India Carbon Black Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

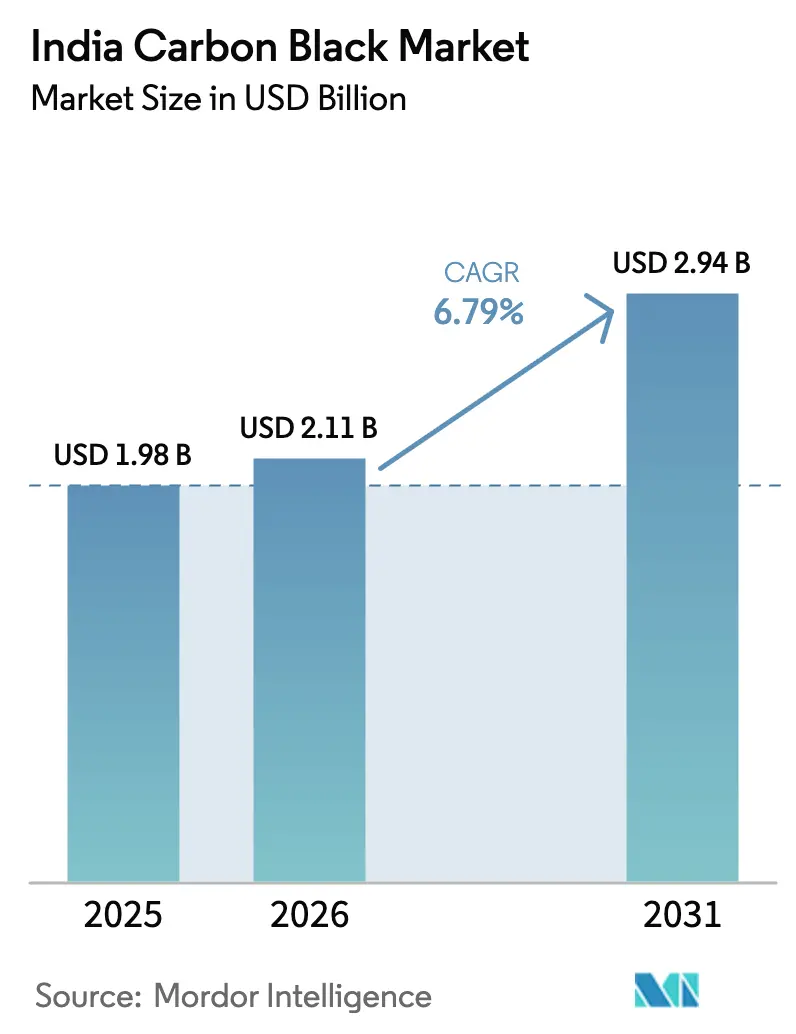

| Base Year Market Size (2025) | USD 1.98 Billion |

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 2.94 Billion |

| Growth Rate (2026 - 2031) | 6.79% CAGR |

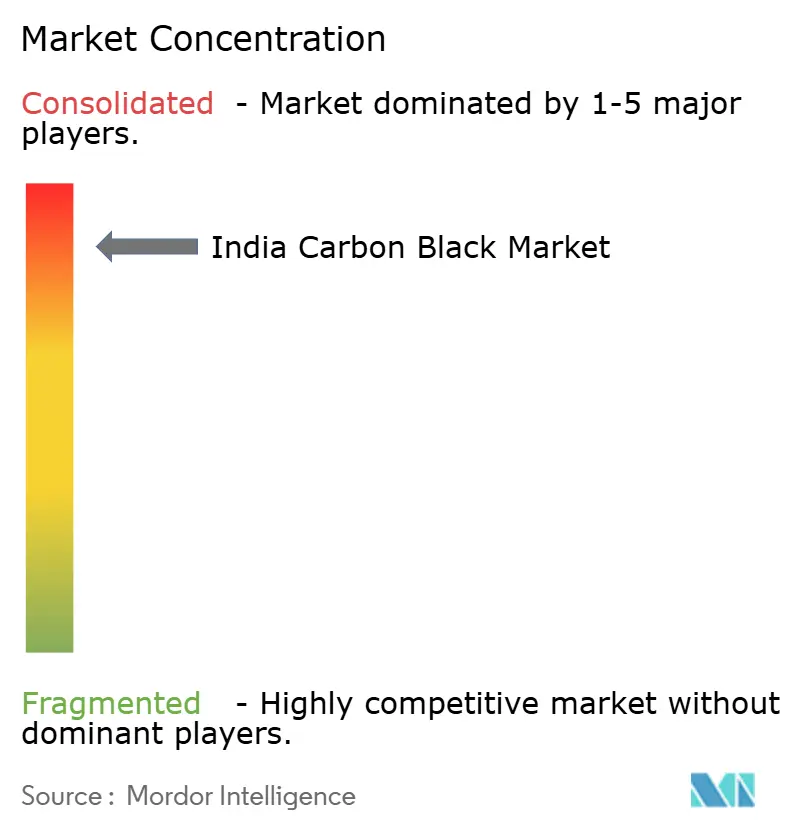

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Carbon Black Market Analysis by Mordor Intelligence

India Carbon Black market size in 2026 is estimated at USD 2.11 billion, growing from 2025 value of USD 1.98 billion with 2031 projections showing USD 2.94 billion, growing at 6.79% CAGR over 2026-2031. Strong tire production, accelerating battery manufacturing programs and expanding polymer demand in infrastructure underpin this outlook, while domestic capacity additions improve supply resilience. Growth is further supported by a shift toward radial tires, an uptick in conductive grades for lithium-ion cells and steady government spending on road, rail and renewable-power corridors. Major producers continue to leverage feedstock integration and waste-heat recovery to contain costs amid volatile petroleum-coke prices. Meanwhile, specialty carbon black development offers margin lift as OEMs seek darker, UV-stable plastics for premium applications.

Key Report Takeaways

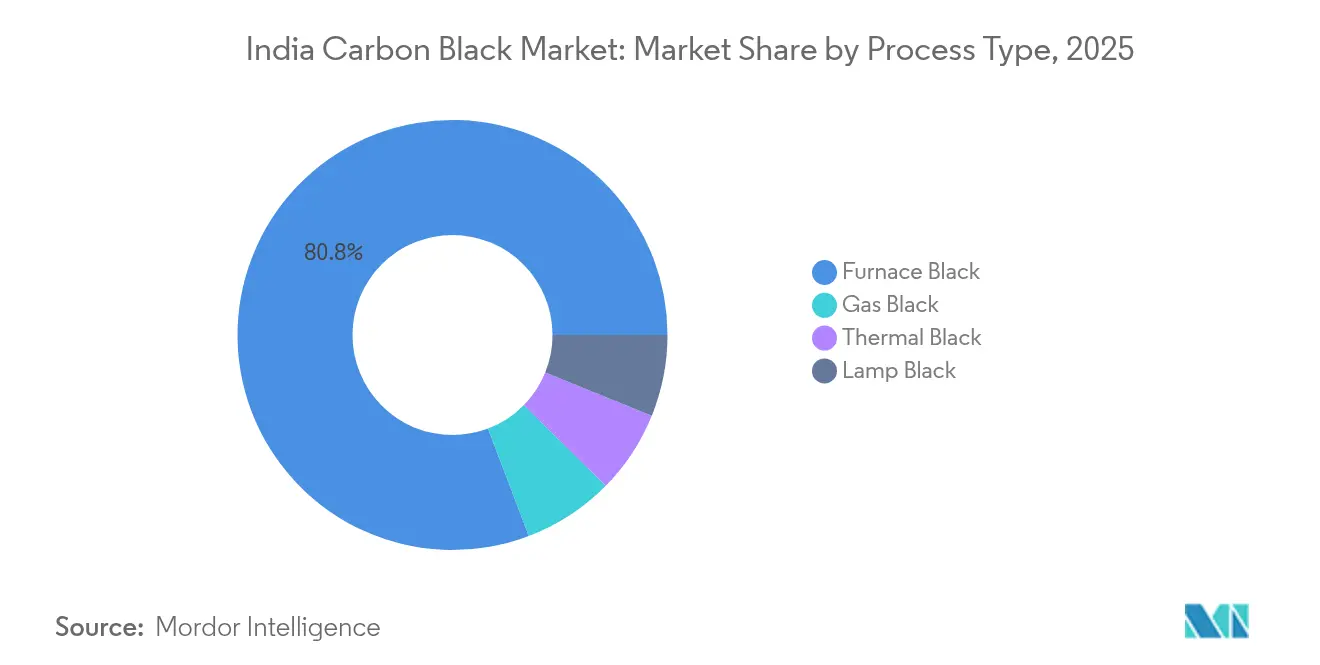

- By process type, furnace black led with 80.78% of the India carbon black market share in 2025, whereas gas black is advancing at an 8.12% CAGR through 2031.

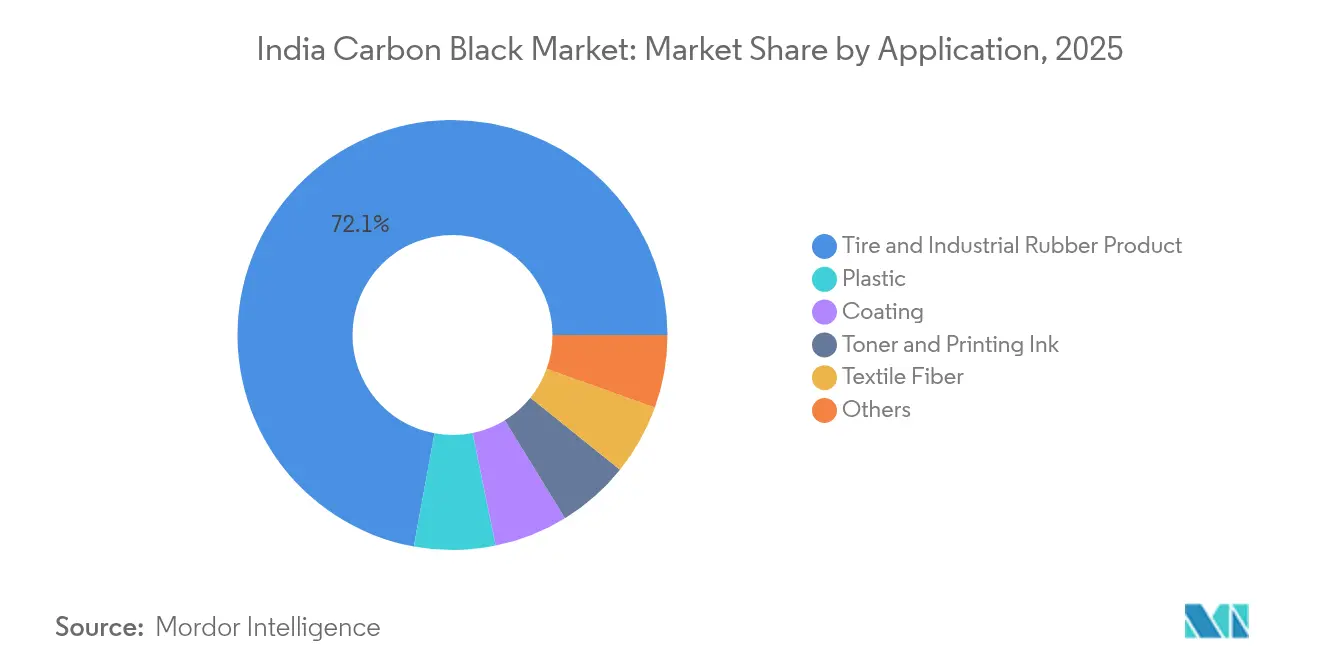

- By application, tire and industrial rubber captured 72.12% of 2025 revenue, while plastic compounds are projected to expand at a 7.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Carbon Black Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging radial-tire production | +2.1% | National – Tamil Nadu, Maharashtra, Gujarat | Medium term (2-4 years) |

| Growing penetration of specialty grades | +1.8% | National – Karnataka, Gujarat, Maharashtra | Long term (≥ 4 years) |

| Ramp-up of lithium-ion cell manufacturing | +1.5% | National – Gujarat, Tamil Nadu, Haryana | Medium term (2-4 years) |

| Infrastructure boom in pipe and cable lines | +1.2% | National infrastructure corridors | Long term (≥ 4 years) |

| OEM push for darker, UV-stable plastics | +0.9% | National automotive clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Radial-Tire Production for Passenger and Commercial Vehicles

Vehicle makers continue to convert truck and bus platforms from bias-ply to radial construction, which requires more reinforcing filler per unit. Replacement cycles remain steady because freight utilization is rising, and highways under Bharatmala have shortened delivery times. Tire plants in Tamil Nadu and Gujarat run high-utilization shifts, sustaining offtake commitments with domestic carbon black suppliers. Higher belt-reinforcement needs raise average carbon black loading by up to 20% over legacy designs. As a result, carbon black demand grows faster than tire unit output, providing volume visibility irrespective of new-vehicle sales variation.

Growing Penetration of Specialty and Conductive Carbon Blacks

Premium conductive and UV-stable grades command two-to-three-times the price of commodity furnace blacks. Birla Carbon’s Continua material and PCBL’s surface-modified lines illustrate the technical shift toward low-ash, narrow-distribution products for battery electrodes and high-gloss polymers[1]Aditya Birla Group, “Birla Carbon – Our Businesses,” adityabirla.com. Indian producers investing in research and development and application labs secure long-term supply contracts because downstream users require formulation support. These grades raise margins and buffer earnings against feedstock swings. The trend encourages capacity earmarked specifically for batteries, cables, and high-performance plastics, diversifying revenue beyond tires.

Rapid Ramp-up of Lithium-ion Battery Cell Manufacturing

India’s Production-Linked Incentive scheme catalyzes multiple gigawatt-hour cell plants in Gujarat and Tamil Nadu. Cathode and anode formulas rely on ultra-pure conductive carbon black with controlled surface area to maintain cycle life. Local sourcing lowers logistics risk and enables just-in-time deliveries that cell makers demand for quality consistency. Producers with battery-grade certification gain an early-mover advantage, and forward contracts lock in pricing premiums that are less exposed to tire industry swings. These volumes sit atop the conventional rubber base, lifting overall domestic consumption.

Domestic Infrastructure Boom Boosting Pipe and Cable Applications

Pipe extruders and power-cable jacketers need 2-4% carbon black loading to meet 20-year outdoor durability targets. Smart-city projects, high-speed rail corridors, and utility upgrades bring steady polymer compound demand across regions. Carbon black’s dual role as colorant and UV stabilizer is hard to replace, ensuring a continuous pull even when automotive cycles cool down. Plants near ports in Gujarat and Maharashtra capitalize on lower freight costs for polyethylene and PVC producers, aligning logistics with national infrastructure rollout schedules.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petroleum-coke and coal-tar prices | -1.4% | Nationwide production clusters | Short term (≤ 2 years) |

| Stringent furnace-emission regulations | -0.8% | Maharashtra and Gujarat enforcement hubs | Medium term (2-4 years) |

| Rising silica-based green-tire adoption | -0.6% | Automotive clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Petroleum-Coke and Coal-Tar Pitch Prices

Feedstock accounts for roughly two-thirds of cash cost, so refinery shutdowns and freight spikes compress margins quickly. Oriental Carbon & Chemicals operated near 70% utilization in FY 2024 because price pass-through lagged cost inflation. Hedging is limited, pushing producers to seek long-term supply agreements with refiners such as ONGC. Integrated waste-heat recovery partly cushions energy swings, yet smaller plants lacking scale remain vulnerable.

Stringent Regulatory Norms for Carbon-Black Furnaces

Tightening particulate-emission rules oblige continuous monitoring and high-efficiency scrubbing. PCBL’s historical Kochi shutdown underscores the risk of non-compliance. New projects budget significant capex for flue-gas desulfurization and bag-filter systems, raising entry barriers. Larger players absorb these costs across higher volumes, whereas regional independents may exit or sell capacity, accelerating consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Furnace Black Retains Scale Advantage

Furnace black held 80.78% of the India carbon black market share in 2025 because it offers the lowest unit cost for large-run production. While niche, gas black posts the fastest 8.12% CAGR because of superior conductivity sought in battery electrodes and antistatic polymers. The India carbon black market size contribution from furnace lines is set to expand in absolute terms as PCBL and Epsilon Carbon commission additional reactors in Gujarat and Karnataka. Environmental investments make new furnace capacity capital-intensive, yet scale economies maintain competitiveness over lamp or thermal processes.

Gas black’s growth is rooted in specialty demand rather than volume leadership. Producers target modest capacities co-located with downstream compounders to offset higher conversion costs. Thermal black remains a micro-segment for ultra-pure applications, while lamp black serves legacy ink markets. As OEMs tighten conductivity and purity specs, suppliers upgrading process control capture premium pricing, lifting average realization per ton across the India carbon black market.

By Application: Tire Rubber Dominance Faces Polymer Upswing

Tire and industrial rubber end-uses represented 72.12% of revenue in 2025, reinforcing the historic link between vehicle build rates and the India carbon black market. The plastic segment, however, is projected to deliver a 7.65% CAGR, supported by pipes, cables, and automotive interior trims that need UV resilience. India's carbon black market size gains from plastic applications will offset any moderation in tire growth as electric vehicles adopt extended tread-wear compounds that reduce per-tire filler load.

Printing inks, toners, and coatings offer stable but smaller volumes driven by packaging and construction. Continuous growth in e-commerce boosts inkjet toners, where small-particle carbon black enables dense optical density. Coating formulators in the building sector specify high-purity grades for façade durability, expanding non-rubber consumption. These diversified outlets improve capacity utilization and decrease dependence on automotive cycles in the India carbon black industry.

Geography Analysis

Western and southern corridors dominate consumption because they host tire plants, chemical parks, and major ports. Maharashtra and Gujarat account for the largest share owing to integrated refinery feedstock and export infrastructure. PCBL’s Mundra and Palej units supply both domestic customers and overseas buyers via deep-draft berths, enhancing the India carbon black market’s logistics efficiency. Tamil Nadu benefits from proximity to commercial-vehicle OEMs and emerging battery manufacturers, pushing regional demand ahead of national averages.

In Karnataka and Andhra Pradesh, capacity additions aim to serve new electrical-cable and pipe plants linked to renewable-energy corridors. The India carbon black market size allocated to southern states is projected to grow through 2031 as solar and wind installations require UV-stable polymer components. Northern regions sustain modest growth tied to off-the-road tire and agricultural machinery hubs around Haryana and Uttar Pradesh.

Export performance complements domestic sales. Currency competitiveness and India’s reputation for quality reinforce these lanes. However, freight volatility and trade-remedy duties in destination markets influence margin realization, motivating producers to balance international exposure with the reliable pull from domestic tire makers.

Competitive Landscape

The India carbon black market is highly consolidated. Capacity expansion is often paired with waste-heat recovery turbines that lower Scope 2 emissions, meeting tightening ESG criteria from tire majors. Technology differentiation centers on surface-modified and low-PAH grades aimed at EV batteries and food-contact polymers. Patent filings from PCBL and collaborative projects between Birla Carbon and downstream compounders illustrate a shift toward application co-development. Smaller regional players cater to inks and coatings but face compliance-cost pressure, opening the door for acquisitions by larger firms seeking footprint diversification in the India carbon black industry. Pricing power remains linked to feedstock swings. Integrated players with long-term petroleum-coke contracts hedge exposure better than standalone units. Strategic sourcing from ONGC’s OPaL complex offers domestic supply security and cost stability OPALINDIA.IN. As customers prioritize reliable delivery, producers with port-adjacent inventory hubs and robust quality systems gain preferred-supplier status, reinforcing incumbency advantages across the India carbon black market.

India Carbon Black Industry Leaders

PCBL Limited

Birla Carbon (Aditya Birla Group)

Himadri Speciality Chemical Ltd

Epsilon Carbon Pvt Ltd

Continental Carbon India Ltd (Continental Carbon Asia)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PCBL Limited announced to establish its sixth carbon black plant in Naidupeta, Andhra Pradesh, with a planned capacity of 400,000–450,000 tonnes/year. The first phase will involve a 150,000-tonne/year facility, backed by an investment of INR 9.5–9.6 billion and a timeline of 2–2.5 years.

- January 2024: Birla Carbon has announced major greenfield expansions in Asia, with two new carbon black manufacturing plants set to open in Naidupet, Andhra Pradesh (India), and Rayong (Thailand). Each facility will begin with a capacity of 120 kMT, scalable to 240 kMT, to meet rising demand in India and Southeast Asia.

India Carbon Black Market Report Scope

Carbon black is a fine carbon powder made by incomplete combustion or thermal decomposition of gaseous or liquid hydrocarbons under controlled conditions. It is extensively used as a color pigment in paints and inks and as a reinforcing filler in rubber products.

The Indian carbon black market is segmented by process type and application. The market is segmented by process type into furnace black, gas black, lamp black, and thermal black. The market is segmented by application into tires & industrial rubber products, plastics, toners and printing inks, coatings, textile fibers, and other applications (insulation, power, construction, etc.). Each segment's market sizing and forecasts are in volume (tons).

| Furnace Black |

| Gas Black |

| Lamp Black |

| Thermal Black |

| Tire and Industrial Rubber Product |

| Plastic |

| Toner and Printing Ink |

| Coating |

| Textile Fiber |

| Others |

| By Process Type | Furnace Black |

| Gas Black | |

| Lamp Black | |

| Thermal Black | |

| By Application | Tire and Industrial Rubber Product |

| Plastic | |

| Toner and Printing Ink | |

| Coating | |

| Textile Fiber | |

| Others |

Key Questions Answered in the Report

What is the current value of the India carbon black market?

It is valued at USD 2.11 billion in 2026 and is projected to reach USD 2.94 billion by 2031.

How fast is demand for carbon black in plastic applications growing?

Plastic compounds are expanding at a 7.65% CAGR through 2031 on the back of infrastructure and automotive needs.

Which process segment dominates the Indian supply?

Furnace black leads with 80.78% share owing to cost-efficient, large-scale production economics.

Why are specialty carbon blacks gaining traction?

Conductive and UV-stable grades fetch premium pricing and support lithium-ion batteries, cables, and high-gloss auto parts.

How are feedstock price swings affecting producers?

Volatile petroleum-coke and coal-tar costs squeeze margins, encouraging long-term supply contracts and vertical integration.

What regions account for the highest consumption?

Maharashtra and Gujarat lead due to tire, chemical, and port infrastructure, while Tamil Nadu and Karnataka are rising on EV and polymer growth.

Page last updated on: