Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

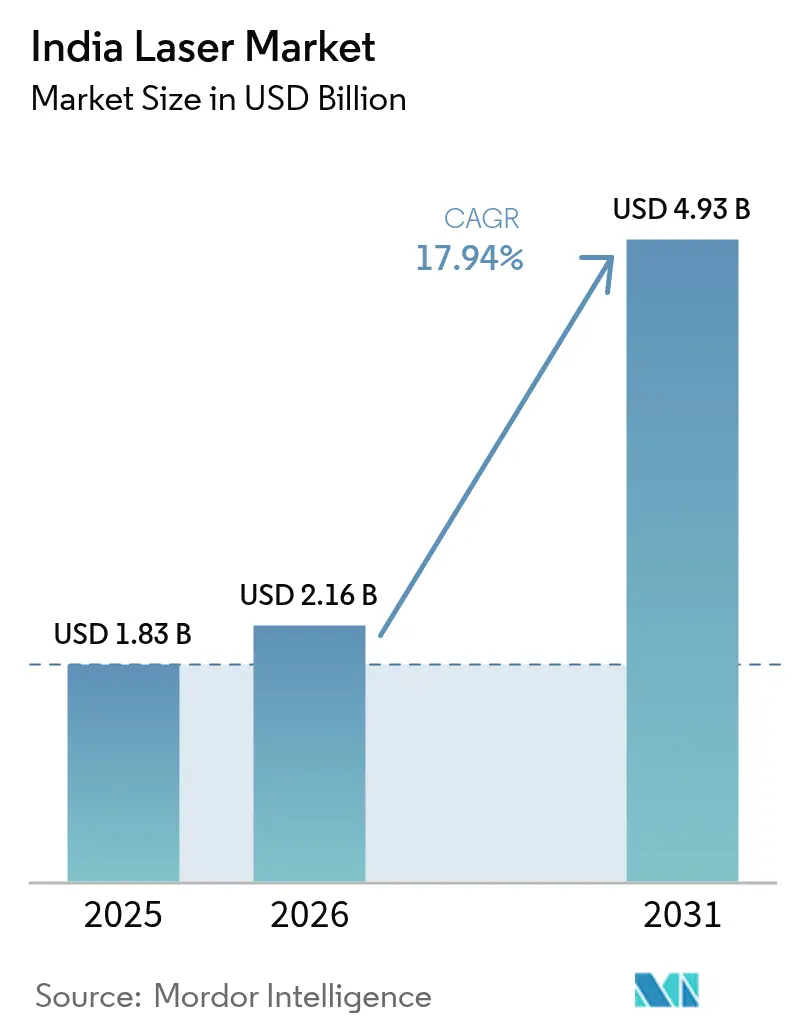

| Base Year Market Size (2025) | USD 1.83 Billion |

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 4.93 Billion |

| Growth Rate (2026 - 2031) | 17.94% CAGR |

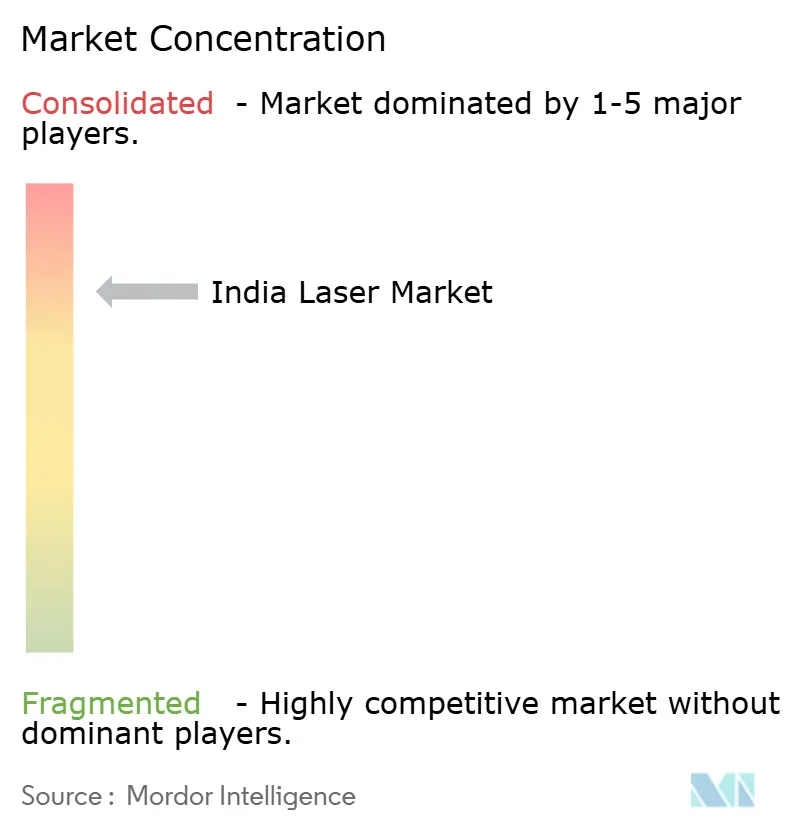

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Laser Market Analysis by Mordor Intelligence

The India laser market size is projected to expand from USD 1.83 billion in 2025 and USD 2.16 billion in 2026 to USD 4.93 billion by 2031, registering a CAGR of 17.94% between 2026 and 2031. Implied demand is shifting from tool-room precision jobs to round-the-clock production assets as semiconductor fabs, EV battery lines and solar-cell plants embed lasers at multiple process nodes. Government incentive programs are front-loading purchases, while falling total cost of ownership for fiber platforms accelerates replacement of plasma, oxy-fuel and mechanical scribing. Chinese brands are sustaining a price gap of 30%-40%, but their share is bounded by after-sales support gaps that favor premium Western and entrenched domestic suppliers. Import tariffs and currency moves remain swing factors for buyers, yet rising lease finance penetration and zero-duty concessions in special economic zones are easing near-term capital constraints.

Key Report Takeaways

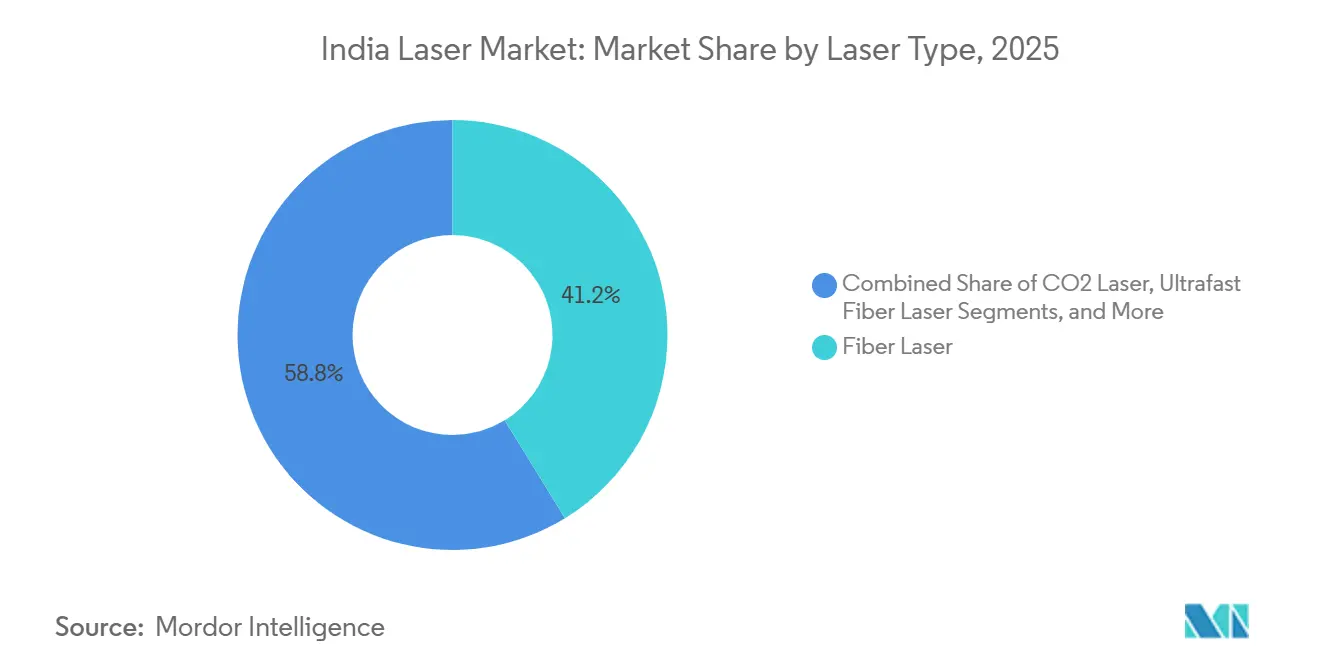

- By laser type, fiber platforms led with 41.23 % revenue share in 2025; ultrafast fiber lasers are advancing at a 19.18 % CAGR through 2031.

- By power output, medium-power units (1-100 watts) held 48.67 % of the India laser market share in 2025, while high-power systems above 100 watts are growing at an 18.67 % CAGR.

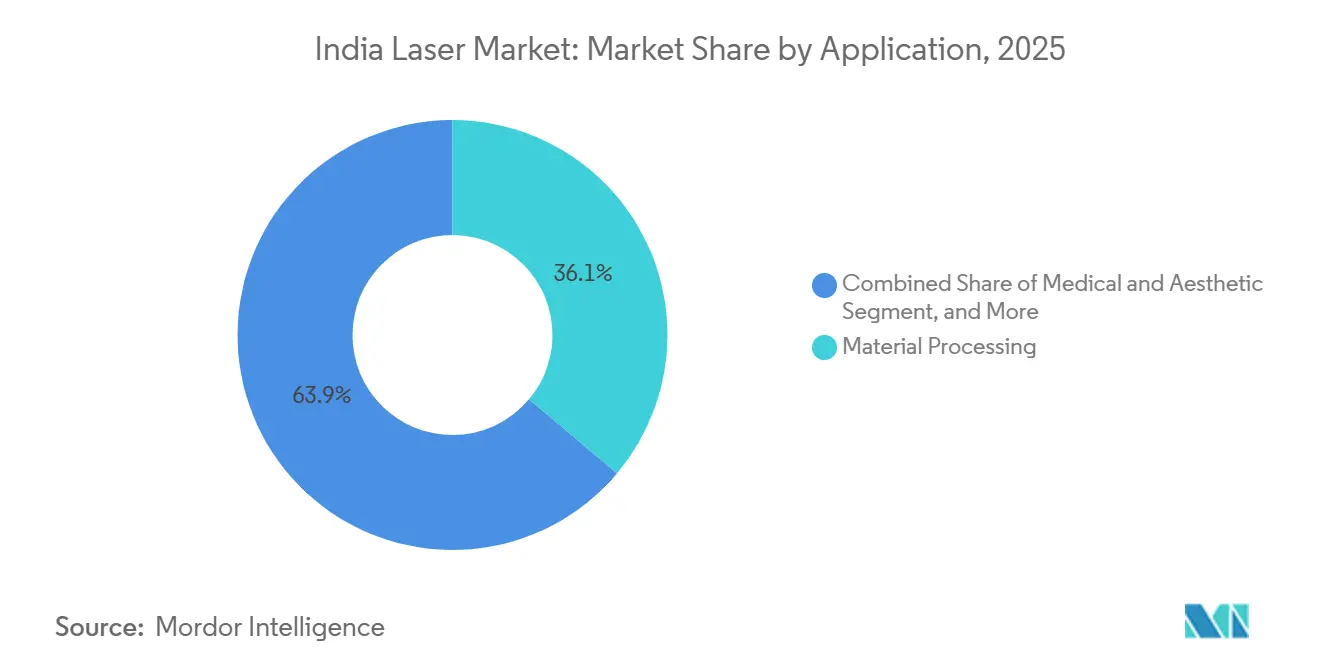

- By application, material processing accounted for 36.12 % of the India laser market size in 2025 and medical and aesthetic procedures are expanding at a 19.43 % CAGR to 2031.

- By end-user industry, electronics and semiconductors contributed 29.63 % of 2025 revenue, whereas healthcare is projected to post the fastest growth at 19.83 % through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Laser Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives for Semiconductor Fabs | +4.1% | Gujarat, Assam, Tamil Nadu | Long term (≥ 4 years) |

| Rapid Adoption of EV and Battery Fabrication Lines | +3.5% | Maharashtra, Gujarat, Tamil Nadu | Medium term (2-4 years) |

| Surge in Domestic Electronics Manufacturing Clusters | +3.2% | Uttar Pradesh, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| PLI for Solar Module Lines Requiring Laser Scribing | +2.3% | Gujarat, Rajasthan, Tamil Nadu | Medium term (2-4 years) |

| Rising Procurement of Laser-Based LiDAR Sensors by Smart-City Projects | +2.1% | Delhi NCR, Mumbai, Bangalore | Short term (≤ 2 years) |

| Expansion of Laser-Based Additive Manufacturing Startups | +1.8% | Bangalore, Pune, Hyderabad | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Incentives For Semiconductor Fabs

Policy support under the India Semiconductor Mission approved 10 fabs with INR 1.6 lakh crore (USD 19.2 billion) committed, each embedding laser dicing, marking and scribing tools that must run at sub-micron tolerances. Zero-duty imports under the Export Promotion Capital Goods window cut ownership cost by 18%-22%, compressing payback periods on high-uptime fiber platforms. Micron’s Sanand plant alone will require several dozen laser-based inspection and marking stations once operations commence. Collectively, the fab build-out implies a 15-fold scale-up in installed laser base by 2030, locking in long-tail service and consumables demand.

Rapid Adoption of EV And Battery Fabrication Lines

The Advanced Chemistry Cell PLI of INR 18,100 crore (USD 2.2 billion) creates a 50 GWh battery capacity pipeline that favors laser welding for aluminum-to-copper joints, cutting joint resistance by 18% relative to spot welding. Subsidies under the PM E-DRIVE scheme support 1.6 million electric two-wheelers and 0.5 million three-wheelers, each battery pack relying on laser seam welds to meet AIS-156 crash norms. Automotive OEMs adapting remote laser welding have recorded 30 % faster roof-seam cycles versus resistance methods. Growing line densities are therefore shifting high-power demand from plasma cutters to multi-kilowatt continuous-wave fiber units.

Surge In Domestic Electronics Manufacturing Clusters

Electronics Manufacturing Clusters 2.0 earmarked INR 3,762 crore (USD 452 million) to fund plug-and-play lines that bundle laser marking and rework cells for SMEs that cannot justify stand-alone capex.[1]Ministry of Electronics and Information Technology, “Electronics Manufacturing Clusters 2.0,” MEITY.GOV.IN Traceability codes mandated by IS 16537:2016 require laser-etched 0.1 mm features on conformal-coated boards. Shared access to selective soldering and micro-machining lasers de-risks adoption, lifting utilization and spreading maintenance costs across tenant manufacturers. The scheme thus raises the India laser market’s addressable base beyond tier-1 multinationals to thousands of mid-tier EMS providers.

PLI For Solar Module Lines Requiring Laser Scribing

The solar PLI allocates INR 24,000 crore (USD 2.9 billion) and ties incentive multipliers to thin-film and heterojunction cells that need laser scribing to avoid edge damage. Laser-cut isolation grooves reduce shunt losses by up to 15%, directly lifting module efficiency and helping makers qualify for higher PLI payouts. Each gigawatt of thin-film capacity demands 8-12 high-rep-rate laser scribers running above 50 kHz, translating into a sizeable baseline for service and optics replacement. Revised electroluminescence tests in 2025 penalize mechanical scribe-induced micro-cracks, further tilting orders toward laser-processed modules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex of High-Power Fiber Lasers | -2.8% | Tier-2 and tier-3 hubs nationwide | Short term (≤ 2 years) |

| Rupee Volatility vs USD/CNY | -1.9% | Import-dependent integrators | Short term (≤ 2 years) |

| Inter-State GST Credit Delays on Capital Machinery | -1.3% | States with complex reconciliation | Medium term (2-4 years) |

| Limited Local Supply Chain for High-Precision Optical Isolators | -1.1% | All laser assemblers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex Of High-Power Fiber Lasers

Multi-kilowatt units priced between USD 150,000 and USD 400,000 strain balance sheets of job shops operating on 12%-18% net margins. Lease finance penetration is below 25% versus 60%-70% in Germany, forcing buyers into working-capital loans at 9%-11% interest, stretching paybacks beyond four years. The absence of a secondary market for refurbished lasers doubles the net outlay, while deferred purchases pressured IPG’s India revenue to fall 8% year-over-year in 2025. SME adopters in tier-3 cities also lack access to application labs, raising perceived technical risk and slowing order conversion.

Rupee Volatility Vs USD/CNY

The INR slipped from 82.8 to 85.4 per USD in 2025, inflating landed costs for imported sources by roughly 3 %.[2]Reserve Bank of India, “Reference Rate Archives,” RBI.ORG.IN A similar 2.8 % depreciation against the yuan narrowed the price advantage of Chinese brands, neutralizing part of their cost edge. Forward hedges cover single-tranche payments, yet laser procurements involve staged installments that expose buyers to spot-rate swings at each milestone. Export-oriented fabs can offset duty through EPCG zero-tariff imports, but domestic-focused users bear the full forex burden, creating a two-speed market where exporters enjoy up to 22 % lower capex on identical models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Laser Type: Fiber Platforms Anchor Revenue, Ultrafast Systems Lead Innovation

Fiber platforms dominated 41.23 % of 2025 revenue, underlining their fit for sheet-metal cutting, battery tab welding and PCB marking. The india laser market size for fiber systems is projected to expand by more than four-fold as fabs, EV lines and solar plants race to standardize on single-mode sources with wall-plug efficiencies exceeding 40%. Ultrafast fiber lasers, though just a niche today, are climbing at a 19.18% CAGR on the back of femtosecond micro-machining in medical devices and transparent-substrate drilling for smartphone cover glass. Solid-state Nd-YAG and diode-pumped variants keep resonance in jewelry welding and watchmaking, protected by installed-base familiarity rather than raw performance. CO₂ units still cut acrylic, wood and leather, yet many job shops are shedding dual-wavelength setups to streamline maintenance under tighter delivery windows.

In research and defense, excimer, ultraviolet and emerging terahertz sources fill specialized roles. ISRO’s December 2025 tender for a harmonics-enabled femtosecond system underscores how national labs are staking claims in quantum optics and high-energy experiments.[3]Indian Space Research Organisation, “IISU Laser Tender,” ISRO.GOV.IN The Council of Scientific and Industrial Research procured frequency-stabilized helium-neon lasers for metrology, hinting at enduring demand for low-power but ultrastable benches. Dye and free-electron configurations remain academic curiosities, yet breakthroughs here often migrate to commercial wavelengths within a decade, ensuring that innovation cycles continue to refresh the india laser market long after the present forecast horizon.

By Power Output: Medium-Power Dominance Meets High-Power Acceleration

Medium-power lasers between 1 and 100 watts accounted for 48.67 % of 2025 revenue, covering serial-number marking, selective soldering and thin-metal cutting tasks that populate most Indian workshops. Their plug-and-play air cooling, 220-volt compatibility and 48-hour nationwide service reach keep total downtime below 2 %, a critical selling point for SMEs. The india laser market share for high-power systems above 100 watts is rising fast, tied to multi-kilowatt weld cells that fuse aluminum battery enclosures and 20-millimeter ship-steel blanks at speeds unattainable by plasma. TRUMPF’s Pune factory, opened in August 2025, now assembles 6 kW through 12 kW disk and fiber sources locally, slicing lead times to 8-10 weeks and comforting OEMs wary of shipment uncertainty.

System integrators still confront a skills gap. Only three in ten can program six-axis robots to the sub-0.1 mm path accuracy that remote welding demands, limiting provincial roll-outs. Conversely, the low-power tier below 1 watt keeps volume leadership in barcode scanners, smartphone depth sensors and alignment modules. ASP compression, however, means this tier contributes a minor fraction of india laser market size, even as shipment counts explode alongside handset assembly.

By Application: Material Processing Anchors Demand, Medical Aesthetics Surge

Material processing held 36.12 % of 2025 spend, cemented by its centrality to cutting, welding and engraving across automotive, aerospace and general fabrication. Fiber units slash traverse time 40 % and kerf width 25 % relative to plasma, reducing scrap on stainless and aluminum. That operational win is propelling replacement cycles in sheet-metal towns like Ludhiana and Rajkot. Medical and aesthetic usage, by contrast, is rising at 19.43% annually, with Q-switched Nd- YAG and fractional CO₂ devices eclipsing dermabrasion in cosmetic clinics. Public-hospital backlogs of eight months for laser dermatology procedures tilt affluent patients toward private chains, inflating procedure counts and broadening service revenue.

Optical communications embed distributed-feedback diodes and erbium-doped amplifiers in 400 G and 800 G transceiver lines as data-center capacity races toward 1,800 MW by end-2026. Instrumentation markets are maturing too, with Indian Railways ordering LiDAR-track scanners across 68,000 route-km. Defense allocations for a 300 kW directed-energy weapon project and 10 kW technology transfers add a dual-use kicker, ensuring that R&D, security and metrology budgets keep the india laser market diversified against cyclical dips in any single vertical.

By End-User Industry: Electronics Lead, Healthcare Accelerates

Electronics and semiconductors formed 29.63 % of 2025 revenue, anchored by the 10-fab pipeline and Electronics Manufacturing Clusters 2.0 that hard-wire laser marking, dicing and trimming into board and silicon flows. The india laser market size linked to healthcare is forecast to scale at a 19.83 % CAGR, fueled by holmium lithotripsy, thulium prostate therapy and femtosecond LASIK platforms. Aesthetic chains expand networks to capture unmet demand from metro millennials, while insurance cashless coverage for urology laser procedures grows acceptance across tier-2 cities.

Auto OEMs remain pivotal. The PM E-DRIVE subsidy is accelerating EV body-in-white adoption of remote laser welding, essential for sealing aluminum-intensive skateboard chassis. Aerospace customers direct titanium powder-bed fusion orders to startups like Fabheads, leveraging the freeform design freedom of laser additive manufacturing. Telecom equipment vendors, spurred by National Telecom Policy 2025, are sourcing or codeveloping laser diode assemblies domestically to qualify for preference-in-procurement quotas. Research institutions account for roughly one-tenth of 2025 buys, but their high-specification ultrafast benches seed downstream commercial platforms, sustaining an innovation loop within the india laser industry.

Geography Analysis

Gujarat, Maharashtra, Tamil Nadu and Karnataka together captured roughly 62 % of installed base in 2025, with semiconductor fabs in Dholera and Sanand, automotive clusters in Pune and Chennai and electronics hubs in Bangalore and Noida acting as anchor customers. State incentives such as 75 % electricity duty waivers and 100 % stamp-duty refunds lower lifetime costs for multi-kilowatt systems, tilting fab planners toward these corridors. Tamil Nadu’s electronics prowess, visible in Sriperumbudur handset lines, drives continuous-duty laser marking demand at process uptimes exceeding 95 %.

Emerging nodes like Assam’s Jagiroad packaging plant and multiple cluster sites in Uttar Pradesh extend the india laser market footprint eastward. These greenfield parks benefit from shared laser rework centers and 48-hour technician reach, though they still lag tier-1 metros on optics inventory depth. Coastal special-economic-zone states leverage zero-duty import privileges and port proximity to shave 18 %-22 % off landed cost relative to landlocked competitors, reinforcing regional disparities.

Defense and R&D spending remains concentrated in Bangalore and Hyderabad, where labs prototype directed-energy weapons and quantum photonics benches. Solar-module PLI winners in Rajasthan, Gujarat and Tamil Nadu are rolling out high-rep-rate scribers, dispersing precision-laser expertise beyond metal fabrication. Taken together, geographic spread is broadening, yet after-sales talent and spare optics logistics remain most mature along the west-and south-coast industrial belt, a factor that purchasers continue to weigh in site-selection calculus.

Competitive Landscape

Global incumbents IPG Photonics, Coherent and TRUMPF held an estimated 45 %-50 % combined revenue in 2025, defending positions through multi-year service contracts, application engineering depth and ISO-compliant documentation packs favored by automotive and aerospace auditors. Chinese challengers Raycus, Maxphotonics and Han’s Laser carved out 25 %-30 % share by pricing 30 %-40 % below Western quotes and courting sheet-metal job shops. Import manifests show Maxphotonics and Han’s Laser shipments rising despite 18 % basic customs duty, hinting at resilient cost appeal.

Domestic specialist Sahajanand Laser Technology dominates diamond cutting and jewelry welding niches on the back of a 21-year installed base, proprietary optics and Gujarat-centric service density. White-space upside exists in ultrafast femtosecond job-shop services for medical-device micro-machining and transparent glass drilling, segments where turn-key local capability is still sparse. Additive-manufacturing startups such as Fabheads and ThinkMetal are disrupting traditional cnc tooling by offering laser powder-bed fusion for rapid mold and aerospace parts, buoyed by Technology Development Board grants.

Technology roadmaps emphasize real-time process monitoring and AI-driven parameter optimization. IPG’s 2025 machine-learning module cut battery-pack weld defects by 12 %-15% in field trials. Partnerships, exemplified by Lam Research’s USD 1 billion India engineering center, localize plasma-etch and laser-anneal know-how, shortening feedback loops between tool makers and fabs. The net result is a moderately concentrated india laser market where top five players control roughly 75 % of value, yet room persists for local champions to scale in application-specific or service-intensive niches.

India Laser Industry Leaders

IPG Photonics Corporation

Coherent Corp.

TRUMPF SE + Co. KG

nLIGHT, Inc.

Jenoptik AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The Tata Institute of Fundamental Research tendered for excimer laser spare parts, maintaining ultraviolet platform continuity for atomic-physics experiments.

- August 2025: TRUMPF inaugurated a Pune plant to assemble 6 kW-12 kW disk and fiber lasers, halving delivery times for domestic buyers.

- August 2025: CSIR-CMERI invited bids for distributed-feedback wavelength-stabilized diodes to enhance precision metrology projects.

- July 2025: The Technology Development Board opened a INR 500 crore call for metal and ceramic additive manufacturing proposals, steering funds toward laser powder-bed fusion research.

India Laser Market Report Scope

The India Laser Market Report is Segmented by Laser Type (Fiber, Solid-State, CO2, Diode, Excimer, Ultrafast Fiber, Other), Power Output (Low-Power, Medium-Power, High-Power), Application (Material Processing, Communication, Medical, Instrumentation, Defense, R&D, Consumer Electronics, Other), End-User Industry (Automotive, Aerospace and Defense, Electronics and Semiconductors, Healthcare, Telecommunications, Research Institutions, Other), and Geography (India). Market Forecasts are Provided in Terms of Value (USD).

By Laser Type

| Fiber Laser |

| Solid-State Laser (Nd-YAG, DPSS etc.) |

| CO2 Laser |

| Diode / Direct Semiconductor Laser |

| Excimer / UV Laser |

| Ultrafast Fiber Laser |

| Other Laser Types |

By Power Output

| Low-Power (less than 1 W) |

| Medium-Power (1-100 W) |

| High-Power (above 100 W) |

By Application

| Material Processing (Cutting, Welding, Marking) |

| Communication and Optical Storage |

| Medical and Aesthetic |

| Instrumentation and Measurement |

| Defense and Security |

| Research and Development |

| Consumer Electronics |

| Other Applications |

By End-User Industry

| Automotive |

| Aerospace and Defense |

| Electronics and Semiconductors |

| Healthcare |

| Telecommunications |

| Research Institutions |

| Other End-User Industries |

| By Laser Type | Fiber Laser |

| Solid-State Laser (Nd-YAG, DPSS etc.) | |

| CO2 Laser | |

| Diode / Direct Semiconductor Laser | |

| Excimer / UV Laser | |

| Ultrafast Fiber Laser | |

| Other Laser Types | |

| By Power Output | Low-Power (less than 1 W) |

| Medium-Power (1-100 W) | |

| High-Power (above 100 W) | |

| By Application | Material Processing (Cutting, Welding, Marking) |

| Communication and Optical Storage | |

| Medical and Aesthetic | |

| Instrumentation and Measurement | |

| Defense and Security | |

| Research and Development | |

| Consumer Electronics | |

| Other Applications | |

| By End-User Industry | Automotive |

| Aerospace and Defense | |

| Electronics and Semiconductors | |

| Healthcare | |

| Telecommunications | |

| Research Institutions | |

| Other End-User Industries |

Key Questions Answered in the Report

How big will the India laser market be by 2031?

It is forecast to reach USD 4.93 billion, expanding at a 17.94% CAGR from 2026 to 2031.

Which laser type holds the largest share in India?

Fiber platforms commanded 41.23 % of 2025 revenue and remain the primary choice for material processing tasks.

What application segment is growing the fastest?

Medical and aesthetic procedures are projected to register a 19.43 % CAGR through 2031 as private clinics add Q-switched and fractional CO₂ systems.

How are government policies affecting laser demand?

Production-Linked Incentive schemes for semiconductors, EV batteries and solar modules embed lasers at multiple process steps, adding more than fourfold tool demand over the forecast period.

Which states dominate laser installations?

Gujarat, Maharashtra, Tamil Nadu and Karnataka together account for about 62 % of installed base due to semiconductor fabs, automotive hubs and electronics clusters.

Who are the leading suppliers?

IPG Photonics, Coherent and TRUMPF lead premium tiers, while Raycus, Maxphotonics and Han’s Laser hold price-focused positions, and Sahajanand Laser Technology leads in jewelry and diamond cutting niches.

Page last updated on: