Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.82 Billion |

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 2.66 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India In-Vitro Diagnostics Market Analysis by Mordor Intelligence

India in-vitro diagnostics market size in 2026 is estimated at USD 1.94 billion, growing from 2025 value of USD 1.82 billion with 2031 projections showing USD 2.66 billion, growing at 6.49% CAGR over 2026-2031. The expansion reflects stronger clinical focus on evidence-based care, wider health-insurance coverage, and public investments that are widening test availability. Rapid molecular methods, artificial intelligence-enabled automation, and digital health linkages are lifting laboratory productivity while shrinking turnaround times. At the same time, the dual burden of infectious and chronic diseases is broadening test menus, and organized diagnostic chains are rolling tier-2 and tier-3 city networks into hub-and-spoke systems that improve access and pricing. Constraints persist around cold-chain logistics, fragmented regulation, and heavy reliance on imported instruments, but technology transfer, Make-in-India incentives and portable cooling solutions are beginning to narrow these gaps across the India in-vitro diagnostics market.

Key Report Takeaways

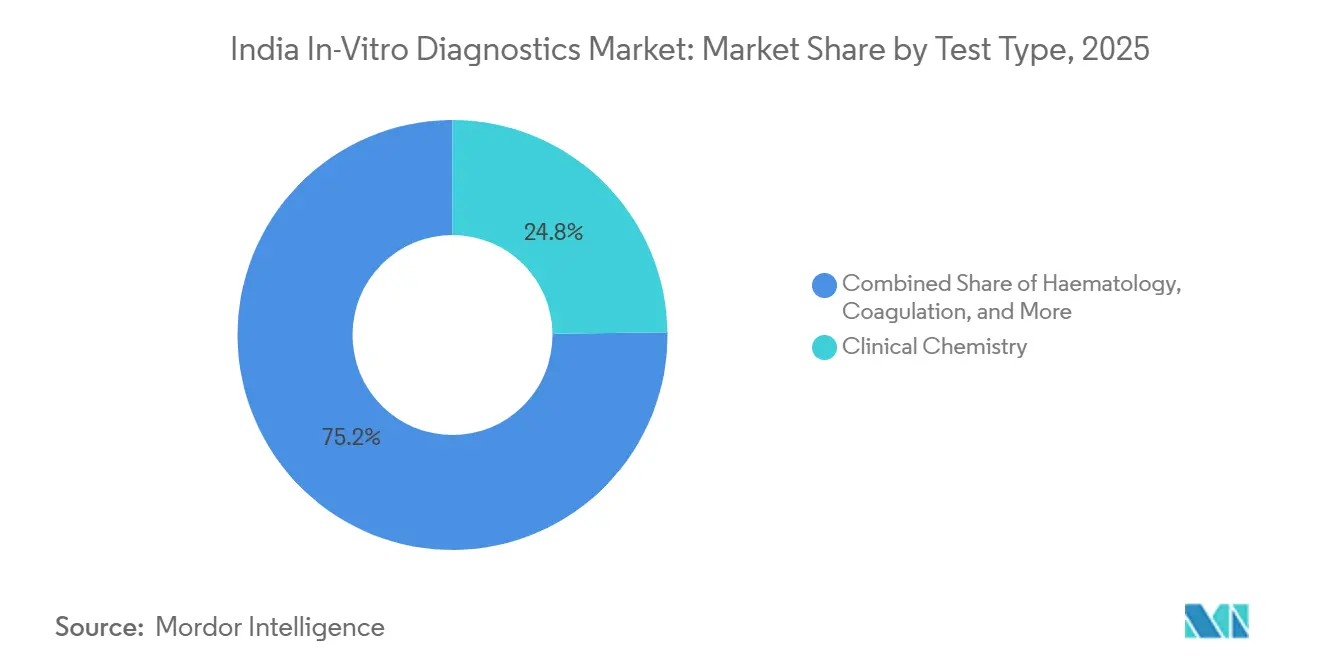

- By test type, clinical chemistry led with 24.36% revenue share in 2025, while molecular diagnostics is projected to expand at a 12.04% CAGR through 2031.

- By technology, ELISA accounted for 31.96% of the India in-vitro diagnostics market share in 2025; next-generation sequencing is advancing at a 16.00% CAGR to 2031.

- By product category, reagents & kits commanded 64.78% of the India in-vitro diagnostics market size in 2025; software & services will grow the fastest at 14.55% CAGR to 2031.

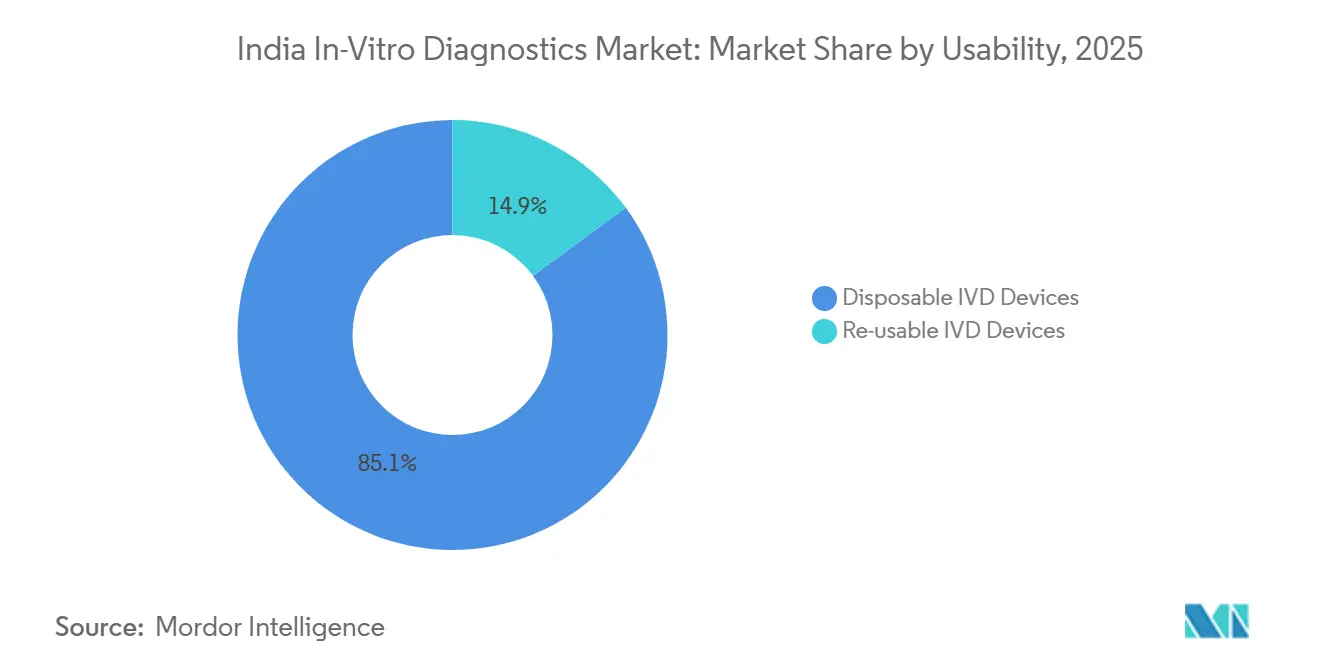

- By usability, disposable devices captured 84.52% of 2025 revenue, whereas reusable devices are forecast to rise at a 10.09% CAGR.

- By testing site, central laboratories held 69.35% share in 2025, yet point-of-care platforms are set to grow at 14.93% CAGR.

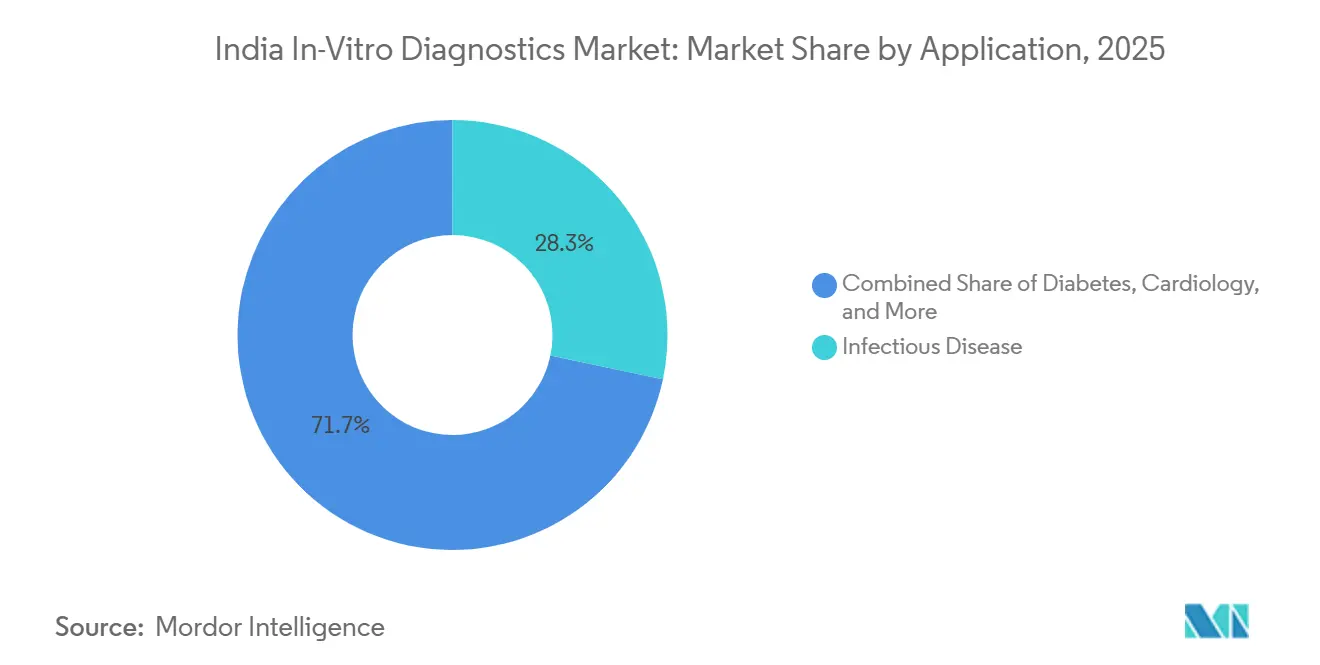

- By application, infectious disease testing led with 28.05% share in 2025; cancer/oncology diagnostics is expanding at 14.08% CAGR through 2031.

- By end-user, diagnostic laboratories retained 54.12% share in 2025, while hospitals & clinics are expected to log 13.75% CAGR to 2031.

- By specimen type, blood dominated with 54.48% share in 2025, while saliva specimens are projected to expand at a 12.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dual burden of communicable and non-communicable diseases | +1.8% | National, higher in urban centres | Medium term (2-4 years) |

| Expanding health-insurance coverage & incomes | +1.2% | Urban, expanding to tier-2/3 cities | Medium term (2-4 years) |

| Public lab infrastructure under National Health Mission | +0.9% | National, emphasis on rural | Long term (≥ 4 years) |

| High-throughput automation & AI adoption | +1.4% | Metro cities, spreading to tier-2 | Medium term (2-4 years) |

| Digital health ecosystem integration | +0.7% | Urban and semi-urban | Medium term (2-4 years) |

| Private lab chain expansion | +0.5% | Tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Dual Burden of Communicable & Non-Communicable Diseases Necessitating Early Diagnostics

Tuberculosis still represents 27% of global cases traced to India, prompting a shift from microscopy to rapid molecular assays that offer higher sensitivity and same-day results. National Family Health Survey data show anemia prevalence of 57% among women and 67% among children under five, driving hematology test demand[1]Frontiers in Health Services, “Enhancing Anemia Diagnostics and Accessibility in India,” frontiersin.org. Parallel growth of diabetes, now affecting 101 million citizens, and rising cardiovascular morbidity are pushing clinical chemistry and immunoassay volumes. Laboratories therefore broaden menus to run infectious disease panels alongside lipid, HbA1c, and cardiac marker testing on integrated platforms. Precision-oriented test adoption is accelerating in oncology as liquid biopsy assays identify actionable mutations without invasive biopsies, underlining why comprehensive diagnostics sit at the centre of India in-vitro diagnostics market development.

Expanding Health-Insurance Penetration & Disposable Incomes Enhancing Test Affordability

Insurance coverage has climbed from 25% to 51% of the population through flagship schemes such as Pradhan Mantri Jan Arogya Yojana. Reimbursement of laboratory procedures is lowering out-of-pocket spending and steering patients toward accredited sites. Growing volumes help labs amortise investments in high-throughput PCR, NGS, and chemiluminescence platforms, enabling price cuts that lure middle-income segments in tier-2 urban belts. Insurers are tightening quality criteria, compelling smaller centres to secure NABL accreditation or partner with organised chains. The resulting virtuous cycle of affordability, quality, and scale improves market depth across the India in-vitro diagnostics market.

Government Investments in Public Laboratory Infrastructure under National Health Mission

The Free Diagnostics Service Initiative has standardised minimum test lists across India’s health-care tiers, from 14 procedures at Sub Centres to 134 at District Hospitals[2]Ministry of Health and Family Welfare, “Free Drugs & Diagnostics Service Initiative,” nhm.gov.in. States such as Tamil Nadu recorded 8.67 million beneficiaries in Tiruchirappalli and 7.98 million in Pudukottai during 2024-25, underscoring public sector pull for reagents, analysers, and quality controls. Public-private partnerships invite reagent vendors and equipment makers to supply on cost-per-test contracts, enlarging addressable demand. Workforce skilling initiatives attached to the program are easing the shortage of lab technologists, a critical enabler for equitable expansion of the India in-vitro diagnostics market.

Adoption of High-Throughput Automation & AI in Laboratories Elevating Efficiency

Laboratories face 14-15% annual test volume growth while staff capacity rises only 3-4%. Automation bridges the gap by loading hundreds of samples per hour with minimal hands-on time. AI augments both workflow and clinical interpretation; algorithms embedded in haematology analysers flag slide review triggers and camera-enabled POCT devices detect anaemia with 94% accuracy in field settings. Predictive maintenance software pre-empts analyser downtime by identifying drift before quality control failures occur. Chains that deploy AI at central labs and satellites achieve uniform reporting standards, positioning themselves at the forefront of the India in-vitro diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket spending | -0.7% | National, higher in rural/semi-urban | Medium term (2-4 years) |

| Dependence on imported instruments & inputs | -0.5% | National | Medium term (2-4 years) |

| Limited cold-chain & logistics infrastructure | -0.6% | Rural and remote | Long term (≥ 4 years) |

| Fragmented regulatory approval pathway | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Cold-Chain & Logistics Infrastructure Restricting Rural Reagent Distribution

One-fifth of temperature-sensitive health products degrade because trucks and storage points cannot sustain 2-8°C. Portable battery-powered units like Phloton hold reagents at 4-6°C for 10 hours, but deployment is nascent. Widespread solar refrigeration roll-outs and passive insulated packaging are being tested to widen rural reach. Cold-chain gaps particularly hinder molecular and immunoassay expansion, slowing rural contribution to the India in-vitro diagnostics market.

Fragmented Regulatory Approval Pathway Increasing Time-to-Market

CDSCO categorises IVDs across four risk classes, each with separate documentation and fee structures. Mandatory local clinical validation after the October 2024 waiver rollback increases timelines for AI-enabled and high-risk assays. Only 12 states have adopted the Clinical Establishments Act, so accreditation requirements differ by location. Harmonised guidance and accelerated review lanes for priority diagnostics would speed innovation diffusion within the India in-vitro diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segmental Analysis

By Test Type: Molecular Diagnostics Reshapes Testing Paradigm

Clinical chemistry retained 24.8% of 2024 revenue through routine lipid, liver, renal, and metabolic panels that guide chronic disease management in both urban and rural settings. The segment’s core appeal is standardised workflows and low per-test cost that align with overburdened public health budgets. In parallel, molecular diagnostics is pacing the India in-vitro diagnostics market at a 12.5% CAGR as real-time PCR and cartridge-based nucleic acid tests deliver fast tuberculosis, HPV, and viral load results that directly inform therapy.

Integrated test menus are expanding further into oncology through liquid biopsy and hotspot mutation panels. Laboratories that once procured single-gene PCR kits now deploy multiplex NGS to detect hundreds of variants in one run, cutting per-sample cost while elevating clinical insight. Emerging antimicrobial resistance panels that detect resistance genes in under two hours are also pulling molecular technology into routine microbiology workflows. The transition underscores the overall shift toward actionable, personalised data that define next-generation care pathways across the India in-vitro diagnostics market.

By Technology: NGS Drives Precision Diagnostics Revolution

ELISA preserved 32.5% revenue share in 2024 due to simple hardware, broad analyte menus, and reagent affordability. The method remains preferred for hormone, infection-serology, and allergy profiles. Yet next-generation sequencing, forecast to climb 16.5% CAGR, is revolutionising tumour profiling, minimal residual disease tracking, and pathogen genome surveillance. Laboratories in Bengaluru, Hyderabad, and Pune have installed mid-throughput benchtop sequencers that process up to 96 samples in parallel, shrinking costs below USD 180 per test.

Polymerase chain reaction, chemiluminescence, and rapid lateral-flow formats remain vital for decentralised screening, but the precision and multitarget depth of NGS place it at the cutting edge of therapeutic decision support. Sequencing output feeds national genomic databases and informs public health interventions during outbreaks. As reagent kit costs fall and bioinformatics pipelines standardise, NGS penetration will widen from apex centres to large tertiary hospitals, reinforcing the high-technology profile of the India in-vitro diagnostics market.

By Product: Software & Services Accelerate Digital Transformation

Reagents and kits generated 65.4% of 2024 revenue, reflecting continuous consumable pull across immunoassay, chemistry, and haematology lines. Their recurring nature underpins stable cash flows for manufacturers and distributors. Software & services, however, will grow 15% CAGR as cloud-linked laboratory information systems, AI-powered analytics dashboards, and cybersecurity tools become integral to operational resilience[3]International Journal for Multidisciplinary Research, “Laboratory Management Information Systems in India,” ijfmr.com.

Pharma-grade quality management modules are automating proficiency testing, while rule-based engines trigger reflex testing workflows that cut manual approvals and improve result consistency. Instrument-agnostic middleware unites multi-brand analysers on a single interface, providing real-time cost-per-test transparency. This blend of hardware, consumables, and digital intelligence epitomises the evolving value proposition inside the India in-vitro diagnostics market.

By Usability: Disposable Devices Dominate Through Convenience

Single-use test strips, cassettes, and microfluidic cartridges held 85.1% share in 2024 by eliminating cross-contamination risk, reducing biosafety requirements, and speeding patient-side workflows. From rapid malaria cassettes to integrated PCR cartridges, disposables fit primary-care clinics and mobile vans that lack sterilisation facilities.

Reusable devices, projected at 10.3% CAGR, are gaining as sustainability mandates push for reduced biomedical waste. Robust plastics tolerate multiple autoclave cycles, and modular analyser parts such as cuvettes and probe heads are designed for refurbishment. Hybrid semi-disposable platforms will likely bridge infection control and eco-design, sustaining innovation momentum across the India in-vitro diagnostics market.

By Testing Site: Point-of-Care Testing Expands Diagnostic Access

Central laboratories processed 70% of 2024 samples, leveraging economies of scale and skilled technologists to run comprehensive menus including high-throughput chemiluminescence and NGS. Automation lines in metros now exceed 8,000 tests per hour, securing low unit costs.

Point-of-care testing, growing 15.5% CAGR, puts creatinine, HbA1c, dengue NS1, and COVID-19 antigen assays into PHC outposts and ambulances. AI-enabled readers guide users through steps and transmit results to cloud dashboards via 4G. Hybrid care models combining central confirmation with on-site triage minimise delays, particularly in stroke and sepsis pathways, anchoring future growth across the India in-vitro diagnostics market.

By Specimen Type: Saliva Testing Gains Momentum

Blood retained 55% share in 2024 because it hosts systemic biomarkers for chemistry, immunology, and haematology. High-throughput auto-analysers process serum and plasma with minimal operator intervention, sustaining leadership.

Saliva, advancing at 13% CAGR, offers painless collection and is increasing in hormonal, genetic, and infectious disease applications. Microfluidic test cards now quantify cortisol, HIV antibodies, and SARS-CoV-2 RNA in under 20 minutes. Expanded analyte validation and smartphone-linked readers are pushing saliva closer to mainstream screening, widening specimen diversity inside the India in-vitro diagnostics market.

By Application: Cancer Diagnostics Drives Precision Medicine

Infectious disease panels accounted for 28.3% of 2024 revenue as tuberculosis, dengue, and emerging viral threats dominate public health priorities. Multiplex PCR cartridges, CLIA antigen assays, and antimicrobial resistance genotyping underpin this leadership.

Cancer diagnostics, projected at 14.6% CAGR, is propelled by rising incidence and precision medicine adoption. Lung tumour panels from tissue and plasma identify EGFR, ALK, and ROS1 alterations in 52% of sequenced cases, informing targeted therapy selection. Companion diagnostic partnerships between oncologists and labs are deepening, positioning oncology as the next high-growth pillar of the India in-vitro diagnostics market.

By End-user: Hospital Integration Enhances Clinical Workflow

Diagnostic laboratories captured 54.6% share in 2024 through extensive collection centre networks and scale-driven cost advantages. Organised chains standardise quality across dozens of cities, competing on turnaround and digital reporting.

Hospitals and clinics, growing 14.2% CAGR, embed laboratories within care pathways for emergency, obstetric, and oncology services. Integrated LIS-HIS interfaces deliver real-time alerts that influence same-visit prescribing. Home-care and self-testing alternatives, ranging from glucose meters to self-collected HPV sampling kits, add flexible access points, collectively broadening demand across the India in-vitro diagnostics market.

Geographical Analysis

Dense hospital clusters, insurance uptake, and advanced lab facilities enable NGS, mass spectrometry, and AI slide-reading to flourish. Competitive pricing and high patient awareness accelerate technology refresh cycles, strengthening the India in-vitro diagnostics market size in metros.

Tier-2 and tier-3 cities are the fastest-expanding pockets. Organised chains install spoke collection sites linked to regional reference labs, spreading costs over higher sample volumes. Government free-diagnostics schemes further lift test utilisation at district hospitals in Tamil Nadu, Punjab, and Odisha. Rising incomes, along with employer-sponsored insurance, are creating sustained volume for chemistry, immunoassay, and basic molecular services.

Key barriers include electricity shortages, cold-chain gaps, and manpower deficits. Point-of-care devices and telepathology bridges partially offset infrastructure limits. Portable cooling units and solar fridges are piloted to safeguard reagents in remote blocks. Continued public investment and digital connectivity will be required for rural catch-up inside the India in-vitro diagnostics market.

Competitive Landscape

The market is moderately fragmented, with thousands of standalone labs. The five largest diagnostic chains gain a minor share annually by acquiring regional firms and rolling out collection franchises. Multinational OEMs supply NGS, CLIA, and high-end PCR systems, while domestic manufacturers focus on low-cost rapid kits and mid-range biochemistry analysers tailored to local budgets.

Technology investments distinguish market leaders. Chains deploy conveyor-linked automation, AI cytology scanners, and integrated middleware to cut errors and accelerate turnaround. Vertical integration is emerging: some groups develop proprietary kits to protect margins, while others run data analytics platforms that monetise de-identified results for research collaborations. White-space opportunities lie in pharmacogenomics, non-invasive prenatal testing, and digital pathology, where penetration is still under 5%.

Competitive intensity also rises around outreach and brand. Providers differentiate by same-day reporting, home sample collection, mobile apps, and subscription health plans. Government tender participation for public-private laboratories offers volume guarantees that offset thin margins. Overall, the India in-vitro diagnostics market remains dynamic, with consolidation and technology convergence reshaping strategic playbooks.

India In-Vitro Diagnostics Industry Leaders

Roche Diagnostics India Pvt Ltd

Abbott Healthcare Pvt Ltd

Siemens Healthineers India

Transasia Bio-Medicals Ltd

Beckman Coulter India (Danaher)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ABL Diagnostics signed an exclusive distribution pact with Genient Tech Private Ltd. to commercialise DeepChek and UltraGene molecular assays across Indian laboratories, broadening access to advanced virology testing.

- August 2024: Siemens Healthineers received CDSCO manufacturing approval for its IMDX Mpox RT-PCR kit, which delivers results in 40 minutes and strengthens national outbreak readiness.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the India in-vitro diagnostics (IVD) market as the aggregate revenue generated in India from instruments, reagents, software, and connected services used to perform clinical laboratory, point-of-care, and home-based diagnostic tests across all major technologies, including immunoassay, molecular, clinical chemistry, hematology, and microbiology, on human specimens.

Scope exclusion: veterinary diagnostics and research-only kits are outside our figures.

Segmentation Overview

- By Test Type

- Clinical Chemistry

- Immuno-Diagnostics

- Haematology

- Molecular Diagnostics

- Coagulation

- Microbiology

- Others

- By Technology

- Polymerase Chain Reaction (PCR)

- Reverse Transcription PCR (RT-PCR)

- Next-Generation Sequencing

- Enzyme-Linked Immunosorbent Assay (ELISA)

- Chemiluminescence

- Rapid Antigen / Lateral Flow

- By Product

- Instruments / Analysers

- Reagents & Kits

- Software & Services

- By Usability

- Disposable IVD Devices

- Re-usable IVD Devices

- By Testing Site

- Central Laboratory Testing

- Point-of-Care Testing

- By Specimen Type

- Blood

- Urine

- Saliva

- Other Body Fluids

- By Application

- Infectious Disease

- Diabetes

- Cancer / Oncology

- Cardiology

- Auto-immune Disorders

- Nephrology

- Others

- By End-user

- Diagnostic Laboratories

- Hospitals & Clinics

- Home-care & Self-testing

- Academic & Research Institutes

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews with medical laboratory directors, reagent manufacturers, trade distributors, and pay-insurer executives across Tier-1 to Tier-3 cities. These conversations validated utilization rates, monthly kit pull-through, reagent-to-instrument ratios, and tariff dynamics that secondary data could not fully resolve.

Desk Research

We began with government sources such as the National Health Profile, India Brand Equity Foundation device export tables, and CDSCO registration rolls, which give foundational volumes, installed base, and regulatory pipelines. Trade bodies like the Association of Diagnostic Manufacturers and the Indian Medical Device Industry Association supplied shipment trends and price corridors, while peer-reviewed journals in IJMR clarified test utilization by disease area. Company filings, IPO prospectuses, and tender portals (GeM, Tenders Info) helped us benchmark average selling prices. Select proprietary databases, D&B Hoovers for lab chain financials and Questel for patent momentum, added depth.

Because open data seldom capture private lab throughput, we supplemented public material with reputable news aggregators (Dow Jones Factiva) to monitor expansion announcements and pricing shifts. The sources listed are illustrative; many additional references informed data collection, sense-checks, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction links Ministry-reported test volumes, import-export codes, and private lab revenue disclosures, then cross-checks with selective bottom-up roll-ups from leading analyzer cohorts to refine totals. Key drivers in our model include diabetes prevalence, RT-PCR capacity additions, PLI-backed reagent plant starts, NABL-accredited lab count, and per-capita health-insurance coverage; each variable is forecast through multivariate regression and scenario analysis before feeding the CAGR engine. Gap pockets in bottom-up samples are balanced with channel-check-derived adjustment factors.

Data Validation & Update Cycle

Outputs pass multi-stage variance checks, senior-analyst peer review, and anomaly flags versus independent signals. Reports refresh yearly, and material events, such as reimbursement resets or infectious-disease surges, trigger interim updates; an analyst re-validates figures just before client delivery.

Why Mordor's India In-Vitro Diagnostics Baseline Commands Reliability

Published estimates often diverge because firms select different product mixes, price bases, and refresh cadences.

Key gap drivers include whether home self-tests are counted, how gray-market imports are treated, exchange-rate timing, and the way forecast elasticity for reagent ASPs is built.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.82 B (2025) | Mordor Intelligence | - |

| USD 5.30 B (2024) | Global Consultancy A | Includes veterinary and OTC self-tests; uses uniform ASP uplift without channel splits |

| USD 4.02 B (2024) | Regional Consultancy B | Uses hospital billings as proxy, assumes single-digit public-lab share, annual refresh absent |

The comparison shows that larger figures stem from broader scopes or unverified price mark-ups, whereas Mordor's disciplined variable selection, annual refresh, and dual-path validation offer decision-makers a balanced, transparent baseline they can trace back to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current value of the India in-vitro diagnostics market?

The market is valued at USD 1.94 billion in 2026 and is expected to reach USD 2.66 billion by 2031.

Which segment is growing the fastest in the India in-vitro diagnostics market?

Molecular diagnostics is expanding the quickest, advancing at a 12.04% CAGR between 2026 and 2031.

How much of the India in-vitro diagnostics market share do reagents and kits hold?

Reagents and kits held 64.78% of revenue in 2025 thanks to their recurring-consumable nature.

Why is next-generation sequencing important for the India in-vitro diagnostics industry?

NGS enables comprehensive genomic profiling for oncology, infectious disease surveillance, and hereditary disorder diagnosis while growing at a 16.00% CAGR.

What limits diagnostic expansion in rural India?

Limited cold-chain infrastructure, shortage of trained personnel, and high out-of-pocket costs constrain rural test availability.

How are private diagnostic chains influencing the market?

Organised chains expand through acquisitions and hub-and-spoke models, bringing advanced testing and competitive pricing to tier-2 and tier-3 locations.

Page last updated on: