Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

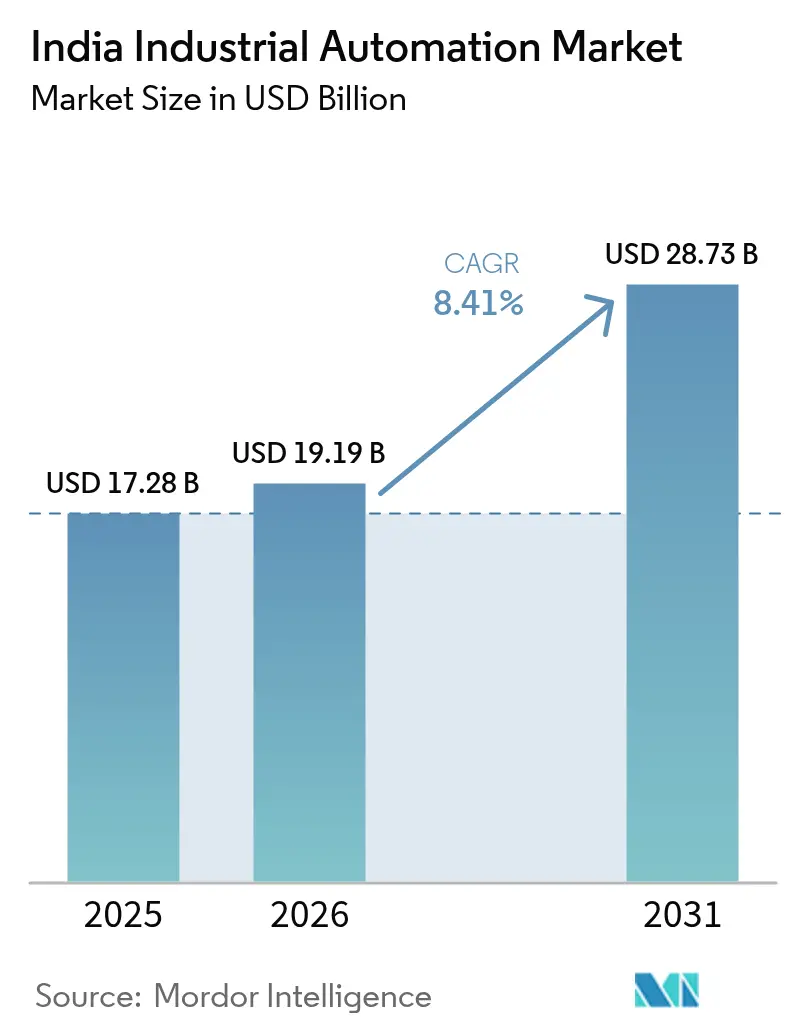

| Base Year Market Size (2025) | USD 17.28 Billion |

| Market Size (2026) | USD 19.19 Billion |

| Market Size (2031) | USD 28.73 Billion |

| Growth Rate (2026 - 2031) | 8.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Industrial Automation Market Analysis by Mordor Intelligence

The India industrial automation market size is expected to increase from USD 17.28 billion in 2025 to USD 19.19 billion in 2026 and reach USD 28.73 billion by 2031, growing at a CAGR of 8.41% over 2026-2031. Moving past the era of capacity-adding greenfield projects, discrete manufacturers are now focused on modular retrofits that pay for themselves in under two years, compressing the adoption timeline for programmable logic controllers, human-machine interfaces, and edge-native manufacturing execution systems. Government production-linked incentive (PLI) disbursements and a sharp fall in sensor prices make these upgrades affordable, while carbon-credit compliance deadlines push energy-intensive verticals toward automated monitoring. Although multinational vendors still dominate the higher-end of the value chain, a wave of micro, small, and medium enterprise retrofits is broadening the addressable base for solution providers, particularly in tier-2 and tier-3 industrial clusters. Mid-decade semiconductor shortages and rising cyber-insurance premiums remain headwinds, yet policy support and localized production commitments continue to underpin the long-term trajectory of the India industrial automation market.

Key Report Takeaways

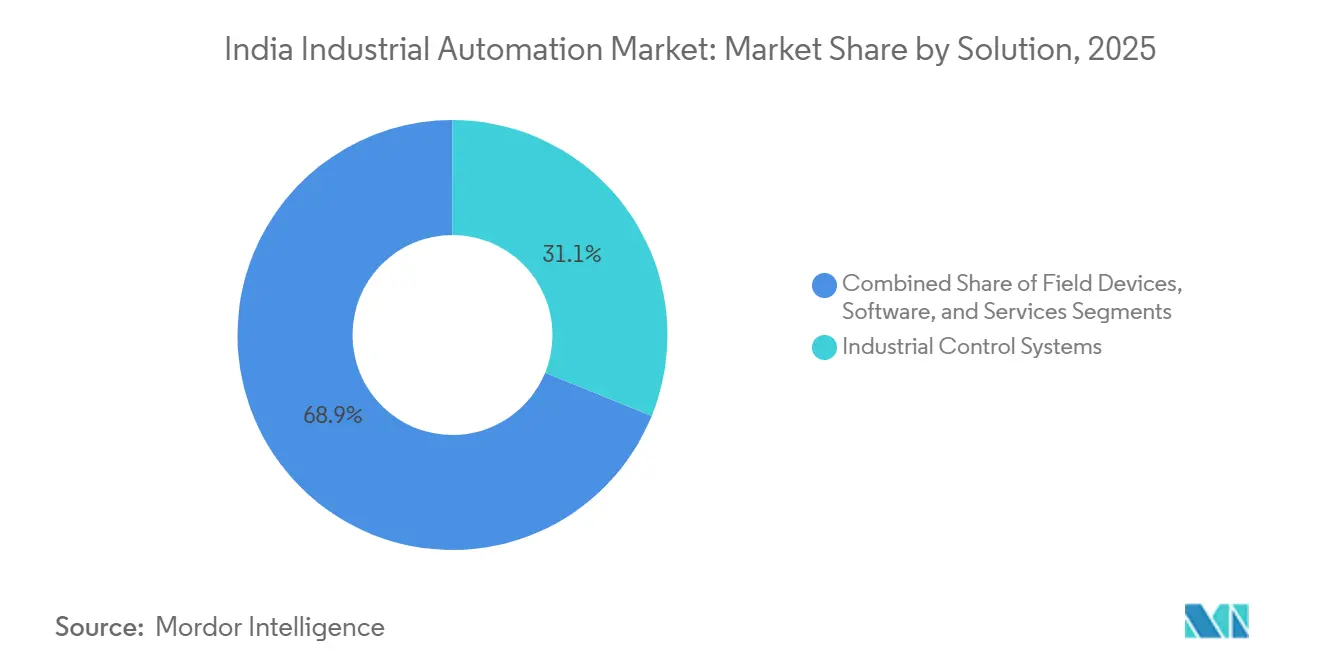

- By solution, industrial control systems led with a 31.14% share of the India industrial automation market in 2025, while software is projected to register a 9.62% CAGR through 2031.

- By automation type, programmable automation commanded 41.39% of the India industrial automation market share in 2025, whereas integrated or hyper-automation is forecast to grow at a 10.31% CAGR to 2031.

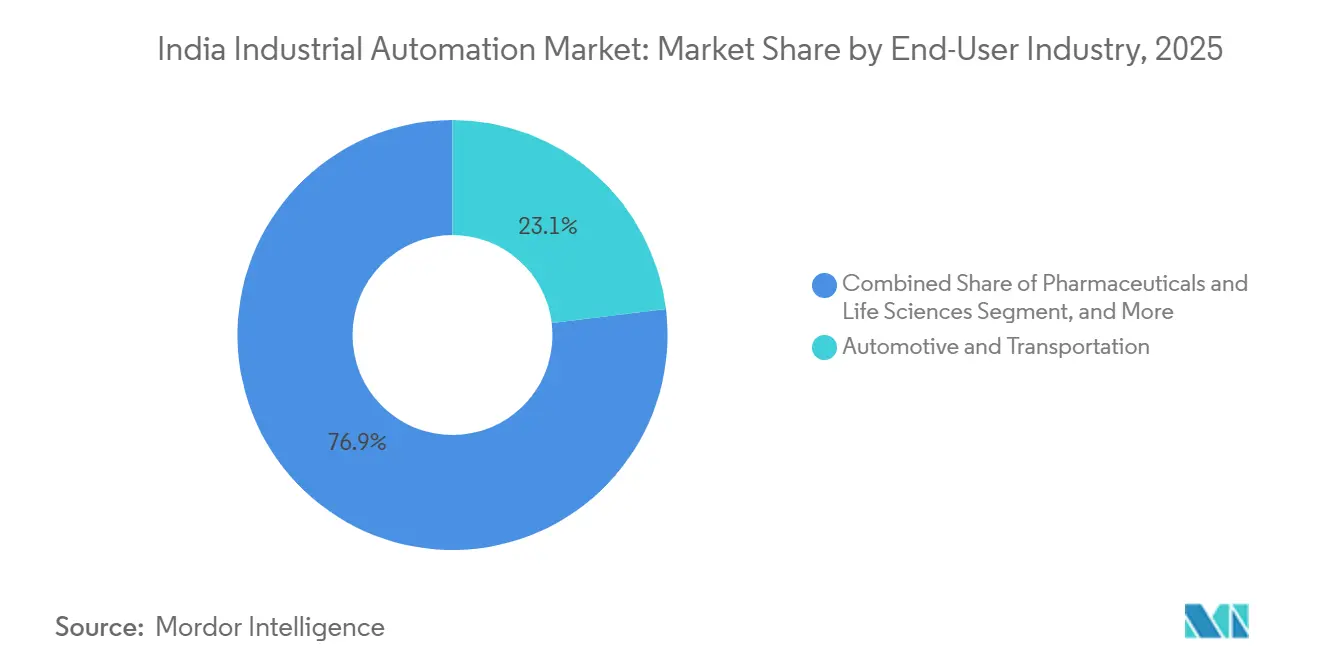

- By end-user industry, automotive and transportation held 23.07% of 2025 demand, but electronics and semiconductors are poised for the fastest expansion at 12.04% CAGR during 2026-2031.

- By deployment mode, on-premise architectures accounted for 43.77% of the 2025 base, yet hybrid configurations are advancing at an 11.23% CAGR owing to their balance of latency and scalability.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Industrial Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Make in India Manufacturing Investments | +2.1% | Gujarat, Maharashtra, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| Government PLI Scheme Incentives for Discrete Industries | +1.8% | National, early gains in automotive and electronics corridors | Short term (≤ 2 years) |

| Rapid Expansion of Brownfield Digital Retrofits across MSMEs | +1.5% | Tier-2 and Tier-3 industrial clusters | Medium term (2-4 years) |

| Sharp Decline in Industrial Sensor Costs | +1.2% | National | Short term (≤ 2 years) |

| AI-Driven Predictive Maintenance Demand from Mid-Tier Plants | +0.9% | Pharmaceuticals, automotive, chemicals | Medium term (2-4 years) |

| Carbon-Credit Linked Automation for Energy-Intensive Metals Vertical | +0.6% | Steel and cement belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Make in India Manufacturing Investments

More than USD 50 billion in new manufacturing announcements during 2024-2025 has set a strong floor for long-run automation demand, with automotive and electronics plants specifying programmable controllers and collaborative robots as baseline equipment.[1]Invest India, “Make in India Progress Report 2025,” investindia.gov.in Facility owners in Pune, Chennai, and Ahmedabad routinely target 25%-30% labor-hour reductions on new lines, aligning with state-level productivity clauses tied to incentive payouts. Electronics contract manufacturers deployed over 1,200 cobots in 2025 to achieve sub-millimeter placement accuracy required by global smartphone brands. Secondary cities, aided by lower land costs and newly minted mechatronics talent from local institutes, are emerging as hotbeds for integrated retrofits. Collectively, these deployments shorten payback horizons and reinforce the upward momentum of the India industrial automation market.

Government PLI Scheme Incentives for Discrete Industries

The Union government disbursed INR 28,748 crore (USD 3.44 billion) under various PLI programs by December 2025, and Budget 2026 nearly doubled allocations to INR 19,482.58 crore (USD 2.33 billion). Eligibility rules now require beneficiaries to demonstrate live production tracking through manufacturing execution or supervisory systems, driving direct purchases of plant-wide software.[2]Press Information Bureau, “PLI Schemes Disbursement Update,” pib.gov.in Automotive component suppliers in Tamil Nadu and Haryana responded by retrofitting legacy machining centers with programmable controllers to meet incentive-linked output thresholds, reducing payback periods to under 20 months. Pharmaceutical firms installed batch-control modules that link to enterprise resource planning, aligning with U.S. Food and Drug Administration data-integrity guidelines. The scheme’s structure channels capital toward automation rather than head-count additions, amplifying demand across solution tiers.

Rapid Expansion of Brownfield Digital Retrofits across MSMEs

Micro, small, and medium enterprises now account for the fastest growing customer group, with 38% of surveyed firms initiating retrofits in 2025, up from 22% a year earlier.[3]Confederation of Indian Industry, “Manufacturing Automation Survey 2025,” cii.in Low-cost programmable-logic-controller kits priced below INR 200,000 (USD 2,400) allow plants to automate single cells without complete line shut-downs, trimming upfront outlays by half. Integrators in Coimbatore and Pune deploy pre-configured human-machine-interface templates that cut commissioning times to four weeks, freeing capacity to serve more customers. Edge-native execution systems store data locally and sync to the cloud only when bandwidth is available, bridging broadband gaps in remote estates. Quality-assurance remains a concern, as nearly one-third of installations still fall short of interoperability standards, yet the retrofit wave materially expands the installed base that will later buy higher-level software.

Sharp Decline in Industrial Sensor Costs

Global oversupply pushed average sensor prices down 15%-20% between 2024 and 2025, stimulating a 35% jump in shipments to Indian factories. Pharmaceutical sites upgraded analog sensors to digital versions with self-diagnostics, cutting false alarms by 40% and feeding data into predictive-maintenance models. Food-processing lines added wireless vibration sensors that extended motor life from 18 to 30 months, slashing downtime by 25%. Redundant sensor arrays are now cost-effective in boiler and reactor controls, where a single failure can halt production valued above USD 100,000 per incident. To curb counterfeit imports, the Bureau of Indian Standards mandated ISI certification for transmitters used in hazardous areas effective January 2026.[4]Bureau of Indian Standards, “ISI Certification for Industrial Sensors,” bis.gov.in Lower costs thus combine with regulatory oversight to accelerate sensing density across the India industrial automation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX Sensitivity among Tier-3 Suppliers | -1.4% | Automotive and electronics supply chains | Short term (≤ 2 years) |

| Fragmented System-Integrator Ecosystem Quality Gaps | -1.1% | Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Persistent Supply Chain Disruptions for Automation Components | -0.8% | Import-dependent segments | Short term (≤ 2 years) |

| Cyber-Insurance Premium Escalation for OT Networks | -0.5% | Large enterprises with connected operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX Sensitivity among Tier-3 Suppliers

Firms with annual turnover below INR 500 crore (USD 60 million) hesitate to automate when order books dip beneath a two-quarter horizon, a scenario observed in 35% of plants during early 2025. Rising interest rates added 75-100 basis points to equipment loans, and collateral requirements moved from 1.2× to 1.5× principal value, constraining credit access. Leasing models remain nascent, covering under 10% of vendor sales, so many projects stall despite clear productivity gains. Tier-1 automakers launched vendor-development schemes that co-fund upgrades, yet coverage touches fewer than 5% of suppliers.[5]Maruti Suzuki India, “Investor Presentation 2025,” marutisuzuki.com Without broader financial instruments, small suppliers will continue to temper the growth trajectory of the India industrial automation market.

Fragmented System-Integrator Ecosystem Quality Gaps

India hosts more than 800 system integrators, yet fewer than 50 carry top-tier vendor certifications, resulting in wide variation in project quality.[6]Automation Industry Association of India, “System Integrator Landscape Report 2025,” aia-india.org An audit found that 28% of 2025 retrofits needed rework within a year due to poor network architecture or weak cybersecurity segmentation. Certification courses are clustered in metropolitan hubs, leaving regional players to reverse-engineer competitor code, which perpetuates non-standard practices. Pharmaceuticals and food processors increasingly bypass local firms in favor of multinational engineering houses, inflating project costs by 20%-30% but safeguarding compliance. Until training pipelines scale and a national registry for integrator performance emerges, inconsistent execution will dampen confidence among would-be adopters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Software Layers Capture Rising Value Share

Industrial control systems retained 31.14% of 2025 revenue, anchored by distributed control systems in continuous-process industries and programmable-logic-controller racks in discrete plants. Field devices still ship in the largest volumes, yet vendors now bundle sensors, drives, and actuators with software-as-a-service contracts to defend margins. The India industrial automation market size for software is projected to expand at a 9.62% CAGR to 2031 as manufacturers bolt product-lifecycle-management and enterprise-resource-planning modules onto aging supervisory systems. In response, Siemens launched MindSphere in 2025, pricing access at INR 50,000 (USD 600) per asset year, signaling a pivot toward recurring revenue.

Robotics shipments expanded 40% in 2025 on the back of sub-USD 25,000 collaborative units that require no cages and switch tasks within hours. Human-machine interfaces moved from stainless-steel panels to ruggedized tablets, trimming hardware spend by 30% and enabling remote maintenance during the monsoon disruptions of July-August 2025. Supervisory control systems increasingly employ hybrid data historians, keeping latency-sensitive tags on-site while exporting anonymized datasets to the cloud for benchmarking. Services consume one-quarter of total project value as users outsource commissioning risk, reinforcing the multi-tiered growth profile of the India industrial automation market.

By Automation Type: Hyper-Automation Gains Traction

Programmable automation led with 41.39% of the India industrial automation market share in 2025 thanks to its flexibility in mid-volume production. Hyper-automation, which fuses machine vision, robotic process automation, and artificial intelligence, is slated to grow at 10.31% through 2031 as high-mix plants chase zero-defect output. A Pune auto-component maker cut changeover time from four hours to twenty minutes after installing a vision-guided cell that self-adjusts for ±2 mm part variance.

Fixed automation still underpins high-volume beverage and cement lines but faces obsolescence risk should SKU counts proliferate. Flexible conveyor systems with quick-change tooling are gaining ground in packaging venues where order fragmentation has risen 50% since 2020. Hyper-automation’s complexity necessitates specialist skills that most mid-tier users lack, ensuring programmable automation remains the single largest bucket even as investment tilts toward artificial-intelligence-enabled upgrades. The net effect keeps the India industrial automation market on a dual-track trajectory of mature in-plant controls and emerging cognitive overlays.

By End-User Industry: Electronics and Semiconductors Lead Growth

Automotive and transportation commanded 23.07% of demand in 2025, buoyed by electric-vehicle assembly and torque-traceability mandates. The India industrial automation market size for electronics and semiconductors is forecast to expand at a 12.04% CAGR as the India Semiconductor Mission 2.0 channels USD 10 billion toward local wafer fabrication. Pharmaceutical sites seek validation-ready systems that meet U.S. and European audit standards, adding consistent baseline demand.

Fast-moving consumer-goods lines automate secondary packaging to handle a 30% spike in e-commerce volumes, while steel mills install energy-management modules linked to carbon-credit registries. Semiconductor fabs under construction in Gujarat and Karnataka specify fully automated material-handling and statistical-process-control loops to achieve 99.9999% uptime for future 28-nanometer nodes. Automotive growth will decelerate once electric-vehicle penetration plateaus near 15% of new sales, yet electronics should sustain double-digit expansion as India targets USD 300 billion in electronics output by 2030.

By Deployment Mode: Hybrid Models Gain Momentum

On-premise architectures secured 43.77% of 2025 installations because process industries cannot compromise on millisecond-grade control loops. Hybrid designs are expected to outpace all others, advancing at an 11.23% CAGR as discrete plants adopt edge controllers for motion control and cloud analytics for predictive maintenance. This model stores mission-critical data locally while uploading contextual metrics for fleet-wide benchmarking, aligning with India’s emerging data-protection norms.

Pharmaceutical exporters prefer hybrids that maintain FDA-compliant audit trails onsite yet allow global collaboration on design changes. Automotive suppliers report 15%-20% shorter order-to-ship cycles after linking shop-floor execution systems with tier-1 customers’ enterprise-resource-planning instances. Cybersecurity worries temper broader adoption, with 42% of manufacturers lacking dedicated operational-technology security teams. Nonetheless, zero-trust and anomaly-detection features bundled into modern platforms help offset risk, ensuring hybrid architectures steadily expand their footprint within the India industrial automation market.

Geography Analysis

Maharashtra, Gujarat, Tamil Nadu, and Karnataka together contributed roughly 55%-60% of 2025 spending, reflecting dense automotive, electronics, and pharmaceutical hubs. Maharashtra led in absolute terms, powered by Pune’s automotive corridor and Mumbai’s life-science cluster. Tamil Nadu is the fastest growing state as electronics contract manufacturers in Chennai and Hosur ramp up output for global smartphone brands. Gujarat’s share is climbing on semiconductor projects in Sanand and Dholera, where automation contracts already exceed USD 500 million. Karnataka saw programmable-logic-controller shipments rise 30% year-over-year amid aerospace and defense investments backed by production incentives.

Northern states such as Uttar Pradesh and Haryana account for another quarter of demand, driven by Noida’s electronics ecosystem and Gurugram’s auto supply base. Eastern regions lag, but Odisha’s metals corridor is piloting energy-management systems that connect directly to carbon-credit ledgers. Proximity to western ports trims delivery times for imported controllers by up to ten days, an edge that resonates when semiconductor shortages stretch lead times beyond sixteen weeks. Tier-2 cities like Coimbatore, Rajkot, and Ludhiana are emerging as micro-automation hubs thanks to the Gati Shakti National Master Plan, which lowers logistics costs and widens access to trained talent.

Regional skill disparities influence commissioning speed: Tamil Nadu’s training institutes graduated 12,000 mechatronics technicians in 2025, twice the output of comparable programs in the east. Cloud-enabled remote monitoring lets vendors support tier-3 locations without maintaining expensive service depots, broadening the practical reach of the India industrial automation market. Yet inconsistent state-level subsidies create arbitrage in project economics, shaping how integrators allocate scarce engineering capacity across India’s diverse manufacturing belts.

Competitive Landscape

The top five multinationals, Siemens, ABB, Schneider Electric, Rockwell Automation, and Honeywell, held an estimated 45%-50% revenue share in 2025, cementing a moderately concentrated structure. Schneider Electric’s INR 3,200 crore (USD 383 million) commitment to three new plants announced at ELECRAMA 2025 underscores the strategic shift toward localized switchgear and controller production. ABB invested INR 140 crore (USD 16.8 million) to add ultra-premium-efficiency motor capacity and capture demand from the Bureau of Energy Efficiency’s new IE3-plus standards. Rockwell Automation plans to double India revenue within eight years, backed by an USD 80 million Chennai site dedicated to discrete automation.

Mid-tier specialists compete on niche expertise: Yokogawa dominates distributed control systems in refineries, Omron focuses on compact controllers for packaging, and Mitsubishi Electric nurtures an e-Factory Alliance to raise integrator capability. Home-grown conglomerates such as Larsen and Toubro act mainly as integrators and panel builders, bundling imported components for infrastructure projects while lacking proprietary software stacks. White-space opportunities center on validation-ready pharmaceutical automation, real-time carbon-tracking modules, and cyber overlays for legacy controllers, each underserved by the current roster.

Start-ups add dynamism: Litmus Automation deployed edge-intelligence platforms at 50 plants after raising USD 17 million in Series B funding, while ABB’s Ability suite displaced incumbent condition-monitoring vendors at three major steel producers. Patent filings for industrial-automation technologies in India rose 22% in 2025, with distributed-ledger applications for supply-chain traceability and digital-twin frameworks leading the surge. Competitive differentiation is therefore tilting from hardware to data-driven services, reinforcing the software-centric evolution of the India industrial automation market.

India Industrial Automation Industry Leaders

ABB India Ltd

Siemens Ltd (India)

Schneider Electric India Pvt Ltd

Rockwell Automation India Pvt Ltd

Mitsubishi Electric India Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Schneider Electric India inaugurated a INR 1,100 crore (USD 132 million) medium-voltage switchgear facility in Hyderabad, equipped with EcoStruxure-enabled self-diagnostics.

- January 2026: ABB India entered a multi-year INR 500 crore (USD 60 million) agreement with Tata Steel to roll out ABB Ability digital solutions across five steel plants.

- December 2025: Rockwell Automation India launched FactoryTalk Design Hub, a cloud engineering suite aligned with GAMP 5 validation.

- November 2025: Siemens India secured a INR 800 crore (USD 96 million) order from Bharat Heavy Electricals Limited for distributed control systems at two supercritical units in Chhattisgarh.

India Industrial Automation Market Report Scope

Industrial automation refers to the use of control systems, such as computers or robots, and information technologies for handling different processes and machinery in an industry to replace human beings. It is the second step beyond mechanization in the scope of industrialization.

The India Industrial Automation Market Report is Segmented by Solution (Industrial Control Systems [Distributed Control System (DCS), Supervisory Control and Data Acquisition (SCADA), Programmable Logic Controller (PLC), Human Machine Interface (HMI), and Other Industrial Control Systems], Field Devices [Sensors and Transmitters, Valves and Actuators, Motors and Drives, Robotics,and Other Field Devices], Software [Product Lifecycle Management (PLM), Enterprise Resource Planning (ERP), Manufacturing Execution System (MES), and Other Softwares], Services [Integration, and Maintenance and Training]), Automation Type (Fixed Automation, Programmable Automation, Flexible or Modular Automation, and Integrated or Hyper-Automation), End-User Industry (Automotive and Transportation, Oil and Gas, Food and Beverage, Pharmaceuticals and Life Sciences, Power and Utilities, Electronics and Semiconductors, Chemicals and Petrochemicals, Metals and Mining, Fast-Moving Consumer Goods (FMCG), Packaging, and Others End-User Industries), Deployment Mode (On-Premise, Cloud, and Hybrid), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Solution

| Industrial Control Systems | Distributed Control System (DCS) |

| Supervisory Control and Data Acquisition (SCADA) | |

| Programmable Logic Controller (PLC) | |

| Human Machine Interface (HMI) | |

| Other Industrial Control Systems | |

| Field Devices | Sensors and Transmitters |

| Valves and Actuators | |

| Motors and Drives | |

| Robotics | |

| Other Field Devices | |

| Software | Product Lifecycle Management (PLM) |

| Enterprise Resource Planning (ERP) | |

| Manufacturing Execution System (MES) | |

| Other Softwares | |

| Services | Integration |

| Maintenance and Training |

By Automation Type

| Fixed Automation |

| Programmable Automation |

| Flexible or Modular Automation |

| Integrated or Hyper-Automation |

By End-User Industry

| Automotive and Transportation |

| Oil and Gas |

| Food and Beverage |

| Pharmaceuticals and Life Sciences |

| Power and Utilities |

| Electronics and Semiconductors |

| Chemicals and Petrochemicals |

| Metals and Mining |

| Fast-Moving Consumer Goods (FMCG) |

| Packaging |

| Others End-User Industries |

By Deployment Mode

| On-Premise |

| Cloud |

| Hybrid |

| By Solution | Industrial Control Systems | Distributed Control System (DCS) |

| Supervisory Control and Data Acquisition (SCADA) | ||

| Programmable Logic Controller (PLC) | ||

| Human Machine Interface (HMI) | ||

| Other Industrial Control Systems | ||

| Field Devices | Sensors and Transmitters | |

| Valves and Actuators | ||

| Motors and Drives | ||

| Robotics | ||

| Other Field Devices | ||

| Software | Product Lifecycle Management (PLM) | |

| Enterprise Resource Planning (ERP) | ||

| Manufacturing Execution System (MES) | ||

| Other Softwares | ||

| Services | Integration | |

| Maintenance and Training | ||

| By Automation Type | Fixed Automation | |

| Programmable Automation | ||

| Flexible or Modular Automation | ||

| Integrated or Hyper-Automation | ||

| By End-User Industry | Automotive and Transportation | |

| Oil and Gas | ||

| Food and Beverage | ||

| Pharmaceuticals and Life Sciences | ||

| Power and Utilities | ||

| Electronics and Semiconductors | ||

| Chemicals and Petrochemicals | ||

| Metals and Mining | ||

| Fast-Moving Consumer Goods (FMCG) | ||

| Packaging | ||

| Others End-User Industries | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the projected size of the India industrial automation market by the end of 2031?

It is forecast to reach USD 28.73 billion, rising from USD 19.19 billion in 2026 on an 8.41% CAGR over 2026-2031.

Which solution category is expanding at the fastest clip?

Software layers such as manufacturing execution systems and product lifecycle management tools are projected to post a 9.62% CAGR, outpacing hardware-led segments.

Why are hybrid automation deployments seeing rapid uptake across Indian plants?

Hybrid architectures keep latency-sensitive control loops on-premise while sending non-critical data to the cloud, giving manufacturers real-time visibility without compromising millisecond response requirements.

How do India's production-linked incentive schemes affect automation investment decisions?

PLI payouts are tied to real-time production tracking and efficiency metrics, so beneficiaries must install advanced controllers and plant-wide software to stay compliant and unlock disbursements.

Which states account for the lion's share of automation spending?

Maharashtra, Gujarat, Tamil Nadu, and Karnataka together contribute about 55%-60% of total outlays, thanks to dense automotive, electronics, and pharmaceutical clusters.

Who holds the leading positions among suppliers?

Multinational vendors Siemens, ABB, Schneider Electric, Rockwell Automation, and Honeywell collectively control roughly half of overall revenue, reflecting moderate concentration.

Page last updated on: