Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 19.07 Billion |

| Market Size (2026) | USD 22.73 Billion |

| Market Size (2031) | USD 54.67 Billion |

| Growth Rate (2026 - 2031) | 19.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Paper Packaging Market Analysis by Mordor Intelligence

India paper packaging market size in 2026 is estimated at USD 22.73 billion, growing from 2025 value of USD 19.07 billion with 2031 projections showing USD 54.67 billion, growing at 19.16% CAGR over 2026-2031. Expansive e-commerce operations, plastic-use restrictions, and rising fast-moving consumer goods (FMCG) volumes combine to lift demand for lightweight, recyclable substrates across primary and secondary formats. Regulatory bans on selected single-use plastics in all 28 states accelerate substitution, while brand owners invest in premium barrier-coated paperboard to meet sustainability pledges and consumer expectations.[1]Ministry of Environment, Forest and Climate Change, “Plastic Waste Management Amendment Rules 2024,” moef.gov.in Digital printing adoption, already at 18% penetration in label lines, supports agile production, late-stage customization, and counterfeit deterrence. Amid growth, raw-material exposure to kraft-paper price swings and cost-competitive zero-duty ASEAN imports pressure margins, prompting domestic mills to scale, backward-integrate, and secure recovered-fiber feedstock. Overall, India paper packaging market participants deploy capital toward coating, molded-fiber, and smart-label technologies that strengthen product stewardship credentials and capture higher-value applications along the supply chain.

Key Report Takeaways

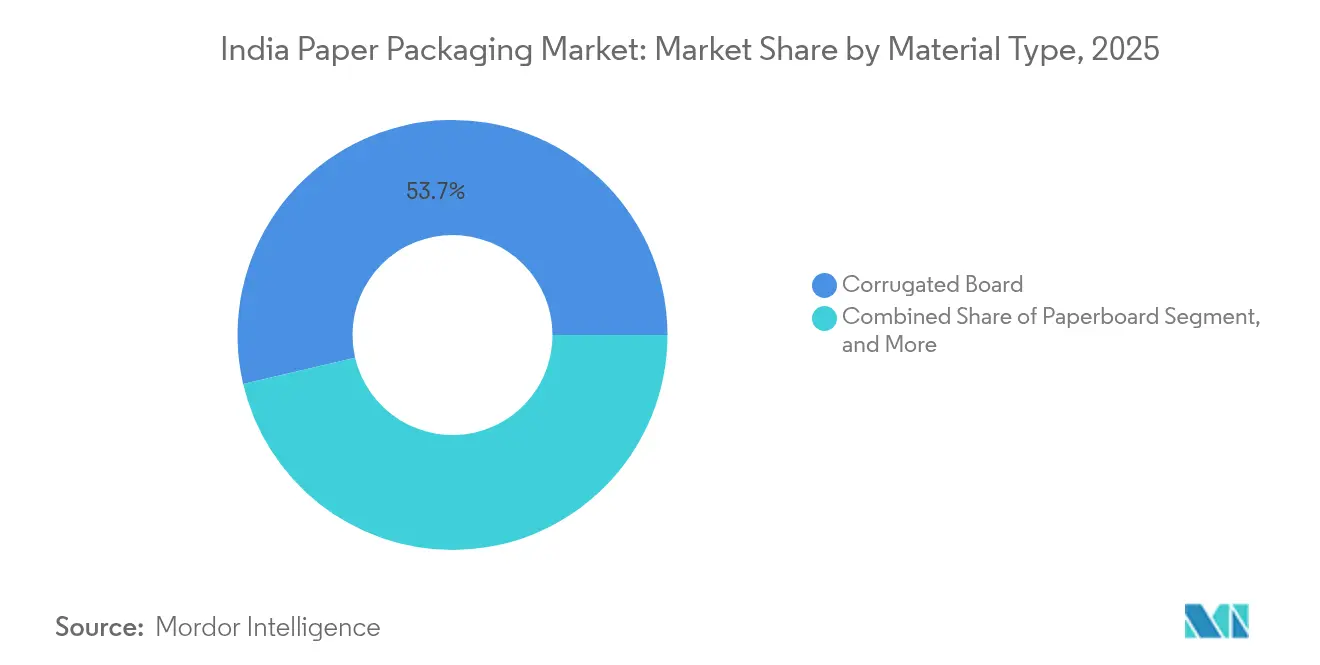

- By material type, corrugated board led with 53.65% of India paper packaging market share in 2025, while paperboard is forecast to advance at a 20.95% CAGR to 2031.

- By product category, flexible paper packaging commanded 53.74% share of the India paper packaging market size in 2025 and is projected to expand at a 21.55% CAGR through 2031.

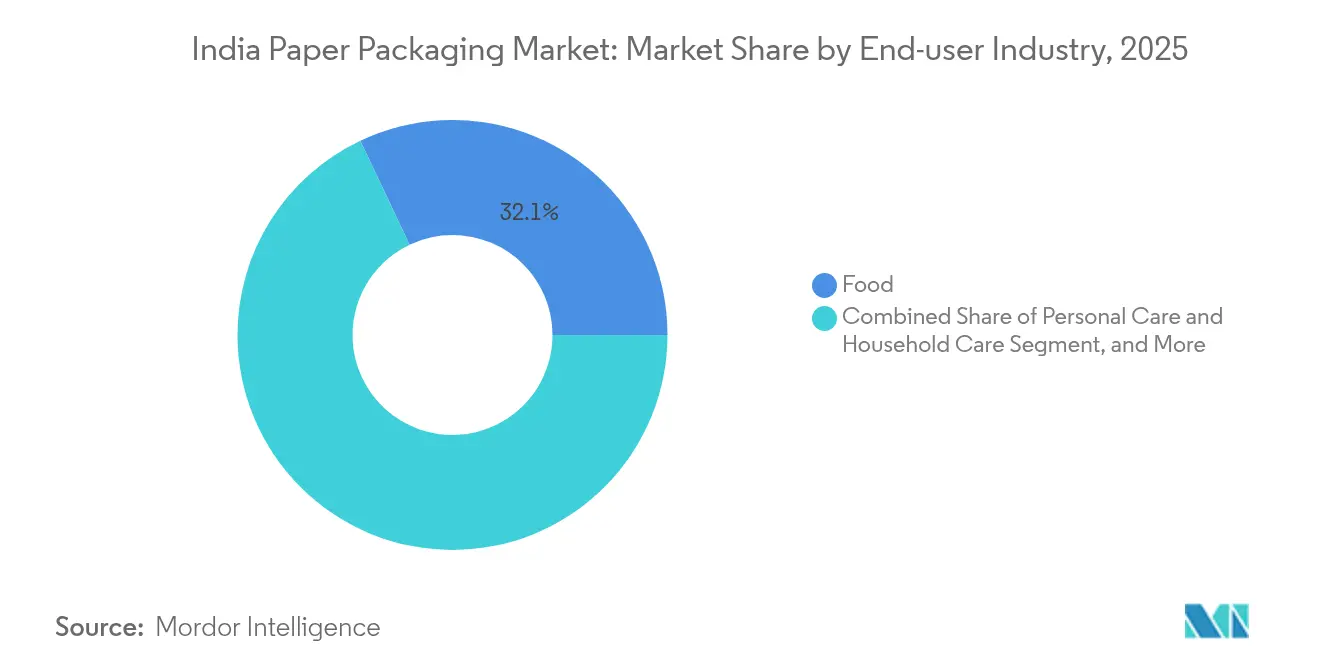

- By end-use industry, food applications captured 32.05% revenue share in 2025; personal care is poised for the fastest growth at a 23.12% CAGR to 2031.

- By packaging format, primary packaging accounted for 45.88% of the India paper packaging market size in 2025, whereas secondary packaging is set to register a 20.64% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating e-commerce fulfillment demand | +4.2% | Major metros and Tier-1 corridors | Medium term (2-4 years) |

| FMCG and packaged-food volume expansion | +3.8% | Pan-India, strong in Gujarat, Maharashtra, Tamil Nadu | Long term (≥ 4 years) |

| Government ban on select single-use plastics | +3.5% | Nationwide; state enforcement varies | Short term (≤ 2 years) |

| Brand-owner switch to premium lightweight board | +2.9% | Urban consumption centers | Medium term (2-4 years) |

| Rapid adoption of digital and on-demand printing | +2.1% | Metro clusters; spreading to Tier-2 cities | Medium term (2-4 years) |

| Supply-chain traceability and smart-label uptake | +1.8% | Export-oriented zones, organized retail | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating E-commerce Fulfillment Demand

India processed 5.2 billion online shipments in 2024 compared with 3.8 billion a year earlier, boosting corrugated-box volumes and encouraging adoption of lightweight high-strength grades. Large platforms added automated packing lines that standardize dimensions and reduce empty space. Quick-commerce operators favor compact corrugated formats designed for micro-fulfillment centers. Digital payment penetration reached 87% in urban areas, allowing removal of cash-on-delivery inserts and lowering material usage. Subscription-commerce models provide predictable demand, enabling converters to dedicate lines and secure raw-material contracts, thereby stabilizing throughput.

FMCG and Packaged-Food Volume Expansion

The packaged-food sector grew 8.2% in 2024, supported by organized retail penetration of 12% nationally and 35% in metros. Nestlé India allocated INR 2,600 crore (USD 29.28 crore ) for capacity upgrades, underscoring confidence in sustained consumption growth. Rural-income support schemes stimulated demand for branded goods sold in small pack sizes that favor coated paperboard. Growth in the organized dairy channel at 12% annually requires insulated corrugated containers for cold-chain logistics. These shifts reinforce multiyear contracting between food majors and packaging suppliers, anchoring baseline order volumes for the India paper packaging market.

Government Ban on Select Single-Use Plastics

The Plastic Waste Management Amendment Rules 2024 prohibit plastic cups, plates, and certain flexible laminates, driving urgent substitution toward paper solutions. Tamil Nadu achieved 78% compliance, compared with a national average of 45%, producing regional demand clusters. Extended Producer Responsibility mandates that brand owners collect 60% of plastic waste, making paper alternatives more attractive despite their 15-20% higher unit cost. Fines ranging from INR 5,000 (USD 56.31 crore) to INR 100,000 (USD 1,126.38 crore) per violation accelerate compliance, particularly in organized food service and retail. While medical uses remain exempt, food, personal care, and e-commerce categories present immediate scale for paper converters.

Rapid Adoption of Digital and On-Demand Printing

Digital presses accounted for 18% of label capacity in 2024, enabling variable data and region-specific graphics without plate costs. Brand owners deploy QR codes and NFC chips to authenticate products and engage consumers, lifting paper substrate requirements that accommodate embedded electronics. Short-run economics cut inventory carrying costs by 25-30% and shorten product-launch cycles. The technology also democratizes premium packaging for small and medium enterprises, expanding the addressable customer base inside the India paper packaging market. Converter investment in color-management software and post-press embellishment further differentiates value propositions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kraft-paper input-price volatility | -2.4% | National, import-reliant processors | Short term (≤ 2 years) |

| Zero-duty ASEAN imports squeezing margins | -1.9% | Coastal hubs adjacent to ports | Medium term (2-4 years) |

| Structural shortage of recovered fiber | -1.6% | North and West mills | Long term (≥ 4 years) |

| Excess corrugator capacity and fragmentation | -1.3% | Regional SME clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Kraft-paper input-price volatility

Spot kraft prices fluctuated 15–20% in 2024 due to ocean-freight spikes and energy-cost swings, eroding SME corrugator margins that lack hedging capacity. Mills with captive pulping muted exposure, underscoring integration’s value. Price uncertainty delays capacity upgrades as payback models become fluid, and it hampers long-term contracts with brand owners expecting stable cost curves.

Zero-duty ASEAN imports squeezing margins

Under free-trade concessions, Indonesian and Thai linerboard enters at zero duty, undercutting domestic rates by up to 10% in coastal markets. Local mills augment value-added coatings and shorter lead-times to compete, but smaller converters face margin compression, often passing costs downstream or forfeiting share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Corrugated board retains lead while coated paperboard accelerates

Corrugated board maintained 53.65% India paper packaging market share in 2025, driven by e-commerce durability requirements and industrial stacking needs. Yet coated paperboard registers a 20.95% CAGR to 2031, propelled by premium FMCG and pharmaceutical applications that demand moisture and grease barriers. India paper packaging market size for paperboard is projected to reach USD 18.47 billion by 2031, up from USD 5.9 billion in 2025. Coated variants also leverage government procurement favoring recyclable substrates, particularly in public food-distribution channels. Investments such as ITC’s INR 800 crore (USD 9.011 crore) barrier-coating line reflect this structural tailwind.

Advanced multiwall kraft innovations cut weight in cement sacks without sacrificing burst strength, winning share from woven polypropylene. Recovered-fiber content rises alongside FSC certification uptake, helping brands achieve Scope-3 carbon reductions. Material diversification cushions mills against kraft price cycles and broadens the India paper packaging market addressable for specialized grades.

By Product Type: Flexible formats dominate but rigid solutions scale

Flexible structures secured 53.74% India paper packaging market share during 2025 thanks to pouches, sachets, and wraps optimized for snack, confectionery, and personal-care items. The sub-category posts a 21.55% CAGR as barrier coatings allow plastic-free laminates. Digital web presses tune graphics to micro-market preferences, reinforcing volume gains. Meanwhile, rigid folding cartons and corrugated cases expand as omnichannel brands harmonize shelf-ready and ship-in-own-container designs.

Rigid formats benefit from micro-flute and litho-lam innovations that reduce fiber by 8-10% yet elevate print fidelity, deepening penetration in cosmetics and electronics. Cartonboard lines tailored for pharmaceutical serialization add tamper evidence crucial to regulatory compliance, accelerating rigid adoption.

By End-Use Industry: Food retains primacy while personal care surges

Food applications accounted for 32.05% of India paper packaging market size in 2025, reflecting ongoing processed-food formalization and cold-chain expansion. Rising snack consumption and direct-to-consumer models sustain corrugated and flexible demand. Personal care, though smaller, advances at 23.12% CAGR, fueled by premiumization, sustainability pledges, and gender-neutral grooming lines.

Beverage paper applications remain mainly secondary due to liquid-pack barriers; however, trials using aqueous-coated board for dairy gable-tops open future avenues. Electronics, automotive, and textiles provide steady secondary and tertiary uptake, tethered to national manufacturing-linked-incentive policies.

By Packaging Format: Primary packs prevail, secondary packs outpace

Primary packs represented 45.88% India paper packaging market share in 2025, largely via food-contact cartons and direct-meal service clamshells. Secondary packs record a 20.64% CAGR on the back of shelf-ready display requirements and brand stories printed on outer sleeves. India paper packaging market size for secondary formats is forecast at USD 11.55 billion by 2031, nearly doubling 2025 levels.

Tertiary logistics solutions standardize around e-commerce parcel dimensions, lowering inventory complexity for fulfillment partners. Government directives encouraging plastic-replacement in public-sector tenders further tilt contracts toward primary and secondary board.

Geography Analysis

The western corridor’s dominance stems from integrated mills situated near container ports that handle recovered-fiber imports and finished-goods exports efficiently. Corrugator clusters around Mumbai and Surat tap robust FMCG backward-linkages. Proximity to chemical feedstocks supports specialty coating lines producing grease-proof wraps for snack majors.

Southern growth reflects diverse industry bases from electronics in Bengaluru to automotive in Chennai each demanding differentiated transit and retail packs. Infrastructure upgrades such as dedicated freight corridors lower inbound raw-material costs, enhancing mill competitiveness. Policy incentives for greenfield pulp units in Andhra Pradesh and Telangana further tilt capacity expansion southward.

Northern expansion aligns with agricultural consolidation and cold-chain rollouts covering perishables bound for Delhi’s cash-rich consumer base. Here, medium mills retrofit biomass boilers to mitigate fuel cost spikes, while brand owners drive certification adoption to meet export protocols. Inland logistics constraints persist but road-widening projects promise cost relief over the forecast horizon.

Competitive Landscape

Roughly 2,000 converters operate nationwide, yet the top-10 integrated firms hold 35% collective share, signaling moderate concentration. ITC’s INR 3,498 crore (USD39.39 crore ) acquisition of Century Pulp and Paper vaults it to an 850,000-tonne capacity lead, underscoring the consolidation trend.[2]The Economic Times, “ITC Completes Century Pulp Acquisition for INR 3,498 Crore,” economictimes.indiatimes.com JK Paper’s INR 1,200 crore (USD 13.51 crore) board line in Gujarat and Pakka’s INR 675 crore (USD 7.60 crore) molded-fiber project illustrate aggressive capex cycles aimed at premium segments.[3]JK Paper, “Capacity Expansion and Strategic Investments,” jkpaper.com

Technology deployment differentiates market leaders: WestRock India and Parksons roll out automated corrugators with inline die-cutting to cut waste, while TCPL leverages digital presses for Amazon’s multicenter contract. Start-ups commercializing agri-waste fiber integrate with legacy players through supply agreements, providing circular-economy narratives without large cap-outlays. International entrants eye high-growth categories but face duty structures favoring local make-in-India conversions.

Competitive intensity remains highest among SME corrugators serving regional produce exporters, where price undercutting is prevalent. Integrated players steer toward coatings, molded-fiber, and smart-packaging value pools that defend margins and embed switching costs.

India Paper Packaging Industry Leaders

Smurfit WestRock

JK Paper Ltd.

Parksons Packaging Ltd.

TCPL Packaging Ltd.

Horizon Packs Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: ITC Limited concluded the Century Pulp and Paper acquisition for INR 3,498 crore (USD 39.39 crore ), creating India’s largest integrated player with 850,000 tonnes annual capacity.

- September 2024: Pakka Limited committed INR 675 crore (USD7.60 crore ) to a molded-fiber plant in Tamil Nadu targeting 50,000 tonnes sustainable pack output by 2026.

- August 2024: JK Paper inaugurated a 200,000-tonne paperboard line in Gujarat equipped with barrier coating and digital-printing readiness.

- July 2024: Smurfit WestRock India raised corrugated capacity by 150,000 tonnes via Maharashtra and Karnataka upgrades incorporating Industry 4.0 control systems.

India Paper Packaging Market Report Scope

Paper packaging is a broader category encompassing various packaging products made from paper-based materials and widely used and versatile solutions for protecting, storing, and transporting a diverse range of goods. The major types of paper packaging used across industries include corrugated boxes, folding cartons, paper bags, and liquid boards.

The Indian paper packaging market is segmented by product type (corrugated boxes, folding cartons, paper bags, and liquid board) and end-user industry (food, beverage, healthcare, personal care and household care, hardware and electrical products, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the segments.

By Material Type

| Kraft Paper |

| Paperboard |

| Corrugated Board |

| Other Material Types |

By Product Type

| Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | |

| Other Flexible Paper Packaging | |

| Rigid Paper Packaging | Folding Carton |

| Corrugated Boxes | |

| Other Rigid Paper Packaging |

By Packaging Format

| Primary Packaging |

| Secondary Packaging |

| Tertiary / Transit Packaging |

By End-Use Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial and Electronic |

| Other End-Use Industries |

| By Material Type | Kraft Paper | |

| Paperboard | ||

| Corrugated Board | ||

| Other Material Types | ||

| By Product Type | Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | ||

| Other Flexible Paper Packaging | ||

| Rigid Paper Packaging | Folding Carton | |

| Corrugated Boxes | ||

| Other Rigid Paper Packaging | ||

| By Packaging Format | Primary Packaging | |

| Secondary Packaging | ||

| Tertiary / Transit Packaging | ||

| By End-Use Industry | Food | |

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Industrial and Electronic | ||

| Other End-Use Industries | ||

Key Questions Answered in the Report

How large is the India paper packaging market in 2026?

India paper packaging market size is USD 22.73 billion in 2026 and is set to hit USD 54.67 billion by 2031.

What CAGR is forecast for India’s paper packaging sector to 2031?

The market is expected to grow at a 19.16% CAGR during 2026-2031.

Which product segment grows fastest in Indian paper packaging?

Flexible formats log the highest growth, expanding at a 21.55% CAGR on rising snack and personal-care demand.

Which region leads capacity in Indian paper packaging?

Western India, led by Maharashtra, accounts for 22% of national capacity, with southern states showing the fastest growth.

How does the plastic ban influence Indian paper packaging?

The ban on selected single-use plastics pushes brands toward recyclable paper solutions, adding roughly 3.5 percentage-points to sector CAGR in the short term.

Who are the key players driving consolidation?

ITC, JK Paper, and Pakka Limited spearhead consolidation via acquisitions and capacity expansions, enlarging integrated footprints.

Page last updated on: