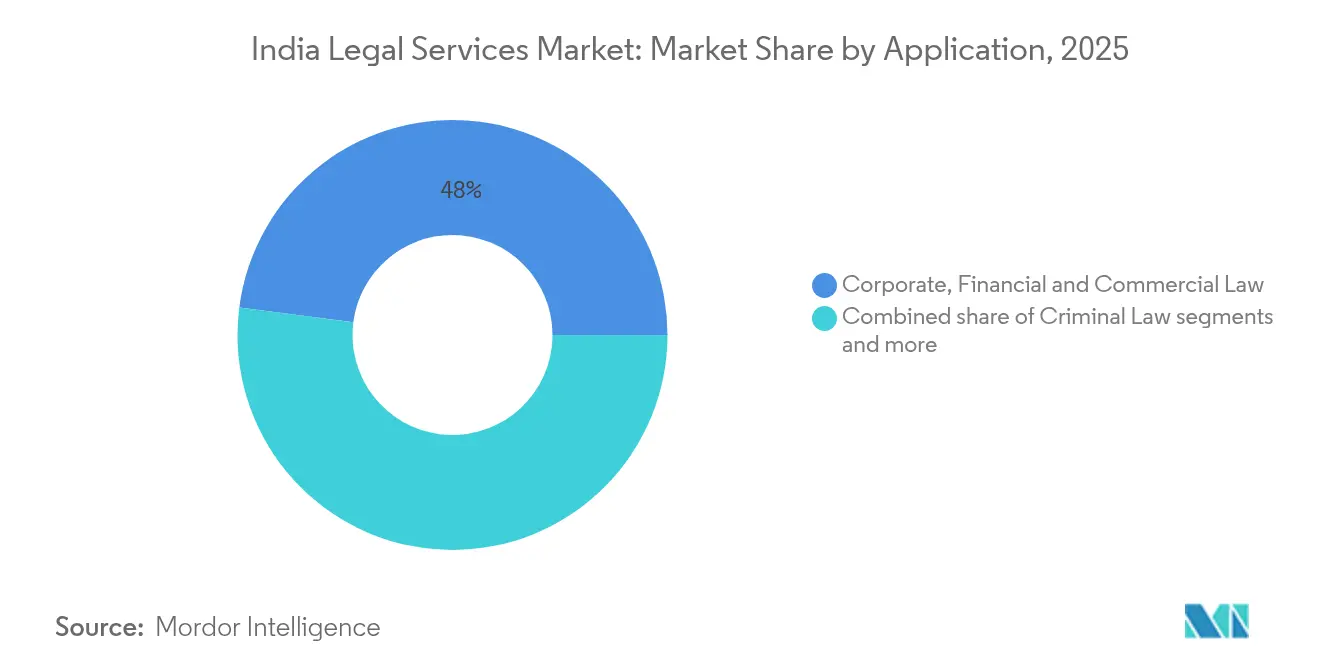

- By application, corporate, financial & commercial law held 47.95% of the India legal services market size in 2025, whereas employment & labor law is projected to grow at a 13.82% CAGR to 2031.

- By service, representation & advocacy accounted for 39.72% of the India legal services market size in 2025, while advisory & consultancy is forecast to expand at a 18.55% CAGR over the period.

- By geography, West India commanded 26.15% of India's legal services market share in 2025 and is expected to maintain the lead with an 10.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Legal Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate & M&A boom post-FDI liberalisation | +1.8% | National, with concentration in West & North India | Medium term (2-4 years) |

| Digital-first economy fuelling compliance work | +1.5% | National, with early gains in Mumbai, Bangalore, Delhi | Short term (≤ 2 years) |

| Surge in ESG & sustainability mandates | +1.2% | National, spill-over to regional centers | Medium term (2-4 years) |

| Rapid ALSP & legal-tech adoption for cost control | +0.9% | Global, with APAC core adoption | Long term (≥ 4 years) |

| Third-party litigation funding is gaining traction | +0.6% | National, with early gains in Mumbai, Delhi | Long term (≥ 4 years) |

| India-seated cross-border arbitration momentum | +0.8% | National, with concentration in Mumbai, Delhi, and GIFT City | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Corporate & M&A Boom Post-FDI Liberalization

India's inbound foreign direct investment (FDI) flows experienced significant growth in 2024, driven by policy reforms that removed sectoral caps in key industries such as insurance, defence, and single-brand retail. These regulatory changes have catalysed an increase in multi-jurisdictional transactions, which now demand comprehensive merger-control filings, meticulous tax structuring, and sector-specific regulatory approvals to ensure compliance and operational efficiency. Cross-border tie-ups, such as the proposed Honda–Nissan joint holding structure, require synchronized advice covering Press Note 3 compliance, indirect-transfer tax exposure, and global competition filings. Firms that field integrated teams across M&A, tax, and antitrust disciplines are best positioned to capture the rising pipeline. As foreign lawyers gain a limited foothold in arbitration and foreign-law advice, domestic firms are moving to cement referral partnerships and sector-focused desks to guard market share.

Digital-First Economy Fueling Compliance Work

India’s rapid digitization, from UPI payments to on-demand services, is spawning ever-denser rules on data governance, platform liability, and algorithmic accountability. The Digital Personal Data Protection Act 2023, with detailed rules due in 2025, will obligate companies to overhaul consent workflows, breach-reporting procedures, and data-processing contracts [1]Press Information Bureau, “Pendency of Cases in Indian Courts,” pib.gov.in . Revised Motor Vehicle Aggregator Guidelines further complicate compliance, as ride-sharing firms balance dynamic pricing freedom with driver-welfare metrics. Fintech regulations on digital lending and payment aggregation create continuous interpretive challenges that keep advisory pipelines full. Rather than shrinking legal spend, the uptake of AI contract-analysis tools is expanding it: enterprises retain counsel to vet training data, bias-mitigation protocols, and contractual risk allocation. Demand is therefore shifting from post-incident litigation toward preventive audits, template redesigns, and product-launch clearances.

Surge in ESG & Sustainability Mandates

The Securities and Exchange Board of India now requires the top 1,000 listed companies to file granular Business Responsibility and Sustainability Reports that detail climate exposure, supply-chain diligence, and board oversight[2]Securities and Exchange Board of India, “Business Responsibility and Sustainability Reporting Framework,” sebi.gov.in . Parallel proposals to widen mandatory CSR outlays under the Companies Act will pull thousands of mid-caps into the compliance net. International investors are pressing Indian issuers to align with EU taxonomy criteria, spawning multi-jurisdictional advisory work on disclosure mapping and green-bond frameworks. Contract clauses are spreading upstream to vendors, compelling rigorous human-rights and environmental audits that few suppliers can navigate alone. Legal advisory now straddles ESG reporting, climate-risk disclaimers, and board-training modules, converting what was once volunteerism into revenue-generating compliance mandates.

Rapid ALSP & Legal-Tech Adoption for Cost Control

Cost-conscious clients are experimenting with ALSPs that blend process engineers, legal project managers, and AI-enabled review stacks. QuisLex’s integration of a generative-AI contract platform illustrates how outsourced review is moving up the value chain [3]Reserve Bank of India, “Master Directions on Digital Lending 2025,” rbi.org.in . Leading domestic firms are responding with captive innovation cells; Trilegal’s Digital Innovation Group, for example, is piloting automated clause-bank generators and predictive analytics for case-strategy design. These shifts are not displacing lawyers but are instead prompting fresh advisory needs around technology procurement, data-transfer agreements, and professional-ethics guardrails. Over time, firms that master hybrid delivery—combining bespoke counsel with scalable tech workflows—stand to win share in the India legal services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Court backlog & slow dispute resolution | -1.4% | National, with acute impact in North & East India | Long term (≥ 4 years) |

| Regulatory uncertainty on foreign-firm rules | -0.8% | National, with concentration in Mumbai, Delhi | Short term (≤ 2 years) |

| Downward fee pressure from price-sensitive clients | -1.1% | National, with regional variations | Medium term (2-4 years) |

| Talent crunch in specialised practice areas | -0.9% | National, with acute shortages in tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Court Backlog & Slow Dispute Resolution

India’s courts are grappling with more than 50 million pending cases, including 62,000 matters older than 30 years in the high courts, a logjam that depresses the effective value of litigation and prolongs receivables cycles for claimants[4]QuisLex, “AI-Enabled Contract Review Enhancements,” quislex.com . Supreme Court congestion—hovering near 80,000 cases—further pushes corporates toward arbitration and pre-institution mediation. While the Mediation Act 2023 and digitized filing systems offer incremental relief, chronic understaffing and infrastructure gaps in tier-2 cities remain. The resulting time-value erosion of claims curtails appetite for large contentious matters and shifts spend toward earlier-stage risk-mitigation reviews. Although ADR work partially offsets the lost litigation income, the negative net effect trims overall growth potential for the India legal services market.

Regulatory Uncertainty on Foreign-Firm Rules

The Bar Council of India’s 2025 guidelines allowing foreign lawyers to advise on foreign law and participate in arbitration have yet to yield detailed registration steps, reciprocity criteria, or fee-sharing boundaries. Baker McKenzie’s public statement that it will open only after procedural clarity underscores the caution of international players. Domestic firms, meanwhile, are unsure whether joint ventures or alliance models will satisfy the reciprocity test, stalling investment decisions in technology and talent. Clients with pan-Asian operations, therefore, face a patchwork: they must split mandates between Indian counsel for local law and foreign counsel for offshore elements, adding coordination costs. Until the implementing framework solidifies, the uncertainty will mildly dampen the otherwise positive liberalization impact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Client Type: Corporate Dominance Drives SME Acceleration

Corporates accounted for 38.85% of India's legal services market share in 2025, reflecting their deep and recurring need for transaction support, regulatory filings, and sophisticated dispute management. SMEs are nonetheless projected to post a 11.94% CAGR, buoyed by mandatory GST registration, data-protection obligations, and mainstream ESG reporting that pull even smaller entities into the formal economy. Many mid-market companies are migrating from ad-hoc local counsel to structured retainers, prompting firms to craft tiered service packages and cloud-based subscription platforms. Individual clients continue to seek advice on property transfers, succession planning, and personal litigation, but fee sensitivity in this cohort caps revenue upside. Government and public-sector undertakings represent episodic opportunities tied to procurement cycles and infrastructure pushes, yet payment delays and rigid fee schedules temper profitability.

The divergence between stable corporate mandates and fast-growing SME work compels firms to balance bespoke partner-led teams with process-driven delivery pods. Corporate legal departments increasingly demand outcome-based pricing that pushes law firms to adopt project-management toolkits. In parallel, SMEs prefer fixed-fee compliance bundles, and AI-enabled document-generation platforms facilitate their rapid onboarding. Firms that can scale without diluting quality will capture the incremental volumes that SMEs bring to the India legal services market. Talent allocation is also evolving associates rotate between high-margin M&A deals and volume-driven SME compliance tasks, broadening skill sets while sustaining utilization rates.

By Application: Employment Law Disrupts Traditional Hierarchies

In 2025, the corporate, financial, and commercial law segment accounted for 47.95% of the Indian legal services market. This dominance was driven by sustained mergers and acquisitions activity, increased private equity exits, and evolving regulatory frameworks within the banking and insurance industries. Yet employment & labour law is on course to outpace every other segment with a 13.82% CAGR through 2031, catalysed by gig-economy classification battles, revised wage-code rules, and expanding workplace-safety mandates. The Bharatiya Nagarik Suraksha Sanhita and updated sexual-harassment guidelines now require continuous policy refreshes, nudging boards to allocate larger budgets for HR-focused counsel. Intellectual property and technology law are also growing as digital product launches spike demand for patent filings and software license negotiations.

Cross-pollination among practice areas is becoming routine: employment lawyers coordinate with data-privacy specialists on workplace-monitoring policies, while ESG teams consult tax advisers on green-investments structuring. Real-estate related mandates are recovering in step with manufacturing expansion under the Production-Linked Incentive scheme. Criminal-law work remains largely confined to white-collar defense, but drawn-out trial timelines limit fee velocity. As clients consolidate panels, firms that deliver integrated, cross-practice advice stand to earn larger wallet share within the India legal services market.

By Service: Advisory Consultancy Outpaces Traditional Advocacy

Representation & advocacy still commanded 39.72% of the India legal services market size in 2025 because litigation and arbitration retain marquee status in complex disputes. Nevertheless, advisory & consultancy is forecast to clock a 18.55% CAGR through 2031 as boards shift resources toward preventive compliance audits and regulatory impact assessments. Taxation services enjoy stable demand, propelled by GST classification controversies and transfer-pricing audits. Bankruptcy and restructuring work tends to spike during economic downturns, but resolution timelines under the Insolvency and Bankruptcy Code have lengthened, tempering revenue realization. Notarial and certification services are benefiting from e-stamp modules and remote authentication, generating steady if modest inflows.

The swing toward advisory mandates is sharpening the industry’s focus on knowledge management and sector specialization. Law firms now invest in domain libraries, automated template suites, and contract analytics dashboards to expedite turnaround times. Clients evaluate proposals on both legal depth and process sophistication, favouring teams that can couple domain insight with data-driven workflow mapping. As a result, representation practices are integrating litigation-readiness assessments into every major transaction review, enhancing cross-sell opportunities and anchoring client relationships within the India legal services market.

Geography Analysis

West India led the pack with 26.15% of India's legal services market share in 2025 and is set to maintain the fastest 10.96% CAGR through 2031, a trajectory powered by Mumbai’s status as financial capital and by GIFT City’s rise as an international financial services hub. Regulatory density, housing the Reserve Bank of India, SEBI, and the Insurance Regulatory and Development Authority, creates a constant stream of compliance work. International arbitration centres in Mumbai are attracting cross-border disputes that historically migrated to Singapore or London, reinforcing demand for complex advocacy and foreign-law coordination. Gujarat’s focus on green energy and port-led development is another growth vector that needs project-finance structuring and environmental approvals. Law firms in the region are therefore beefing up multidisciplinary benches that blend capital markets, infrastructure, and arbitration expertise to capture upstream and downstream mandates of large deals.

North India ranks second, anchored by Delhi’s proximity to federal ministries and apex courts, which produces a steady flow of policy-interpretation assignments and constitutional litigation. The National Capital Region’s sprawling corporate base drives regular company-law, real estate, and employment mandates, while public-sector undertakings retain counsel for infrastructure tenders and dispute-board proceedings. Although Uttar Pradesh’s industrial corridors are expanding, payment cycles remain elongated, which deters smaller firms from aggressive entry. South India capitalizes on Bangalore’s tech ecosystem and Chennai’s manufacturing footprint, generating a robust pipeline in data privacy, IP, and cross-border supply-chain contracts. Regional universities churn out a steady talent pool, reducing onboarding costs for local offices.

East and Central India together account for a smaller slice of the India legal services market but offer upside through coal, steel, and infrastructure projects that require land-acquisition clearances and environmental-impact evaluations. Judicial infrastructure, however, is thinner, and practitioners often commute to metro courts for complex matters, inflating client expenses. North-East India is still an emerging market, yet cross-border trade agreements with Bangladesh and Myanmar are birthing mandates in customs law, logistics contracts, and special-economic-zone compliance. Collectively, these variations underscore why geography-led strategies, such as satellite offices and virtual-courtroom capabilities, are becoming decisive in shaping competitive advantage.

Competitive Landscape

The India legal services market is moderately fragmented: the top five firms together hold more than one-fourth share, leaving ample room for mid-tier specialists and tech-enabled disruptors. Traditional full-service leaders such as Cyril Amarchand Mangaldas, AZB & Partners, and Khaitan & Co. are doubling down on sector-focused task forces that integrate M&A, tax, and antitrust advice to defend their benches. Aggressive lateral hiring remains the favoured tactic, with partner compensation for niche practices like ESG and data privacy spiking to retain rainmakers. Baker McKenzie and other global giants are positioning to enter once reciprocity rules are clarified, a move that could rearrange referral networks and put pricing pressure on outbound-work premiums.

The deployment of generative AI research tools by Trilegal has streamlined memo-drafting processes, significantly reducing the average time required for completion. This operational efficiency has enabled the firm to reallocate resources toward higher-margin advisory services, enhancing overall productivity and profitability. QuisLex and other ALSPs continue to chip away at commoditized tasks by blending Six-Sigma workflows with AI-assisted review, prompting traditional firms to repackage due diligence offerings as managed services modules. Contract-lifecycle-management vendors like SpotDraft are partnering with in-house teams to automate playbooks, thereby reducing routine external spend and pushing law firms to compete on complex problem-solving rather than volume review.

Strategic white space abounds in ESG, international arbitration, and technology-risk advisory areas, where client demand is outpacing trained talent supply. Mid-sized boutiques that offer deep domain expertise without large-firm overhead are seizing marquee mandates, particularly in renewable-energy finance and fintech regulation. Meanwhile, court backlogs are tilting the revenue mix away from contested matters toward pre-emptive compliance strategies, compelling litigation-heavy firms to diversify. Overall, competitive intensity is rising, but the market’s breadth ensures multiple growth paths—from regional expansion to sector specialization—within the India legal services market.

India Legal Services Industry Leaders

Cyril Amarchand Mangaldas

Khaitan & Co.

AZB & Partners

Shardul Amarchand Mangaldas & Co.

JSA Advocates & Solicitors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nishith Desai Associates published a comprehensive analysis of the proposed Honda–Nissan joint holding company, underscoring multi-disciplinary demand across competition, tax, and FDI compliance work.

- November 2024: Trilegal announced a collaboration with Lucio AI to embed generative AI tools across knowledge-management and document-review workflows.

- July 2024: Baker McKenzie confirmed its intent to establish an India office once Bar Council registration rules are finalized, signaling renewed foreign-firm interest in direct market participation.

- May 2024: QuisLex expanded its partnership with ContractPodAi, integrating a generative-AI module to accelerate contract-lifecycle management tasks.

India Legal Services Market Report Scope

Legal services, provided by lawyers and legal professionals, assist individuals, businesses, and organizations in navigating legal complexities and ensuring law compliance. These services include contract advice, court representation, and document assistance. Lawyers often specialize in family, real estate, or criminal law, tailoring their expertise to specific needs. Legal services uphold justice, safeguard rights, and resolve disputes within the legal framework. Access to these services ensures legal guidance, protection, and resolution, fostering a fair and orderly society.

The Indian legal services market is segmented by end user, application, and service. By end user, the market is segmented into legal aid consumers, private consumers, SMEs, charities, large businesses, and government. By application, the market is segmented into corporate, financial, and commercial law, personal injury, commercial and residential property, wills, trusts, and probate, family law, employment law, and criminal law. By service, the market is segmented into representation, taxation, litigation, bankruptcy, advice, notarial activities, and research. The report offers market size and forecasts in terms of value (USD) for all the above segments.

| Corporates |

| Small and Medium Enterprises (SMEs) |

| Individual Clients |

| Government and Public Sector |

| Corporate, Financial, and Commercial Law |

| Real Estate and Property Law |

| Family and Personal Law |

| Employment and Labor Law |

| Criminal Law |

| Intellectual Property and Technology Law |

| Dispute Resolution and ADR |

| Taxation and Regulatory Law |

| Representation and Advocacy |

| Taxation Services |

| Advisory and Consultancy |

| Bankruptcy and Restructuring |

| Notarial and Certification Services |

| Legal Research and Documentation |

| North India |

| South India |

| West India |

| East India |

| Central India |

| North-East India |

| By Client Type | Corporates |

| Small and Medium Enterprises (SMEs) | |

| Individual Clients | |

| Government and Public Sector | |

| By Application | Corporate, Financial, and Commercial Law |

| Real Estate and Property Law | |

| Family and Personal Law | |

| Employment and Labor Law | |

| Criminal Law | |

| Intellectual Property and Technology Law | |

| Dispute Resolution and ADR | |

| Taxation and Regulatory Law | |

| By Service | Representation and Advocacy |

| Taxation Services | |

| Advisory and Consultancy | |

| Bankruptcy and Restructuring | |

| Notarial and Certification Services | |

| Legal Research and Documentation | |

| By Geography | North India |

| South India | |

| West India | |

| East India | |

| Central India | |

| North-East India |

Key Questions Answered in the Report

How large is the India legal services market in 2026?

India Legal Services Market Size valued at USD 2.64 billion in 2026 and is projected to grow to USD 3.52 billion by 2031.

What is the main growth driver for legal services in India?

Expanding FDI-driven M&A transactions, combined with new data-protection and ESG regulations, are driving sustained demand.

Which service segment is growing the fastest?

Advisory & consultancy services are forecast to expand at a 18.55% CAGR through 2031 due to rising compliance complexity.

Why is West India the largest regional market?

Mumbai’s concentration of financial regulators, arbitration centres, and multinational headquarters gives West India a 26.15% share and the fastest 10.96% CAGR.

How will foreign-lawyer liberalization affect competition?

Limited entry for foreign lawyers will intensify rivalry in cross-border arbitration and transactional work, motivating domestic firms to deepen sector expertise.

What technological trends are reshaping service delivery?

Generative-AI tools for document review and contract analytics, along with ALSP process-engineering models, are elevating efficiency expectations across client segments.

Page last updated on: