India Satellite Communication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

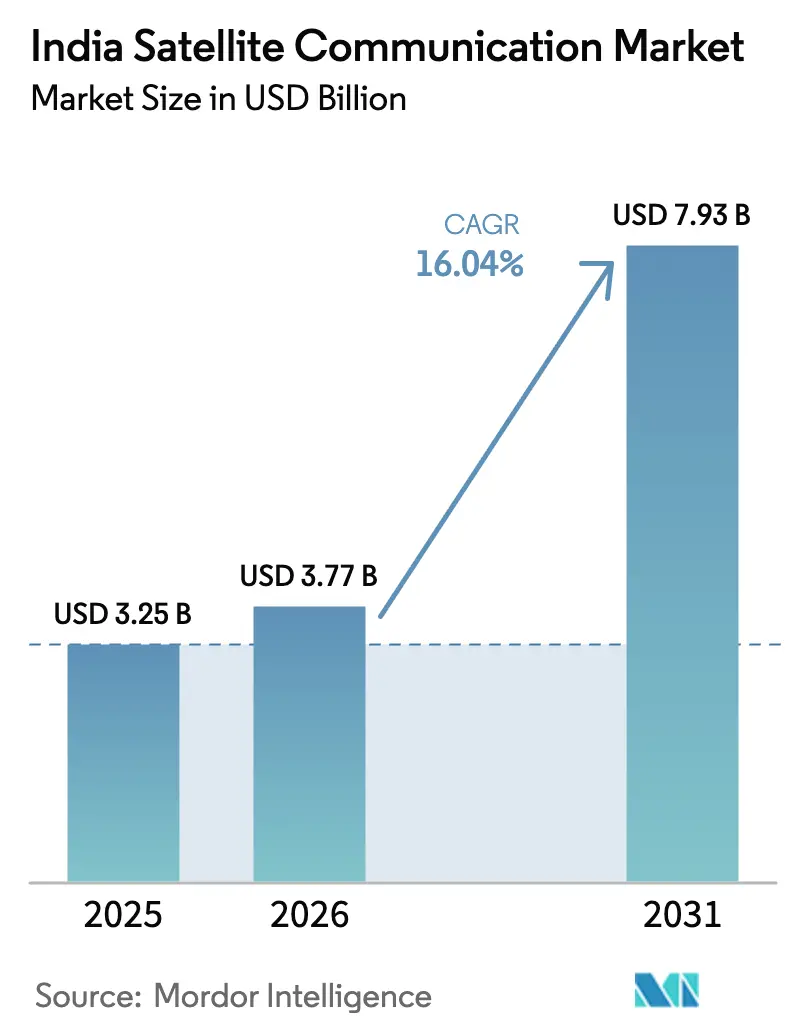

| Base Year Market Size (2025) | USD 3.25 Billion |

| Market Size (2026) | USD 3.77 Billion |

| Market Size (2031) | USD 7.93 Billion |

| Growth Rate (2026 - 2031) | 16.04% CAGR |

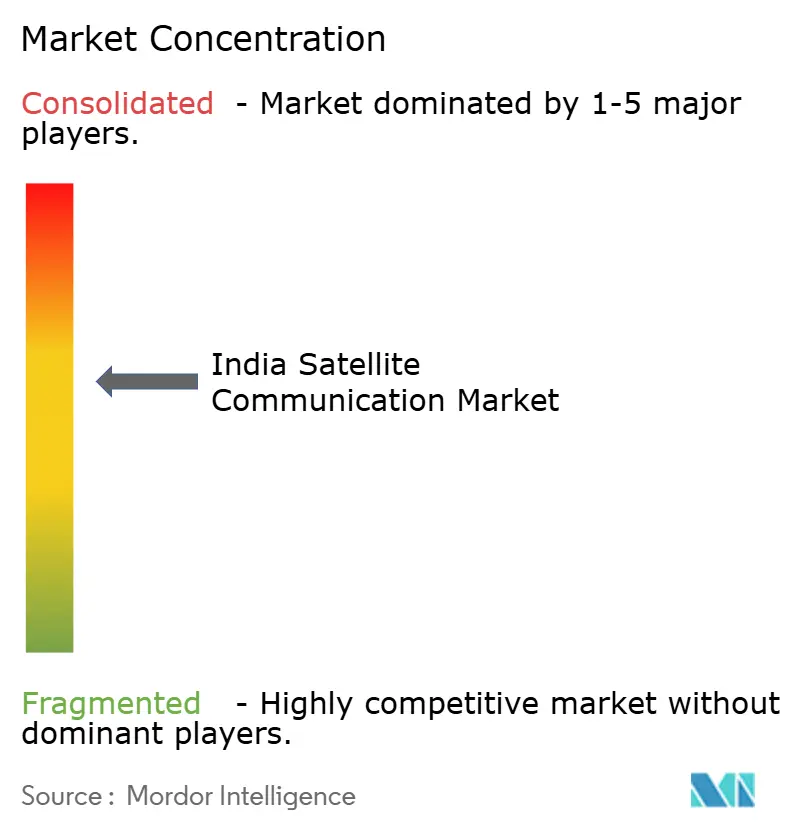

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Satellite Communication Market Analysis by Mordor Intelligence

The India's satellite communication market size is expected to grow from USD 3.25 billion in 2025 to USD 3.77 billion in 2026 and is forecast to reach USD 7.93 billion by 2031 at 16.04% CAGR over 2026-2031. Accelerated growth reflects sustained government investments in rural broadband, rising defense bandwidth needs, and surging demand for video streaming resiliency. Enterprise VSATs underpin banking, retail, and energy operations, while direct-to-device (D2D) concepts promise fresh revenue streams once spectrum approvals materialize. Intensifying competition from global LEO constellations is pushing incumbents toward software-defined networking and hybrid GEO-LEO offerings that lower latency and boost throughput. At the same time, stepped-up security rules and spectrum usage charges tighten margins, compelling operators to pursue high-value managed services and turnkey solutions.

Key Report Takeaways

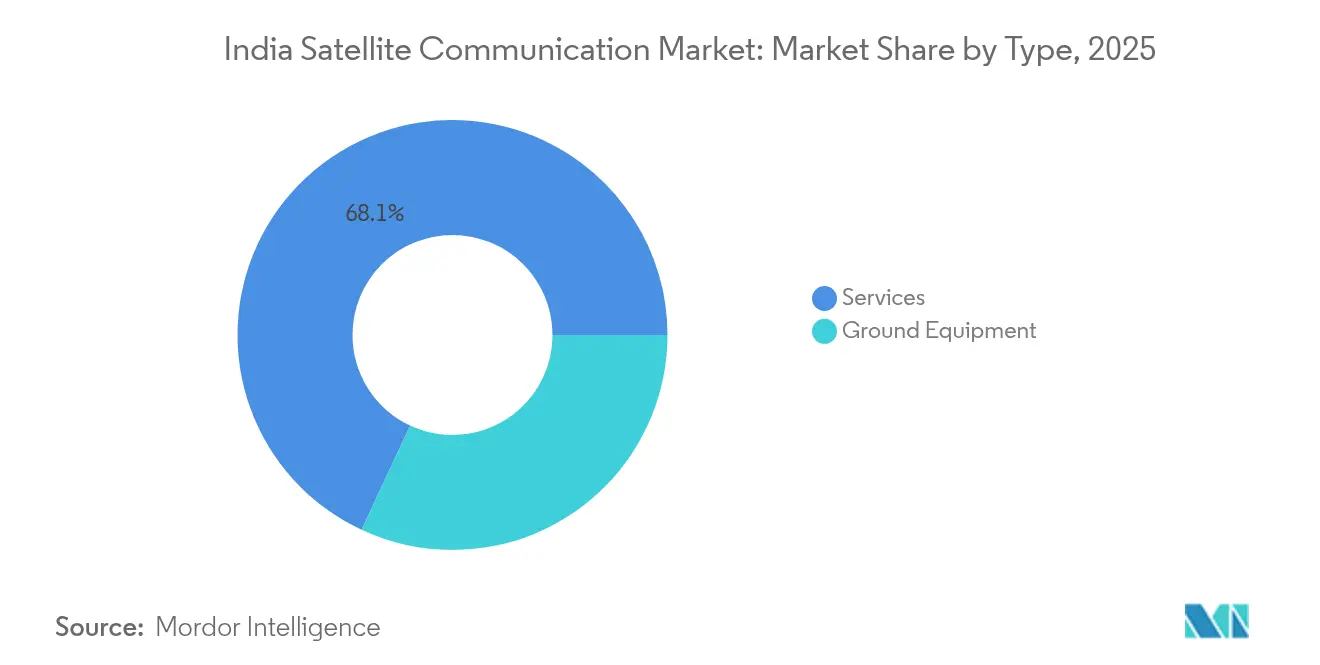

- By type, Services captured 68.05% of India's satellite communication market share in 2025 and are expanding at a 16.72% CAGR through 2031, outpacing all other categories.

- By platform, Airborne platforms are forecast to post the fastest 17.05% CAGR between 2026-2031, while land platforms retained 58.85% revenue share of India's satellite communication market in 2025.

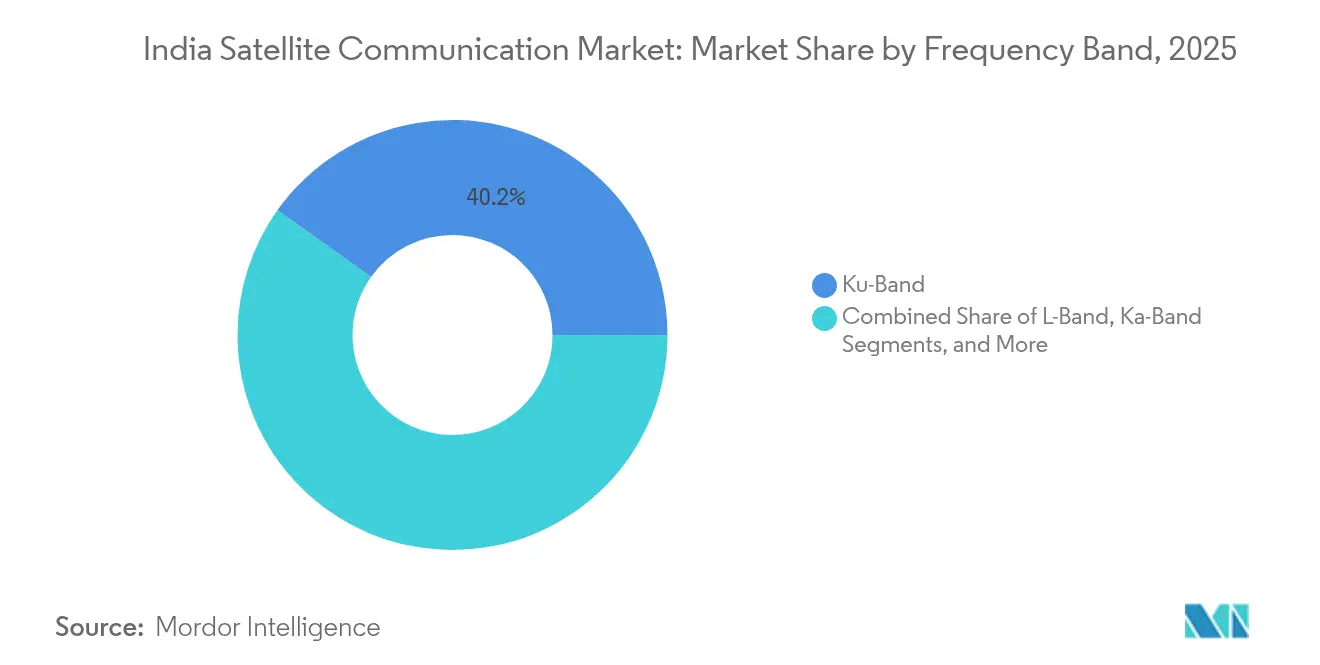

- By frequency band, Ku-band held 40.15% share of India satellite communication market size in 2025; Ka-band is poised to grow at 17.28% CAGR to 2031 on the back of GSAT-20’s 48 Gbps capacity.

- By end-user vertical, Defense and government users commanded 36.78% of the India satellite communication market share in 2025, whereas media and entertainment lead future growth at a 16.96% CAGR.

- By region, South India accounted for 33.85% of India's satellite communication market revenue in 2025; East and North-East India will advance the fastest at 17.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Satellite Communication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BharatNet 3.0 and Digital India broadband roll-outs | +3.2% | National (rural focus) | Long term (≥ 4 years) |

| OTT/video traffic explosion | +2.8% | Urban and Tier-2/3 cities | Medium term (2-4 years) |

| Defense modernization programs | +2.4% | Border and coastal zones | Long term (≥ 4 years) |

| Mass-scale IoT/M2M deployments | +2.1% | Agricultural belts, utilities | Medium term (2-4 years) |

| Direct-to-Device satellite services | +1.9% | Remote low-coverage areas | Medium term (2-4 years) |

| ISRO small-sat launchers | +1.7% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Led BharatNet and Digital India Broadband Roll-Outs

Massive public-sector funding anchors long-term demand. BharatNet 3.0 allocates INR 1.39 lakh crore (USD 16.8 billion) to connect 250 million rural residents, funneling satellite backhaul orders to cover terrain where fiber is infeasible. [1]Economic Times Bureau, “BharatNet 3.0: Cabinet approves Rs 1.39 lakh crore scheme to connect 2.5 crore rural population,” economictimes.indiatimes.com The 5G Intelligent Village pilot in ten states calls for 1 Gbps satellite links with scalable 10 Gbps pathways, positioning satellites as equal partners to terrestrial networks rather than fallback options. Secure gateways mandated by data-localization rules further stimulate domestic ground-segment investments. Together, these policies provide operators with predictable multi-year revenue and underpin the continued expansion of the India satellite communication market.

OTT/Video Traffic Explosion Boosting Satellite Bandwidth Demand

Peak-time video streaming routinely saturates terrestrial backbones. During IPL 2025, concurrent viewership exceeded 32 million, sending spillover traffic to satellite capacity leases. [2]FICCI, “FICCI WAVES 2025 Summit,” ficci.in High-definition 4K and HDR formats multiply per-user data rates, prompting broadcasters to reserve Ka-band beams on GSAT-20 for edge caching in Tier-2 cities. Long-term contracts signed by major streaming platforms create stable utilization rates that lift average revenue per megahertz and enhance the profitability of the India satellite communication market.

Defense and Homeland-Security Modernization Programs

The Indian Army’s Satellite-Based Surveillance (SBS-3) roadmap envisions 52 satellites by 2029, ensuring secure command-and-control across remote theaters. Border outposts now incorporate L-band terminals that ride through jamming episodes, while naval units leverage Ku-band maritime VSATs for real-time ISR feeds. Domestic NewSpace firms like Dhruva Space gain from indigenization mandates that require local bus design and integration facilities in Bengaluru and Hyderabad, broadening the supplier base and reducing import dependence.

Mass-Scale IoT/M2M Roll-Outs in Agriculture and Utilities

Satellite IoT links are projected to grow from 3.6 million to 41 million connections by 2030, powered by precision farming, smart grids, and pipeline monitoring. Heimdall Power’s sensors using Iridium Certus modems already raise transmission-line capacity by 40%, cutting blackout risks. Hybrid LoRa-satellite architectures pioneered by Tata Communications seamlessly switch between cellular and satellite footprints, offering ubiquitous coverage at optimized cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-intrusion and jamming vulnerabilities | -1.8% | Border zones, metros | Short term (≤ 2 years) |

| High CAPEX for gateways/VSAT and spectrum fees | -2.3% | Nationwide | Medium term (2-4 years) |

| Spectrum-allocation delays and regulatory ambiguity | -1.6% | National | Short term (≤ 2 years) |

| New debris-mitigation rules raising costs | -1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Intrusion and Jamming Vulnerabilities

Security audits of NavIC exposed spoofing risks that threaten both civilian logistics and military navigation. Electronic warfare incidents near sensitive borders highlight potential service blackouts, prompting TRAI to mandate end-to-end encryption and two-factor terminal authentication. Compliance adds latency to deployment cycles and inflates opex, moderating near-term uptake.

High CAPEX for Gateways/VSAT and Spectrum Fees

Gateway build-outs run USD 10–50 million each, while spectrum usage charges hover near 3% of adjusted gross revenue, eroding ROI for new entrants. Despite falling VSAT prices, payback periods stretch to seven years for rural tele-education projects, dampening appetite among smaller integrators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Drive Market Evolution

Services commanded 68.05% of 2025 revenue as enterprises favored turnkey bandwidth and network-management contracts over owning hardware. India's satellite communication market size for services is projected to climb at a 16.72% CAGR, fueled by long-term VSAT outsourcing deals in banking and energy. Banks rely on 70,000+ Hughes VSATs for ATM uptime, illustrating how managed capacity assures regulatory service-level targets. OTT platforms and telecoms likewise lease backup Ka-band beams to guarantee 99.9% availability during marquee events.

Ground equipment retained a 31.95% share, yet the category is migrating toward software-defined gateways that remotely re-point beams and load-balance traffic. India's satellite communication market share for equipment suppliers could slide as operators prefer opex-light models, but vendors offset the shift by bundling security, analytics, and orchestration software that deepens integration stickiness.

By Platform: Land Dominance Meets Airborne Innovation

Land platforms held 58.85% revenue in 2025, supported by BSNL’s satellite backhaul roll-outs across 3,500 4G towers in North India. India's satellite communication market size for land-based links will continue growing as state agencies digitize public-service delivery across Panchayats. Portable terminals serve disaster-relief agencies and TV newsgathering units that need high mobility and quick setup.

Airborne systems will grow fastest at 17.05% CAGR as airlines retrofit fleets with Ka-band IFC to meet passenger expectations for streaming video. The Indian Air Force’s iDEX-funded mini-satellites enable beyond-line-of-sight control of UAV swarms, showcasing new high-throughput use cases. Equipment vendors now tailor electronically steered phased-array antennas that fit small fuselage footprints, removing installation hurdles.

By Frequency Band: Ku-Band Legacy Meets Ka-Band Innovation

Ku-band maintains leadership with a 40.15% share owing to the entrenched VSAT base and lower migration costs. Disaster-relief authority NDMA keeps Ku-band sets on standby because of their rain-fade resilience, a critical factor during the monsoon season.

However, India's satellite communication market size for Ka-band capacity will escalate rapidly thanks to GSAT-20’s 48 Gbps payload and 32 spot beams. Smaller dish size and higher throughput make Ka-band attractive for residential broadband and in-flight connectivity, though operators must deploy adaptive modulation to counter rainfall attenuation in coastal belts.

By End-User Vertical: Defense Leadership Amid Media Surge

Defense and government agencies contributed 36.78% of 2025 revenue, cementing their position as anchor tenants for secure bandwidth leases. Ministry of Home Affairs integrated satellite links into border outposts to maintain resilient communications during fiber cuts.

Yet media and entertainment, propelled by OTT expansion, will log the highest 16.96% CAGR as broadcasters secure overflow capacity for live sports streams. Agricultural IoT and smart-grid utilities follow closely, diversifying demand across economic cycles.

Geography Analysis

South India’s 33.85% revenue share stems from a dense supplier ecosystem anchored by ISRO headquarters and private manufacturers like Dhruva Space, which jointly advance component localization. Ports across Tamil Nadu and Kerala use GEO and LEO hybrid terminals to track cargo, while tech firms in Bengaluru demand redundant Ka-band connectivity for cloud workloads. The presence of satellite control centers and skilled aerospace talent sustains innovation and quickens new-service adoption.

West India hosts extensive VSAT deployments supporting Mumbai’s banking sector, where 30,000+ branches and 40,000 ATMs rely on always-on connectivity for real-time settlement. Gujarat’s industrial corridors tap satellite IoT to manage energy pipelines and solar farms across vast desert stretches. Ship-to-shore links at JNPT and Kandla port are now trial multi-orbit services to cut latency for real-time crane operations.

East and North-East India will record the fastest gains at 17.12% CAGR as the government accelerates road, rail, and telecom projects in hilly and border districts. BSNL’s satellite backhaul fills last-mile gaps, while the defense establishment outfits forward posts with secure X-band terminals. Agrarian states in the Indo-Gangetic plain adopt satellite-enabled precision irrigation, using C-band links to mitigate monsoon interference.

Competitive Landscape

The market is moderately concentrated, with the top five players accounting for roughly 55% of 2024 revenue. Hughes Communications India leverages its 70,000-terminal VSAT network and manages centralized network operations centers that small rivals struggle to match. Bharti Airtel deepened integration by securing 100% ownership of OneWeb India and signing distribution rights with SpaceX Starlink, hedging its portfolio with both GEO and LEO capacity. [4]Moneycontrol News, “Bharti Airtel signs pact with SpaceX,” moneycontrol.com Jio entered a similar Starlink pact and is piloting D2D messaging that may broaden its rural footprint once spectrum clearances are finalized.

Foreign operators pursue local gateways to satisfy data-localization rules. Eutelsat OneWeb is completing two Ka-band gateways in Gujarat and Tamil Nadu, while SES seeks JV arrangements to avoid capex duplication. Domestic NewSpace firms target niche constellations: Pixxel focuses on hyperspectral imaging, Astrome on flat-panel antennas, and SatSure on analytics, each aiming for bundled data-connectivity packages that increase switching costs for enterprise clients.

Strategic alliances dominate recent maneuvers. Thales Alenia Space inked a contract with NIBE for a private EO constellation that will ride SSLV, signaling French suppliers’ commitment to Make-in-India frameworks. Meanwhile, gateway equipment providers such as ST Engineering iDirect partner with TCS for software-defined network orchestration, reflecting rising demand for virtualized ground segments.

India Satellite Communication Industry Leaders

Jio Satellite Communications Ltd.

Hughes Communications India Ltd.

Bharti Airtel Limited

Tata Communications Limited

Nelco Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Globalstar sought IN-SPACe licenses for direct-to-cell demonstrations using temporary spectrum.

- March 2025: Bharti Airtel signed a distribution agreement with SpaceX to bring Starlink services nationwide, subject to IN-SPACe and DoT approvals.

- March 2025: Jio Platforms executed a separate Starlink distribution pact aiming to integrate the service with JioFiber and JioAirFiber offerings.

- March 2025: IN-SPACe shortlisted six consortiums, including SatSure-Pixxel-Dhruva Space, for the INR 1,500 crore earth-observation constellation project.

- March 2025: Iridium integrated its Certus 9704 module into Heimdall Power’s line-monitoring sensors, delivering 40% additional grid capacity.

- February 2025: Thales Alenia Space signed a satellite supply contract with NIBE Space for India’s first private EO constellation.

India Satellite Communication Market Report Scope

Satellite communication is the transfer of data and information via satellites orbiting the Earth. It enables long-distance communication by relaying signals between ground stations and satellite receivers in orbit, enabling television broadcasts, internet access, and phone calls. The satellite communication (SATCOM) market is defined based on the revenues generated from the types used in various end-user verticals such as maritime, defense and government, enterprises, and media and entertainment. The analysis is based on the market insights captured through secondary research and the primaries. The report also covers the major factors impacting the market's growth in terms of drivers and restraints.

The scope of the study has been segmented based on the type of satellite communication equipment and services (ground equipment (a gateway, very small aperture terminal (VSAT) equipment, network operation center (NOC), and satellite newsgathering (SNG) equipment) and services (mobile satellite services (MSS), fixed satellite services, and earth observation services), platform (portable, land, maritime, and airborne), and end-user vertical (maritime, defense and government, enterprises, media and entertainment, and other end-user verticals). Common satellite communication services include voice calling and internet access for different applications. The report offers market forecasts and size in value (USD) for all the above segments.

The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, supporting the market estimations and growth rates over the forecast period. In addition, the study provides the SATCOM market trends, along with key vendor profiles. The study further analyzes the overall impact of COVID-19 on the ecosystem.

| Ground Equipment | Gateway |

| Very Small Aperture Terminal (VSAT) | |

| Network Operation Centre (NOC) | |

| Satellite News Gathering (SNG) | |

| Services | Mobile Satellite Services (MSS) |

| Fixed Satellite Services (FSS) | |

| Earth-Observation Services |

| Portable |

| Land |

| Maritime |

| Airborne |

| L-Band |

| S-Band |

| C-Band |

| X-Band |

| Ku-Band |

| Ka-Band |

| Defence and Government |

| Maritime |

| Enterprises |

| Media and Entertainment |

| Agriculture and Environmental Monitoring |

| Other End-user Verticals |

| North India |

| West India |

| South India |

| East and North-East India |

| Central India |

| By Type | Ground Equipment | Gateway |

| Very Small Aperture Terminal (VSAT) | ||

| Network Operation Centre (NOC) | ||

| Satellite News Gathering (SNG) | ||

| Services | Mobile Satellite Services (MSS) | |

| Fixed Satellite Services (FSS) | ||

| Earth-Observation Services | ||

| By Platform | Portable | |

| Land | ||

| Maritime | ||

| Airborne | ||

| By Frequency Band | L-Band | |

| S-Band | ||

| C-Band | ||

| X-Band | ||

| Ku-Band | ||

| Ka-Band | ||

| By End-user Vertical | Defence and Government | |

| Maritime | ||

| Enterprises | ||

| Media and Entertainment | ||

| Agriculture and Environmental Monitoring | ||

| Other End-user Verticals | ||

| By Region | North India | |

| West India | ||

| South India | ||

| East and North-East India | ||

| Central India | ||

Key Questions Answered in the Report

What is the current value of India satellite communication market?

It is valued at USD 3.77 billion in 2026 with projections reaching USD 7.93 billion by 2031.

Which segment holds the largest India satellite communication market share?

Services dominate with 68.05% revenue in 2025, reflecting the preference for managed connectivity solutions.

How fast is Ka-band growing in India’s satcom space?

Ka-band capacity is forecast to rise at a 17.28% CAGR through 2031, driven by high-throughput satellites like GSAT-20.

Which region is expanding the quickest in satellite connectivity?

East and North-East India are projected to grow at 17.12% CAGR, benefiting from border infrastructure projects and tough terrain.

What factor poses the biggest capital hurdle for new entrants?

High gateway and VSAT capex, compounded by spectrum usage fees, lengthens payback periods and limits small-operator entry.

How are telecom operators integrating satellite services?

Companies like Bharti Airtel and Jio are partnering with Starlink and OneWeb to blend GEO and LEO capacity into their fixed-wireless and fiber portfolios.

Page last updated on: