India Engineering, Procurement, And Construction Management (EPCM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

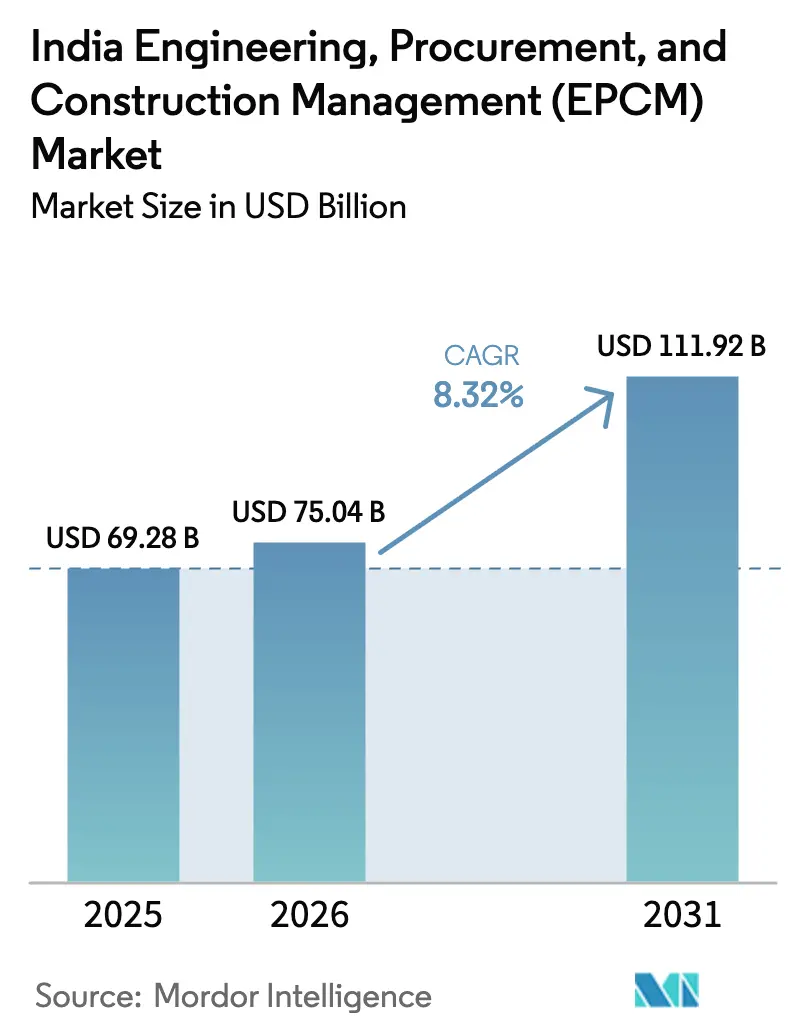

| Base Year Market Size (2025) | USD 69.28 Billion |

| Market Size (2026) | USD 75.04 Billion |

| Market Size (2031) | USD 111.92 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

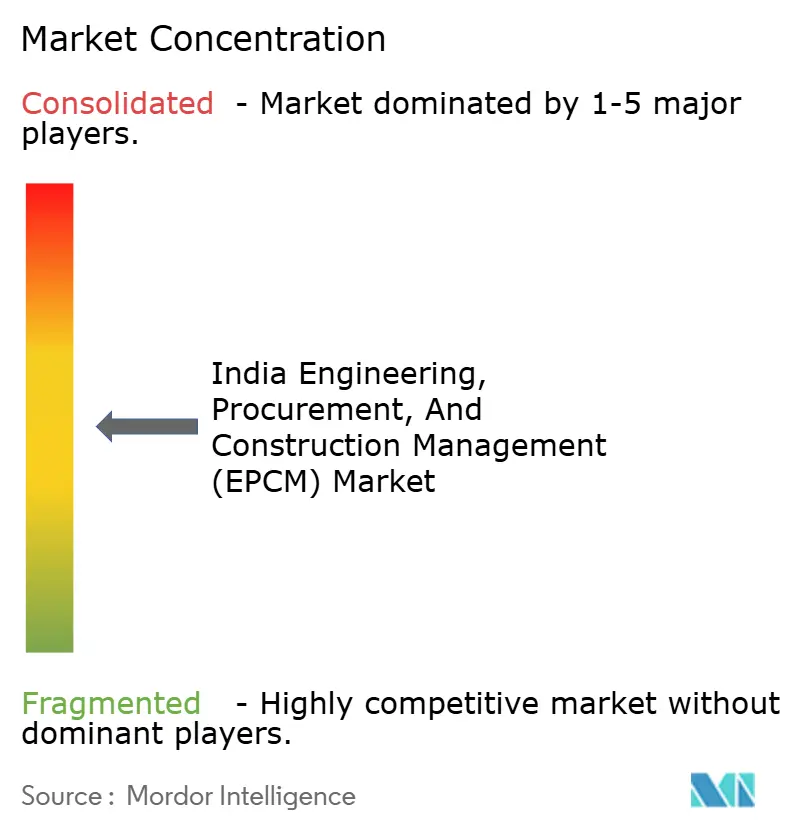

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Engineering, Procurement, And Construction Management (EPCM) Market Analysis by Mordor Intelligence

The India Engineering Procurement Construction Management market size in 2026 is estimated at USD 75.04 billion, growing from 2025 value of USD 69.28 billion with 2031 projections showing USD 111.92 billion, growing at 8.32% CAGR over 2026-2031. Growth is anchored by the National Infrastructure Pipeline’s USD 1.4 trillion commitment, a record USD 133.9 billion federal capital-expenditure push, and stronger public–private partnership frameworks that are unlocking institutional capital at lower financing costs. Rapid renewable-energy and green-hydrogen giga-projects in Gujarat and Rajasthan, surging hyperscale data-center parks in Mumbai and Chennai, and mandatory digital-twin/BIM adoption across public tenders are intensifying demand for integrated, technology-enabled EPCM services. Momentum is reinforced by ESG-linked finance that trims borrowing spreads for qualifying projects and by global OEMs introducing modular “design-for-India” solutions that shorten schedules and improve quality. Persistent headwinds remain, land-acquisition delays, steel-cement price swings, and a mid-senior talent shortage, but rising digitization is helping contractors mitigate cost overruns and safety incidents.

Key Report Takeaways

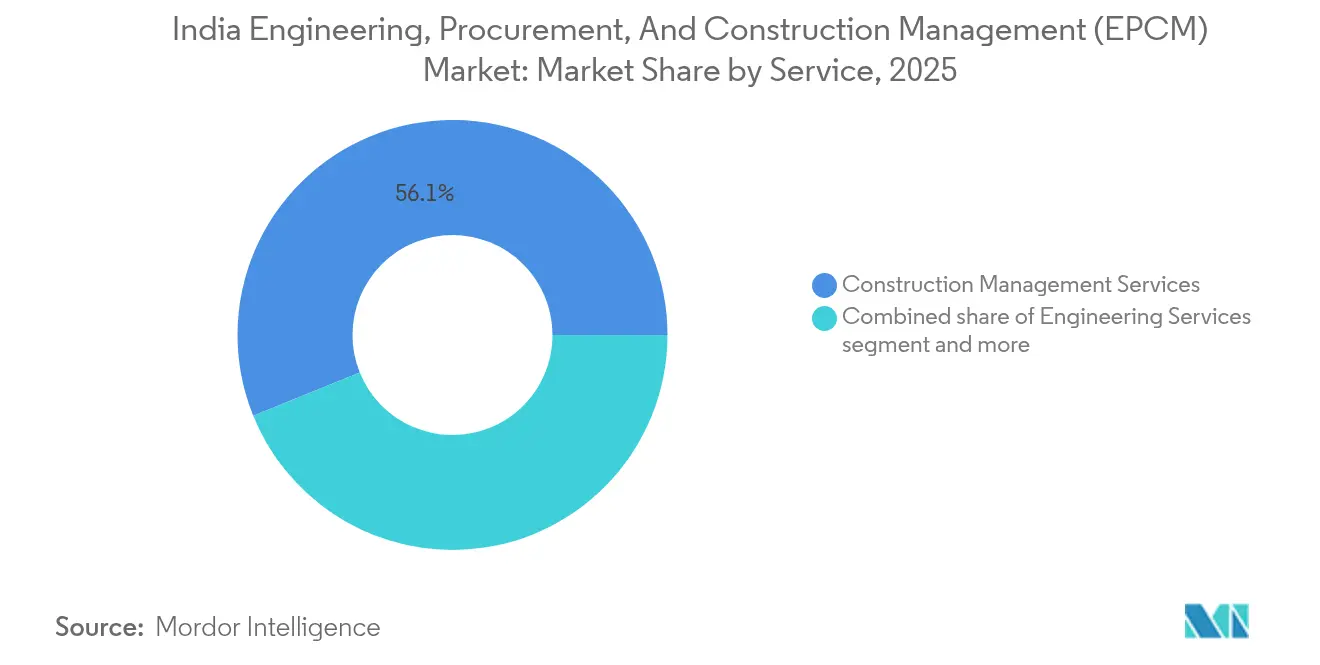

- By service type, Construction Management Services led with 56.12% of the India Engineering Procurement Construction Management market share in 2025; “Other Services” is forecast to register a 9.96% CAGR through 2031

- By sector, Infrastructure accounted for 34.02% of the India Engineering Procurement Construction Management market size in 2025, while Residential is projected to expand at an 11.02% CAGR to 2031

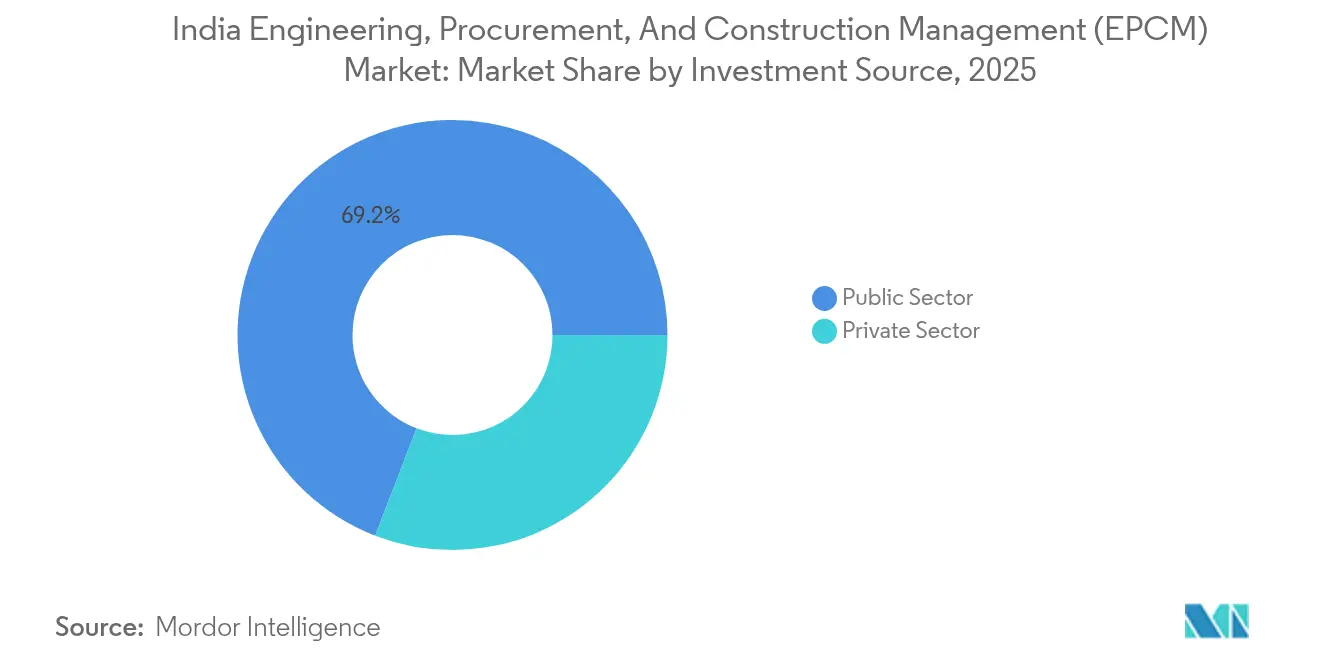

- By investment source, public spending drove 69.15% of 2025 activity, yet private investment is set to accelerate at a 9.55% CAGR during 2026-2031

- By geography, West India held 28.62% revenue share in 2025; South India is advancing at a 9.42% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Engineering, Procurement, And Construction Management (EPCM) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government infrastructure mega-capex outlay (NIP, Budget FY25) | +2.8% | National, with early gains in Delhi NCR, Mumbai, Chennai | Medium term (2-4 years) |

| Rapid scale-up of renewable & green-hydrogen giga-projects | +2.1% | Gujarat, Rajasthan, Karnataka, Tamil Nadu | Long term (≥ 4 years) |

| Surge in data-center & hyperscale industrial parks | +1.8% | Mumbai, Chennai, Hyderabad, Bangalore, Delhi NCR | Medium term (2-4 years) |

| Accelerated digital twin & BIM mandates in public tenders | +1.2% | Metro cities and state capitals | Short term (≤ 2 years) |

| ESG-linked financing lowering cost of capital for EPCM projects | +0.9% | National, concentrated in renewable and infrastructure projects | Long term (≥ 4 years) |

| Entry of global OEM-led "design-for-India" modular solutions | +0.7% | Industrial corridors and manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Mega-Capex Outlay Drives Market Acceleration

Federal capital expenditure doubled between FY 2021-2024, culminating in a USD 133.9 billion allocation for FY 2025 that covers 25,000 km of new highways and USD 142.3 billion for road infrastructure. The Delhi–Mumbai Expressway is already 82% complete across 52 EPC/HAM packages, exemplifying how diversified procurement is sustaining long-run EPCM order books. Water and urban projects such as the USD 53.7 billion Ken-Betwa river-link and AMRUT’s USD 879.5 million tranche expand opportunities beyond transport. Yet 637 live projects face delays tied to land and finance hurdles, underscoring the importance of streamlined clearances and robust contractor balance sheets. Even so, the scale of the state-led pipeline remains the single largest catalyst for the India Engineering Procurement Construction Management market[1]Ministry of Finance, “National Infrastructure Pipeline: Status Update 2025,” Department of Economic Affairs, dea.gov.in.

Renewable Energy and Green-Hydrogen Projects Create Specialized EPCM Demand

The 30 GW Khavda Renewable Park is the world’s largest single-site project, requiring bifacial modules, 5.2 MW turbines, and AI-enabled O&M centers that demand high-end EPCM skills. Parallel green-hydrogen ventures, including a USD 5 billion plan by AM Green and Reliance’s integrated complex, are spawning new workstreams around electrolyzer installation and H₂ storage. Battery-storage costs fell 66% over two years, prompting a 1 GWh BESS plant by JSW, Asia’s largest to date. However, unsigned PPAs covering 55 GW introduce offtake risk and can slow EPCM award cycles. Long-haul transmission upgrades worth USD 9 trillion (2025-2032) balance that risk by creating a parallel flow of grid EPCM contracts[2]Vineet S. Jaain, “Khavda Ultra-Mega Solar Park Investor Update Q1-2025,” Adani Green Energy Ltd., adanigreenenergy.com.

Data-Center and Hyperscale Industrial Parks Drive Infrastructure Demand

India’s live data-center capacity is on track to hit 2 GW by 2026, attracting USD 5.7 billion of fresh capex, USD 1.1 billion for civil works, and USD 4.5 billion for MEP. Mumbai and Chennai will absorb 81% of new megawatts, with Mumbai alone needing 4.41 million ft² of real estate, driving HVAC, high-density cooling, and power-distribution EPCM scopes. CtrlS is developing a 600 MW “data-center park” on 40 acres near Hyderabad, including a dedicated gas-insulated substation, setting a new benchmark for integrated industrial estates. Tier-II cities such as Lucknow and Ahmedabad now feature in project pipelines, decentralizing demand and creating a broader geographic spread for EPCM firms. Sustainability targets add complexity: hyperscale operators stipulate on-site renewables and circular water loops, generating niche consulting work under the “Other Services” banner.

Digital-Twin and BIM Mandates Transform Delivery Standards

Public tenders above USD 60 million now routinely insist on BIM Level 2 compliance, with the Kanpur–Lucknow Expressway piloting automated machine-guided grading and stringless paving. A survey of domestic contractors shows 54% already deploy AI/ML and 72% use analytics, leading APAC peers in construction tech maturity. Firms that introduce each incremental technology log an average USD 1.14 million revenue lift and 50% fewer safety incidents, proving that digitization delivers bottom-line benefits. Still, 36% of companies cite a shortage of digital talent as the primary obstacle, exposing an urgent up-skilling need. The cumulative effect is a structural rise in productivity that keeps the India Engineering Procurement Construction Management market on its high-growth path[3]Confederation of Indian Industry, “2025 Construction Digital Maturity Benchmark,” CII-Tech, cii.in.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-acquisition & environmental-clearance bottlenecks | -1.8% | National, acute in forest-rich states and tribal areas | Long term (≥ 4 years) |

| Working-capital squeeze from elongated public-sector receivables | -1.4% | National, concentrated in government project-dependent firms | Medium term (2-4 years) |

| Volatile steel-cement pricing compressing EPC margins | -1.2% | National, with regional variations in transportation costs | Short term (≤ 2 years) |

| Acute shortage of mid-senior project managers/QA-QC talent | -0.9% | Metro cities and industrial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Land Acquisition and Clearance Delays Constrain Timelines

Land and environmental approvals are India’s most chronic bottleneck, delaying 637 national projects and trimming 1.8 percentage points from forecast growth. The Parivesh digital portal and fast-track railway over-bridge clearances have shortened specific workflows, yet forest-area projects in Odisha and Jharkhand still face multi-year litigation. Renewable parks also suffer: several solar farms in Rajasthan stalled after local opposition triggered re-surveys, escalating interest costs for developers and their EPCM partners. Procedural reforms remain vital to unlock the full potential of the India Engineering Procurement Construction Management market.

Working-Capital Pressure from Public-Sector Payment Delays Erodes Margins

Government bodies owed micro and small enterprises USD 973.6 million across 13,974 cases at mid-2024, with state governments responsible for 52% of the backlog. Jal Jeevan-linked contractors, excluding L&T, saw operating margins fall to 10.3% and interest-coverage slide to 3.2× during 9M FY 2025. Election-cycle spending pauses further lengthened receivable days, restricting tender participation capacity for mid-tier firms and delaying technology investments. Until payment cycles shorten, financial stress will cap the upside from rising order inflows in the India Engineering Procurement Construction Management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Construction Management Dominance and Digital-Led “Other Services” Upswing

Construction Management Services contributed 56.12% to the India Engineering Procurement Construction Management market share in 2025, underscoring the nation’s preference for single-point accountability on complex, multi-package contracts. Integrated oversight of schedule, quality, and multi-vendor coordination has become indispensable as average project sizes exceed USD 600 million and include advanced digital controls. The segment grows in tandem with sophisticated procurement models, EPC, HAM, and PPP hybrid structures that need strong governance frameworks from pre-bid to handover.

The fastest-rising “Other Services” tranche, projected at a 9.96% CAGR, reflects burgeoning demand for BIM implementation, ESG compliance, and AI-based analytics support. Engineers India Limited, for instance, now offers R&D on carbon-footprint reduction and cathodic-protection consulting, capturing high-margin advisory work beyond its traditional remit. As more public tenders stipulate digital-twin deliverables, specialized consultants are poised to secure a growing slice of the India Engineering Procurement Construction Management market.

By Sector: Infrastructure Scale and Residential Momentum

Infrastructure remained the anchor, supplying 34.02% of 2025 receipts in the India Engineering Procurement Construction Management market size, thanks to highway, water, and transmission megaprojects backed by record federal spending. Highway builds of 25,000 km and the USD 53.7 billion Ken-Betwa program illustrate how transport and water drive recurring EPCM flows. The commercial-industrial subset, led by data-center builds exceeding USD 5.7 billion through 2026, injects additional scope for high-spec MEP and power-evacuation works.

Residential is the volume growth engine, advancing at an 11.02% CAGR on the back of Pradhan Mantri Awas Yojana subsidies and RERA-driven transparency. Maharashtra alone floated residential and civic tenders worth USD 244.0 million during 2024, highlighting how state governments are pivoting toward mass redevelopment programs. As sustainable building norms proliferate, EPCM firms with green-design and smart-city credentials will outpace peers in the India Engineering Procurement Construction Management industry.

By Investment Source: Public Primacy with Rising Private Velocity

Public entities funded 69.15% of total outlays in 2025, reflecting the government’s infrastructure-first policy and its USD 133.9 billion budget allocation. Large PSU awards, Engineers India Limited’s USD 88.0 million Middle-East PMC and Kalpataru’s USD 277.8 million domestic T&D mandates, demonstrate steady order conversion. Multi-package structuring (31 EPC and 21 HAM lots on the Delhi–Mumbai corridor) distributes risk and supports a diverse contractor base.

Private capital is accelerating at a 9.55% CAGR, catalyzed by NaBFID’s USD 12.0 billion loan approvals and relaxed InvIT rules that now welcome insurers and pension funds holding USD 749.0 billion in assets. Vedanta’s open call for global EPC alliances and Adani’s award of a 2,200 TPD chlor-alkali EPCM scope to Nuberg underscore how corporates seek specialized, globally benchmarked delivery partners. Together, these flows diversify risk and expand the opportunity set within the India Engineering Procurement and Construction Management market.

Geography Analysis

West India commanded 28.62% of 2025 revenue, buoyed by its petrochemical belt, major ports, and the 30 GW Khavda renewable cluster. State tenders in Maharashtra for coastal works (USD 213.3 million) and rail upgrades (USD 132.5 million) widen EPCM prospects across marine, rail, and urban infra. Mumbai’s 4.41 million ft² data-center pipeline enhances demand for high-density power infrastructure and critical cooling works.

South India is the fastest-growing zone at a 9.42% CAGR to 2031, anchored by large IT campuses, renewable parks, and supportive state policies. Hyderabad’s 600 MW data-center park and Chennai’s 27% share of national capacity additions exemplify the region’s digital-infra tilt. Projects such as Patel Engineering’s USD 86.5 million HEO hydro contract in Arunachal evidence the South’s ability to export EPCM expertise into challenging terrains across the wider eastern corridor.

North, East–North-East, and Central regions are catching up through multimodal corridors under PM Gati Shakti and airport builds like Jewar International, where Tata Projects integrates onsite renewables and advanced utilities. Engineers India Limited’s USD 30.5 million polypropylene EPCM at Numaligarh marks a petrochemical milestone in Assam, while Central India’s strategic logistics hubs benefit from its pan-Indian location advantage. Execution hurdles persist, yet rising public spending is gradually addressing historic under-investment across these geographies.

Competitive Landscape

India’s EPCM arena is moderately concentrated, with the top five players controlling roughly 45% of award values. Larsen & Toubro leverages its multi-sector footprint and digital command center to win megaprojects, while Tata Projects taps group synergies in metals, power, and aviation. Engineers India Limited has diversified into carbon-management consulting and overseas PMC, handling 7,000 assignments worth USD 200 billion to date.

Rising competition comes from niche specialists and foreign entrants offering modular, factory-built packages that compress lead times. Nuberg EPC captured India’s largest chlor-alkali plant by offering standardized process skids adapted for local supply chains. Global OEMs are also forming joint ventures with corridor-based fabricators, helping to localize high-precision hydraulics and electronic controls. Digital maturity and ESG credentials are now central to pre-qualification, pushing laggards to invest in AI-driven project controls to stay relevant in the India Engineering Procurement Construction Management market.

India Engineering, Procurement, And Construction Management (EPCM) Industry Leaders

Larsen & Toubro

Tata Projects

Reliance Infrastructure

GMR Group

Megha Engineering and Infrastructures Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Vedanta issued a global EPC expression of interest covering multi-metal and energy expansions over the next three years.

- April 2025: Patel Engineering emerged L1 for the USD 86.5 million, 240 MW HEO hydro project in Arunachal Pradesh with a 44-month schedule.

- March 2025: Engineers India Limited won two Middle-East PMC contracts totaling USD 88.0 million, reinforcing its international backlog.

- March 2025: Kalpataru Projects booked USD 277.8 million of new domestic and overseas orders, lifting its order book above USD 2.7 billion.

India Engineering, Procurement, And Construction Management (EPCM) Market Report Scope

The engineering, procurement, and construction management (EPCM) market offers services encompassing diverse industries' project planning, design, procurement, construction, and management.

The Indian EPCM market is segmented by services (engineering, procurement, construction, and other services) and sectors (residential, commercial, industrial, infrastructure [transportation], and energy and utilities). The report offers market size forecasts in value (USD) for all the above segments.

| Engineering Services |

| Procurement Services |

| Construction Management Services |

| Other Services |

| Residential |

| Commercial |

| Infrastructure |

| Public Sector |

| Private Sector |

| North India |

| West India |

| South India |

| East & North-East India |

| Central India |

| By Service | Engineering Services |

| Procurement Services | |

| Construction Management Services | |

| Other Services | |

| By Sector | Residential |

| Commercial | |

| Infrastructure | |

| By Investment Source | Public Sector |

| Private Sector | |

| By Region | North India |

| West India | |

| South India | |

| East & North-East India | |

| Central India |

Key Questions Answered in the Report

What is the current value of the India Engineering Procurement Construction Management market?

It stands at USD 75.04 billion in 2026 and is forecast to climb to USD 111.92 billion by 2031.

Which region is expanding the fastest?

South India leads growth with a projected 9.42% CAGR through 2031, powered by data-center and renewable investments.

Which service segment is growing quickest?

“Other Services,” covering digital-twin, ESG, and compliance consulting, is advancing at a 9.96% CAGR.

How large is public versus private investment?

Public entities fund roughly 69% of spending today, while private capital is accelerating at a 9.55% CAGR.

Page last updated on: