India Omni-Channel And Warehouse Management Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

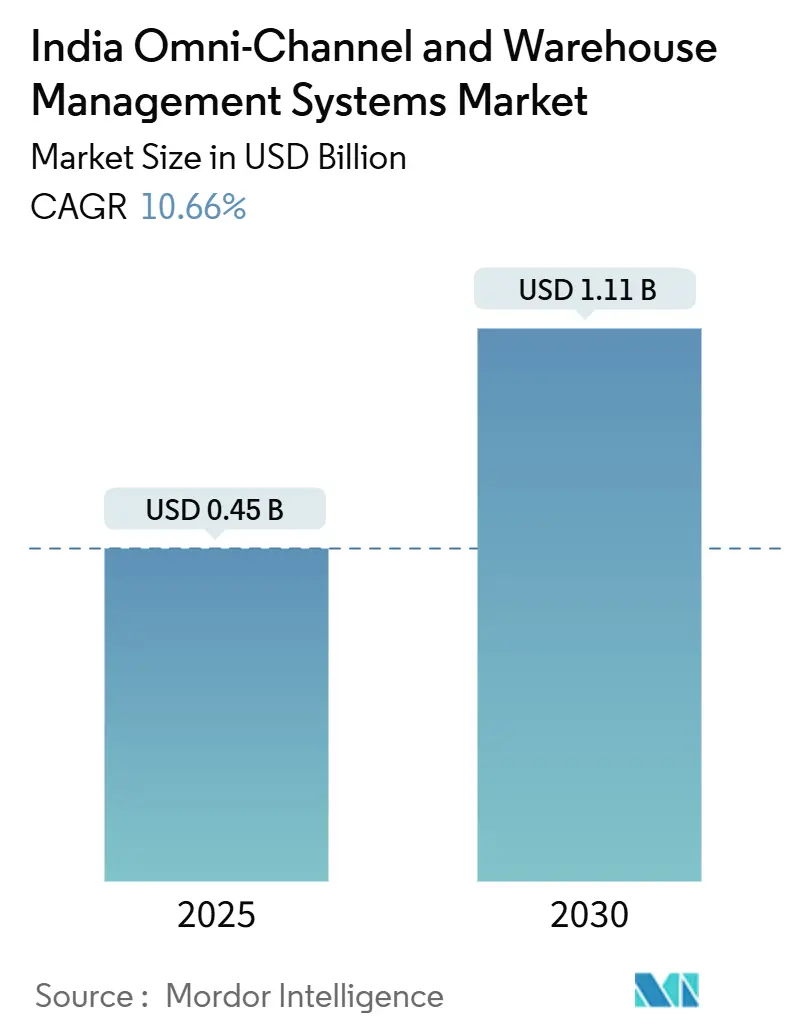

| Market Size (2025) | USD 0.45 Billion |

| Market Size (2030) | USD 1.11 Billion |

| Growth Rate (2025 - 2030) | 10.66% CAGR |

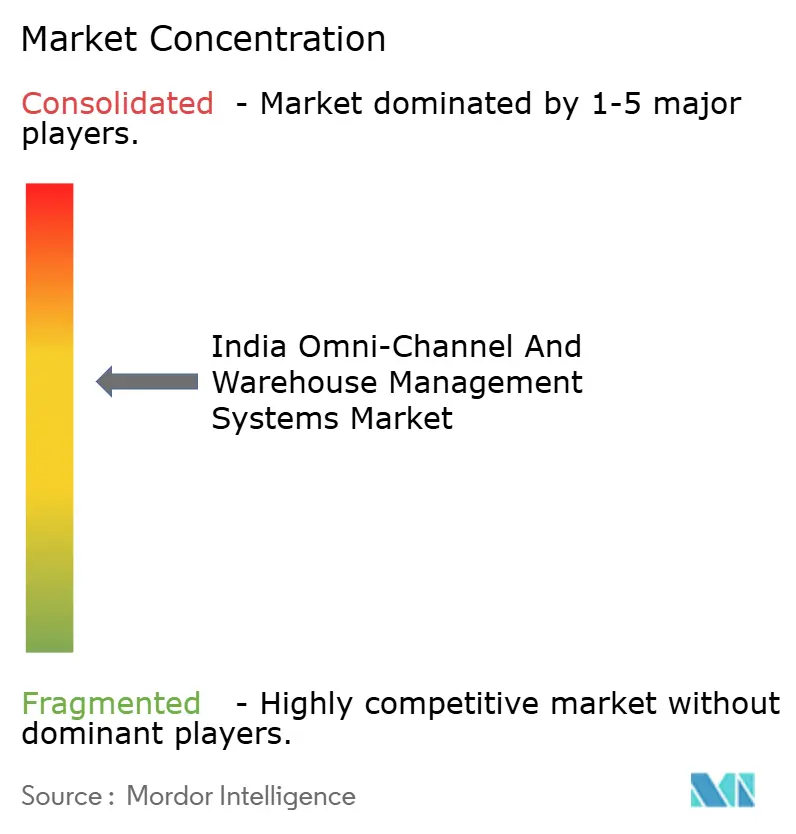

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Omni-Channel And Warehouse Management Systems Market Analysis by Mordor Intelligence

The India omni-channel and warehouse management systems market size is estimated at USD 0.45 billion in 2025 and is projected to reach USD 1.11 billion by 2030, growing at a 10.66% CAGR. Rising e-commerce volumes, expanding quick-commerce networks, and a supportive policy environment are accelerating capital spending on modern fulfillment infrastructure. Cloud-based deployments are gaining favor as hosting prices fall, enabling mid-market firms to access sophisticated inventory orchestration without the burden of on-premise hardware. Government incentives under Production Linked Incentive (PLI) schemes, the National Logistics Policy, and the Open Network for Digital Commerce (ONDC) are reframing warehouse management systems (WMS) as essential infrastructure rather than optional software. Competitive dynamics remain fragmented as no vendor controls more than a 15% share, encouraging vertical-specific product differentiation. Finally, regional disparities in real-estate quality and labor skills continue to shape adoption timelines, especially outside the top eight metropolitan areas.

Key Report Takeaways

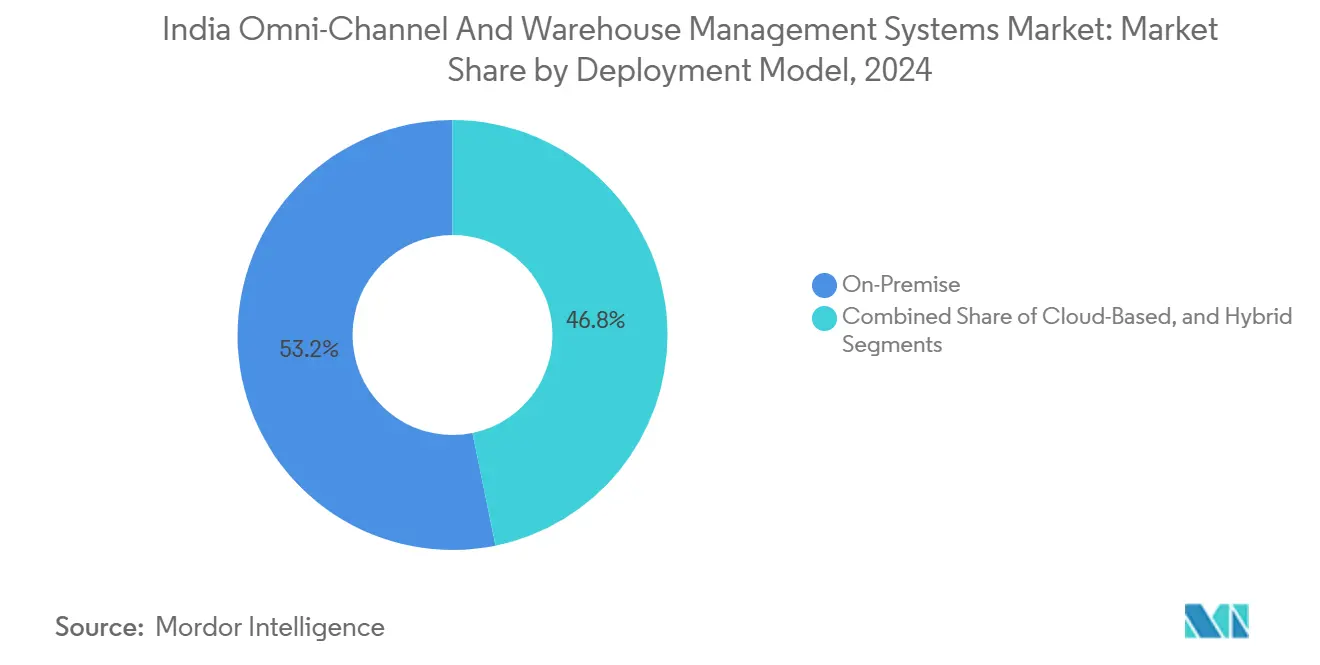

- By deployment model, on-premises solutions held 53.21% of the India omni-channel and warehouse management systems market share in 2024, while Cloud-Based deployments are advancing at a 12.17% CAGR through 2030.

- By component, Software commanded 68.94% share of the India omni-channel and warehouse management systems market size in 2024, and Services are expanding at a 12.46% CAGR.

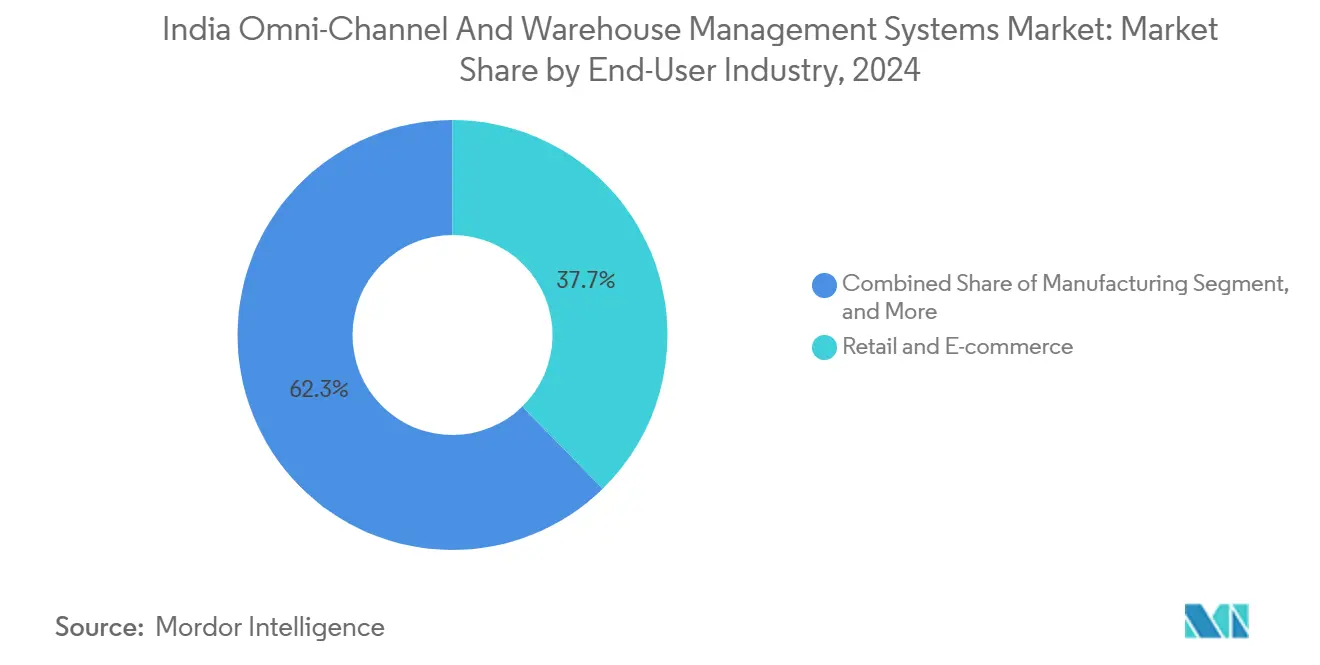

- By end-user industry, Retail and E-commerce led with 37.69% revenue share in 2024; Third-Party Logistics is forecast to expand at a 10.89% CAGR to 2030.

- By warehouse type, Distribution Centers accounted for a 31.57% share of the India omni-channel and warehouse management systems market size in 2024, and E-commerce Fulfillment Centers are advancing at an 11.14% CAGR.

- By geography, West India captured 34.76% of the Indian omni-channel and warehouse management systems market share in 2024, while South India is projected to deliver the highest CAGR at 11.34% through 2030.

India Omni-Channel And Warehouse Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid e-commerce penetration and same-day delivery race | +2.8% | National with concentration in metros and tier-1 cities | Short term (≤ 2 years) |

| GST-enabled pan-India network optimization by 3PLs | +2.1% | National, strongest in manufacturing corridors | Medium term (2-4 years) |

| Government PLI schemes for logistics tech and cold-chain | +1.9% | National with focus on manufacturing hubs | Long term (≥ 4 years) |

| Surge of ONDC-compliant omni-channel retail pilots | +1.4% | Urban markets, expanding to tier-2 cities | Medium term (2-4 years) |

| Fall in cloud-hosting costs below INR 3/hr instance | +1.2% | National, benefiting distributed operations | Short term (≤ 2 years) |

| AI-driven labor-planning cutting put-away time 25-40% | +1.2% | Metro clusters and Grade A warehouses | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid e-commerce penetration and same-day delivery race

Same-day and quick-commerce promises are now standard in India’s top metros, and demand real-time inventory visibility and sub-minute slotting optimization. Flipkart’s Haringhata facility exemplifies the shift, utilizing nine kilometers of conveyors to reduce turnaround time by 35-50%.[1]ITLN, “Warehouse Automation in India gets smarter, faster and sustainable,” itln.in Cloud-native WMS platforms orchestrate inventory across micro-fulfillment nodes, replacing legacy systems that cannot handle sub-4-hour delivery windows. Retailers are investing in predictive analytics to anticipate demand spikes by locality, which balances stock across multiple smaller sites. The India omni-channel and warehouse management systems market benefits directly from these technology upgrades, with quick-commerce operators prioritizing speed, accuracy, and scalability.

GST-enabled pan-India network optimization by 3PLs

The removal of interstate tax barriers allows 3PLs to consolidate smaller warehouses into fewer, automated mega-facilities. Many providers have reduced node counts by 30-40% while boosting throughput, cutting real estate costs, and improving labor utilization.[2]Business World, “Should Automation Be Restricted to Within the Warehouses?” bwdisrupt.com Such consolidation demands a WMS capable of multi-client billing, compliance monitoring, and dynamic space allocation. As 3PLs expand, they anchor recurring revenue streams for vendors in the India omni-channel and warehouse management systems market by signing multi-year managed-services agreements.

Government PLI schemes for logistics tech and cold-chain

PLI incentives, covering up to 6% of incremental sales, drive the adoption of temperature-controlled WMS modules among pharmaceutical and food processors. Cold-chain facilities now feature continuous temperature logging, automated alerts, and traceability down to the item level, including batch tracking. Mid-market firms, previously priced out of advanced systems, find deployments financially viable, thereby enlarging the addressable base for the India omni-channel and warehouse management systems market.

Surge of ONDC-compliant omni-channel retail pilots

ONDC’s protocol demands real-time inventory synchronization and automated order routing. Retailers upgrading their systems to meet compliance requirements are driving demand for cloud-ready, API-first WMS solutions capable of channel-agnostic fulfillment. Pilot success in early locations is encouraging a rapid rollout to 100 cities by 2025. The India omni-channel and warehouse management systems market is expected to see a wave of small and medium retailers adopting subscription WMS to connect with ONDC gateways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented tier-2/3 warehouse real-estate ownership | -1.8% | Tier-2 and tier-3 cities, rural logistics hubs | Long term (≥ 4 years) |

| Low RF infrastructure quality outside metro clusters | -1.4% | Non-metro areas, industrial corridors | Medium term (2-4 years) |

| Scarcity of WMS-skilled workforce (≤1.2 technicians/10k ft²) | -1.1% | National, acute in tier-2/3 cities | Long term (≥ 4 years) |

| Data-localization and cross-border flow restrictions | -0.9% | National, affecting multinational operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented tier-2/3 warehouse real-estate ownership

Family-owned warehouses, averaging 10,000-25,000 square feet, dominate smaller cities. Landlords resist tenant-specific upgrades, while tenants fear the sunk costs associated with immovable assets. Licensing and hardware fees become uneconomic when spread across many tiny sites. Although tier-2 locations host approximately 100 million square feet of space, penetration remains low unless shared WMS platforms or cost-sharing models emerge. This fragmentation limits near-term expansion of the India omni-channel and warehouse management systems market beyond metro clusters.

Scarcity of WMS-skilled workforce

India has only 1.2 qualified WMS technicians per 10,000 ft², which is well below the 2.5-3.0 benchmark.[3]SiliconIndia, “Challenges And Opportunities In Warehouse Automation,” industry.siliconindia.com Training spans six to eight weeks, plus supervised operation, which raises onboarding costs. Skill gaps in integration, troubleshooting, and data analytics further delay ROI. Vendors respond with simpler interfaces and remote diagnostics, yet workforce shortages still dampen adoption rates in the India omni-channel and warehouse management systems market outside major cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud migration accelerates despite control concerns

The India omni-channel and warehouse management systems market size for on-premise solutions stood at USD 0.24 billion in 2024, accounting for a 53.21% share. Cloud adoption, however, is projected to expand at a 12.17% CAGR to 2030 as compute costs fall below INR 3 per hour per instance. Mid-sized 3PLs experience a 40-60% lower total cost of ownership over five years compared to local installations. Data residency rules keep sensitive verticals on private clouds, fostering hybrid architectures. Overall, shifting demand toward subscription models supports recurring revenue for vendors, enlarging the India omni-channel and warehouse management systems market.

Greater agility attracts retailers that need seasonal scale-up during festive periods, while automatic software updates lighten internal IT loads. Faster deployment cycles-eight to twelve weeks versus up to twenty-four for on-premise-enable quicker ROI. Vendors now bundle analytics modules on public clouds, allowing clients to run machine-learning predictions without incurring heavy capital outlays. As a result, the India omni-channel and warehouse management systems market is expected to see cloud deployments overtake on-premise by the late forecast years.

By Component: Services growth reflects implementation complexity

Software retained 68.94% share of the India omni-channel and warehouse management systems market size in 2024. Yet Services revenue is climbing at 12.46% CAGR, outpacing licenses. Integrations with robotics, AS/RS, and IoT sensors require custom coding and process redesign. A consumer-electronics project ran for 18 months and saw service costs exceed license costs by 40%. Managed services appeal to firms lacking internal experts, ensuring continuous optimization. The trend supports ecosystem partners-system integrators, automation vendors, and consultants-who capture a growing slice of the Indian omni-channel and warehouse management systems market.

As predictive maintenance and AI-driven planning modules come online, ongoing support contracts become increasingly important. Vendors now price services through outcome-based models, tying fees to improvements in throughput. This aligns incentives and deepens customer relationships, making switching less likely and fortifying market stickiness.

By End-User Industry: 3PL growth outpaces traditional leaders

Retail and E-commerce generated 37.69% of 2024 revenue, leveraging WMS to manage omnichannel flows. The India omni-channel and warehouse management systems market size for 3PLs is smaller but rising fastest at 10.89% CAGR as companies outsource logistics. Consolidated mega-warehouses increase throughput, driving demand for advanced systems to support multi-client billing. Manufacturing and FMCG sectors maintain steady growth, utilizing WMS for just-in-time inventory management and quality compliance.

Pharmaceuticals pay a premium for batch traceability and thermal monitoring, a niche boosted by cold-chain PLI incentives. Cross-vertical momentum indicates a broadening customer base for the India omni-channel and warehouse management systems market. 3PLs also spearhead innovation, piloting goods-to-person robots and AI-driven labor planning. Their scale gives vendors reference deployments that accelerate penetration into other segments.

By Warehouse Type: Fulfillment Centers Lead Automation Adoption.

Distribution centers held a 31.57% share in 2024. E-commerce fulfillment centers are expected to expand at a 11.14% CAGR, driven by the growing demand for sub-4-hour delivery expectations. These facilities rely on real-time analytics and robotic picking to manage thousands of small orders. Cold-storage warehouses, although niche, command high licensing fees due to stringent temperature and traceability needs.

Cross-docking hubs emphasize dock scheduling and transport yard interfaces. Manufacturing warehouses integrate WMS with production execution for seamless inbound-to-line flows. Each subtype drives specialized requirements, encouraging vendors to tailor their modules and fueling diversification within the Indian omni-channel and warehouse management systems market.

Geography Analysis

West India led with 34.76% share in 2024, anchored by Mumbai’s Jawaharlal Nehru Port Trust handling 55% of India’s containerized cargo and Gujarat’s strong manufacturing base. Regulations for hazardous materials and customs compliance push demand for advanced WMS features, ensuring sustained upgrades.

South India is expected to post an 11.34% CAGR to 2030, driven by the expansion of technology, automotive, and pharmaceutical clusters in Bengaluru, Chennai, and Hyderabad. NX Logistics’ 16,608 m² facility in Bengaluru dedicated to Zepto quick-commerce illustrates rapid Grade A expansion. Skilled IT labor and government digitization support speed adoption. Vendors often pilot novel analytics and robotics here before rolling them out nationally, thereby bolstering the Indian omni-channel and warehouse management systems market.

North India’s growth is tied to the progress of the Dedicated Freight Corridor, which links Delhi’s consumption hub with industrial centers. East India benefits from the expansion of port facilities and mining-related manufacturing in West Bengal and Odisha. However, uneven RF infrastructure and fragmented real estate moderate uptake, creating demand for shared-services WMS and landlord-tenant financing models.

Competitive Landscape

Moderate fragmentation defines the India omni-channel and warehouse management systems market. Global leaders Manhattan Associates, Blue Yonder, and Körber emphasize the use of AI modules and robotics orchestration. Domestic specialists Vinculum Solutions, Increff Technologies, and Unicommerce leverage local knowledge and rapid customization. No single provider exceeds a 15% share, reflecting the varied requirements across different warehouse types and industries.

Technology differentiation shapes competition. GreyOrange’s 2024 patents on multilevel robot mobility signal investment in proprietary algorithms. Cloud-native entrants offer subscription licensing and eight-week implementations, challenging traditional perpetual-license models. Cold-chain compliance, ONDC-ready APIs, and quick-commerce slotting optimization are emerging white-space niches. Vendors forming ecosystem partnerships with automation and IoT suppliers accelerate the development of integrated solutions, strengthening their positions in the Indian omni-channel and warehouse management systems market.

India Omni-Channel And Warehouse Management Systems Industry Leaders

Manhattan Associates, Inc.

Blue Yonder Group, Inc.

Körber Supply Chain Software GmbH

Infor, Inc.

Tecsys Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Vinculum Solutions Pvt. Ltd. introduced an ONDC-ready omni-channel WMS tailored for Indian retailers. The platform offers real-time inventory synchronization across brick-and-mortar and digital storefronts, supporting merchants in tier-1 cities that plan to join the ONDC network.

- August 2025: Increff Technologies Pvt. Ltd. raised INR 75 crore (USD 9 million) in Series B financing led by Sequoia Capital India. The new capital will help extend the firm’s AI-driven warehouse optimization tools into tier-2 and tier-3 cities, with an aim of lowering operational expenses by 30–40% through machine-learning analytics.

- June 2025: Ramco Systems Ltd. partnered with Amazon Web Services to unveil a cloud-native WMS for small and midsize enterprises. Priced from INR 25,000 a month, the solution runs on AWS’s Mumbai region, delivers sub-three-second response times, and comes with built-in links to leading Indian ERP platforms and GST compliance modules.

- March 2025: Unicommerce eSolutions Pvt. Ltd. acquired a Bengaluru-based robotics integration firm for INR 45 crore (USD 5.4 million). The deal adds autonomous mobile robot and process-automation capabilities to Unicommerce’s WMS, targeting e-commerce fulfillment centers that require sub-four-hour delivery performance.

India Omni-Channel And Warehouse Management Systems Market Report Scope

| On-Premise |

| Cloud-Based |

| Hybrid |

| Software |

| Services |

| Retail and E-commerce |

| Third-Party Logistics (3PL) |

| Manufacturing |

| Fast-Moving Consumer Goods (FMCG) |

| Healthcare and Pharmaceuticals |

| Other End-User Industry |

| Distribution Centers |

| E-commerce Fulfillment Centers |

| Cold-Storage Warehouses |

| Manufacturing Warehouses |

| Cross-Docking Facilities |

| North India |

| South India |

| East India |

| West India |

| By Deployment Model | On-Premise |

| Cloud-Based | |

| Hybrid | |

| By Component | Software |

| Services | |

| By End-User Industry | Retail and E-commerce |

| Third-Party Logistics (3PL) | |

| Manufacturing | |

| Fast-Moving Consumer Goods (FMCG) | |

| Healthcare and Pharmaceuticals | |

| Other End-User Industry | |

| By Warehouse Type | Distribution Centers |

| E-commerce Fulfillment Centers | |

| Cold-Storage Warehouses | |

| Manufacturing Warehouses | |

| Cross-Docking Facilities | |

| By Geography | North India |

| South India | |

| East India | |

| West India |

Key Questions Answered in the Report

What is the projected value of the India omni-channel and warehouse management systems market by 2030?

The market is expected to reach USD 1.11 billion by 2030.

Which deployment model is growing fastest for warehouse management systems in India?

Cloud-based deployments are advancing at a 12.17% CAGR through 2030, driven by lower hosting costs and faster implementation cycles.

Which end-user segment leads demand for WMS solutions in India?

Retail and e-commerce held 37.69% revenue share in 2024, reflecting the sector’s high throughput and omnichannel requirements.

Which Indian region is forecast to grow quickest for WMS adoption?

South India is projected to grow at 11.34% CAGR through 2030 due to strong technology, automotive, and pharma clusters.

How do PLI schemes influence WMS investments?

PLI incentives offset up to 6% of incremental sales for qualifying logistics and cold-chain projects, making sophisticated WMS deployments financially attractive.

What is a key barrier to WMS adoption outside metro areas?

Fragmented ownership of small warehouses and a shortage of skilled technicians limit technology penetration in tier-2 and tier-3 cities.

Page last updated on: