Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

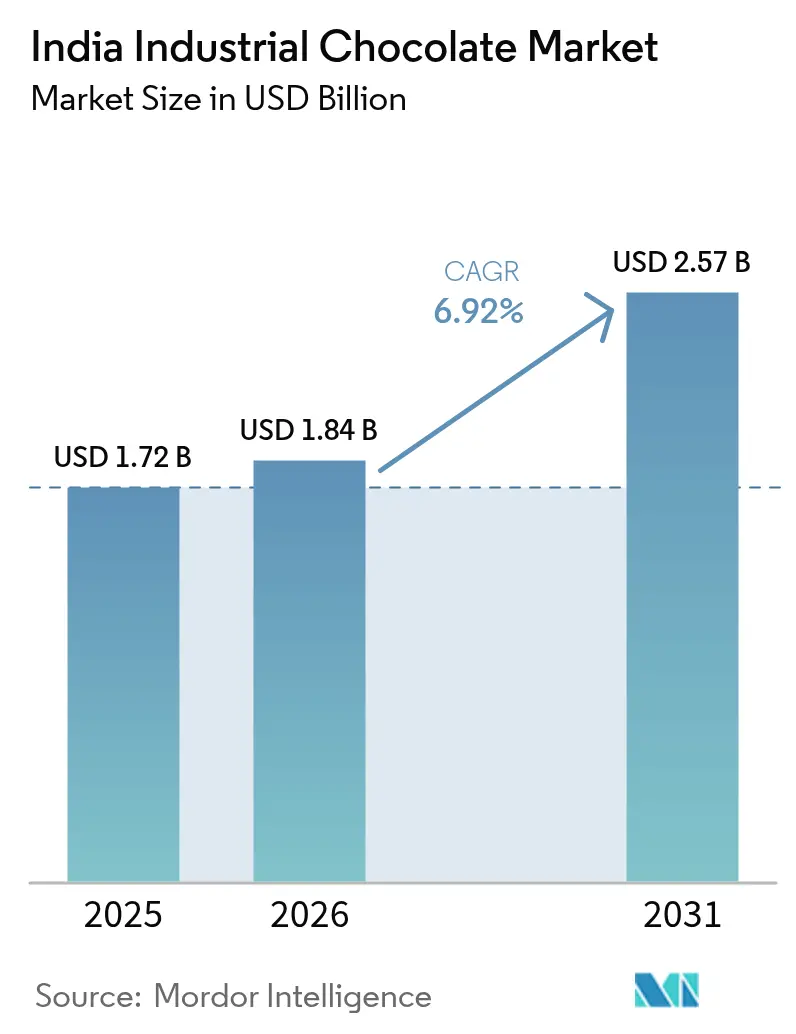

| Base Year Market Size (2025) | USD 1.72 Billion |

| Market Size (2026) | USD 1.84 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Industrial Chocolate Market Analysis by Mordor Intelligence

The India industrial chocolate market size is expected to grow from USD 1.72 billion in 2025 to USD 1.84 billion in 2026 and is forecast to reach USD 2.57 billion by 2031 at 6.92% CAGR over 2026-2031. Robust growth is driven by expanding food-processing capacity, sustained investment programs from global and domestic players, and supportive government policies that lower entry barriers for value-added manufacturing. Demand accelerates as organized bakery chains, premium confectionery stores, and quick-service restaurants source larger volumes of cost-efficient compound and premium real chocolates, leveraging enlarged cold-chain networks that safeguard quality during transportation. Disposable income gains and urban migration enhance per-capita chocolate consumption, while the Production Linked Incentive Scheme for Food Processing triggers capacity expansion that supports consistent off-take of industrial chocolate across multiple downstream applications. Multinationals deepen localization to hedge against import duties and logistics risks, whereas niche craft manufacturers exploit origin stories and sustainable sourcing to capture premium pockets within the India industrial chocolate market.

Key Report Takeaways

- By category, Compound Chocolate commanded 61.88% of India industrial chocolate market share in 2025. Real Chocolate is forecast to post the fastest 8.01% CAGR through 2031.

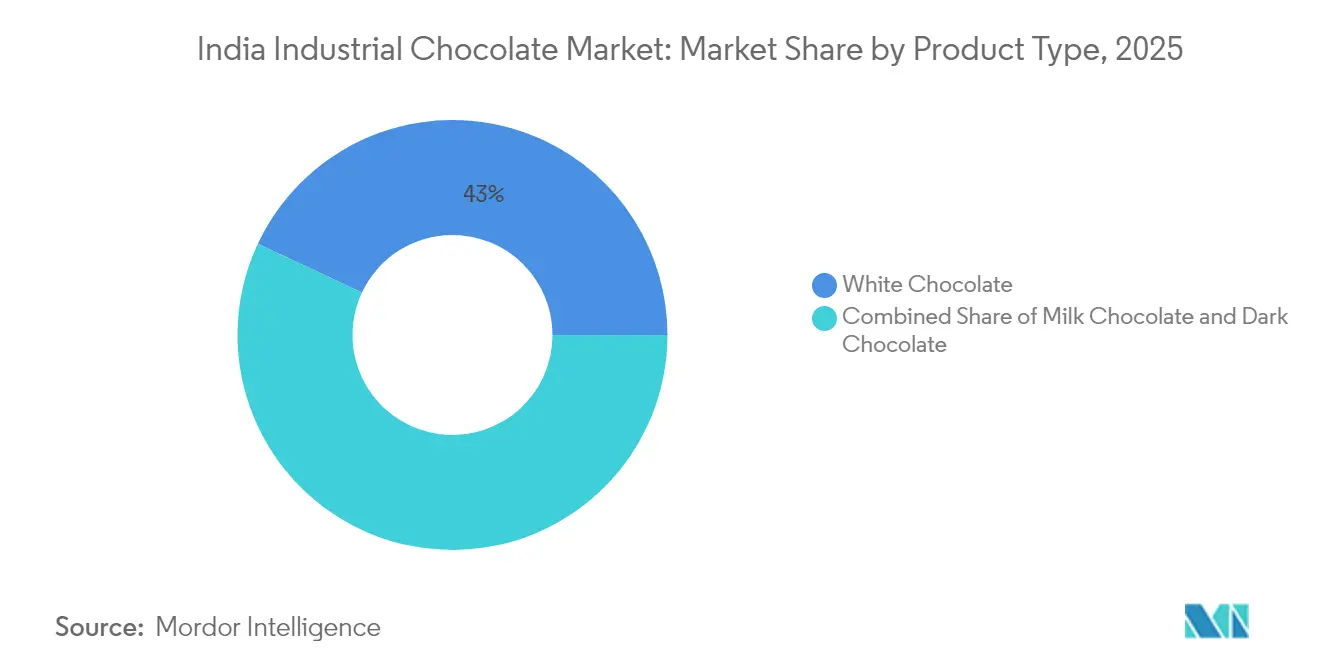

- By product type, White Chocolate led with 43.02% share of the India industrial chocolate market size in 2025, while Dark Chocolate is projected to grow at an 8.41% CAGR to 2031.

- By form, Blocks and Slabs accounted for 46.01% share of the market in 2025, while liquid is projected to grow at a 7.53% CAGR through 2031.

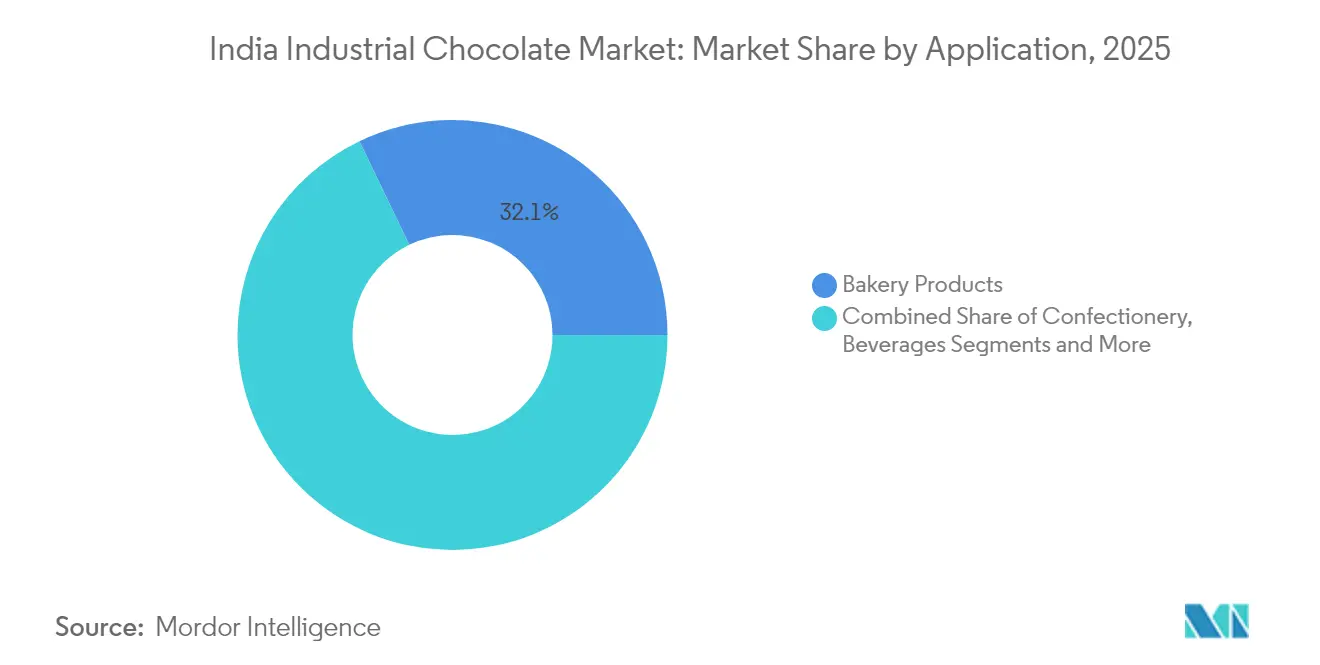

- By application, Bakery Products held 32.12% revenue share in 2025; Frozen Desserts and Ice Creams are advancing at a 7.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Industrial Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of bakery and confectionery industries | +1.5% | National, with concentration in Maharashtra, Gujarat, Karnataka | Medium term (2-4 years) |

| Rising chocolate consumption and gifting culture | +0.8% | Urban centers expanding to Tier-2 cities | Short term (≤ 2 years) |

| Expansion of organised retail and cold-chain infrastructure | +1.2% | National, with early gains in Delhi NCR, Mumbai, Bangalore | Long term (≥ 4 years) |

| Increasing popularity of premium and specialty chocolates | +0.9% | Metro cities with spillover to emerging urban markets | Medium term (2-4 years) |

| Government support for food processing industry | +0.6% | National, with state-specific incentive variations | Long term (≥ 4 years) |

| Cocoa-crop incentives lower import dependence | +0.4% | Kerala, Karnataka, Andhra Pradesh, Tamil Nadu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of bakery and confectionery industries

The growth of bakery and confectionery industries is a significant driver of the India Industrial Chocolate Market. The increasing demand for baked goods and confectionery products, fueled by changing consumer preferences and rising disposable incomes, has led to a surge in the consumption of industrial chocolate. Regional bakery clusters in Maharashtra and Gujarat leverage their proximity to major ports for efficient ingredient sourcing, while Karnataka's IT corridor drives demand for premium bakery products that require higher-grade chocolate inputs. Additionally, the sector's evolution toward health-conscious formulations creates opportunities for dark chocolate variants and sugar-reduced industrial chocolate solutions. The growing popularity of premium and innovative chocolate-based products has encouraged manufacturers to invest in high-quality industrial chocolate to cater to evolving consumer tastes. Furthermore, regulatory compliance under FSSAI standards increasingly favors suppliers with robust quality management systems, consolidating market share among established industrial chocolate manufacturers. This dynamic growth in the bakery and confectionery sectors is expected to continue driving the demand for industrial chocolate in India during the forecast period.

Rising chocolate consumption and gifting culture

The increasing consumption of chocolate, coupled with the expanding gifting culture, is driving the growth of the India Industrial Chocolate Market. Chocolates have become a popular choice for gifting during festivals, celebrations, and special occasions, reflecting a shift in consumer preferences. This trend is further supported by the rising disposable income and urbanization in India, which have contributed to the growing demand for premium and customized chocolate products. Additionally, E-commerce platforms are facilitating the growth of direct-to-consumer chocolate brands, creating demand for specialized industrial chocolate formulations that support artisanal positioning while maintaining cost competitiveness. Seasonal demand spikes during Diwali, Valentine's Day, and wedding seasons require industrial chocolate suppliers to maintain flexible production capacities and efficient inventory management systems. Additionally, the shift toward premium gifting preferences is driving demand for Belgian-style compounds and specialty coatings that deliver perceived luxury without incurring premium cocoa costs. The evolution of consumer preferences toward experiential flavors is also creating opportunities for industrial chocolate manufacturers to develop region-specific taste profiles and innovative texture applications, further fueling market growth.

Expansion of organised retail and cold-chain infrastructure

The expansion of organized retail and cold-chain infrastructure is a significant driver of the India Industrial Chocolate Market. The growth of organized retail, particularly modern retail formats, has increased the availability and accessibility of industrial chocolate products, catering to a broader consumer base. This proliferation has also created demand for portion-controlled chocolate applications in ready-to-eat products, pushing industrial chocolate suppliers toward specialized packaging and formulation capabilities. Additionally, advancements in cold-chain infrastructure, including the development of cold storage hubs in urban centers, have improved the storage and transportation of chocolate products. These improvements reduce distribution costs for chocolate-containing products, enhancing margin structures for both manufacturers and retailers. The emphasis on farm-to-fork supply chains further benefits cocoa processing facilities that can demonstrate traceability and quality consistency throughout temperature-controlled logistics networks. Regional cold-chain development particularly benefits southern states, where cocoa cultivation intersects with established food processing infrastructure. This creates opportunities for vertical integration among industrial chocolate manufacturers, enabling them to streamline operations and meet the rising demand for industrial chocolate across various applications, including confectionery, bakery, and dairy industries.

Increasing popularity of premium and specialty chocolates

The increasing popularity of premium and specialty chocolates is driving the growth of the India Industrial Chocolate Market. Gen Z consumers' preference for sophisticated gifting options is fueling demand for industrial chocolate that supports artisanal positioning while maintaining scalable production economics. Craft chocolate brands like Paul And Mike and Soklet exemplify market acceptance for premium positioning based on origin stories and sustainable sourcing, creating opportunities for industrial chocolate suppliers to develop traceable, single-origin formulations. Additionally, the emergence of health-focused variants, including sugar-free and organic options, is pushing industrial chocolate manufacturers to invest in specialized processing capabilities and ingredient sourcing networks. Regional flavor preferences, such as cardamom-infused varieties and tropical fruit combinations, require flexible manufacturing systems capable of small-batch customization within industrial-scale operations. The premium segment's growth is particularly concentrated in metro cities, where rising disposable incomes support price premiums for quality differentiation, influencing industrial chocolate suppliers' geographic expansion strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in cocoa prices affecting raw material costs | -1.8% | National impact with acute effects on Northern and Western regions | Short term (≤ 2 years) |

| Health concerns related to sugar and fat content limiting chocolate consumption | -0.7% | Urban educated demographics with spillover effects | Medium term (2-4 years) |

| Lack of awareness and limited penetration in rural areas | -0.5% | Rural India, particularly northeastern and central regions | Long term (≥ 4 years) |

| Complex regulatory environment and stringent food safety standards | -0.3% | National, with varying state-level implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in cocoa prices affecting raw material costs

India's heavy reliance on imports for 70% of its cocoa needs makes it highly susceptible to global price fluctuations. This dependency poses significant challenges, particularly for small and medium-sized chocolate manufacturers in the country, who often lack the financial resources or mechanisms to hedge against these price swings or secure long-term supply contracts. The situation is further exacerbated by a 35% import duty on cocoa beans, which increases cost pressures on domestic processors [1]Source: Food and Agriculture Organization. "Cocoa", www.fao.org. This places them at a competitive disadvantage compared to finished chocolate imports that benefit from preferential trade agreements, allowing foreign manufacturers to offer more cost-effective products in the Indian market. Even large-scale operators like Barry Callebaut are not immune to these challenges. The company has implemented substantial price increases and introduced additional financing arrangements to manage working capital requirements, highlighting the widespread impact of cocoa market volatility. Furthermore, supply chain disruptions in West Africa, which accounts for 55% of global cocoa exports, create significant procurement uncertainties. These disruptions compel industrial chocolate manufacturers to adopt strategies such as maintaining higher inventory levels and diversifying their supply sources to mitigate risks. The volatility is particularly pronounced in the compound chocolate segment, where cost competitiveness plays a critical role in determining market positioning.

Health concerns related to sugar and fat content limiting chocolate consumption

Health concerns over sugar and fat content are curbing chocolate consumption in the India Industrial Chocolate Market. Rising awareness among consumers about the adverse effects of excessive sugar and fat intake, such as obesity, diabetes, and cardiovascular diseases, has led to a shift in preferences. This growing health consciousness is prompting consumers to reduce their consumption of traditional chocolate products, which are often high in sugar and fat. Additionally, regulatory bodies are implementing stricter guidelines on sugar content in food products, further impacting the market. These factors collectively act as a significant restraint on the growth of the industrial chocolate market in India. Furthermore, the increasing prevalence of lifestyle-related diseases has heightened the demand for healthier alternatives, such as low-sugar or sugar-free chocolates, which are gaining traction among health-conscious consumers. However, the production of such alternatives often involves higher costs and technological challenges, which can limit their widespread adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Compound Chocolate Dominates Cost-Sensitive Applications

Compound chocolate holds the largest market share in the India industrial chocolate segment, accounting for 61.88% of the market in 2025. This dominance is attributed to its cost-effectiveness and the preference among industrial users for affordable solutions in mass-market bakery, confectionery, and snack applications. Compound chocolate utilizes cocoa butter substitutes, making it considerably cheaper without drastically compromising on taste for large-scale manufacturing needs. The product's easy handling characteristics and stable texture have further boosted its popularity among commercial bakers and confectioners, allowing brands to manage ingredient costs while delivering products that satisfy mainstream consumer tastes. The rising demand for chocolate-flavored bakery items and snacks continues to reinforce the prominence of compound chocolate, given its versatility and wide application. Major players in the segment consistently innovate product offerings to maintain their market position, targeting the needs of high-volume production and cost efficiency.

In contrast, the fastest growing segment in the India industrial chocolate market is real chocolate, which is projected to accelerate at a robust CAGR of 8.01% through 2026-2031. This surge is largely driven by premiumization trends, as consumers increasingly seek chocolates with higher cocoa content and superior flavor profiles. Artisanal and premium chocolate brands are capturing attention with their emphasis on quality ingredients and authentic chocolate experiences, justifying higher price points despite the increased cost of raw materials. Urban consumers, influenced by global trends and rising disposable incomes, are willing to pay more for chocolates perceived as healthier or more luxurious, fueling the transition toward finer chocolate options. Premium chocolate now finds favor not just among gift buyers, but also with everyday consumers seeking indulgence in their snacks and desserts. The expanded presence of premium and real chocolate products in organized retail and online channels is further accelerating segment growth. As a result, brands operating in this segment are focusing on artisanal positioning, innovative flavors, and ethical sourcing to meet discerning customer expectations.

By Product Type: White Chocolate Leads Despite Dark Chocolate Acceleration

White chocolate secures the largest market share in India's industrial chocolate sector, capturing 43.02% of the market in 2025. Its dominance primarily stems from its extensive use in confectionery coatings and premium dessert formulations, offering manufacturers color neutrality that allows for a wide spectrum of flavor combinations and visual designs. The versatility of white chocolate enables the creation of intricate dessert presentations and innovative products that appeal to evolving consumer tastes, especially among younger demographics and premium market segments. Major food manufacturers and bakers rely on white chocolate for its capacity to blend seamlessly with other flavors without overwhelming base ingredients, making it ideal for diversified product portfolios. New product launches often showcase creative pairings, such as fruit or nut infusions, further enhancing white chocolate’s appeal in mass-market and high-end offerings. As a result, white chocolate remains a favored choice for confectionery brands aiming to deliver indulgence alongside creative flexibility and attractive aesthetics.

Conversely, dark chocolate emerges as the fastest growing segment, boasting an impressive CAGR of 8.41% from 2026 to 2031 in the India industrial chocolate market. This segment’s rapid ascent is propelled by rising health consciousness, as consumers increasingly associate dark chocolate with antioxidants and potential wellness benefits. Brands are leveraging these trends by marketing dark chocolate as a premium ingredient with clean labels, higher cocoa content, and natural sweeteners, which supports a higher price point in both industrial and retail applications. Manufacturers are introducing products that spotlight origin-specific cocoa and functional ingredients, further fueling demand as consumers seek both indulgence and perceived health benefits. The trend aligns with shifting urban preferences, wherein younger buyers are more willing to indulge in chocolates that claim superior nutritional properties and ethical sourcing. The segment’s dynamic growth is also supported by innovation in flavors and formats, ensuring dark chocolate’s expanding presence in industrial baking, functional foods, and specialty confectionery products.

By Form: Blocks and Slabs Dominate Processing Applications

Blocks and slabs constitute the largest market share in the Indian industrial chocolate market, commanding 46.01% in 2025. These formats cater primarily to industrial users who require bulk processing capabilities for their high-volume production environments. Blocks and slabs offer significant versatility, serving as fundamental components for melting, molding, and seamless integration into complex food manufacturing operations such as bakery, confectionery, and dessert production. Their bulk form is particularly favored by large-scale manufacturers since it simplifies storage and transportation while enabling efficient ingredient management during production. Major suppliers like Cargill have tailored their block and slab offerings to meet the demands of bakers and food processors, ensuring consistent quality and extended shelf life for industrial applications. The ability to create a wide variety of end products from a standardized bulk chocolate input renders blocks and slabs the preferred choice for firms prioritizing scale, consistency, and operational efficiency.

In contrast, liquid chocolate is emerging as the fastest growing segment, with a forecasted CAGR of 7.53% between 2026 and 2031 in the industrial chocolate sector. The rise of automation and just-in-time manufacturing systems in the food processing industry has propelled demand for liquid chocolate, which provides immediate usability and reduces the need for additional processing steps. Liquid chocolate supports streamlined operations, enabling manufacturers to optimize production lines and swiftly integrate chocolate coatings or fillings into a wide range of products. Its ready-to-use nature also addresses the needs of modern food manufacturers who seek to minimize labor, save time, and reduce processing losses linked with solid chocolate forms. As industrial facilities increasingly migrate toward technology-driven solutions and adaptable production protocols, liquid chocolate's compatibility with automated equipment becomes a strong selling point. Consequently, the segment's robust growth trajectory is supported by its efficiency advantages and the ability to bolster flexible, high-speed food production environments.

By Application: Bakery Products Lead While Frozen Desserts Accelerate

Bakery products hold the largest market share within the Indian industrial chocolate sector, accounting for 32.12% in 2025. This leading position reflects the ongoing expansion of India's organized bakery industry, where industrial chocolate is an essential ingredient in manufacturing cakes, pastries, and biscuits supplied across traditional and modern retail channels. The growth of urban lifestyles, influence of Western eating habits, and heightened demand for indulgent snacks have propelled widespread adoption of chocolate-based baked goods in India. Chocolate’s versatile application in both coating and filling forms helps brands enhance the appeal and shelf-life of their bakery offerings, making it a staple for countless manufacturers. Technological improvements in bakery processing, alongside innovative product development featuring new flavors and formats, continue to reinforce the segment’s prominence.

Meanwhile, frozen desserts and ice creams constitute the fastest growing application in India’s industrial chocolate market, projected to expand at a CAGR of 7.76% from 2026 to 2031. This segment’s impressive momentum is closely linked to the rapid expansion of cold-chain infrastructure, enabling efficient distribution and storage of temperature-sensitive desserts across the nation. Premiumization within the dairy-based dessert category has driven manufacturers to experiment with gourmet chocolate inclusions and richer, higher-quality formulations. Rising disposable incomes and shifting consumer preferences toward indulgent, premium treats have fostered greater experimentation with chocolate flavors, textures, and layered inclusions in frozen desserts and ice creams. The proliferation of new retail formats and food service channels, including QSRs and dessert cafés, has amplified visibility and demand for premium chocolate-based frozen creations.

Geography Analysis

India's industrial chocolate market is witnessing concentrated growth in Maharashtra, Gujarat, and Karnataka. These states boast established food processing infrastructures and easy port access for both importing raw materials and distributing finished products. Maharashtra, with its 40 pharmaceutical clusters as per government surveys, showcases a robust industrial backbone that bolsters its chocolate manufacturing capabilities . Meanwhile, Gujarat, home to 13 identified clusters, leverages its proximity to major ports to streamline cocoa imports. Karnataka's burgeoning IT sector is fueling a rising demand for premium food products, especially in the urban market of Bangalore. In the southern states, Kerala, Tamil Nadu, and Andhra Pradesh play pivotal roles in domestic cocoa cultivation. Kerala, in particular, spearheads production initiatives, bolstered by collaborations with agricultural universities and Mondelez's Cocoa Life program, which actively engages local farming communities.

Regional dynamics highlight disparities in infrastructure capabilities and market maturity. For instance, northern states like Uttar Pradesh, with dedicated food processing policies, are targeting a 6% processing rate, lagging behind the national average of 10% . The India-EFTA Trade and Economic Partnership Agreement, set to take effect in October 2025, stands to benefit western coastal regions. The agreement promises reduced duties on Swiss chocolate imports, a move that could significantly alter the competitive landscape for domestic industrial chocolate producers. Cold-chain infrastructure development is primarily centered in urban hubs and key transportation corridors. Government initiatives are focusing on establishing integrated pack-houses and enhancing refrigerated transport connectivity, both vital for efficient chocolate distribution. The concentration of cocoa cultivation in the southern states presents industrial chocolate manufacturers with opportunities for vertical integration, allowing them to exert greater control over their supply chains and optimize costs.

While eastern and northeastern regions present untapped potential, they grapple with infrastructure challenges and a cultural inclination towards traditional sweets over chocolate. Yet, government initiatives, notably the PM Kisan Sampada Yojana, are making strides. With 41 Mega Food Parks and 394 Cold Chain projects, the aim is to broaden processing capabilities beyond the conventional manufacturing hubs. The rise of organized retail and e-commerce is enhancing chocolate distribution, reaching markets that were once overlooked. However, rural areas still face hurdles due to income limitations and distribution issues. Regional taste preferences are shaping product development: southern markets are warming up to dark chocolate, while northern regions maintain a preference for milk chocolate. This divergence presents a unique opportunity for tailored industrial chocolate solutions catering to specific geographic tastes.

Competitive Landscape

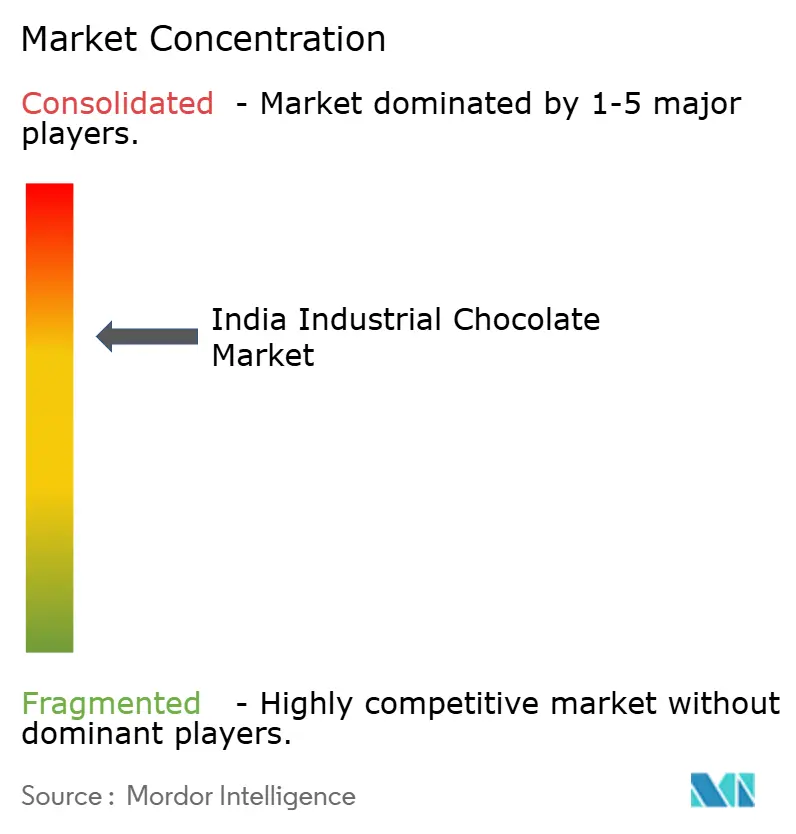

The India industrial chocolate market demonstrates moderate concentration, with a score of 7. Established multinational companies leverage their scale advantages and efficient supply chain capabilities to maintain a strong foothold. Meanwhile, emerging craft producers are gaining traction in premium segments by focusing on differentiated positioning and promoting sustainable sourcing practices. This dual dynamic creates a competitive environment where both established players and new entrants strive to capture market share through unique strategies and offerings.

The market is highly competitive, with the presence of numerous local and international players. Prominent companies operating in the market include Barry Callebaut Group, DP Cocoa Products Pvt. Ltd., Lotus Chocolate Company Ltd., Puratos Group, and Aadra International. These players are actively adopting strategies such as product innovations and geographical expansions to strengthen their market presence. Additionally, acquisitions have emerged as a significant approach for companies to enhance their capabilities and broaden their reach within the market.

Another notable trend in the market is the increasing focus on single-origin chocolate production. Companies are collaborating with Indian farmers to source cocoa that meets specific requirements, enabling them to cater to the growing demand for premium and authentic chocolate products. This approach not only supports local farming communities but also aligns with the rising consumer preference for sustainably sourced and high-quality ingredients. Such initiatives are expected to further intensify competition in the market during the forecast period.

India Industrial Chocolate Industry Leaders

-

Barry Callebaut Group

-

DP Cocoa Products Pvt Ltd

-

Lotus Chocolate Company Ltd.

-

Puratos Group

-

Aadra International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Barry Callebaut has opened its third chocolate manufacturing facility in India. The new 20,000-square-meter greenfield factory, situated in the Ghiloth industrial area of Neemrana and about 120 kilometers from Delhi, boasts state-of-the-art production lines for chocolate and compound in various formats, along with integrated warehousing.

- March 2025: Mondelez ramped up cocoa cultivation in South India and explored prospects in the North-East as African cocoa supplies faced challenges. In collaboration with research institutions like the Central Plantation Crops Research Institute (CPCRI) and Kerala Agriculture University, Mondelez India ensured the distribution of premium seedlings and established optimal cocoa farming practices.

- February 2024: Nestlé India announced a substantial manufacturing expansion, investing between INR 6,000 to 6,500 crore. The expansion included the establishment of its tenth factory in Orissa and the enhancement of its chocolate production lines, reflecting robust demand projections and its commitment to the 'Make in India' initiative.

India Industrial Chocolate Market Report Scope

In the chocolate industry, chocolate is the primary ingredient required for the production of consumable chocolate or desserts, which require the application of varied kinds of chocolate. The Indian industrial chocolate market is segmented by type and application. By type, the market is segmented into cocoa powder, cocoa liquor, cocoa butter, and compound chocolate. By application, the market is segmented into bakery products, confectionery, bakery premixes, beverages, frozen desserts and ice creams, and other applications. Additionally, the bakery products segment is further segmented into cakes, biscuits, pastries, and other bakery products. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Category

| Real Chocolate |

| Compound Chocolate |

By Product Type

| Dark Chocolate |

| Milk Chocolate |

| White Chocolate |

By Form

| Blocks and Slabs |

| Liquid |

| Chips and Chunks |

| Others |

By Application

| Bakery Products | Cakes and Pastries |

| Biscuits | |

| Other Types | |

| Confectionery | |

| Bakery Premixes | |

| Beverages | |

| Frozen Desserts and Ice Creams | |

| Other Applications |

| By Category | Real Chocolate | |

| Compound Chocolate | ||

| By Product Type | Dark Chocolate | |

| Milk Chocolate | ||

| White Chocolate | ||

| By Form | Blocks and Slabs | |

| Liquid | ||

| Chips and Chunks | ||

| Others | ||

| By Application | Bakery Products | Cakes and Pastries |

| Biscuits | ||

| Other Types | ||

| Confectionery | ||

| Bakery Premixes | ||

| Beverages | ||

| Frozen Desserts and Ice Creams | ||

| Other Applications | ||

Key Questions Answered in the Report

How large is the India industrial chocolate market in 2026?

It is valued at USD 1.84 billion and is projected to reach USD 2.57 billion by 2031 at a 6.92% CAGR.

Which segment holds the highest India industrial chocolate market share?

Compound Chocolate leads with 61.88% share in 2025 due to cost efficiency and versatility.

What is driving demand in Frozen Desserts applications?

Rapid cold-chain expansion and consumer premiumization are lifting Frozen Desserts and Ice Creams at a 7.76% CAGR.

Which regions are most attractive for new capacity?

Western and southern states such as Maharashtra, Gujarat, and Karnataka offer port access, trained labor, and proximity to cocoa-growing belts.

Page last updated on: