India Foundry Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

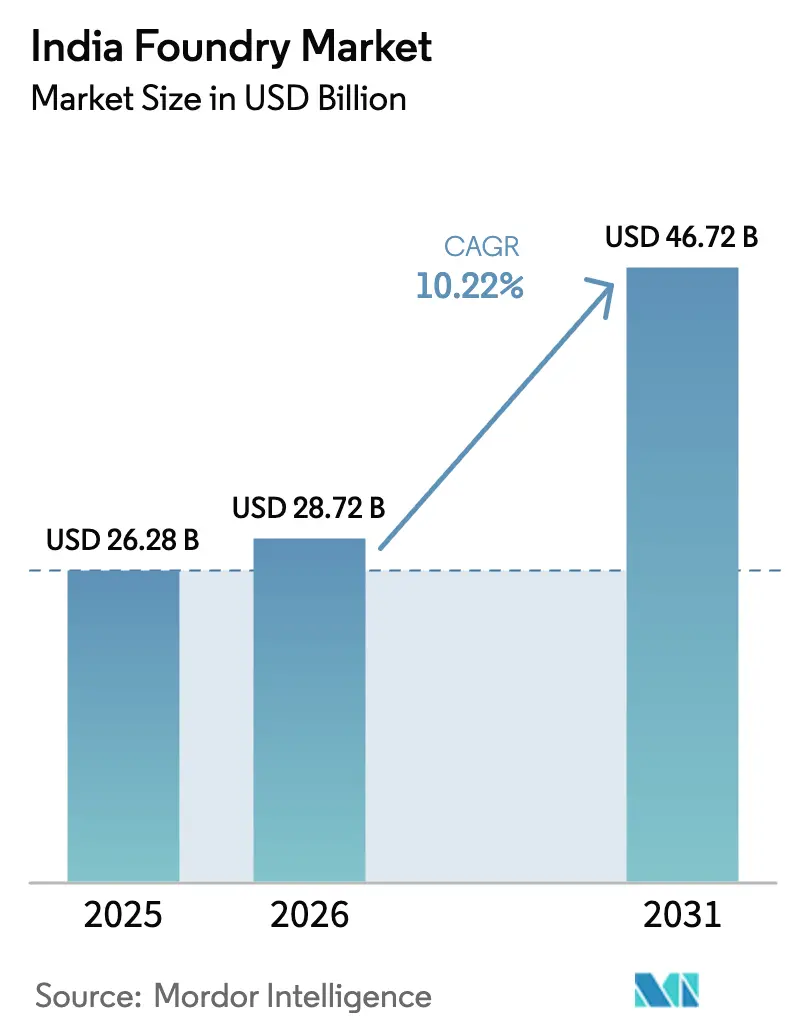

| Base Year Market Size (2025) | USD 26.28 Billion |

| Market Size (2026) | USD 28.72 Billion |

| Market Size (2031) | USD 46.72 Billion |

| Growth Rate (2026 - 2031) | 10.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Foundry Market Analysis by Mordor Intelligence

The India Foundry Market size is projected to be USD 26.28 billion in 2025, USD 28.72 billion in 2026, and reach USD 46.72 billion by 2031, growing at a CAGR of 10.22% from 2026 to 2031.

Supported by import-substitution duties, electric-vehicle (EV) localization, and public-works spending, the India foundry market has moved from spot contracting toward long-term programs that reward metallurgical consistency and lower embedded carbon. Aluminum high-pressure die-casting (HPDC) lines are running close to capacity as domestic EV production passed 1 million units in fiscal 2026, while the Vehicle Scrappage Policy is unlocking low-cost scrap that trims melt costs by 12–18%. Safeguard duties of 40% on Chinese iron castings have redirected orders to domestic shops and compressed lead times, and green-hydrogen subsidies are nudging early adopters to convert coke-fired cupolas to low-carbon furnaces. Together, these levers have allowed most Tier 1 suppliers to maintain pricing power even as scrap and energy prices remain volatile.

Key Report Takeaways

- By casting type, sand casting accounted for 58.82% of the India foundry market share in 2025, whereas investment casting is projected to expand at a 12.05% CAGR through 2031.

- By material, ferrous alloys held 84% of the India foundry market size in 2025, but non-ferrous alloys are set to grow at an 11.54% CAGR to 2031.

- By end-user, automotive applications contributed 31.88% of 2025 revenue, while aerospace components will post the fastest 12.06% CAGR through 2031.

- By geography, West India led with 35.11% of 2025 revenue, whereas South India is on track for a 10.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Foundry Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic EV output passing 1 million units in FY-26 boosts aluminum HPDC demand | +1.8% | West & South India | Medium term (2–4 years) |

| 40% duty on Chinese iron castings accelerates import substitution | +1.5% | National | Short term (≤ 2 years) |

| Vehicle Scrappage Policy delivers cheaper ferrous and non-ferrous scrap | +1.2% | National | Short term (≤ 2 years) |

| Global OEM Scope-3 mandates drive EAF/induction investment | +1.0% | National | Medium term (2–4 years) |

| Green-hydrogen subsidies support furnace conversion in select clusters | +0.8% | West, South & East India | Long term (≥ 4 years) |

| ONDC B2B metals marketplace cuts raw-material costs for SMEs | +0.5% | National | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Domestic EV Output Passing 1 Million Units in FY-26 Boosts Aluminum HPDC Demand

EV power-train localization is diverting HPDC lines from engine ancillaries to battery enclosures, motor housings, and structural frames that demand tighter tolerances and higher thermal conductivity. Hindalco’s USD 59 million Chakan plant shipped 10,000 battery enclosures to Mahindra Electric by December 2024 and is scaling to 160,000 units a year by FY-2027. Uno Minda is commissioning a USD 25 million HPDC facility in Maharashtra with 3,629 t annual capacity aimed at Tata’s Nexon EV and Mahindra’s XUV400 platforms. India’s production-linked incentive for advanced-chemistry cells compels 60% domestic value-addition by 2027, further anchoring HPDC orders in Pune, Chakan, and Hosur clusters. Although flame-retardant coatings add 8–12% processing cost, they unlock premium contracts with Ola Electric and Ather Energy, lifting average selling prices on enclosure castings.

40% Duty on Chinese Iron Castings Accelerates Import Substitution

A 40% basic customs duty, effective January 2025, has slashed ordering cycles from 90–120 days to 30–45 days. Mahindra & Mahindra and Tata Motors have shifted 12,000 t of housing from China to Kirloskar Ferrous and Electrosteel. Bharat Forge’s Baramati EV-component plant uses AI mold-fill tools to keep rejections below 1%, enabling same-week deliveries. Construction-equipment OEMs, buoyed by a future production incentive, are localizing hydraulic-cylinder barrels and boom castings. Unless plants reach Chinese productivity by the duty’s scheduled 2028 expiry, import risk will resurface, but digital-twin roll-outs under the SAMARTH Udyog Bharat 4.0 program are closing the gap.

Vehicle Scrappage Policy Delivers Cheaper Ferrous and Non-Ferrous Scrap

The Vehicle Scrappage Policy had 84 scrapping facilities processing 96,980 vehicles by July 2024[1]Press Information Bureau, “Vehicle Scrappage Policy: 84 RVSFs Operational, 96,980 Vehicles Scrapped by July 2024,” pib.gov.in. Scrap flows are lifting the scrap ratio in induction furnaces to as high as 70%, slicing pig-iron purchases and trimming energy intensity. Tata Steel and JSW Steel plants now run dedicated scrap-sorting lines, offering foundries cleaner feed that reduces gray-iron costs by USD 40–60 per t. The policy’s fitness-certificate mandate could retire 1.2 million vehicles a year by 2028, generating 2.8 million t of ferrous scrap enough to cover 15–20% of national melt requirements. Margins widen as melt costs fall, letting foundries underbid imports without eroding profitability.

Green-Hydrogen Subsidies Support Furnace Conversion in Select Clusters

The National Green Hydrogen Mission budgets USD 2.35 billion to 2030 for direct-reduced iron and hydrogen furnaces[2]Ministry of New and Renewable Energy, “National Green Hydrogen Mission,” mnre.gov.in. Kolhapur’s cupola-heavy basin is piloting hydrogen-oxy burners that can slash particulate emissions by 85% and sulfur dioxide to near zero. Tata Steel is testing a 5 MW electrolyzer feeding a 50 t-per-day DRI module, with learnings aimed at its captive foundry. Conversion economics hinge on hydrogen prices falling from today’s USD 4.5 per kg to the mission’s USD 1.2 per kg target, but early adopters could comply with the European Carbon Border Adjustment Mechanism (CBAM) well ahead of peers.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU CBAM raises landed cost of high-carbon castings | -1.4% | Export-oriented clusters | Short term (≤ 2 years) |

| Petcoke and high-sulfur coal import curbs inflate melt-fuel costs | -0.9% | West, East & Central India | Short term (≤ 2 years) |

| Semiconductor-fab hiring drains metallurgical engineers | -0.6% | West & South India | Medium term (2–4 years) |

| Shift to glass-reinforced plastics in micro-mobility reduces small-part demand | -0.4% | West & South India | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

EU CBAM Raises Landed Cost of High-Carbon Castings

The CBAM applies a 38.8% levy on castings above 1.5 t CO₂ per t from January 2026. Kolhapur’s exporters, emitting 1.8–2.2 t CO₂ per t, face immediate margin compression. Larger players absorb compliance costs, yet 70% of shops are MSMEs with limited capital. At least 8–12 micro-foundries have shut each quarter since mid-2025, accelerating consolidation as buyers shift to CBAM-compliant suppliers.

Import Curbs on Petcoke and High-Sulfur Coal Inflate Melt-Fuel Costs

India slashed the January–June 2025 coke import quota to 1.43 million t and cut the sulfur cap to 1.5%, driving delivered prices from about USD 360 per t to nearly USD 480 per t. Melt-fuel bills for coke-fired cupolas rose roughly 25%, squeezing margins by 4–6 points and forcing a dozen Kolhapur micro-foundries to shut. Without cheaper energy alternatives, the next quota cut slated for 2027 could trigger wider closures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Casting Type: Investment Casting Lifts Precision Output

Investment casting captured 600 t of aerospace-grade capacity in 2025 and is set for a 12.05% CAGR, outperforming every other route in the India foundry market. Sand casting, however, remained the largest at 58.82% of 2025 volume. HAL’s USD 21.4 billion order book for 201 Tejas Mk 2 jets is driving turbine-blade contracts for PTC Industries, Dynamatic Technologies, and Aequs.[3]Defence R&D Organisation, “Monograph on Investment Casting for Aero-Engine Applications,” drdo.gov.in Investment-cast superalloys such as Inconel 718 deliver 950–1,200 MPa tensile strength and can tolerate 1,050 °C gas-path temperatures, attributes that are impossible via sand molds. Although tools and waxing stages inflate part costs to USD 10 per kg, OEMs accept premiums for tight tolerance and fatigue life.

Sand casting still underpins the India foundry market size for automotive cylinder blocks, railway couplers, and pump housings. Kolhapur and Pune alone ship about 600,000 t of sand-cast iron parts annually. Die casting, led by Uno Minda’s upcoming Maharashtra unit, is pivoting to EV motor housings and battery frames at cycle times of 45 seconds. Permanent-mold, evaporative-pattern, and centrifugal casting form a small share, serving pistons, crankshafts, and ductile-iron pipes. Even with investment casting’s fast growth, sand casting will likely keep more than half of India's foundry market share through 2031 because large diesel engines and rail bogies will stay iron-intensive.

By Material: Non-Ferrous Alloys Gain Traction

Ferrous grades held 84% of 2025 revenue, but aluminum, zinc, and copper castings will log an 11.54% CAGR to 2031 on EV lightweighting mandates. Hindalco’s HPDC line achieved a 40% battery-enclosure weight cut versus steel, improving range by 15 km. Pune’s aluminum cluster, which accounts for more than 20% of national non-ferrous output, benefits from pipeline natural gas and ONDC sourcing that shave 5–7% off ingot costs. Despite growth, non-ferrous alloys still track London Metal Exchange swings; at USD 2,600 per t, aluminum costs roughly quadruple pig iron, squeezing margins when contracts lack metal pass-through clauses.

Gray and ductile irons keep leadership on cost-sensitive, high-fatigue parts such as railway couplers and wind-turbine hubs. Nelcast’s Chennai expansion added 60,000 t a year and uses 100% renewable power, achieving 0.8 t CO₂ per t, well below the CBAM threshold. As EV penetration rises, aluminum and magnesium usage per vehicle will climb, yet iron content in heavy-machinery frames, couplers, and brake discs will remain sticky, ensuring ferrous dominance in India's foundry market share for at least the next five years.

By End-User: Aerospace Outpaces Automotive Growth

Automotive uses still generated 31.88% of 2025 demand, but content per car is falling as internal-combustion engines give way to simpler EV drivetrains. By contrast, aerospace castings, now under 10% of shipments, will post a 12.06% CAGR as HAL ramps Tejas jets from 16 to 24 units a year and Air India’s 470-aircraft order feeds aftermarket blade replacements. Precision-cast nickel alloys carry double-digit margins and longer contracts, insulating suppliers such as PTC Industries from auto-cycle volatility.

Construction equipment, railways, pumps, and electrical components together account for the remainder. Hydraulic-cylinder barrels for excavators, railway bogie frames for Vande Bharat trainsets, and ductile-iron pump housings for water grids maintain steady tonnage. These bulkier parts favor sand or static molds, reinforcing ferrous tonnage even as premium investment-cast alloys take value share.

Geography Analysis

West India retained 35.11% of 2025 revenue as Kolhapur’s 275 iron foundries and Pune’s 50-unit aluminum cluster together poured over 1 million t. Proximity to Tata Motors, Mahindra & Mahindra, and Bajaj Auto keeps shipping distances short, while state subsidies on natural gas curb melt costs for non-ferrous shops. Bharat Forge’s USD 47 million Chakan forging-casting campus and Mahindra CIE’s USD 59 million Igatpuri die-casting plant will add almost 60,000 t of aluminum capacity by 2027, lifting the region’s share of non-ferrous tonnage toward 46%.

South India is the fastest-growing region at a projected 10.74% CAGR through 2031 thanks to aerospace and wind-energy work in Tamil Nadu and Karnataka. Nelcast’s 60,000 t ductile-iron facility in Chennai, powered entirely by renewables, already meets CBAM limits and feeds Vestas and Siemens Gamesa hubs. Sundaram Clayton’s 18,000 t die-casting expansion and Brakes India’s 12,000 t brake-caliper line deepen automotive supply to Hyundai and Renault-Nissan export programs. Coimbatore’s investment-casting shops link directly into HAL’s turbine-blade supply chain, securing multi-year orders that smooth cyclicality.

North, East & North-East, and Central India trail in share but leverage captive steel-plant foundries and railway demand. Tata Steel’s Jamshedpur and JSW Steel’s Dolvi sites pour large crankcases and couplers for Indian Railways and Bharat Heavy Electricals. The USD 2.27 billion Delhi–Panipat RRTS corridor and metro works in Kolkata and Guwahati are pulling ductile-iron pipe and brake-disc orders eastward, while coal-rich Raipur–Bhilai maintains a cost advantage on feedstock for construction-equipment castings.

Competitive Landscape

Roughly 5,000 units compete nationwide, but the top 20 groups control 35–40% of revenue, giving the India foundry market a moderate concentration. Integrated players are co-locating forging, machining, and casting on single campuses to shorten lead times. Bharat Forge operates 716,500 t of capacity across five countries, including 77,700 t of iron casting via JS Auto Cast, and uses AI vision to cap defects below 1%. Mahindra CIE’s Phase I Igatpuri facility introduced digital twins that cut cycle time to 45 seconds, winning aluminum motor-housing orders from European EV platforms.

The second cohort, including Endurance Technologies, Sundaram Clayton, and Nelcast, specializes in high-pressure die casting or ductile-iron hubs. Their edge lies in renewable power procurement and first-mover CBAM compliance. Nelcast’s Chennai plant, for example, runs on 100% wind and solar, earning preferred-supplier status through 2028 for Suzlon and Vestas. Such decarbonization narratives are now essential for export quotes, and several MSMEs face exclusion for lacking ISO 14067 footprints.

Technology adoption remains the key strategic variable. IoT sensors, machine-learning defect prediction, and blockchain carbon ledgers cost upward of USD 0.5 million per line, a sum prohibitive for MSMEs. The ONDC metals marketplace offers one lever of relief by lowering raw material prices, but most micro shops still struggle to fund automation. As duties phase out and CBAM ramps up, consolidation is expected to accelerate, with the largest groups eyeing tuck-in acquisitions in Pune, Kolhapur, and Coimbatore clusters.

India Foundry Industry Leaders

A-Cast Foundry

Aditya Birla Management Corp.

Brakes India

Larsen & Toubro

JSW Steel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Bharat Forge opened a USD 47 million aluminum forging plant in Chakan, Maharashtra, with 36,000 t capacity, powered entirely by renewables.

- October 2024: JSW Steel commissioned a USD 574 million pellet plant in Odisha, adding 12 million t to in-house feedstock.

- September 2024: Bharat Forge launched a USD 18 million R&D center in Pune focusing on aluminum-lithium alloys and additive manufacturing.

- August 2024: JSW Steel activated a second 12 million t pellet line at Meramandali for captive and merchant supply.

India Foundry Market Report Scope

A foundry is a factory where castings are produced by melting the metal, pouring the liquid into a mold, and allowing it to cool and solidify into the desired shape. Foundries are one of the most significant contributors to the manufacturing recycling movement, melting and recasting millions of tons of scrap metal every year to create new, durable products. Moreover, many foundries use sand in their molding process. These foundries often use, recondition, and reuse sand, which is another form of recycling.

The India foundry market is segmented by Material (Ferrous and Non-Ferrous), by End-User (Automotive, Aerospace, Construction, Machinery, and Other End-Users) and by Type (Sand Casting, Investment Casting, Die Casting, and Other Types).

The India foundry market report offers the market size and forecast value in (USD) for all the above segments.

| Sand Casting |

| Die Casting |

| Investment Casting |

| Other Types - Permanent-Mold Casting, Evaporative casting, High-Pressure Die Casting, and Centrifugal |

| Ferrous |

| Non-Ferrous |

| Automotive |

| Aerospace |

| Construction |

| Machinery |

| Railways |

| Power Generation |

| Pumps & Valves |

| Electrical Components |

| Others - General Engineering, etc. |

| North India |

| West India |

| South India |

| East & North-East India |

| Central India |

| By Casting Type | Sand Casting |

| Die Casting | |

| Investment Casting | |

| Other Types - Permanent-Mold Casting, Evaporative casting, High-Pressure Die Casting, and Centrifugal | |

| By Material | Ferrous |

| Non-Ferrous | |

| By End-User | Automotive |

| Aerospace | |

| Construction | |

| Machinery | |

| Railways | |

| Power Generation | |

| Pumps & Valves | |

| Electrical Components | |

| Others - General Engineering, etc. | |

| By Geography | North India |

| West India | |

| South India | |

| East & North-East India | |

| Central India |

Key Questions Answered in the Report

How large is the India foundry market in 2026?

The market reached USD 28.72 billion in 2026 and is projected to grow at a 10.22% CAGR to USD 46.72 billion by 2031.

Which casting route holds the biggest share today?

Sand casting retained 58.82% of 2025 production, mainly supplying automotive engines and railway couplers.

What is driving aluminum casting demand?

Localization of electric-vehicle battery enclosures and motor housings, plus import duties on Chinese castings, are lifting aluminum HPDC orders.

Which region is growing the fastest?

South India is expected to post a 10.74% CAGR, supported by aerospace precision casting and wind-energy hubs.

How will CBAM affect exporters?

Castings above 1.5 t CO? per t incur a 38.8% levy from 2026, pressuring coke-fired cupola shops to shift to electric or hydrogen routes.

What technology investments are most common?

Foundries are adopting AI mold-fill simulation, IoT defect detection, and blockchain carbon tracking to meet global OEM Scope-3 targets.

Page last updated on: