India Metal Fabrication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.03 Billion |

| Market Size (2026) | USD 8.51 Billion |

| Market Size (2031) | USD 11.56 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

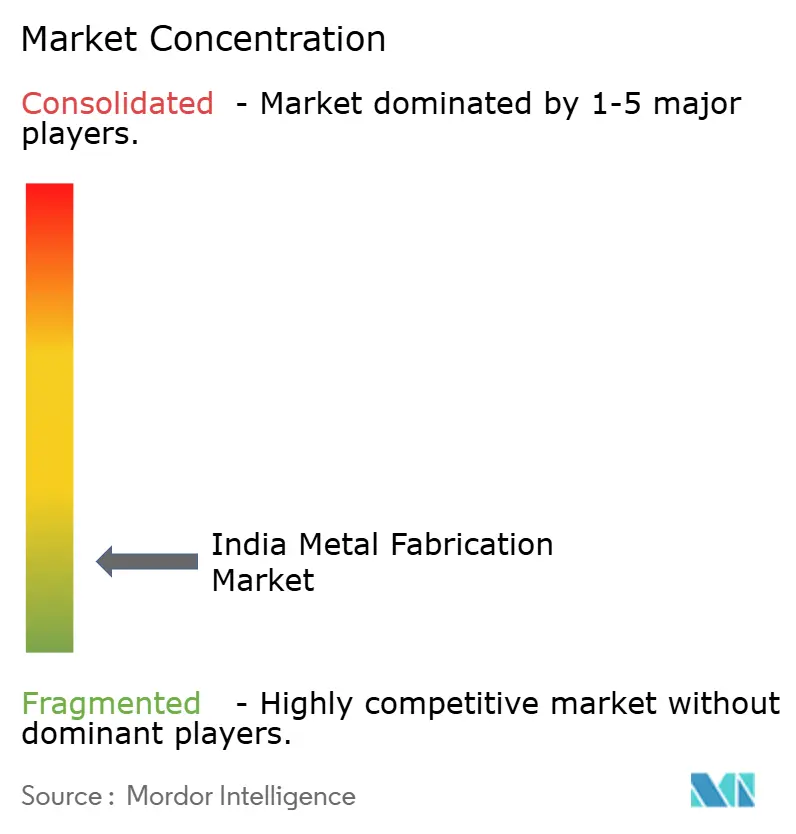

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Metal Fabrication Market Analysis by Mordor Intelligence

The India Metal Fabrication Market size is expected to increase from USD 8.03 billion in 2025 to USD 8.51 billion in 2026 and reach USD 11.56 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

Growth reflects stronger public capital formation and a broad rebound in steel capacity, as domestic crude steel reached 235 million tonnes by November 2025, while policy targets still point to 300 million tonnes by 2030. Large public programs are sustaining multi-year demand for structural steel, rail systems, and station infrastructure, and defence indigenization has lifted domestic output and shifted orders toward certified suppliers with tighter traceability. Rising data center deployments and energy transition projects are pulling orders for modular racks, mounting structures, and pressure vessels, which is prompting investment in welding quality and corrosion-resistant coatings. Export-facing producers are preparing for the EU’s Carbon Border Adjustment Mechanism from January 1, 2026, which raises the need for lower-emission routes and higher documentation standards on embedded emissions.

Key Report Takeaways

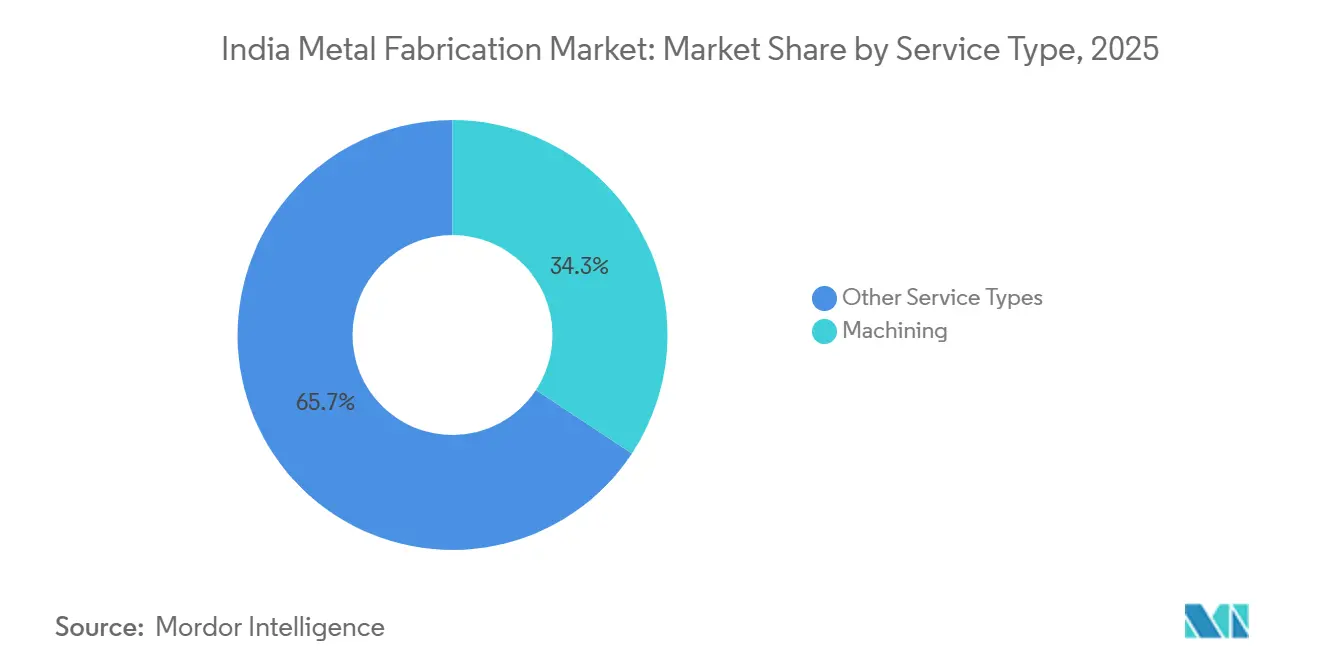

- By service type, machining held a 34.28% share in 2025, while welding is forecast to record the highest growth at a 7.34% CAGR to 2031.

- By material, carbon steel accounted for a 46.55% share in 2025, while aluminium is set to grow at a 7.96% CAGR through 2031.

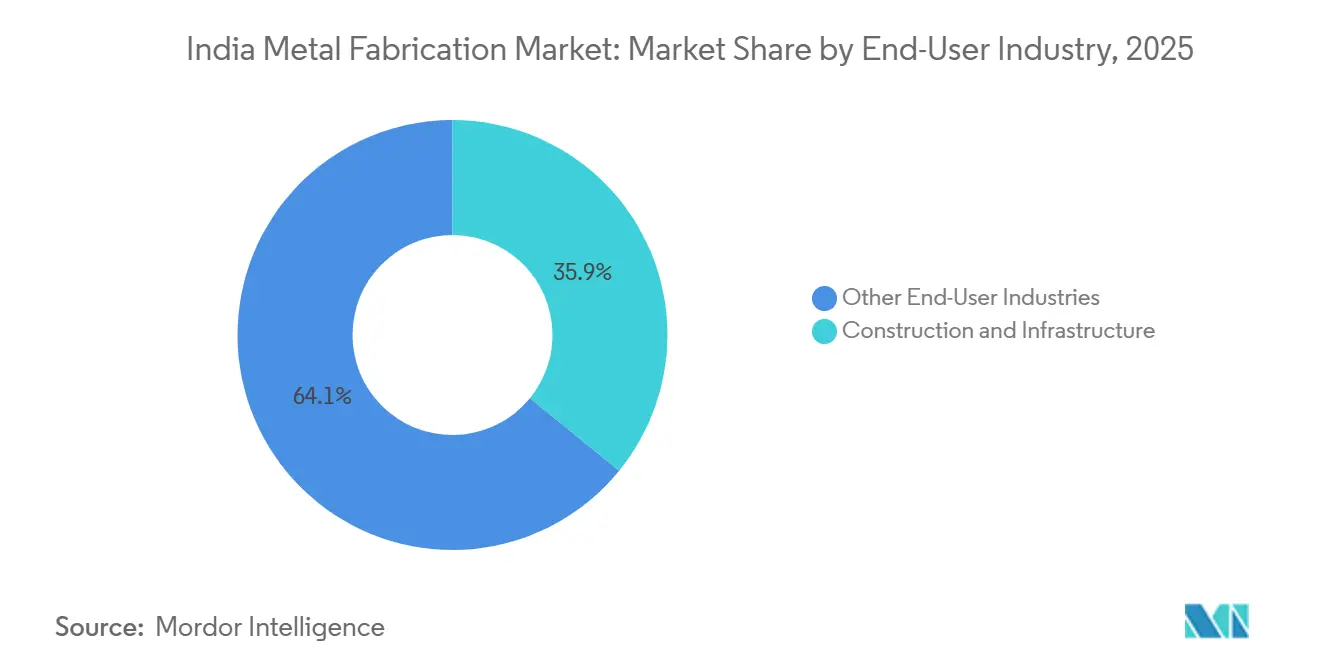

- By end-user industry, construction and infrastructure led with 35.88% revenue share in 2025, while aerospace and defence is projected to expand at an 8.18% CAGR through 2031.

- By region, Western India retained a 32.88% share in 2025, while Southern India is expected to advance at a 7.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Metal Fabrication Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy OEM localization for wind towers and solar MMS | +1.8% | National, notably Gujarat, Tamil Nadu, Maharashtra | Medium term (2-4 years) |

| Infrastructure super-cycle with Gati Shakti and NIP | +1.5% | National, early gains in Western and Northern India | Long term (≥ 4 years) |

| Defence offsets and indigenization lifting precision fabrication | +1.2% | Southern and Western defence corridors | Long term (≥ 4 years) |

| Data-center build-out driving heavy modular fabrication | +0.9% | Mumbai, Bangalore, Chennai, Delhi NCR | Short term (≤ 2 years) |

| EV and battery-pack light-weighting boosting aluminium sub-assemblies | +0.8% | Central and Eastern tier-2 and tier-3 cities | Medium term (2-4 years) |

| Green-steel procurement mandates in public tenders | +0.7% | National, pilot clusters in Gujarat and Odisha | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renewable-Energy OEM Localization For Wind Towers And Solar MMS

Defense against supply chain risk and policy incentives are bringing component manufacturing onshore across modules, towers, and mounting systems. Solar module manufacturing capacity nearly doubled from 38 GW in March 2024 to 74 GW by March 2025 as the Approved List of Models and Manufacturers and Basic Customs Duty supported domestic build-out, translating to steady orders for MMS, trackers, and galvanized structures. Wind turbine component capacity stands near 18 GW, and localization is reinforced by new lists that raise the bar on welding standards and certification for tower makers that serve coastal and high-wind sites. The National Green Hydrogen Mission has earmarked INR 14.66 billion for electrolyzer integration, which pulls precision frames and high-pressure vessels into the workload of certified shops, equal to USD 176.7 million in parentheses next to the original value (INR 14.66 billion, USD 176.7 million). Long-life solar and wind assets are shifting buyers toward pre-galvanized or hot-dip galvanized steel and higher-grade fasteners to extend structure life in saline and humid zones, increasing unit value while reducing field failures. From September 2026, BIS Scheme-X will demand domestic certification on specified heavy electrical and mounting equipment, which will push lagging small shops to upgrade in-house testing or exit sensitive supply chains.[1]https://www.pib.gov.in/indexd.aspx?reg=3&lang=2

Infrastructure Super-Cycle with Gati Shakti And NIP

Public investment has sustained momentum into FY 2025-26 with INR 11.21 lakh crore in capital expenditure and a 50-year interest-free loan of INR 1.5 lakh crore to states for infrastructure, which together support steel-intensive highways, rail, and urban transit programs, equal to USD 135.1 billion and USD 18.1 billion respectively at the prevailing exchange rate in parentheses next to the original values (INR 11.21 lakh crore, USD 135.1 billion) and (INR 1.5 lakh crore, USD 18.1 billion). The Ministry of Road Transport and Highways allocated INR 2.87 lakh crore for FY26 to expand the national highway network, equal to USD 34.6 billion in parentheses next to the original value (INR 2.87 lakh crore, USD 34.6 billion). Indian Railways’ record capex of INR 2,65,200 crore for FY26 prioritizes rolling stock, station moder nization, and corridor capacity additions that intensify demand for certified structural fabrication, equal to USD 31.9 billion in parentheses next to the original value (INR 2,65,200 crore, USD 31.9 billion). Metro rail packages are anchoring complex steelwork orders that require higher welding standards and stronger documentation, including an underground stretch in Indore awarded to a large consortium during 2025 at an order value of INR 2,189 crore, equal to USD 263.7 million in parentheses next to the original value (INR 2,189 crore, USD 263.7 million). These commitments keep the India metal fabrication market aligned with multi-year pipelines, which support capacity utilization and encourage investment in advanced cutting, forming, and inspection systems.[2]https://www.ibef.org/

Defence Offsets and Indigenization Lifting Precision Fabrication

Domestic defence production reached INR 1.27 lakh crore in FY 2023-24 as procurement shifted to Indian suppliers with higher indigenous content thresholds, equal to USD 15.3 billion in parentheses next to the original value (INR 1.27 lakh crore, USD 15.3 billion). Policy levers such as the Defence Acquisition Procedure 2020 have reserved certain order values for MSMEs and mandated local value addition, which supports smaller certified suppliers entering precision machining and welding work packages. Dassault Aviation and Tata Advanced Systems signed production-transfer agreements for Rafale fuselage assemblies in 2025, which readies a greenfield site to deliver 24 fuselages per year from FY 2028 and expands Tier-1 precision fabrication in India. Leading private suppliers reported expanded volumes into aero-engine components for global OEMs, underlining that AS9100 and NADCAP adoption is translating into export wins with higher margins. These moves bring durable order visibility to precision fabrication and reinforce the premium segment of the India metal fabrication market, where documentation and process control are decisive.[3]https://avitrader.com/

Data-Center Build-Out Driving Heavy Modular Fabrication

India’s data-center power capacity is charted to scale from a 1.4–1.8 GW range in late 2024 to 3.5–4.5 GW by 2030, absorbing USD 20–25 billion in investment and turning modular steel superstructures and equipment skids into mainstream procurement items. Investment announcements from major technology and infrastructure groups are translating into demand for high-load racks, tall bays, and structural steel suited to heavy cooling plant and electrical gear, which supports complex welded frames and floor systems. Global suppliers are expanding domestic manufacturing footprints to serve this wave, as seen in Modine’s 2025 commissioning of a Chennai facility focused on Airedale cooling modules for large campuses. Data localization requirements under India’s privacy regime are also spurring edge facilities, which are smaller but widely distributed and add reliable offtake for regional fabricators. Rising deployment of prefabricated modules and higher expectations around welding quality are drawing more bids toward integrators with ISO 3834-2 and strong in-factory inspection, which benefits the organized tier of the India metal fabrication market.[4]https://hl.com/

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported coking-coal cost volatility | -1.4% | National, higher exposure in Eastern and Western steel hubs | Short term (≤ 2 years) |

| CBAM-linked carbon-compliance cost on aluminium and steel exports | -1.2% | National, affecting export-oriented BF-BOF and coal-powered smelters | Long term (≥ 4 years) |

| MSME power-supply bottlenecks and cost pressures | -0.8% | Central and Eastern rural industrial clusters | Medium term (2-4 years) |

| Fragmented quality assurance limits export readiness | -0.6% | Pan-India unorganized sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CBAM-Linked Carbon-Compliance Cost on Aluminum and Steel Exports

The EU’s Carbon Border Adjustment Mechanism enters full financial enforcement on January 1, 2026, which means EU importers will purchase CBAM certificates linked to embedded emissions in covered goods. Indian crude steel emission intensity near 2.55 tonnes CO2 per tonne implies a sizable price wedge if producers do not reduce emissions intensity toward European benchmarks, which puts pressure on blast furnace routes. India’s steel and aluminium shipments to the EU already fell from USD 7.71 billion in FY24 to USD 5.82 billion in FY25, signaling exposure for export-oriented mills and downstream suppliers. Analytical estimates put annual CBAM liability for India near USD 1–2.5 billion, with iron and steel accounting for most covered exports, which strengthens the case for scrap-based EAFs and renewable captive power. Planning for measurement, reporting, and verification is a new requirement for many exporters, which increases the value of documented, lower-emission inputs across the India metal fabrication market.

MSME Power-Supply Bottlenecks and Cost Pressures

Small and mid-sized fabrication shops continue to face power quality and tariff issues in select locations, which pushes production into diesel genset hours and lifts unit costs during peak workload. Persistent skill shortfalls, including a large gap in certified welding personnel, limit throughput and make adoption of newer welding processes slower among smaller shops. Regulatory consolidation under the new labor codes raises wage costs and compliance rigor across states for overtime and benefits, which adds to fixed costs for MSMEs with limited balance sheet strength. Higher compliance on contractor payrolls and benefits also increases scrutiny and documentation requirements for principal employers, which cascades into stricter vendor qualification. Over time, these constraints are nudging procurement teams toward organized, certified suppliers, which further segments the India metal fabrication market into quality-led and price-led tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Machining Anchors Value, Welding Sprints on Renewable Assembly

Machining held 34.28% of the 2025 service-type revenue and continues to anchor high-precision workload in power, oil and gas, and defence, where dimensional tolerance and surface finish targets dictate process choice in the India metal fabrication market. Buyers frequently require inspection traceability and formal process control, which sustains demand for advanced machining centers with in-line metrology, and encourages integration with digital quality systems. Organized suppliers align capacity around long-cycle capital orders that prioritize uptime and adherence to PQR and WPS protocols, which stabilizes throughput. Service providers with sustained investments in automation and maintenance tend to report higher machine utilization and consistent delivery performance, which maintains their position in the India metal fabrication market. Certification regimes like ISO 3834-2 and EN 1090 support this profile by embedding welding quality and structural component compliance into the sourcing checklist for tier-1 buyers.

Welding is projected to expand at a 7.34% CAGR through 2031 as tower sections, tracker frames, and defense structures introduce higher welding-quality expectations, which raises the process value within the India metal fabrication market. Predictable demand from wind and solar assembly runs favors submerged arc and robotic MIG cells, while defense and rail packages pull in certified TIG and specialized consumables for thicker sections. Integrated suppliers use offline fixtures, weld-positioners, and end-of-line inspection records to support serial production and to maintain consistent bead quality across batches. Shops that record interpass temperature, heat input, and post-weld treatment provide stronger documentation and face fewer NCRs in audits, which shortens cycle time and reduces rework on large modules. Over the forecast period, service-type specialization will remain visible as machining concentrates on high-precision workloads and welding absorbs a larger share of renewable and rolling-stock assemblies within the India metal fabrication market.

By Material: Carbon Steel Dominates, Aluminum Sprints on EV and Data-Center Demand

Carbon steel accounted for 46.55% of the 2025 material mix within the India metal fabrication market, reflecting deep installed capacity and broad usage in structural frames, pipelines, and tanks. Policy-driven infrastructure projects continue to pull beams, plate girders, and heavy sections, which keeps the core of demand anchored despite volatility in input prices. Downside risks include import dependence for coking coal and higher exposure to carbon-cost adjustments in export markets, which sharpen the need for fuel transition and scrap availability. Buyers are also increasing requests for higher-grade coatings and corrosion protection in coastal and industrial zones, which lifts material and finishing standards. The persistent presence of carbon steel in large public and industrial jobs will keep it central to the India metal fabrication market, even as other materials expand their share.

Aluminium fabrication is projected to grow at a 7.96% CAGR through 2031 as EV battery enclosures, data-center racks, and aerospace structures prioritize weight and corrosion performance within the India metal fabrication market. The shift toward non-magnetic racks in hyperscale facilities and light-weight platforms in mobility is enlarging the installed base of aluminium joining and finishing lines. End users are also adopting mixed-material approaches and advanced joining to meet crash, thermal, and electrical requirements, which supports the premium end of aluminium fabrication. Stainless and alloy steels maintain critical roles in chemical, nuclear, and pharma equipment, with planned expansions at specialty producers focused on serving public-sector orders and regulated projects. Quality enforcement by BIS and tighter import management by DGFT shape availability and pricing, which influences material selection for higher-specification projects.

By End-User Industry: Construction Strength Versus Aerospace Acceleration

Construction and infrastructure captured 35.88% of the 2025 end-user revenue in the India metal fabrication market, driven by national highway expansion, track-and-station upgrades, and large EPC orders that sustain serial fabrication of structural components. Over the near term, elevated public capex and heightened ordering in metro rail corridors will keep structural steel demand firm for station roofs, bridges, and yards. In FY26, the highway budget of INR 2.87 lakh crore and the railway capex of INR 2,65,200 crore continue to support large fabrication packages, equal to USD 34.6 billion and USD 31.9 billion, respectively, in parentheses next to the original values (INR 2.87 lakh crore, USD 34.6 billion) and (INR 2,65,200 crore, USD 31.9 billion). EPC contractors secured packages spanning pellet plants and material handling in 2025, indicating steady industrial demand for heavy modules that rely on platework and precision welding. These dynamics sustain volume for organized suppliers and ensure tighter scheduling and documentation across high-value projects within the India metal fabrication market.

Aerospace and defence is forecast to be the fastest-growing end-user, expanding at an 8.18% CAGR through 2031 as procurement shifts toward local platforms and global OEM tie-ups raise the precision bar in the India metal fabrication market. Production-transfer agreements for fighter fuselages and engine-component contracts are moving into execution, which spreads AS9100 and NADCAP adoption and puts quality management at the center of bidding. Domestic defence output reached INR 1.27 lakh crore in FY 2023-24, and the policy direction is to lift exports and increase local value addition, equal to USD 15.3 billion in parentheses next to the original value (INR 1.27 lakh crore, USD 15.3 billion). Private suppliers also reported multi-year contracts from global aero-engine OEMs during 2025, which adds consistency to order flow and encourages capacity upgrades. Together, these end-use shifts raise the share of precision fabrication and enhance margins for certified players within the India metal fabrication market.

Geography Analysis

Western India remains the largest regional contributor with 32.88% of 2025 revenue, a position supported by mill proximity, EPC yards, and multi-sector projects that consolidate demand for heavy structural and plate fabrication within the India metal fabrication market. The concentration of large industrial conglomerates in the region sustains long-run order visibility for pre-engineered buildings, process modules, and transmission towers. Rapid fulfillment cycles benefit from coastal logistics and access to ports that shorten delivery time for bulk materials and finished structures. The India metal fabrication market share in this region is reinforced by a steady pipeline of industrial, logistics, and energy projects that spread across public and private sponsors.

Southern India is forecast to be the fastest-growing region at a 7.33% CAGR to 2031, with defense, shipbuilding, and electronics activity raising demand for precision assemblies and large modules within the India metal fabrication market. Cochin Shipyard’s dry-dock addition and collaboration agreements with global partners reinforce the south’s position in heavy ship modules and naval fabrication. Recent aerospace supplier contracts have extended local capabilities in high-precision machining and high-specification welding for aero-engine and structure parts. The region’s EV and electronics clusters are also lifting aluminium fabrication volumes, which encourages the adoption of advanced joining and finishing. These demand sources combine to create a favorable mix for certified fabricators that can assure consistent quality and timely project delivery in the India metal fabrication market.

Northern and Eastern India contribute a diverse mix of public infrastructure, rail, and steel-adjacent work, where policy-led capex and industrial projects support the base load for structural and process equipment fabrication. The rail and highways pipeline, supported by a strong FY26 budget for both sectors, keeps steady demand for bridge components, station canopies, and freight infrastructure. In Eastern India, steel-mill expansions and material handling orders for mining and metals continue to absorb heavy fabrication workload, with EPC and public-sector jobs emphasizing process documentation. Across the heartland, smaller clusters link into national programs and private investments, where vendors that can meet certification and traceability requirements gain an edge in the India metal fabrication market. Over time, the spread of quality certification and adoption of stronger QA systems will help more regional shops move up the value chain.

Competitive Landscape

Competition in the India metal fabrication market spans organized tier-1 integrators and a large base of MSMEs, with buyers increasingly prioritizing quality, documentation, and delivery reliability. Larsen & Toubro secured a series of EPC orders in 2025 across steel expansions and material handling, reinforcing its position in heavy engineering projects that require platework, structural steel, and high-capacity modules. Tata Steel progressed its Kalinganagar expansion in 2025 to raise crude steel capacity and modernize processing assets, which sustains local demand for heavy fabrication and supports advanced project execution. Pre-engineered building leaders, including Kirby Building Systems, continue to invest in certifications such as AISC and EN ISO 3834-2 to meet corporate buyer requirements, which strengthens quality assurance across large serial projects.

Strategic moves are reinforcing capacity and capability across the value chain in 2025 and 2026. ISGEC Heavy Engineering reported a robust order book and stronger profitability in FY25, reflecting a tilt toward shorter-duration, higher-margin projects that demand greater engineering content, equal to USD 973.1 million and USD 57.5 million, respectively, in parentheses next to the original values (INR 8,077 crore, USD 973.1 million) and (INR 477 crore, USD 57.5 million). Welspun Corp pursued international expansion, including a pact with Saudi Aramco and capacity increases across India and the United States to serve large-diameter pipe demand, which complements domestic water and energy projects. Global OEMs are expanding local manufacturing for data-center equipment, as seen in Modine’s Chennai facility for Airedale cooling modules, signaling confidence in the precision-fabrication ecosystem.

Project wins and cross-border partnerships are shaping competitive dynamics within the India metal fabrication market. Godrej Aerospace secured long-term contracts with global aero-engine OEMs and has increased investments in advanced machining and assembly, which sets a higher bar for supplier capabilities. L&T’s awards in aluminium and steel, including smelter and coke-oven projects, point to deeper integration with metals producers and a broadening set of fabrication opportunities. Credit rating upgrades for select joint ventures underscore steady scale-up and profitability in high-spec pressure vessels and process equipment, which is increasing the share of quality-driven projects. The direction of travel favors integrated players that deploy robotic welding cells, AI-assisted inspection, and strong traceability, while MSMEs that cannot meet documentation and certification standards will see tighter access to premium orders within the India metal fabrication market.

India Metal Fabrication Industry Leaders

Larsen & Toubro Ltd

Kirby Building Systems India

Zamil Industrial Investment Co.

ISGEC Heavy Engineering Ltd

Pennar Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cochin Shipyard and HD Hyundai signed a strategic collaboration agreement valued at INR 10,000 crore for domestic shipbuilding scale-up, which will drive large-module fabrication for naval and commercial vessels, equal to USD 1.2 billion in parentheses next to the original value (INR 10,000 crore, USD 1.2 billion).

- June 2025: Dassault Aviation and Tata Advanced Systems executed production-transfer agreements for Rafale fuselage work in Hyderabad targeting 24 units per year from FY 2028, which will demand AS9100-certified precision machining and NADCAP-approved surface treatments.

- June 2025: L&T’s Minerals and Metals division won major EPC orders from SAIL and domestic clients valued between INR 5,000 crore and INR 7,000 crore, including IISCO Steel Plant expansion, a 4-MTPA pellet plant, and sinter and material-handling systems, equal to USD 602.4 million to USD 843.4 million in parentheses next to the original values (INR 5,000–7,000 crore, USD 602.4–843.4 million).

- June 2025: Tata Steel inaugurated Phase II expansion at Kalinganagar in Odisha with INR 27,000 crore to raise crude-steel capacity from 3 to 8 MTPA, featuring advanced blast furnace and pellet plants, equal to USD 3.3 billion in parentheses next to the original value (INR 27,000 crore, USD 3.3 billion).

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the India metal fabrication market as the value generated when professional shops cut, bend, weld, machine, and finish carbon steel, stainless and alloy steel, aluminum, and other common industrial metals to deliver ready-to-assemble parts or complete structures for industrial buyers. The figures measure revenue earned by contract and captive fabricators that operate fixed facilities across the country and invoice clients in US dollars after currency translation.

Scope exclusion: Jewelry, precious-metal artistry, and hand-tool craft units run by micro enterprises are outside the study's boundary.

Segmentation Overview

- By Service Type

- Cutting

- Forming / Bending

- Welding

- Machining

- Punching / Stamping

- Finishing / Surface Treatment

- Others (Assembling, etc.)

- By Material

- Carbon Steel

- Stainless & Alloy Steel

- Aluminium

- Others (Copper, Brass, Specialty Alloys, Sheet Metal (CRCA, GI, HR))

- By End-User Industry

- Construction & Infrastructure

- Automotive & Auto Components

- Railways & Metro

- Power & Utilities

- Aerospace & Defence

- Oil, Gas & Refinery

- Marine and Shipbuilding

- Manufacturing - Heavy Machinery & Consumer Durables

- Others (Job shops, Agricultural Equipment, Electricals, Consumer Durables, etc)

- By Region

- Western India (Maharashtra, Gujarat, Goa)

- Southern India (Tamil Nadu, Karnataka, Telangana, Andhra Pradesh, Kerala)

- Northern India (Delhi NCR, Haryana, Punjab, Uttar Pradesh, Uttarakhand, Himachal Pradesh, Rajasthan)

- Eastern India (West Bengal, Jharkhand, Odisha, Bihar, Chhattisgarh)

- Central India (Madhya Pradesh, parts of Chhattisgarh)

Detailed Research Methodology and Data Validation

Primary Research

We next spoke with fabrication shop owners, EPC procurement heads, automotive tier-one engineers, and regional trade-association officers across West, South, and North India. Their inputs clarified typical conversion margins, subcontracting ratios, and the pace at which CNC and laser systems replace manual lines, allowing us to refine growth drivers and stress-test desk findings.

Desk Research

We began by mining authoritative open files such as the Annual Survey of Industries, Directorate General of Commercial Intelligence & Statistics export data, Ministry of Road Transport project trackers, Automobile Production statistics from SIAM, and periodic releases from the Construction Industry Development Council. Company 10-Ks, exchange filings, EPC bid documents, and reputable business dailies then helped us map capacity additions and contract values. Subscription databases, including D&B Hoovers for plant financials and Dow Jones Factiva for deal flow, rounded out the desk work. These examples are illustrative; many additional public and paid sources informed smaller data points throughout the build.

Two analysts sifted this material to flag service mix, material splits, and regional hot spots before we shaped initial baselines.

Market-Sizing & Forecasting

A top-down reconstruction uses industrial gross output, steel and aluminum apparent consumption, and infrastructure capex pipelines, which are then filtered through sector-specific fabrication intensity factors. Select bottom-up checks, such as sampled average selling price times volume from eight medium and large shops, anchor reasonableness. Key variables in the multivariate regression forecast include public capex outlay, automotive production, power-equipment orders, CNC machine installations, and residential steel demand. Data gaps where shop disclosures were weak were bridged by regional wage and electricity cost proxies before final triangulation.

Data Validation & Update Cycle

Model outputs pass anomaly scans and peer review, then senior analysts sign off. We refresh models annually and trigger interim updates when budget announcements, raw-material shocks, or major plant additions move the market.

Why Our India Metal Fabrication Baseline Commands Reliability

Published figures differ because firms pick unequal scopes, price assumptions, and refresh rhythms.

We acknowledge these gaps up front, so decision-makers see exactly what drives divergence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.01 Bn (2025) | Mordor Intelligence | |

| USD 3.38 Bn (2024) | Regional Consultancy A | Narrow service scope; extrapolated past CAGR; no primary validation |

| USD 2.91 Bn (2025) | Industry Portal B | Relies on tax filings only; omits captive units; single-factor growth math |

| USD 30 Bn (2025) | Global Consultancy C | Bundles equipment sales; mixes value with tonnage; uses outdated FX rates |

Key gaps arise when some publishers count only sheet or structural work, others bundle equipment sales, and several lift historical CAGRs without on-ground checks, whereas we anchor every adjustment to verifiable capacity, demand, and price data gathered this year. These contrasts show that Mordor's disciplined variable selection, blended top-down plus sampled bottom-up checks, and annual refresh give buyers a balanced, transparent baseline they can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current size and growth outlook for the India metal fabrication market?

What is the current size and growth outlook for the India metal fabrication market?

Which end-use sector leads demand in India metal fabrication?

Construction and infrastructure lead with a 35.88% revenue share in 2025, supported by sustained highway and railway capex in FY26.

Which segments are growing fastest within the India metal fabrication market?

Aerospace and defence is the fastest-growing end user at an 8.18% CAGR to 2031, and aluminium is the fastest-growing material at a 7.96% CAGR.

Which region will grow fastest through 2031 in India metal fabrication?

Southern India is set to grow at a 7.33% CAGR on the back of defence, shipbuilding, and electronics clusters.

What regulatory and policy factors will shape the market most?

Public capex, localization in renewables, and defence procurement will support demand, while EU CBAM enforcement from Jan 1, 2026, increases the need for lower-emission inputs and robust documentation.

Page last updated on: