Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

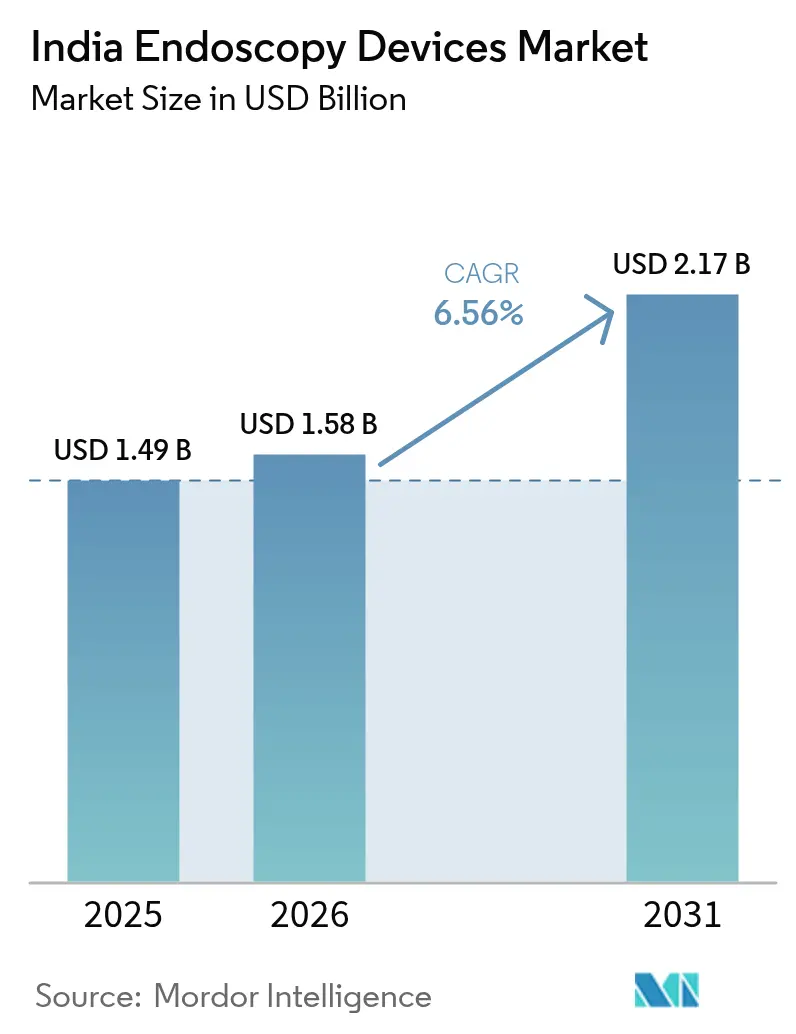

| Base Year Market Size (2025) | USD 1.49 Billion |

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.17 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Endoscopy Devices Market Analysis by Mordor Intelligence

The India Endoscopy Devices Market size is projected to expand from USD 1.49 billion in 2025 and USD 1.58 billion in 2026 to USD 2.17 billion by 2031, registering a CAGR of 6.56% between 2026 to 2031.

Sustained demand stems from an escalating non-communicable disease burden, broadened insurance under Ayushman Bharat, and rapid migration to HD/4K and AI-ready imaging towers that improve diagnostic confidence and throughput. The January 2026 India-EU Free Trade Agreement (FTA) removed duties of up to 27.5% on optical and surgical devices, cutting landed costs for advanced systems and narrowing price gaps between premium imports and locally assembled units. Private hospital chains have committed INR 30,000-40,000 crore (USD 3.6-4.8 billion) to add 34,000 beds by FY29, much of it in Tier-2/3 cities, spurring purchases of mid-range flexible scopes that match cost-per-procedure targets. Meanwhile, the Production-Linked Incentive (PLI) scheme allocates INR 3,420 crore (USD 410 million) to 16 firms to localize endoscopes and visualization systems, aiming to cut import dependence from 80% to 30-40% by 2028. These converging forces position the Indian endoscopy devices market as a priority growth arena for multinationals and domestic assemblers alike.

Key Report Takeaways

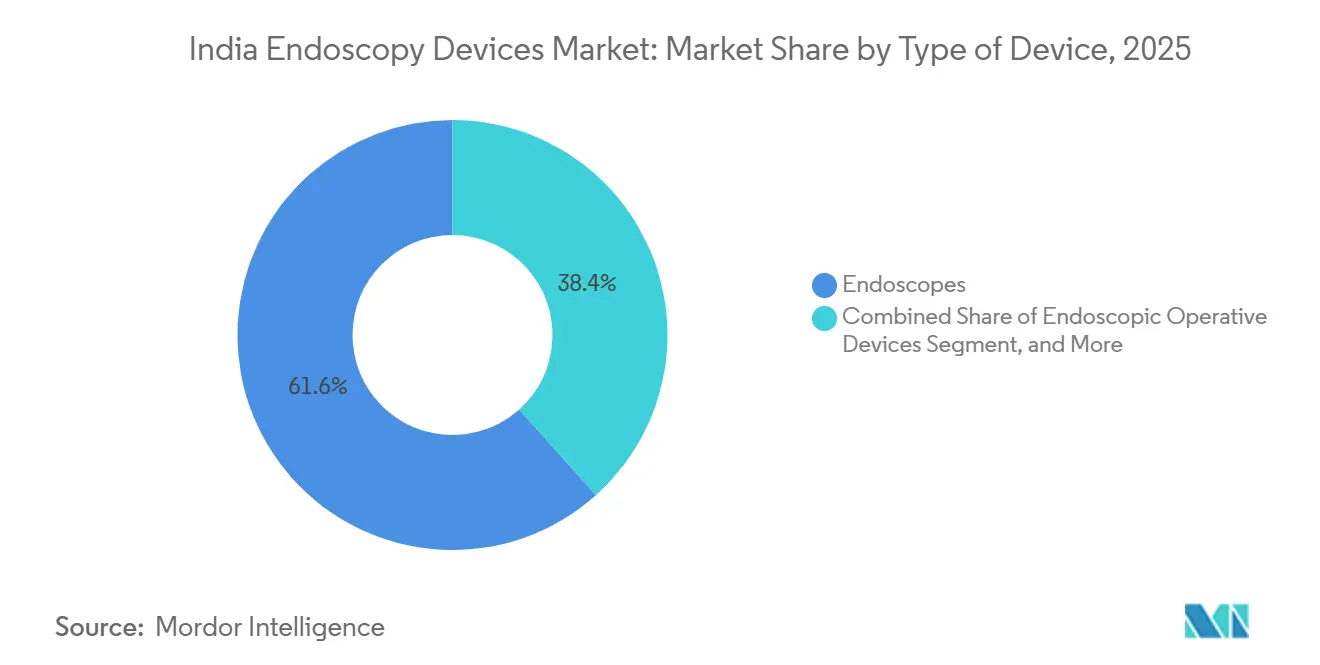

- By device type, endoscopes led with 61.62% of the Indian endoscopy devices market share in 2025 and visualization equipment is projected to expand at an 8.55% CAGR, the fastest in the device segment, through 2031.

- By application, gastrointestinal endoscopy accounted for 44.13% of India's endoscopy device market in 2025, while gynecology endoscopy is forecast to grow at a 8.97% CAGR through 2031.

- By usability, reusable products accounted for 83.78% of revenue in 2025; single-use devices are advancing at a 10.01% CAGR driven by infection-control mandates.

- By end user, hospitals accounted for 75.38% of revenue in 2025, whereas specialty clinics are expected to post a 12.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Gastrointestinal Diseases | +1.8% | Pan-India, with acute concentration in urban metros and Tier-1 cities | Medium term (2-4 years) |

| Government Healthcare Expenditure & Insurance Expansion | +1.5% | National, with early gains in Uttar Pradesh, Bihar, Madhya Pradesh | Long term (≥ 4 years) |

| HD/4K, AI & Single-Use/Capsule Endoscopy Innovations | +1.3% | Metros and Tier-1 cities; spillover to Tier-2 by 2028 | Short term (≤ 2 years) |

| Expansion of Private Hospitals & ASCs Beyond Tier-1 Cities | +1.2% | North India (UP, Rajasthan, Bihar), Karnataka, Tamil Nadu | Medium term (2-4 years) |

| PLI Incentives & Medtech Parks for Local Manufacturing | +0.5% | Himachal Pradesh, Tamil Nadu, Madhya Pradesh, Uttar Pradesh (medtech parks) | Long term (≥ 4 years) |

| Medical-Tourism Packages Bundling Advanced Endoscopy | +0.3% | Delhi-NCR, Mumbai, Chennai, Bengaluru (medical tourism hubs) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Gastrointestinal Diseases

India carries the world’s highest burden of enteric infections, and inflammatory bowel disease cases are projected to jump 69% from 270,000 in 2019 to 457,000 by 2050, expanding screening demand.[1]World Health Organization, “Inflammatory Bowel Disease in South Asia,” who.int Ayushman Bharat issued 420 million health cards to 33,000 hospitals by 2025, unlocking latent rural demand for upper and lower GI scopes. Tier-2 facilities now add day-care endoscopy suites that prefer flexible scopes over robotic platforms, aligning with cost ceilings. National cancer-control guidelines that mandate protocol-driven surveillance are also lengthening replacement cycles as high-volume sites seek durable, fast-reprocessing models.

Government Healthcare Expenditure & Insurance Expansion

Public health outlay rose from 0.9% of GDP in 2004 to 2.1% in 2023, and the FY25 Union Budget earmarked INR 9,406 crore (USD 1.13 billion) for Ayushman Bharat.[2]Federation of Indian Chambers of Commerce & Industry, “Ayushman Bharat Performance Review,” ficci-india.org PM-JAY’s package-rate reimbursements for colonoscopy, ERCP, and polypectomy assure baseline volumes that de-risk hospital investment. Tamil Nadu’s state insurance, integrated with PM-JAY, covers up to INR 500,000 per family member, stimulating private-sector endoscopy growth. North India, where bed density trails the south, is on track for 12-14% healthcare-delivery CAGR to FY28, translating into brisk device procurement. However, lower package prices pressure facilities to prefer reusable scopes unless outbreaks raise single-use uptake.

HD/4K, AI & Single-Use/Capsule Endoscopy Innovations

Fujifilm’s ELUXEO 8000 system, launched in April 2025, ships with amber-red color imaging and extended dynamic-range processing to improve lesion visibility. Stryker’s 1788 platform debuted in September 2024 with a 62.5 times wider color gamut and fluorescence modes for perfusion mapping. Fujifilm’s Gastro AI Academy pilots cut polyp-miss rates 45% in 2024 screenings, accelerating 4K upgrades in tertiary centers. Single-use bronchoscopes from Ambu and Boston Scientific entice pulmonology units worried about reprocessing contamination; capsule endoscopy pilots support remote GI screening. The India-EU FTA’s tariff removal lowers the prices of imported devices by 15-20%, shortening payback periods for high-spec towers.

Expansion of Private Hospitals & ASCs

Hospital chains are investing INR 30,000-40,000 crore to add 34,000 beds by FY29, with 40% in Tier-2/3 cities, fueling demand for mid-range, flexible scopes priced at INR 1.7-2.6 million per camera stack. North India’s bed density of 16 per 10,000 is the lowest nationally, prompting a projected 12-14% CAGR in healthcare delivery that underpins volume growth. Stand-alone endoscopy-only centers in Kanpur, Patna, and Ludhiana leverage PM-JAY’s fixed packages to achieve faster equipment payback. Such clinics value bundled service contracts, consumables, and vendor-led training, tipping procurement toward suppliers that minimize the total cost of ownership.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Endoscopy Systems | -0.9% | National, with acute impact in Tier-2/3 cities and public hospitals | Short term (≤ 2 years) |

| Shortage of Trained Endoscopists & Reprocessing Staff | -0.7% | Pan-India, severe in rural and Tier-3 cities | Long term (≥ 4 years) |

| Fragmented Optical/Sensor Supply Chain Limits Localisation | -0.6% | Concentrated in India’s manufacturing clusters; dependency on imports | Medium term (2–3 years) |

| Infection-Control Compliance Raises Cost of Reusable Scopes | -0.5% | Urban tertiary hospitals and large public institutions | Short to medium term (1–3 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Endoscopy Systems

AI-ready 4K towers cost INR 15-25 million (USD 180,000-300,000). Robotic platforms such as Intuitive Surgical’s da Vinci 5, deployed in 76 Indian installations by Q3 2024, demand multi-million-dollar budgets that most public facilities lack. State hospitals wrestle with staggered funding and delayed receivables, curbing big-ticket purchases despite tariff relief. Private hospitals mitigate risk through leasing and outcome-based service contracts, but these shift margin pressure onto vendors. Consequently, many buyers continue to favor durable, lower-spec reusable scopes over premium disposables even after the FTA price cut.

Shortage of Trained Endoscopists & Reprocessing Staff

Only 1,500-2,000 gastroenterologists serve 1.4 billion Indians, one per 700,000-900,000 people, versus one per 50,000 in developed markets. Training programs cluster in metros; rural and Tier-3 cities often have none. AIIMS reported 87,209 surgical cases in 2021-22 and runs simulation labs, but the national fellowship capacity lags demand. Technician shortages slow reprocessing, prompting some pulmonology units to adopt single-use bronchoscopes despite higher per-case costs. Fujifilm’s second Mumbai service center, opened in July 2024, pairs repair with technician upskilling to reduce downtime. Without medical-education reform, procedural capacity will remain the primary bottleneck on India endoscopy devices market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Visualization Equipment Outpaces Legacy Endoscope Growth

Visualization equipment revenue is projected to rise at an 8.55% CAGR from 2026-2031, surpassing endoscopes, which still held 61.62% of India endoscopy devices market share in 2025. The launch of Stryker’s 1788 platform lets hospitals install 4K imaging and fluorescence without replacing entire scope fleets. Rigid endoscopes dominate ENT and orthopedic procedures, while flexible scopes remain foundational for GI and pulmonology. Capsule endoscopy serves remote-screening pilots, and robotic scopes remain a niche 76-unit installed base. Domestically, PLI-enabled assemblers can now import zero-duty optics post-FTA, helping them supply mid-range 4K towers to Tier-2 buyers.

Hospitals view visualization towers as a shared asset across specialties, generating quicker ROI than single-discipline robots. AI-enabled processors that overlay polyp-detection prompts raise adenoma-detection rates and drive upgrades. Advanced operative tools, such as Fujifilm’s 360° Tracmotion ESD device, expand the therapeutic scope of demand. Net effect: visualization-first upgrades lengthen the life of reusable scopes, widening the installed base and unlocking recurring accessories revenue for suppliers.

By Application: Gynecology Endoscopy Surges on Fertility and Day-Care Demand

Gastrointestinal procedures accounted for 44.13% of India's endoscopy devices market in 2025. Yet gynecology will post the fastest growth, with an 8.97% CAGR through 2031, as fertility clinics favor hysteroscopy and laparoscopy for PCOS and endometriosis. Laparoscopy remains the No. 2 application across bariatrics and oncology. Pulmonology growth is tied to the burden of COPD and the adoption of single-use bronchoscopes. ENT volumes pivot around functional endoscopic sinus surgery; urology benefits from aging demographics and rising prostate cancer diagnoses. Cardiology uses transesophageal scopes for structural heart interventions, but remains a niche.

Fertility-center expansion in Tier-2 hubs creates day-care throughput, rewarding mid-tier 4K systems with rapid instrument turnarounds. Package-rate reimbursements under PM-JAY also encourage gynecology units to adopt reusable hysteroscopes. Meanwhile, GI demand continues to surge thanks to aging, rising IBD, and new screening protocols. The dual-engine effect ensures diversified opportunities within the Indian endoscopy devices market.

By Usability: Single-Use Devices Gain Ground on Infection-Control Mandates

Reusable scopes accounted for 83.78% of revenue in 2025; however, single-use devices will grow at a 10.01% CAGR following multiple biofilm-related alerts. Automated reprocessors boost per-case costs by INR 500-1,000, eroding reusable economics in high-volume pulmonology. Hospitals with weak sterile-processing infrastructure choose Ambu or Boston Scientific disposables. Yet high-throughput tertiary centers still favor reusables, relying on Fujifilm’s expanded Mumbai repair hub to maintain high uptime.

Tariff removal narrows price gaps, but widespread adoption of disposables hinges on payors' willingness to fund higher consumable outlays. Domestic PLI players concentrate on reusable flexible scopes for public-sector bids, constrained by imported optics. The resulting usability mix should stabilize with disposables penetrating infection-prone specialties and reusables dominating multiprocedure environments.

By End User: Specialty Clinics Capitalize on Package-Rate Optimization

Hospitals accounted for 75.38% of 2025 revenue, yet specialty clinics will grow fastest at a 12.01% CAGR through 2031. Clinics in Lucknow, Patna, and Ludhiana offer procedure-only packages, slashing overhead and improving asset turns. They deploy mid-range towers costing INR 1.7-2.6 million, often on vendor financing. Diagnostic centers add capsule endoscopy to reach rural populations via telemedicine.

Hospital procurement still dominates high-acuity therapeutic gear such as ERCP duodenoscopes and robotic systems. Private chains earmark INR 2.5-3 million per new bed for devices, supporting both premium and mid-tier purchases. Government hospitals, despite having 850,000 beds, struggle with fragmented funding but remain a vast, addressable market for rugged, reusable scopes. The Indian endoscopy devices market thus bifurcates between high-spec metro hospitals and value-focused clinics, each with different vendor-selection criteria.

Geography Analysis

North India will post the fastest regional growth at 12-14% CAGR to FY28 as private investors close the region’s 10-bed density gap versus the south. INR 30,000-40,000 crore in fresh capital targets 34,000 new beds, reserving INR 2.5-3 million per bed for equipment, including endoscopes. Tier-2 clusters such as Kanpur and Meerut lean toward bundled mid-range scopes suited to PM-JAY tariffs. Flexible gastroscopes with durable insertion tubes and low reprocessing costs appeal most.

Maharashtra, Karnataka, Tamil Nadu, and Delhi-NCR remain revenue leaders owing to dense tertiary centers and 690,000 foreign patients treated in 2023. Tamil Nadu’s state scheme empanelled 1,137 hospitals, guaranteeing volumes that cross-subsidize premium 4K towers. Metro hospitals installed Fujifilm’s ELUXEO 8000 in early 2025 to retain tourism clientele seeking AI-assisted precision.

The India-EU FTA’s tariff cuts benefit metro buyers able to absorb higher-spec imports, whereas Tier-2/3 buyers still prefer PLI-backed domestic options. Medtech parks in Uttar Pradesh and Tamil Nadu aim to shorten supply chains for these regions, but optics' reliance on Japan and Germany persists. Overall, the India endoscopy devices market displays a two-speed geography: value-driven north and technology-driven metros.

Regulatory Landscape

Endoscopy devices sold in India are regulated as medical devices under the Medical Devices Rules, 2017 (under the Drugs and Cosmetics Act, 1940) and administered by the Central Drugs Standard Control Organisation (CDSCO), Ministry of Health and Family Welfare. Products are classified across four risk classes (A to D) and go through licensing and conformity requirements for both domestic manufacture and imports. Compliance covers labeling, quality documentation, and post-market controls.

In April 2026, the Ministry of Health and Family Welfare issued a draft Medical Devices (Amendment) Rules notification (G.S.R. 270(E)) that tightens documentation around sterilization traceability and introduces a more standardized government testing fee structure. For endoscopy suppliers and hospitals, these proposed changes increase the importance of verifiable reprocessing and sterility documentation, along with more predictable testing costs, which is particularly relevant for high-throughput users where downtime and compliance audits can disrupt procedure scheduling and total cost of ownership.

Value Chain Analysis

The India endoscopy devices value chain is anchored by multinational OEMs supplying core systems, including flexible and rigid endoscopes, visualization towers, and therapeutic platforms. Domestic players focus more on assembly, accessory manufacturing, and distribution to hospitals and specialty clinics. Import dependence remains high (about 80% to 85%), especially for high-precision optics, sensors, and advanced imaging components, while local manufacturing is stronger in consumables and accessories such as biopsy forceps, snares, and other operative tools.

Upstream localization is supported through policy-backed manufacturing and industrial infrastructure, including medical device parks (for example, the Yamuna Expressway Industrial Development Authority, YEIDA, Medical Device Park) and the Production-Linked Incentive (PLI) program. A March 2026 Government of India update reported cumulative eligible sales of INR 13,624.52 crore under the PLI scheme by December 2025 with 24 greenfield projects commissioned, which supports expansion of local assembly and testing capacity. Downstream, procurement is led by large hospital chains (such as Apollo, Manipal, and Fortis) and a growing specialty-clinic segment, where service networks, spares availability, and repair turnaround times are key differentiators alongside device performance.

Competitive Landscape

Olympus, Boston Scientific, Fujifilm, Karl Storz, Medtronic, and Stryker dominate premium lanes through AI, 4K, and therapeutic accessories. Fujifilm strengthened its market share by releasing Tracmotion ESD (April 2024) and ELUXEO 8000 (April 2025), which bundled AI detection and single-operator tools. Stryker addresses modular-upgrade demand with its 1788 imaging tower. Intuitive Surgical’s da Vinci 5 anchors 76 systems across 150 hospitals, enabling 35,000 robotic procedures in 2023.

Domestic assemblers under PLI, such as Poly Medicure, pursue mid-tier segments but face imported sensors. Single-use challenger Ambu rides infection-control momentum, while AI startups license cloud-based detection algorithms that bolt onto existing towers. Post-FTA price erosion intensifies competition; service differentiation grows critical, exemplified by Fujifilm’s second Mumbai repair center (July 2024) that halves turnaround times. Overall, suppliers vie for imaging clarity, AI workflow integration, financing models, and uptime guarantees to serve buyers across varying budgets in the Indian endoscopy devices market.

India Endoscopy Devices Industry Leaders

Medtronic PLC

Olympus Corporation

Stryker Corporation

Karl Storz SE & Co. KG

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities in India are widening around compliance-ready workflows and quicker access to advanced platforms as policy changes affect licensing, testing, and procurement. In April 2026, the draft amendments to the Medical Devices Rules proposed fixed government laboratory testing fees and mandatory sterilization facility license numbers on product labels. This creates whitespace for vendors that can supply traceability-enabled single-use options, validated reprocessing accessories, and documentation toolkits that reduce compliance friction for hospitals and clinic networks.

A second opportunity is localization of imaging and accessory ecosystems to reduce landed costs and improve uptime for Tier-2 and Tier-3 expansion, supported by active government programs. A March 2026 Government of India update cited INR 13,624.52 crore in cumulative eligible sales under the PLI scheme by December 2025 and 24 greenfield projects commissioned, indicating that local assembly, component sourcing, and testing capacity are being built into the domestic supply chain. In parallel, the Department of Pharmaceuticals review of the Global Tender Enquiry (GTE) exemption list (June 2026) points to procurement preferences that favor domestically available, specification-compliant systems, while importers tend to concentrate on high-end configurations that are harder to localize. Finally, AI enablement and digital integration offer room for adoption of clinical workflow upgrades, reinforced by government-linked Centers of Excellence for AI in healthcare at AIIMS Delhi, PGIMER Chandigarh, and AIIMS Rishikesh, and by Technology Development Board support for indigenous AI imaging platforms. These efforts support pilots, validation, and integration of AI-assisted detection modules and imaging upgrades into routine endoscopy pathways.

Recent Industry Developments

- February 2026: Stryker announced the launch of the F88 flexible reusable ureteroscope within its endoscopy and urology portfolio, designed to work with the 1788 visualization ecosystem. The release strengthens cross-specialty tower utilization for hospitals that standardize on shared imaging platforms and want to add flexible endourology capability without rebuilding their visualization stack.

- September 2025: Olympus opened a new repair facility for its Surgical Business at its national headquarters in Gurugram, India. Expanding in-country service capacity supports higher equipment uptime and can influence purchasing decisions for hospitals and specialty centers that place heavy weight on turnaround times and lifecycle support.

- September 2024: Stryker launched the 1788 Advanced Imaging Platform in India to provide upgraded surgical visualization. The introduction accelerated modular upgrades toward 4K-class imaging and helped hospitals add visualization capability across multiple endoscopy applications without replacing entire fleets at once.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues from endoscopy devices sold in India, including rigid and flexible endoscopes, related operative instruments, and tower-based visualization systems used for diagnostic and therapeutic procedures.

Scope exclusions: Reprocessing services, third party maintenance, and standalone sterilization units are excluded from the market size.

Segmentation Overview

- By Device Type

- Endoscopes

- Rigid Endoscopes

- Flexible Endoscopes

- Capsule Endoscopes

- Robotic-assisted Endoscopes

- Endoscopic Operative Devices

- Irrigation / Suction Systems

- Access Devices

- Wound Protectors

- Other Endoscopic Operative Devices

- Visualization Equipment

- Endoscopes

- By Application

- Gastrointestinal Endoscopy

- Laparoscopy

- Pulmonology / Bronchoscopy

- ENT / Otolaryngology

- Urology

- Gynecology

- Cardiology

- Other Applications

- By Usability

- Reusable Devices

- Single-use / Disposable Devices

- By End-User

- Hospitals

- Diagnostic Centers

- Specialty Clinics

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to sanity check procedure demand and import dependence for endoscopy equipment in India. We referenced public sources such as Ministry of Health and Family Welfare updates, CDSCO notices, government trade statistics and customs publications, and peer-reviewed clinical literature on GI and respiratory disease burden and procedure trends.

To translate this into market numbers, we added checks from company annual reports, investor presentations, reputable press, and distributor or hospital procurement disclosures when available. In a few places, we also used paid subscriptions for company financials and intelligence, patent tracking, and shipment level import export data, so the pricing and volume assumptions did not drift too far from observed conditions. These sources are illustrative only, and many other references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what gets purchased, how often it gets replaced, and what typical pricing looks like across major care settings in India. We spoke with hospital procurement teams, clinicians who use scopes daily, distributors, and service partners so the model could be corrected where desk signals were thin.

Coverage was balanced across metros and tier 2 cities. Respondent input was used to confirm adoption of video towers, shifts toward minimally invasive procedures, and the mix between reusable and single use usage where relevant.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | |

| Mid tier: 47% | Functional/Unit leaders: 30% | |

| Smaller Players: 15% | Managers: 58% |

Market-Sizing & Forecasting

Sizing started with a top down demand build where procedure volumes and care setting mix in India were translated into device demand using utilization and replacement cycle assumptions. The totals were then corroborated with selective bottom-up approximations, including sampled price points for scopes, accessories, and towers, and supplier and channel checks to keep the output realistic.

Inputs that mattered most included endoscopy procedure growth in GI and pulmonology, installed base and replacement timing for rigid and flexible scopes, average selling price ranges by care setting, import share and currency movement affecting landed pricing, and uptake of upgraded visualization systems such as 4K. When a data gap appeared for smaller facilities, we filled it using proxy ratios from similar hospitals and then rechecked it with interview feedback.

For forecasting, scenario analysis was used so growth could be flexed based on elective procedure recovery, hospital capex cycles, and infection control driven shifts toward single use where applicable. Final year values were converted and presented in USD using consistent timing assumptions to avoid mixing rates across years.

Data Validation & Update Cycle

Outputs were validated through triangulation across demand indicators, trade signals, and price checks, and then reviewed for unusual jumps across years, segments, or care settings. When a variance could not be explained by a real world trigger, the assumptions were reopened and the relevant respondents were recontacted.

Before sign-off, a separate analyst review is completed so the logic, units, and conversions remain consistent, and the storyline matches the numbers. The report is refreshed annually, and interim updates are made if a material event changes procurement, regulation, or pricing, followed by a final pre-delivery scan so clients receive the latest view.

Mordor Intelligence's India Endoscopy Devices Market Sizing Compared With Other Published Estimates

Published market sizes for India endoscopy devices do not always match because the scope line is drawn differently and because pricing and volume assumptions are refreshed at different times. Differences also show up when one estimate is built around a narrow product definition, or when currency conversion timing is not aligned to the base year.

Services like reprocessing and third party maintenance sit outside Mordor Intelligence's scope for this market, which can make some broader healthcare equipment totals look higher even if device volumes are similar. Another common gap comes from endoscopes only studies that exclude visualization towers and operative instruments, then apply faster growth rates to a smaller starting pool without validating procedure to device ratios across hospitals and clinics.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.49 B (2025) | |

| Trade Journal A | USD 1.48 B (2025) | Often reported as an industry outlook number with limited detail on whether factory-gate revenues are used, and with scope language that can be interpreted to include adjacent equipment or service items depending on the reader. |

| Global Consultancy A | USD 0.85 B (2024) | This estimate is for endoscopes only, so it typically excludes towers and several operative instruments and accessories that are part of a full endoscopy devices spend pool, and the year and growth window differ as well. |

The comparison shows that the spread is mostly explained by what product set is counted, and whether the estimate is endoscopes-only versus a wider device bundle that includes visualization and instruments. By keeping the scope tied to observable purchase categories and cross-checking demand with procedure and replacement signals, the final value stays traceable and repeatable for planning.

Key Questions Answered in the Report

How fast is the India endoscopy devices market expected to expand between 2026 and 2031?

It is projected to grow at a 6.56% CAGR, moving from USD 1.58 billion in 2026 to USD 2.17 billion by 2031.

Which device category will witness the highest growth?

Visualization equipment is forecast to post the quickest rise at an 8.55% CAGR through 2031, driven by 4K and AI-ready upgrades.

Why are specialty clinics gaining share in endoscopy equipment purchases?

Package-rate reimbursements under PM-JAY and lower overheads let clinics achieve faster asset payback, supporting a 12.01% CAGR to 2031.

How does the India-EU FTA influence equipment pricing?

Tariff elimination cuts landed costs of imported optical and surgical devices by 15-20%, accelerating adoption of premium 4K and AI systems.

What is the main supply-side challenge for domestic manufacturers?

Dependence on imported high-precision optics and sensors from Japan and Germany limits full localization despite PLI incentives.

Page last updated on: