India Nuclear Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

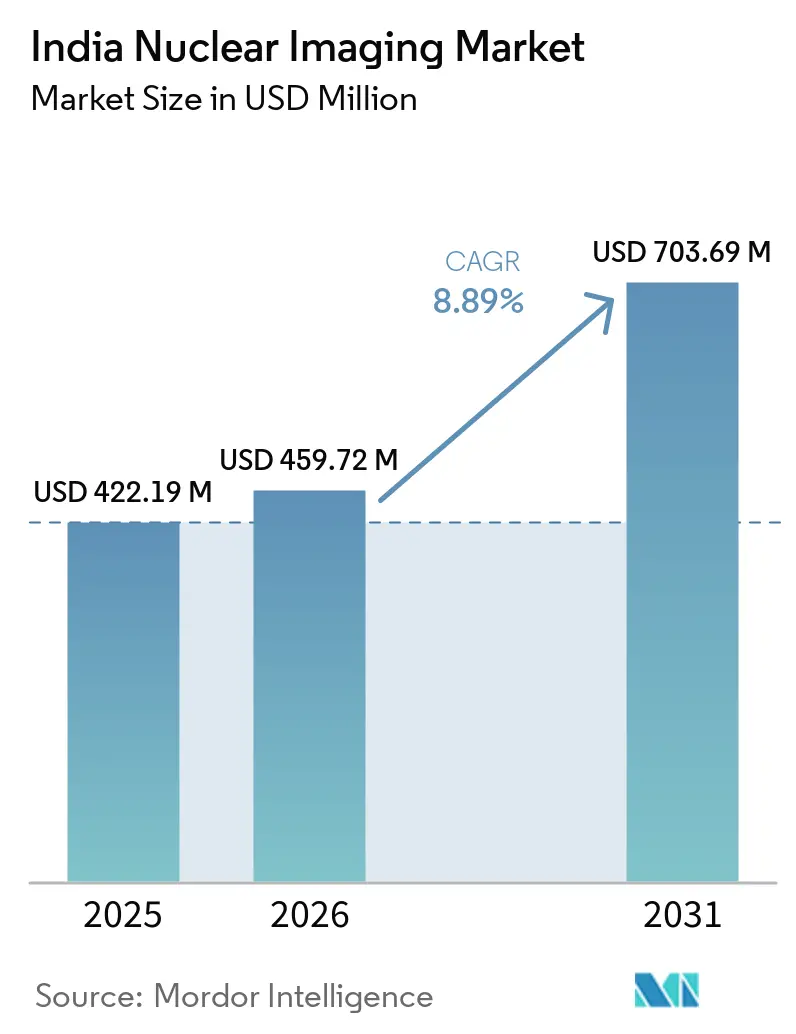

| Base Year Market Size (2025) | USD 422.19 Million |

| Market Size (2026) | USD 459.72 Million |

| Market Size (2031) | USD 703.69 Million |

| Growth Rate (2026 - 2031) | 8.89% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Nuclear Imaging Market Analysis by Mordor Intelligence

The India Nuclear Imaging Market size is expected to grow from USD 422.19 million in 2025 to USD 459.72 million in 2026 and is forecast to reach USD 703.69 million by 2031 at 8.89% CAGR over 2026-2031.

Diagnostic and therapeutic demand continues to climb as India confronts a steep rise in cancer and cardiovascular cases, while the government’s Ayushman Bharat program accelerates imaging infrastructure across tier-2 and tier-3 cities. Growing availability of domestic radioisotopes from BARC reactors reduces import dependence and stabilizes pricing for providers. Hybrid PET-CT and SPECT-CT systems equipped with cadmium-zinc-telluride (CZT) detectors improve image quality at lower radiation doses, prompting wider adoption in tertiary hospitals. Private-equity-backed chains are scaling standalone PET-CT centers, signaling investor confidence in the long-run growth of the India nuclear imaging market.

Key Report Takeaways

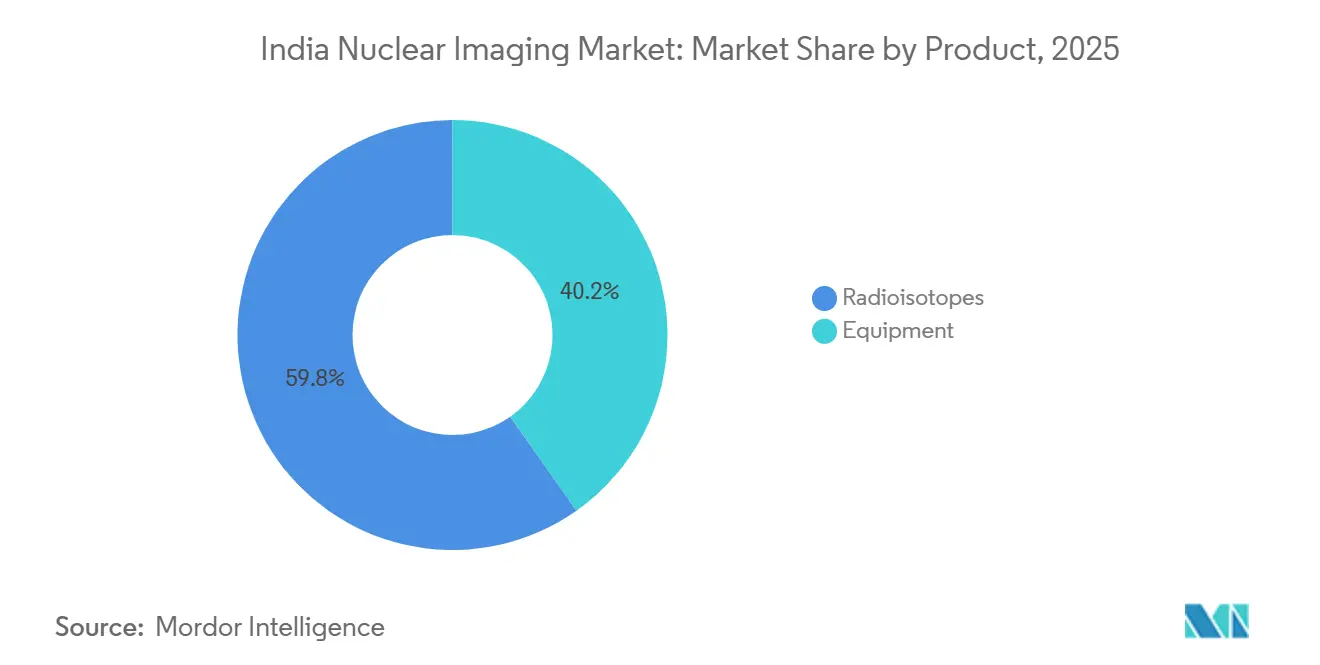

- By product category, radioisotopes captured 59.78% of the India nuclear imaging market share in 2025 and are projected to expand at a 9.62% CAGR through 2031.

- By application, oncology accounted for a 51.46% share of the India nuclear imaging market size in 2025, while neurology is advancing at a 9.08% CAGR through 2031.

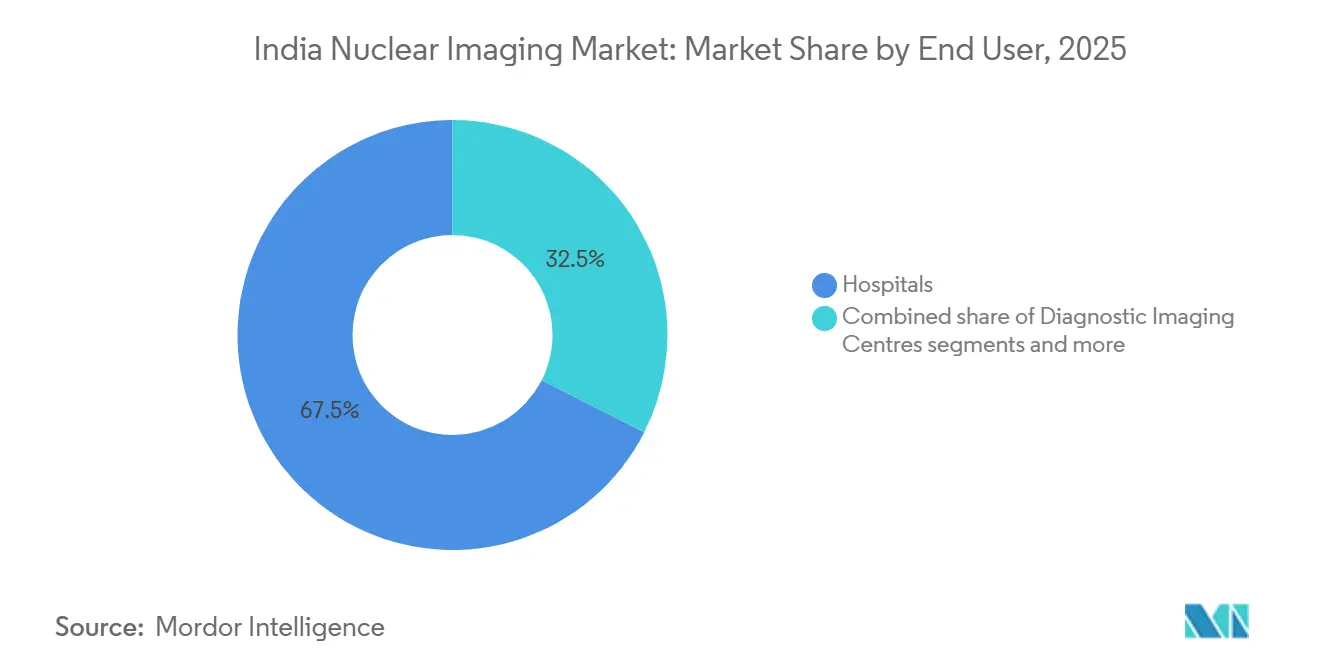

- By end user, hospitals held 67.52% of the India nuclear imaging market share in 2025; diagnostic imaging centers record the highest projected CAGR at 9.71% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Nuclear Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of cancer and cardiac diseases | +2.8% | National, with higher impact in urban centers | Long term (≥ 4 years) |

| Rising adoption of hybrid imaging modalities in tertiary hospitals | +1.9% | Metro cities and tier-1 urban centers | Medium term (2-4 years) |

| Government initiatives under Ayushman Bharat to expand imaging infrastructure | +1.6% | National, with focus on tier-2 and tier-3 cities | Medium term (2-4 years) |

| Increasing domestic radioisotope production via BARC | +1.2% | National supply chain impact | Long term (≥ 4 years) |

| Shift to low-dose CZT detectors driven by radiation-safety norms | +0.8% | Urban tertiary care centers | Short term (≤ 2 years) |

| Emergence of private-equity-funded standalone PET-CT chains | +0.7% | Metro and tier-1 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Cancer and Cardiac Diseases

India logged 1.4 million new cancer cases in 2024, and the National Cancer Registry projects a 12.8% jump by 2025[1]Indian Journal of Medical Research, "Cancer Incidence Estimates for 2022 & Projections for 2025: Results from India's National Cancer Registry Programme". Late-stage diagnosis remains common, with only 29% of tumors detected early, raising demand for precise PET and SPECT procedures that can delineate disease spread. Nuclear cardiology volumes are climbing as coronary artery disease afflicts younger cohorts; two-thirds of Indians aged 25-45 are now pre-hypertensive, prompting clinicians to choose non-invasive myocardial perfusion imaging to triage intervention. Rising lifestyle-related morbidity therefore directly boosts utilization across all nuclear imaging modalities, reinforcing the structural growth of the India nuclear imaging market.

Adoption of Hybrid PET-CT and SPECT-CT in Tertiary Hospitals

PET-CT installations have surpassed 50 units nationwide while SPECT-CT growth trails because of higher per-scan costs. However, cost-effectiveness studies show a PET-CT scan in India is priced at INR 4,600–31,000 (USD 55–372), far below global averages, shortening payback periods for large centers. CZT detectors and AI-assisted reconstruction improve resolution while lowering tracer dose, making hybrid imaging more attractive in radiation-safety-conscious facilities. As tertiary hospitals upgrade equipment, referral patterns shift toward comprehensive nuclear imaging suites, which further enlarges the India nuclear imaging market.

Ayushman Bharat Imaging-Infrastructure Roll-out

The Ayushman Bharat Health Infrastructure Mission earmarks INR 64,180 crore (USD 7.84 billion) for diagnostics, including nuclear imaging units at district hospitals. Over 175,000 Ayushman Arogya Mandirs now provide screening pathways that feed into higher-level PET-CT services. The PM-JAY insurance scheme covers 550 million beneficiaries with annual limits of INR 5 lakh (USD 6,100), creating a predictable reimbursement stream for nuclear imaging. Improved public funding closes the urban-rural accessibility gap, sustaining multi-year demand momentum for the India nuclear imaging market.

Expansion of Domestic Radioisotope Production at BARC

The Dhruva research reactor operates at 100 MW and, together with the upgraded Apsara-U pool reactor, supplies Technetium-99m, Iodine-131, Lutetium-177, and emerging alpha emitters for local use. Cyclone-30 in Kolkata is the largest medical cyclotron in Asia, delivering Fluorine-18 and Gallium-68, with surplus capacity for export. Strong domestic supply mitigates disruptions in the global Mo-99 market and lowers tracer prices by up to 18%, enabling smaller centers to adopt PET-based protocols. Reliable isotope availability underpins predictable procedure volumes, consolidating the long-term expansion of the India nuclear imaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of equipment acquisition and maintenance | -1.8% | National, more pronounced in tier-2/3 cities | Long term (≥ 4 years) |

| Scarcity of skilled nuclear-medicine technologists | -1.4% | National, acute in non-metro areas | Medium term (2-4 years) |

| Mo-99 import supply-chain disruptions | -0.9% | National supply chain impact | Short term (≤ 2 years) |

| AERB licensing delays for new cyclotrons | -0.6% | National regulatory bottleneck | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Equipment Acquisition and Maintenance Cost

Setting up a gamma-knife or PET-CT suite can cost INR 400 million (USD 4.88 million) when real estate, shielding, and licensing expenses are included. Smaller hospitals often lack patient throughput to justify such outlays, so metropolitan tertiary centers remain the primary installation sites, limiting geographic penetration of the India nuclear imaging market. Post-warranty service contracts priced at 8-10% of capital value per year strain operating budgets, particularly since spare parts are imported and dollar-denominated. Leasing programs and public-private partnerships are emerging, yet they remain nascent and do not fully erase the high-capex hurdle.

Scarcity of Skilled Nuclear-Medicine Technologists

Occupational-stress studies reported 89% of working technologists experience burnout symptoms, raising attrition risks. Shortages are most acute outside large metros, extending scan appointment wait times and constraining capacity utilization. GE HealthCare launched a nationwide upskilling program in late 2024 to train 10,000 technologists over five years, but the pipeline will still lag the growth of the India nuclear imaging market in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Radioisotopes Sustain Diagnostic and Therapeutic Momentum

Radioisotopes generated 59.78% of the India nuclear imaging market share in 2025, and the subsegment is forecast to post a 9.62% CAGR through 2031. Technetium-99m remains the workhorse for SPECT, accounting for roughly 80% of single-photon studies, yet its reactor-based production chain presents well-documented supply risk. PET radioisotopes such as Fluorine-18 are growing more swiftly, aided by new cyclotrons in Chennai and Hyderabad that reduce tracer decay losses during transport. On the therapeutic front, Lutetium-177 labeled compounds for neuroendocrine tumors and prostate cancer secured Drug Controller General of India approvals in 2024[2]CDSCO - List of New Drugs Approved in 2024, spurring wider adoption. Domestic Lu-177 output at BARC meets 65% of national demand, trimming procedure costs by nearly 20% versus imported doses.

The equipment segment adds incremental value through hardware innovation, especially solid-state detector arrays that boost sensitivity in low-dose scans. Localization initiatives by GE HealthCare and Siemens Healthineers promise to shave 10-12% off unit prices by 2027, but maintenance costs remain elevated because high-precision crystals and vacuum components still come from overseas. Even so, rising equipment affordability broadens the customer base, supporting a virtuous cycle of radioisotope demand that further scales the India nuclear imaging market size.

By Application: Oncology Remains Dominant while Neurology Accelerates

Oncology commanded a 51.46% slice of the India nuclear imaging market size in 2025, driven by growing use of PSMA-based theranostics in prostate cancer and FDG PET for treatment response assessment. As the national cancer burden mounts, follow-up imaging volumes rise in tandem, reinforcing oncology’s lead. Neurology, while smaller, is the fastest-growing application at a 9.08% CAGR, propelled by regional clinical trials of amyloid-PET tracers for Alzheimer’s disease and dopamine transporter agents for Parkinson’s disease. Early evidence shows Ga-68 FAPI PET-CT improves detection of neuro-oncologic lesions that traditional imaging misses, catalyzing protocol updates in large teaching hospitals.

Cardiology holds steady demand thanks to rising nuclear stress test referrals, and the expected launch of Flurpiridaz F-18 in 2026 could push myocardial-perfusion PET volumes higher once reimbursement codes settle. Thyroid imaging retains a loyal clinical base through proven I-131 scan-and-treat protocols. Broader clinical acceptance of theranostic pairs spanning multiple disease areas spreads fixed costs, enlarging the total addressable segment pool and giving oncology and neurology a demand halo that anchors the India nuclear imaging market share leadership over the forecast horizon.

By End User: Hospitals Dominate as Imaging Centers Scale Up

Hospitals accounted for 67.52% of the India nuclear imaging market share in 2025 because they already control oncology referral pathways and possess shielded bunkers that meet AERB standards. Public tertiary institutes such as AIIMS lead in procedure volumes, but the private sector now contributes more than 55% of new PET-CT installations, reflecting investor appetite for high-margin diagnostics. Diagnostic imaging centers are expanding at a 9.71% CAGR, underpinned by franchise models that replicate PET-CT suites in tier-1 clusters. Lease-to-own arrangements lower upfront capital needs, enabling faster network rollouts.

Academic and research institutes nurture translational science, piloting first-in-human trials of alpha emitters like Actinium-225, yet their commercial footprint remains small. Nonetheless, they help seed clinical evidence, which later diffuses into hospital practice and imaging-center protocols. As outpatient care shifts higher imaging volumes away from inpatient departments, nimble standalone centers are poised to capture greater wallet share, adding diversity to the India nuclear imaging market structure.

Geography Analysis

Northern, western, southern, and eastern clusters display distinct maturity levels in the India nuclear imaging market. The western corridor centered on Mumbai and Pune boasts the densest concentration of PET-CT scanners, reflecting both private capital inflows and proximity to BARC isotope supplies. Southern states such as Tamil Nadu and Karnataka leverage strong medical-education ecosystems and favorable state procurement policies to pilot CZT SPECT installations in secondary cities. Northern India will soon gain strategic isotope resilience from the Gorakhpur nuclear project in Haryana, which promises to add Mo-99 production capacity by 2029.

Eastern India historically lagged in advanced imaging density, but the Cyclone-30 facility in Kolkata now delivers F-18 and Ga-68 to the region, shrinking scan wait times from five days to under 48 hours. Rural cancer incidence hotspots in the Northeast underscore ongoing access gaps; government-funded mobile PET-CT initiatives trialed in Assam could become scalable solutions if AERB refines interim licensing norms. Across geographies, Ayushman Bharat reimbursement parity reduces out-of-pocket cost variance, nudging patient flow toward accredited centers and reinforcing uniform growth across the India nuclear imaging market.

Regional competitive dynamics vary as well. Western metros remain price-competitive due to equipment density, while southern states differentiate through subspecialty expertise in theranostics. Northern operators invest aggressively in outreach clinics that funnel complex cases to flagship tertiary hubs. Collectively, these cross-currents propel a nationwide growth trajectory, confirming the India nuclear imaging market’s resilience to localized supply-demand imbalances.

Competitive Landscape

Multinational imaging giants lead in hardware innovation, yet Indian suppliers strengthen the radiopharmaceutical value chain. GE HealthCare’s USD 959 million manufacturing program will localize PET-CT gantry production, targeting a 20% cost reduction by 2027. Siemens Healthineers broadened its isotope footprint by acquiring Advanced Accelerator Applications Molecular Imaging, adding 13 European sites that can funnel surplus Lu-177 and Ga-68 generators into India. Canon Medical Systems announced a USD 34 million U.S. imaging-resource center, with software R&D earmarked for SPECT reconstruction algorithms deployable on India-sold systems.

On the radiopharmaceutical side, Curium Pharma’s acquisition of Monrol elevates it to the top tier of global Lu-177 suppliers and opens a distribution channel for India via local cold-kit partners. Cardinal Health continues to expand trial-dose logistics that support early-phase Indian oncology studies. Domestic companies such as Radeosys leverage BARC master-supply agreements to produce cold kits at prices 15–18% below imported alternatives, appealing to cost-sensitive public hospitals.

Competitive differentiation now centers on integrated offerings, hardware-plus-tracer-plus-AI workflow, rather than price alone. Firms capable of bundling scanners with vetted tracers and remote-reading software lock in long-term service contracts, raising switching costs for providers. Nevertheless, pockets of under-penetration in tier-3 cities keep the door open for nimble regional players, ensuring the India nuclear imaging market retains moderate rather than high concentration.

India Nuclear Imaging Industry Leaders

-

Koninklijke Philips N.V.

-

GE Healthcare

-

Siemens Healthineers

-

Bracco Imaging S.p.A.

-

Canon Medical Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: IBA (Ion Beam Applications S.A., EURONEXT) and Shreeji (Shreeji Imaging and Diagnostic Centre Pvt. Ltd.) have entered into a multi-site agreement for the supply and installation of four mid-energy Cyclone KIUBE 300 cyclotrons. These systems, to be deployed in Ahmedabad, Nagpur, Kochi, and Bhubaneswar, aim to enhance the industrial-scale production of fluorine-18 (F-18) labeled compounds and other PET radiopharmaceuticals.

- March 2025: Government announced North India's first nuclear project in Haryana at Gorakhpur, featuring six reactors with 10,380 MW total capacity as part of India's goal to achieve 100 GW nuclear energy by 2047, directly supporting radioisotope production infrastructure.

India Nuclear Imaging Market Report Scope

As per the scope of the report, nuclear imaging is a medical imaging technique that uses small amounts of radioactive materials, called radiotracers, which are introduced into the body. These radiotracers emit gamma rays that are detected by special cameras to create detailed images of organs, tissues, or cellular activity. Nuclear imaging helps diagnose and monitor various medical conditions by providing functional information about the body's processes.

The segmentation by product in the India nuclear imaging market includes equipment used in nuclear imaging. Additionally, the market covers radioisotopes, which are further categorized into SPECT and PET radioisotopes. SPECT radioisotopes include Technetium-99m (Tc-99m), Thallium-201 (Tl-201), Gallium-67 (Ga-67), Iodine-123 (I-123), and other SPECT isotopes. PET radioisotopes include Fluorine-18 (F-18), Rubidium-82 (Rb-82), and other PET isotopes. The segmentation by application includes various areas such as cardiology, neurology, thyroid-related imaging, oncology, and other applications. The segmentation by end user includes hospitals, diagnostic imaging centers, and academic and research institutes. The report offers the value (in USD) for the above segments.

| Equipment | ||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) |

| Thallium-201 (Tl-201) | ||

| Gallium-67 (Ga-67) | ||

| Iodine-123 (I-123) | ||

| Other SPECT Isotopes | ||

| PET Radioisotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (Rb-82) | ||

| Other PET Isotopes | ||

| Cardiology |

| Neurology |

| Thyroid |

| Oncology |

| Other Applications |

| Hospitals |

| Diagnostic Imaging Centres |

| Academic & Research Institutes |

| By Product | Equipment | ||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) | |

| Thallium-201 (Tl-201) | |||

| Gallium-67 (Ga-67) | |||

| Iodine-123 (I-123) | |||

| Other SPECT Isotopes | |||

| PET Radioisotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (Rb-82) | |||

| Other PET Isotopes | |||

| By Application | Cardiology | ||

| Neurology | |||

| Thyroid | |||

| Oncology | |||

| Other Applications | |||

| By End User | Hospitals | ||

| Diagnostic Imaging Centres | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What is the current value of the India nuclear imaging market?

The market is valued at USD 459.72 million in 2026 and is projected to reach USD 703.69 million by 2031.

Which product segment leads in India nuclear imaging space?

Radioisotopes dominate with 59.78% market share in 2025 and will remain the fastest-growing category through 2031.

How fast is neurology imaging growing within nuclear medicine?

Neurology applications are expanding at a 9.08% CAGR through 2031, the highest among all clinical segments.

How will Ayushman Bharat influence future demand?

The program funds imaging facilities beyond metro areas and provides insurance coverage, broadening patient access to nuclear medicine procedures.

What are the main challenges to market expansion?

High equipment costs and a shortage of trained nuclear-medicine technologists are the primary restraints on growth.

Page last updated on: