Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.05 Billion |

| Market Size (2026) | USD 3.39 Billion |

| Market Size (2031) | USD 5.71 Billion |

| Growth Rate (2026 - 2031) | 11.02% CAGR |

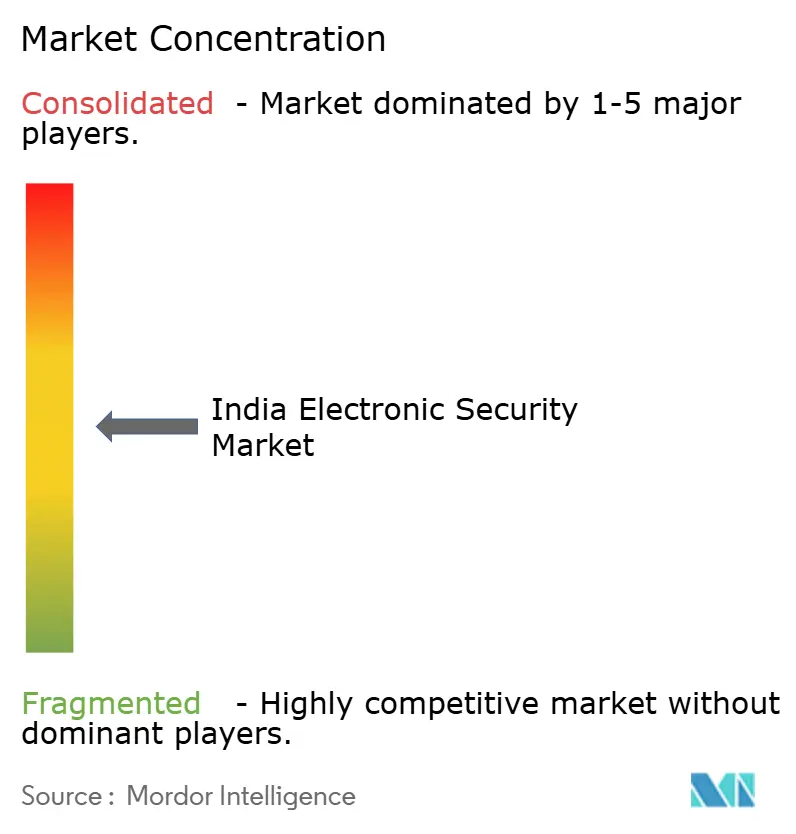

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Electronic Security Market Analysis by Mordor Intelligence

India Electronic Security market size in 2026 is estimated at USD 3.39 billion, growing from 2025 value of USD 3.05 billion with 2031 projections showing USD 5.71 billion, growing at 11.02% CAGR over 2026-2031. Intensifying regulatory oversight, infrastructure modernization, and steadily declining hardware costs together accelerate adoption across public and private sectors. Mandatory Bureau of Indian Standards (BIS) certification for closed-circuit television (CCTV) equipment, effective April 2025, is reshaping supply chains in favor of compliant domestic producers. Simultaneously, Production Linked Incentive (PLI) schemes bolster local manufacturing capacity, while smart-city allocations, women’s safety programs under the Nirbhaya Fund, and National Rail modernization budgets expand procurement pipelines. Enterprises are reallocating capital from basic cameras toward AI-enabled video analytics, and the diffusion of cloud and edge architectures is unlocking demand in Tier-2 and Tier-3 cities where bandwidth and budget constraints once limited modernization.

Key Report Takeaways

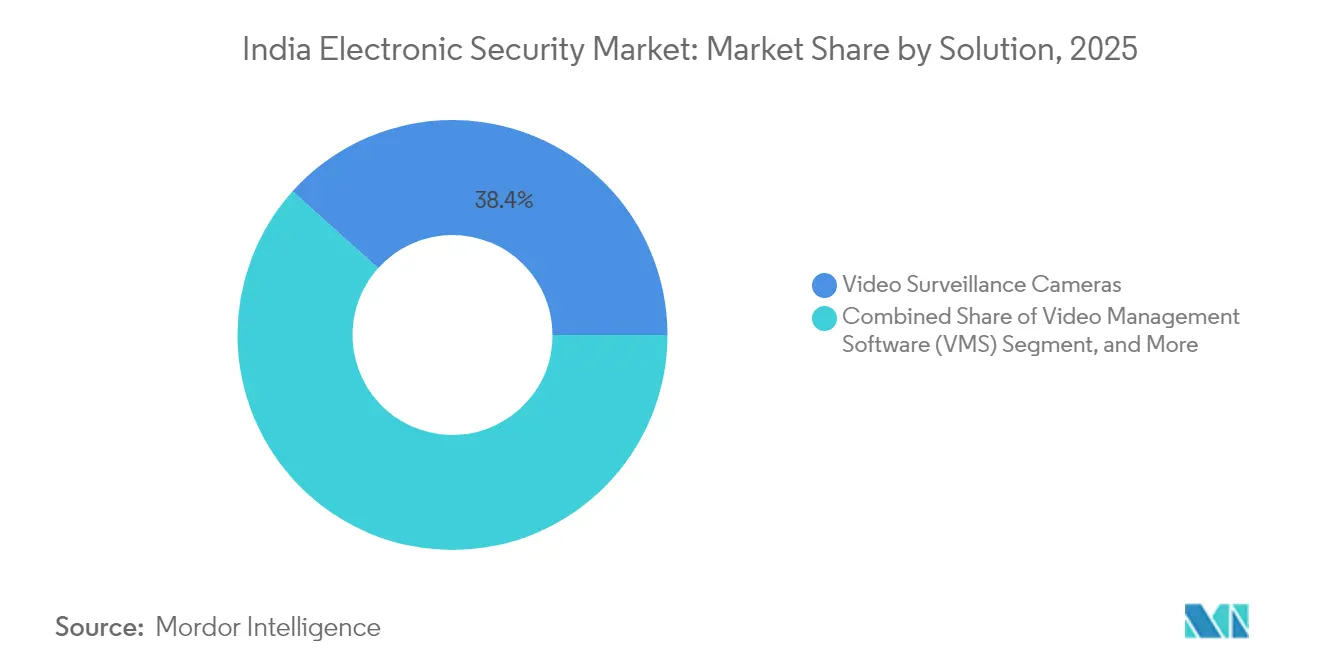

- By solution, video surveillance cameras led with 38.35% revenue share of the India Electronic Security market in 2025; video management software is projected to expand at a 12.44% CAGR through 2031.

- By services, installation and integration accounted for 48.05% share of the India Electronic Security market in 2025, while managed security services are forecast to record the fastest 12.22% CAGR to 2031.

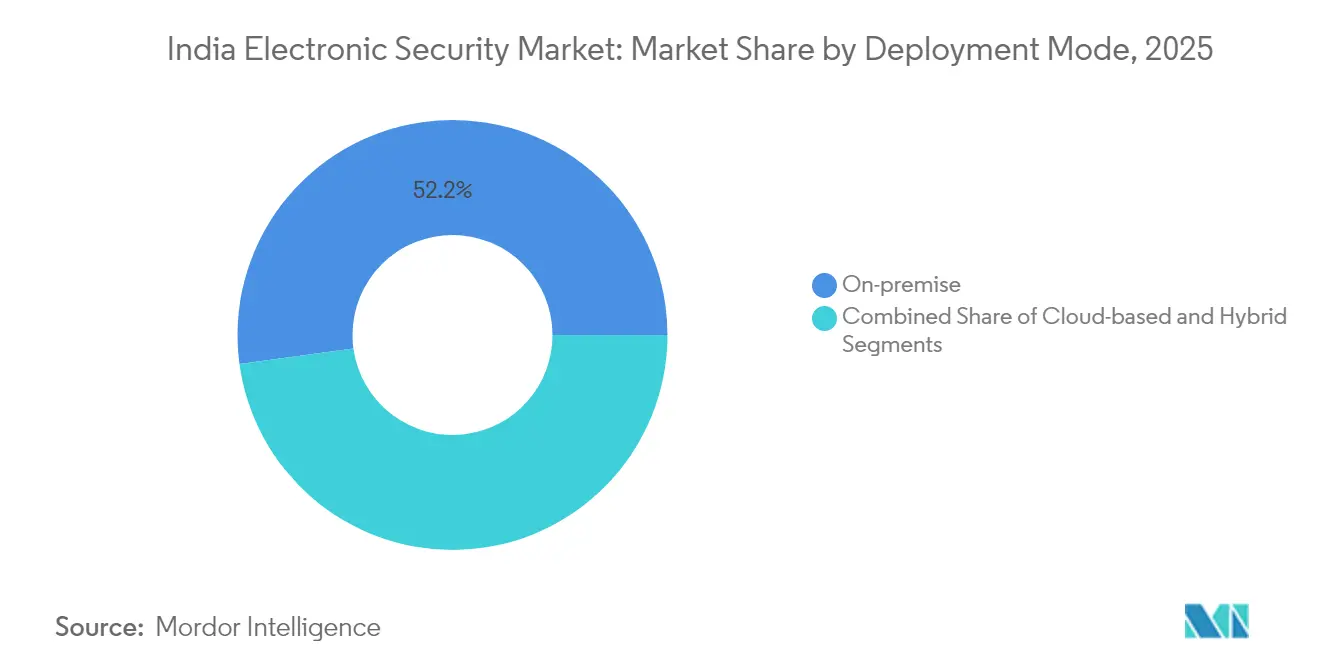

- By deployment mode, on-premise systems retained a 52.15% share of the India Electronic Security market in 2025; cloud-based deployments are expected to grow at a 11.94% CAGR through 2031.

- By component, hardware dominated with a 59.65% share of the India Electronic Security market in 2025, whereas software and analytics are set to advance at a 12.03% CAGR over the forecast period.

- By end-user vertical, government and law enforcement held a 30.85% share of the India Electronic Security market in 2025; the residential segment is poised for the quickest 12.84% CAGR to 2031.

- By geography, North India captured a 33.95% share of the India Electronic Security market in 2025, while South India is projected to be the fastest-growing region at a 12.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Electronic Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-city project pipeline beyond 2027 | +2.1% | National; Tier-1 and Tier-2 cities | Long term (≥ 4 years) |

| Rising crime and terrorism concerns | +1.8% | National; urban centers | Medium term (2-4 years) |

| Mandatory BIS re-certification for CCTV (Apr 2025) | +1.5% | National | Short term (≤ 2 years) |

| AI-enabled video analytics lowering guard costs | +1.3% | National; metros and industrial hubs | Medium term (2-4 years) |

| Domestic PLI incentives for security hardware | +1.2% | Andhra Pradesh, Tamil Nadu | Medium term (2-4 years) |

| IoT-integrated building platforms in Tier-2/3 cities | +0.9% | Tier-2/3; rural spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smart-City Project Pipeline Beyond 2027

Government allocations under the Smart Cities Mission now span more than 300 urban centers and earmark surveillance, traffic management, and emergency response as core deliverables. Delhi International Airport Limited showcased an AI-powered airside management platform in March 2025 that cut taxi-out times while integrating with perimeter security feeds. [1]Delhi International Airport Limited, “APR 2025 Airside AI Press Release,” newdelhiairport.in Indian Railways set aside INR 2.52 lakh crore (USD 30.2 billion) in its 2024-25 capital plan, reserving funds for GPS-enabled coaches and 40,000 camera upgrades, thereby standardizing ruggedized devices across rolling stock. [2]Ministry of Railways, “Pink Book 2024-25,” indianrailways.gov.in Municipal corporations in satellite towns emulate these benchmarks to attract investment, driving cascading demand for interoperable access control and analytics software. Longer-term, proposed urban renewals in Tier-2 centers such as Jaipur and Indore embed video analytics, vehicle-to-infrastructure signaling, and connected alarm systems into master plans, supporting steady equipment refresh cycles. The cumulative multiplier effect elevates baseline specifications for private developers, which, in turn, reinforces minimum-feature expectations among residential buyers.

Rising Crime and Terrorism Concerns

National Crime Records Bureau data show persistent upticks in urban property offenses and cyber-enabled crimes, compelling city and state agencies to increase surveillance budgets. Maharashtra Police deployed the MARVEL AI platform in mid-2025, enabling real-time license-plate matching and behavioral anomaly alerts across 5,000 live streams. Private enterprises mirror these investments: Larsen & Toubro announced an INR 800 crore (USD 9.6 million) cyber-physical security program in May 2025 focused on integrated SOCs that manage both digital and perimeter assets. Women’s safety initiatives continue funneling Nirbhaya Fund grants toward CCTV networks in metro stations and smart poles fitted with emergency call buttons. Rising insurance premiums for facilities lacking certified perimeter detection further nudge industrial operators toward proactive sensor deployment.

Mandatory BIS Re-Certification for CCTV (April 2025)

The April 2025 enforcement of BIS IS 13252 standards immediately barred non-certified imports, trimming Chinese low-cost share by double digits and opening space for compliant Indian incumbents such as CP PLUS, Prama Hikvision India, and Godrej Security. The rule now extends to firmware integrity checks and local data-storage conformity, pushing system integrators to reassess bill-of-materials and documentation processes. Although only seven accredited laboratories handled initial compliance loads, BIS fast-tracked additional facilities in Hyderabad and Panchkula by August 2025 to clear backlogs. Import substitution, coupled with PLI rebates of up to 15% on value addition, is catalyzing backward integration into printed circuit board assembly and lens modules. During the transition, some public-sector projects invoked procurement extensions, yet most resumed by Q3 2025 once warehouse inventories normalized.

AI-Enabled Video Analytics Lowering Guard Costs

Enterprises calculate that a single AI-assisted control-room operator can supervise 600 cameras versus 80 under manual viewing, translating into guard cost reductions of 30-40% within two years of deployment. [3]Honeywell International, “AI Video Analytics Lower Guard Costs Case Study,” honeywell.com Chennai International Airport will commission a facial-verification immigration corridor in 2025, expected to cut passenger clearance times by 60%. To address privacy activism, several municipalities pivot toward behavior-based analytics that flag loitering or crowd surges without capturing biometric identifiers. Edge inference chipsets embedded in cameras pass metadata rather than raw video to cloud dashboards, limiting bandwidth usage and mitigating data-sovereignty concerns. Return-on-investment analyses also highlight maintenance savings as predictive algorithms forecast lens dirt and network congestion, reducing truck rolls for field technicians.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance and data-governance hurdles | -1.4% | National; government and BFSI | Medium term (2-4 years) |

| High cap-ex sensitivity of SMEs | -1.1% | Tier-2/3 cities and rural | Short term (≤ 2 years) |

| Shortage of accredited BIS test labs | -0.8% | National | Short term (≤ 2 years) |

| Privacy litigation slowing facial-ID roll-outs | -0.7% | Urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Compliance and Data-Governance Hurdles

The absence of a finalized Personal Data Protection Bill leaves gray areas around biometric retention periods and cross-border cloud replication, prompting public agencies to default to on-premise archives. Financial institutions must reconcile Reserve Bank of India cybersecurity directives with emerging Computer Emergency Response Team advisories that mandate near-real-time incident logging. Procurement cycles lengthen while legal teams vet vendor data-processing agreements, often delaying cloud migrations by 6-9 months. Multisite operators confront the added cost of mirroring data centers across state lines to satisfy evolving data-localization drafts. Until a unified privacy statute is enacted, conservative technology adoption, especially for facial recognition, will cap upside in regulated verticals.

High Cap-Ex Sensitivity of SMEs

Micro and small enterprises form the spine of India’s manufacturing and retail sectors, yet frequently operate on thin margins, leaving limited budget for advanced analytics or multi-sensor fusion platforms. Basic four-camera kits priced between INR 10,300-20,990 (USD 123-251) remain the preferred entry point, crowding the low-value end of the channel. Although bank-led equipment-leasing programs exist, credit availability remains uneven in peri-urban regions, and owners often favor outright purchase to avoid monthly charges. Managed security services help convert cap-ex to op-ex, but subscription fatigue has emerged after a proliferation of SaaS fees for accounting, CRM, and utility payments. Consequently, SME adoption will track macro indicators such as GST filings and collateral-free loan disbursements rather than purely technology cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Video Management Software Drives Innovation

Video surveillance cameras continued to represent 38.35% of 2025 revenue, signifying the foundational layer of the India Electronic Security market size for solution offerings. Nevertheless, spending is tilting toward software that extracts actionable insight from existing hardware; video management software is forecast to grow at a 12.44% CAGR as firms pursue forensic search, object classification, and incident-response automation. AI engines that deliver license-plate recognition or fall-detection analytics can be licensed per-camera, allowing incremental upgrades without forklift replacements. Perimeter security sensors such as 3D LiDAR and distributed acoustic sensing are gaining favor in critical infrastructure after trial deployments cut false alarms by 70% at oil-pipeline sites. Access control is converging with visitor-management kiosks, enabling single-credential passage from parking gate to office turnstile.

Second-generation software architectures expose open REST APIs, making them integral to facilities’ wider IoT stacks and paving the way for predictive maintenance across elevators and chillers. As cyber-attack vectors migrate to networked cameras, integrators differentiate by offering secure-boot firmware and zero-trust segmentation templates. While domestic camera assembly enjoys PLI support, high-performance video analytics often rely on imported GPU accelerators, which keeps blended margins favorable for software-heavy propositions. Consequently, multinationals are acquiring specialist analytics startups to bundle capabilities, while Indian independents leverage lower-cost development talent to undercut license fees. Competitive intensity, therefore, remains balanced between scale and specialization.

By Services: Managed Security Services Transform Operations

Installation and integration retained 48.05% share of the India Electronic Security market size in 2025 as public-sector mega-projects demanded nationwide roll-outs spanning thousands of endpoints. Yet enterprises increasingly offload daily monitoring, firmware patching, and incident triage to managed security service providers (MSSPs), driving a 12.22% CAGR for this revenue stream. MSSPs pool analysts in centralized command centers and leverage AI triage to shrink average response time to under four minutes, a performance level difficult for single-tenant setups. Training and consulting revenues climb as customers seek guidance on BIS compliance documentation, data-localization schemas, and zero-trust network architecture. Maintenance contracts are shifting toward predictive models powered by embedded health probes that forecast disk failures seven days in advance, slashing unexpected downtime.

As competition intensifies, integrators pursue mergers to widen geographic footprints and diversify vertical expertise. Pricing models evolve from flat monthly fees to outcome-based contracts pegged to incident-reduction percentages. Government tenders increasingly bundle five-year managed-service clauses, stabilizing revenue visibility for vendors while raising the bar for technical certifications. The Managed Detection and Response (MDR) sub-segment edges into physical security, analyzing badge-reader logs alongside firewall alerts to spot insider threats. Collectively, these trends move the industry toward lifecycle-centric engagement, extending customer lifetime value well beyond initial hardware deployment.

By Deployment Mode: Cloud Adoption Accelerates Despite On-Premise Dominance

On-premise systems held 52.15% of the India Electronic Security market share in 2025, reflecting data-sovereignty and latency preferences among defense entities and regulated sectors. Cloud subscriptions, however, are advancing at a 11.94% CAGR as businesses with distributed branches recognize the economics of centralized analytics and elastic storage. Hybrid topologies that combine edge gateways with regional cloud nodes resolve bandwidth constraints while enabling metadata-level replication for disaster recovery. Service providers have started offering sovereign-cloud regions hosted in Indian data centers certified under MeitY empanelment, assuaging compliance officers. Additionally, the government’s Digital Locker APIs inspire similar tokenized approaches in surveillance, allowing citizens to consent to video access for specified durations.

Capital-intensive compression and transcoding work now offloads to GPUs in the cloud, cutting local CPU needs by 40%, an attractive saving for SME budgets. Meanwhile, adaptive bitrate streaming reduces data egress fees, a traditional pain point in cloud video. Vendors bundle cybersecurity toolsets intrusion detection, anomaly scanning into subscription tiers, escalating value capture beyond mere storage sales. Even public-sector units experiment with pilot cloud nodes for non-critical areas such as parking lots to validate performance before wider adoption, signalling a gradual, measured migration path ahead.

By Component: Software and Analytics Drive Value Creation

Hardware still accounted for 59.65% of 2025 spend, yet commoditization pressures temper margin upside as low-cost IP cameras flood channels. Software and analytics, the fastest-growing bucket at 12.03% CAGR, orchestrate real-time detection, post-event forensics, and compliance audit trails, elevating the India Electronic Security market as a data-driven service platform. Camera-agnostic analytics modules extend the life of installed base assets by layering modern AI over legacy RTSP feeds. This retrofit trend particularly resonates with municipal budgets strained by multiple urban-development obligations. Service revenues benefit from complexity: each machine-learning model update or regulatory patch necessitates managed roll-outs, further embedding integrators within client operations.

Hardware vendors respond by embedding secure elements and AI accelerators on-device, slicing inference latency to sub-100 milliseconds, thereby supporting edge-only deployments in bandwidth-starved rural zones. Component ecosystems deepen as Indian PCB fabricators integrate image-signal-processor (ISP) dies locally, targeting 40% domestic value addition by 2027. Analytics dashboards increasingly interweave physical alarms with cyber telemetry, a misconfigured firewall rule surfaces alongside an unauthorized door access attempt, meeting converged security governance frameworks.

By End-User Vertical: Residential Segment Accelerates Growth

Government and law enforcement represented 30.85% of 2025 demand, anchored by Central Armed Police Forces upgrades and smart-city control rooms. Nevertheless, the residential category is accelerating at a 12.84% CAGR and is projected to outpace commercial verticals by install counts over the next five years. Falling camera prices coincide with expanding e-commerce distribution that delivers do-it-yourself kits within 24 hours in most metros. Mobile apps offering live viewing and two-way talk appeal to nuclear families with dual-income parents seeking remote oversight of children and elders. Interoperability with smart-lighting ecosystems reduces app fragmentation, supporting stickiness.

Commercial real-estate owners integrate visitor-management kiosks with access control to simplify tenant onboarding, while the BFSI sector pilots behavioral biometrics to flag coercion attempts at ATMs. Manufacturing plants deploy radar-based perimeter fencing to meet zero-incident mandates under global supply-chain audits. Healthcare facilities adopt multi-factor identity verification QR passes plus temperature screening to align with updated National Healthcare Accreditation regulations. Each vertical’s nuanced regulatory regime deepens specialization among vendors, fostering targeted product SKUs and advisory services.

Geography Analysis

North India’s dominance is anchored by massive public-sector tenders and a well-developed integrator base operating across Delhi, Haryana, and Uttar Pradesh. Smart-city control rooms in Lucknow and Kanpur generate recurring software-license income, while the National Capital Region influences specification standards such as mandatory 4K resolution that ripple into adjoining states. Federal ministries require on-premise data retention, making the region a stronghold for network video recorder sales.

South India’s growth trajectory leverages its status as a technology crucible. Bangalore International Airport’s planned DigiYatra biometric corridors and Hyderabad Metro’s cloud-based video walls illustrate the region’s appetite for innovation. The prevalence of data centers from hyperscale operators like AWS and Microsoft Azure eases compliance hurdles for cloud-hosted surveillance dashboards, shortening deployment cycles for corporates. State governments in Karnataka and Telangana foster startup collaboration through open-data sandboxes, accelerating AI solution maturation.

West India benefits from the confluence of financial services in Mumbai and manufacturing clusters in Pune and Vadodara. Strict Reserve Bank of India guidelines prompt banks to adopt redundant video retention arrays with 180-day archival mandates. Meanwhile, Gujarat’s industrial safety regulations have stimulated the adoption of perimeter intrusion detection systems at petrochemical complexes. As port expansions and dedicated freight corridors come online, demand will broaden beyond city centers, diversifying the competitive landscape inside the India Electronic Security market.

Competitive Landscape

The India Electronic Security market remains moderately fragmented; the top five vendors collectively account for roughly 38% share, leaving ample opportunity for niche specialists. Domestic manufacturers such as CP PLUS, Prama Hikvision India, and Godrej Security Solutions leverage PLI incentives and proximity to BIS labs to undercut importers on both cost and compliance lead-time. Global brands Honeywell, Bosch, and Axis Communications differentiate through cyber-hardened firmware, ONVIF-conformant openness, and global service agreements appealing to multinational clients.

Technology convergence is reshaping the value curve. Camera suppliers bundle on-device analytics, while software firms embed access-control plug-ins, blurring category boundaries. System integrators increasingly offer outcome-based managed security contracts, leveraging AI triage to handle multi-sensor incident data. Strategic alliances proliferate: Honeywell’s 2024 acquisition of Carrier’s Global Access Solutions arm boosted its badge-reader portfolio, whereas Bharat Electronics Limited expanded civilian perimeter-detection products, tapping defense-grade R&D for critical-infrastructure clients.

Local channel strength is decisive in Tier-2/3 cities where procurement hinges on trust and near-instant support. Regional integrators possessing multilingual technicians win school and hospital projects, while national players focus on capex-heavy airports and rail corridors. The mandatory CCTV re-certification temporarily tilted the share toward compliant domestics, yet global incumbents are fast-tracking joint ventures to regain lost ground. In sum, capability breadth, certification agility, and service intimacy now define competitive advantage.

India Electronic Security Industry Leaders

PRAMA Hikvision India Pvt. Ltd.

Dahua Technology India Pvt. Ltd.

Aditya Infotech Ltd. (CP PLUS)

Honeywell Automation India Ltd.

Bosch Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Aditya Infotech (CP PLUS) raised INR 1,300 crore (USD 15.6 million) via an IPO oversubscribed 106 times, allocating funds toward new manufacturing lines.

- July 2025: Indian Railways reiterated a capital allocation of INR 2.52 lakh crore (USD 30.2 billion) for 2024-25, covering GPS and CCTV across 40,000 coaches.

- June 2025: Maharashtra Police rolled out the MARVEL AI video analytics platform statewide to assist real-time law enforcement.

- May 2025: Larsen & Toubro committed INR 800 crore (USD 9.6 million) to an integrated cyber-physical security initiative for enterprise customers.

- April 2025: BIS commenced mandatory CCTV certification enforcement, reshaping vendor qualification pathways.

- March 2025: Delhi International Airport deployed an AI-powered airside management system integrating surveillance, radar, and gate-assignment analytics.

- January 2025: Chennai International Airport confirmed a 2025 launch of biometric immigration corridors projected to reduce passenger processing time by 60%.

India Electronic Security Market Report Scope

Electronic security systems perform various security tasks to improve the protection of a specific area using computer software and electrical gadgets. These systems keep track of and gather data from subsystems, allowing system operators to analyze the information, choose a course of action, and promptly respond to occurrences.

The India electronic security market is segmented by type (solution and services) and end-user vertical (government, commercial, and industrial). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

By Solution

| Video Surveillance Cameras |

| Video Management Software (VMS) |

| Access Control Systems |

| Biometric Readers and Terminals |

| Intrusion Detection and Alarms |

| Perimeter Security Sensors |

By Services

| Installation and Integration |

| Maintenance and Support |

| Monitoring and Response (Command-Centre) |

| Managed Security Services |

| Training and Consulting |

By Deployment Mode

| On-premise |

| Cloud-based |

| Hybrid |

By Component

| Hardware |

| Software and Analytics |

| Services |

By End-user Vertical

| Government and Law-Enforcement |

| Commercial Buildings |

| Industrial and Manufacturing |

| BFSI |

| Transportation and Logistics |

| Residential |

| Retail and Hospitality |

| Healthcare Facilities |

| Other End-user Verticals |

By Region

| North India |

| West India |

| South India |

| East and North-East India |

| Central India |

| By Solution | Video Surveillance Cameras |

| Video Management Software (VMS) | |

| Access Control Systems | |

| Biometric Readers and Terminals | |

| Intrusion Detection and Alarms | |

| Perimeter Security Sensors | |

| By Services | Installation and Integration |

| Maintenance and Support | |

| Monitoring and Response (Command-Centre) | |

| Managed Security Services | |

| Training and Consulting | |

| By Deployment Mode | On-premise |

| Cloud-based | |

| Hybrid | |

| By Component | Hardware |

| Software and Analytics | |

| Services | |

| By End-user Vertical | Government and Law-Enforcement |

| Commercial Buildings | |

| Industrial and Manufacturing | |

| BFSI | |

| Transportation and Logistics | |

| Residential | |

| Retail and Hospitality | |

| Healthcare Facilities | |

| Other End-user Verticals | |

| By Region | North India |

| West India | |

| South India | |

| East and North-East India | |

| Central India |

Key Questions Answered in the Report

What is the 2026 value of the India Electronic Security market?

The market is valued at USD 3.39 billion in 2026.

Which solution segment is growing fastest?

Video management software is projected to grow at a 12.44% CAGR through 2031.

How is BIS certification affecting suppliers?

Mandatory certification, enforced in April 2025, is reducing non-compliant imports and boosting domestic manufacturers’ share.

Why is residential demand rising?

Affordable AI-enabled camera kits and mobile app control are driving a 12.84% CAGR in residential installations.

Which region will see the quickest growth to 2031?

South India is forecast to expand at a 12.56% CAGR, propelled by tech-hub investments and early adoption of cloud-based security.

What services model is gaining traction?

Managed security services that bundle monitoring, updates, and analytics are expanding at 12.22% CAGR as firms convert cap-ex to op-ex.

Page last updated on: