Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 3.92 Billion |

| Market Size (2031) | USD 5.57 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

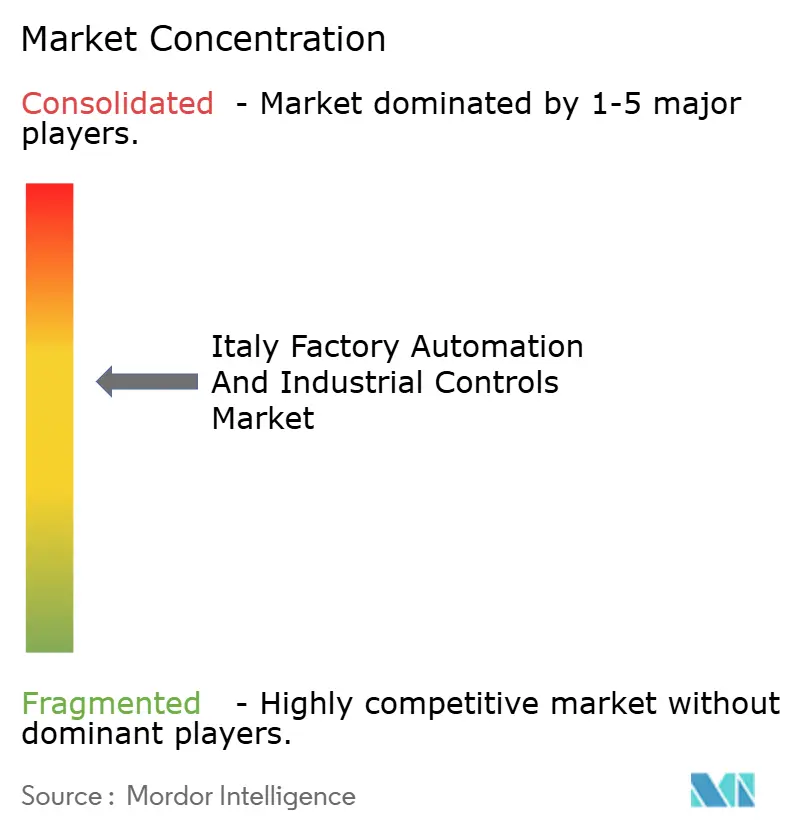

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The Italy Factory Automation and Industrial Controls Market size was USD 3.92 billion in 2026 and is projected to reach USD 5.57 billion by 2031, growing at a 7.28% CAGR over the forecast period. Demand is accelerating as Transition 4.0 and Transition 5.0 tax credits link reimbursements to measurable energy savings, steering budgets toward edge-enabled controls and real-time energy-management software. Automotive electrification programs led by Ferrari, Stellantis, and STMicroelectronics are accelerating demand for programmable-logic controllers and industrial PCs, while 5G private networks in Lombardy, Emilia-Romagna, and Veneto deliver sub-10-millisecond latency, unlocking digital twins for small and medium-sized enterprises. Hardware remains the revenue anchor, yet software subscriptions are scaling faster because NIS2 cybersecurity rules favor centrally patched architectures. Competitive rivalry is intense: global integrators must pair technology with audit-ready energy documentation to unlock subsidies, whereas local robotics specialists leverage agility to win turnkey projects.

Key Report Takeaways

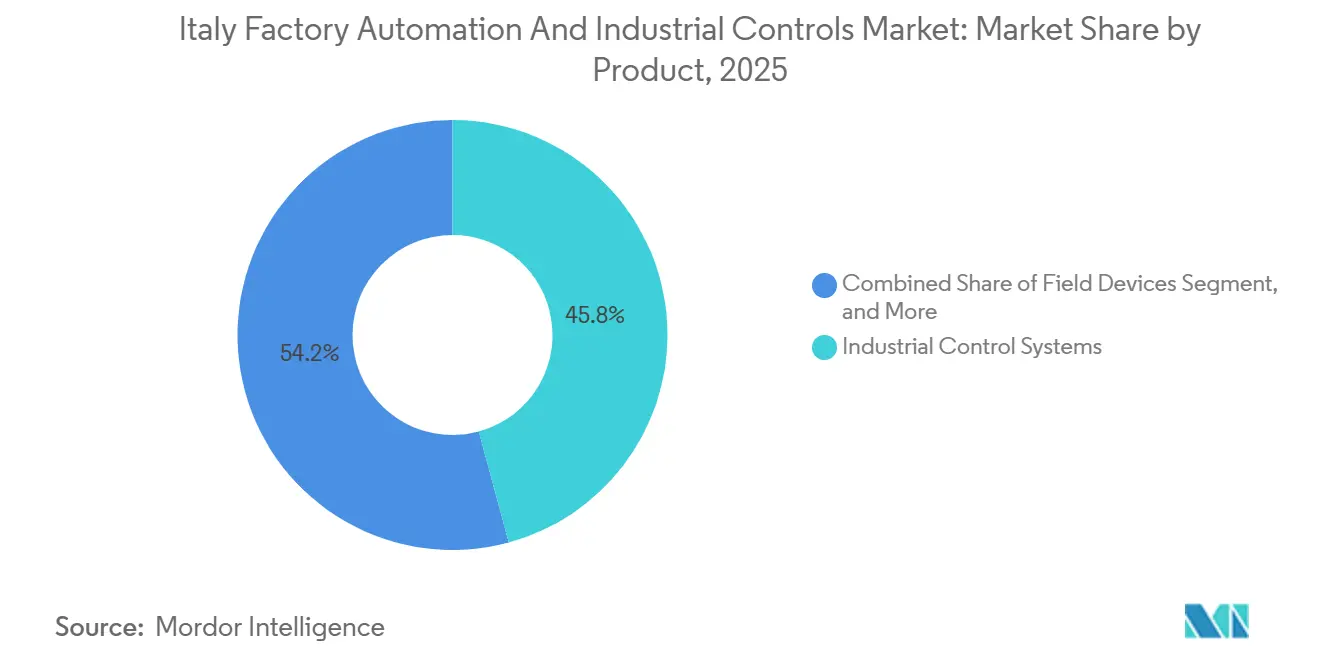

- By product category, industrial control systems led with a 45.78% revenue share in 2025, while industrial software and services are projected to advance at a 7.81% CAGR to 2031.

- By component, hardware accounted for 56.19% of the Italy Factory Automation and Industrial Controls Market share in 2025, whereas software is forecast to record the fastest growth at a 7.93% CAGR through 2031.

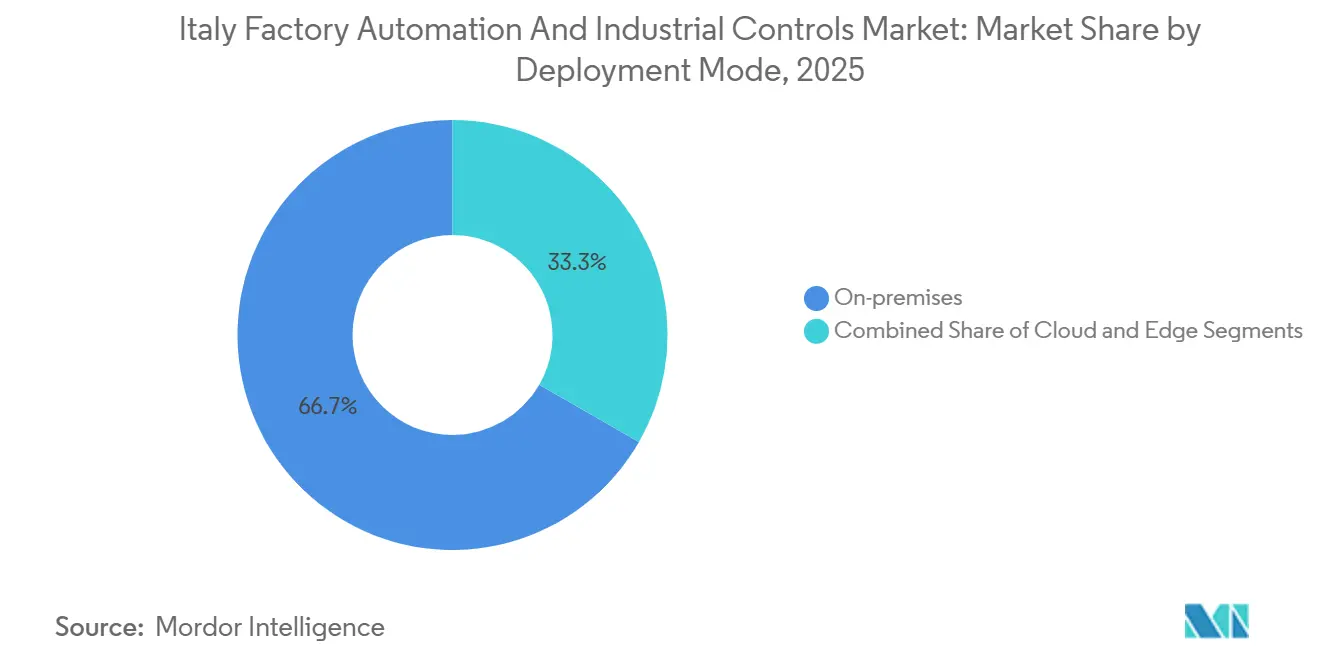

- By deployment mode, on-premises installations accounted for 66.71% of 2025 revenue, while cloud architectures are expected to expand at a 7.89% CAGR through 2031.

- By end-user industry, automotive and transportation contributed 29.12% of demand in 2025, while electronics and semiconductor manufacturing are expected to grow at an 8.77% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continuation of Transition 4.0 and 5.0 Tax Incentives | +1.2% | National, highest uptake in Lombardy, Emilia-Romagna, Veneto | Medium term (2-4 years) |

| Rising Labor Shortages in Skilled Manufacturing Roles | +0.9% | National, acute in northern industrial corridors | Long term (≥ 4 years) |

| Accelerating Automotive Electrification Investments | +1.1% | National, concentrated in Emilia-Romagna, Piedmont | Medium term (2-4 years) |

| Expansion of 5G and Fiber Industrial IoT Connectivity | +0.8% | National, early rollout in Lombardy, Emilia-Romagna, Veneto | Short term (≤ 2 years) |

| Surge in Modular DC Power Distribution Retrofits | +0.5% | National | Short term (≤ 2 years) |

| Integration of Leonardo Supercomputer for SME Simulation | +0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Continuation of Transition 4.0 and 5.0 Tax Incentives

Transition 5.0, introduced in 2025, ties a 35% to 45% rebate to a 3% facility-level or 5% process-level energy reduction, turning automation into a lever for decarbonization.[1]Italian Ministry of Economic Development, “Transition 4.0 and 5.0 Tax Incentives,” mise.gov.it Closed-loop edge gateways that document continuous savings now dominate purchasing shortlists, and Comau reported that energy-monitoring modules accompanied 63% of 2025 robot orders. The 2026 budget extended eligibility to 2027, prompting firms to front-load purchases and creating cyclical order spikes. Vendors, therefore, bundle audit-ready documentation with hardware to assure credit approval. Although frequent revisions create demand lumpiness, the incentive framework remains the single largest growth catalyst for the Italy factory automation and industrial controls market.

Rising Labor Shortages in Skilled Manufacturing Roles

Workers aged 55 and older accounted for 31% of Italy’s manufacturing headcount in 2025, the highest ratio among G7 economies.[2]Istat, “Manufacturing Employment and Production Data,” istat.it Unfilled machinist and technician vacancies exceeded 18,000 in northern districts, driving a 27% year-over-year increase in collaborative-robot shipments. Yaskawa’s Bologna training center compresses cobot-cell deployment time by half, allowing firms to offset lost tribal knowledge with standardized digital workflows. As retirements accelerate, manufacturers codify tacit knowledge into machine-vision and digital-twin systems that less specialized staff can supervise. Labor scarcity, therefore, structurally supports a shift toward autonomous systems and predictive analytics.

Accelerating Automotive Electrification Investments

Ferrari’s EUR 200 million (USD 226 million) e-building, which opened in June 2025, utilizes Siemens Totally Integrated Automation and ABB robots to achieve 10-micrometer bonding precision. Stellantis has earmarked EUR 2 billion (USD 2.26 billion) for the retooling of its Mirafiori and Melfi plants, devoting nearly one-fifth of the funds to control hardware and edge analytics. Brembo and Lamborghini executed similar high-specification upgrades, illustrating the tight tolerances electric powertrains demand. The electrification wave therefore amplifies orders for motion-control, machine-vision, and quality-assurance software, lifting the Italy factory automation and industrial controls market above the broader European average.

Expansion of 5G and Fiber Industrial IoT Connectivity

TIM and Vodafone delivered 5G standalone cores to 47 industrial sites in 2025, achieving sub-10-millisecond latency and dedicated network slices for mission-critical traffic.[3]TIM, “5G Industrial IoT Deployments Press Release,” gruppotim.it Danieli synchronized a rolling-mill digital twin at 100 Hz, validating parameter changes virtually before executing them on the line. Open-RAN architectures reduce private-network costs by 40% compared to 2023, expanding eligibility to mid-sized firms. The National Recovery and Resilience Plan allocates EUR 1.2 billion (USD 1.36 billion) to extend 5G and fiber connectivity to 300 industrial parks by 2026, positioning ubiquitous, low-latency connectivity as a near-term accelerator.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Frequent Policy Changes Reducing Investment Visibility | -0.7% | National | Medium term (2-4 years) |

| Persistent Shortage of Automation-Cybersecurity Engineers | -0.6% | National, acute in OT domains | Long term (≥ 4 years) |

| High Up-Front Costs Limiting SME Adoption | -0.8% | National, most severe for firms with above 50 employees | Medium term (2-4 years) |

| EU Data-Residency Rules Restricting Non-EU ICS SaaS | -0.5% | European Union-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Frequent Policy Changes Reduce Investment Visibility

Threshold revisions in 2020-2025, including a sudden energy-saving jump from 0% to 3% in 2024, shortened planning horizons and caused 48% of surveyed firms to defer projects until regulations were finalized. Multi-year software subscriptions appear risky when credit eligibility can be revoked, so buyers prefer discrete hardware with near-term payback. Energy-intensive sectors such as chemicals need 18-24 months to validate process changes, making abrupt rule shifts especially burdensome. Schneider Electric noted a 19% contraction in its pipeline in early 2025, as clients waited for clarity on cloud-hosted analytics. Policy predictability, therefore, remains a drag on the Italy factory automation and industrial controls market.

Persistent Shortage of Automation-Cybersecurity Engineers

NIS2 imposed 24-hour incident reporting and mandatory vulnerability assessments in January 2025; yet, the country graduated only 1,400 operational technology security specialists in 2024, against an annual demand exceeding 3,200. Manufacturers must either delay projects or outsource cybersecurity at costs approaching EUR 150,000 (USD 169,500) per site per year. Honeywell’s Milan apprenticeship program places 80 trainees annually, accounting for less than 1% of the shortfall. Small and medium-sized enterprises lacking dedicated staff often rely on shared-service models, which heighten supply-chain exposure and limit cloud migration, thereby slowing the adoption of advanced analytics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Software and Services Gain Momentum

The industrial control systems segment generated 45.78% of the 2025 revenue, underpinning legacy distributed-control and SCADA footprints across chemicals, power, and oil and gas sites. Industrial software and services, although smaller, are growing at a 7.81% CAGR, the swiftest pace within the Italy factory automation and industrial controls market. CINECA’s allocation of 20% of the Leonardo supercomputer's capacity to manufacturing workloads enabled small and medium-sized enterprises to perform computational fluid dynamics simulations without incurring capital outlay. Subscription-based analytics from Siemens MindSphere and AVEVA PI System achieved ISO 27001 certification in 2025, alleviating concerns under the General Data Protection Regulation.

Software growth also reflects the marginal economics of virtual sensors and digital twins, whose incremental cost approaches zero once the platform exists. Rockwell Automation’s FactoryTalk Design Studio reduces engineering time by 30%, encouraging integrators to transition from perpetual licenses to recurring revenue. Field devices retain steady demand because energy-monitoring mandates lift sensor density per line, yet their growth tracks the overall Italy factory automation and industrial controls market rather than outpacing it. The evolving mix shows value migrating from hardware toward data-rich platforms that improve uptime and regulatory compliance.

By Component: Software Chips Away at Hardware Dominance

Hardware still contributed 56.19% of 2025 sales, but software is rising fastest at a 7.93% CAGR as edge analytics, cybersecurity overlays, and digital twin engines become mandatory under NIS2. ABB Ability subscriptions grew 41% in 2025, with predictive-maintenance modules comprising two-thirds of new contracts. Service revenues are now bundled with software; Emerson’s DeltaV platform includes five-year managed-service contracts covering patching and operator training.

The hardware market is bifurcating. Legacy relay-based controllers face retirement, while high-performance motion controls for robotics and semiconductor tools remain indispensable. Beckhoff EtherCAT controllers have expanded their share to 12% by leveraging a software-centric architecture. Consequently, software pull-through boosts services, anchoring long-term vendor margins within the Italy factory automation and industrial controls market industry.

By Deployment Mode: Cloud and Edge Form a Hybrid Future

On-premises systems accounted for 66.71% of installations in 2025, reflecting a tradition of air-gapped reliability. Cloud deployments, growing at a 7.89% CAGR, benefit from Microsoft and AWS opening GDPR-compliant industrial IoT regions in Milan. However, EU data-residency clauses keep critical loops local, so most manufacturers adopt a hybrid strategy. Schneider Electric EcoStruxure places time-sensitive analytics at the edge, while reserving the cloud for long-term modeling, and wins 18 Italian food and beverage contracts in 2025.

Edge gateways bridge latency and compliance. Siemens Industrial Edge shipped 2,300 units to Italy in 2025, a threefold increase from the prior year, confirming momentum. The Italy factory automation and industrial controls market size for hybrid architectures is projected to eclipse purely on-premises spending by 2029, driven by cost advantages and real-time capabilities.

By End-User Industry: Electronics Growth Outpaces Automotive Maturity

Automotive and transportation remained the largest buyer, with a 29.12% revenue share in 2025, supported by electrification projects from Ferrari, Lamborghini, and Stellantis. Electronics and semiconductor plants are expanding at an 8.77% CAGR, the fastest among verticals, as STMicroelectronics triples 300-millimeter wafer capacity by 2027. Barilla rolled out FactoryTalk software across 14 pasta facilities, demonstrating that food and beverage players are now adopting advanced automation for energy savings.

Traditional process industries, including oil, gas, and chemicals, still account for roughly one-quarter of spending, as predictive maintenance yields significant operational expenditure reductions. Textiles and luxury leather goods are automating cutting and finishing to offset wage inflation, exemplified by Prada’s EUR 35 million (USD 39.6 million) investment in robotic leather cutting. Diversification across verticals broadens the base of the Italy factory automation and industrial controls market and cushions cyclical shocks in any single sector.

Geography Analysis

Northern Italy dominated the Italian factory automation and industrial controls market in 2025, with Lombardy, Emilia-Romagna, Veneto, and Piedmont accounting for approximately 68% of the national manufacturing value added. Lombardy alone accounted for roughly 28% of revenue, buoyed by STMicroelectronics’ Agrate Brianza fab and a dense network of export-oriented small and medium-sized enterprises upgrading to collaborative robots. Emilia-Romagna registered the fastest annual growth at 9.2% as Ferrari, Lamborghini, and pharmaceutical packagers deployed precision motion control and environmental monitoring.

Southern regions accounted for nearly 12% of 2025 revenue but are expanding at a rate faster than the national average. Campania’s aerospace cluster used Transition 5.0 credits and a 10-point regional bonus to automate composite lay-up lines, while Puglia’s offshore-wind suppliers installed Siemens Gamesa robots in Taranto. The regional premium raised southern credit coverage to 55% of eligible spending, accelerating robot density from 78 to 94 units per 10,000 workers between 2023 and 2025.

Veneto leveraged modular automation for seasonal prosecco and furniture demand, adopting Beckhoff magnetic-levitation transport systems that make batch-size-one production economical. Although northern dominance will persist through 2031 thanks to installed bases and supplier ecosystems, fiscal incentives and 5G infrastructure are gradually narrowing the automation intensity gap across Italy.

Regulatory Landscape

Italy's factory automation and industrial controls deployments sit within a layered EU and national compliance stack that tightened in 2025-2026, covering machinery safety, cybersecurity, and eligibility rules for state-backed digitalization incentives. A key timeline anchor for OEMs and users is the shift from the Machinery Directive 2006/42/EC to the EU Machinery Regulation (EU) 2023/1230, which becomes applicable on 20 January 2027. In the run-up, Italy enacted Law No. 36 of 17 March 2026 (European Delegation Law 2025), delegating the Government to issue implementing legislative decrees by 9 October 2026 to align national law with the regulation.

Cybersecurity obligations are also moving toward product and lifecycle requirements for industrial controls and connected field devices. The EU Cyber Resilience Act entered into force in December 2024 and introduces obligations for products with digital elements, including reporting requirements that start from 11 September 2026, reinforcing demand for secure-by-design architectures and patchable, centrally managed control stacks. On the incentives side, the Ministry of Enterprises and Made in Italy (MIMIT) administers Piano Transizione 5.0 via the GSE (Gestore dei Servizi Energetici) portal, with the booking platform operational as of 12 June 2026. It links automation reimbursements to documented energy-performance improvements, placing audit-ready monitoring and reporting at the center of project specifications.

Value Chain Analysis

The Italy factory automation and industrial controls value chain covers (1) component and subsystem suppliers (sensors, drives, motion, PLCs, industrial PCs, networking), (2) software layers (SCADA, MES, historians, analytics, cybersecurity tooling), (3) system integrators and OEM machine builders that engineer and commission turnkey lines, and (4) end users across discrete and process industries that run continuous improvement cycles around energy, quality, and uptime. Trade bodies and ecosystem intermediaries shape demand signals and skills formation, while competence centers and testbeds support validation, training, and pilot-to-scale transitions for SMEs.

In 2026, Italy's ecosystem activity stayed visible through association and industry platforms as well as end-user modernization programs. ANIE Automazione presented its Italian Automation Industry Observatory 2026 during SPS Italia, positioning 2024 as a year of inventory normalization-driven contraction and 2025 as a stabilization year, which affects how distributors, OEMs, and integrators manage lead times and stock policies. SPS Italia 2026 in Parma drew more than 37,500 visitors and 720 exhibitors, underscoring how trade events support supplier discovery, partner formation, and the spread of predictive maintenance and process optimization use cases. On the downstream side, projects such as Marcegaglia's selection of Fives to deploy the Virtuo L digital solution at the Gazoldo degli Ippoliti steel plant show how demand increasingly bundles control upgrades with data collection, thermal process automation, and software layers delivered through multi-vendor delivery teams.

Competitive Landscape

The Italy factory automation and industrial controls market shows moderate concentration. Siemens, ABB, Schneider Electric, Rockwell Automation, and Mitsubishi Electric collectively controlled approximately 42% of the 2025 revenue, leaving 58% to specialized robotics firms, edge software developers, and system integrators. Siemens booked a 22% increase in orders in the first half of 2025 by bundling programmable-logic controllers with pre-certified energy-tracking software. Schneider Electric shortened transition times for ISO 50001 certification by obtaining certification for 18 customer sites, a differentiator that resonated with energy-intensive sectors.

Comau capitalized on its automotive pedigree to win 14 non-automotive contracts in 2025, including turnkey robot cells with five-year maintenance. Startups offering software-defined control that runs on commercial servers erode hardware lock-in, while cybersecurity vendors position secure-boot silicon ahead of the EU Cyber Resilience Act. Ecosystem partnerships are strategic: ABB Ability integrates with Microsoft Azure and SAP S/4HANA, giving clients a seamless path from shop-floor telemetry to enterprise planning.

Price competition is less severe than service competition because buyers value documentation that guarantees tax-credit approval and cybersecurity compliance. Consequently, solution completeness and regulatory fluency are more decisive than component cost in vendor selection within the Italy factory automation and industrial controls market industry.

Italy Factory Automation And Industrial Controls Industry Leaders

ABB Ltd

Siemens AG

Schneider Electric SE

Honeywell International Inc.

Mitsubishi Electric Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity in Italy centers on incentive-aligned retrofits that pair controls modernization with measurable energy savings and auditable baselining. In June 2026, MIMIT opened the booking platform for the Transizione 5.0 incentive scheme via the GSE portal, reserving EUR 9.8 billion for industrial digitization, advanced technology adoption, and renewable energy investments. That mechanism pushes buyers to specify energy metering, edge gateways, and software that can generate documentation supporting credit approval, creating room for vendors and integrators to package PLC and drive upgrades with ISO 50001-ready measurement and verification workflows, especially for SMEs where integration and audit requirements can block adoption.

A second opportunity area comes from targeted SME programs and capability-building infrastructure that broaden adoption beyond northern industrial corridors. In July 2026, the Punti Impresa Digitale (PID) launched the Double Transition Voucher scheme, allocating EUR 150 million over three years to co-fund SME investments in technologies including AI, collaborative robotics, and IoT sensors. This supports demand for standardized, repeatable automation bundles with short deployment cycles. Separately, PNRR Investment 2.3 targets the reorganization of at least 45 technology transfer centers, with financial agreements finalized by Q2 2026, expanding local access to test-before-buy services, skills training, and applied engineering support that helps SMEs move from basic digitization to secure, connected, and energy-accountable automation architectures.

Recent Industry Developments

- July 2026: Marcegaglia selected Fives to deploy the Virtuo L digital solution at its Gazoldo degli Ippoliti steel plant, targeting tighter thermal process control and improved production data collection. The project reinforces the shift in Italian heavy industry toward software-led process optimization layered on top of automation retrofits, with integrators coordinating multi-vendor control and data stacks.

- January 2025: Schneider Electric completed a system migration at Lavazza's manufacturing plant in Settimo Torinese, integrating AVEVA software platforms with Modicon M580 process controllers to improve production efficiency and cybersecurity compliance. The upgrade highlights how Italian manufacturers are pairing modernization of control hardware with standardized software layers to support centralized patching and governance requirements.

- August 2024: ABB concluded its four-year Lighthouse Plant project, investing EUR 9.2 million across ABB sites in Dalmine, Frosinone, and Santa Palomba to advance digital transformation under Piano Transizione 4.0. The program serves as a reference deployment for integrating automation, data systems, and operational improvements within Italian facilities, supporting replication by OEMs and end users pursuing incentive-backed upgrades.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers revenues generated in Italy from factory automation and industrial control solutions used to monitor, control, and automate industrial operations, across hardware, software, and related services.

Scope exclusions: We exclude consumer automation products and non-industrial building automation that is not directly tied to factory or process control use cases.

Segmentation Overview

- By Product

- Industrial Control Systems

- Field Devices

- Industrial Software and Services

- By Component

- Hardware

- Software

- Services

- By Deployment Mode

- On-premises

- Cloud

- Edge

- By End-user Industry

- Oil and Gas

- Chemical and Petrochemical

- Power and Utilities

- Automotive and Transportation

- Textile

- Food and Beverage

- Electronics and Semiconductor

- Other End-user Industries

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to pin down Italy-specific demand signals before interviews began. We referred to public sources such as ISTAT releases, Eurostat industrial production series, trade and customs statistics from UN Comtrade, and manufacturing and automation publications from groups such as the European Commission and relevant industry associations.

We also reviewed company annual reports, investor decks, product catalogs, and reputable press to understand pricing direction, channel structure, and typical deployment patterns across Italian manufacturing. In addition, a few paid subscriptions for company financials, patent lookups, and shipment-level trade checks were used to cross-check company exposure and import intensity for selected automation components. These desk research sources are illustrative only, and many other public references were consulted to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary interviews and short surveys were completed with Italy-focused stakeholders across automation hardware, software, services, and distribution, as well as with end users that run discrete and process operations. To keep assumptions realistic, we tested adoption, refresh cycles, typical project sizing, and the split between new installations and retrofits across major industrial clusters, and then we re-checked unclear points with follow-up outreach.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 16% | |

| Mid tier: 42% | Functional/Unit leaders: 24% | |

| Smaller Players: 21% | Managers: 60% |

Market-Sizing & Forecasting

Sizing starts from a top-down reconstruction of Italy demand using industrial activity signals and automation spend intensity, and then the totals are shaped to match what is actually deployed in plants. In practice, we mapped manufacturing output trends and capex appetite into automation categories, and then adjusted for solution mix shifts that were confirmed through interviews.

Key model inputs included Italy manufacturing production momentum, machinery investment cycles, retrofit versus greenfield project share, average solution pricing movement across hardware and software, and the pace of edge and cloud deployments in industrial settings. Since not every sub-category has clean public data, selective bottom-up approximations were used as a check, such as supplier revenue exposure to Italy, sampled pricing times estimated shipment or install volumes, and distributor channel checks for fast-moving product groups, followed by gap-filling using conservative ratios validated by interviewees.

For forecasting, scenario analysis was used because energy costs, incentive timing, and export-driven production cycles can change purchasing plans quickly. The scenarios were anchored to expert views on project pipelines and budgeting, and then translated into yearly trajectories for hardware, software, and services so the forecast stays explainable and repeatable.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the final market value does not rely on a single indicator. We compared modeled results against independent signals such as production trends, trade intensity for automation components, and stated investment priorities, and then reviewed any large variances at category level before sign-off.

If a number looked off, the drivers behind it were traced back to the specific assumption, and respondents were re-contacted when the change could materially shift the estimate. Reports are refreshed annually, and interim updates are made when major events change the outlook. Before delivery, a final analyst pass is completed so clients receive the most current view that can be supported by the documented inputs.

Mordor Intelligence's Italy Factory Automation and Industrial Controls Market Size Versus Other Published Estimates

Published market values for this space often differ because the scope can shift between a narrow factory-floor view and a broader industrial automation umbrella, and because year labeling and currency timing are not always handled the same way. Differences also show up when one estimate treats software and services as a small add-on, but another counts them as a large recurring revenue pool.

Some external figures roll factory automation together with wider industrial automation and process control coverage, which can pull in extra categories that are not always purchased by discrete manufacturers. For Mordor Intelligence, the estimate is limited to factory automation and industrial controls revenues in Italy that align to the report scope (industrial control systems, field devices, and industrial software and services), and it is presented on the same forecast base year so comparisons do not mix different time windows.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.92 B (2026) | |

| Industry Research Group A | USD 2.42 B (2023) | Uses a different base year and presents incremental growth framing over 2023-2028, which can understate the later-year level when compared to a 2026 starting point. The scope summary also emphasizes industrial control systems and field devices, which can compress totals if industrial software and services are treated lightly. |

| Data Publisher B | USD 5.20 B (2024) | Covers a wider industrial automation basket that can include process automation and other adjacent solutions beyond factory automation and industrial controls, which inflates the addressable revenue pool. Higher growth assumptions can also result if category definitions include broader system and solution layers. |

The comparison mainly shows two drivers behind the spread, the year being compared and how wide the automation basket is defined. By keeping the category scope consistent and then checking the model with practical demand signals and interview feedback, the final number stays traceable to clear inputs and can be re-run when conditions change.

Key Questions Answered in the Report

How large is the Italy factory automation and industrial control systems market today?

The Italy factory automation and industrial control systems market size reached USD 3.92 billion in 2026 and is forecast to climb to USD 5.57 billion by 2031.

What growth rate is expected through 2031?

The market is projected to register a 7.28% CAGR from 2026 to 2031, led by tax-credit incentives and automotive electrification projects.

Which product category is expanding fastest?

Industrial software and services are growing at a 7.81% CAGR, outpacing hardware and field devices as firms shift to subscription-based analytics.

Which Italian region is seeing the quickest adoption?

Emilia-Romagna posted a 9.2% year-on-year increase in 2025 automation spending, the highest regional growth rate, thanks to automotive and packaging clusters.

What restrains wider SME adoption?

High up-front integration and energy-audit costs, often exceeding EUR 50,000, deter about 40% of small and medium-sized enterprises despite available tax credits.

Who are the leading vendors?

Siemens, ABB, Schneider Electric, Rockwell Automation, and Mitsubishi Electric together controlled about 42% of 2025 revenue, indicating moderate concentration.

Page last updated on: