Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

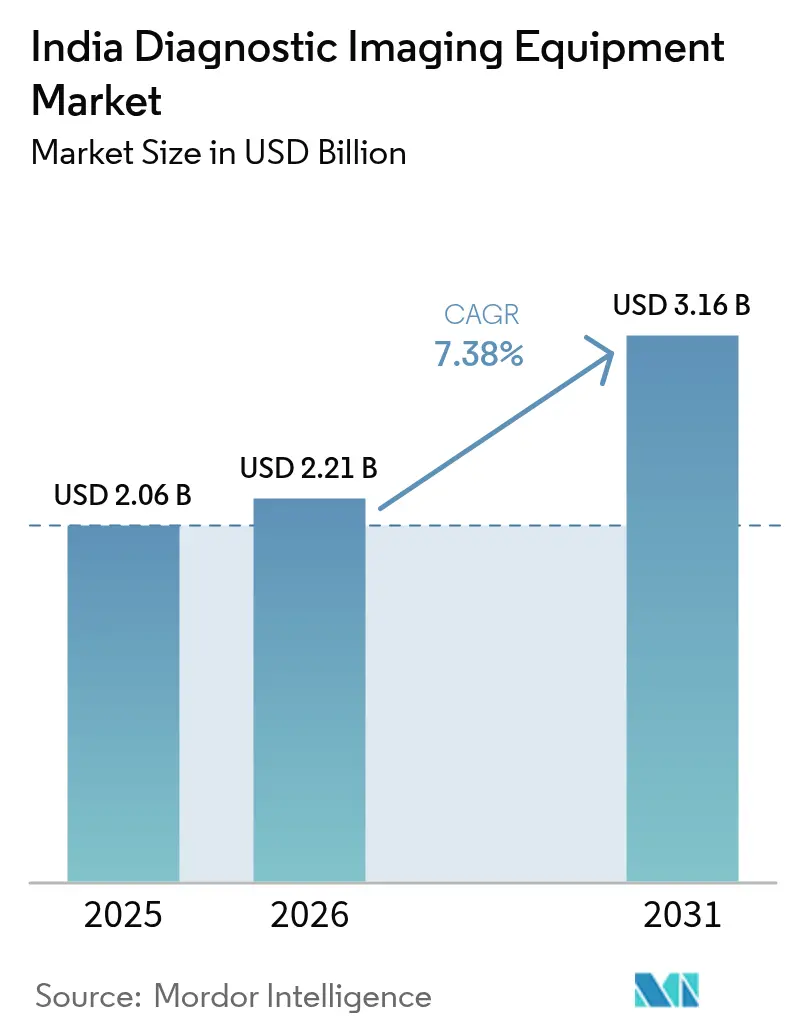

| Base Year Market Size (2025) | USD 2.06 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 3.16 Billion |

| Growth Rate (2026 - 2031) | 7.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

The India Diagnostic Imaging Equipment Market size was valued at USD 2.06 billion in 2025 and estimated to grow from USD 2.21 billion in 2026 to reach USD 3.16 billion by 2031, at a CAGR of 7.38% during the forecast period (2026-2031). This growth trajectory reflects the country's shift toward self-reliance under the Production Linked Incentive scheme, which has funded 19 greenfield plants that now manufacture MRI scanners, CT systems, and other devices previously imported.[1]Source: Press Information Bureau, “PLI scheme incentivizes domestic manufacturing, increases production, creates new jobs and boosts exports,” pib.gov.in Indigenous innovation, including India’s first home-grown 1.5 T MRI scanner expected to cut examination costs by 30-50%, is lowering barriers to advanced imaging adoption. Demand is reinforced by an epidemiological transition marked by rising chronic disease prevalence, an expanding elderly cohort, and a national insurance push that is enlarging the reimbursable diagnostic pool. Meanwhile, multinational vendors are doubling down on AI-enhanced platforms and sealed-helium magnets, while domestic firms leverage cost advantages and policy incentives to challenge incumbents.

Key Report Takeaways

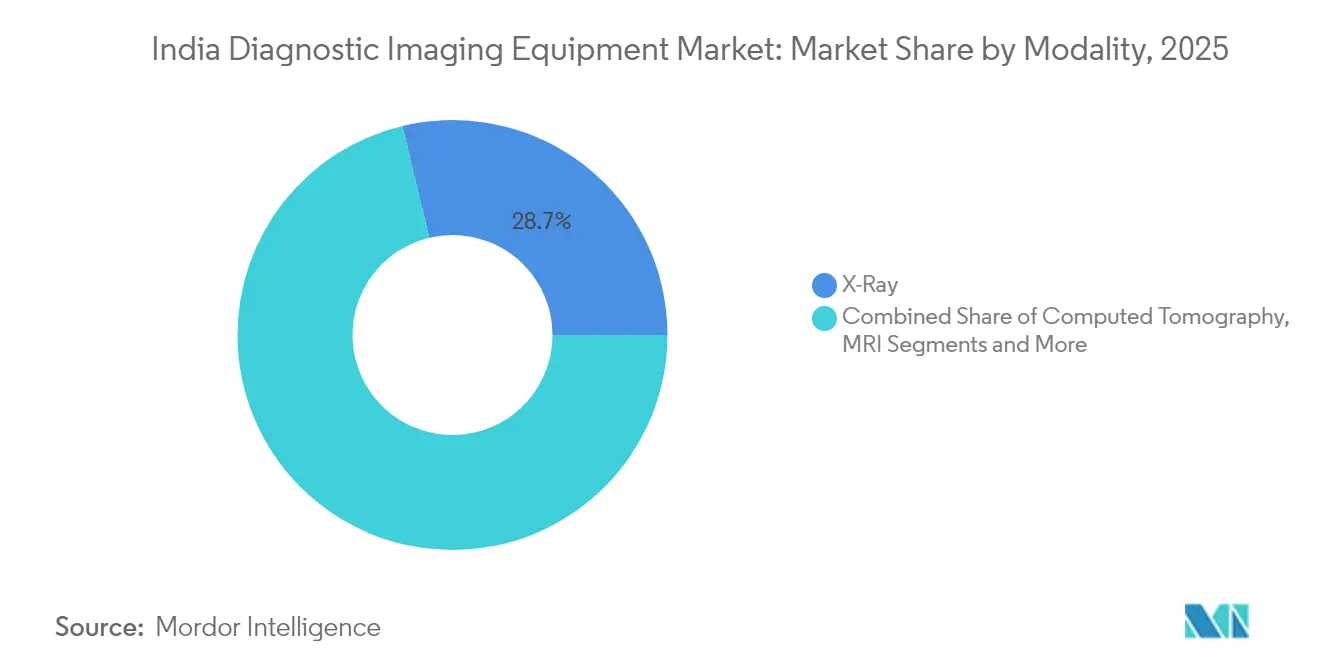

- By modality, X-ray systems led with 28.74% of the India diagnostic imaging equipment market share in 2025, whereas computed tomography is forecast to expand at an 8.62% CAGR through 2031.

- By portability, fixed installations accounted for 82.05% of the India diagnostic imaging equipment market size in 2025, while mobile and handheld systems are set to grow at an 7.86% CAGR to 2031.

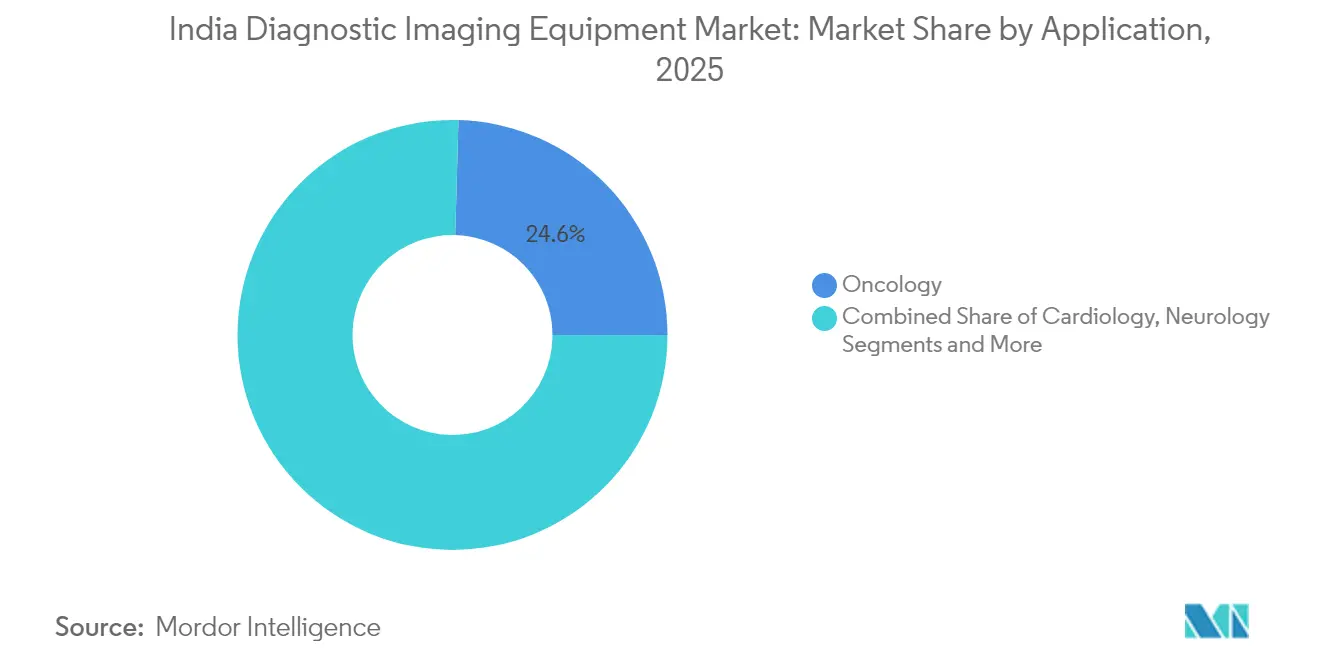

- By application, oncology captured 24.56% revenue share of the India diagnostic imaging equipment market in 2025 and cardiology is advancing at an 8.47% CAGR through 2031.

- By end user, hospitals held 65.42% share of the India diagnostic imaging equipment market size in 2025, whereas diagnostic imaging centers record the highest projected CAGR at 7.74% during 2026-2031.

- South India commanded 29.12% of the India diagnostic imaging equipment market share in 2025; North India shows the fastest regional CAGR of 8.72% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Prevalence of Chronic Diseases | +1.2% | National, with higher concentration in urban areas | Long term (≥ 4 years) |

| Growing Geriatric Population | +0.9% | National, with early gains in South India, West India | Long term (≥ 4 years) |

| Increased Adoption of Advanced Imaging Technologies | +1.5% | Metro cities and Tier-1 locations, expanding to Tier-2 | Medium term (2-4 years) |

| Government Insurance & PPP Thrust on Diagnostics | +1.1% | National, with focus on rural and underserved areas | Medium term (2-4 years) |

| Expansion of Teleradiology & Cloud-Based PACS in Tier-2/3 Cities | +0.8% | Tier-2 and Tier-3 cities, rural healthcare networks | Short term (≤ 2 years) |

| Production-Linked-Incentive (PLI) Scheme Boosting Local Manufacture | +1.3% | Manufacturing hubs in Karnataka, Tamil Nadu, Gujarat | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Chronic Diseases

Diabetes now affects 11.4% of Indian adults, while hypertension touches 35.5%, and cancer incidence is forecast to increase to 549 per 100,000 inhabitants by 2031.[2]Source: Ranjit Mohan Anjana et al., “Metabolic non-communicable disease health report of India,” thelancet.com These numbers translate into sustained need for CT angiography, multiphase MRI, and PET-CT workflows capable of detecting early lesions and monitoring therapy response. Providers are shifting from single-modality rooms to integrated suites that streamline oncologic and cardiometabolic pathways, accelerating capital expenditure on high-slice CT and 3 T MRI. Gender-specific imaging protocols are emerging as women above 60 years show higher non-communicable disease prevalence, influencing scanner throughput planning and coil inventory. The chronic disease surge is therefore rewiring procurement decisions across the India diagnostic imaging equipment market.

Growing Geriatric Population

The number of Indians aged 60 years and above is climbing steadily, with higher life expectancy concentrated in southern and western states. Age-related musculoskeletal degeneration, neuro-degenerative conditions, and cardiovascular remodeling demand low-dose, comfort-optimized imaging systems. Hospitals are adding dual-energy X-ray absorptiometry, low-contrast cardiac CT, and silent MRI sequences to accommodate frail patients who may not tolerate lengthy procedures. In turn, vendors emphasize patient-centric ergonomics such as wide bores, noise-reduction software, and automated positioning, hallmarks now critical to competing in the India diagnostic imaging equipment market.

AI-Enabled and Advanced Imaging Adoption

GE HealthCare’s collaborations with NVIDIA and AWS to embed autonomous acquisition and cloud-based analytics into X-ray, ultrasound, and MRI systems exemplify the rapid digitization of radiology workflows. Siemens Healthineers’ MAGNETOM Flow platform reduces helium usage by 90% and integrates deep-learning reconstruction algorithms, lowering lifetime operating costs while boosting image clarity. The upgrade cycle initially unfolds in metros but quickly tracks along established referral corridors into Tier-2 cities as payors expand coverage for AI-assisted modalities. Handheld ultrasound devices such as Vscan Air already demonstrate 99.11% sensitivity for pediatric pneumonia versus 69.8% for chest radiography, catalyzing point-of-care adoption.

Insurance Expansion & PPP Programs

Ayushman Bharat PM-JAY received INR 9,406 crore in 2025, widening coverage for advanced imaging in secondary and tertiary care. Parallel PPP contracts bring multi-slice CT and 1.5 T MRI scanners into district hospitals, while a standardized fee schedule guarantees predictable reimbursement for private partners. The dedicated INR 4,200 crore Health Infrastructure Mission budget earmarks imaging purchases, enabling district-level hubs to service cluster facilities via hub-and-spoke teleradiology. As insurers ratify AI-based reporting, previously discretionary imaging procedures migrate into reimbursable categories, solidifying demand across the India diagnostic imaging equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Equipment & Procedure Costs | -1.4% | National, with higher impact in rural and tier-3 cities | Medium term (2-4 years) |

| Shortage Of Skilled Radiologists & Technicians | -0.9% | National, with acute shortage in North and East India | Long term (≥ 4 years) |

| Fragmented Regulatory Approval Timelines for Indigenous Devices | -0.7% | National, affecting domestic manufacturers | Short term (≤ 2 years) |

| Supply-Chain Vulnerability for Critical Inputs (E.G., Liquid Helium) | -0.8% | National, with higher impact on MRI installations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Equipment & Procedure Costs

Capital intensity remains a formidable hurdle as MRI and CT scanners can consume 20-25% of a mid-size hospital’s equipment budget. Smaller facilities rely on a USD 180 million secondary market for pre-owned units, which now equals 10% of overall medical equipment trade. Stakeholders continue to lobby for GST cuts on X-ray and diagnostic kits, arguing that a lower tax slab would widen adoption.[3]Source: Medical Buyer, “Industry call for rationalizing GST on diagnostic kits, x-ray equipment,” medicalbuyer.co.in Indigenous MRI prototypes priced 30-50% below imports promise relief, but scale-up hinges on validated clinical performance and after-sales networks, factors that still temper diffusion in the India diagnostic imaging equipment market.

Shortage of Skilled Radiologists & Technicians

India has almost doubled its medical colleges in a decade, yet sub-specialty radiology seats remain limited, perpetuating a mismatch between equipment availability and interpretive capacity. Vacancy rates are especially acute in North and East India, where imaging volumes outpace trained manpower. Teleradiology bridges gaps but relies on reliable broadband, often absent in rural belts. Vendors are embedding AI triage tools that flag critical findings, but regulatory approval for fully autonomous reads is still evolving. The workforce deficit therefore constrains throughput and return on investment for high-end devices, moderating growth of the India diagnostic imaging equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: X-Ray Dominance Amid CT Innovation

X-ray systems retained 28.74% share of the India diagnostic imaging equipment market in 2025 thanks to ubiquity in emergency and primary care. Computed tomography, however, is projected to post the fastest 8.62% CAGR as cardiac calcium scoring, trauma imaging, and oncology staging protocols proliferate in secondary and tertiary centers. Digital radiography upgrades, driven by lower detector prices and sharper images, are rapidly supplanting analog systems, while AI algorithms now automate fracture detection and tuberculosis screening. High-field MRI installations are also climbing, aided by domestic 1.5 T prototypes slated for clinical validation at AIIMS Delhi, which could shrink scan fees by over 30% and amplify the India diagnostic imaging equipment market size within the segment.

CT vendors increasingly bundle spectral imaging, metal-artifact reduction, and remote service diagnostics, reducing downtime and improving cost-per-study economics. Nuclear medicine retains a niche footprint confined to tertiary oncology hubs, yet PET-CT demand rises as precision oncology gains traction. Ultrasound remains the modality of choice for obstetrics, gastroenterology, and emergency evaluations, but handheld probes are gaining ground in out-of-hospital care. Overall, modality mix evolution underscores how technological sophistication and affordability now co-determine capital budgets across the India diagnostic imaging equipment market.

By Portability: Fixed Systems Lead, Mobile Solutions Accelerate

Fixed installations accounted for 82.05% of the India diagnostic imaging equipment market size in 2025, reflecting decades-old infrastructure geared to inpatient imaging and trauma care. Yet mobile and handheld devices are escalating at an 7.86% CAGR, buoyed by government vans serving rural districts and corporate wellness camps. Handheld ultrasound offers 99.11% sensitivity for pediatric pneumonia, surpassing chest X-ray and validating portable diagnostics’ clinical utility. Cart-based ultrasound and mobile DR units now include hotspot connectivity, funneling images to cloud PACS for instant reads.

Advances in battery density, wireless data transfer, and rugged casings have broadened deployment in disaster zones and sports medicine. Global Fund endorsements of portable X-ray solutions further legitimize the category. Over time, utilization of mobile scanners redeploys imaging load away from overburdened tertiary centers, expanding the India diagnostic imaging equipment market into new geographies while improving asset ROI.

By Application: Oncology Leadership, Cardiology Acceleration

Oncology captured 24.56% of the India diagnostic imaging equipment market in 2025 as multimodality imaging underpins every phase of cancer management. PET-CT fusion for metabolic mapping, diffusion-weighted MRI for response evaluation, and cone-beam CT for interventional procedures anchor purchasing decisions. Cardiology is set to log an 8.47% CAGR, tied to a 35.5% adult hypertension rate and rising CAD screening volume. High-temporal-resolution CT angiography, 3-D echocardiography, and cardiac MRI are gaining reimbursement traction, shifting procurement toward ECG-synchronized scanners.

Neurology rounds out high-growth niches as stroke protocols mandate sub-5-minute CT and perfusion imaging. Orthopedic centers invest in dual-energy CT for crystal arthropathy and low-dose trauma protocols. Gastroenterology leans on endoscopic ultrasound coupled with contrast-enhanced MRI for liver fibrosis staging. Such diversified clinical demand cements imaging as the diagnostic backbone across specialties, fortifying the India diagnostic imaging equipment market.

By End User: Hospital Dominance, Diagnostic Center Growth

Hospitals commanded 65.42% share of the India diagnostic imaging equipment market in 2025 because emergency rooms, surgical suites, and ICUs require on-premise scanners for real-time decisions. Diagnostic centers, though, are expanding at an 7.74% CAGR as urban patients prefer one-stop outpatient imaging with shorter waits and bundled wellness packages. Center chains leverage economies of scale to negotiate service contracts and centralized reporting, boosting uptime and reducing per-study costs.

Corporate preventive programs and telehealth triage funnel more routine scans to stand-alone facilities, freeing hospitals to focus on acute and interventional cases. Specialty clinics—orthopedics, cardiology, oncology—are adding in-house ultrasound and low-field MRI to expedite procedure planning. Together, these shifts diversify demand channels inside the India diagnostic imaging equipment market, encouraging vendors to tailor service models from enterprise-wide managed equipment services to pay-per-scan rentals.

Geography Analysis

South India led the India diagnostic imaging equipment market with 29.12% share in 2025, underpinned by high per-capita spend, dense medical college networks, and a robust medical tourism ecosystem. States like Karnataka and Tamil Nadu pioneer AI-embedded MRI installations and host manufacturing clusters benefiting from electronics supply chains. Regulatory compliance regimes are mature, enabling quicker installation certification and accelerating hybrid operating models that blend in-person and teleradiology workflows.

North India is the breakout growth engine, projected at a 8.72% CAGR through 2031, catalyzed by new AIIMS campuses and upgraded district hospitals funded by central schemes. Delhi-NCR functions as a hub for corporate insurance panels and attracts private equity into diagnostic center networks. Uttar Pradesh and Punjab drive volume through new cancer institutes and cath labs, while Haryana leverages proximity to the capital to launch PPP imaging suites. Still, workforce deficits necessitate aggressive adoption of AI pre-reads and cross-state teleradiology to meet burgeoning scan loads.

West India posts steady expansion anchored by Maharashtra’s specialty hospitals and Gujarat’s device manufacturing corridors. Pharmaceutical R&D in these states bolsters demand for pre-clinical imaging. East and North-East India trail on penetration but present white-space potential as infrastructure grants upgrade secondary hospitals. Improved air connectivity and government viability-gap funding are expected to unlock latent demand, gradually enlarging the geographic footprint of the India diagnostic imaging equipment market.

Regulatory Landscape

India regulates diagnostic imaging equipment as medical devices under the Drugs and Cosmetics Act, 1940 and the Medical Devices Rules, 2017 (MDR 2017), with the Central Drugs Standard Control Organization (CDSCO) and the Drugs Controller General of India acting as the central licensing authority through a risk-based device classification framework. For radiology installations, compliance extends beyond device licensing to site and radiation-safety requirements where applicable (notably for X-ray systems). Importers and manufacturers must also follow the MDR 2017 documentation requirements and post-market obligations administered through CDSCO.

In April 2026, the Ministry of Health and Family Welfare issued a draft Medical Devices (Amendment) Rules, 2026 notification (G.S.R. 270(E)), indicating continued refinement of expectations around testing and traceability for devices supplied into India. The Department of Pharmaceuticals has also continued industrial-policy actions under Make in India, including a June 2026 review of the Global Tender Enquiry (GTE) exemption list, which can affect public procurement access for imported high-end imaging systems when domestic alternatives are being emphasized.

Value Chain Analysis

The India diagnostic imaging equipment value chain spans (i) upstream components and critical inputs (detectors, high-end electronics, tubes, and, for MRI, helium-related dependencies), (ii) OEM design, manufacturing/assembly, and quality systems, (iii) import and channel partners, (iv) installation, shielding and site readiness (particularly for CT and MRI suites), and (v) service, upgrades, consumables, and software (PACS, AI applications) that generate lifecycle revenue. While India has historically relied heavily on imports for high-technology imaging platforms, localization has progressed through the Production Linked Incentive (PLI) scheme, with manufacturing commenced for CT scanners, MRI machines, C-arm X-ray machines, mammography systems, and ultrasound equipment under the program.

Distribution and deployment depend on hospital procurement decisions, diagnostic center networks, and PPP structures that place scanners into district facilities, with service uptime, remote diagnostics, and application training acting as differentiators. Infrastructure enablers such as the Andhra Pradesh MedTech Zone (AMTZ) offer plug-and-play manufacturing facilities and common testing infrastructure, which can reduce entry barriers for domestic manufacturers. At the same time, compliance remains multi-layered for imaging suppliers (CDSCO under MDR 2017, and additional licensing for X-ray equipment under the Atomic Energy Regulatory Board), making regulatory affairs, calibration, and after-sales field service capabilities important across the chain.

Competitive Landscape

Multinationals dominate technology leadership yet face mounting price competition. Siemens Healthineers alone allocated USD 27.38 billion to med-tech R&D, with USD 3.36 billion carved out for imaging innovations such as helium-light 1.5 T magnets. GE HealthCare’s USD 960 million India plan backs a Bengaluru plant turning out PET-CT scanners for export to 15 countries. Philips focuses on sealed-magnet MRI models that consume 0.7 liters of helium, positioning itself for supply-chain resilience.

Domestic players respond with cost-effective offerings. Voxelgrids Innovations gained CDSCO approval for its 1.5 T MRI at roughly 50% of import prices, signaling credible indigenous alternatives. Trivitron Healthcare scales frugal engineering to develop sub-USD 30,000 handheld ultrasound units, targeting primary clinics. Wipro GE’s “made-in-India” Discovery IQ PET-CT demonstrates policy-driven localization’s power to marry global quality with domestic cost structures.

Competition increasingly hinges on digital ecosystems. Vendors bundle AI triage, zero-footprint viewers, and cloud PACS subscriptions, creating sticky revenue streams that outlast hardware lifecycles. Managed equipment services, uptime guarantees, and pay-per-scan models help cash-constrained hospitals access premium technology. In aggregate, the India diagnostic imaging equipment market shows moderate consolidation but fast-evolving value propositions that give nimble local firms room to erode incumbent shares.

India Diagnostic Imaging Equipment Industry Leaders

Fujifilm Holdings Corporation

Koninklijke Philips N.V.

Siemens Healthineers AG

Canon Medical Systems Corp.

GE HealthCare

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity set sits where localization and upgrade-driven replacement demand intersect: the PLI-backed manufacturing base, together with government emphasis on prioritizing indigenous production of high-value categories (including MRI components and X-ray systems referenced in June 2026 policy discussions), creates room for locally built configurations, component ecosystems, and India-specific service models. With equipment and procedure costs still constraining adoption, offerings that reduce total cost of ownership (including sealed-magnet or helium-light MRI platforms, remote service diagnostics, and pay-per-scan arrangements) can broaden addressable demand across hospitals and diagnostic imaging centers, especially beyond the top metros.

Another opportunity involves capacity expansion in oncology and advanced diagnostics backed by ongoing projects and institutional partnerships. In February 2026, IBA and Shreeji signed a multi-site agreement for four cyclotrons across Ahmedabad, Nagpur, Kochi, and Bhubaneswar, strengthening PET radiopharmaceutical availability and supporting PET-CT utilization beyond a limited number of tertiary hubs. Provider-side network build-outs also indicate equipment pull-through in Tier-I and Tier-II markets, including the October 2025 Superhealth and United Imaging partnership for supply and lifecycle management of radiology systems across 100 hospitals, and the March 2025 Aarthi Scans investment in Siemens helium-free MRI technology across multiple Indian cities, both pointing to demand for higher-throughput, digitally integrated imaging workflows.

Recent Industry Developments

- April 2026: GE HealthCare partnered with AIIMS New Delhi to establish an AI Health Innovations Hub, committing USD 1 million over five years for R&D and clinical deployment. The collaboration supports clinical validation and workflow automation for imaging, aligning product development with public-sector scale needs and radiologist capacity constraints.

- August 2025: Canon Medical Systems India signed an MoU with Rajiv Gandhi Cancer Institute and Research Centre to support research using the Aquilion ONE/INSIGHT Edition CT system. The tie-up expands evidence generation around advanced CT applications in oncology care pathways and can inform protocol standardization and upgrade decisions in large hospital systems.

- March 2024: Wipro GE Healthcare announced an investment plan of over INR 8,000 crore over five years to expand manufacturing output and local R&D in India. The program supports deeper localization of imaging equipment and subsystems, enabling shorter supply lines, improved serviceability, and India-for-India production strategies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from diagnostic imaging equipment sold and installed in India for medical diagnosis in hospitals, imaging centers, and similar care settings. It includes major modalities used in routine and advanced imaging, and it is measured in current USD.

Scope exclusions: We exclude imaging consumables and contrast media, routine service-only contracts, and software sold as a standalone product without an equipment sale.

Segmentation Overview

- By Modality

- MRI

- Low-Field (< 1.5 T)

- Standard (1.5–3 T)

- High-Field (3 T & above)

- Computed Tomography

- ≤64-Slice CT

- >64-Slice CT

- Ultrasound

- Cart-based

- Portable/Hand-held

- X-Ray

- Analog

- Digital

- Nuclear Imaging

- PET

- SPECT

- Other Modalities (Mammography, Fluoroscopy, etc.)

- MRI

- By Portability

- Fixed Systems

- Mobile and Hand-held Systems

- By Application

- Cardiology

- Oncology

- Neurology

- Orthopedics

- Gastroenterology

- Gynecology & Obstetrics

- Other Applications

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Specialty Clinics & Other End Users

- By Regional Zone

- North India

- South India

- West India

- East & North-East India

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand and supply picture, and then to cross-check whether growth patterns match what is visible in public data. We referred to sources such as the Ministry of Health and Family Welfare publications, National Health Accounts, and updates from NITI Aayog to understand system capacity and funding direction. Import and export statistics from official customs and trade portals were also reviewed to sense-check equipment inflow by category over time.

We also used information from medical device and radiology associations, peer-reviewed clinical journals, and tender portals that show public procurement intent and timing. On the company side, annual reports, investor presentations, and press releases helped confirm product positioning and installed-base commentary. For consolidation, we additionally used a paid subscription that supports company financials and another that supports patent and innovation tracking to validate technology shift assumptions. These examples are illustrative, and many other public sources were also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were carried out with a mix of equipment suppliers, distributors, radiology heads, biomedical teams, and procurement managers across hospitals and imaging centers. Inputs were used to confirm demand drivers, replacement cycles, pricing direction (especially for mid-range systems), and how utilization differs by city tier and care setting. Since this is an India-only market, coverage was ensured across major zones and a blend of public and private buyers so assumptions could be corrected where desk signals were unclear.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 18% | |

| Mid tier: 45% | Functional/Unit leaders: 34% | |

| Smaller Players: 19% | Managers: 48% |

Market-Sizing & Forecasting

Sizing starts from a top-down view where imaging procedure demand, facility expansion, and procurement intensity are translated into equipment requirement by modality, and then valued using typical system pricing bands. The model is then checked with selective bottom-up approximations, such as channel feedback on unit shipments in key states and sampled average selling price times volume for high-run modalities like ultrasound and X-ray.

Key inputs used (illustrative) include the pace of new hospital and diagnostic center additions, replacement cycles for older installed equipment, procedure mix shifts toward CT and MRI, public procurement timing, and import dependence changes linked to local manufacturing initiatives. Forecasting is done using scenario analysis supported by a simple multivariate regression on healthcare spend direction, imaging access expansion, and price erosion versus feature upgrades, with assumptions reviewed and adjusted using primary feedback. Where bottom-up visibility is weaker in smaller cities, adoption rates are built from comparable facility cohorts and then normalized to known procurement and utilization signals.

Data Validation & Update Cycle

Outputs are validated through triangulation across demand signals, trade flow direction, and what interviewees report for ordering patterns, lead times, and pricing movement. Any sharp year-on-year jumps are flagged, and then traced back to a clear driver such as a procurement wave, a modality-specific upgrade cycle, or a change in price mix. Before sign-off, the model goes through multi-step analyst reviews, and follow-up calls are triggered when a key assumption changes or when secondary indicators move against the forecast.

The report is refreshed annually, and interim updates are made when material events occur, such as policy changes affecting procurement, import duties, or major shifts in hospital capex. Right before delivery, a fresh check is performed so the numbers reflect the latest available signals and interview-backed assumptions.

Mordor Intelligence's India Diagnostic Imaging Equipment Market Market Sizing Compared With Other Published Estimates

Published market sizes for India diagnostic imaging often do not match, even when the topic sounds similar. Differences usually come from what is counted as equipment versus broader imaging, the year used as the base, and how pricing and replacement demand are treated.

In this market, the biggest gap drivers are whether the estimate includes service-heavy imaging revenues, whether accessories and components are blended into the total, and how imports are converted to revenue when distributor margins and local assembly are involved. Another common reason is refresh cadence, where older pricing assumptions can stay in the model even after discounting and mix-shifts change the realized value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.21 B (2026) | |

| Trade Publisher A | USD 0.85 B (2024) | This figure appears to align more with a narrower equipment-only view valued closer to procurement spend in a different base year, and it may treat modality coverage and distributor-to-end-user price build-up more conservatively. |

| Industry Analytics Firm B | USD 1.32 B (2024) | The estimate is positioned as a broader medical imaging view, which can use different product groupings and a different pace of price change, especially if CT and MRI mix upgrade is not fully reflected year by year. |

The spread is mainly explained by how equipment revenue is separated from broader imaging revenues, and by how year-to-year pricing is updated as mix shifts toward advanced modalities, a choice applied by Mordor Intelligence. With the scope and conversion steps kept explicit, buyers can trace the number back to repeatable inputs like adoption, replacement, and pricing bands.

Key Questions Answered in the Report

How large is the India diagnostic imaging equipment market in 2026?

The India diagnostic imaging equipment market size reached USD 2.21 billion in 2026 and is poised to attain USD 3.16 billion by 2031 at a 7.38% CAGR.

Which modality is growing fastest in India?

Computed tomography leads growth with an 8.62% CAGR through 2031, driven by expanding cardiovascular and oncology protocols.

Why are mobile and handheld scanners gaining traction?

Mobile devices enable point-of-care services in rural and emergency settings and are projected to post an 7.86% CAGR to 2031.

Which region offers the highest growth potential?

North India shows the fastest regional expansion at a 8.72% CAGR thanks to new AIIMS campuses and district-hospital upgrades.

What policy supports domestic imaging equipment manufacture?

The Production Linked Incentive scheme has funded 19 greenfield plants producing MRI, CT, and ultrasound systems locally, reducing import dependence.

How is helium scarcity influencing MRI procurement?

Vendors now market sealed-magnet or helium-free systems, mitigating supply-chain risks and lowering long-term operating costs.

Page last updated on: