Warehouse Management System (WMS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

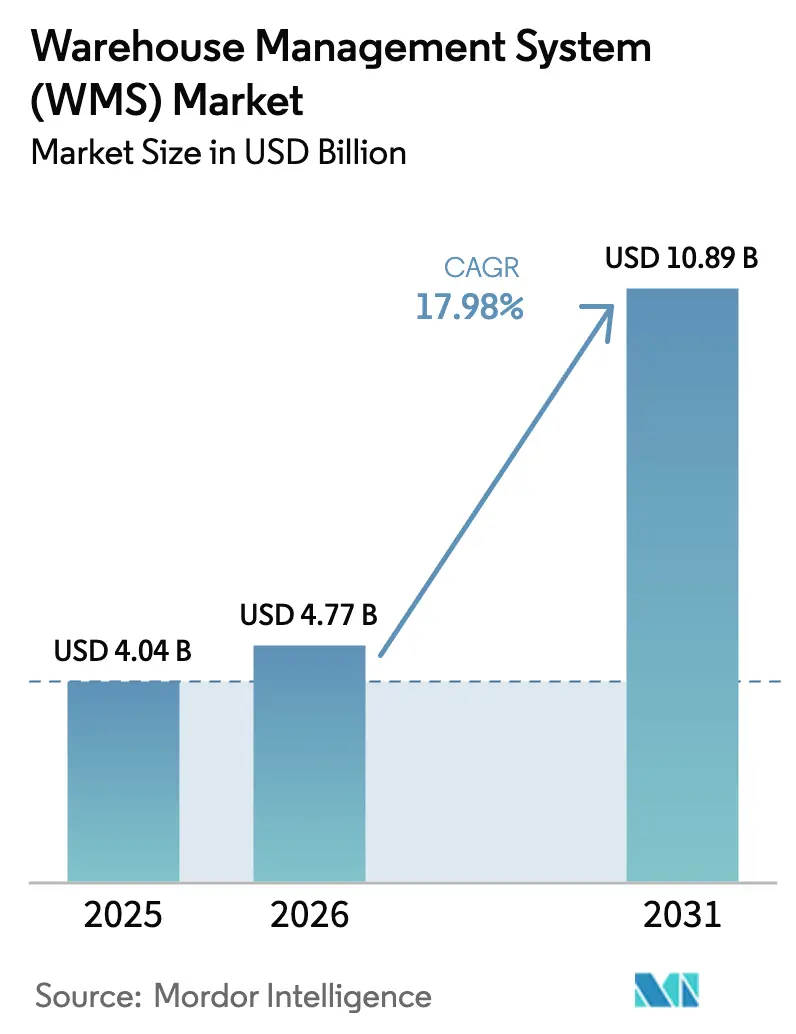

| Market Size (2026) | USD 4.77 Billion |

| Market Size (2031) | USD 10.89 Billion |

| Growth Rate (2026 - 2031) | 17.98% CAGR |

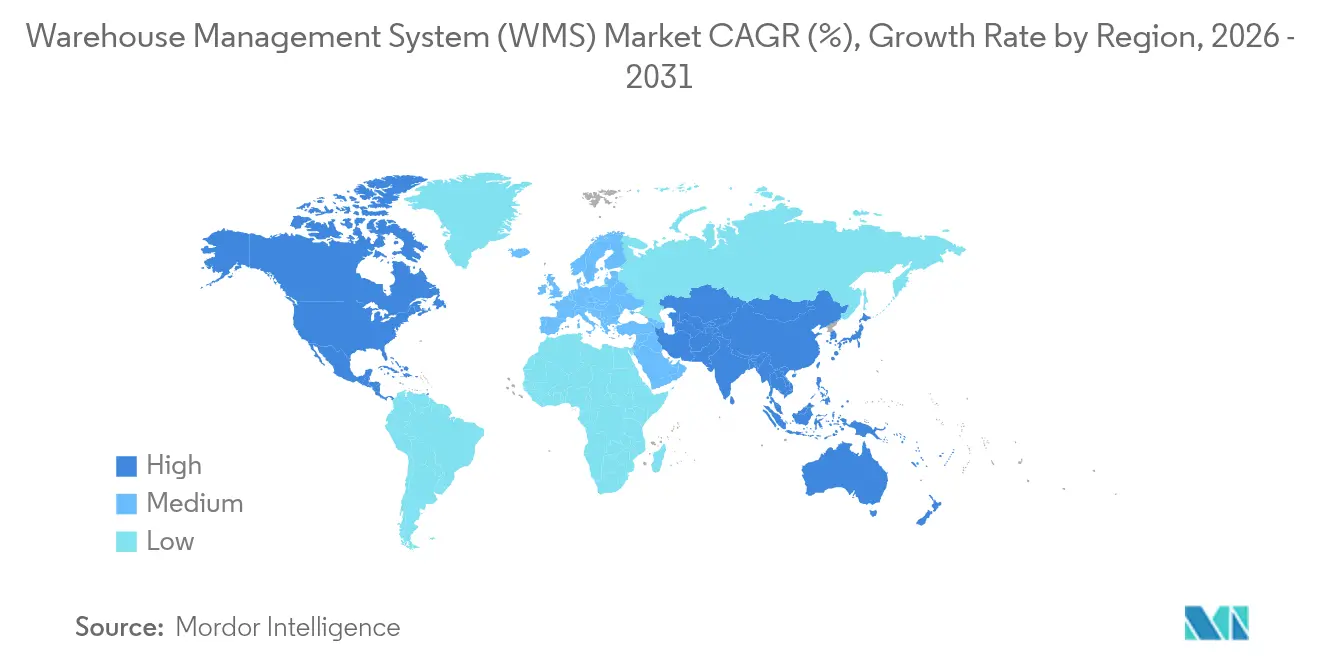

| Fastest Growing Market | North America and Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Warehouse Management System (WMS) Market Analysis by Mordor Intelligence

Warehouse management system market size in 2026 is estimated at USD 4.77 billion, growing from 2025 value of USD 4.04 billion with 2031 projections showing USD 10.89 billion, growing at 17.98% CAGR over 2026-2031. Adoption accelerates because e-commerce operators need real-time inventory insight, while persistent labor shortages make software-orchestrated automation a necessity. Cloud deployment is the primary growth engine, supported by scalable subscription pricing and continuous feature updates. Artificial-intelligence modules now integrate predictive analytics that can improve inventory accuracy by 30%, lowering costs and boosting customer-service levels. Vendors that combine software with specialized services win complex enterprise projects, yet modular API-first architectures let mid-market firms access advanced functions without prohibitive capital outlay.

Key Report Takeaways

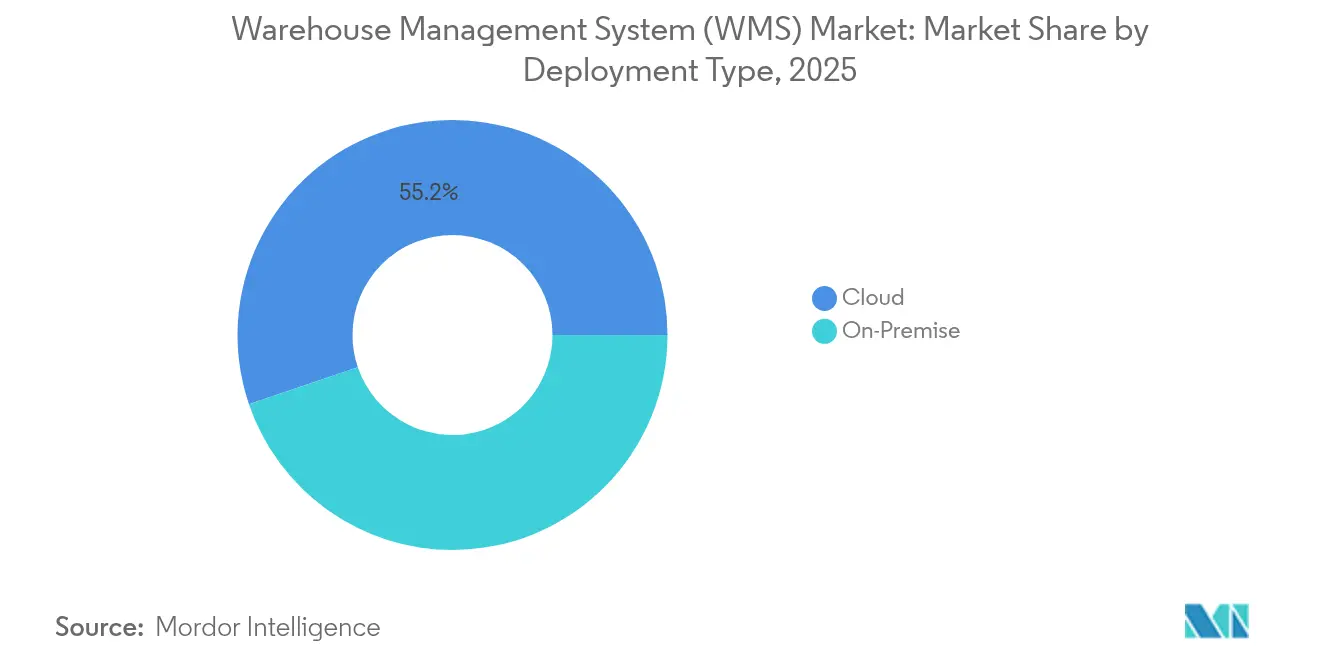

- By deployment type, cloud-based platforms led with 55.21% revenue share in 2025, and this segment is projected to expand at a 19.12% CAGR through 2031.

- By component, services commanded 80.05% of the warehouse management system market share in 2025, while software is forecast to grow fastest at a 16.92% CAGR.

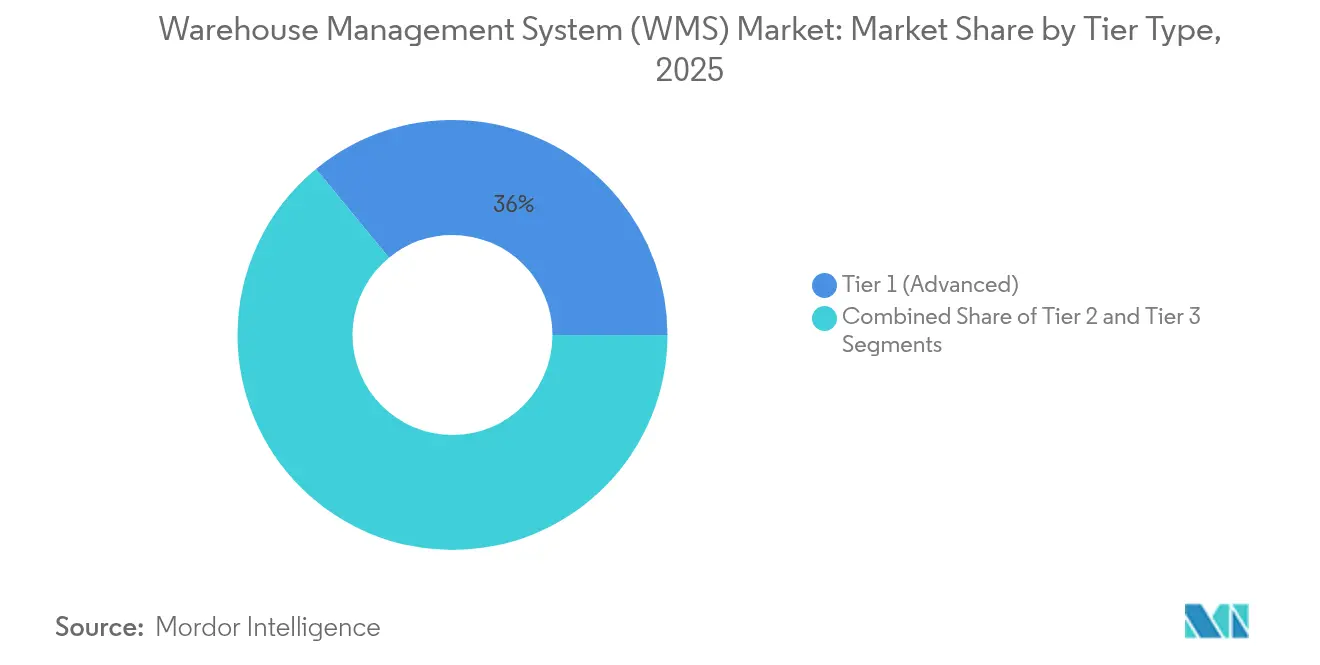

- By tier type, Tier 1 advanced solutions captured 35.95% share of the warehouse management system market size in 2025; Tier 2 intermediate solutions are poised for an 18.1% CAGR to 2031.

- By end-user industry, manufacturing held 30.22% of the warehouse management system market share in 2025, whereas transportation and logistics is set to post an 18.32% CAGR.

- By geography, North America dominated with 35.55% share of the warehouse management system market in 2025; Asia-Pacific is anticipated to register a 18.74% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Warehouse Management System (WMS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom and SKU proliferation | +4.2% | Global with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Cloud/SaaS adoption across fulfillment networks | +3.8% | Global led by North America and Europe | Short term (≤ 2 years) |

| Labor shortages accelerating warehouse automation | +3.1% | North America and Europe expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-driven predictive workflows lowering stock-outs | +2.7% | Global with early adoption in developed markets | Long term (≥ 4 years) |

| Urban micro-fulfillment and “nano-WMS” demand | +1.9% | Urban centers worldwide, high in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Sustainability mandates for scope-3 reporting | +1.5% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce boom and SKU proliferation

Online retail keeps expanding and drives a sharp increase in the number of stock-keeping units that warehouses must handle. Walmart’s AI-enabled inventory engine maintained 99% availability during peak season, showing how technology offsets complexity. Rapid SKU growth strains manual processes, so operators deploy WMS modules that support dynamic slotting and real-time location tracking. Asia-Pacific facilities move fastest; more than 90% of operators in the region plan to automate picking and replenishment tasks within two years. The ability to orchestrate millions of item-level movements across multiple channels has therefore become a core purchase criterion.

Cloud/SaaS adoption across fulfillment networks

Manhattan Associates posted USD 90.3 million in cloud subscription revenue in Q4 2024, a 33% year-over-year jump that mirrors the market-wide pivot to SaaS[1]Editorial staff, “Manhattan Associates Q4 2024 Results,” Manhattan Associates, manh.com. Cloud eliminates lengthy implementation cycles and heavy capital outlays, letting even mid-size 3PLs roll out enterprise-grade functions quickly. Eighty-nine percent of logistics firms intend to run labor-management features in a modern WMS by 2024. API-first architectures simplify links to IoT sensors and machine-learning engines, enabling a steady cadence of incremental upgrades that legacy on-premise models cannot match.

Labor shortages accelerating warehouse automation

The United States recorded 490,000 logistics job openings in 2024, and European distribution centers reported staffing gaps of up to 25%. Robots fill the void; Asia-Pacific facilities expect 92% autonomous mobile robot penetration within five years=. AutoStore’s deployment at Master Electronics tripled pick rates and illustrates the productivity uplift when WMS software orchestrates goods-to-person workflows. Software that harmonizes human and robotic tasks is now a must-have for operators seeking both resiliency and cost control.

AI-driven predictive workflows lowering stock-outs

Generix embedded AI into its WMS at Cameron’s Specialty Coffee, cutting waste and improving on-time fill rates. Machine-learning models that blend historical demand, supplier performance, and external variables create accurate forecasts and automate replenishment triggers. IoT-based predictive maintenance can halve downtime by spotting equipment failures before they interrupt throughput. As supply chains continue to experience external shocks, predictive functionality becomes a decisive differentiator for WMS vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront investment and integration effort | -2.8% | Global, stronger on SMEs | Short term (≤ 2 years) |

| Legacy-system complexity and cybersecurity risk | -2.1% | North America and Europe | Medium term (2-4 years) |

| Data-sovereignty limits on cross-border cloud hosting | -1.6% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| Shortage of domain-specialized WMS talent | -1.3% | Global, acute in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront investment and integration effort

Deployment costs range from USD 5,000 to USD 22,000 per facility, and multi-month rollouts strain cash flows for small and mid-size firms. Integration with ERP, TMS, and automation hardware often doubles original budgets. Dietz and Watson needed a phased six-month schedule to avoid major disruption during its Softeon implementation. The capital hurdle sustains a two-tier market in which large enterprises keep widening their operational advantage.

Legacy-system complexity and cybersecurity risk

Many warehouses still run decade-old ERP suites that lack modern APIs, so teams rely on middleware that adds cost and expands the attack surface. Cyber incidents targeting operational systems rose, and outdated inventory tools offer easy entry points for ransomware ==. RFgen research shows patch delays exceed six months at 40% of sites. Security and technical debt can derail projects or force compromises that blunt expected efficiency gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominance Accelerates Digital Transformation

Cloud-based platforms accounted for 55.21% of the warehouse management system market in 2025 and are on track for a 19.12% CAGR to 2031. Vendors deliver quarterly feature releases that sharpen functionality without user downtime. Multi-location operators gain centralized visibility over inventory and labor activities, which boosts fulfillment accuracy and lowers overhead. On-premise deployments still serve defense and regulated sectors that require complete data control. Hybrid models emerge where firms keep sensitive workloads onsite but use cloud modules for analytics and collaboration. The warehouse management system market size for cloud deployments will likely surpass USD 6.7 billion by 2031, reflecting sustained investment in subscription models.

Lower entry costs attract mid-market firms that previously relied on manual spreadsheets. API connectors link warehouse management system market applications directly to ecommerce storefronts, ERP suites, and transport systems. This interoperability reduces integration timelines from months to weeks and supports rapid scaling during peak seasons. As advanced analytics and robotics interfaces ship as cloud services, on-premise buyers face functional gaps. Consequently, most new contracts in the warehouse management system market are awarded to cloud-native vendors that guarantee 99.9% availability.

By Component: Services Lead While Software Innovation Accelerates

Services secured 80.05% revenue share in 2025 because every large project still requires process redesign, data migration, and change management. Consulting teams configure slotting rules, labor standards, and automation pathways that fit unique operations. Nevertheless, software revenue is growing faster at a 16.92% CAGR. Modular codebases let customers add functions such as AI labor forecasting without full re-implementation.

The warehouse management system market size for software is forecast to double by 2031 as subscription licensing replaces perpetual models. Continuous delivery keeps features current, minimizing disruptive big-bang upgrades. Managed-services contracts rise because operators prefer handing system maintenance to specialists. Training services also expand as warehouses blend human labor with robots, creating new workflows that require upskilling. Overall, services and software remain interdependent, but innovation velocity now stems from the software layer.

By Tier Type: Advanced Systems Drive Market While Intermediate Solutions Gain Momentum

Tier 1 suites held 35.95% of 2025 revenue due to their ability to orchestrate complex multi-site networks with high-volume automation. These platforms integrate inventory, labor, yard, and transport modules on one data model, supporting near-instant decision making. However, cost and complexity limit Tier 1 penetration beyond global enterprises.

Intermediate Tier 2 solutions will see an 18.1% CAGR to 2031 as cloud economics make advanced functionality affordable to mid-size distributors. The warehouse management system market share for Tier 2 will thus expand as modular add-ons let firms start small and upgrade over time. Tier 3 basic offerings remain relevant for simple storage needs yet risk replacement when users outgrow static pick-list workflows. Converging architectures blur historical tier definitions, letting vendors upsell existing customers rather than lose them to rivals.

By End-User Industry: Manufacturing Leadership Challenged by Logistics Growth

Manufacturing commanded 30.22% of warehouse management system market revenue in 2025. Plant-attached warehouses depend on tight integration between production lines and storage zones to minimize work-in-process buffers. Traceability mandates in pharmaceuticals and automotive drive further investment.

Transportation and logistics providers will outpace all verticals with an 18.32% CAGR. Multi-client operations need highly configurable rules and self-service portals that Tier 1 or Tier 2 suites deliver. The warehouse management system market size for 3PL contracts will therefore rise sharply as retailers outsource fulfillment. Food and beverages, healthcare, and consumer goods maintain steady adoption because shelf-life control and regulatory compliance remain essential. Emerging industries such as renewable-energy components enter the market as they scale distribution networks.

Geography Analysis

North America’s 35.55% share in 2025 reflects a mature ecommerce base and early adoption of automation. United States retailers expanded regional fulfillment networks to cut last-mile costs, while Canadian operators manage seasonal swings in resource exports. Mexico’s nearshoring wave drives modern WMS rollouts in maquiladora hubs. Labor gaps raise operating costs, so 70% of regional 3PLs now budget automation projects to protect margins .

Asia-Pacific is forecast to record a 18.74% CAGR through 2031, the fastest worldwide. Governments channel more than USD 200 billion into logistics corridors, smart ports, and bonded warehouses. Chinese e-commerce giants build multilevel automated facilities, while India’s fulfillment centers expand in tier-2 cities. Japan and South Korea apply robotics to counter aging-workforce constraints. Southeast Asian operators deploy cloud WMS to coordinate cross-border sales across fragmented markets. Combined, these trends will push the warehouse management system market size for Asia-Pacific above North America before 2030.

Europe posts steady growth because Industry 4.0 and sustainability rules require granular material tracking. The United Kingdom and Germany lead with advanced omnichannel networks, whereas France and Spain position regional hubs near major ports. GDPR and local data-storage mandates complicate cloud deployments, opening space for providers that guarantee regional hosting. Middle East and Africa see early-stage adoption centered on Gulf logistics parks. South America shows incremental gains, driven by Brazilian online retail and Argentina’s agribulk exports. Collectively, these regions keep global demand diversified and resilient.

Mordor Intelligence provides coverage of the warehouse management system (wms) market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

Market concentration is moderate. Manhattan Associates, SAP, Oracle, and Blue Yonder anchor the top tier with full-suite offerings and large partner ecosystems. Manhattan crossed USD 1 billion revenue in 2025, and record RPO bookings show sustained pipeline strength. SAP’s cloud revenue reached EUR 4.99 billion in Q1 2025, with warehouse functions embedded in its ERP suite. These incumbents leverage integration breadth and upgrade paths to retain enterprise clients.

Challengers gain ground through vertical specialization and faster time-to-value. LuminX raised USD 5.5 million to embed vision-language AI at the edge, promising better pick accuracy without heavy server footprints[3]Reporter, “LuminX Funding Round,” Unite.ai, unite.ai. Extensiv focuses on mid-market 3PLs with turnkey SaaS that deploys in weeks. Vendors differentiate via robotics orchestration, carbon-dashboard modules, and no-code workflow design. Patent filings around multi-cluster routing and autonomous inventory carry suggest accelerated innovation.

Strategic alliances intensify. GXO partnered with Blue Yonder to speed onboarding for global clients. Hardware-software cooperation also deepens as robot makers pre-integrate control APIs into partner WMS. Vendors expand managed-service arms to capture lifecycle revenue. As the warehouse management system market continues double-digit growth, competition will hinge on ecosystem reach, modular extensibility, and rapid ROI proof points.

Warehouse Management System (WMS) Industry Leaders

SAP SE

Oracle Corporation

Manhattan Associates

Blue Yonder Group Inc.

Infor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: LuminX secured USD 5.5 million in Series A funding to advance vision-language models for edge-deployed warehouse intelligence.

- May 2025: GXO Logistics formed a partnership with Blue Yonder to enhance WMS-enabled service speed and flexibility for global clients.

- April 2025: SAP reported Q1 2025 cloud revenue of EUR 4.99 billion, up 27% year-over-year, reflecting stronger demand for integrated WMS functions.

- January 2025: Manhattan Associates achieved USD 1 billion annual revenue with record Q4 2024 sales and 25% RPO growth.

Global Warehouse Management System (WMS) Market Report Scope

Warehouse Management System (WMS) is a software application designed to support and optimize warehouse operations and distribution center management. It helps control and manage various tasks such as inventory tracking, order picking, packing, shipping, and receiving. A WMS improved efficiency by automating processes, providing real-time data for inventory levels, and facilitating better space utilization. By doing so, it enhances accuracy, reduces labor costs, minimizes errors and increases overall productivity in the supply chain.

The study tracks the revenue generated from the sale of warehouse management software (WMS) products and services by various WMS developers worldwide. It also tracks the key market parameters, underlying growth influencers, and major manufacturers operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The warehouse management system (WMS) market is segmented by deployment type (on-premises WMS, cloud-based WMS, and hybrid WMS), by end user vertical (retail, manufacturing, food and beverage, healthcare and pharmaceuticals, logistics and transportation, automotive, consumer goods, and others), and by geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| On-Premise WMS |

| Cloud-Based WMS |

| Hybrid WMS |

| Software |

| Services (Implementation, Support, Training) |

| Tier 1 (Advanced) |

| Tier 2 (Intermediate) |

| Tier 3 (Basic) |

| Retail and E-commerce |

| Third-Party Logistics (3PL) |

| Manufacturing |

| Food and Beverages |

| Healthcare and Pharma |

| Automotive |

| Consumer Goods |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| By Deployment Type | On-Premise WMS | ||

| Cloud-Based WMS | |||

| Hybrid WMS | |||

| By Component | Software | ||

| Services (Implementation, Support, Training) | |||

| By Tier Type (System Sophistication) | Tier 1 (Advanced) | ||

| Tier 2 (Intermediate) | |||

| Tier 3 (Basic) | |||

| By End-User Industry | Retail and E-commerce | ||

| Third-Party Logistics (3PL) | |||

| Manufacturing | |||

| Food and Beverages | |||

| Healthcare and Pharma | |||

| Automotive | |||

| Consumer Goods | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current size of the warehouse management system market?

The market stands at USD 4.77 billion in 2026 and is projected to rise to USD 10.89 billion by 2031.

Which deployment model is growing fastest?

Cloud-based platforms are expanding at a 19.12% CAGR as firms prefer scalable subscription services.

Which region is expected to lead future growth?

Asia-Pacific is forecast to register the highest regional CAGR of 18.74% because of heavy logistics investment and surging e-commerce demand.

Why are services such a large revenue component?

Services account for 80.05% of 2025 revenue because implementation, integration, and optimization work remain complex and labor-intensive.

Page last updated on: