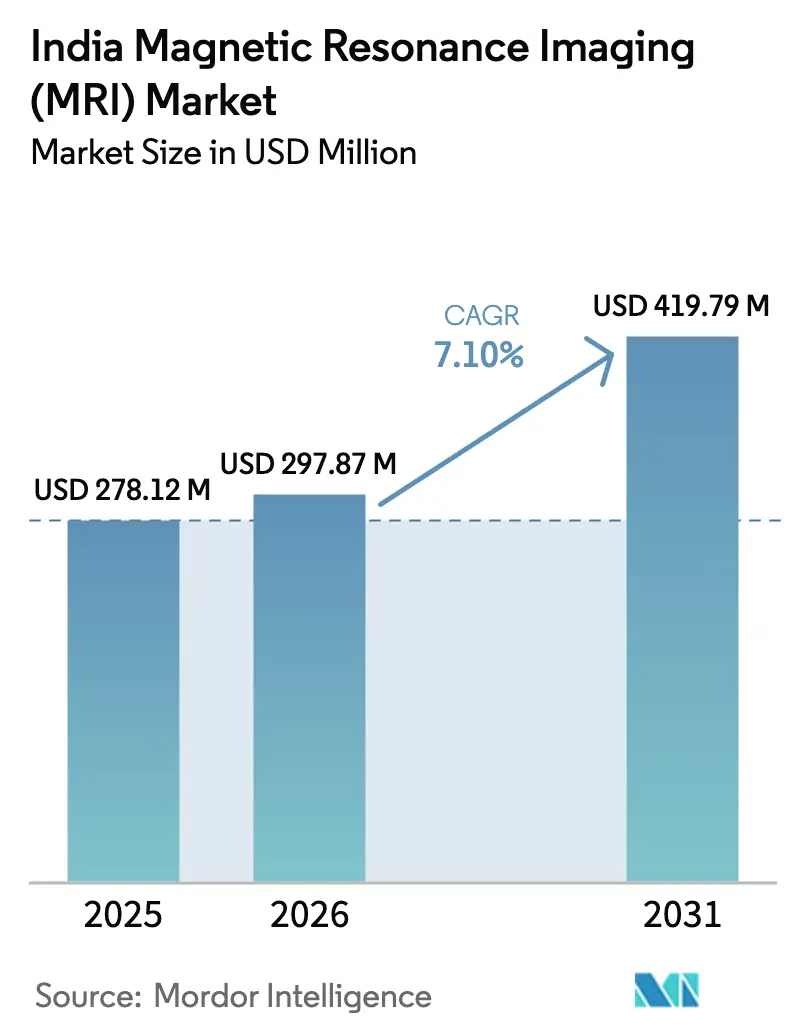

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 278.12 Million |

| Market Size (2026) | USD 297.87 Million |

| Market Size (2031) | USD 419.79 Million |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Magnetic Resonance Imaging (MRI) Market Analysis by Mordor Intelligence

India Magnetic Resonance Imaging (MRI) market size in 2026 is estimated at USD 297.87 million, growing from 2025 value of USD 278.12 million with 2031 projections showing USD 419.79 million, growing at 7.10% CAGR over 2026-2031. The India MRI market is expanding because non-communicable diseases (NCDs) now account for nearly 66% of the country’s total disease burden, and clinicians rely on high-resolution MRI scans to detect tumors, neurological lesions, and complex musculoskeletal injuries at earlier stages. Private diagnostic-center chains continue to roll out new facilities across tier-2 and tier-3 cities, amplifying India MRI market adoption outside the traditional metro strongholds. Public-hospital upgrades under Ayushman Bharat funnel additional capital toward advanced imaging suites, while Production Linked Incentive (PLI) schemes make locally manufactured scanners a cost-effective alternative for value-conscious buyers, further stimulating India MRI market demand. The convergence of AI-enabled workflow automation, helium-lean magnet architectures, and patient-comfort innovations supports sustainable profitability for providers, keeping the India MRI market’s growth trajectory intact through 2030.

Key Report Takeaways

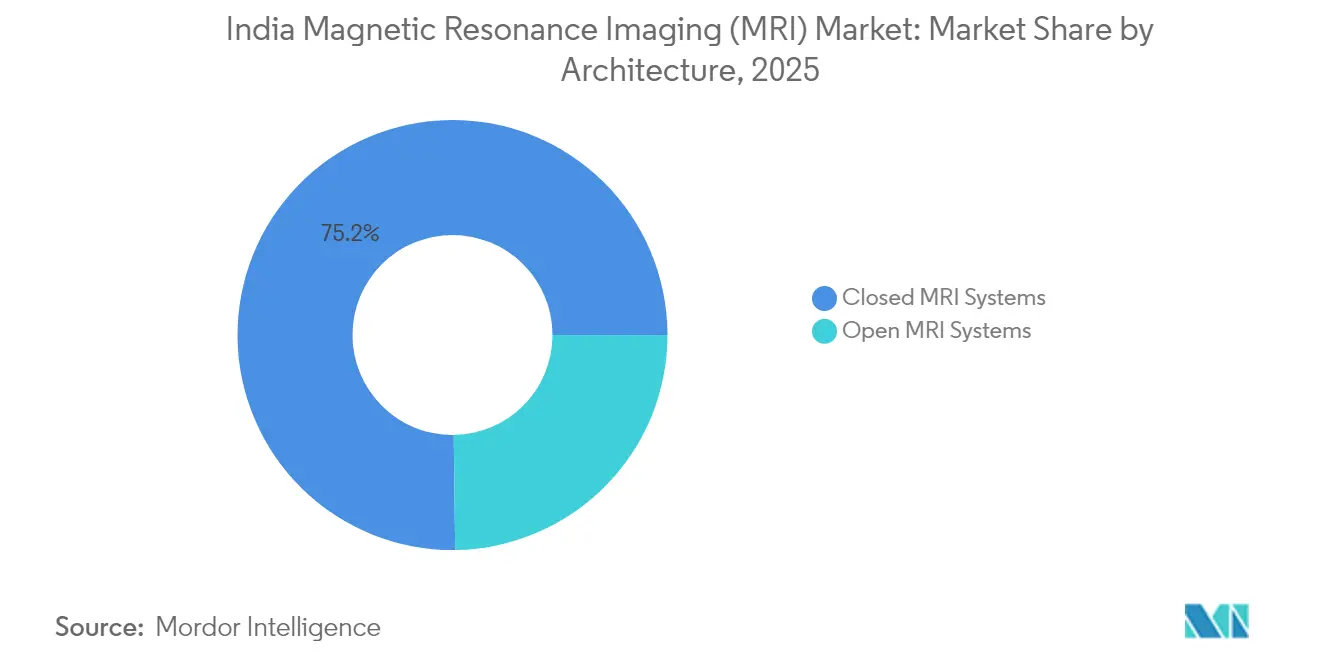

- By architecture, closed MRI systems led with 75.20% revenue share in 2025, while open systems are forecast to expand at an 8.05% CAGR through 2031, highlighting their status as the fastest-growing segment within the India Magnetic Resonance Imaging (MRI) Market.

- By field strength, 1.5 T high-field systems commanded 55.72% share of the India Magnetic Resonance Imaging (MRI) Market size in 2025, and very-high field (≥3 T) systems are advancing at a 7.72% CAGR between 2026-2031.

- By application, neurology captured 42.00% of India Magnetic Resonance Imaging (MRI) Market share in 2025, while oncology is projected to grow at an 8.08% CAGR through 2031.

- By end user, hospitals accounted for a 47.68% share of the India Magnetic Resonance Imaging (MRI) Market size in 2025, whereas specialized clinics & imaging centers are rising at an 8.65% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Magnetic Resonance Imaging (MRI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising NCD burden | +1.8% | Urban and peri-urban clusters nationwide | Medium term (2–4 years) |

| Expansion of private diagnostic-center chains & medical tourism | +1.5% | Tier-2 and tier-3 cities; tourism corridors | Short term (≤ 2 years) |

| Public-hospital imaging upgrades under Ayushman Bharat | +1.2% | Rural districts and aspirational blocks | Long term (≥ 4 years) |

| AI-enabled high-field imaging boosts throughput & quality | +1.0% | Metro health hubs, expanding to secondary cities | Medium term (2–4 years) |

| Make-in-India MRI manufacturing lowers cap-ex | +0.9% | Bengaluru, Chennai, Pune and Noida industrial clusters | Long term (≥ 4 years) |

| Ban on refurbished imports shifts demand to new units | +0.7% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising NCD Burden Accelerates Diagnostic Imaging Demand

India’s escalating NCD prevalence raises the clinical urgency for high-resolution soft-tissue imaging. Cancer incidence is expected to climb from 529.40 per 100,000 in 2022 to 549.17 per 100,000 by 2031, underpinning structural demand for MRI-based oncology diagnostics. Stroke, epilepsy, and neuro-degenerative conditions also continue to rise, so neurologists increasingly prescribe MRI scans for finer lesion mapping, boosting daily scanner utilization, particularly in secondary cities where care gaps remain acute. Government screening programs for breast and cervical cancer routinely direct patients toward MRI for confirmatory scans, embedding the modality into standard care pathways. Health-insurance payouts under Ayushman Bharat further raise affordability for low-income households, sustaining patient-volume growth in the India MRI market. Consequently, providers view MRI capacity expansion as a prerequisite for clinical relevance as disease patterns evolve.

Expansion of Private Diagnostic-Center Chains & Medical Tourism

Organized diagnostic networks such as Dr. Lal PathLabs, Neuberg, and Metropolis collectively operate over 1,500 imaging hubs, and the number could double by 2028 as asset-light franchise models reduce capital intensity. These groups channel fresh scanner installations into smaller cities where competition is limited, thus diffusing India MRI market penetration beyond metro clusters. In parallel, medical-tourism arrivals rose to 463,725 visas in 2024 as foreign patients sought cost-advantaged cancer, spine, and cardiac care bundled with MRI diagnostics.[1]Nushaiba Iqbal, “How India is turning into a popular medical-tourism hub,” indiaspend.com Hospitals in Delhi, Chennai, and Kochi advertise fixed-price oncology packages that include pre- and post-surgical 3 T MRI scans, reinforcing MRI as a revenue anchor. Such inbound traffic incentivizes providers to install premium-spec systems with AI-accelerated throughput to maintain service levels. The dual tailwind of domestic and foreign demand keeps scanner-purchase pipelines healthy for OEMs and local assemblers.

Public-Hospital Imaging Upgrades Under Ayushman Bharat

The central government budgeted INR 90,659 crore (USD 11.3 billion) for the Ministry of Health & Family Welfare in FY 2024–25, with a notable slice earmarked for diagnostic-equipment modernization. More than 8,700 public health facilities completed upgrades in FY 2023–24, many of which involved installing new 1.5 T magnets to fulfill Ayushman Bharat referral commitments. Five greenfield All India Institute of Medical Sciences (AIIMS) campuses that opened in 2024 each added at least two 3 T scanners, creating training hubs for advanced neuroradiology. State governments mirror this momentum: Tamil Nadu’s health-infrastructure program funded 26 scanners in district hospitals, anchoring localized MRI services that previously required referrals to metro centers. Because public hospitals still conduct roughly 35% of all scans nationwide, the ripple effect on India MRI market volumes is decisive and long lasting.

AI-Enabled High-Field Imaging Boosts Throughput & Quality

AI-embedded reconstruction engines shrink average scan times from 30 minutes to under 10 minutes for routine neuro and MSK protocols, thereby tripling per-scanner daily throughput in busy outpatient settings. Siemens Healthineers’ MAGNETOM Flow and Philips’ SmartSpeed Precise platforms integrate zero-click protocol selection, relieving technologists of repetitive control-panel tasks and mitigating operator shortages. Diagnostic chains leverage these efficiency gains to drive same-center revenue without adding floorspace, strengthening the investment case for premium-priced systems in the India MRI market. AI-based denoising also lets providers down-field to 1.5 T systems for certain tasks, easing helium and power burdens while preserving image fidelity—an attractive proposition for facilities coping with utility-cost spikes. As radiologist burnout mounts, AI-assisted precohorting and lesion-flagging deliver interpretive consistency, thereby elevating clinical acceptance and boosting competitive advantage for facilities that adopt next-gen scanners early.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High scanner cost & low reimbursement tariffs | -1.4% | All states, acute in low-income districts | Medium term (2–4 years) |

| Shortage of trained radiologists/technologists | -1.1% | Tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Helium supply volatility elevates opex | -0.8% | Nationwide | Short term (≤ 2 years) |

| CDSCO approval lags for >3 T systems | -0.6% | Nationwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Scanner Cost & Low Reimbursement Tariffs

Imported 1.5 T or 3 T scanners cost INR 6–9 crore (USD 730,000–1.1 million at FY 2024 exchange rates), a steep hurdle for small hospitals serving low-to-middle-income populations. Government reimbursement under Ayushman Bharat averages INR 3,000 (USD 36) per scan, barely covering electricity, helium, and maintenance. Consequently, many district-level facilities limit MRI utilization to complex cases, undercutting economies of scale and elongating ROI timelines beyond seven years. Although domestic manufacturing promises lower prices, early units still face validation delays, prolonging the affordability gap. Without tariff recalibration or bundled-payment alternatives, bottom-line pressure could temper India MRI market uptake in cost-constrained geographies.

Shortage of Trained Radiologists/Technologists

India has roughly 15,000 practicing radiologists for a population exceeding 1.4 billion, equating to one specialist per 93,000 people, far below OECD norms.[2]ACR Bulletin, “How Will We Solve Our Radiology Workforce Shortage?” acr.org The 612 medical colleges graduate only about 1,200 radiologists annually, and most migrate to metros, leaving smaller cities underserved. Limited technologist training centers exacerbate bottlenecks; many institutions operate with a single technician running double shifts, raising burnout and quality-control risks. AI can automate select tasks, yet final interpretation still demands skilled oversight. Unless fellowship seats expand and tele-radiology networks scale nationally, the talent deficit could impede scanner-utilization rates and dilute India MRI market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Systems Maintain Dominance Amid Open MRI Innovation

Closed systems generated 75.20% of 2025 revenue in the India Magnetic Resonance Imaging market, reflecting provider preference for higher signal-to-noise ratios essential for neuro-oncology and vascular imaging. The sealed bore design also supports gradient strengths above 45 mT/m, enabling advanced diffusion and functional protocols that smaller clinics use to attract complex referrals. High utilization levels keep per-scan costs competitive, reinforcing closed scanners as the workhorse of the India Magnetic Resonance Imaging market. Patient comfort, however, remains a pain point; claustrophobia-induced cancellations can reach 8% in urban centers, prompting providers to explore supplemental open-system capacity.

Open systems, though holding only 24.80% of 2025 value, are projected to grow at 8.05% CAGR through 2031, outpacing the overall India Magnetic Resonance Imaging market. Better patient tolerance, bariatric-friendly table loads, and pediatric volumes drive adoption, especially within suburban diagnostic chains. AI-powered image-reconstruction software narrows the historical resolution gap, letting providers conduct routine spine and MSK studies with acceptable quality. Local OEMs leverage modular coil designs to shorten installation footprints, positioning open scanners as pragmatic expansion units where real estate costs are high. As reimbursement parity between open and closed scans spreads beyond Karnataka and Maharashtra, incremental installations may accelerate, diversifying vendor portfolios and reducing the dominance of sealed-bore architectures.

By Field Strength: High-Field 1.5 T Dominance Faces Ultra-High Field Challenge

1.5 T scanners captured 55.72% of the India Magnetic Resonance Imaging market size in 2025, balancing diagnostic versatility with infrastructure friendliness; they require only 600 sq ft of shielded space and standard 45 kVA power. Public hospitals favor 1.5 T for broad-spectrum applications—from trauma triage to liver volumetry—maximizing reimbursement throughput. Domestic manufacture could trim acquisition costs by 35–40%, preserving 1.5 T’s market lead through 2031. Yet academic centers seek finer gradient fidelity for research; thus, 3 T and higher systems, although currently 14% of installed base, are forecast to grow faster than the India Magnetic Resonance Imaging market at 7.72% CAGR.

Ultra-high field (7 T) remains niche because of CDSCO clearance lags and INR 40 crore (USD 4.8 million) price tags. Still, premier institutes in Delhi, Bengaluru, and Hyderabad are provisioning space for future 7 T suites, encouraged by early neuroscience grants from the Department of Biotechnology. Low-field systems (<1.5 T) maintain marginal presence in point-of-care stroke and neonatal ICUs; Hyperfine’s 0.064 T portable unit gained marketing authorization in 2024 and can fit into ambulance bays, hinting at decentralized imaging opportunities. Taken together, field-strength segmentation underscores stratified purchasing behavior within the India Magnetic Resonance Imaging market: value-driven district hospitals gravitate toward 1.5 T, while flagship centers stretch into the ultra-high field frontier to differentiate academic output.

By Application: Neurology Leadership Challenged by Oncology Growth

Neurology retained 42.00% share of India Magnetic Resonance Imaging market revenue in 2025, propelled by higher case volumes of stroke, multiple sclerosis, and epilepsy, which all demand soft-tissue contrast unachievable with CT. Epilepsy pre-surgical mapping, for instance, drives routine 3 T functional MRI referrals in tertiary centers. Post-COVID neurological sequelae also boost outpatient MRI bookings, raising per-scanner workloads in urban regions. The segment’s leadership derives from entrenched clinical guidelines and rising awareness among neurologists practicing beyond metros.

Oncology, holding 18.90% value in 2025, now expands at 8.08% CAGR, nearly 1 percentage-point faster than the overall India Magnetic Resonance Imaging market. Multiparametric MRI underpins prostate and breast-cancer screening algorithms that state insurance schemes increasingly reimburse. Hospitals leverage AI-assisted lesion-grading tools to reduce reporting variance, enticing oncologists to order MRI over PET-CT for pre-operative staging in select cancers. Musculoskeletal, cardiology, and abdominal applications collectively make up the remainder, each advancing in mid-single digits as sports-medicine clinics, interventional cardiology programs, and gastroenterology departments adopt MRI for functional assessments that avoid ionizing radiation.

By End User: Hospital Dominance Faces Specialized Center Competition

General and specialty hospitals generated 47.68% of 2025 revenue in the India Magnetic Resonance Imaging market, benefitting from integrated care pathways that funnel in-patients and emergency cases directly to in-house scanners. Network expansions by Apollo, Fortis, and Max add 2,000 new beds and at least 30 magnets through 2027, anchoring hospital share near the 50% threshold. Government hospitals, including five new AIIMS campuses, bolster public-sector demand with procurement budgets protected from currency swings.

Specialized clinics and imaging centers contributed 35.85% in 2025 but will climb fastest at 8.65% CAGR, capitalizing on outpatient convenience, shorter wait times, and aggressive marketing of health-check packages. Franchise models allow asset-light growth; combined with vendor financing, smaller centers can deploy mid-field scanners in cities of 300,000–800,000 people. Research and academic institutes, though fewer, invest in ultra-high field capabilities for translational projects, sustaining a pipeline for advanced applications that filter downstream into clinical practice. These dynamics reinforce a multi-tiered delivery model that broadens India Magnetic Resonance Imaging market penetration while sharpening competition for specialized talent and maintenance contracts.

Geography Analysis

India Magnetic Resonance Imaging market adoption remains uneven across regions. The north—including Delhi, Uttar Pradesh, and Haryana—commands roughly one-third of installed scanners thanks to a dense private-hospital network and medical-tourism inflows. Western states such as Maharashtra and Gujarat follow closely because of robust corporate health-insurance coverage among formal-sector employees. Southern hubs—Karnataka, Tamil Nadu, and Telangana—benefit from domestic manufacturing ecosystems that simplify spare-parts logistics and technician availability. Eastern states still lag; West Bengal’s per-capita scanner density is 40% below the national mean, while neighboring Odisha and Bihar depend heavily on centralized government hospitals for access. Government capital-grant programs aim to reduce this disparity, allocating funds for three new district imaging centers per underserved state in FY 2025–26, which should widen geographic reach for the India Magnetic Resonance Imaging market.

Urban areas dominate revenue, accounting for 70% of 2025 scans. Metro centers house multi-national hospital chains that run high-field and ultra-high field systems, catering to complex neurology and oncology cases. As land prices soar, these providers increasingly prefer compact 3 T units with 70 cm bore diameters and helium-free designs to lower operating costs. Suburban clusters evolve into overflow zones where mid-field scanners absorb elective imaging volume. Tier-2 cities such as Jaipur, Coimbatore, and Lucknow witness double-digit scanner growth as organized diagnostic chains establish satellite facilities, democratizing MRI access and reinforcing India Magnetic Resonance Imaging market momentum outside metro cores.

Rural utilization remains sparse. Only 14% of primary health-care blocks reported local MRI availability in 2024. Mobile 1.5 T vans funded under public-private partnerships now operate in Himachal Pradesh and Rajasthan, offering on-site scans two days weekly and forwarding images to tele-radiology hubs in Bengaluru. While these pilots cover fewer than 50 vans nationwide, early clinical audits report 92% patient-satisfaction rates. If scaled, such models could unlock latent demand among the 65% of Indians living in non-urban locales, materially altering the spatial dynamics of the India Magnetic Resonance Imaging market.

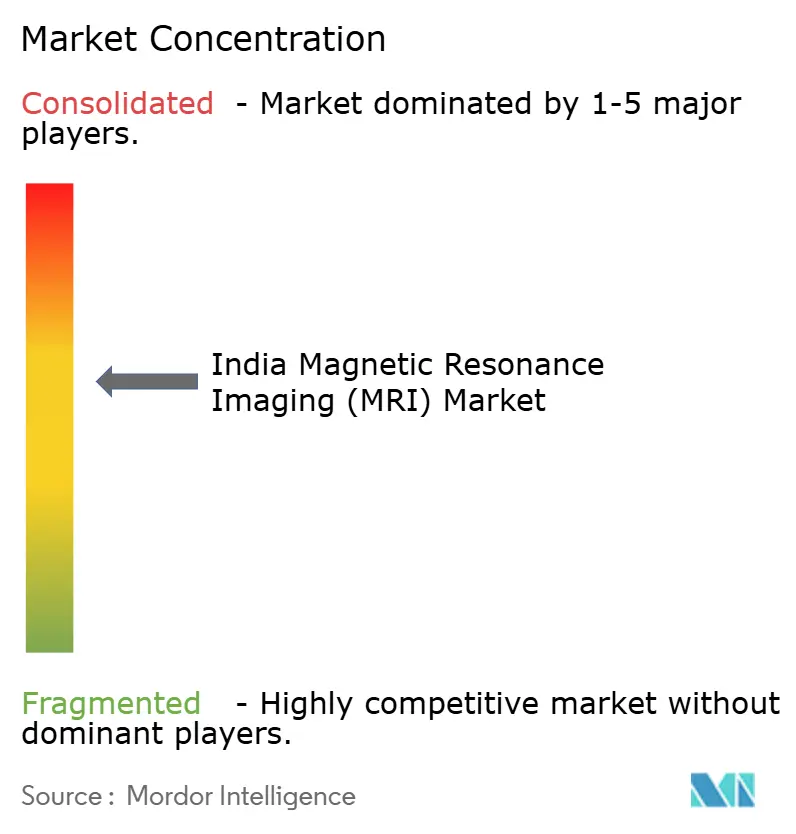

Competitive Landscape

The India Magnetic Resonance Imaging market hosts a mix of multinational heavyweights and emergent domestic innovators. Siemens Healthineers, Philips, and Wipro GE Healthcare jointly control a significant revenue share, leveraging extensive service networks and brand trust. Siemens invested EUR 60 million in its Kemnath production site to support Indian sub-assembly inflows, minimizing lead times for 1.5 T orders. Philips enlarged its Pune healthcare R&D campus to develop AI algorithms tailored to ethnic-specific imaging phenotypes, giving the firm localized software differentiation. Wipro GE pledged USD 960 million through 2028 to scale magnet and gradient-coil manufacturing in Bengaluru, aligning with PLI incentives.[3]Reuters, “Wipro GE Healthcare to invest $960 mln in R&D,” reuters.com

Domestic entrants rely on cost agility. Voxelgrids’ 1.2 T Made-in-India system lists at INR 2.8 crore (USD 340,000), undercutting imported rivals by 40%. Paras Defence works with SAMEER on 1.5 T prototypes that use indigenous cryocoolers to cut helium dependency by 60%. Although still small in volume, such players garner attention from midsize hospitals constrained by cap-ex budgets. The ban on refurbished imports further tilts procurement toward these local options, reshaping competitive parameters in the India Magnetic Resonance Imaging market.

Strategic collaborations intensify. Hyperfine appointed Radiosurgery India as distributor for its portable Swoop MRI, a move that targets neuro-ICU applications in 20 premium hospitals. GE partnered with the Tata Trusts cancer-care initiative to deploy 3 T scanners across new oncology hubs, locking in multi-year service contracts. Meanwhile, Promaxo secured funding from Zynext Ventures to explore decentralized urology MRI pods, hinting at segment-specific device proliferation. Overall, vendor rivalry now hinges on after-sales uptime, AI-software add-ons, and flexible financing—not just static magnet specifications—keeping pressure on all players to innovate continuously.

India Magnetic Resonance Imaging (MRI) Industry Leaders

-

Siemens AG

-

Canon Medial Systems

-

GE Healthcare

-

Fujifilm Holdings Corporation

-

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Hon’ble Lieutenant Governor of Delhi Vinai K. Saxena inaugurated the Mahajan Imaging & Labs Centre in Dwarka, which houses India’s first ultra-fast AI-powered Excel 3 T MRI scanner.

- April 2025: Paras Defence & Space Technologies announced its role in a SAMEER-led consortium to commercialize home-grown MRI technology aimed at lowering import dependence.

- March 2025: India’s first indigenous MRI scanner completed development for AIIMS Delhi installation, offering a projected 50% price reduction versus imports.

- May 2024: Hyperfine partnered with Radiosurgery India to market the Swoop portable MRI for neuro-critical care across tertiary hospitals.

India Magnetic Resonance Imaging (MRI) Market Report Scope

As per the scope of the report, magnetic resonance imaging is a medical imaging technique that is used in radiology to produce pictures of the anatomy and the physiological processes of the body. These pictures are further used to diagnose and detect the presence of abnormalities in the body.

India magnetic resonance imaging (MRI) market is segmented by Architecture (Closed MRI Systems, Open MRI Systems), Field Strength (Low-field (Less than 0.3 T), Mid-field (0.3–1.5 T), High-Field (3 T), Ultra-high Field (Above 3 T)), Application (Neurology, Musculoskeletal, Cardiovascular, Abdominal and Pelvic, Breast Imaging, and Oncology (Whole Body)), End User (Public Hospitals, Private Hospitals, Diagnostic Imaging Centers, Ambulatory Surgical Centers). The report offers the value (in USD million) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-field (Less than 0.3 T) |

| Mid-field (0.3–1.5 T) |

| High-field (3 T) |

| Ultra-high field (Above 3 T) |

By Application

| Neurology |

| Musculoskeletal |

| Cardiovascular |

| Abdominal & Pelvic |

| Breast Imaging |

| Oncology (Whole Body) |

By End User

| Public Hospitals |

| Private Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-field (Less than 0.3 T) |

| Mid-field (0.3–1.5 T) | |

| High-field (3 T) | |

| Ultra-high field (Above 3 T) | |

| By Application | Neurology |

| Musculoskeletal | |

| Cardiovascular | |

| Abdominal & Pelvic | |

| Breast Imaging | |

| Oncology (Whole Body) | |

| By End User | Public Hospitals |

| Private Hospitals | |

| Diagnostic Imaging Centers | |

| Ambulatory Surgical Centers |

Key Questions Answered in the Report

What is the projected value of the India Magnetic Resonance Imaging market in 2031?

The India Magnetic Resonance Imaging Market size is expected to reach USD 419.79 million by 2031.

Which architecture leads current adoption in India?

Closed MRI systems captured 75.20% revenue share in 2025.

Why are 1.5 T scanners still dominant?

They balance diagnostic versatility with lower infrastructure costs, giving them 55.72% share in 2025.

Which application is growing fastest?

Oncology scans are forecast to expand at an 8.08% CAGR through 2031.

Page last updated on: