India Plastic Industry Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

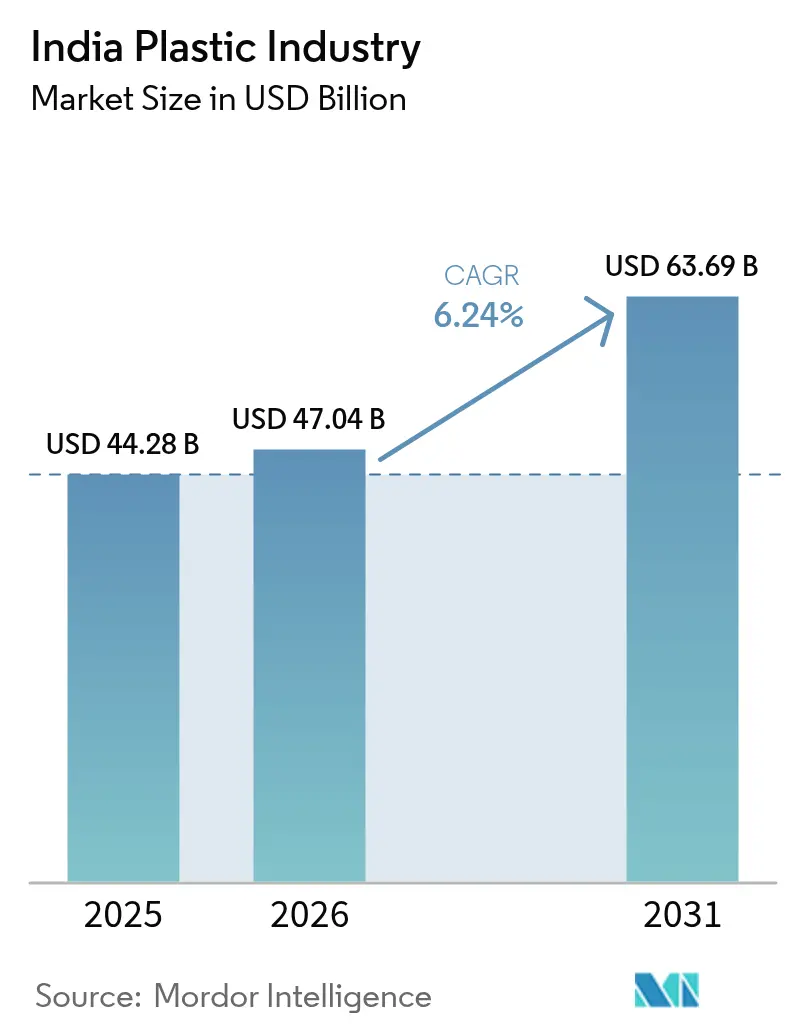

| Base Year Market Size (2025) | USD 44.28 Billion |

| Market Size (2026) | USD 47.04 Billion |

| Market Size (2031) | USD 63.69 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Plastic Industry Analysis by Mordor Intelligence

The India Plastic Industry size is projected to be USD 44.28 billion in 2025, USD 47.04 billion in 2026, and reach USD 63.69 billion by 2031, growing at a CAGR of 6.24% from 2026 to 2031. Strong public-sector incentives such as the Production-Linked Incentive scheme, large-scale infrastructure programs and accelerating consumer demand across packaging, construction and mobility are sustaining this double-digit trajectory. Western India remains the consumption epicenter, powered by Gujarat’s and Maharashtra’s dense petrochemical clusters, while specialty grades are gaining share as brands look for lightweighting and recyclability. Supply-side additions in polyolefins and PVC, amplified by recent brownfield and greenfield investments, are easing the country’s long-standing dependence on imports. Meanwhile, rising waste-management regulations, volatile feedstock costs and rapid adoption of digital production controls are shaping a sharper focus on operational efficiency and circularity.

Key Report Takeaways

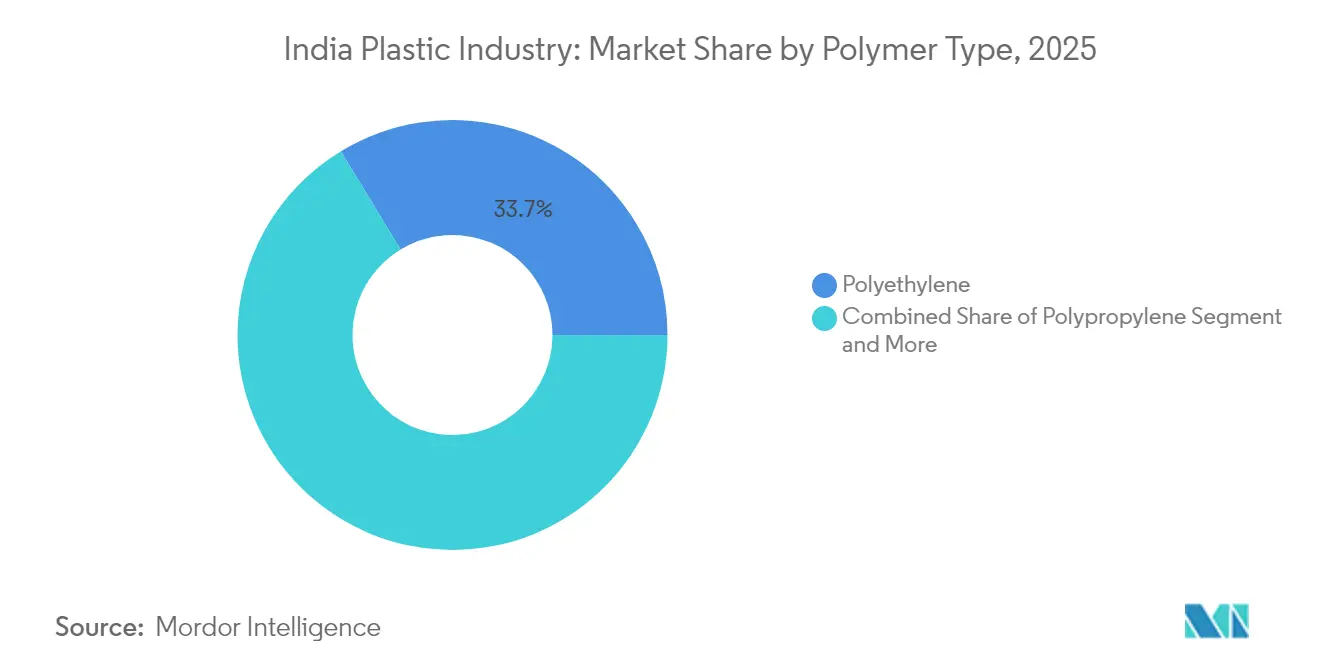

- By polymer type, polyethylene led with 33.68% of the India plastic industry market share in 2025; biodegradable/bio-plastics are projected to advance at a 6.82% CAGR to 2031.

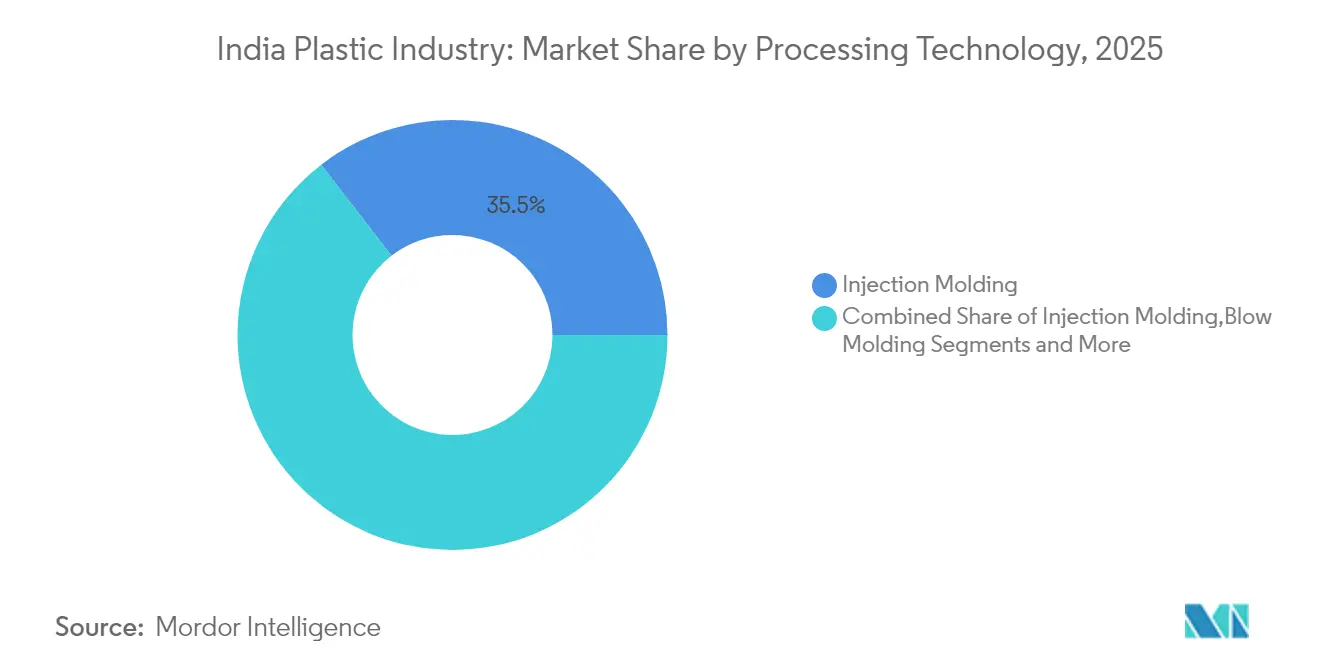

- By processing technology, injection molding commanded 35.45% share of the India plastic industry market size in 2025, while blow molding is poised for a 6.65% CAGR through 2031.

- By specialty and bioplastics type, the segment accounted for approximately USD 2.6–2.9 billion of the India plastics market size in 2025, with demand projected to grow at a 9.5–11.0% CAGR during 2025–2031.

- By application, packaging accounted for 41.62% of the India plastic industry market size in 2025 and is expanding at a 6.44% CAGR through 2031; healthcare and pharmaceuticals post the fastest segment CAGR at 6.56%.

- By region, Western India captured 46.55% revenue share in 2025; South India is forecast to grow at an 7.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Plastic Industry Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Government PLI scheme catalyzing polymer capacity in Gujarat | +2.1% | Western India with nationwide spillovers | Medium term (2–4 years) |

| Quick-commerce demand for high-rigidity food containers | +1.7% | Tier-I urban centers | Short term (≤ 2 years) |

| Swachh Bharat Phase II spurring HDPE pipe upgrades | +1.4% | Water-stressed urban clusters | Medium term (2–4 years) |

| EV lightweighting pushing engineering plastics in two-wheelers | +1.2% | Western and Southern hubs | Medium term (2–4 years) |

| Pharma export surge lifting medical-grade resin offtake | +0.9% | Gujarat and Maharashtra | Short term (≤ 2 years) |

| Tier-II mall construction raising PVC profiles demand | +0.8% | Nationwide Tier-II cities | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government PLI Scheme Accelerating Polymer Capacity Expansions in Gujarat

Investment incentives under the PLI program are funneling unprecedented capital into Gujarat’s Jamnagar-Dahej petrochemical corridor. Projects such as Reliance Industries’ 1.5 MTPA PVC complex and Adani’s 2 MTPA PVC build-out are expected to narrow the 2.5 million-tonne local supply gap by 2027.[1]Manufacturing Today India, “Adani Group Resumes USD 4 Billion PVC Plant Project for 2026 Completion,” manufacturingtodayindia.com Alongside output gains, firms are deploying chemical-recycling technologies that convert mixed plastic waste into ISCC-Plus certified resins, positioning Gujarat as a regional circular-economy hub. Allied logistics upgrades, including dedicated polymer rail corridors, further strengthen the material flow from western coast ports to inland processors.

Quick-Commerce Boom Driving Demand for High-Rigidity Food Containers

Same-hour grocery delivery is reshaping rigid packaging specifications. Operators require containers that resist impact, maintain barrier integrity under rapid temperature swings and stack efficiently in micro-fulfilment centers. Injection-grade polypropylene and clarified random copolymers dominate current supply, but brand owners are piloting mono-material designs to comply with 2026 recyclability targets. Major rigid packaging converters have announced capacity additions in Maharashtra and Telangana to address forecast container demand growth above 15% annually.[2]Syed Ali, “Packaging Plastic Waste from E-commerce Sector,” ScienceDirect, sciencedirect.com

Swachh Bharat Phase II Fueling Urban HDPE Pipe Replacement

Municipal water boards are mandating corrosion-resistant HDPE piping for new sewerage lines and rehabilitation projects. Standard-dimension ratio (SDR) 11 and SDR 17 grades are preferred, given their strength-to-weight balance and leak-free butt-fusion joints. Pipe makers are ramping three-layer co-extrusion lines that embed recycled polymer in the middle layer while keeping virgin HDPE on outer surfaces to satisfy both cost and quality metrics. With 500+ towns set for upgrades by 2028, domestic pipe demand is forecast to exceed 1.2 million tonnes per year.[3]Central Pollution Control Board, “Standard Operating Procedure for Assessment & Characterization of Plastic Waste,” cpcb. nic. in

EV Lightweighting Strategy Boosting Engineering Plastics in Two-Wheelers

Electric scooter OEMs target a vehicle kerb-weight ceiling of 110 kg to meet customer range expectations. Glass-fiber-reinforced polypropylene, PA6/66 and PC-ABS blends now replace stamped steel in battery enclosures, side panels and subframes. Partnership models between resin suppliers and Tier-1 molders speed application development; cycle times of under 35 seconds are being achieved on multi-cavity molds outfitted with servo-electric drives. Southern clusters around Hosur and Krishnagiri host several of these dedicated engineering-plastic lines.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Single-Use Plastic Ban Escalating Compliance Costs for FMCG Packagers | -1.3% | Nationwide, with higher impact in urban centers | Short term (≤ 2 years) |

| Volatile Naphtha Feedstock Prices from Middle-East Tensions | -1.1% | Nationwide, with concentrated impact on manufacturing hubs | Short term (≤ 2 years) |

| Inter-State Waste Rules Causing Logistic Bottlenecks and Capacity Under-Utilization | -0.8% | Cross-state borders, particularly affecting recycling supply chains | Medium term (2-4 years) |

| Consumer Backlash on Microplastics in Packaged Drinking Water | -0.6% | Urban centers, particularly among higher-income demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Single-Use Plastic Ban Escalating Compliance Costs for FMCG Packagers

Ban enforcement has removed 19 disposable items from legal circulation, forcing brands to pivot toward paper laminates, biodegradable films or thicker reusable formats. Substitute materials cost at least 40% more than legacy LDPE flexibles, squeezing price-sensitive categories such as condiments and on-the-go beverages. Smaller converters report capital-expenditure hurdles in retrofitting extrusion-coating and lamination lines for alternative substrates.

Volatile Naphtha Feedstock Prices from Middle-East Tensions

Spot naphtha jumped 28% between April 2024 and March 2025, eroding ethylene cracker margins. To hedge exposure, Haldia Petrochemicals inked a decade-long supply deal with QatarEnergy for up to 2 million tonnes annually [economictimes.com]. Several producers are evaluating propane dehydrogenation and ethane imports as diversification strategies, but port constraints and refrigerant limitations temper near-term relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: Polyethylene Dominates Amid Bio-Shift

Polyethylene retained a 33.68% slice of the India plastic industry market in 2025, anchored by film and blow-molded container demand. High-density grades grew faster than low-density grades owing to pipe, cap and closure applications. The India plastic industry market size for biodegradable/bio-plastics is projected to widen at a 6.82% CAGR, as brands adopt PLA, PBS and PHA blends in serviceware and personal-care packaging. Polypropylene remains intrinsic to woven sacks, appliance housings and automotive trim, while PVC’s future hinges on the timely start-up of domestic chlor-alkali expansions.

Circularity gains momentum through mechanical and chemical recycling. India’s PET bottle stream already touches a 95% recovery rate, supported by well-organized informal collection networks. New depolymerization ventures in Gujarat intend to close the loop on polyester textiles, signalling a shift from export-oriented bottle flakes toward domestic resin circularity.

By Specialty and Bioplastics Type: Sustainability Drives Innovation

Biodegradable grades capture most venture attention, yet bio-based drop-in resins such as bio-PE and bio-PET are scaling faster in beverage and personal-care lines because they slot into existing molds without process change. Local compounders are experimenting with lignin-filled PLA and starch-grafted PBAT to cut cost premiums below 70% versus fossil-based equivalents. Certification schemes under the India Plastics Pact require 50% recycled content or biogenic feedstock in rigid packaging by 2030, pushing brand owners to lock in forward supply contracts.

Pilot‐scale projects in Karnataka and Tamil Nadu demonstrate enzymatic recycling of multilayer films into feedstock monomers. Although volumes remain small, successful commercialization would open pathways to recover up to 2 million tonnes of composite waste annually, mitigating landfill pressure.

By Processing Technology: Injection Molding Leads Transformation

Injection molding represented 35.45% of installed processing capacity in 2025, driven by automotive, appliance and consumer-goods tooling. High-cavitation machines above 450 tons are increasingly fitted with all-electric clamping systems that trim energy use by 20% and meet OEM sustainability scorecards. Blow molding grew at 6.65% CAGR on the back of single-serve beverage bottles and household cleaners. The India plastic industry market share for injection-molded parts will hold steady around one-third through 2031, while blow molding gains incremental points in personal-care and pharmaceutical packaging.

Extrusion lines for pipe and film benefit from multi-layer die heads that integrate recycled pellets in core layers without sacrificing outer surface aesthetics. Thermoforming, rotational molding and compression molding together form a niche but resilient 10% slice of capacity, serving ice-cream tubs, water tanks and melamine tableware respectively. Additive manufacturing shows promise for custom orthopedic devices and low-volume aerospace ducts, though material qualification remains a hurdle.

By Application: Packaging Dominates Amid Healthcare Surge

Packaging consumed 41.62% of polymer demand in 2025, equivalent to nearly 10 million tonnes. Rigorous e-commerce speed requirements elevate impact-resistant PP copolymers and clear PET. Flexible multilayer pouches still dominate salty snacks and confectionery, but mono-material PE-PE laminates grow fast as converters test EVOH-free oxygen barriers.

Healthcare uses absorb around 1 million tonnes of high-purity resins, rising at 6.56% CAGR to 2031. Syringe barrels, IV bags and diagnostic housings increasingly specify cyclic olefin copolymers and radiation-sterilizable PP. Construction remains PVC-heavy, while automotive embraces glass-filled PA and PC-ABS for weight savings. Electrical/electronics demand tracks upward with domestic television and refrigerator output.

Geography Analysis

Western India, anchored by Gujarat and Maharashtra, held 46.55% of polymer consumption in 2025, reflecting the co-location of refineries, crackers and downstream processors. The India plastic industry market size for this region is forecast to reach USD 30.55 billion by 2031 at a 6.79% CAGR, bolstered by coastal logistics and duty-free feedstock zones. Proximity to raw materials shortens pipeline supply chains and lowers conversion costs, allowing processors to price competitively in export bids.

South India follows as the fastest growing geography, projected to expand at an 7.05% CAGR through 2031. States such as Tamil Nadu, Telangana and Karnataka attract investment in engineering plastics, medical devices and electronics assembly, underpinning resin uptake. SEZ incentives around Chennai and Krishnagiri further boost the region’s pull for auto-component molders and EV start-ups.

North and East India record moderate but steady growth. Uttar Pradesh’s smart-city programs and Bihar’s irrigation upgrades maintain demand for PVC and HDPE pipe, while Odisha’s emerging petrochemical complex at Paradip may shift feedstock availability eastward, closing logistic gaps for processors in Kolkata’s hinterland. Across rural belts, micro-irrigation and affordable housing continue to generate baseline consumption, tempering regional volatility.

Competitive Landscape

Upstream supply is moderately consolidated. Reliance Industries, GAIL and Indian Oil collectively own about 55% of domestic polyolefin nameplate capacity. Reliance also pioneers chemical recycling, launching CircuRepol™ and CircuRelene branded resins certified by ISCC-Plus [indianchemicalnews.com]. Midstream PVC capacity is poised for shake-up as Adani’s 2 MTPA Mundra complex starts phasing in from 2026, while Reliance readies a 1.5 MTPA dual-site expansion.

Downstream conversion remains fragmented with over 30,000 mostly micro-small units. Supreme Industries leads organized pipe systems and is investing INR 11 billion to push annual capacity beyond 1 million tonnes by FY 2026 [tickertape.in]. Time Technoplast is scaling composite cylinder output and intermediate bulk containers to tap medium-haul logistics growth. Digitalisation differentiates larger processors; industry leaders report 95% forecast accuracy from AI-driven pricing and inventory models.

Entry barriers in specialty bio-resins and high-modulus engineering compounds are rising due to proprietary technology and certification costs. Global players entering with local partners—such as Loop Industries with Ester Industries—highlight collaboration as a pathway to scale novel chemistries under India’s cost constraints.

India Plastic Market Leaders

Reliance Industries Ltd

Indian Oil Corporation Ltd

GAIL (India) Ltd

Supreme Industries Ltd

Nilkamal Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Reliance Industries posted 11% YoY revenue growth in its Oil-to-Chemicals division, supported by higher domestic placement of gasoline, gasoil and ATF. The firm prepares a 1 million-tonne polyester capacity add-on and accelerates PVC

- February 2025: GAIL committed INR 300 billion over three years for additional petrochemical and pipeline assets, including the acquisition of JBF Petrochemicals’ PTA unit to broaden feedstock flexibility

- January 2025: The PetroChem Summit 2024 emphasized alignment with UN SDGs, propelling industry consensus on lifecycle assessments and quality control in specialty chemicals

- April 2024: Haldia Petrochemicals locked a 10-year naphtha purchase agreement with QatarEnergy for up to 2 million tonnes annually, insulating feedstock volatility

India Plastic Industry Report Scope

Plastics are organic materials similar to wood, paper, or wool. Plastics are produced using natural products, such as cellulose, coal, natural gas, salt, and crude oil. The report provides insights on technological advancements, various trends shaping the market, and government regulations on the industry. The report includes various players' revenues and key developments in the industry, accompanied by drivers, restraints, and opportunities. The Plastic Industry in India is segmented by type, technology, and application. By type, the market is segmented as traditional plastics, engineering plastics, and bioplastics. By technology, the market is segmented as blow molding, extrusion, injection molding, and other technologies. By application, the market is segmented as packaging, electrical and electronics, building and construction, automotive and transportation, housewares, furniture and bedding, and other applications. The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Polyethylene (LDPE, LLDPE, HDPE) |

| Polypropylene |

| Polyvinyl Chloride |

| Polyethylene Terephthalate (PET) |

| Polystyrene and EPS |

| Acrylonitrile Butadiene Styrene (ABS) |

| Polycarbonate |

| Others (PMMA, POM, etc.) |

| Biodegradable Bioplastics (PLA, PHA, Starch Blends) |

| Bio-Based Non-Biodegradable Plastics (Bio-PE, Bio-PET) |

| Injection Molding |

| Blow Molding |

| Extrusion |

| Thermoforming |

| Rotational Molding |

| Compression Molding |

| Additive Manufacturing (3D Printing) |

| Packaging | Rigid Packaging |

| Flexible Packaging | |

| Building and Construction | |

| Automotive and Transportation | |

| Electrical and Electronics | |

| Agriculture and Irrigation | |

| Healthcare and Pharmaceuticals | |

| Consumer Goods and Housewares | |

| Furniture and Bedding | |

| Others (Textiles, Sports and Leisure) |

| West India (Gujarat, Maharashtra, Goa) |

| North India (Delhi-NCR, Uttar Pradesh, Punjab, Haryana, Rajasthan) |

| South India (Tamil Nadu, Karnataka, Telangana, Andhra Pradesh, Kerala) |

| East and North-East India (West Bengal, Odisha, Bihar, Assam and NE States) |

| By Polymer Type | Polyethylene (LDPE, LLDPE, HDPE) | |

| Polypropylene | ||

| Polyvinyl Chloride | ||

| Polyethylene Terephthalate (PET) | ||

| Polystyrene and EPS | ||

| Acrylonitrile Butadiene Styrene (ABS) | ||

| Polycarbonate | ||

| Others (PMMA, POM, etc.) | ||

| By Specialty and Bioplastics Type | Biodegradable Bioplastics (PLA, PHA, Starch Blends) | |

| Bio-Based Non-Biodegradable Plastics (Bio-PE, Bio-PET) | ||

| By Processing Technology | Injection Molding | |

| Blow Molding | ||

| Extrusion | ||

| Thermoforming | ||

| Rotational Molding | ||

| Compression Molding | ||

| Additive Manufacturing (3D Printing) | ||

| By Application | Packaging | Rigid Packaging |

| Flexible Packaging | ||

| Building and Construction | ||

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Agriculture and Irrigation | ||

| Healthcare and Pharmaceuticals | ||

| Consumer Goods and Housewares | ||

| Furniture and Bedding | ||

| Others (Textiles, Sports and Leisure) | ||

| By Region (India) | West India (Gujarat, Maharashtra, Goa) | |

| North India (Delhi-NCR, Uttar Pradesh, Punjab, Haryana, Rajasthan) | ||

| South India (Tamil Nadu, Karnataka, Telangana, Andhra Pradesh, Kerala) | ||

| East and North-East India (West Bengal, Odisha, Bihar, Assam and NE States) | ||

Key Questions Answered in the Report

What is the current size of the India plastic industry?

The market is worth USD 47.04 billion in 2026 and is projected to hit USD 63.69 billion by 2031.

Which segment holds the largest India plastic industry share?

Packaging leads with 41.62% share in 2025, driven by e-commerce and food-service growth.

How fast are biodegradable plastics growing in India?

Biodegradable and bio-based plastics are expanding at a 6.82% CAGR through 2031.

Which region in India consumes the most plastic?

Western India accounts for 46.55% of national consumption, anchored by Gujarat and Maharashtra.

What is driving investment in domestic PVC capacity?

A persistent supply deficit of 2.5 million tonnes per year is prompting large-scale projects by Reliance and Adani.

How are feedstock price swings affecting manufacturers?

Volatile naphtha prices compress margins, leading firms to secure long-term contracts and explore alternative feedstocks such as propane and ethane. Continue Research

Page last updated on: