Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

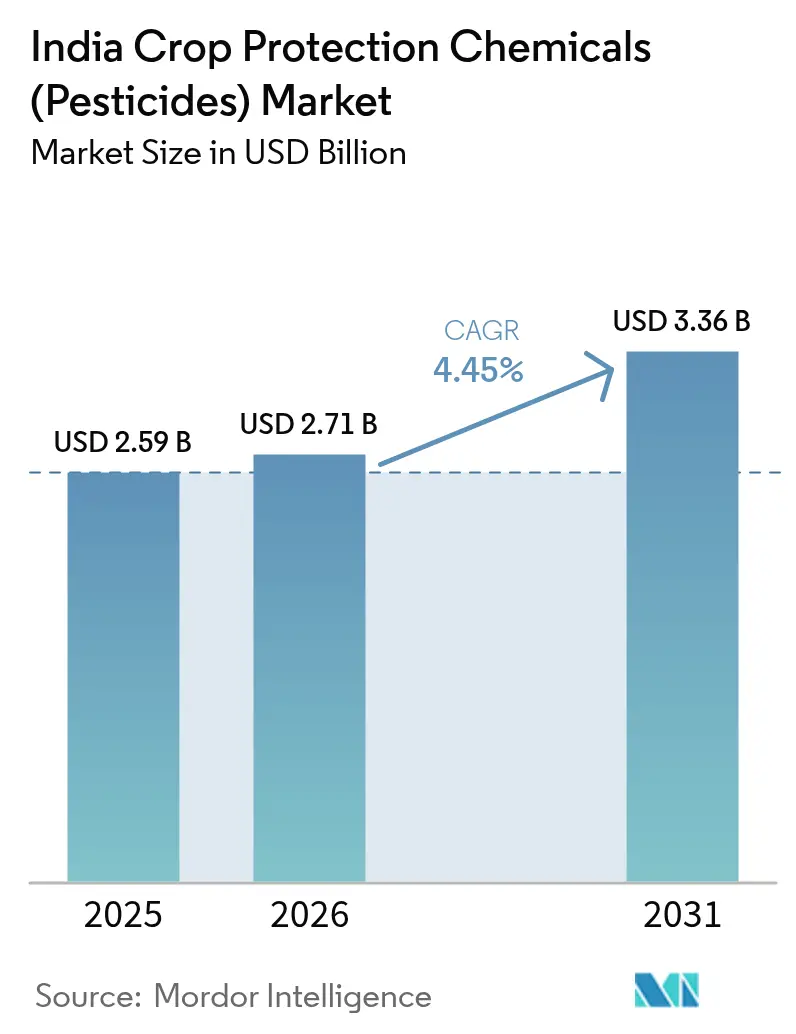

| Base Year Market Size (2025) | USD 2.59 Billion |

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 3.36 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Crop Protection Chemicals (Pesticides) Market Analysis by Mordor Intelligence

The India crop protection chemicals (pesticides) market size is expected to grow from USD 2.59 billion in 2025 to USD 2.71 billion in 2026 and is forecast to reach USD 3.36 billion by 2031 at 4.45% CAGR over 2026-2031. Rising adoption of precision‐driven digital farming, government incentives for indigenous manufacturing, and the need to counter pest resistance are steering steady demand growth. Farmers are shifting from blanket applications to data‐based prescriptions, trimming input waste and aligning with emerging sustainability standards. Public investment in digital agriculture infrastructure, including the USD 338 million Digital Agriculture Mission, will accelerate demand for products that integrate with soil mapping, drone spraying, and chemigation systems [1]Source: Ministry of Agriculture and Farmers Welfare, “Cabinet approves the Digital Agriculture Mission,” PIB.GOV.IN. However, market players must navigate frequent state bans on specific molecules, infiltration of counterfeit products in rural channels, and tightening residue regulations that favor safer formulations.

Key Report Takeaways

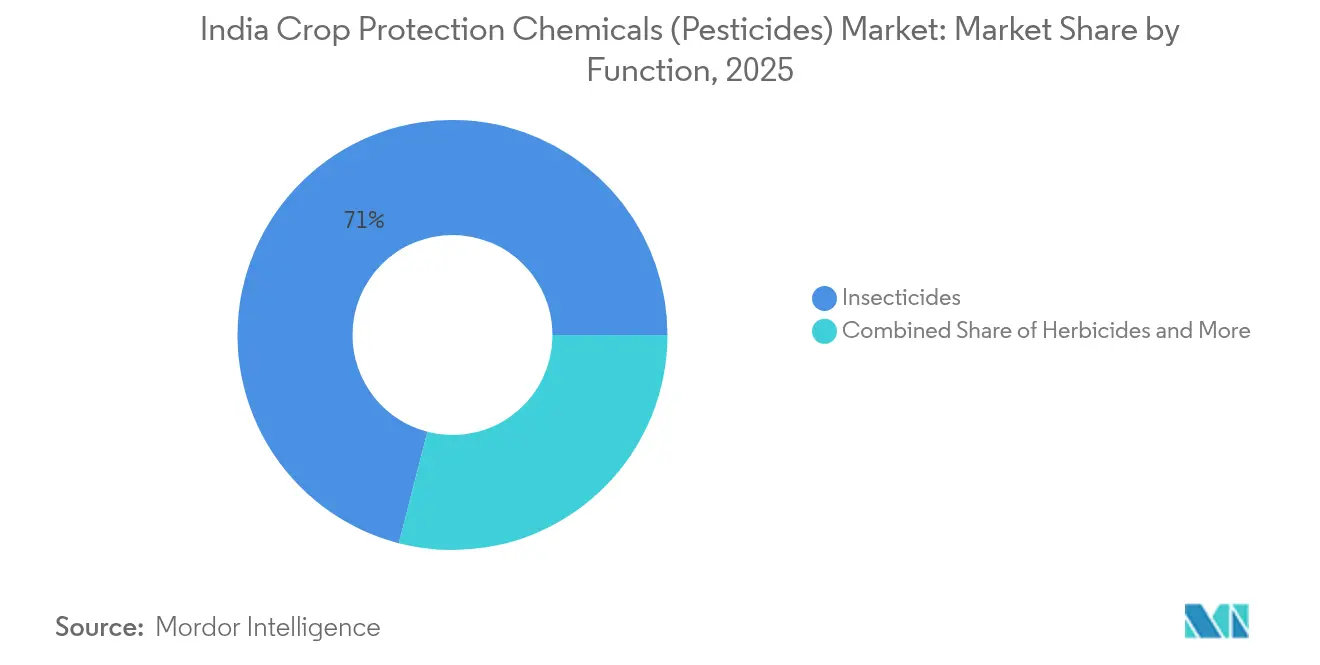

- By function, insecticides led with 70.98% of the India crop protection chemicals (pesticides) market share in 2025, while herbicides are projected to expand at a 8.55% CAGR to 2031.

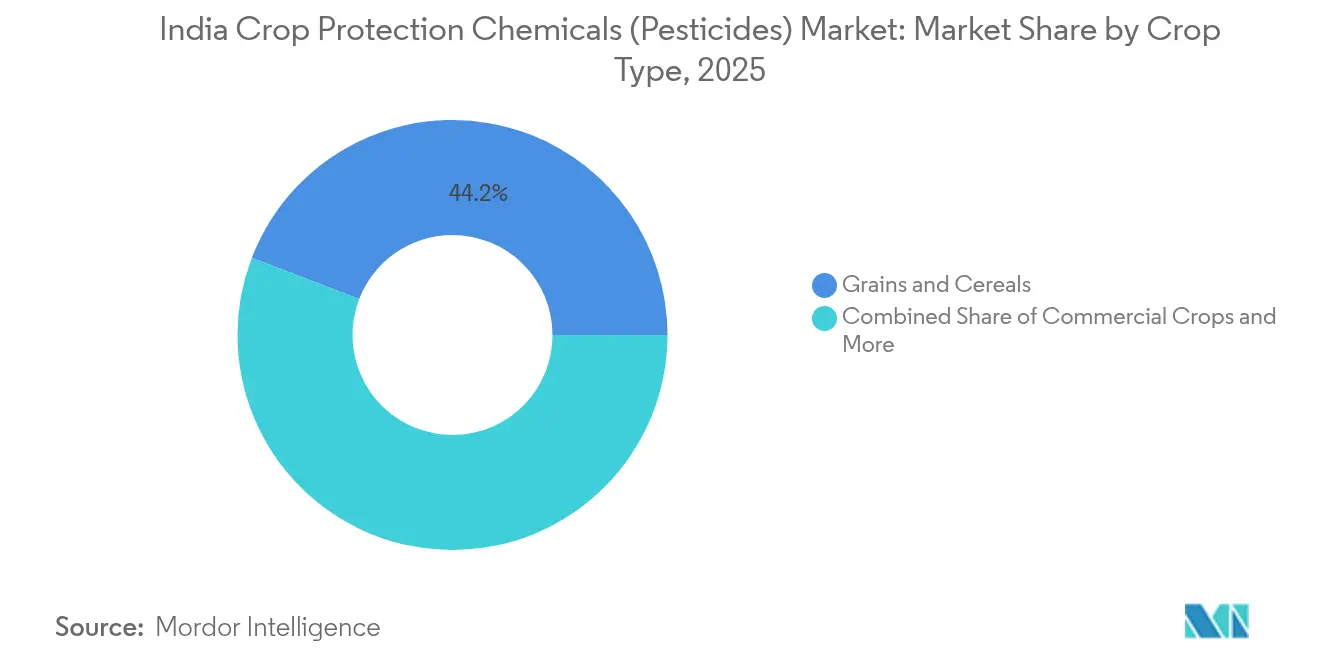

- By crop type, grains and cereals accounted for a 44.15% share of the India crop protection chemicals (pesticides) market size in 2025, while commercial crops post the fastest CAGR at 4.72% through 2031.

- By application mode, foliar spraying commanded 52.65% share of the India crop protection chemicals (pesticides) market size in 2025, whereas soil treatment is forecast to grow at a 5.92% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Crop Protection Chemicals (Pesticides) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidy extension for indigenous AI manufacturing | +1.2% | National, with concentration in Gujarat, Maharashtra, Andhra Pradesh | Medium term (2-4 years) |

| Rising pest-resistance incidences in rice and cotton | +0.8% | North India (Punjab, Haryana), Central India (Maharashtra, Madhya Pradesh) | Short term (≤ 2 years) |

| Expansion of micro-irrigation acreage boosting chemigation use | +0.6% | West India (Maharashtra, Gujarat), South India (Karnataka, Tamil Nadu) | Long term (≥ 4 years) |

| Shift toward herbicide-tolerant GM cotton hybrids | +0.5% | Central India (Maharashtra, Telangana), West India (Gujarat) | Medium term (2-4 years) |

| Precision-spraying drone adoption in sugarcane belt | +0.4% | North India (Uttar Pradesh), West India (Maharashtra) | Medium term (2-4 years) |

| Climate-induced locust migration risk across Rajasthan | +0.3% | West India (Rajasthan), extending to Gujarat, Madhya Pradesh | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government subsidy extension for indigenous AI manufacturing

Production Location Incentive schemes are catalyzing a structural shift toward domestic active ingredient manufacturing, reducing India's dependence on Chinese imports while strengthening supply chain resilience. The government's commitment to supporting backward-integrated agrochemical plants through PLI-style incentives has attracted significant private investment, with companies like Matix Fertilizers announcing INR 7,500 crore (USD 900 million) capacity expansion plans in 2024. This policy intervention addresses critical supply vulnerabilities exposed during the COVID-19 pandemic when import disruptions caused severe shortages. The focus on indigenous manufacturing is particularly strategic given China's dominance in intermediate chemicals, with domestic production capabilities reducing both cost volatility and geopolitical supply risks. Companies are leveraging these incentives to establish integrated manufacturing facilities that produce both technical-grade active ingredients and formulated products, capturing higher value-added margins while ensuring quality control throughout the production process.

Rising Pest-Resistance Incidences in Rice and Cotton

Escalating resistance patterns in key crops are forcing farmers to increase application frequencies and adopt novel chemistry classes, directly driving volume growth in the India crop protection chemicals (pesticides) market. Pink bollworm resistance to Bt cotton has reached critical levels in major cotton-producing states, compelling growers to supplement transgenic traits with conventional insecticides and rotate between different modes of action. Herbicide resistance in rice weeds, particularly against commonly used molecules like butachlor and pretilachlor, is spreading across the Indo-Gangetic plains, where continuous rice-wheat cropping systems create intense selection pressure. This resistance crisis is accelerating the adoption of newer chemistry classes and combination products that offer multiple modes of action. The Central Insecticides Board's approval of 46 new molecules by Super Crop Safe in 2024 reflects the industry's response to these resistance challenges. Farmers are increasingly willing to pay premium prices for effective solutions, creating opportunities for innovative formulations and integrated pest management approaches that combine chemical and biological control methods.

Expansion of Micro-Irrigation Acreage Boosting Chemigation Use

The rapid expansion of drip and sprinkler irrigation systems under government subsidy programs is creating new application pathways for India crop protection chemicals (pesticides) market through fertigation and chemigation systems. Micro-irrigation coverage has expanded significantly in high-value crops like sugarcane, cotton, and horticulture, where precise water and nutrient delivery systems can be adapted for pesticide application. This trend is particularly pronounced in water-stressed regions where farmers are adopting micro-irrigation to optimize water use efficiency while maintaining crop productivity. Chemigation offers superior application uniformity and reduced labor requirements compared to conventional spraying methods, making it attractive in regions facing acute agricultural labor shortages. The integration of digital soil health cards with precision irrigation systems enables farmers to apply crop protection pesticides based on real-time soil and crop health data, optimizing both efficacy and environmental stewardship. Companies are developing specialized formulations compatible with drip irrigation systems, including water-soluble concentrates and emulsifiable formulations that maintain stability in fertigation solutions.

Shift Toward Herbicide-Tolerant GM Cotton Hybrids

The unofficial but widespread adoption of herbicide-tolerant cotton varieties is driving substantial growth in post-emergence herbicide demand, particularly for glyphosate and glufosinate-based formulations. While regulatory approval for herbicide-tolerant cotton remains pending, farmer adoption has accelerated due to severe labor shortages for manual weeding and the economic advantages of chemical weed control. This trend is most pronounced in Maharashtra and Gujarat, where large-scale cotton cultivation and mechanization adoption create favorable conditions for herbicide-based weed management systems. The shift represents a fundamental change in cotton production practices, moving from labor-intensive cultivation toward mechanized, input-intensive systems that rely heavily on chemical weed control. Companies are positioning themselves to capitalize on this transition by developing herbicide formulations specifically optimized for cotton applications and establishing distribution networks in key cotton-growing regions. The regulatory uncertainty surrounding herbicide-tolerant traits creates both opportunities and risks, as policy changes could significantly impact demand patterns for specific herbicide classes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Frequent state-level bans on single AI products | -0.9% | National, with concentration in Punjab, Kerala, Andhra Pradesh | Short term (≤ 2 years) |

| Rising counterfeit product penetration in tier-3 markets | -0.7% | East India, Central India rural markets | Medium term (2-4 years) |

| Stringent draft regulation on 27 harmful molecules | -0.5% | National regulatory impact | Long term (≥ 4 years) |

| Acute labor shortages limiting labor-intensive foliar sprays | -0.4% | North India, West India agricultural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Frequent State-Level Bans on Single AI Products

State governments' tendency to impose temporary moratoriums on specific active ingredients creates significant supply chain disruptions and inventory write-offs for manufacturers and distributors. Punjab's periodic bans on chlorpyrifos and other organophosphate insecticides, driven by groundwater contamination concerns, exemplify how regional regulatory actions can eliminate substantial market segments overnight. These bans often lack scientific justification or adequate transition periods, forcing farmers to switch to alternative chemistries that may be less effective or more expensive. The unpredictable nature of these regulatory interventions makes long-term planning difficult for companies, particularly those with significant investments in banned molecules. Compliance with the Central Insecticides Board and Registration Committee's federal guidelines provides limited protection against state-level restrictions, creating a complex regulatory environment where the same product may be legal in one state but banned in neighboring regions. This fragmentation undermines market efficiency and increases compliance costs for companies operating across multiple states.

Rising Counterfeit Product Penetration in Tier-3 Markets

The proliferation of gray-market copies in rural and semi-urban markets is eroding branded product volumes while undermining farmer confidence in legitimate crop protection solutions. Counterfeit products typically contain substandard active ingredients or incorrect concentrations, leading to poor field performance and potential crop damage that damages the reputation of legitimate brands. The problem is most acute in tier-3 markets where price sensitivity is high and regulatory enforcement is limited, creating opportunities for unscrupulous manufacturers to exploit farmers' cost constraints. Distribution networks in these markets often lack the technical expertise to distinguish between genuine and counterfeit products, particularly when packaging closely mimics established brands. The rise of e-commerce platforms has created new channels for counterfeit distribution, making it easier for illegitimate suppliers to reach farmers directly without traditional dealer oversight. Companies are investing in anti-counterfeiting technologies including holographic labels, QR codes, and blockchain-based authentication systems, but enforcement remains challenging in remote rural markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Insecticides Dominate Despite Herbicide Acceleration

Insecticides maintained their commanding position with 70.98% of the India crop protection chemicals (pesticides) market share in 2025, reflecting persistent pest pressure across India's diverse cropping systems and the continued prevalence of labor-intensive cultivation practices that favor foliar spray applications. The segment's dominance stems from the critical nature of insect pest management in food security crops like rice and cotton, where yield losses from untreated infestations can exceed 30-40% in favorable pest conditions. However, herbicides are experiencing the most rapid expansion with a projected CAGR of 8.55% through 2031, driven by acute labor shortages for manual weeding and the unofficial adoption of herbicide-tolerant crop varieties. Fungicides occupy a stable but smaller market position, with growth concentrated in high-value crops like fruits and vegetables, where disease management commands premium pricing. Nematicides represent a niche but growing segment as soil-borne pest problems intensify with continuous cropping systems, while molluscicides remain limited to specific crops like rice, where golden apple snail infestations create localized demand spikes.

The shift toward herbicides reflects fundamental changes in Indian agriculture, where rising labor costs and declining availability of agricultural workers are forcing mechanization and chemical substitution for traditional hand-weeding practices. Jubilant Ingrevia's recovery in pyridine-based intermediate volumes during 2024 signals renewed demand for herbicide active ingredients, with the company securing a USD 300 million five-year contract for agrochemical intermediate manufacturing . This trend is particularly pronounced in commercial crops like cotton and sugarcane, where large field sizes and mechanized cultivation systems favor herbicide-based weed management over manual labor.

By Application Mode: Foliar Dominance Challenged by Soil Treatment Growth

Foliar application methods command 52.65% of the India crop protection chemicals (pesticides) market share in 2025, reflecting the continued prevalence of traditional spraying equipment and farmer familiarity with above-ground pest management practices. This dominance is supported by the immediate visibility of treatment effects and the flexibility to adjust application timing based on pest scouting and weather conditions. However, soil treatment applications are experiencing robust growth at 5.92% CAGR through 2031, driven by the expansion of systemic insecticides and the integration of crop protection pesticides with precision agriculture technologies. The growth in soil treatment methods reflects broader trends toward integrated pest management and precision agriculture adoption across Indian farming systems. The Digital Agriculture Mission's soil profile mapping initiative, targeting 142 million hectares with detailed 1:10,000 scale maps, will enable farmers to apply soil-based treatments based on specific soil health and pest risk profiles. This precision approach is particularly valuable for managing soil-borne pests and diseases that require preventive rather than reactive treatment strategies.

Seed treatment represents a growing segment as companies develop advanced coating technologies that deliver targeted protection during critical germination and early growth phases. Chemigation is gaining traction in irrigated areas where micro-irrigation infrastructure enables precise chemical delivery through water systems, while fumigation remains limited to high-value crops and soil sterilization applications. The expansion of drip irrigation systems under government subsidy programs is creating new opportunities for chemigation applications, where crop protection pesticides can be delivered directly to root zones with minimal environmental exposure and maximum uptake efficiency.

By Crop Type: Grains Drive Volume While Commercial Crops Accelerate

Grains and cereals dominate the market with 44.15% of the India crop protection chemicals (pesticides) market share in 2025, reflecting India's focus on food security crops and the large cultivation areas devoted to rice, wheat, and other staple grains. This segment's size is driven by both the extensive acreage under cereal cultivation and the intensive pest management requirements of crops like rice, where multiple pest complexes require season-long protection programs. Commercial crops are experiencing the fastest growth at 4.72% CAGR through 2031, driven by expanding cotton and sugarcane cultivation and the higher value-per-hectare that justifies increased crop protection investments. The growth trajectory in commercial crops reflects India's agricultural transformation toward higher-value cultivation systems that can support increased input investments and mechanization. Cotton cultivation in particular is driving demand for integrated pest management programs that combine transgenic traits with chemical applications to manage complex pest resistance patterns. Sugarcane's expansion in states like Uttar Pradesh and Maharashtra is creating demand for specialized herbicide and insecticide applications suited to the crop's long growing season and mechanized cultivation practices.

Fruits and vegetables represent a premium segment where quality requirements and export standards drive adoption of advanced crop protection solutions, while pulses and oilseeds face specific pest challenges that require specialized chemical interventions. Turf and ornamentals remain a niche segment concentrated in urban and peri-urban areas where aesthetic and functional requirements command premium pricing. The government's emphasis on doubling farmer incomes is encouraging shifts toward higher-value crops that require more sophisticated crop protection strategies, creating opportunities for companies with specialized product portfolios and technical service capabilities.

Geography Analysis

North India maintains its position as the largest regional market, driven by the intensive rice-wheat cropping systems of Punjab, Haryana, and Uttar Pradesh that require comprehensive pest management programs across multiple growing seasons. The region's dominance stems from high agricultural mechanization levels, established distribution networks, and strong farmer purchasing power that supports adoption of premium crop protection solutions. Punjab's leadership in agricultural productivity has created sophisticated pest management practices, though recent state-level bans on specific molecules like chlorpyrifos have forced farmers to adopt alternative chemistries and integrated pest management approaches. Labor shortages in traditional agricultural areas are driving mechanization and chemical substitution for manual pest management practices, creating opportunities for herbicides and soil-applied systemic insecticides that reduce labor requirements.

West India, anchored by Maharashtra and Gujarat, represents the fastest-growing regional market with expansion driven by commercial crop cultivation, advanced irrigation infrastructure, and progressive farming practices that embrace technological innovation. Maharashtra's leadership in cotton and sugarcane cultivation creates substantial demand for specialized pest management solutions, while Gujarat's diversified agriculture and strong industrial base support adoption of advanced crop protection technologies. The region's extensive micro-irrigation infrastructure, supported by government subsidies, is enabling chemigation applications that deliver precise chemical applications through drip and sprinkler systems.

South India maintains steady growth supported by diverse cropping systems including rice, cotton, and high-value horticulture crops that require specialized pest management solutions tailored to tropical and subtropical growing conditions. Karnataka and Tamil Nadu lead in adoption of digital agriculture technologies, with state-level initiatives like Karnataka's Digital Agriculture Centre of Excellence creating frameworks for precision crop protection applications based on real-time field data Agri Collaboratory . The region's focus on export-oriented horticulture creates demand for residue-compliant crop protection solutions that meet international food safety standards.

Competitive Landscape

The top 5 players, namely Bayer AG, FMC, UPL, Sumitomo Chemical Co., Ltd., and Corteva Agriscience, control roughly 74.6% of market revenue, illustrating high consolidation. Their advantage rests on broad pipelines and multichannel distribution. Companies are prioritizing product innovation by introducing new active ingredients and formulations to address evolving pest resistance challenges and changing agricultural needs. Operational agility is demonstrated through the establishment of local manufacturing facilities and R&D centers, enabling quick response to market demands and regulatory requirements. Domestic firms pursue scale through backward integration and M&A. Best Agrolife’s 2024 acquisitions boosted technical manufacturing capacity and opened synergies with Syngenta for pyroxasulfone herbicide production.

White-space opportunities are emerging in precision agriculture integration, biopesticide development, and digital advisory services that combine crop protection recommendations with real-time field monitoring data. Companies are leveraging technology to differentiate their offerings, with investments in drone-compatible formulations, IoT-enabled application monitoring, and AI-driven pest forecasting systems that optimize chemical usage timing and dosing. Agritech startups injecting AI-based pest forecasting and drone services present collaboration or acquisition targets for incumbents seeking tech differentiation.

Partnership models are evolving as multinationals license proprietary molecules to local formulators to secure manufacturing cost efficiencies and faster regulatory clearance. The regulatory landscape managed by the Central Insecticides Board and Registration Committee creates barriers to entry for new players while providing opportunities for companies with strong regulatory affairs capabilities to accelerate product registrations. Emerging disruptors include agritech startups that integrate crop protection recommendations with comprehensive farm management platforms, potentially reshaping how farmers access and apply chemical solutions through data-driven decision support systems.

India Crop Protection Chemicals (Pesticides) Industry Leaders

Bayer AG

Corteva Agriscience

FMC Corporation

Sumitomo Chemical Co. Ltd

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Central Insecticides Board and Registration Committee (CIB&RC) approved 27, including new herbicides, insecticides, and fungicides, to expand options for farmers and encourage innovation.

- October 2024: Jubilant Ingrevia secured a USD 300 million five-year contract with a multinational agro-innovator to produce key intermediates for strategic agrochemicals using proprietary technology. The agreement represents significant revenue expansion for the company's agrochemical Contract Development and Manufacturing Organization (CDMO) segment and signals growing demand for India-based contract manufacturing of crop protection intermediates.

- September 2024: The Union Cabinet approved the Digital Agriculture Mission with a total outlay of INR 2,817 crore (USD 338 million) to create a comprehensive digital public infrastructure for agriculture. The mission targets the creation of digital identities for 11 crore farmers over three years and will enable precision crop protection applications through soil health mapping and real-time advisory services.

India Crop Protection Chemicals (Pesticides) Market Report Scope

Function

| Fungicides |

| Herbicides |

| Insecticides |

| Molluscicide |

| Nematicide |

Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Function | Fungicides |

| Herbicides | |

| Insecticides | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms