Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

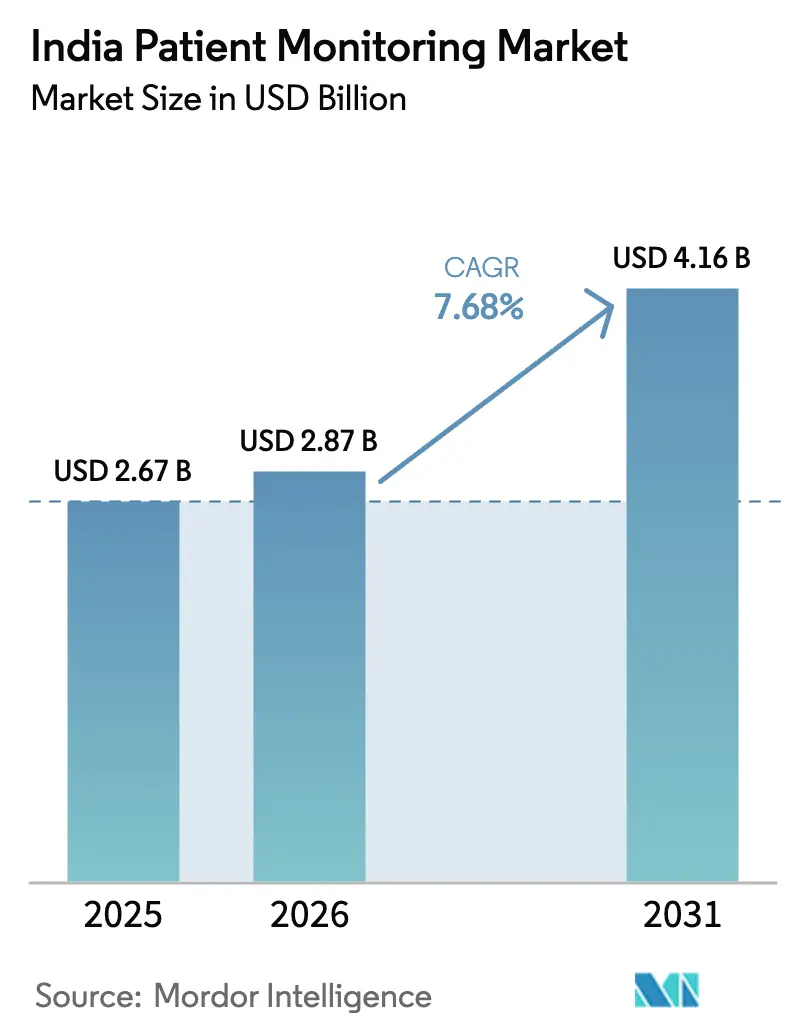

| Base Year Market Size (2025) | USD 2.67 Billion |

| Market Size (2026) | USD 2.87 Billion |

| Market Size (2031) | USD 4.16 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Patient Monitoring Market Analysis by Mordor Intelligence

The India Patient Monitoring Market size is expected to increase from USD 2.67 billion in 2025 to USD 2.87 billion in 2026 and reach USD 4.16 billion by 2031, growing at a CAGR of 7.68% over 2026-2031.

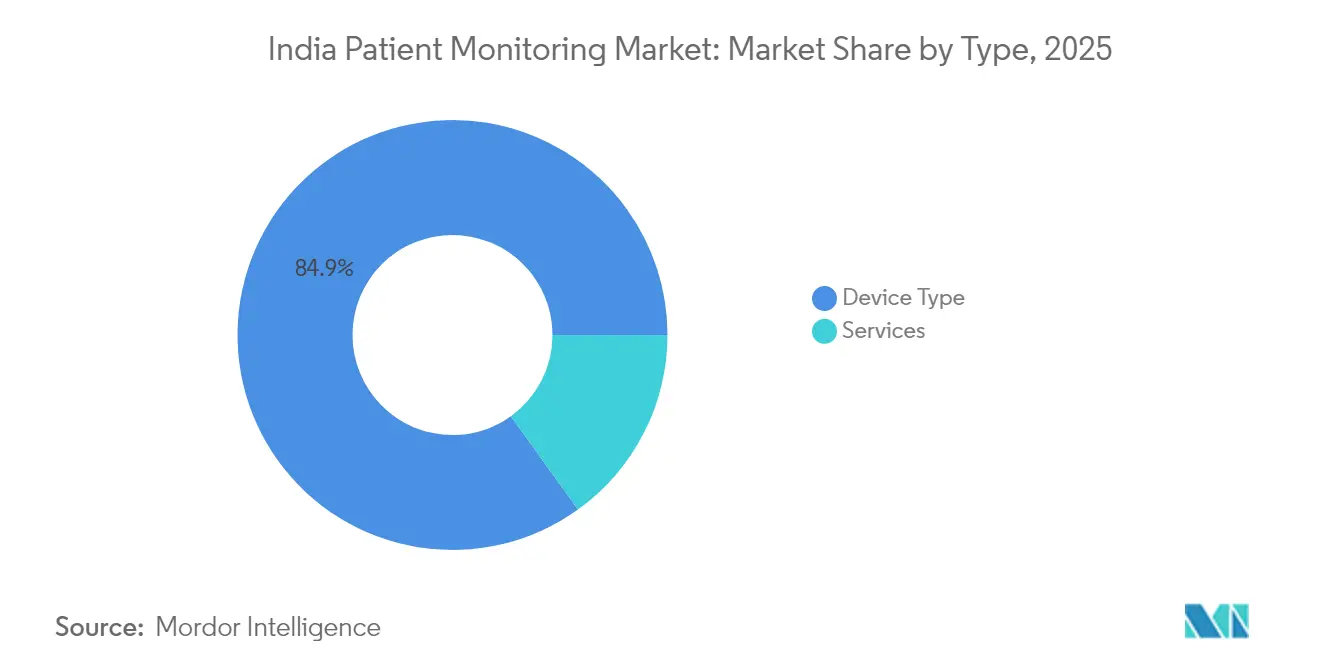

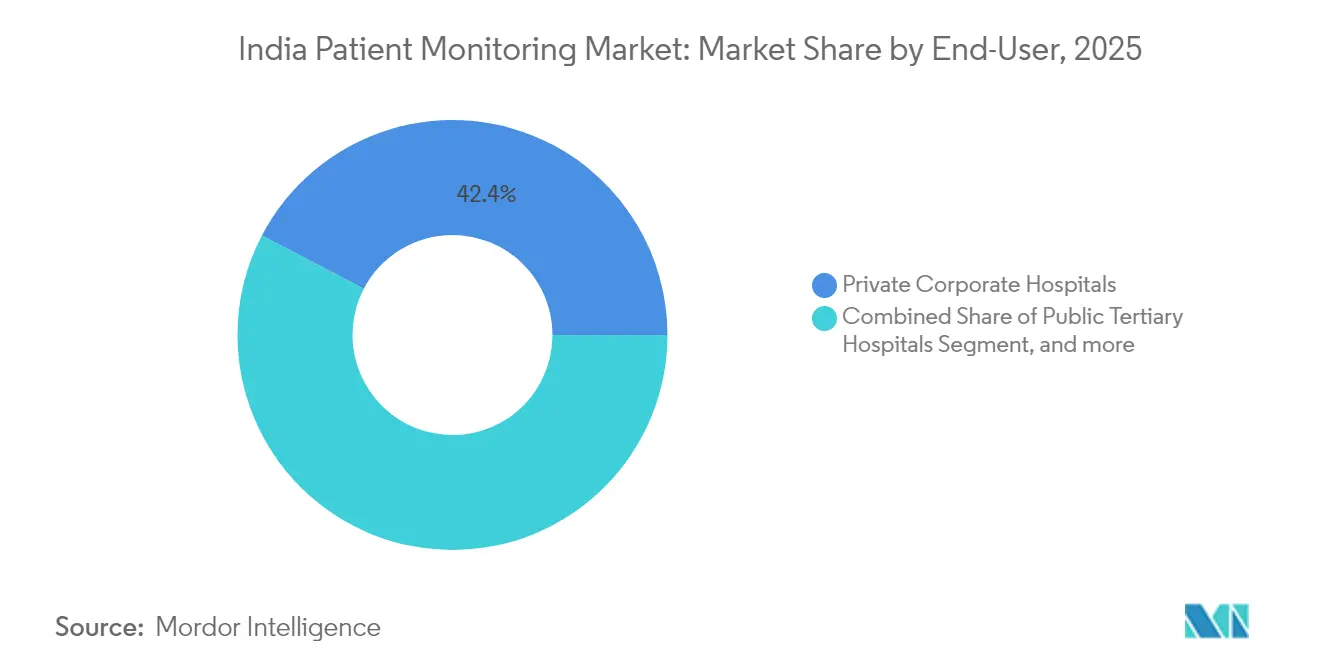

Growth is supported by rising chronic disease prevalence, with more than 100 million adults living with diabetes and a very large hypertensive population that depends on regular vital-signs surveillance across hospital and home settings. Devices account for 85.43% of revenue while services expand at 9.67% CAGR as providers adopt managed monitoring and integration services aligned with national digital health rails. Private corporate hospitals lead adoption with 42.82% share while home-healthcare providers post the fastest expansion at 9.98% CAGR due to government telehealth pilots and falling sensor prices. Policy levers like the Production Linked Incentive scheme and the Ayushman Bharat Digital Mission are enabling local manufacturing and interoperability that lower costs and ease cross-platform data exchange.

Key Report Takeaways

- By type, devices led with 84.92% revenue share in 2025. Services are forecast to expand at a 9.21% CAGR through 2031.

- By end-user, private corporate hospitals held 42.35% share in 2025. Home-healthcare providers are projected to record the highest CAGR at 9.44% through 2031.

- By application, cardiology accounted for a 28.74% share in 2025. Neurology monitoring is expected to be the fastest-growing application at a 9.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Patient Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic disease burden | +2.1% | Pan-India, concentrated in urban centers and tier-1 cities | Long term (≥ 4 years) |

| Expansion of telehealth programs and reimbursement pilots | +1.8% | National, early gains in Karnataka, Telangana, Maharashtra | Medium term (2-4 years) |

| Government PLI and med-tech clusters accelerate local manufacturing | +1.5% | Manufacturing hubs in Tamil Nadu, Karnataka, Andhra Pradesh | Medium term (2-4 years) |

| Shift to hospital-at-home, virtual ICUs, and connected beds in private chains | +1.3% | Metro cities, Delhi NCR, Mumbai, Bangalore, Hyderabad | Short term (≤ 2 years) |

| Growing adoption of AI-powered analytics in monitoring workflows | +0.9% | Private corporate hospitals in tier-1 cities, select public tertiary centers | Medium term (2-4 years) |

| Rapid penetration of low-cost wearables and India-first sensors enabling RPM at scale | +1.2% | Pan-India, strongest in semi-urban and rural catchments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Burden

India’s diabetes and hypertension prevalence is shifting episodic care toward continuous monitoring at home and in hospitals. Over 100 million adults live with diabetes and a very large hypertensive population remains undertreated, which sustains demand for home BP monitors and sensor-based glucose tracking. Cardiovascular disease contributes a significant share of national mortality, prompting tertiary hospitals to upgrade with multiparameter monitors that extend surveillance beyond manual rounds. Private corporate hospitals are deploying connected beds that integrate ECG, pulse oximetry, and scales into dashboards that help teams intervene earlier. Post-discharge cardiology and diabetes pathways increasingly rely on remote patient monitoring kits to flag arrhythmias and glucose excursions in real time. These patterns reinforce an always-on approach that supports the India patient monitoring market as chronic conditions intensify in urban and peri-urban populations.

Expansion of Telehealth Programs and Reimbursement Pilots

The Ayushman Bharat Digital Mission has created digital identities and consent rails at national scale, and several states are piloting RPM reimbursement under public insurance[1]Editorial Team, “National Digital Health Ecosystem,” National Health Authority, abdm.gov.in. Karnataka, Telangana, and Maharashtra operate pilots that reimburse virtual visits linked to device-submitted vitals, creating a funding path that did not exist before 2024. The National Health Authority is evaluating bundled chronic-care payments that include Bluetooth-enabled BP cuffs and glucometers for primary-care clinics. Platform companies integrating devices with teleconsultation workflows are offering subscription RPM packages to improve adherence and continuity of care. Although state-by-state fee schedules differ, new payment models are paving the way for wider routine monitoring and boosting the India patient monitoring market over the medium term.

Government PLI and Med-Tech Clusters Accelerate Local Manufacturing

The PLI program for medical devices expanded in 2024 and includes patient monitors, with approved manufacturers committing INR 12 billion (USD 145 million) to scale domestic capacity. Med-tech clusters in Tamil Nadu, Karnataka, and Andhra Pradesh are drawing contract manufacturers that assemble multiparameter monitors for India and export markets, which reduces landed costs compared with fully imported systems. Local firms are increasing output to address public tenders that prefer higher domestic content, aligned with Make in India procurement norms[2]Editorial Team, “Public Procurement Preference for Make in India,” Department for Promotion of Industry and Internal Trade, dpiit.gov.in. Capital subsidies are enabling investments in calibration lines and compliant production environments to meet ISO 13485 and IEC 60601 quality and safety standards. Shorter lead times and better serviceability strengthen provider confidence and ease lifecycle costs, which supports sustained adoption in the India patient monitoring market.

Shift to Hospital-At-Home, Virtual ICUs, and Connected Beds in Private Chains

Large private chains expanded hospital-at-home and virtual ICU programs in 2024 and 2025, routing real-time vitals to centralized command centers for triage. Apollo scaled remote monitoring for post-surgical and chronic patients across major metros, while Manipal piloted central oversight of multiple monitored beds across campuses. Fortis deployed connected monitors that write vitals directly into its HIMS to reduce manual data entry and improve auditability of care. These models unlock bed capacity by moving stable cases home while maintaining clinical vigilance, although they require resilient connectivity and round-the-clock tech support. As adoption spreads in tier-1 cities, these workflows normalize continuous monitoring outside the ICU and support recurring services revenue across the India patient monitoring market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin |

|---|---|---|---|

| High import dependency and forex volatility for electronics and components | -0.8% | National, acute for manufacturers reliant on semiconductor imports | Short term (≤ 2 years) |

| Fragmented state procurement and tendering complexity | -0.6% | Pan-India, most severe in decentralized states such as Uttar Pradesh, Bihar, Rajasthan | Medium term (2-4 years) |

| Low physician adoption of home BP and RPM protocols in primary care | -0.5% | Tier-2 and tier-3 cities, rural primary health centers | Long term (≥ 4 years) |

| Data-privacy and device-EHR or HIMS integration gaps versus ABDM consent rails | -0.4% | National, most pronounced in private hospitals with legacy HIMS | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Import Dependency and Forex Volatility for Electronics/Components

Despite policy support, most monitors still depend on imported semiconductors, sensor modules, and displays, which raises exposure to currency swings and supply risk. The rupee near INR 83 per USD in 2025 raises landed costs of critical components and narrows margins for smaller manufacturers that cannot hedge or secure long-term pricing[3]Editorial Team, “Foreign Exchange Rates,” Reserve Bank of India, rbi.org.in. Specialty analog front-ends and high-resolution TFT components remain concentrated in East Asian supply chains, keeping domestic makers reliant on external suppliers. Public procurement that prioritizes lowest price complicates pass-through of cost increases, especially for vendors lacking scale to absorb volatility. Plans for local semiconductor capacity are advancing, yet commercial-scale output will take time to stabilize upstream supply for patient monitoring.

Fragmented State Procurement and Tendering Complexity

Procurement is managed across 28 states and several union territories, each with distinct tender rules, content requirements, and bid evaluation processes. Vendors often prepare separate bids on different state portals, which raises compliance effort and legal review costs. Divergent local-content thresholds drive multiple bill-of-material configurations to qualify across states. Long and inconsistent evaluation timelines delay awards, which strains working capital for smaller innovators. Non-standard specifications can result in approvals in one state and disqualifications in another on features not articulated upfront, which increases market-entry uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Devices Dominate, Services Surge on Managed-Monitoring Demand

Devices captured 84.92% of revenue in 2025, and services are expanding at 9.21% CAGR through 2031, underscoring a shift toward managed operations and analytics. Multiparameter vital-signs monitors remain the workhorse across ICUs and operating rooms, with replacement cycles favoring connectivity and centralized alarm management. Cardiac monitoring, including Holter and event recorders, is expanding among urban cardiologists for outpatient arrhythmia workups supported by rapid interpretation. Respiratory devices such as pulse oximeters, capnographs, and spirometers maintain elevated use given persistent COPD and asthma burdens and the emphasis on perioperative safety. Fetal and neonatal monitoring continues to build in tertiary maternity centers while neonatal ICU capacity in tier-2 cities increases the installed base. Neuro-monitoring and hemodynamic sensors gain traction in trauma and critical care, while wearable patches and contactless sensors are the fastest-growing form factors as clinical-grade consumer wearables converge with care delivery.

Services are gaining share as hospitals pursue continuous oversight without expanding onsite headcount, and as providers prioritize interoperability, analytics, and uptime. Remote monitoring and telehealth services benefit from reimbursement pilots that package devices and clinician review into per-member payments. Data-integration and interoperability services are critical for bridging device protocols with ABDM-aligned exchanges and hospital HIMS, which requires custom middleware development. Managed-monitoring operations staffed by nurses and respiratory therapists triage alarms across sites to improve response times and standardize workflows. Training services remain underpenetrated, and structured programs for alarm management and artifact recognition could reduce false alerts and improve frontline confidence across the India patient monitoring industry.

By End-User: Private Corporate Hospitals Lead, Home-Healthcare Providers Accelerate

Private corporate hospitals held 42.35% in 2025 supported by multi-hospital networks, standardized platforms, and investments in connected ICU ecosystems. Chains standardize on integrated platforms linking monitors, infusion devices, and ventilators into central dashboards to reduce ICU length of stay. Public tertiary hospitals drive meaningful volumes through centralized procurement and capacity additions, though budget limits can delay adoption of higher-end analytics. Specialty clinics deploy targeted monitoring for dialysis, cardiology, and sleep medicine with strong price sensitivity. Ambulatory surgical centers expand monitored recovery bays to meet accreditation and safety standards that favor continuous surveillance until discharge readiness.

Home-healthcare providers are the fastest-growing end-users with a 9.44% CAGR projected through 2031, helped by aging demographics and telehealth normalization. Providers equip field teams with portable monitors and distribute RPM kits for post-discharge care and long-term chronic programs supported by 24/7 triage centers. Reimbursement pilots under public schemes test per-member payments that bundle devices and monitoring, which expands beyond pure out-of-pocket models. Policy clarity for device licensing and provider distribution continues to evolve under CDSCO, and broadband gaps in smaller cities remain an adoption constraint. As workflows mature, managed RPM operations and clear escalation protocols are becoming standard in the India patient monitoring industry.

By Application: Cardiology Dominates, Neurology Monitoring Surges on Trauma-Care Upgrades

Cardiology led with 28.74% in 2025, reflecting a heavy burden of ischemic heart disease and stroke and the need for continuous ECG telemetry and post-procedural surveillance. Outpatient diagnostics using Holter and event recorders expand access to rhythm analysis and speed treatment decisions in metro and tier-2 settings. Remote ECG services that transmit 12-lead strips to specialists are widening access to expert interpretation outside major centers. Respiratory monitoring demand remains steady due to COPD, asthma, and perioperative safety protocols that mandate oxygenation and ventilation oversight. Critical-care applications span organ systems around multiparameter monitoring as the standard of care for hemodynamic surveillance.

Neurology monitoring is the fastest-growing application with a 9.08% CAGR expected through 2031 as trauma centers add intracranial pressure monitoring, EEG, and cerebral oximetry. National traffic safety initiatives emphasize faster trauma response, which drives installations along major roadway corridors to manage head injuries quickly. AI-assisted seizure detection on continuous EEG is being piloted in epilepsy units to reduce false positives and speed interventions. Diabetes and metabolic monitoring grows with sensor-based care pathways, although uptake is concentrated among urban patients with higher willingness to pay. Maternal and neonatal monitoring receives support under national programs to reduce maternal and infant mortality, with more labor-room and NICU monitoring in district hospitals.

Geography Analysis

Tier-1 metros in Maharashtra, Karnataka, and Tamil Nadu account for more than half of 2025 patient monitoring devices market revenue, underpinned by dense private hospital networks and early adopter culture. Bengaluru’s tech ecosystem attracts AI start-ups that pilot algorithms inside corporate chains, while Chennai’s medical-tourism hub upgrades ICUs to meet Joint Commission standards. Gujarat leverages its manufacturing base and PLI designations to localize supply, shortening delivery lead times and lowering landed cost for regional buyers.

Tier-2 cities such as Jaipur, Lucknow, and Coimbatore post double-digit growth as insurers expand cashless coverage to middle-income cohorts. Providers here prefer portable monitors that can shuttle between wards and outreach camps, favoring vendors with strong field support. The patient monitoring devices market size in rural clusters remains modest yet strategic: community health officers use tablet-linked pulse oximeters under national screening programs, planting early seeds for upgrade cycles.

Inter-state variability in digital infrastructure influences adoption velocity. States with robust fiber connectivity integrate cloud dashboards smoothly, whereas low-bandwidth districts rely on store-and-forward uploads. Central government programs subsidize 4G towers in aspirational districts, gradually erasing this divide. Cumulatively these dynamics allow the patient monitoring devices market to expand south and west initially, then radiate to northern hinterlands by the decade’s end.

Competitive Landscape

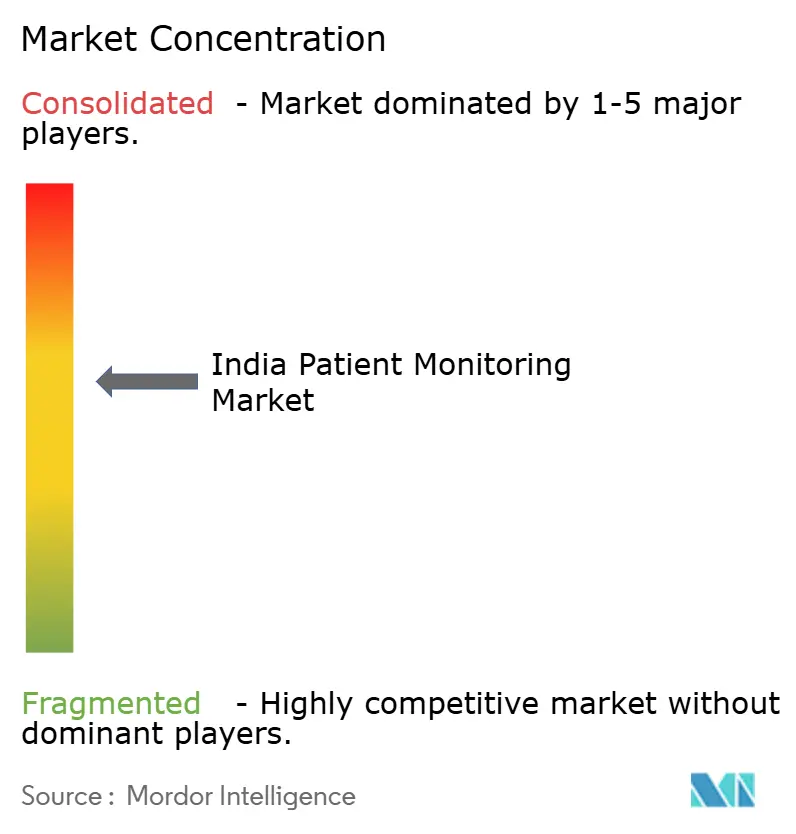

The India patient monitoring market shows moderate concentration with multinational incumbents such as GE HealthCare, Philips, Medtronic, Dräger, and Nihon Kohden competing alongside India-first innovators. Multinationals benefit from brand equity and installed-base lock-in through central stations and interoperability layers that shape upgrade paths. Domestic firms win tenders by meeting local-content norms and bundling training and multi-year maintenance services that align with public procurement requirements. Startups differentiate with form factors such as contactless sensors and portable kiosks that fit resource-constrained settings and scale through pilot-to-contract models.

Emerging disruptors are bundling devices, teleconsultation, and AI coaching in subscription models with insurer and employer partnerships to build recurring revenue. Data and analytics capabilities are a battleground as vendors seek to monetize early-warning and trend predictions beyond hardware margins. Strategic moves include platform launches that bridge bedside to home settings, capacity expansions under PLI, and co-development partnerships targeting open architectures for tier-2 and tier-3 hospitals. Multinationals held about 50% of the India patient monitoring market share in 2024, yet their premium pricing faces pressure from local substitutes that leverage frugal engineering and shorter service cycles.

Evidence generation is rising in importance as software-as-a-medical-device and AI models seek clearer validation in Indian settings under regulatory oversight. Providers favor solutions proven to integrate with ABDM consent flows and HIMS while reducing false alarms and clinician workload. As supply chains localize and analytics mature, competition is shifting from box sales to outcomes and uptime, reinforcing managed services and lifecycle support as differentiators in the India patient monitoring market.

Competition is shifting from hardware to data platforms. Vendors monetize analytics subscriptions that flag risk scores, while open APIs encourage third-party app ecosystems. Compliance with CDSCO’s Medical Device Rules 2017 has become a gatekeeper, favoring firms with robust quality systems. As PLI subsidies mature, more multinationals are localizing assembly to match domestic price points, pushing incumbents to differentiate via AI and workflow integration rather than pure capital equipment.

India Patient Monitoring Industry Leaders

BPL Group

Koninklijke Philips N.V.

GE Healthcare

Nihon Kohden Corporation

Mindray Medical International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Abu Dhabi Investment Authority pledged USD 200 million for a 3% stake in Meril Life Sciences, valuing the firm at USD 6.6 billion and signaling global confidence in Indian med-tech

- March 2024: Health Minister Dr. Mandaviya inaugurated 13 medical-device plants focusing on critical-care monitors, imaging, and body implants under the PLI scheme

India Patient Monitoring Market Report Scope

As per the scope of this report, patient monitoring consists of devices and equipment that are used to continuously monitor a patient's vital parameters using a medical monitor and collect medical and other forms of health data.

The India Patient Monitoring Market is Segmented by Type (Devices, Services), End-User (Public Tertiary Hospitals, Private Corporate Hospitals, Specialty & Single-Specialty Clinics, Home-Healthcare Providers, Ambulatory Surgical Centers), and Application (Cardiology, Respiratory, Neurology, Critical Care (ICU/CCU), Diabetes & Metabolic, Maternal & Neonatal). The report offers the value (in USD million) for the above segments.

By Type

| Device Type | Multiparameter Vital-Signs Monitors |

| Cardiac Monitoring Devices | |

| Respiratory Monitoring Devices | |

| Fetal & Neonatal Monitoring Devices | |

| Neuro-Monitoring Devices | |

| Hemodynamic & Pressure Monitoring Devices | |

| Remote Patient Monitoring Kits | |

| Wearable Sensors & Patches | |

| By Service/Offering | Installation & Maintenance Services |

| Training & Education Services | |

| Remote Monitoring & Telehealth Services | |

| Data Integration & Interoperability Services | |

| Analytics & Reporting Services | |

| Managed Monitoring Operations & Triage Services |

By End-User

| Public Tertiary Hospitals |

| Private Corporate Hospitals |

| Specialty & Single-Specialty Clinics |

| Home-Healthcare Providers |

| Ambulatory Surgical Centers |

By Application

| Cardiology |

| Respiratory |

| Neurology |

| Critical Care (ICU/CCU) |

| Diabetes & Metabolic |

| Maternal & Neonatal |

| By Type | Device Type | Multiparameter Vital-Signs Monitors |

| Cardiac Monitoring Devices | ||

| Respiratory Monitoring Devices | ||

| Fetal & Neonatal Monitoring Devices | ||

| Neuro-Monitoring Devices | ||

| Hemodynamic & Pressure Monitoring Devices | ||

| Remote Patient Monitoring Kits | ||

| Wearable Sensors & Patches | ||

| By Service/Offering | Installation & Maintenance Services | |

| Training & Education Services | ||

| Remote Monitoring & Telehealth Services | ||

| Data Integration & Interoperability Services | ||

| Analytics & Reporting Services | ||

| Managed Monitoring Operations & Triage Services | ||

| By End-User | Public Tertiary Hospitals | |

| Private Corporate Hospitals | ||

| Specialty & Single-Specialty Clinics | ||

| Home-Healthcare Providers | ||

| Ambulatory Surgical Centers | ||

| By Application | Cardiology | |

| Respiratory | ||

| Neurology | ||

| Critical Care (ICU/CCU) | ||

| Diabetes & Metabolic | ||

| Maternal & Neonatal | ||

Key Questions Answered in the Report

What is the current size and projected growth of the India patient monitoring market?

The India patient monitoring market size is USD 2.87 billion in 2026 and is forecast to reach USD 4.16 billion by 2031 at an 7.68% CAGR.

Which segments lead adoption within the India patient monitoring market?

Devices led with 84.92% revenue share in 2025, while services are projected to grow at 9.21% CAGR as providers adopt managed monitoring and integration services.

Who are the fastest-growing end users in India for patient monitoring?

Home-healthcare providers are the fastest-growing end users with a 9.44% CAGR outlook supported by telehealth reimbursement pilots and falling sensor costs.

Which clinical application is expanding the quickest in India patient monitoring?

Neurology monitoring is the fastest-growing application with a 9.08% CAGR as trauma centers add ICP, EEG, and cerebral oximetry capacity.

What policy frameworks most influence the India patient monitoring market?

CDSCO's MDR 2017, ABDM's consent-based data exchange, BIS certification norms, and PLI incentives for medical devices shape compliance, interoperability, and localization.

How concentrated is competition among vendors in India patient monitoring?

Competition is moderate, with multinationals holding about 49.60% of the India patient monitoring market share in 2025, while domestic players gain through local content and services bundling.

Page last updated on: