Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.61 Billion |

| Market Size (2031) | USD 11.58 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

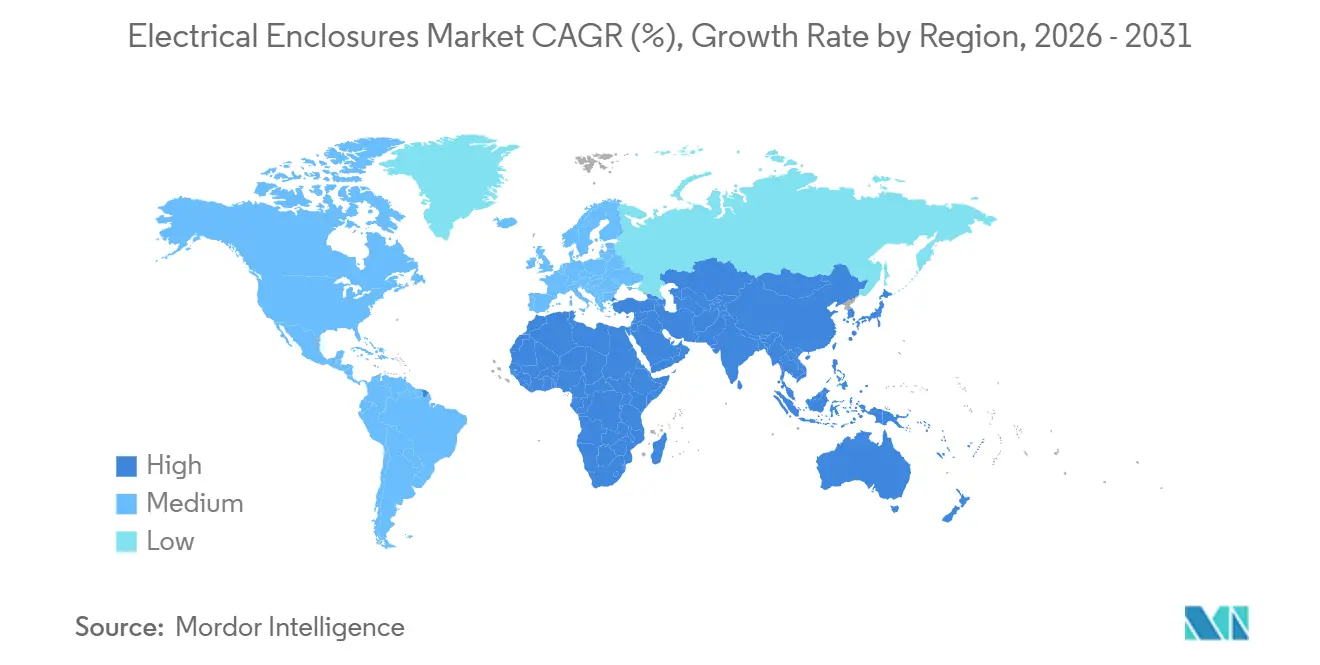

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrical Enclosures Market Analysis by Mordor Intelligence

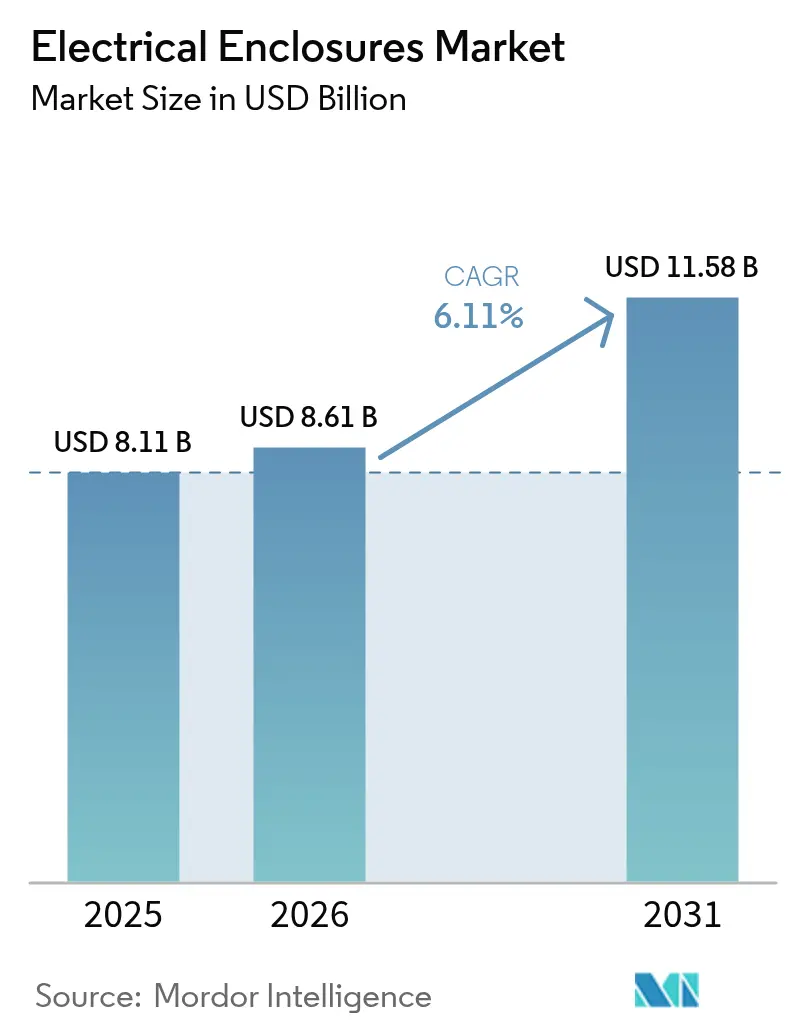

The electrical enclosures market size is expected to increase from USD 8.11 billion in 2025 to USD 8.61 billion in 2026 and reach USD 11.58 billion by 2031, growing at a CAGR of 6.11% over 2026-2031. Strong policy support for renewable generation, rising factory automation, and grid-resilience mandates keep capital flowing toward rugged housings that protect increasingly digital assets. Metallic products continue to dominate because of their structural strength and electromagnetic interference shielding, yet composite alternatives are eroding market share as corrosion-resistant fiberglass and polycarbonate pass stringent salt-spray and chemical-exposure tests. Telecom operators accelerating 5G densification and utilities modernizing substations are standardizing on IP66- and IP67-rated designs, lifting average selling prices even as unit volumes grow. Vendors able to certify to evolving IEC 60529, UL 50E, and IEC 62443 requirements enjoy a widening moat while laggards struggle to fund test-chamber upgrades. The electrical enclosures market thus balances high-volume commodity lines against premium smart cabinets that integrate sensors and edge gateways, creating multiple growth avenues.

Key Report Takeaways

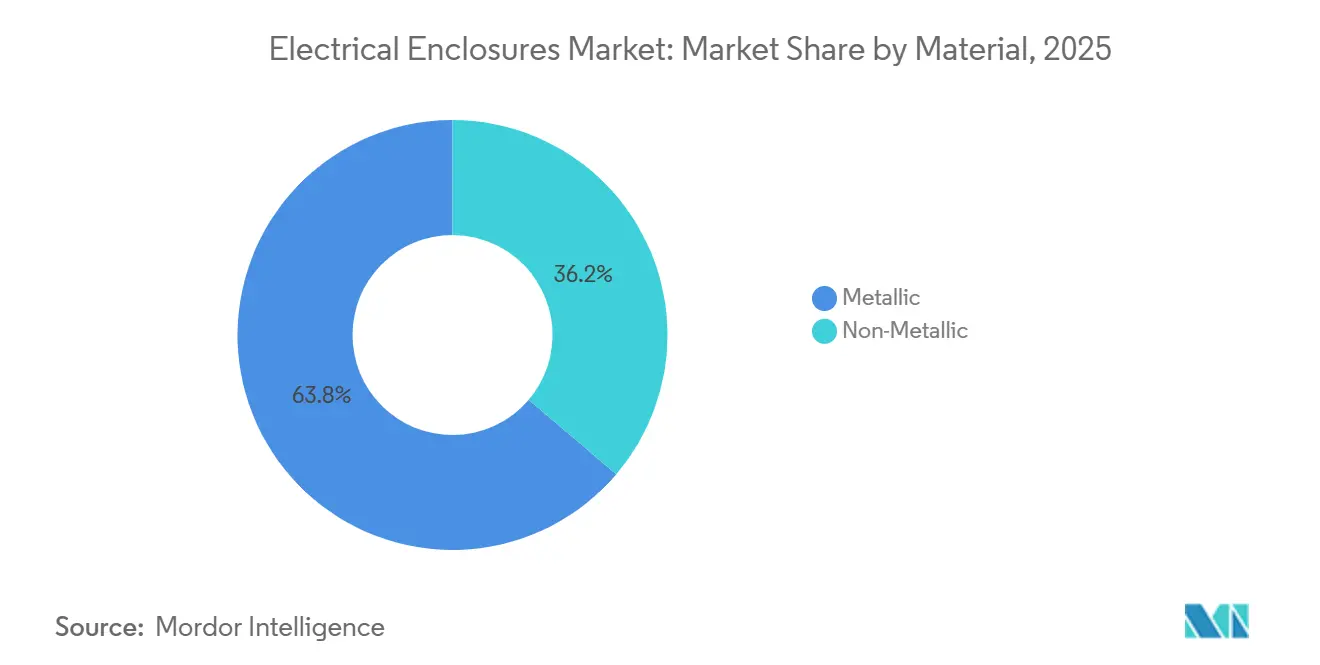

- By material, metallic enclosures led with 63.78% of 2025 revenue, while non-metallic composites are projected to expand at a 6.57% CAGR through 2031.

- By mounting type, wall-mounted units accounted for 43.67% of 2025 shipments, whereas pole-mounted designs are forecast to grow at 6.88% over 2026-2031.

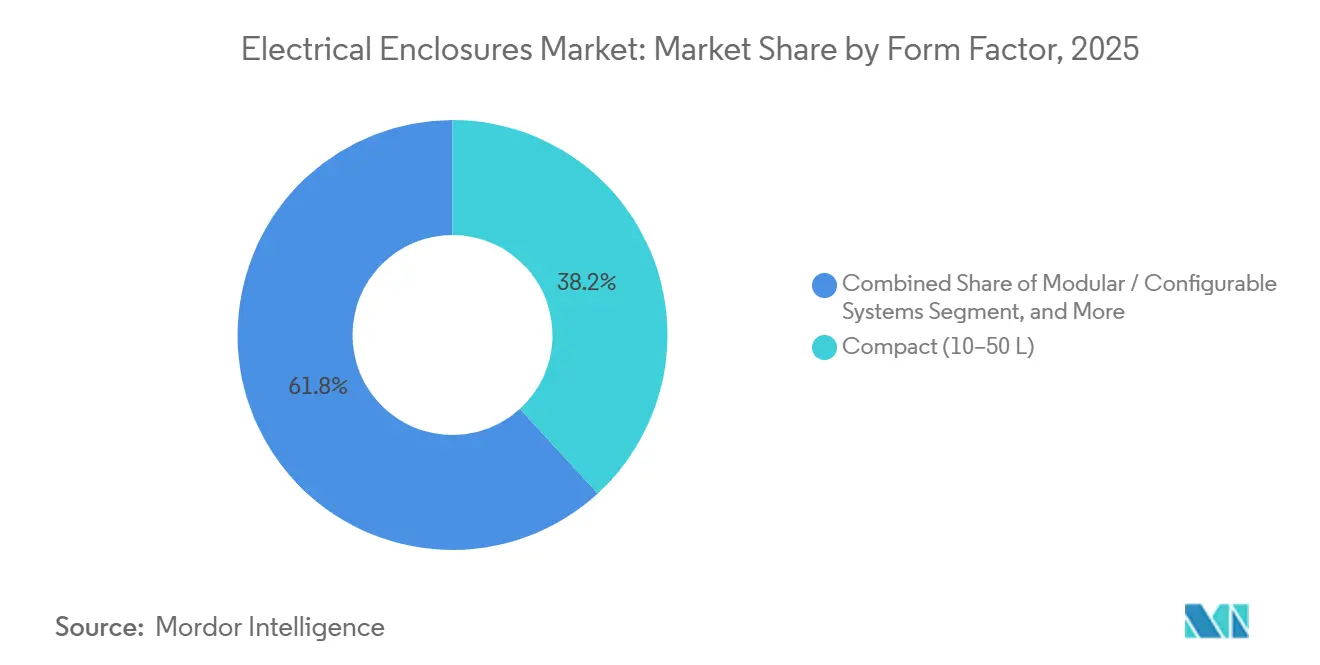

- By form factor, compact 10-50 liter cabinets accounted for 38.19% of the 2025 electrical enclosures market, and modular configurable systems are set to grow at a 6.93% CAGR during the same period.

- By end-user, energy and power applications represented 29.73% of 2025 demand, while data centers and telecom infrastructure are advancing at 7.54% through 2031.

- By geography, Asia Pacific captured 35.67% of 2025 revenue, whereas the Middle East is poised to expand at a 7.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electrical Enclosures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating renewable-energy build-out | +1.2% | Asia Pacific, Europe, Middle East, Global | Medium term (2-4 years) |

| Industrial automation and Industry 4.0 | +1.0% | Asia Pacific, North America, Global | Long term (≥ 4 years) |

| Grid-modernization and substation retrofits | +0.9% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Stricter global safety and ingress codes | +0.7% | Europe, North America, Global | Short term (≤ 2 years) |

| Outdoor 5G small-cell rollout | +0.6% | Asia Pacific, North America, Middle East, Global | Short term (≤ 2 years) |

| Smart IoT-enabled enclosures | +0.5% | North America, Europe, expanding to Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Renewable-Energy Build-Out

Utility-scale solar and offshore wind projects specify IP65 or higher combiner boxes, inverter housings, and transformer kiosks that withstand corrosive spray, ultraviolet radiation, and temperature swings for 25 years.[1]Germany Federal Ministry for Economic Affairs and Climate Action, “Industry 4.0 Funding Programs 2024,” bmwk.de Stainless-steel 316L dominates North Sea farms, while powder-coated aluminum with passive louvers protects equipment in the Arabian Peninsula’s 50 °C heat. Battery-energy-storage systems co-located with solar arrays add a fire-test layer, as UL 9540A certification becomes non-negotiable for bankability. Because renewable capacity is deployed across thousands of micro-sites rather than a few centralized stations, logisticians must orchestrate just-in-time deliveries of smaller, varied enclosure SKUs, pressuring traditional build-to-order plants to embrace modular production.

Industrial Automation and Industry 4.0 Expansion

Factory digitalization programs funded by Germany’s EUR 2 billion (USD 2.26 billion) 2024 grant scheme subsidize sensor networks that each consume five to twenty cabinets per cell.[2]U.S. Department of Energy, “Grid Resilience and Innovation Partnerships Program 2024,” energy.gov Automotive lines in China and Mexico mount collaborative-robot controllers inside IP65 stainless enclosures that prevent electromagnetic interference from servo drives. Food processors prefer sloped-roof, continuous-hinge designs that comply with FDA sanitary codes, while pharmaceutical clean rooms specify polycarbonate windows to enable visual checks without breaching sterile zones. As operational technology integrates with information technology, NEMA TS-2 and IEC 62443 locks, tamper sensors, and intrusion alarms migrate from data centers to plant floors, cementing the electrical enclosures market as a cybersecurity stakeholder.

Grid-Modernization and Substation Retrofits

The United States Department of Energy disbursed USD 3.5 billion in 2024 for wildfire-resilient substations, each outfitted with NEMA 3R cabinets cooled by thermoelectric modules that keep internals below 40 °C during heatwaves.[3]International Energy Agency, “Renewable Energy Market Update – June 2024,” iea.org European networks, scarred by 2023 arc-flash accidents, now retrofit medium-voltage bays with pressure-relief channels to meet IEC 61641 Type 2B requirements. India’s INR 300 billion (USD 3.6 billion) feeder-segregation plan mandates pole-mounted IP54 boxes that deter meter tampering during the monsoon season. Digital relays and synchrophasors shrink form factors, but higher electronic density increases thermal loads, driving demand for cabinets that combine fiber patch panels, convection vents, and arc barriers in a single frame.

Stricter Global Safety and Ingress-Protection Codes

The European Union’s 2024 update to the Low Voltage Directive obliges accredited lab testing before a CE mark may appear on any housing, elevating certification costs and discouraging fly-by-night entrants. NFPA 70E revisions in the same year require arc-rated enclosures above 240 V, affecting more than one million U.S. installations. China’s harmonization of GB 4208 with IEC 60529 now sets IP65 as the national outdoor minimum, banning legacy foam-gasket boxes. UL 50E adds a 1,000-hour salt-spray exposure for corrosive settings, tilting project awards toward vendors with stainless or fiberglass lines. Collectively, these rules funnel volume toward suppliers that maintain in-house chambers and third-party audit pipelines, entrenching the top tier of the electrical enclosures market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.8% | Asia Pacific, Europe, Global | Short term (≤ 2 years) |

| Seal-integrity and thermal-management issues | -0.4% | Middle East, Africa, tropical Asia, Global | Medium term (2-4 years) |

| Cyber-attack risk in connected cabinets | -0.3% | North America, Europe, advanced Asia Pacific | Long term (≥ 4 years) |

| Skilled-labor shortage for customization | -0.3% | North America, Europe, emerging Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

London Metal Exchange aluminum contracts fluctuated 10% intra-year during 2024, eroding margins for enclosure makers that operate on 8-12% net spreads. Chinese cold-rolled steel soared when blast-furnace curbs coincided with unexpected iron-ore outages, forcing contract renegotiations or losses for fabricators tied to fixed-price purchase orders. Stainless-steel surcharges linked to nickel and molybdenum spiked 15-20%, stalling offshore wind substation awards. Buyers now write commodity-index clauses into tenders, but the administrative burden complicates procurement and forecasting in the electrical enclosures industry.

Cyber-Attack Risk in Connected Enclosures

CISA reported 87 cyber-intrusion attempts against industrial control systems in 2024, a dozen of which exploited vulnerabilities inside IoT-enabled housings. A ransomware incident that forced manual operation of 45 European substations underscored the cascading risk of firmware compromise. IEC 62443-4-2 demands encrypted links and role-based controls for any cabinet with a network interface, yet retrofits lag due to cost. Builders are embedding trusted-platform modules that add USD 50-150 per unit, but utilities sometimes turn off radios altogether, sacrificing remote diagnostics to mitigate breach exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Composites Challenge Metallic Dominance

Metallic units accounted for 63.78% of the electrical enclosures market share in 2025, reflecting cold-rolled steel’s price advantage and aluminum’s weight savings for pole-top gear. Non-metallic cabinets are expected to grow 6.57% annually through 2031 as offshore wind, coastal substations, and chemical plants shift toward fiberglass-reinforced polyester, which shows no rust after 3,000 hours of ASTM B117 salt spray testing. Polycarbonate lids dominate clean rooms where technicians need visual confirmation without breaking the sterile boundary.

Hybrid designs are multiplying: steel frames with polycarbonate doors or aluminum backplates balance cost, grounding, and corrosion resistance. Stainless-steel 316L still owns hazardous zones, meeting NEMA 4X and IP66 while resisting acid and chlorine attack. Meanwhile, carbon steel with epoxy coatings remains the indoor workhorse, but as composite costs fall and flame-retardant ratings reach UL 94 V-0, even factories are questioning legacy metal spend. The electrical enclosures market thus moves toward a mixed-material toolkit tailored to the environment and lifecycle economics.

By Mounting Type: Pole-Mounted Gains Traction in 5G and Grid Edge

Wall-mounted boxes delivered 43.67% of 2025 shipments, anchoring control rooms and machine cells where vertical real estate is cheap. Pole-mounted designs are forecast to expand 6.88% through 2031 as telecom operators add tens of thousands of 5G small cells, each requiring IP65-rated housings for rectifiers, splice trays, and backup batteries. Distribution utilities also retrofit auto-reclosers and fault indicators on overhead feeders, cutting rural outage minutes by 40%.

Pad-mounted and underground units serve urban aesthetics and public-safety rules, hiding transformers out of view while resisting soil moisture and rodent ingress. Floor-standing cabinets remain in heavy-industry motor centers and server rooms where cable depth matters. The outward shift in generation, sensing, and compute power is pushing the electrical enclosures market toward smaller, resilient pole-top shells that must withstand wind and lightning, while wall-mounts will persist in climatized interiors.

By Form Factor: Modular Systems Reshape Scalability

Compact 10-50 liter cabinets captured 38.19% of the 2025 electrical enclosures market size, dotting every conveyor, pump, and robot arm on a shop floor. Modular configurable systems, however, are on pace for a 6.93% CAGR through 2031 as plants chase tool-free expansion. Rittal’s TS 8 frame snaps together without welding, trimming assembly labor by 60% and allowing hot-swap side panels for future cable runs.

Small housings below 10 liters power PV optimizers and smart-building sensors, while free-size walk-in shelters above 50 liters protect substation switchgear and telecom core nodes. Value is migrating toward modularity: buyers pay 20-30% premiums for rails, busbars, and fan trays that can be reconfigured over decades. Compact boxes keep the unit-count crown, but revenue will skew toward higher-priced platform cabinets as the electrical enclosures market monetizes lifecycle adaptability.

By End-User Industry: Data Centers and Telecom Outpace Legacy Verticals

Energy and power contributed 29.73% of 2025 demand, spanning IP66 inverter kiosks, arc-resistant switchgear, and UL 9540A battery racks. Hyperscale clouds expanded their footprint in 2024 by adding 120 facilities, each outfitted with 500 to 1,000 racks featuring integrated sensors and liquid-cooled coil doors. As a result, data centers and telecoms are projected to achieve a CAGR of 7.54% through 2031.

Industrial manufacturing, mining, and transport lines still absorb roughly one-third of units, from IP65 robot controllers to EV-charging pedestals. Oil and gas prefer NEMA 4X aluminum around wellheads, though capital is pivoting to hydrogen and carbon-capture projects that need similar enclosures. Food and beverage, plus pharma, require stainless wash-down models under FDA rules. As digital traffic surges, the electrical enclosures market is increasingly serving servers and radio heads rather than just transformers and motors.

Geography Analysis

Asia Pacific generated 35.67% of 2025 revenue, buoyed by China’s CNY 520 billion (USD 73 billion) grid spend that deployed 1.8 million smart meters and 12,000 automated feeder switches, all nestled inside dust-tight housings. India’s INR 300 billion (USD 3.6 billion) revamp funds tamper-proof polycarbonate meter boxes resilient against monsoon splash. Japan and South Korea retrofit nuclear and coal controls into seismic-rated cabinets that sustain magnitude-7 shocks. Southeast Asian data-center approvals in Singapore reached 400 MW in 2024, translating to roughly 18,000 rack enclosures with rear-door heat exchangers. The electrical enclosures market thus tracks the region’s dual energy and digital build-out.

The Middle East is projected to grow 7.13% through 2031. Saudi Arabia’s NEOM program alone will need about 80,000 inverter and transformer housings suited for 50 °C air laden with sand. The UAE’s Barakah plant specified 12,000 stainless cabinets with arc venting, setting a high bar for nuclear projects. Qatar’s North Field LNG expansion ordered 5,000 explosion-proof shells for Zone 1. Across the Persian Gulf, desert resilience drives stainless or powder-coated aluminum spend, stretching average order values in the electrical enclosures market.

North America and Europe together hold roughly 45% of global sales. The U.S. Grid Resilience program finances NEMA 3R outdoor cabinets with solid-state coolers to mitigate the impacts of wildfires and hurricanes. Europe’s Energiewende funnels EUR 1.8 billion (USD 2.03 billion) into IP67 subsea junction and converter housings for offshore wind. Replacement cycles lengthen in these mature zones, but stricter arc-flash and cybersecurity standards sustain a steady retrofit cadence. Consequently, while growth moderates, specification complexity keeps margins healthy for established vendors in the electrical enclosures market.

Regulatory Landscape

Electrical enclosures are shaped by safety, ingress, EMC, and market-access rules that affect design validation and total cost. In the United States, UL and NFPA requirements influence enclosure construction and labeling, with UL 50E referenced in procurement for corrosive and outdoor use, and 2025 UL 508A revisions tightening industrial control panel enclosure practices (including segregation to reduce leakage contact risk with live parts). In Europe, CE-marking pathways are reinforced by the EU Low Voltage Directive update in 2024, which raises the bar for accredited lab testing and documentation for housings sold into EU channels.

Compliance requirements are also getting more prescriptive for grid edge, telecom, and storage. India has multiple layers: MeitY issued an amendment (S.O. 1246(E)) that becomes effective 15 June 2026, updating exemption criteria for Highly Specialized Equipment under BIS CRS processes and affecting how some specialized enclosure-integrated systems are imported; and India’s Central Electricity Authority notified Technical Standards Amendment Regulations (2026) with an effective date of 1 April 2027, adding construction and fire-safety/segregation expectations relevant to BESS enclosures. In South Korea, KATS communicated an EMC compliance roadmap accelerating alignment toward IEC 61000-4-30:2025 Class A accuracy, with enforcement tied to 1 January 2027 for covered equipment categories, increasing the test and documentation workload for enclosure solutions that integrate signal barriers or metering functions.

Value Chain Analysis

The electrical enclosures value chain begins with raw materials (carbon steel, stainless steel, aluminum, fiberglass-reinforced polyester, polycarbonate) and purchased components such as gaskets, locks, hinges, mounting plates, and thermal-management accessories. It then moves through engineering and configuration (CAD, sizing, IP/NEMA selection, and, increasingly, cybersecurity and connectivity requirements for smart cabinets), followed by fabrication processes including laser cutting/punching, bending, welding or fastening, machining, and surface finishing (powder coating, passivation, or other corrosion-protection steps). The final steps cover assembly (doors, seals, internal rails, busbars, fans/heat exchangers, and sensors/gateways where applicable), testing and certification to standards such as IEC 60529, NEMA types, and UL 50E/UL 508A-related build requirements, then packaging and logistics to EPCs, panel builders, utilities, OEMs, and data center integrators.

Value capture increasingly depends on customization speed and compliance readiness. Global vendors and regional fabricators balance build-to-stock commodity boxes with build-to-order projects for renewables, substations, and telecom, where documentation, salt-spray performance, and thermal validation are bid prerequisites. Capacity additions and portfolio expansions, such as ABB expanding its EH3 outdoor GRP lineup and introducing CombiLine MP interior fittings for distribution applications, show a push toward modular interior architectures that reduce field labor and standardize BOMs for installers. Supply chain risk management, including dual-sourcing metals and polymers, expanding regional finishing capacity, and ensuring validated test-chamber access, has become a differentiator as projects demand shorter lead times and proof of compliance across IP/NEMA, EMC, and sector-specific requirements.

Competitive Landscape

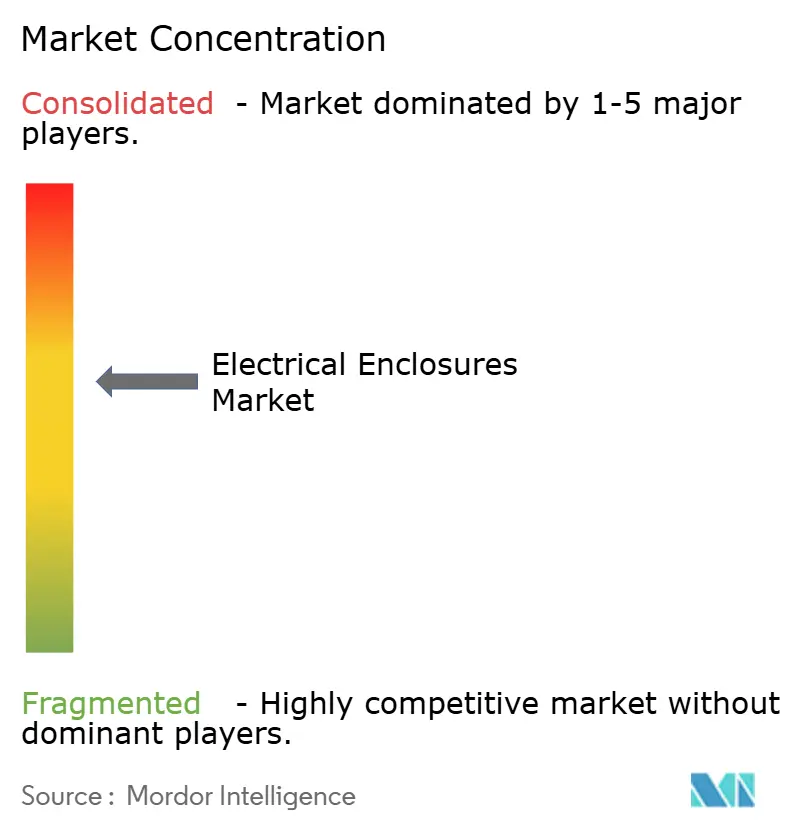

Roughly 48-52% of 2025 revenue was accounted for by the top ten vendors, giving the electrical enclosures market a moderate level of concentration. Schneider Electric’s 2023 integration of AVEVA software bundles edge gateways into cabinets, locking clients into analytics subscriptions. Rittal’s 2024 TS 8 launch reduced commissioning time, helping it win orders from automakers facing skilled-labor shortages. ABB patented a phase-change cooling wall that dissipates heat without vents, a boon for dusty mines.

Regional fabricators such as Hammond Manufacturing and Allied Moulded carve niches with five-day custom builds against global lead times of a month. nVent’s 2024 Trachte buyout boosted its footprint in utility shelters, while Eaton’s UL 50E certification positions it for corrosive offshore work. Pentair and Legrand drill into water treatment and AI-laden server racks, respectively, demonstrating vertical specialization.

Emerging disruptors leverage additive manufacturing to produce low-volume, high-complexity geometries that sheet-metal brakes cannot economically match. Meanwhile, smart enclosures with vibration and humidity sensors transition from pilots to procurement catalogs, slowly shifting revenue from once-off hardware to recurring monitoring fees. The electrical enclosures industry, therefore, balances scale economics with customization speed, with digital services as the next battleground.

Electrical Enclosures Industry Leaders

Schneider Electric SE

ABB Ltd.

Emerson Electric Company

Hubbell Incorporated

Legrand SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity areas are most visible where enclosure specifications are shifting from basic protection toward higher-function, validated systems. One clear whitespace is outdoor GRP/composite platforms with modular interior architectures that simplify configuration for distribution and infrastructure builds. ABB’s March-April 2026 expansion of its EH3 outdoor enclosure portfolio, including a taller 1,310 mm option, and its launch of the CombiLine MP interior fitting system for distribution applications up to 440 A signals vendor focus on standardized outdoor cabinets designed for scalable rollout rather than one-off builds. This direction supports utilities, renewables, and edge deployments that need corrosion resistance, repeatable layouts, and faster commissioning, while still aligning with procurement preferences for documented compliance (IEC 60529/IP, UL 50E for corrosive environments, and relevant national rules).

Another opportunity comes from enclosure designs that handle heat, weight, and serviceability constraints created by densification in data centers and telecom. Schneider Electric’s June 2025 data center solution releases, including NetShelter SX Advanced Enclosure capabilities aimed at high-density AI and liquid-cooling configurations, point to a shift toward racks and cabinets built to carry higher loads and support thermal-management requirements. At the same time, regulatory and standards tightening supports demand for suppliers that can bundle product, documentation, and test evidence across jurisdictions, including India’s evolving import/compliance pathways (MeitY BIS CRS-related exemptions effective 15 June 2026) and upcoming CEA technical standard amendments effective 1 April 2027 that raise the engineering bar for storage-related enclosures. Together, these factors support premiumization through certified corrosion resistance, EMC/ingress validation, modular interiors, and digitally enabled service workflows (including configuration tools and field-accessible documentation) that reduce downtime and audit friction for end users.

Recent Industry Developments

- April 2026: ABB expanded its EH3 outdoor GRP enclosure portfolio and introduced the CombiLine MP interior fitting system at Light + Building 2026. The move strengthens ABB’s position in standardized outdoor distribution and infrastructure cabinets by pairing weather-resistant housings with a modular interior ecosystem that can be configured faster in the field.

- June 2025: ABB Electrification Canada Inc. acquired Bel Products Inc., a North American manufacturer of custom industrial and utility enclosures. The acquisition adds regional customization capacity and broadens ABB’s enclosure offering for utility and industrial customers that require short lead times and application-specific builds.

- June 2024: Schneider Electric released the NetShelter SX Gen2 enclosure range targeting higher-weight IT and high-performance computing deployments. This upgrade supports data center operators as rack loads and thermal constraints increase, pushing enclosure selection toward designs engineered for denser equipment and more demanding cooling architectures.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of electrical enclosures used to house and protect electrical and electronic equipment across indoor and outdoor installations, including common material and mounting formats sold into industrial, infrastructure, and building end uses.

Scope exclusions: We exclude unrelated electrical components and accessories that are not sold as part of an enclosure assembly (for example, stand-alone breakers, meters, and wiring devices).

Segmentation Overview

- By Material

- Metallic

- Non-Metallic

- By Mounting Type

- Wall-Mounted

- Floor-Mounted / Free-Standing

- Underground / Pad-Mounted

- Pole-Mounted

- By Form Factor

- Small (Below 10 L)

- Compact (10–50 L)

- Free-Size / Full-Size (Above 50 L)

- Modular / Configurable Systems

- By End-User Industry

- Energy and Power

- Oil and Gas

- Industrial Manufacturing and Robotics

- Metals and Mining

- Transportation

- Data Centres and Telecom

- Food and Beverage

- Pharmaceuticals

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the model structure and anchor it to observable market signals, before finalizing assumptions. We mainly relied on public sources that show how quickly electrification and industrial activity are moving, and how protective equipment demand tends to follow.

Typical inputs came from sources such as US Energy Information Administration releases, International Energy Agency statistics, US Census Bureau manufacturing data, UN Comtrade trade flows for relevant product codes, and electrical safety and standards bodies such as IEC and NEMA for protection and compliance context. Alongside this, company annual reports, investor decks, and reputed press were used to understand product mix changes, pricing posture, and capacity expansions. We then used paid subscription sources for company financials and a paid patent database selectively to cross-check innovation intensity and supplier scale. These examples are illustrative, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the demand pool and keep the sizing grounded in what buyers and suppliers are seeing in real orders. We spoke with a mix of enclosure manufacturers, distributors, panel builders, and end-user procurement and engineering teams across major regions, so gaps from desk research could be filled and assumptions on mix, pricing, and replacement demand could be aligned to what is actually getting quoted and installed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 13% | APAC: 41% |

| Mid tier: 45% | Functional/Unit leaders: 27% | EMEA: 32% |

| Smaller Players: 17% | Managers: 60% | Americas: 27% |

Market-Sizing & Forecasting

Sizing started from a top-down build where industrial output, grid and renewable build-out activity, and construction and automation spending were used to reconstruct the likely enclosure demand pool by region, then map it to enclosure mix. To keep the result grounded, we corroborated totals with selective bottom-up checks, such as sampling average selling prices by material and protection level, and pairing them with plausible shipment and project volumes from channel feedback.

Key inputs tracked included industrial production indices, utility and generation capacity additions, data center and telecom rollout intensity, and oil and gas project cycles, plus the split between indoor and outdoor installations that drives protection requirements. Product-level assumptions also reflected the mix shift between metallic and non-metallic formats, common mounting choices, and typical upgrade or replacement timing in harsh environments. Forecasting leaned on scenario analysis built around these drivers, and the final growth path was aligned to the consensus range shared by interviewees for near-term backlog and mid-term capex plans. Where bottom-up visibility was thin in smaller countries, we used proxy relationships tied to industrial and power infrastructure indicators, then adjusted the results after expert review.

Data Validation & Update Cycle

Model outputs were triangulated against independent signals, including trade movement patterns, supplier commentary on backlog and lead times, and implied spend per project type, and then variances were investigated before sign-off. If a segment result looked inconsistent with known installation cycles or recent pricing direction, the assumptions were reopened and clarified through follow-up calls.

A second analyst review was applied to check math, scope boundaries, and the logic linking drivers to demand, and only then were the numbers locked for publication. Reports are refreshed annually, with interim updates triggered by material events such as large policy changes, sharp commodity-driven pricing swings, or major capacity announcements. A final pre-delivery pass is completed so clients receive the latest view.

Mordor Intelligence's Electrical Enclosures Market Size Versus Other Published Estimates

Published market sizes for electrical enclosures often do not match because the boundary of what gets counted can shift in small but meaningful ways. The biggest differences usually come from whether the estimate is tracking enclosure shipments only, factory-gate revenue, or a wider bundle that can include related assembly work and channel markups.

Trade flows for relevant enclosure categories, combined with cross-checks on end-use build activity in power, manufacturing, and data centers, are the evidence used to keep Mordor Intelligence's estimate aligned to enclosure demand rather than broader electrical equipment value. Differences also show up when one study uses a faster price uplift for stainless steel and outdoor-rated units, or when the refresh cadence lags and does not capture recent project timing changes and mix shifts between metallic and non-metallic enclosures.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.11 B (2025) | |

| Industry Research Group A | USD 7.83 B (2025) | Uses a narrower definition that can undercount higher-spec outdoor and industrial formats, and it may apply a more conservative price progression for higher-grade materials in the base year. |

| Global Publisher B | USD 8.89 B (2025) | Uses a factory-gate framing that can include some services bundled with manufactured goods, which can lift value versus a scope focused strictly on enclosure products sold into end uses. |

Taken together, the spread in values is mostly explained by what is included at the boundary and how pricing and mix are treated in the base year. By keeping assumptions tied to visible demand drivers and then rechecking them through supplier and buyer feedback, the sizing stays transparent and repeatable for planning.

Key Questions Answered in the Report

What is the forecast value of the electrical enclosures market by 2031?

The market is projected to reach USD 11.58 billion by 2031, expanding at a 6.11% CAGR over 2026-2031.

Which material segment is growing fastest?

Non-metallic composites, especially fiberglass-reinforced polyester and polycarbonate, are expected to grow 6.57% annually through 2031.

Why are pole-mounted enclosures gaining popularity?

5G small-cell rollouts and distribution-automation programs place equipment on utility poles, driving a 6.88% CAGR for pole-mounted cabinets.

Which end-user vertical shows the highest growth?

Data centers and telecom infrastructure lead with a 7.54% CAGR as hyperscalers and edge facilities expand worldwide.

How do stricter safety codes affect suppliers?

Updated IEC, UL, and NFPA standards increase certification costs, favoring established vendors with in-house test labs and raising entry barriers.

What is the market concentration level?

The top ten players account for roughly half of global revenue, indicating moderate concentration in this sector.

Page last updated on: