Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

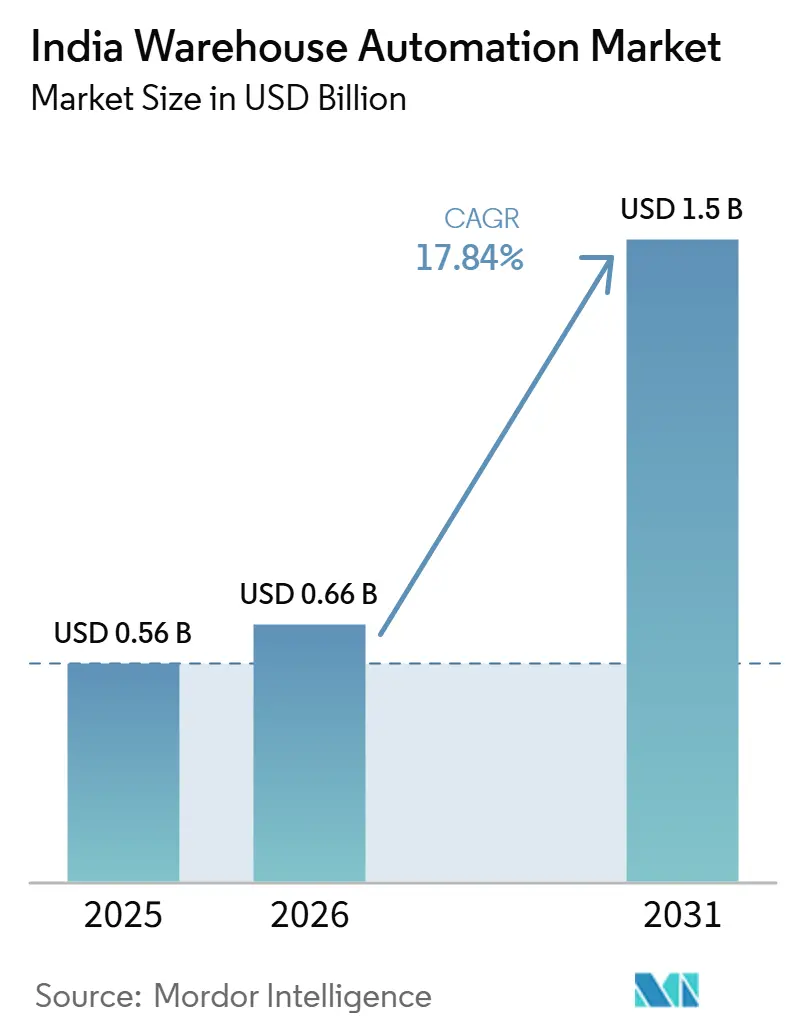

| Base Year Market Size (2025) | USD 0.56 Billion |

| Market Size (2026) | USD 0.66 Billion |

| Market Size (2031) | USD 1.5 Billion |

| Growth Rate (2026 - 2031) | 17.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Warehouse Automation Market Analysis by Mordor Intelligence

The India Warehouse Automation Market size was valued at USD 0.56 billion in 2025 and is estimated to grow from USD 0.66 billion in 2026 to reach USD 1.5 billion by 2031, at a CAGR of 17.84% during the forecast period (2026-2031).

Strong e-commerce demand, GST-led consolidation, and Production-Linked Incentive (PLI)–driven SKU proliferation are pushing enterprises to replace labor-intensive processes with automated systems. Quick-commerce platforms that promise 10-minute deliveries are reshaping fulfillment priorities, while rising wage inflation in Tier-1 logistics hubs is tightening the payback window for automation investments. Vendors are responding with modular, upgradeable solutions that lower upfront costs and de-risk technology adoption. Market leaders are also localizing production, evidenced by Daifuku’s 2025 plant launch, which shortens lead times and cushions foreign-exchange exposure. Together, these forces are expected to keep the India warehouse automation market on an accelerated adoption curve well beyond 2030.

Key Report Takeaways

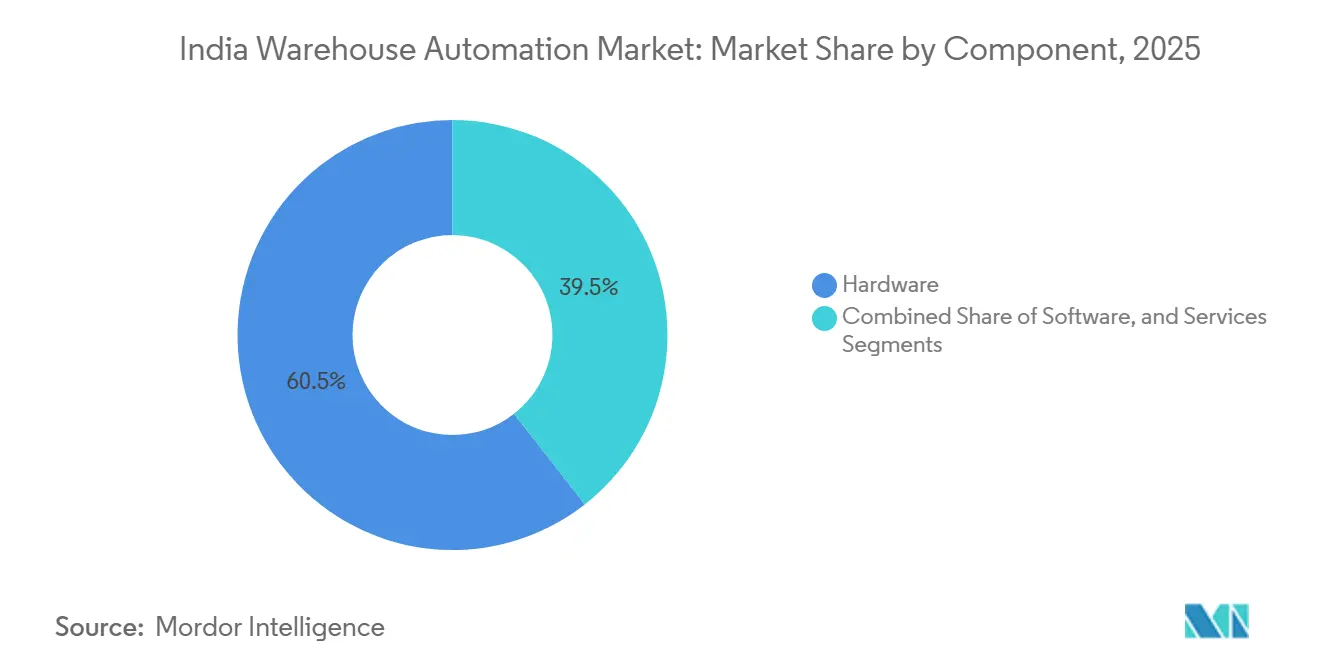

- By component, hardware captured 60.55% of India warehouse automation market share in 2025, while software recorded the highest projected CAGR of 27.40% through 2031.

- By automation level, semi-automated systems accounted for 48.60% of the India warehouse automation market size in 2025; fully automated robotics and AS/RS solutions are projected to grow at a 27.10% CAGR to 2031..

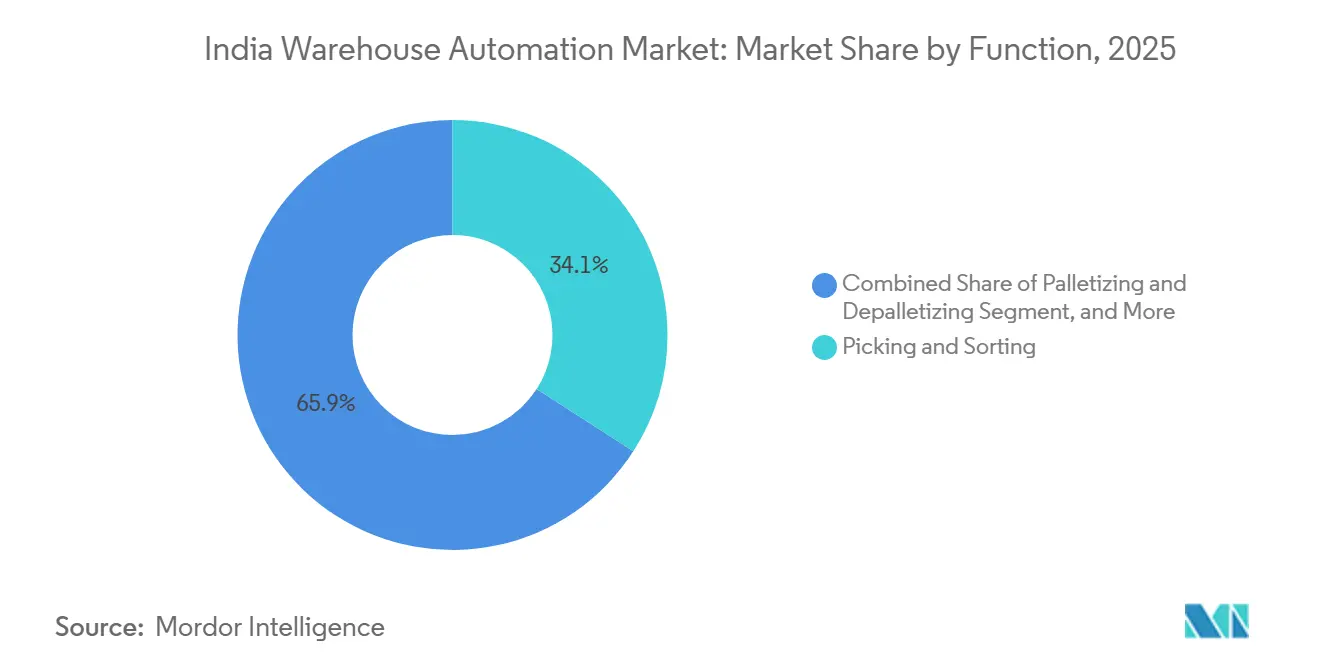

- By function, picking and sorting led with 34.10% revenue share in 2025, whereas transportation and AGV/AMR solutions are forecast to expand at a 26.90% CAGR over the same period.

- By end-user industry, e-commerce and 3PLs made up 35.10% of 2025 demand, yet pharmaceuticals and healthcare are expected to post the fastest 26.80% CAGR through 2031.

- Addverb Technologies, GreyOrange, Daifuku, Swisslog, and Honeywell Intelligrated together held roughly 31% of 2025 revenue, indicating a moderately fragmented competitive field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Warehouse Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth of Indian e-commerce | +8.2% | National; early gains in Mumbai, Delhi, Bangalore | Short term (≤ 2 years) |

| Fast-track GST-led consolidation of warehouses | +6.5% | National; industrial corridors | Medium term (2-4 years) |

| GST e-invoicing APIs adoption | +4.1% | National; organized retail | Medium term (2-4 years) |

| Government PLI schemes boosting SKU counts | +3.8% | Gujarat, Maharashtra, Karnataka | Long term (≥ 4 years) |

| 10-minute quick-commerce fulfillment demand | +2.9% | Metro cities; Tier-2 urban centers | Short term (≤ 2 years) |

| Labor-shortage spikes in logistics hubs | +2.1% | Mumbai, Delhi, Bangalore, Chennai | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of Indian E-commerce

India’s online retail sector is on track to reach USD 300 billion by 2030, propelled by a surge in grocery orders and a 41.5% sales contribution from Tier-2 and Tier-3 cities in 2022. Traditional block-stack warehouses can no longer support same-day or 10-minute expectations, prompting 4,000+ dark stores to install automated picking pods and robotic sorters. Logistics costs, which consumed 7.8-8.9% of GDP in 2024, are forecast to fall as automated hubs cut mis-picks and shrink delivery kilometers. Forward-looking operators are layering AI-based inventory engines over AS/RS grids to orchestrate multi-channel stock pools in real time.

Fast-track GST-Led Consolidation of Warehouses

GST removed state-border inventory buffers, allowing national distribution networks to flourish. Average facility size jumped from 50,000 sq ft in 2023 to over 200,000 sq ft by 2025, cementing the economic case for high-bay AS/RS and shuttle systems. Pallet counts per site often top 10,000, encouraging multilevel clad-rack designs that maximize vertical space while trimming civil costs. FMCG and pharmaceuticals benefit most because consolidated nodes simplify batch traceability and cold-chain compliance. Rental rates climbed 5% in Pune and NCR during 2024 as developers raced to deliver Grade-A boxes with flat floors and 11-12 m clear heights, prerequisites for fast-moving cranes.

Adoption of Goods and Services Tax E-invoicing APIs

Mandatory e-invoicing has tethered warehouse management systems (WMS) directly to government databases, forcing real-time SKU-level visibility. Early adopters discovered that the same data pipes drive predictive slotting algorithms that cut carrying costs by up to 20% while lifting order accuracy to 98%. As manual documentation cannot keep pace, software spend is outpacing hardware for the first time in brown-field upgrades. API-native WMS platforms are now gateways to broader AI deployments spanning labor scheduling, demand sensing, and fleet routing.

Government PLI Schemes Boosting SKU Proliferation

The USD 24 billion PLI budget spanning electronics, automotive, and pharma has multiplied part numbers from hundreds to thousands per product line. Electronics exporters, for example, now juggle high-mix kits that collapse batch sizes and overwhelm manual pick faces. To cope, firms are installing put-to-light walls and piece-picking robots that sustain 1,200 lines per hour with near-zero errors. PLI also reimburses 4-6% of capital outlays, effectively shaving years off automation payback calculations and creating a virtuous adoption loop in clusters such as Noida and Sriperumbudur.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant low-cost manual labor pool | -4.8% | Rural and semi-urban regions | Long term (≥ 4 years) |

| High upfront CAPEX of AS/RS and robotics | -3.2% | National; SME adoption | Medium term (2-4 years) |

| Fragmented SME-owned warehouse footprint | -2.1% | Tier-2 and Tier-3 cities | Long term (≥ 4 years) |

| Inconsistent power and floor-flatness norms | -1.9% | Infrastructure-light industrial areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Abundant Low-cost Manual Labor Pool

With 500 million workers in the informal sector, entry-level wages of Rs 15,000-20,000 per month extend the payback window for mechanization. In Tier-3 centers, costs are 30-40% lower, tempting SMEs to delay automation. Yet wage inflation topped 15-20% in Mumbai and Delhi during 2024 as warehouses competed for skilled handlers. Simultaneously, younger workers are pivoting to higher-skill jobs, eroding labor quality and fueling interest in semi-automated aids such as voice picking and goods-to-person carts.

High Upfront CAPEX of AS/RS and Robotics

Medium-scale AS/RS installations demand USD 2-5 million, while fully robotic hubs can cost USD 10-20 million. Traditional lending channels hesitate because ROI calculations wobble if wage escalation slows. Vendors now market automation-as-a-service plans that trim entry CAPEX by 60-70% and tie monthly fees to productivity gains. PLI rebates plus service models are slowly unlocking SME demand, though broad penetration awaits cheaper domestic component ecosystems promised by the Electronics Component Manufacturing Scheme 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces Software Disruption

Hardware commanded 60.55% of 2025 revenue, underscoring India warehouse automation market reliance on conveyors, shuttle racks, and robotic arms. Large brownfield campuses in Bhiwandi and Sriperumbudur tapped high-bay AS/RS to quadruple pallet density within existing footprints, reinforcing hardware’s role as the operational backbone. Yet as installed bases mature, decision-makers are shifting budget toward cloud WMS, digital twins, and AI engines that unlock latent capacity and lift utilization above 85%.

Software’s 27.40% CAGR through 2031 mirrors this pivot. SaaS platforms such as Addverb’s Mobinity orchestrate multi-vendor fleets and inject machine learning into slotting, labor assignment, and energy management. Retro-fits dominate 2026-2028 spending cycles as operators realize that data-rich control layers deliver step-change returns on earlier hardware layouts. Services follow suit because integrators are needed to weave siloed machines into unified, API-compliant ecosystems.

By Automation Level: Semi-Automated Systems Bridge Manual-to-Robotic Transition

Semi-automated solutions held 48.60% of India warehouse automation market share in 2025, reflecting a pragmatic appetite for incremental change. Put-to-light stations, carousel modules, and lift trucks fitted with real-time location sensors typically raise productivity 40-60% but cost 30-50% less than full robotics. Enterprises pair these tools with flexible financing, testing workflows before upgrading to goods-to-person bots.

Fully automated robotics, advancing at 27.10% CAGR, are surfacing in pharmaceutical and cold-chain facilities where compliance fines dwarf equipment costs. Vendors bundle environmental monitoring, traceability logs, and AI vision into turnkey cells that slash error rates to under 0.1%. Price parity is also improving as domestic component lines scale under the Component Manufacturing Scheme. By 2031, industry consensus expects a 60-40 split favoring fully automated formats in greenfield builds.

By Function: Transportation and AGV/AMR Solutions Accelerate Beyond Traditional Picking

Picking and sorting led 2025 spending with 34.10% of the India warehouse automation market, powered by e-commerce’s single-piece orders. But transportation and AGV/AMR fleets are outpacing at a 26.90% CAGR, reflecting a shift toward end-to-end flow orchestration. Facilities once stitched together by fixed conveyors are migrating to robot swarms that reroute around congestion and reconfigure for peak seasons.

Modern AGV-ready floors enable mission planners to choreograph tasks from inbound staging to dock allocation, cutting travel distances by up to 45%. Vision-based inspection is another fast-emerging use case as pharma warehouses automate batch-label verification to satisfy global audit trails. Packaging and labeling modules that personalize orders for D2C brands are also rising, completing the loop from storage to shipment without manual touches.

By End-user Industry: Pharmaceuticals Emerge as Automation Growth Leader

E-commerce and India 3PL providers controlled 35.10% of 2025 shipments, leveraging scale to pilot early robotics. However, pharmaceuticals and healthcare will chart the fastest 26.80% CAGR, buoyed by strict temperature and traceability mandates. Facilities near Hyderabad’s Genome Valley already staff robotic cold rooms where ambient variation stays within ±1 °C, ensuring vaccine integrity for export consignments.

Automotive and electronics follow close behind, aided by JIT sequencing and PLI-linked output boosts. Electronics assemblers in Greater Noida now use shuttle-based mini-load stores that feed SMT lines every three minutes. FMCG and retail are banking on shelf-ready mixed-case palletizers that blend SKU variety with labor savings, while chemical majors retrofit hazardous-zone robots to reduce human exposure risks.

Geography Analysis

Western and southern states anchor more than 60% of India's warehouse automation market deployments. Maharashtra benefits from Mumbai’s port and Pune’s auto corridor, attracting USD 15.1 billion FDI in FY23 and encouraging turnkey fulfillment platforms that compress lead times from port to shelf. Gujarat’s petrochemical and emerging battery clusters add scale, with clad-rack projects in Dahej reaching 40-m heights. Karnataka blends tech expertise with manufacturing breadth; Bengaluru-based integrators co-develop AI modules and export them alongside robots, reinforcing local adoption loops.

Tamil Nadu leverages Chennai’s auto and electronics bases to pilot dark-room inspection bots and collaborative palletizers, aligning with ISO 26262 traceability. Northern India, especially the Delhi-NCR belt, is witnessing a surge in multi-story e-commerce hubs that concentrate last-mile routes within 30 km radial networks. Although infrastructure bottlenecks, power fluctuations, and sub-spec floor flatness slow adoption in certain industrial pockets, developers are investing in transformer redundancy and laser-graded slabs to qualify for high-speed cranes.

Eastern and northeastern corridors are at an early stage but could unlock new demand as ports like Paradip and Dhamra scale container throughput. Government-funded multimodal logistics parks along the Bharatmala routes promise integrated rail-road nodes, offering a blank slate for greenfield automated hubs once energy reliability improves. By 2030, analysts expect the India warehouse automation market to see its geographic split diversify beyond the current west-south concentration.

Competitive Landscape

India warehouse automation market competition remains moderately fragmented, with the top five vendors holding roughly one-third of 2024 revenue. Domestic champions Addverb Technologies and GreyOrange leverage local cost structures and regulatory insight to outmaneuver global rivals in price-sensitive bids. Addverb’s Atom sortation robot and GreyOrange’s Butler goods-to-person system are now exported to over 60 countries, demonstrating design credibility.

Global integrators are responding by localizing production. Daifuku’s April 2025 plant in Maharashtra trims import duties and slashes lead times by 30%. Swisslog is partnering with Indian civil contractors to install carton shuttle systems in turnkey mode, while Honeywell Intelligrated bundles IoT sensors with Manhattan WMS connectors to appeal to data-hungry 3PLs.

Technology roadmaps emphasize platform ecosystems over stand-alone machines. Vendors increasingly pitch AI-augmented orchestration layers that unify AS/RS, AMRs, and yard-management modules under one UI. Flexible pricing ranging from pay-per-pick to revenue-sharing is widening SME access. Certification under the Bureau of Indian Standards’ 2024 auto-storage code is now a prerequisite for pharma contracts, further raising the technology bar and incentivizing R&D partnerships with academic institutes in IIT-Madras and IISc-Bengaluru.

India Warehouse Automation Industry Leaders

Addverb Technologies Pvt. Ltd

Alligator Automations

Alstrut India Private Limited

Armstrong Machine Builders Pvt. Ltd

Clearpack India Pvt. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Daifuku launched a new manufacturing plant in India, boosting local supply of AS/RS and material-handling equipment.

- March 2025: Government scaled up PLI allocations for electronics, automobiles, and textiles, intensifying SKU complexity and automation demand.

- February 2025: Daifuku released a trend report highlighting India’s shift toward clad-rack warehouses and EV-battery logistics.

- January 2025: Armstrong Dematic unveiled AI- and BI-driven intralogistics platforms for omnichannel fulfillment.

India Warehouse Automation Market Report Scope

Warehouse automation is the process of automating the movement of inventory into, within, and out of warehouses to customers with minimal human assistance. Warehouse automation refers to devices or systems that streamline repetitive warehouse operations and make them less labor-intensive to generate greater operational efficiencies. Warehouse automation is an integral entity of supply chain optimization, as it reduces time, effort, and errors caused due to manual or repetitive tasks.

The market size for the Indian warehouse automation market (henceforth referred to as the market studied) was evaluated by analyzing the independent type of solutions, such as conveyor and sortation systems, palletizers, mobile robots (AGV/AMR), vision inspection equipment, and labeling equipment that are employed in the FMCG industry. The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the market study, which supports the market estimations and growth rates over the forecast period. The report also covers the major factors impacting the market growth regarding drivers and restraints. The study analyzes the overall impact of the COVID-19 pandemic and addresses the market dynamics. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Component

| Hardware |

| Software |

| Services |

By Automation Level

| Basic Mechanization |

| Semi-Automated Systems |

| Fully Automated (Robotics/AS-RS) |

By Function

| Picking and Sorting |

| Palletizing and Depalletizing |

| Storage and Retrieval |

| Packaging and Labelling |

| Vision Inspection and QC |

| Transportation and AGV/AMR |

By End-user Industry

| E-commerce and 3PL |

| FMCG and Retail |

| Pharmaceuticals and Healthcare |

| Automotive |

| Electronics |

| Other End-user Industries |

| By Component | Hardware |

| Software | |

| Services | |

| By Automation Level | Basic Mechanization |

| Semi-Automated Systems | |

| Fully Automated (Robotics/AS-RS) | |

| By Function | Picking and Sorting |

| Palletizing and Depalletizing | |

| Storage and Retrieval | |

| Packaging and Labelling | |

| Vision Inspection and QC | |

| Transportation and AGV/AMR | |

| By End-user Industry | E-commerce and 3PL |

| FMCG and Retail | |

| Pharmaceuticals and Healthcare | |

| Automotive | |

| Electronics | |

| Other End-user Industries |

Key Questions Answered in the Report

How large will India’s warehouse automation market be by 2031?

The India Warehouse Automation Market size is estimated at USD 0.56 billion in 2025, and is expected to reach USD 1.5 billion by 2031, at a CAGR of 17.84% during the forecast period (2026-2031).

Which segment is growing fastest in India’s automation deployments?

Software solutions are expanding at the fastest rate as firms overlay AI-enabled orchestration on existing hardware.

Why are pharmaceuticals emerging as the leading adopter of warehouse automation?

Stringent temperature, batch-tracking, and regulatory demands make robotics and AS/RS critical for compliance and export readiness.

What geographic hotspots are driving automation demand?

Maharashtra, Gujarat, Karnataka, Tamil Nadu, and the Delhi-NCR corridor house most large-scale projects due to manufacturing density and logistics infrastructure.

How are vendors addressing high upfront capital barriers?

Automation-as-a-service models and PLI rebates reduce initial outlays by up to 70% while aligning fees with realized productivity gains.

Page last updated on: