Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

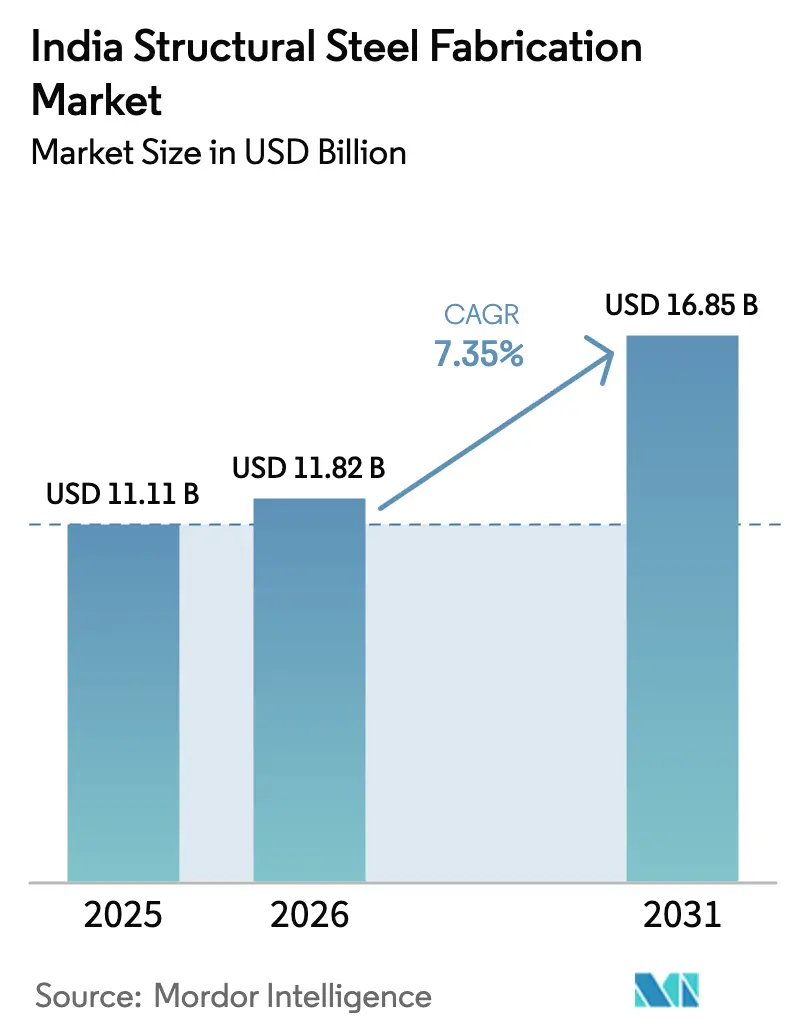

| Base Year Market Size (2025) | USD 11.11 Billion |

| Market Size (2026) | USD 11.82 Billion |

| Market Size (2031) | USD 16.85 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Structural Steel Fabrication Market Analysis by Mordor Intelligence

The India Structural Steel Fabrication Market size is expected to increase from USD 11.11 billion in 2025 to USD 11.82 billion in 2026 and reach USD 16.85 billion by 2031, growing at a CAGR of 7.35% over 2026-2031.

Sustained federal spending through the USD 1.4 trillion National Infrastructure Pipeline and the cross-sector PM Gati Shakti program has turned what were once episodic construction bursts into a predictable multiyear order book, ensuring steady tonnage off-take from fabricators. Demand is also widening beyond commodity beams; data center campuses, green hydrogen electrolyser plants, and offshore wind monopiles are driving a shift toward custom plate-worked assemblies that command price premiums but require greater engineering capability. At the same time, automation is moving from aspiration to necessity: CNC laser, plasma, and water-jet lines are replacing manual cutting to meet hyperscale developers’ tolerance targets and shorten project cycles. These forces together underpin the 7.35% growth outlook for the India structural steel fabrication market.

Key Report Takeaways

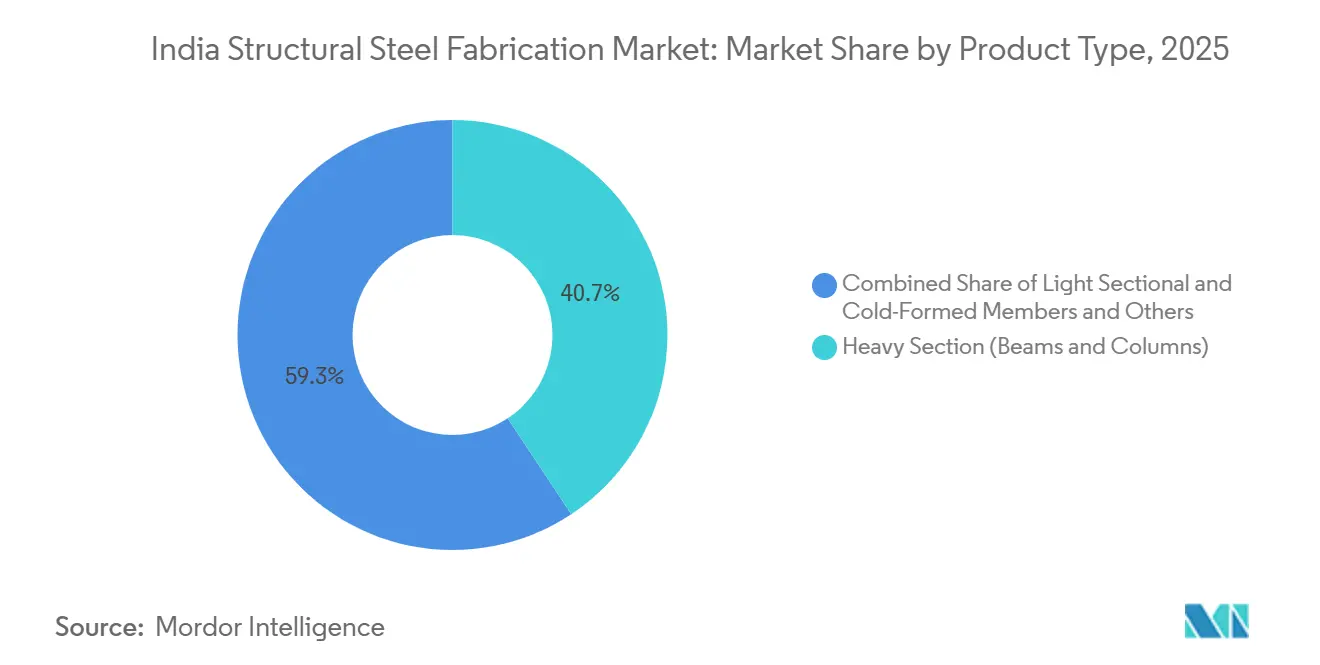

- By product type, heavy sections led with 40.68% of the India structural steel fabrication market share in 2025, while custom plate-worked modules are projected to record the fastest CAGR at 8.73% through 2031.

- By end-user, construction accounted for 40.38% of 2025 revenue; within that, infrastructure transport is advancing at a 9.08% CAGR to 2031 on the back of dedicated freight corridors, metro extensions, and airport upgrades.

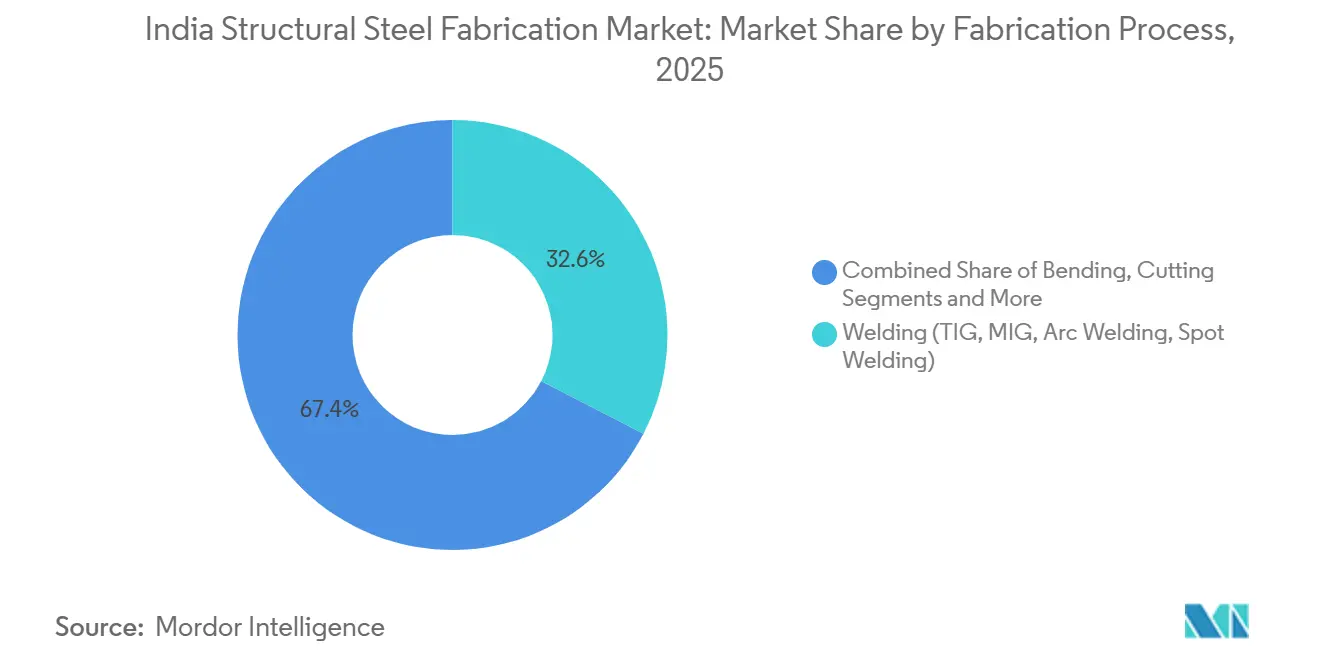

- By fabrication process, welding dominated with 32.6% of 2025 activity, yet CNC cutting technologies are expanding at an 8.56% CAGR over 2026-2031 as fabricators automate to curb scrap and labor costs.

- By geography, West India accounted for 33.04% of 2025 demand, whereas East and North-East India is forecast to log the strongest 8.34% CAGR to 2031, propelled by coal-to-chemicals complexes and port expansions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Structural Steel Fabrication Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-year rail/road/airport/port capex under NIP/PM Gati Shakti sustaining bridge, terminal, and metro steel | 1.9% | National, with early gains in Delhi NCR, Mumbai Metropolitan Region, Bengaluru, Kolkata, Chennai, Hyderabad, Pune | Long term (≥ 4 years) |

| Warehousing and industrial PEB surge into Tier II/III under National Logistics Policy and PM Gati Shakti | 1.8% | National, with concentration in Gujarat, Haryana, Uttar Pradesh, Tamil Nadu, Madhya Pradesh logistics corridors | Medium term (2-4 years) |

| Data center campus build-out to 1.8 GW capacity by 2027 driving heavy steel shells and long-span floors | 1.5% | Mumbai, Chennai, Hyderabad, Pune, Noida, Bengaluru hyperscale clusters | Short term (≤ 2 years) |

| Renewable tenders (solar/wind/BESS) expanding BOS steel needs across mounting, yards, and substations | 1.4% | Rajasthan, Gujarat, Karnataka, Andhra Pradesh, Tamil Nadu, Maharashtra renewable energy zones | Medium term (2-4 years) |

| Green Hydrogen Mission (SIGHT, low-carbon steel pilots) catalyzing electrolyser and ammonia plant structures | 1.0% | Gujarat, Rajasthan, Odisha, Tamil Nadu (coastal industrial clusters with renewable energy access) | Medium term (2-4 years) |

| Offshore wind and port modernization kick-offs requiring complex marine steel fabrication | 0.8% | Gujarat, Tamil Nadu offshore wind zones; national port modernization under Sagarmala (Mumbai, Chennai, Visakhapatnam, Paradip, Haldia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Multiyear Rail, Road, Airport, Port Capex Under NIP/PM Gati Shakti

Budget 2025-26 earmarked USD 134 billion for infrastructure, locking in demand for bridges, viaducts, and terminal roofs through 2031.[1]Press Information Bureau, “Union Budget 2025-26 Infrastructure Outlay,” pib.gov.in The Eastern and Western Dedicated Freight Corridors alone need more than 2 million tonnes of fabricated steel for bridges and gantries, with completion timelines stretching to 2028. Metro additions across seven metros add 400-500 route-km, each km requiring 1,200-1,500 tonnes of steel. Sagarmala’s port upgrades and airport modernizations further widen the order funnel but impose liquidated-damages clauses that penalize schedule lapses, raising the premium on just-in-time delivery and automated inspection.

Warehousing and Industrial PEB Surge into Tier II/III Cities

The National Logistics Policy aims to cut logistics cost to below 10% of GDP by 2030, sparking a warehouse boom that absorbed 58 million ft² of Grade A capacity during 2024, 42% of which rose in Tier II/III locations.[2]Department for Promotion of Industry and Internal Trade, “National Logistics Policy,” dpiit.gov.in Pre-engineered buildings (PEBs) dominate these projects because standardized portal frames allow a 100,000 ft² hub to go live in 120 days versus 180-plus days for concrete. PM Gati Shakti’s single digital window has trimmed statutory clearances by 10 months, compressing developers’ working-capital cycles. For fabricators, a single multimodal park can lock in 8,000-12,000 tonnes across warehouses, truck terminals, and cold storage, but tight reverse-auction pricing keeps EBITDA margins in the mid-single digits. Transporting 12-meter members from coastal yards to inland sites adds 8-12% to delivered costs, nudging larger fabricators to open satellite welding yards near demand centers.

Data-Center Campus Build-Out to 1.8 GW IT Capacity

Hyperscale cloud and colocation players have earmarked USD 100 billion for 1.8 GW of IT load by 2027, clustering in Mumbai, Chennai, Hyderabad, Pune, and Noida.[3]Ministry of Electronics and Information Technology, “Data Center Policy 2023,” meity.gov.in Each megawatt needs roughly 40,000 ft² of column-free white space, forcing live-load designs of 1,200-1,500 kg/m² and seismic-rated frames under BIS IS 800. Off-site modularization lets a 10 MW hall top out in as little as 75 days, twice as fast as concrete, while state subsidies of 25-50% on power and land sweeten economics. Fabricators serving this niche must carry ISO 3834 and AWS D1.1 welding certifications, but once qualified, they gain a high-entry-barrier moat and repeat-order visibility through three- to five-year frame agreements.

Renewable Tenders Expanding BOS Steel Needs

Installed renewable capacity climbed to 203 GW by February 2025, and annual Solar Energy Corporation of India auctions of 15-20 GW translate into 60,000-80,000 tonnes of steel per GW for module tables and tracker systems.[4]Ministry of New and Renewable Energy, “Renewable Capacity Statistics 2025,” mnre.gov.in Wind projects consume 150-200 tonnes/MW, while 61 GWh of awarded battery energy-storage system (BESS) tenders add IP-rated steel enclosures. Developers embrace aggressive reverse auctions that squeeze BOS margins below 8%, yet still require 25-year corrosion warranties. Fabricators must therefore couple hot-dip galvanizing with lean sourcing to stay profitable, an operational balance that favors larger, automated yards.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported coking coal dependence and price volatility inflating input costs and buffers | -0.9% | National, affecting all steel-consuming fabricators across regions | Short term (≤ 2 years) |

| Persistent welder/detailer scarcity and slow upskilling at MSME clusters | -0.6% | Concentrated in Gujarat, Maharashtra, Tamil Nadu, Haryana, Karnataka industrial belts and fabrication hubs | Medium term (2-4 years) |

| Elongated receivables cycles and bid-driven margin pressure for MSME fabricators | -0.5% | National, with acute impact on MSME clusters in Pune, Coimbatore, Ahmedabad, Faridabad, Howrah | Medium term (2-4 years) |

| Tender/PSA slippages and undersubscription in renewables delaying steel-intensive projects | -0.4% | Rajasthan, Karnataka, Andhra Pradesh, Maharashtra renewable energy project zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Imported Coking-Coal Dependence and Price Volatility Inflating Input Costs

In 2024-2025, spot prices for coking coal, which India imports 85% of, fluctuated between USD 350 and USD 425 per tonne, primarily due to logistical challenges at Queensland mines. A 10% rise in hot-rolled coil prices typically results in a 4-6% increase in related prices. However, public-sector and PEB contracts seldom permit mid-cycle price adjustments. While large yards mitigate risks through inventory management or swap contracts, over 60% of MSME shops faced negative cash flow in 2024, as steel prices surged beyond their bid buffers. Integrated producers, like Tata Steel’s Australian JV, benefit from a 7-10% cost advantage due to their captive mine stakes, putting pressure on standalone fabricators to either forward-buy or face margin erosion.

Persistent Welder/Detailer Scarcity and Slow Upskilling

Concurrent infrastructure, renewable, and shipyard expansions pushed AWS D1.1-certified welder wages up 12-18% year-on-year across Pune, Ahmedabad, and Coimbatore during 2025. Although the National Skill Development Corporation trains 50,000 welders annually, field audits suggest only 35% hit productivity benchmarks in their first year. Larger EPC contractors lure talent with permanent housing and allowances, draining MSME yards that operate on 90-day payment cycles. Robotic welding cells cut labor intensity by one-third but cost USD 240,000-320,000 each, an outlay feasible only for fabricators topping USD 12 million in annual revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heavy Sections Anchor Volume, Custom Modules Capture Premium

Heavy sections such as W-beams and H-columns captured 40.68% of the India structural steel fabrication market share in 2025, mirroring their ubiquity in multi-story offices, industrial sheds, and metro viaducts. Commodity profiles enjoy mill-direct pricing and standardized design tables, enabling fast quoting and high throughput. Yet commodity tonnage offers thin margins, so top-tier fabricators funnel earnings into engineering software and submerged-arc welding lines to chase higher-value plate-worked girders and modular skids. The fastest-growing custom module segment is projected to expand at an 8.73% CAGR from 2026-2031, as data center, hydrogen, and offshore wind developers demand bespoke assemblies pre-integrated with electrical and mechanical systems.

The India structural steel fabrication market for custom plate-worked products is rising significantly, driven by these specialized needs. Plate girders for long-span bridges, for example, require UT-tested full-penetration welds and third-party inspection under AWS D1.5; only 20-25 Indian yards presently carry this accreditation. Fabricators that pair BIM-driven detailing with off-site modular assembly cut on-site labor by 40-50%, meet EPC schedules, and carve a defensible niche above commodity players.

By End-User Industry: Construction Dominates, Infrastructure Transport Accelerates

Construction accounted for 40.38% of the total 2025 demand, with Grade A offices, high-rise residences, and industrial PEBs driving baseline tonnage. Within construction, infrastructure, transport, dedicated freight corridors, metros, and airports, the fastest-expanding pocket is advancing at a 9.08% CAGR through 2031. Elevated viaducts alone absorb 1,200-1,500 tonnes of steel per route-kilometer, while new terminal roofs in Delhi and Bengaluru showcase architecturally exposed structural steel (AESS) that commands 15-20% premiums over standard finishes.

The India structural steel fabrication market, linked to infrastructure and transport, is expected to rise significantly. Rail-over-rail bridges on the Eastern DFC feature 90-meter plate-girders weighing 1,800 tonnes apiece, contracts that only high-capacity yards can execute. Conversely, MSME shops still thrive on sub-1,000 tonne PEBs for warehousing and cold storage, albeit with EBITDA margins squeezed below 6% due to commodity price risk and 120-day receivable cycles.

By Fabrication Process: Welding Leads, Cutting Technologies Gain on Automation

Welding processes represented 32.6% of 2025 fabrication-shop activity, underpinning everything from multi-pass column splices to robotic fillet welds on lattice nodes. Manual shielded metal arc welding remains widespread in MSME clusters, but top-tier yards have pushed robotic cells to 20% of weld volume, slashing defect rates below 0.5%. Cutting technologies, laser, plasma, and water-jet, are the fastest-growing process group, projected to grow at an 8.56% CAGR over 2026-2031, as nesting software drives plate yields up to 97% and reduces scrap transport costs.

India structural steel fabrication market, attributed to CNC cutting, is forecast to grow significantly, reflecting both equipment capex and value-added processing fees. Fabricators that integrate upstream 3D modeling with downstream CNC code shorten detailing-to-floor cycles to 24 hours, winning schedule-critical orders such as data-center trusses and EV battery-pack enclosures. Bending and forming lag behind on automation because changeover times still depend on skilled operators, yet hybrid servo-press brakes are emerging to lift throughput for curved facades and cold-formed Z-purlins.

Geography Analysis

West India led the India structural steel fabrication market with a 33.04% share in 2025, anchored by Gujarat’s petrochemical corridors and Maharashtra’s automotive and port ecosystems. The Delhi-Mumbai Industrial Corridor alone is soaking up 15,000 tonnes per month for warehouses, rail terminals, and process plants. South India follows closely, buoyed by USD 30 billion in hyperscale data-center commitments across Chennai, Hyderabad, and Bengaluru, plus 4 GW of offshore wind tenders off Tamil Nadu’s coast. Fabricators in Chennai, Mangaluru, and Krishnapatnam have added submerged-arc lines and robotic welding to serve the marine-grade monopiles and long-span floors markets.

North India benefits from metro expansions in Delhi, Lucknow, and Patna, as well as the 1,856 km Eastern DFC, which alone requires 1.2 million tonnes of fabricated steel by 2028. Demand here skews to bridge girders and station canopies, favoring heavy-section producers with in-house painting and galvanizing. Yet land prices around Delhi-NCR are pushing fabricators to relocate their finishing yards to Haryana and Rajasthan, where statutory clearances are faster.

East and North-East India such as, West Bengal, Odisha, Jharkhand, Chhattisgarh, and the seven sister states are poised for the fastest 8.34% CAGR to 2031, lifted by coal-to-chemicals hubs in Odisha and by Sagarmala port upgrades in Paradip and Haldia. Cross-border highways under the Act East Policy add a new artery of demand for bridge trusses and gantry frames. Fabrication capacity is migrating inland to Ranchi and Raipur where Tata Steel and SAIL are setting up downstream parks, providing captive slab feedstock and single-window approvals within 60 days.

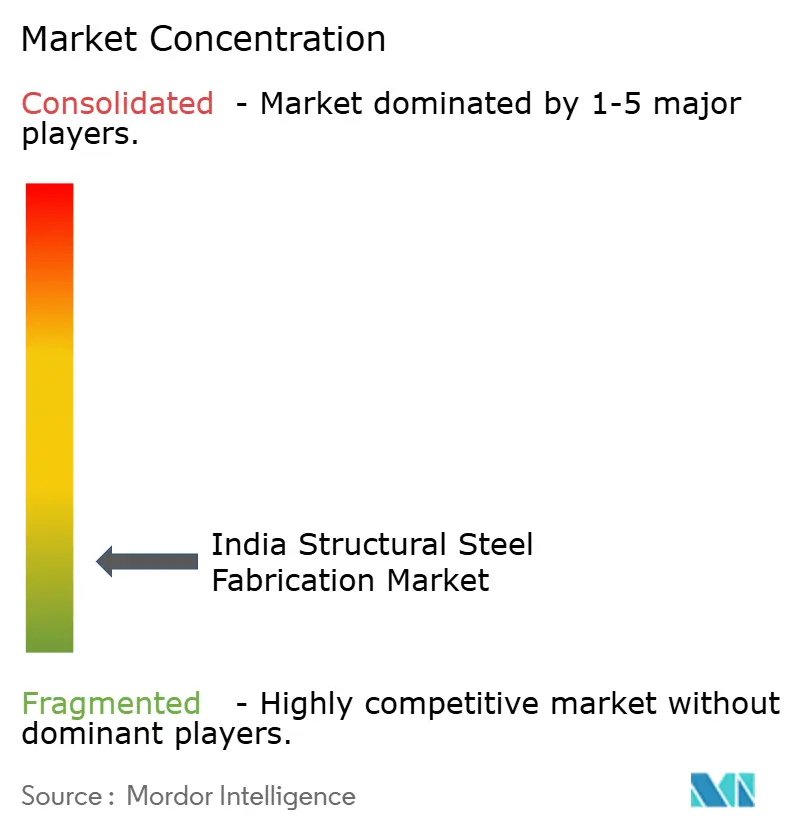

Competitive Landscape

The India structural steel fabrication market remains fragmented. Entry barriers are moderate, USD 1.2–1.5 million for a baseline shop, yet scaling to annual revenue above USD 12 million requires ISO 9001 systems, BIM-capable engineers, and robotic welding, a threshold that only 50-odd players have crossed.

Strategic differentiation hinges on capability depth and supply-chain control. Larsen & Toubro Construction and Tata Projects leverage captive yards to secure megaprojects, including Delhi Metro Phase IV and 20 MW hyperscale data halls. Pre-engineered building specialists such as Tata BlueScope, Kirby, Pennar, Zamil excel at design-build speed, promising 90-day delivery for 100,000 ft² warehouses, often bundling erection in turnkey bids to lock clients into multi-year call-off contracts.

Technology adoption is widening the gap between leaders and followers. JSW Severfield’s new Bellary yard has submerged-arc gantries and inline UT that raise monthly throughput to 4,000 tonnes with 92% on-time delivery, while Pennar’s Chennai plant added laser lines and powder coating for EV battery enclosures. Mid-tier yards unable to finance automation face shrinking order books or resort to razor-thin bids that jeopardize cash flows under volatile input prices.

India Structural Steel Fabrication Industry Leaders

Bridge & Roof Co. (India) Ltd.

EPACK Prefab Technologies

Everest Industries (Steel Buildings)

Geodesic Techniques

Interarch Building Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Larsen & Toubro Construction won a USD 1.03 billion contract for Delhi Metro Phase IV, covering 95,000 tons of viaduct and station steel, enabled by a new robotic line at its Kanchipuram yard.

- November 2025: Tata Projects secured a USD 504 million turnkey order for a 20 MW data center campus in Hyderabad, integrating 18,000 tons of heavy sections within a 14-month schedule.

- September 2025: Pennar Industries added 120,000 tpa of PEB and EV enclosure capacity at Tarapur and Chennai, targeting 25% topline growth in FY 2026.

- August 2025: KEC International landed a USD 456 million 765 kV transmission-tower package needing 85,000 tonnes of lattice fabrication across three state.

India Structural Steel Fabrication Market Report Scope

By Product Type

| Heavy Section(Beams & Columns) |

| Light Sectional & Cold-Formed Members |

| Tubular & Hollow Structural Sections (HSS) |

| Other Product Types(Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) |

By End-user Industry

| Construction | Commercial |

| Residential | |

| Industrial Buildings | |

| Infrasructure(Transport) | |

| Power & Energy (include utilities and renewable energy) | |

| Manufacturing & Industrial Equipment | |

| Oil and Gas | |

| Automotive & Transportation (railways systems, metro components, etc.) | |

| Other End User Industries(Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications) |

By Fabrication Process

| Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) |

| Bending (Press brakes, roll bending, rotary bending) |

| Welding (TIG, MIG, arc welding, spot welding) |

| Machining (Milling, turning, drilling, grinding, CNC machining) |

| Forming (Stamping, forging, rolling, hydroforming) |

| Casting (Sand casting, die casting, investment casting) |

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) |

By Geography

| North India |

| West India |

| South India |

| East & North-East India |

| By Product Type | Heavy Section(Beams & Columns) | |

| Light Sectional & Cold-Formed Members | ||

| Tubular & Hollow Structural Sections (HSS) | ||

| Other Product Types(Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) | ||

| By End-user Industry | Construction | Commercial |

| Residential | ||

| Industrial Buildings | ||

| Infrasructure(Transport) | ||

| Power & Energy (include utilities and renewable energy) | ||

| Manufacturing & Industrial Equipment | ||

| Oil and Gas | ||

| Automotive & Transportation (railways systems, metro components, etc.) | ||

| Other End User Industries(Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications) | ||

| By Fabrication Process | Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) | |

| Bending (Press brakes, roll bending, rotary bending) | ||

| Welding (TIG, MIG, arc welding, spot welding) | ||

| Machining (Milling, turning, drilling, grinding, CNC machining) | ||

| Forming (Stamping, forging, rolling, hydroforming) | ||

| Casting (Sand casting, die casting, investment casting) | ||

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) | ||

| By Geography | North India | |

| West India | ||

| South India | ||

| East & North-East India | ||

Key Questions Answered in the Report

How fast is the India structural steel fabrication market expected to grow between 2026-2031?

The value of the India structural steel fabrication market is projected to increase at a 7.35% CAGR, rising from USD 11.82 billion in 2026 to USD 16.85 billion by 2031.

Which product type commands the largest share today?

Heavy sections including standard beams and columns led with 40.68% of 2025 revenue because of their widespread use in commercial, industrial, and infrastructure projects.

What end-user segment is expanding the quickest?

Infrastructure transport including dedicated freight corridors, metros, and airports—is forecast to advance at an 11.2% CAGR through 2031 on the back of sustained federal capex commitments.

Which region will register the highest growth through 2031?

East and North-East India is expected to post the fastest 12.4% CAGR, fueled by coal-to-chemicals complexes, port modernization, and cross-border connectivity corridors.

How are fabricators dealing with skilled-labor shortages?

Leading yards invest in robotic welding, BIM workflows, and higher wages to attract AWS-certified welders, while MSME shops rely on government upskilling programs and subcontracting.

What certification helps fabricators win high-margin data-center orders?

ISO 3834 welding-quality certification, often paired with AWS D1.1 or D1.5 codes, is now a de-facto entry ticket for hyperscale data-center and offshore wind projects.

Page last updated on: