Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

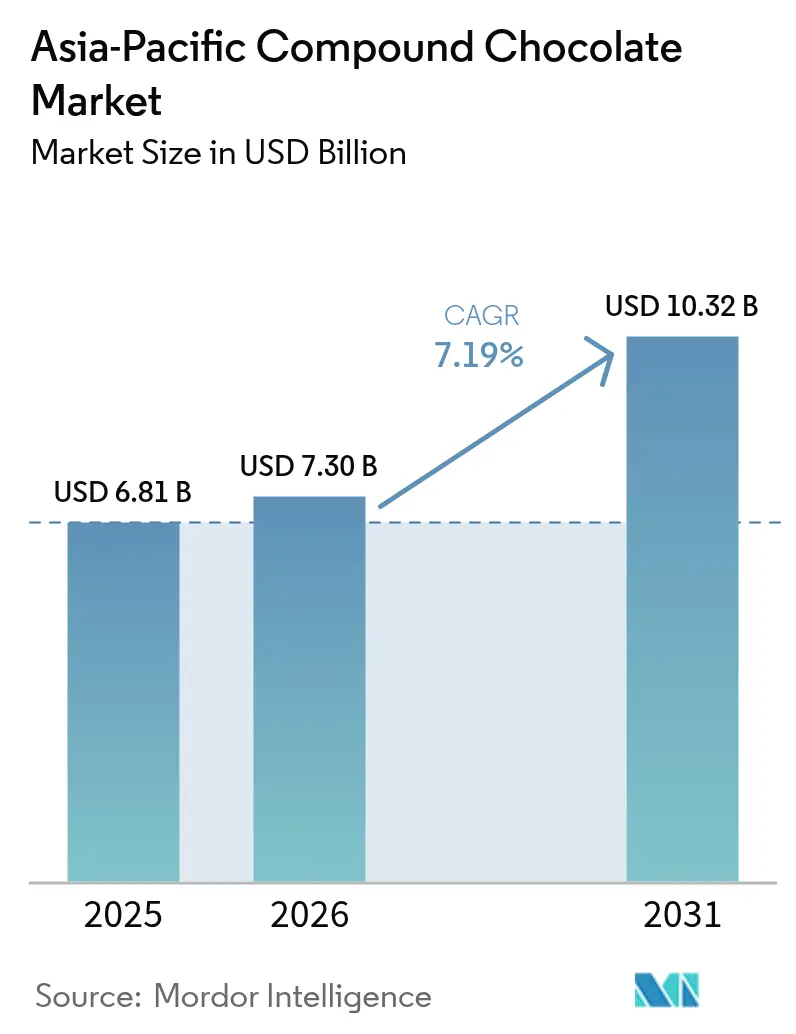

| Base Year Market Size (2025) | USD 6.81 Billion |

| Market Size (2026) | USD 7.3 Billion |

| Market Size (2031) | USD 10.32 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Compound Chocolate Market Analysis by Mordor Intelligence

The compound chocolate market size in Asia-Pacific market size in 2026 is estimated at USD 7.3 billion, growing from 2025 value of USD 6.81 billion with 2031 projections showing USD 10.32 billion, growing at 7.19% CAGR over 2026-2031. This growth is driven by increasing demand from industrial bakers, the cost-effectiveness of compound chocolate compared to real chocolate, and its superior heat resistance in tropical climates. China leads the market due to its large-scale manufacturing capabilities, while Australia's focus on premium products is boosting the use of certified-sustainable ingredients. The expansion of modern retail and e-commerce platforms is making compound chocolate more accessible to small bakeries. Additionally, research and development efforts are fostering innovation, particularly in plant-based and cocoa-free alternatives. However, challenges such as fluctuating raw material prices and stricter labeling regulations may slow growth but are unlikely to hinder the market's overall expansion.

Key Report Takeaways

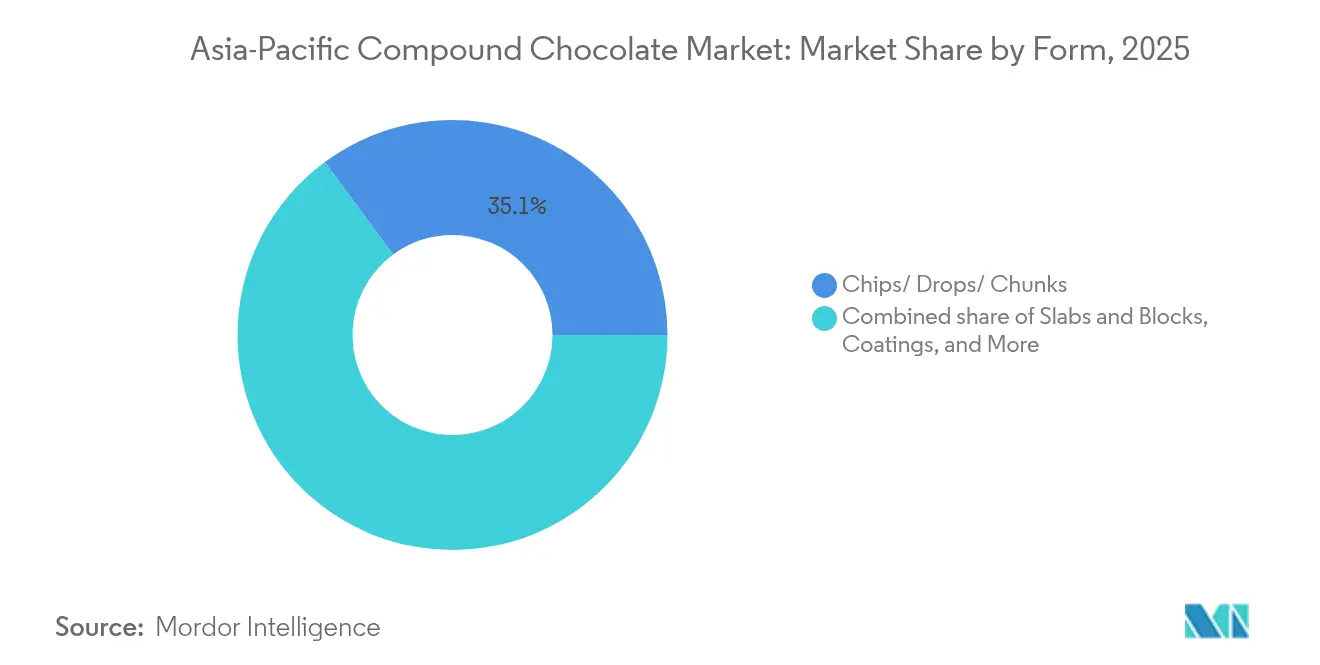

- By form, chips, drops, and chunks held 35.12% of the Asia-Pacific compound chocolate market share in 2025; fillings and spreads are advancing at a 7.63% CAGR to 2031.

- By type, milk compound chocolate accounted for 41.85% share of the Asia-Pacific compound chocolate market size in 2025, while dark compound chocolate is growing at the fastest 7.92% CAGR through 2031.

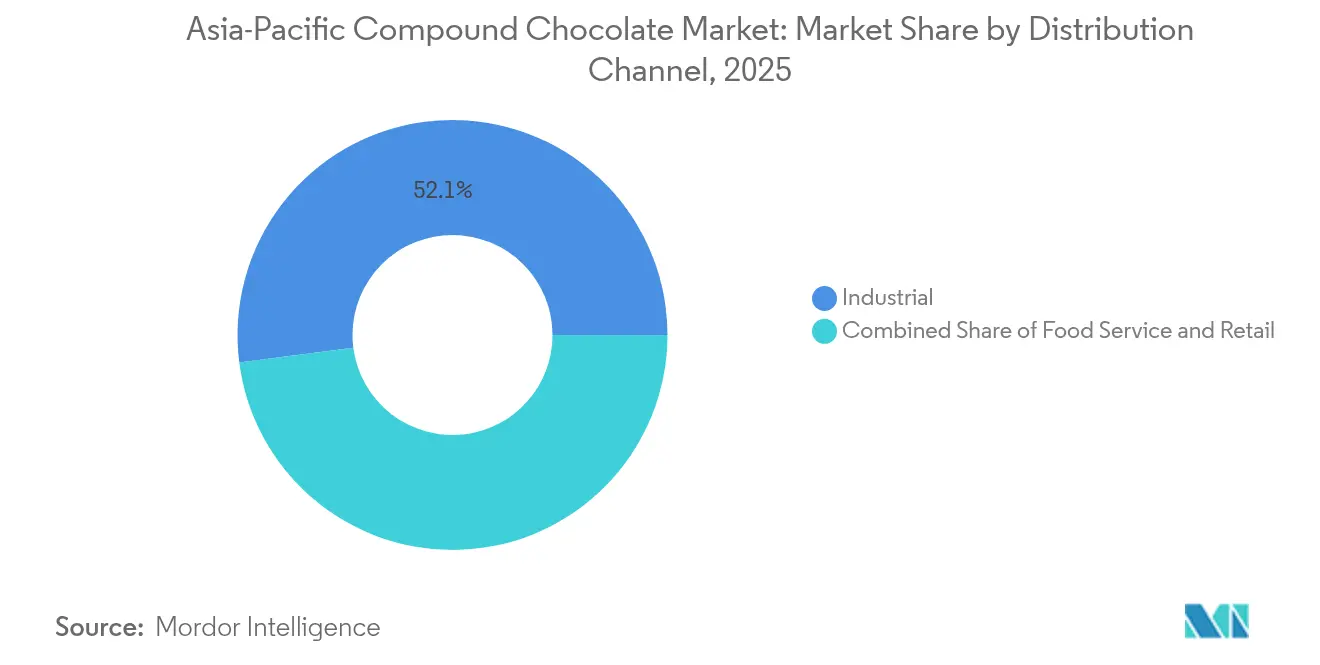

- By distribution channel, industrial buyers commanded 52.05% of the Asia-Pacific compound chocolate market share in 2025; foodservice is expanding at an 8.34% CAGR to 2031.

- By geography, China led with 35.70% revenue share in 2025; Australia records the highest forecast CAGR at 7.13% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Compound Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from expanding confectionery and bakery industries | +1.8% | China, India, Southeast Asia | Medium term (2-4 years) |

| Urbanization and fast-paced lifestyles | +1.5% | Urban centers across APAC, particularly China, India, Indonesia | Long term (≥4 years) |

| Influence of Western lifestyles and festivals | +0.9% | Japan, Australia, urban India, China | Medium term (2-4 years) |

| Product innovation in flavors and textures | +1.2% | Global, with early adoption in Japan, Australia | Short term (≤2 years) |

| Expansion of modern retail and e-commerce | +1.4% | Southeast Asia, India, China | Medium term (2-4 years) |

| Technological advancements in production | +0.8% | Manufacturing hubs in China, Thailand, Indonesia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Expanding Confectionery and Bakery Industries

The confectionery and bakery sectors in China and India are undergoing structural expansion, with India's chocolate and cocoa product imports reaching USD 879 million in 2024, reflecting a 12% year-on-year increase[1]UN Comtrade, "List of supplying markets for a product imported by IndiaMetadata", trademap.org. The growing demand for chocolate-based products in India has been a key factor behind this increase. Similarly, the confectionery and bakery sectors in China are experiencing rapid growth, supported by rising urbanization and changing consumer preferences. Compound chocolate, which is 20-30% cheaper than real chocolate due to the substitution of vegetable fats, has emerged as the preferred ingredient for mass-market products such as biscuits, wafers, and enrobed confections. China's role as a leading contract manufacturer for global brands has further boosted the demand for standardized compound coatings. These coatings not only meet export standards but also ensure shelf stability, making them ideal for non-refrigerated supply chains. This trend is expected to contribute 1.8 percentage points to the overall CAGR, with the most significant impact anticipated in the medium term as production capacities in tier-2 and tier-3 cities continue to expand.

Urbanization and Fast-Paced Lifestyles

Rapid urbanization across Asia-Pacific, with urban populations projected to exceed 50% by 2050, is reshaping food consumption patterns toward convenience-oriented, packaged snacks and ready-to-eat desserts[2]Economic and Social Commission for Asia and the Pacific, "Urban transformation in Asia and the Pacific: from growth to resilience", unescap.org. Compound chocolate-coated products such as protein bars, granola clusters, and single-serve pastries align with on-the-go consumption habits, particularly among working professionals and students in metro areas. The proliferation of convenience stores, growing at positive rate in ASEAN markets according to retail analytics, provides last-mile distribution for impulse-purchase chocolate products. This lifestyle shift is forecast to add 1.5 percentage points to the CAGR over the long term, with sustained momentum as disposable incomes rise and cold-chain infrastructure improves in emerging markets.

Product Innovation in Flavors and Textures

Manufacturers are focusing on flavor diversification and texture innovation to make their compound chocolate products stand out in a highly competitive market. They are introducing local flavors such as matcha in Japan, pandan in Southeast Asia, and cardamom in India to cater to regional preferences. Additionally, they are developing heat-resistant formulations to ensure chocolates remain stable in tropical climates, preventing issues like melting or blooming. In 2024, Barry Callebaut partnered with NotCo to use artificial intelligence in creating plant-based compound chocolate alternatives. These products replicate the taste and texture of dairy-based chocolates while offering lower saturated fat content. Similarly, Cargill collaborated with Voyage Foods to develop cocoa-free chocolate substitutes made from grape seeds and sunflower seeds. This innovation addresses supply chain challenges and promotes sustainability in the chocolate industry.

Expansion of Modern Retail and E-Commerce

The growing presence of organized retail and digital commerce platforms is revolutionizing access to compound chocolate products. This change allows smaller bakeries and home-based confectioners to easily source industrial-grade ingredients that were previously limited to B2B distributors. In 2024, e-commerce sales of food ingredients in Southeast Asia showed robust growth, with platforms like Alibaba's Tmall and Lazada providing bulk purchase options for compound chocolate chips, slabs, and coatings. Additionally, hypermarkets and specialty ingredient stores are expanding their private-label compound chocolate offerings, appealing to price-sensitive consumers who focus on affordability rather than brand legacy. This shift in retail dynamics is expected to boost the CAGR by 1.4 percentage points in the medium term, driven by improvements in last-mile logistics and cold-chain infrastructure, particularly in tier-2 cities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory compliance | -0.6% | Global, with heightened scrutiny in Australia, Japan | Short term (≤2 years) |

| Health concerns over sugar and fats | -1.1% | Australia, Japan, urban India, China | Medium term (2-4 years) |

| Supply chain disruptions | -0.5% | Southeast Asia, China | Short term (≤2 years) |

| Fluctuations in raw material prices | -1.3% | Global, particularly Indonesia, Malaysia, West Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over Sugar and Fats

Growing consumer awareness of the health risks associated with trans fats, saturated fats, and refined sugars is driving increased scrutiny of compound chocolate formulations, particularly in developed markets such as Australia and Japan. Advocacy groups and health authorities are pressuring manufacturers to reformulate their products by reducing sugar content and replacing hydrogenated fats with non-hydrogenated vegetable fats. However, these changes are raising production costs and complicating supply-chain management. In Australia, the clean-label movement, fueled by consumer demand for natural ingredients and transparent labeling, is further encouraging manufacturers to use certified sustainable palm oil and organic cocoa powder. This shift has led to a 10-15% increase in input costs.

Fluctuations in Raw Material Prices

Palm oil and cocoa powder, the two main ingredients for compound chocolate, experience frequent price fluctuations due to factors like weather conditions, geopolitical issues, and sustainability regulations. In 2024, palm oil prices rose sharply because of El Niño-driven droughts in Indonesia and Malaysia, the largest producers globally. At the same time, cocoa powder prices remained high following poor harvests in West Africa, which accounts for 70% of the world's cocoa bean supply. These price changes have tightened profit margins for compound chocolate manufacturers, who operate in a highly price-sensitive market and have limited ability to pass on higher costs to their customers. According to the 2024 Solidaridad Barometer, only 38% of palm oil used in food applications is certified as sustainable. This creates supply chain challenges, especially as regulatory authorities enforce stricter traceability requirements. These challenges are expected to reduce the compound annual growth rate (CAGR) by 1.3 percentage points in the medium term, with industrial buyers relying on spot-market purchases rather than long-term contracts being the most affected.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Chips and Drops Dominate Industrial Baking

In 2025, chips, drops, and chunks account for 35.12% of the market, highlighting their versatility in industrial baking applications such as cookies, muffins, and ice cream inclusions. These formats provide manufacturers with precise portion control, consistent melting properties, and reduced handling waste, making them ideal for high-volume production. The segment's strong position is further supported by the growth of quick-service restaurant chains and in-store bakeries in China and Southeast Asia, where standardized recipes require dependable ingredient performance. To address this demand, Cargill is expanding its Gresik facility in Indonesia in 2024 to focus on producing compound chocolate chips and drops for bakery clients in the region, emphasizing the segment's importance.

Fillings and spreads are projected to grow at a 7.63% CAGR from 2026 to 2031, driven by the increasing popularity of artisanal bakeries and premium patisseries. These businesses prefer ready-to-use options for layered cakes, pastries, and filled croissants. The premiumization trend in urban markets is encouraging consumers to spend more on visually appealing and multi-textured desserts. Additionally, advancements in shelf-stable fillings that do not require refrigeration are expanding distribution to smaller towns and rural areas, where cold-chain infrastructure is limited. Slabs, blocks, coatings, and other forms cater to specialized uses such as molding, enrobing, and artisan chocolate-making. Coatings, in particular, are becoming more popular in the confectionery sector for products like dragées and enrobed nuts.

By Type: Milk Leads, Dark Gains Health Halo

In 2025, milk compound chocolate holds a 41.85% share of the market, driven by its popularity in mass-market confections, biscuits, and ice cream coatings. Consumers prefer its sweeter and creamier taste, especially in price-sensitive retail channels where affordability and flavor are prioritized over health concerns. Milk compound chocolate is typically made with 20-30% cocoa powder, 40-50% sugar, and 20-30% vegetable fat, offering consistent flavor and texture at a lower cost compared to milk chocolate made with cocoa butter. Its strong market position is supported by long-standing consumer habits and the reliance of established confectionery brands on milk compound chocolate for their key products.

Dark compound chocolate is expected to grow at a CAGR of 7.92% from 2026 to 2031, driven by increasing demand from health-conscious consumers. These consumers prefer lower-sugar and higher-cocoa formulations. This segment is gaining popularity in premium foodservice, specialty retail, and e-commerce platforms, where dark chocolate is associated with health benefits like antioxidants and lower calorie content. Research has linked cocoa flavonoids to improved cardiovascular health, but the vegetable fat in compound chocolate reduces these benefits compared to real dark chocolate. Additionally, white compound chocolate and niche variants like ruby and blonde are used in artisan confectionery and decorative baking. While their market volume is small, they generate high per-unit margins.

By Distribution Channel: Foodservice Outpaces Industrial

In 2025, the industrial distribution channel holds 52.05% of the market, serving large-scale confectionery and bakery manufacturers. These manufacturers prioritize bulk volumes, consistent quality, and competitive pricing. The segment's dominance stems from the capital-intensive nature of compound chocolate production, where economies of scale encourage long-term contracts between suppliers and buyers. Industrial customers focus on functional attributes like melting point, viscosity, and shelf stability, making compound chocolate ideal for products such as biscuit coatings, wafer fillings, and ice-cream inclusions. Low switching costs and market maturity provide stable revenues for global suppliers like Barry Callebaut, Cargill, and Fuji Oil Holdings.

The foodservice sector is expected to grow at a CAGR of 8.34% from 2026 to 2031, driven by the expansion of quick-service restaurants, cafés, and hotels. These businesses seek cost-effective yet artisanal dessert solutions. The premiumization of dining out has increased demand for indulgent desserts like molten lava cakes and chocolate fondues. Mars Wrigley's 2024 strategy in Southeast Asia, featuring smaller pack sizes and heat-resistant products for live-shopping platforms, highlights the channel's growth potential. The retail channel, including supermarkets, hypermarkets, online platforms, and convenience stores, caters to home bakers and small-scale confectioners. E-commerce is growing rapidly in India and Southeast Asia, supported by improved digital payment systems.

Geography Analysis

In 2025, China holds a 35.70% share of the Asia-Pacific compound chocolate market, driven by its role as a global manufacturing hub. Compound chocolate is widely used as a cost-effective ingredient in the production of bakery and confectionery items, particularly for export. The bakery sector in China is expected to grow steadily through 2030, supported by increasing per-capita consumption of Western-style baked goods and the expansion of domestic chains like BreadTalk and Paris Baguette. The National Health Commission regulates labeling and safety standards for compound chocolate, but enforcement varies across provinces. This inconsistency creates opportunities for regional suppliers to expand in tier-2 and tier-3 cities. In 2024, Shanghai's market surveillance bureau conducted inspections to ensure compliance with net content regulations for chocolate products. This increased regulatory focus is likely to benefit larger, compliant manufacturers while posing challenges for smaller, informal producers.

Australia is the fastest-growing market in the region, with a projected CAGR of 7.13% from 2026 to 2031. This growth is driven by the rising demand for clean-label products and premium offerings that appeal to health-conscious consumers. Australia's affluent population and strict food safety standards create a favorable environment for compound chocolate products made with certified sustainable palm oil and organic cocoa powder, despite these ingredients increasing production costs by 10-15%. The foodservice sector, particularly specialty cafés and patisseries, is increasingly using compound chocolate to create innovative desserts while balancing quality and cost. In 2024, Nestlé focused on sustainability-driven product lines, including premium chocolates in Asia-Pacific travel retail, highlighting the importance of Australia's premium segment.

India, Japan, and other Asia-Pacific countries account for the remaining market share. India benefits from rapid urbanization, higher disposable incomes, and growing demand for packaged snacks and confections. The country’s imports of chocolate and cocoa products grew by 12% year-on-year, reflecting increased domestic processing capacity and the expansion of modern retail formats. In Japan, the market is characterized by a focus on premium quality and high standards. Compound chocolate is primarily used in foodservice, such as dessert cafés and hotel pastry kitchens, where maintaining quality while controlling costs is essential.

Competitive Landscape

The Asia-Pacific compound chocolate market is moderately consolidated, with global confectionery manufacturers and strong regional processors shaping the supply dynamics. Leading players, including Cargill Incorporated, Barry Callebaut AG, Fuji Oil Holdings Co., Ltd., Puratos Group NV, and Nestlé S.A., maintain dominance by leveraging extensive distribution networks, cost-effective manufacturing, and consistent product quality to serve both industrial and retail segments effectively.

Regional companies stay competitive by offering customized formulations that cater to local taste preferences, price sensitivities, and diverse applications in bakery, confectionery, and ice cream products. Although new players are entering the market, factors such as reliance on stable cocoa substitutes, cost advantages driven by scale, and established client relationships create moderate barriers to entry.

Opportunities for growth include developing heat-resistant formulations suitable for tropical climates, incorporating local flavors like matcha and pandan, and expanding e-commerce channels to enable direct-to-consumer sales of specialty coatings and fillings. Emerging trends include plant-based and cocoa-free alternatives. For example, Cargill's collaboration with Voyage Foods focuses on creating cocoa-free chocolate substitutes using grape seeds and sunflower seeds, addressing supply chain challenges and promoting sustainability.

Asia-Pacific Compound Chocolate Industry Leaders

-

Barry Callebaut AG

-

Fuji Oil Holdings Co., Ltd.

-

Puratos Group NV

-

Nestlé S.A.

-

Cargill Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Barry Callebaut has introduced its third chocolate manufacturing facility in India. Strategically located in the Ghiloth industrial area of Neemrana, approximately 120 kilometers from Delhi, the 20,000-square-meter greenfield factory is equipped with advanced production lines for chocolate and compound in multiple formats, and integrated warehousing, according to the company.

- March 2025: Mondelez ramped up cocoa cultivation in South India and explored prospects in the North-East as African cocoa supplies faced challenges. In collaboration with research institutions like the Central Plantation Crops Research Institute (CPCRI) and Kerala Agriculture University, Mondelez India ensured the distribution of premium seedlings and established optimal cocoa farming practices.

- November 2024: Fuji Oil, as a part of strengthening its offerings for commercial-use chocolates, released its new “CP Series”. According to the company, the new series includes Sweet Chocolate CP25 Flakes and White Chocolate CP07 Flakes.

- March 2024: Cargill unveiled its NatureFresh Professional range of block chocolates, chocolate chips, and cocoa powder at AAHAR 2024, New Delhi, targeting the Indian food and bakery industry with products crafted from extensive research among top bakers and available in Intense Dark, Dark, Milk, and White variants.

Asia-Pacific Compound Chocolate Market Report Scope

The Asia-Pacific chocolate market is segmented by type that includes dark chocolate, milk chocolate, and white chocolate. Based on form, the market is divided into chocolate chips/drops/chunks, chocolate slab, chocolate coatings, and other products. By application, the market is classified into the bakery, confectionery, frozen desserts, and ice-cream, beverages, cereals, and others. The study also involves the analysis of regions such as China, Japan, India, Australia and the rest of Asia-Pacific.

Type

| Dark |

| Milk |

| White |

| Others |

Form

| Chips / Drops / Chunks |

| Slabs and Blocks |

| Coatings |

| Fillings and Spreads |

| Others |

Distribution Channel

| Foodservice | |

| Industrial | |

| Retail | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels |

Country

| China |

| India |

| Japan |

| Australia |

| Rest of Asia-Pacific |

| Type | Dark | |

| Milk | ||

| White | ||

| Others | ||

| Form | Chips / Drops / Chunks | |

| Slabs and Blocks | ||

| Coatings | ||

| Fillings and Spreads | ||

| Others | ||

| Distribution Channel | Foodservice | |

| Industrial | ||

| Retail | Supermarket/Hypermarket | |

| Online Retail Store | ||

| Convenience Store | ||

| Other Distribution Channels | ||

| Country | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is Asia-Pacific’s compound chocolate market in 2026?

The Asia-Pacific compound chocolate market size is USD 7.3 billion in 2026.

What is the expected CAGR for compound chocolate through 2031?

The market is forecast to expand at a 7.19% CAGR between 2026 and 2031.

Which form contributes the highest share today?

Chips, drops, and chunks hold 35.12% of Asia-Pacific compound chocolate market share in 2025.

Why is Australia the fastest-growing country segment?

Clean-label reformulations and premium positioning help Australia achieve a 7.13% CAGR to 2031.

Page last updated on: