Engineering Services Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

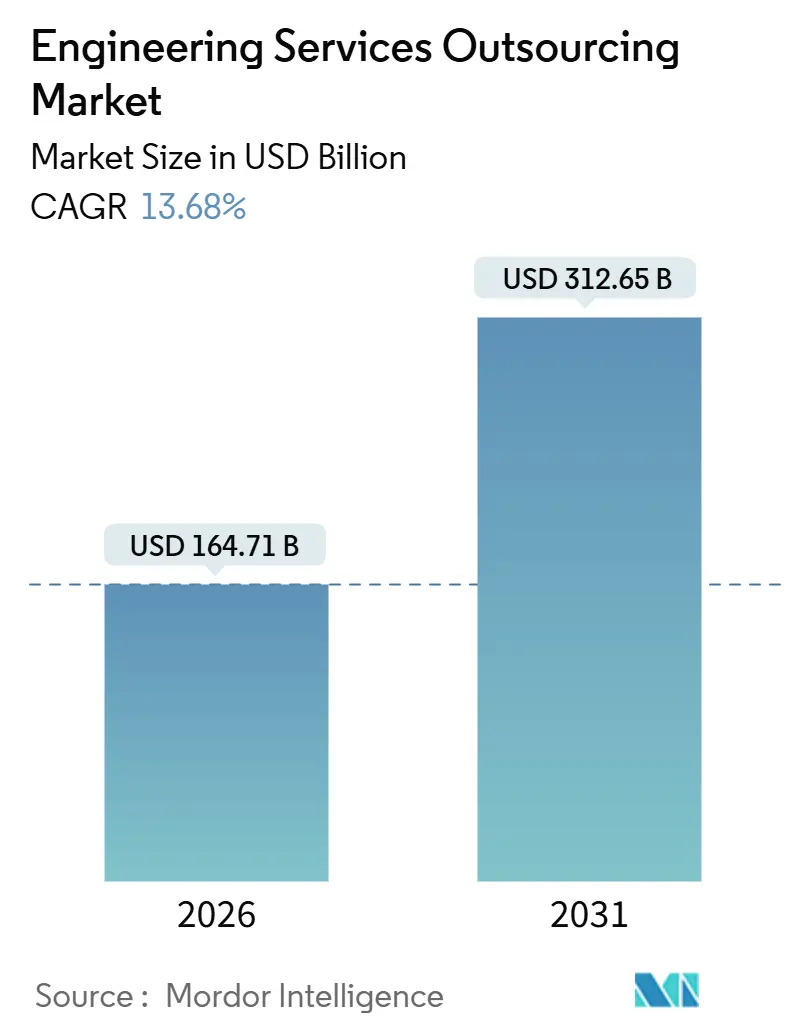

| Market Size (2026) | USD 164.71 Billion |

| Market Size (2031) | USD 312.65 Billion |

| Growth Rate (2026 - 2031) | 13.68% CAGR |

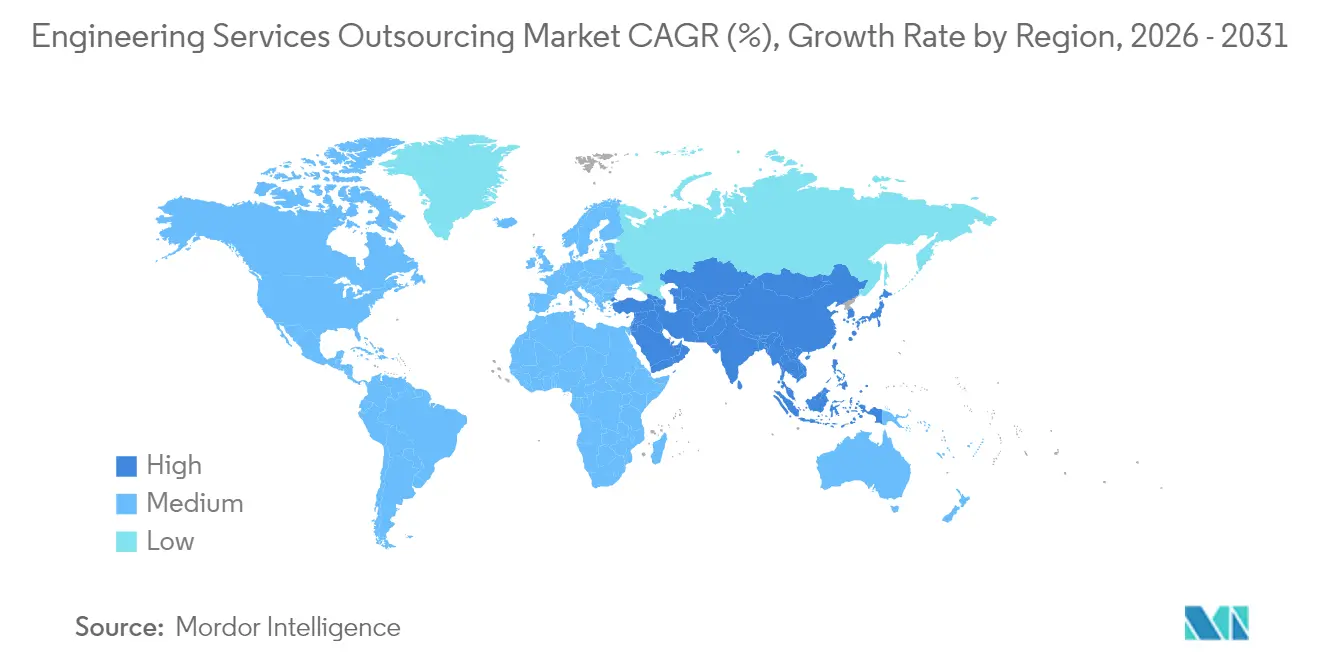

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Engineering Services Outsourcing Market Analysis by Mordor Intelligence

The Engineering Services Outsourcing Market size is estimated at USD 164.71 billion in 2026, and is expected to reach USD 312.65 billion by 2031, at a CAGR of 13.68% during the forecast period (2026-2031). Software-defined product road maps are shortening design cycles, geopolitical tensions are rerouting work to balanced delivery footprints, and AI-augmented computer-aided engineering is compressing validation timeframes. Providers now function as strategic R&D extensions rather than tactical cost centers, a shift that redefines pricing models, contract scopes, and vendor selection criteria. Capital expenditure controls at original-equipment manufacturers (OEMs) reinforce outsourcing uptake, while domain-specific talent shortages raise demand for partners that meld software skills with deep engineering know-how. These converging forces collectively sustain double-digit growth across the engineering services outsourcing market.

Key Report Takeaways

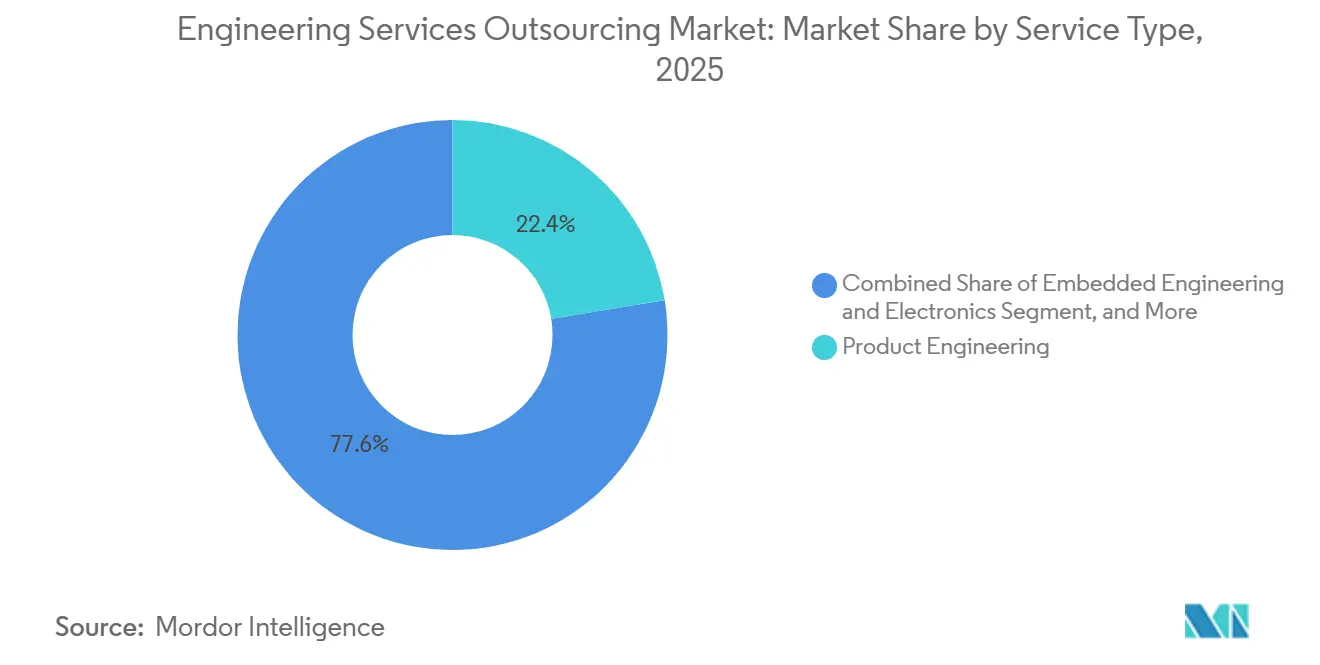

- By service type, Product Engineering commanded 29.02% of the engineering services outsourcing market share in 2025, whereas Digital Engineering and Software is advancing at a brisk 14.35% CAGR through 2031.

- By end user, Automotive and Transportation led with 28.55% revenue share in 2025; Aerospace and Defense is forecast to expand at a 13.12% CAGR to 2031.

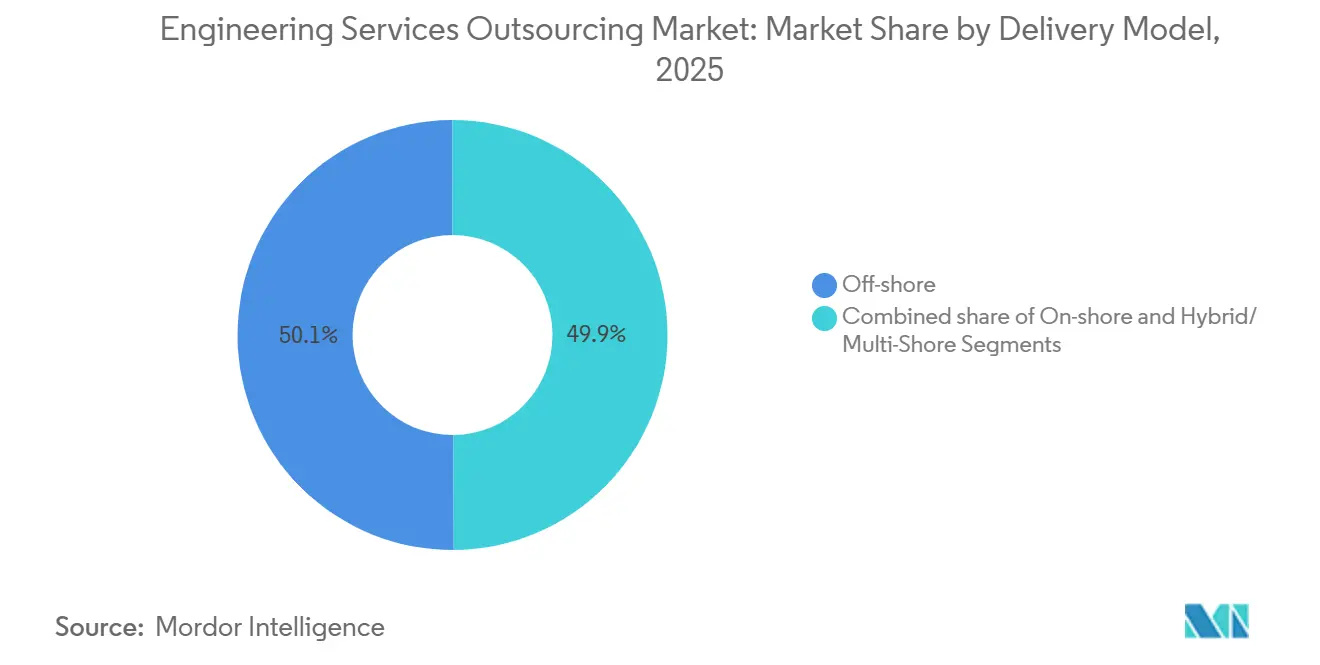

- By delivery model, offshore hubs retained a 69.85% share of the engineering services outsourcing market size in 2025, while near-shore models are slated to grow at a 13.98% CAGR over the same horizon.

- By client size, large enterprises accounted for 59.78% of the engineering services outsourcing market size in 2025; small and mid-sized enterprises are on track for a 12.92% CAGR through 2031.

- By geography, Asia-Pacific dominated at 41.92% in 2025, yet the Middle East and Africa region is accelerating at a 15.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Engineering Services Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acceleration of software-defined product road maps | +3.2% | North America, Europe, global spillover | Medium term (2-4 years) |

| Rising cost pressure on OEM R&D budgets | +2.8% | APAC hubs, global | Short term (≤ 2 years) |

| Near-shoring demand amid geopolitical risk diversification | +2.1% | North America, EU, Mexico, Eastern Europe | Medium term (2-4 years) |

| Talent shortages in advanced engineering domains | +1.9% | North America, Western Europe, global | Long term (≥ 4 years) |

| AI-augmented CAE and digital twin adoption | +1.7% | Global early adopters | Long term (≥ 4 years) |

| Sustainability-driven re-engineering of legacy products | +1.2% | Europe, North America, and expanding APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acceleration of Software-Defined Product Road Maps

OEMs shifting to software-centric architectures now channel as much as 40% of R&D budgets toward code development, creating sustained workloads for embedded systems, connectivity stacks, and cybersecurity validation. Continuous over-the-air update models require partnering with firms that can maintain digital twins and deliver agile releases throughout operating lifecycles. The heightened integration of mechanical, electronic, and software layers raises complexity beyond many in-house teams, elevating demand for full-stack engineering partners that bridge vehicle-to-everything protocols with legacy drivetrain design.

Rising Cost Pressure on OEM R&D Budgets

Economic volatility and supply-chain shocks press manufacturers to convert fixed engineering headcount into variable project-based spending. Outsourcing cushions CAPEX swings by offering elastic capacity and specialized skills for domains such as additive-manufacturing optimization or IoT sensor validation. Semiconductor leaders illustrate the trend by reallocating FPGA front-end design and embedded firmware tasks to external partners that already possess certified toolchains and seasoned staff. Consolidation among service vendors also accelerates as buyers streamline rosters toward fewer, multi-disciplinary suppliers capable of turnkey delivery.

Near-Shoring Demand amid Geopolitical Risk Diversification

Legislation such as the CHIPS and Science Act incentivizes domestic design while data-sovereignty rules limit cross-border transfer of sensitive files. Providers in Mexico, Poland, and Vietnam capitalize on proximity, language alignment, and aligned legal frameworks to secure projects once shipped to distant offshore centers. Initiatives like Accenture’s sovereign-cloud engineering services demonstrate how localized delivery coupled with cloud-native security satisfies national requirements without sacrificing collaboration efficiency.

Talent Shortages in Advanced Engineering Domains

Global deficits in areas like AI-augmented simulation, neuromorphic chip design, and secure edge computing boost bill rates for niche specialists. Engineering service providers respond with university partnerships, upskilling curricula, and internal AI-assisted design pipelines that multiply output per engineer. Scarcity premiums lift overall pricing power and reinforce the engineering services outsourcing market’s value-creation narrative rather than pure labor arbitrage[1]National Science Foundation, “Engineering Workforce Statistics 2025,” nsf.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IP and data-sovereignty concerns | -2.3% | Global, acute in defense and telecom | Short term (≤ 2 years) |

| Fragmented standards across industries | -1.8% | Variable by vertical | Medium term (2-4 years) |

| Wage inflation in traditional offshore hubs | -1.5% | India, Philippines, APAC core | Short term (≤ 2 years) |

| High switching costs for long-term engineering programs | -1.2% | Aerospace, automotive | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IP and Data-Sovereignty Concerns

Defense, telecom, and healthcare OEMs must keep sensitive design artifacts within compliant jurisdictions, narrowing vendor pools and extending procurement cycles. Regulations like ITAR restrict aerospace projects to approved domestic providers, trimming the accessible pie for cost-efficient offshore shops. Service partners invest in zero-trust collaboration platforms and blockchain-enabled audit trails, yet national policies still slow cross-border scaling, keeping certain high-value segments insular[2]United States Department of Defense, “ITAR Compliance Requirements for Technical Data,” defense.gov.

Fragmented Standards across Industries

Divergent frameworks, ISO 26262 for automotive functional safety versus DO-178C for avionics software, force service firms to maintain multiple certification tracks and tools, eroding economies of scale. As software content rises, new cyber-safety norms overlay onto mechanical rules, compounding complexity. Limited harmonization means providers can rarely cross-utilize resources seamlessly between sectors, dampening margin leverage even amid rising demand[3]European Commission, “Proposal to Revise the Machinery Directive,” europa.eu.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Engineering Champions Platform Transformation

Digital Engineering and Software generated the fastest trajectory with a 29.97% CAGR, propelled by electric-vehicle operating systems, industrial IoT stacks, and cloud-native product life-cycle management rollouts. Providers embed DevOps pipelines, model-based systems engineering, and containerized microservices that allow continuous feature releases across multi-domain products. Product Engineering maintained its dominance at 22.42% of 2025 revenue in the engineering services outsourcing market, underpinning core mechanical design, structural analysis, and materials engineering, which remain indispensable across industries. Upskilling efforts now blend AI-augmented finite-element analysis with traditional CAD workflows, accelerating iteration cycles. Embedded Engineering and Electronics grows as edge AI chips proliferate; Verification, Validation, and Compliance services expand in response to autonomy regulations. Sustenance and Value Engineering gain relevance as circular-economy mandates spur redesigns aimed at material efficiency. Collectively, providers are evolving toward integrated platforms rather than siloed offerings, enabling clients to orchestrate ideation-to-launch under a single governance structure.

The engineering services outsourcing market rewards firms that deliver modular service bundles aligned to agile sprints, allowing OEMs to consume discrete digital assets on demand. Digital twin libraries shorten prototype loops, while automated test rigs lower human error in compliance validation. Cloud-native prototyping trims capital investment for physical labs, shifting cost focus from hardware to simulation accuracy. System Integration offerings increasingly include cyber-resilient architectures to safeguard connected assets. As a result, service-type silos blur, positioning full-stack partners for cross-selling at scale.

By End User: Aerospace and Defense Drives Premium Growth

The engineering services outsourcing market share for Automotive and Transportation was 18.67% in 2025, with a 19.79% CAGR, bolstered by electrification, battery-thermal models, and autonomous driving algorithms. The complexity of software-defined vehicles, along with regulations such as UNECE R-155 on cybersecurity, compels OEMs to rely on external specialists to orchestrate hardware-software convergence.

Aerospace and Defense, fleets modernize with composite materials, hydrogen propulsion studies, and next-generation avionics. Defense primes re-channel engineering spend toward resilient satellite communications and unmanned aerial systems, segments that demand certified supply chains and secure data environments. Industrial Equipment clients leverage digital twins for predictive maintenance, whereas Consumer Electronics players outsource commodity mechanical tasks to free in-house teams to focus on user-interface differentiation. Semiconductor firms, facing chronic analog-design shortages, outbid other industries for niche expertise, inflating rates in that micro-segment.

Energy and Utilities customers engage service partners for grid-optimization analytics and renewable-integration models, while Oil and Gas firms emulate downstream asset-integrity programs pioneered in chemicals. Medical Device makers, contending with ISO 13485 and FDA 21 CFR Part 820 audits, outsource design-for-manufacturing and human-factor testing to reduce non-conformance risk. Telecom and Networking clients require 5G O-RAN interoperability and edge-cloud orchestration, areas where cross-disciplinary teams span RF, software, and security competencies. The diversified demand profile sustains robust growth across verticals, even as each vertical applies unique compliance gates that shape provider qualification strategies.

By Delivery Model: Near-Shore Gains Strategic Importance

Offshore hubs still anchored 34.10% of 2025 revenue in the engineering services outsourcing market, reflecting decades-long talent pipelines in India and Eastern Europe. The engineering services outsourcing market continues to exploit currency differentials and mature process frameworks in these regions. Yet near-shore locations are advancing at 43.95% CAGR through 2031 as geopolitics, time-zone overlap, and data-location statutes converge to redefine proximity benefits.

Hybrid models emerge in which providers split sensitive firmware tasks between compliant onshore centers and offshore centers for non-classified simulation workloads. Outcome-based contracts diminish the centrality of hourly labor costs, enabling near-shore teams to compete on innovation velocity and domain familiarity. Enhanced collaboration tools narrow distance frictions, but compliance regimes keep certain workloads fenced within prescribed jurisdictions, cementing regional centers’ roles.

Time-zone alignment optimizes agile cadence by allowing daily stand-ups without nocturnal shifts. Linguistic and cultural affinity improves design-review clarity, reducing rework. Providers in Poland, Portugal, and Mexico gain traction by coupling European or North American language fluency with STEM graduates versed in modern toolchains. Automation parity means wage inflation in traditional offshore hubs narrows cost gaps versus near-shore peers, further equalizing economics. As a result, delivery-model selection becomes a portfolio decision balancing cost, compliance, and collaborative efficiency rather than a singular focus on rate arbitrage.

By Client Size: SMEs Embrace Democratized Engineering

Large enterprises accounted for 77.48% of the engineering services outsourcing market in 2025, recording a 71.82% CAGR to 2031. They leverage mature vendor-management offices, multi-year master service agreements, and co-innovation labs that tie partners into long-range product strategies. These buyers continue to drive volume, but growth momentum is shifting toward small- and mid-sized enterprises (SMEs).

Cloud-based CAD/PDM stacks reduce up-front software licensing, letting SMEs access the same tool maturity that once only global majors could afford. Platform-as-a-service providers offer pay-as-you-go simulation hours and AI-assisted design wizards, amplifying lean engineering teams. Subscription pricing and self-service portals simplify onboarding, while marketplaces match specialized freelancers to niche tasks. SMEs value outcome-aligned contracts that fit variable cash flows, prompting providers to craft modular service catalogs.

Regulatory burdens pose a hurdle for smaller firms, so vendors differentiate by offering turnkey documentation packs, certification checklists, and regulatory liaison services. The engineering services outsourcing industry benefits as SME innovators in robotics, smart-agriculture equipment, and clean-tech devices outsource subsystems to accelerate first-to-market timelines. As democratized tooling spreads, the addressable client base broadens beyond tier-1 suppliers to a long tail of emerging manufacturers, compounding total market opportunity.

Geography Analysis

Asia Pacific held 41.92% of global revenue in 2025 in the engineering services outsourcing market, anchored by India’s expansive talent pool and China’s scale in manufacturing engineering. Wage inflation, however, compresses labor-cost differentials, nudging providers to layer automation on top of human expertise. India invests in upskilling through national AI centers, positioning its workforce for digital twin and analytics tasks. China advances smart-factory blueprints, melding robotics with cloud-native SCADA, yet faces export-control headwinds that shift advanced aerospace contracts to alternative sites. Vietnam and the Philippines cultivate specialized niches: Vietnam in embedded firmware, the Philippines in animation engineering for infotainment, diversifying regional portfolios.

The Middle East and Africa are seeded by Gulf-state Vision 2030 diversification programs. Saudi Arabia’s NEOM smart-city project catalyzes demand for green hydrogen, IoT, and intelligent infrastructure engineering; the UAE channels sovereign wealth funds into aerospace MRO and advanced composite R&D hubs. South Africa enters renewable-energy plant design outsourcing, while Egypt leverages multilingual talent for European near-shore work. Investment in STEM education accelerates, yet talent pipelines remain immature, requiring ongoing partnerships with global universities and technology vendors.

North America held 35.07% global revenue of 2025 in the engineering services outsourcing market, and exhibits the fastest trajectory at 34.12% CAGR through 2031, continues to purchase high-value scopes, especially for defense platforms and autonomous truck pilots. CHIPS Act incentives stimulate domestic semiconductor design centers, bolstering local outsourcing within secure enclaves. Europe emphasizes eco-design and circular-economy compliance; strict GDPR and emerging cyber-resilience mandates steer workloads to regional providers offering certified data environments. Eastern European countries, notably Poland and Romania, win spillover contracts from Western Europe thanks to EU-aligned regulations and competitive cost structures. Latin America expands slowly but gains recognition for Spanish-language technical documentation and agile collaboration, overlapping U.S. work hours.

Competitive Landscape

The engineering services outsourcing market displays moderate fragmentation. Indian IT majors such as Tata Consultancy Services, Infosys, and HCLTech scale horizontal offerings by combining software services with mechanical design, while niche specialists such as Cyient focus on aerospace certification, and L&T Technology Services excels in industrial automation. Consolidation accelerates: Cognizant acquired Belcan for USD 1.3 billion in 2024 to fuse regulated aerospace capabilities with cloud-native DevOps.

Technology differentiation is increasingly decisive. Providers deploy AI-driven generative design tools that slash iteration cycles and reduce dependency on scarce senior engineers. Digital-twin platforms integrated with product life-cycle management systems enable continuous, revenue-generating post-launch services. Lear Corporation’s February 2025 purchase of StoneShield Engineering broadens its automation portfolio for complex wire-harness production, signaling OEMs’ appetite for vertical integration.

Geographic diversification strategies surface as buyers seek resilience. Mid-tier firms build satellite centers in Mexico, Portugal, and Vietnam to hedge geopolitical and currency risk. Secure engineering centers meeting ITAR, FedRAMP, or GDPR standards command premium rates, erecting barriers to entry. Emerging white-space opportunities in quantum computing, neuromorphic chips, and sustainable-materials R&D invite academic-industry consortia to bid alongside traditional vendors, adding new flavors of competition.

Talent ecosystems become strategic assets; firms partner with universities to curate curricula around model-based systems engineering, functional safety, and AI ethics. Hackathons and open-source community contributions burnish employer brands, aiding recruitment in tight labor markets. As contract scopes evolve toward joint IP ownership and co-investment, providers that can shoulder risk and deliver outcome-based commitments capture larger wallet share.

Engineering Services Outsourcing Industry Leaders

Tata Consultancy Services (TCS)

Infosys

HCLTech

Wipro

Tech Mahindra

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alliance Machine Systems International disclosed its intent to acquire Systec Corporation and Automatan LLC, expanding automation solutions across corrugated-packaging lines.

- February 2025: Lear Corporation bought StoneShield Engineering for an undisclosed sum, enhancing advanced automation capabilities for next-generation wire-harness assembly in its E-Systems division.

- October 2024: Var Group S.p.A. agreed to purchase 55% of SMART Engineering GmbH for USD 2.16 million, broadening computer-aided engineering reach in Germany’s DACH region.

- September 2024: XPartners, backed by Axcel, acquired Danish firms Aqvila A/S and M&E Engineering A/S, lifting group revenue to USD 161.5 million and workforce to 970 employees.

Global Engineering Services Outsourcing Market Report Scope

Engineering services outsourcing (ESO) refers to the process of hiring various non-physical engineering functions, such as designing, prototyping, system integration, and testing, from an external source.

Global Engineering Services Outsourcing Market is Segmented By Services (Designing, Prototyping, System Integration, Testing, and Others), By End User (Automotive, Consumer Electronics And Semiconductors, Telecom and Others), and By Geography (North America, Europe, Asia-Pacific, and Rest of the World).

| Product Engineering (Mechanical/Mechatronics, Concept and industrial design, CAE/Simulation) |

| Embedded Engineering and Electronics (PCB/PCBA, FPGA/ASIC front-end, firmware) |

| Digital Engineering and Software |

| Verification, Validation and Compliance (V&V, HIL/SIL/MIL, certification) |

| Prototyping and NPI |

| Sustenance / Value Engineering (VAVE, re-engineering, localization, EOL) |

| System Integration |

| Automotive and Transportation |

| Industrial Equipment and Machinery |

| Consumer Electronics |

| Semiconductors |

| Oil and Gas |

| Telecom and Networking |

| Aerospace and Defense |

| Energy and Utilities |

| Medical Devices |

| Other End Users |

| On-shore |

| Off-shore |

| Hybrid/ Multi-Shore |

| Large Enterprises |

| Small and Mid-sized Enterprises (SMEs) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Service Type | Product Engineering (Mechanical/Mechatronics, Concept and industrial design, CAE/Simulation) | |

| Embedded Engineering and Electronics (PCB/PCBA, FPGA/ASIC front-end, firmware) | ||

| Digital Engineering and Software | ||

| Verification, Validation and Compliance (V&V, HIL/SIL/MIL, certification) | ||

| Prototyping and NPI | ||

| Sustenance / Value Engineering (VAVE, re-engineering, localization, EOL) | ||

| System Integration | ||

| By End User | Automotive and Transportation | |

| Industrial Equipment and Machinery | ||

| Consumer Electronics | ||

| Semiconductors | ||

| Oil and Gas | ||

| Telecom and Networking | ||

| Aerospace and Defense | ||

| Energy and Utilities | ||

| Medical Devices | ||

| Other End Users | ||

| By Delivery Model | On-shore | |

| Off-shore | ||

| Hybrid/ Multi-Shore | ||

| By Client Size | Large Enterprises | |

| Small and Mid-sized Enterprises (SMEs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the engineering services outsourcing market in 2026?

It is valued at USD 164.71 billion in 2026, with expectations of reaching USD 312.65 billion by 2031 under a 13.68% CAGR.

Which region leads demand for outsourced engineering work?

North America holds 35.07% share in 2025, and growing at a CAGR of 34.12%.

What is driving near-shore delivery growth?

Geopolitical risk diversification and stricter data-sovereignty rules are lifting near-shore engagements at a 13.98% CAGR.

Which end-user vertical is expanding fastest?

Automotive and Transportation is projected to grow at 19.79% CAGR.

Page last updated on: