Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

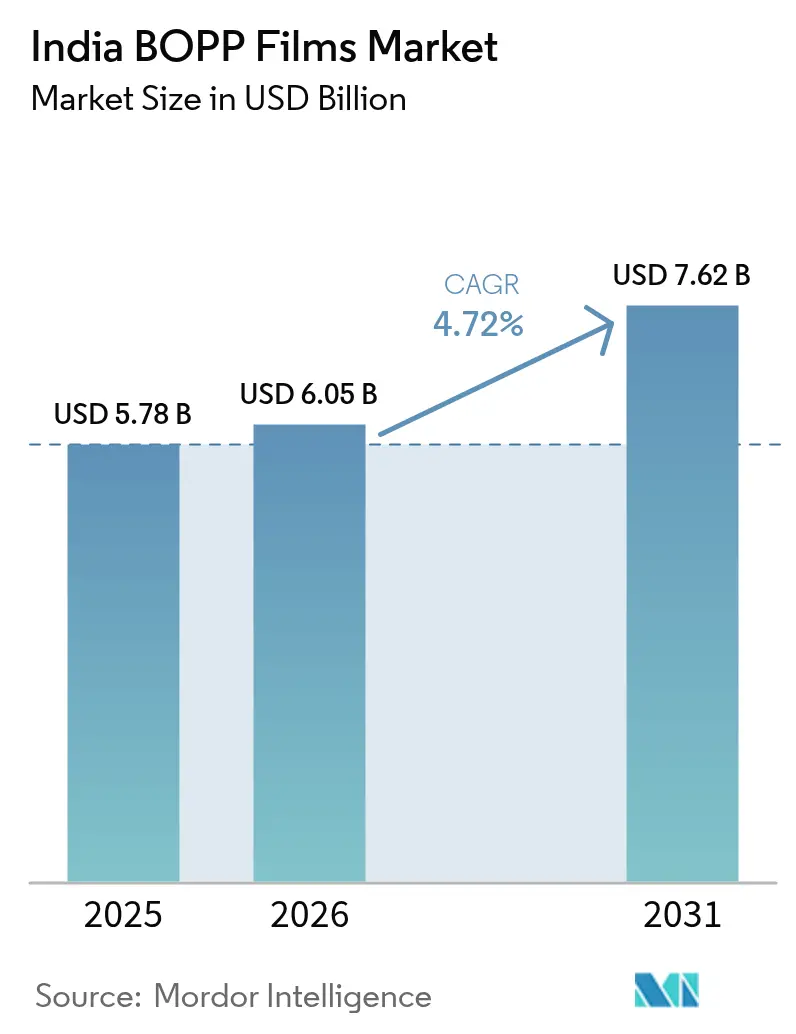

| Base Year Market Size (2025) | USD 5.78 Billion |

| Market Size (2026) | USD 6.05 Billion |

| Market Size (2031) | USD 7.62 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India BOPP Films Market Analysis by Mordor Intelligence

The India BOPP films market size is expected to grow from USD 5.78 billion in 2025 to USD 6.05 billion in 2026 and is forecast to reach USD 7.62 billion by 2031 at 4.72% CAGR over 2026-2031. Sustained demand from processed food, e-commerce and FMCG brands continues to offset margin pressure stemming from over-capacity and tighter regulations. Urban consumers are trading up to better-looking packs, while brand owners demand recyclable mono-material formats, nudging manufacturers toward specialty grades. Capacity additions under the Production Linked Incentive (PLI) scheme are improving feedstock security and lowering manufacturing costs. At the same time, rising extended-producer-responsibility (EPR) compliance costs are forcing film producers to invest in take-back and recycling partnerships, influencing pricing strategies across the India BOPP films market.

Key Report Takeaways

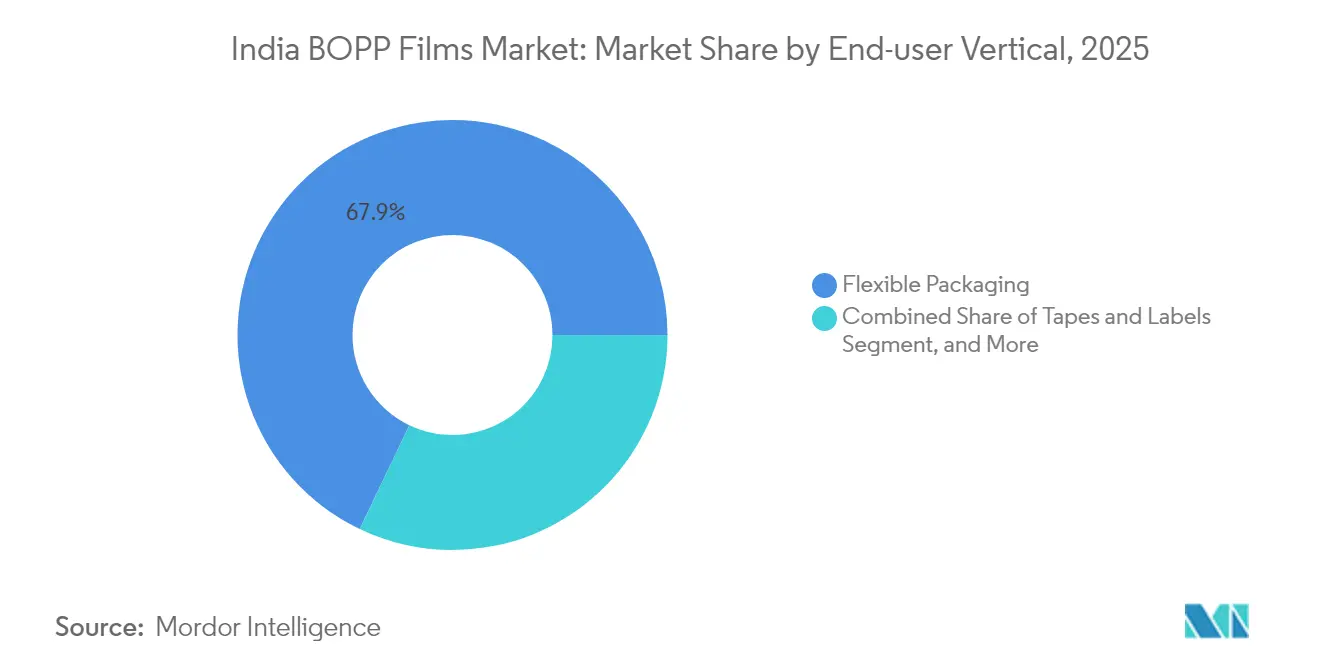

- By end-user vertical, flexible packaging captured 67.90% of the India BOPP films market share in 2025.

- By film type, the India BOPP films market size for metallized films is projected to grow at a 6.12% CAGR between 2026-2031.

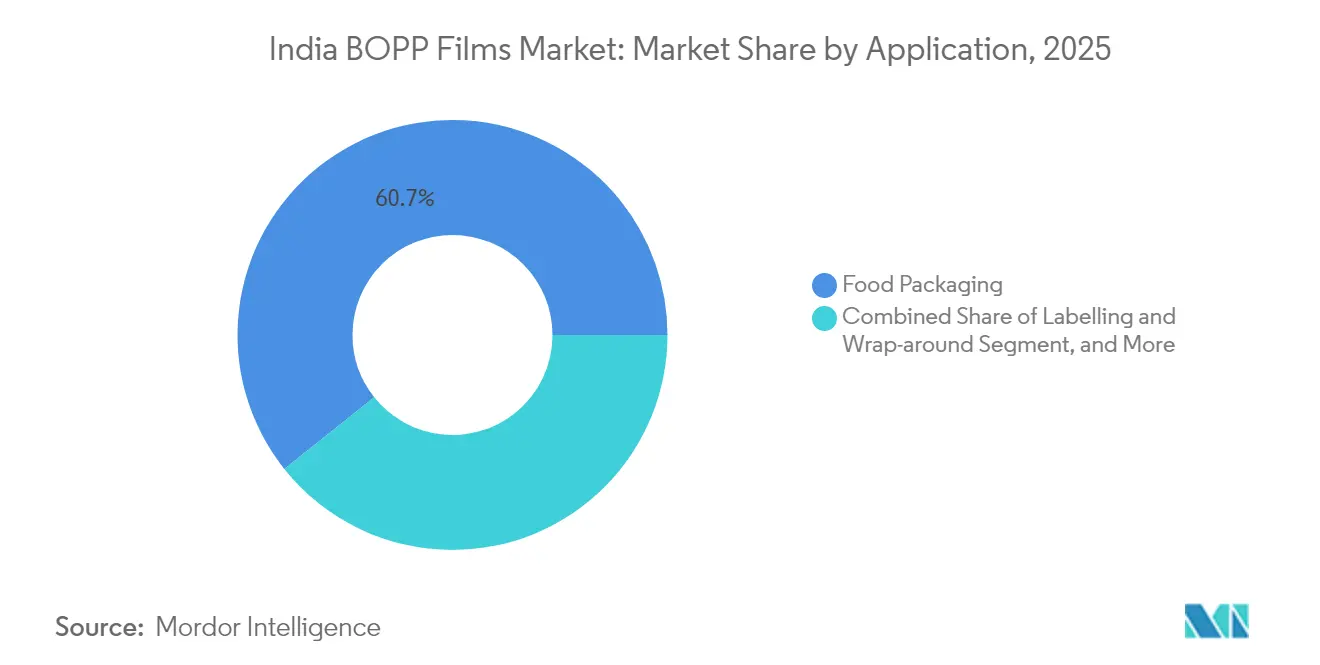

- By application, food packaging captured 60.70% of the India BOPP films market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India BOPP Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid penetration of packaged and ready-to-eat foods | +1.2% | National, with urban concentration | Medium term (2-4 years) |

| E-commerce boom raising demand for protective mailer films | +0.8% | National, led by metro cities | Short term (≤ 2 years) |

| Shift by FMCG brands toward mono-material flexible packs | +0.6% | National, FMCG hub regions | Medium term (2-4 years) |

| Government PLI and PCPIR incentives for petrochemicals | +0.5% | National, manufacturing clusters | Long term (≥ 4 years) |

| Brand owner mandates for high-barrier recyclable labels | +0.4% | National, premium brand segments | Medium term (2-4 years) |

| Rising Flexible Packaging Demand Driving Growth in BOPP Film Consumption | +0.7% | National, industrial corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid penetration of packaged and ready-to-eat foods

India’s surging processed-food ecosystem is a primary engine for the India BOPP films market. The FMCG sector is expanding retail distribution into tier-2 and tier-3 cities, lifting demand for cost-effective barrier films that lengthen shelf life and boost shelf appeal. Southern states Tamil Nadu, Karnataka, and Andhra Pradesh anchor export-oriented plants requiring high-barrier laminates for overseas shipments. Gen Z shoppers value convenience and aesthetics, so brand owners specify printable, puncture-resistant films with matte finishes. The upshot is rising average selling prices within the India BOPP films market as converters shift toward premium SKUs. Equipment upgrades for faster line speeds and inline coating stations are becoming commonplace to service this growth pocket.

E-commerce boom raising demand for protective mailer films

Online retail growth is fueling a new stream of protective packaging needs, particularly mailers that guard against moisture, abrasion and pilferage during multi-node delivery. Lightweight but tough BOPP envelopes minimize shipping weight yet resist tears better than paper-based alternatives, making them a favorite for apparel and consumer electronics shipments.[1]UFlex Limited, “Company Presentation,” uflexltd.com Converters have rolled out post-consumer-recycled (PCR) grades to align with seller sustainability pledges, unlocking premium margins. Planned mega-ports such as Vadhvan will cut logistics costs and shorten export lead times, positioning domestic producers to supply global e-commerce packaging networks.

Shift by FMCG brands toward mono-material flexible packs

Extended Producer Responsibility rules are accelerating the migration from multilayer laminates to mono-material formats. BOPP’s innate recyclability and clarity make it the substrate of choice for brands replacing PET/PE constructions in snack, noodle and personal-care packs. Global food majors are piloting all-BOPP stand-up pouches that integrate transparent windows, metallized barriers and sealable layers to meet both shelf-life and collection-efficiency targets. Barrier-enhancing coatings and surface-treatment know-how are becoming key competitive differentiators inside the India BOPP films market.

Government PLI and PCPIR incentives for petrochemicals

The USD 1.97 trillion-rupee PLI scheme is reshaping domestic supply chains by underwriting new polypropylene and BOPP capacities within petrochemical corridors. Producers benefit from subsidized capex, faster permitting and tax rebates, translating to lower delivered costs for converters and brand owners. Feedstock security has improved as upstream crackers in Gujarat and Odisha ramp production, lowering import reliance and price volatility for propylene. Over the long term this policy thrust is expected to expand the India BOPP films market by attracting fresh investments into specialty-film lines and recycling plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening EPR and plastic-waste rules inflating compliance costs | -0.9% | National, manufacturing hubs | Short term (≤ 2 years) |

| Persistent over-capacity pressuring film margins | -0.7% | National, concentrated in Gujarat/Maharashtra | Medium term (2-4 years) |

| PP feedstock volatility linked to crude swings | -0.5% | National, import-dependent regions | Short term (≤ 2 years) |

| Port congestion hindering export fulfilment | -0.3% | Coastal regions, export-oriented units | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening EPR and plastic-waste rules inflating compliance costs

India’s EPR framework obliges packaging producers to recycle up to 70% of their plastic footprint by FY 2028, raising operating overhead for film converters.[2]Centre for Science and Environment, “Unpacking EPR for Plastic Packaging in India,” cseIndia.org Because fewer than 5% of current recycling units can deliver closed-loop outputs at requisite purity levels, companies are financing new washing lines, digital traceability systems, and audit processes. These expenditures trim industry EBITDA by an estimated 2-4 percentage points and could slow near-term expansion across the India BOPP films market.

Persistent over-capacity pressuring film margins

Domestic installed BOPP capacity exceeds 1.1 million tons, yet utilization hovered in the mid-70s through 2024 as new lines from large incumbents and mid-tier entrants came onstream. Price discounting has intensified, especially in commodity plain-film grades. Although leaders such as SRF and UFlex invest in metallized and coated variants that secure higher spreads, smaller players remain stuck in a price-driven cycle. This dynamic compresses cash flow available for R&D and restricts new entrants, tempering short-term profitability within the India BOPP films market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user Vertical: Flexible Packaging Dominance Amid Specialty Growth

Flexible packaging retained 67.90% of India BOPP films market share in 2025 as snack food, confectionery and personal-care brands favored lightweight rollstock for cost and logistical savings. Within this huge base, the India BOPP films market size for flexible packs is projected to expand modestly as volume growth is balanced by unit-weight light-weighting. Despite commoditization, brand owners increasingly specify matte coatings, anti-fog and cold-seal layers, generating revenue uplift for suppliers capable of rapid grade customization. Tapes and labels constitute the fastest-growing vertical, advancing at a 5.68% CAGR through 2031 amid booming e-commerce shipments, POS-label demand and brand-security applications. Suppliers that mastered top-coat formulation and surface-energy consistency enjoy higher realizations here. Industrial uses such as lamination base film or capacitor dielectrics provide steady volumes but limited margin headroom. Balanced portfolios blending high-volume flexible packs with higher-margin labels help producers navigate the cyclical swings inherent to the India BOPP films industry.

Beyond 2025, converters anticipate a portfolio pivot: commodity plain films will cede share to printable white and coated barrier grades that combine down-gauging with performance retention. In parallel, fast-moving D2C brands are driving niche applications such as tamper-evident courier bags, lifting specialty demand inside the India BOPP films market. To capture this upside, leading producers are investing in wide-width tenter lines coupled with in-line metallizers and high-vacuum coaters, a strategy expected to lift asset utilization and sustain earnings.

By Film Type: Transparent Films Lead While Metallized Gains Premium Traction

Transparent/plain grades continued to generate volume leadership with a 43.70% slice of the India BOPP films market size in 2025 because snack and bakery items still prefer clear windows for product visibility. Yet their growth is slower than the market as brand owners experiment with matte-finish white and metallized variants. Metallized films are outpacing at a 6.12% CAGR, thanks to rising demand for high-barrier mono-material structures that resist oxygen, moisture, and light. Producers such as SRF report that their high-barrier metallized lines operate at near-full capacity, fetching spreads 35-50 basis points above commodity grades. Specialty coated films anti-fog, pearlized, and anti-static, represent a smaller slice but deliver margins up to 2 percentage points higher because of proprietary chemistries and testing protocols.

Going forward, heat-sealable pearlized films for ice-cream wraps and matte-coated grades for premium snack pouches are poised to attract brand-owner attention. Technological advances in reactive-gas barrier deposition and electron-beam curing will likely sustain premium pricing, reinforcing the revenue mix uplift across the India BOPP films market.

By Application: Food Packaging Stability Contrasts with Labelling Dynamism

Food packaging consistently accounted for 60.70% of India BOPP films market share in 2025, anchored by the unstoppable march of processed staples and convenience meals. Safety-critical packs require migration-compliant inks and seal integrity, advantages that entrenched suppliers wield through established quality systems. Nevertheless, labelling and wrap-around sleeves are charting a faster 6.55% CAGR through 2031, propelled by beverage and detergent categories that lean on in-mold and resistant labels for brand blocking. Film demand for this segment is small in tonnage yet rich in margin, underscoring why incumbents pursue high-gloss, scuff-resistant facestocks.

Non-food consumer goods, spanning shampoos to household cleaners, exhibit steady momentum tied to urbanization and rising incomes, favoring recyclable all-BOPP refill pouches. Industrial wraps and component protection films ride on capex cycles in textiles and electronics; they remain vulnerable to macro-volatility yet serve as hedges during consumer down-cycles. This multidimensional application mix underpins resilience inside the India BOPP films market.

Geography Analysis

Western India mainly Gujarat and Maharashtra houses roughly 60% of domestic BOPP capacity, leveraging integrated petrochemical hubs and proximity to major ports for both propylene feedstock and film exports. These clusters benefit from state incentives on power and logistics, reinforcing cost leadership for firms like Jindal Poly and UFlex. Southern states, led by Tamil Nadu and Karnataka, rank as the fastest-growing demand nodes as processed-food units and contract-manufacturing hubs mushroom. Their export orientation fuels uptake of metallized and high-barrier grades that satisfy stringent overseas shelf-life mandates.

Northern India, especially the Delhi-NCR belt and Punjab, forms a sizable consumption hinterland driven by packaged foods, beverages and booming e-commerce fulfilment. Film converters there focus on quick-turn job orders and shorter reel lengths suited to SME brand owners. Eastern corridors such as Odisha and West Bengal are emerging capacity sites spurred by greenfield petrochemical complexes that promise stable feedstock pipelines under PLI coverage.

Logistics upgrades including the 23-million-TEU Vadhvan port will tilt export competitiveness toward western and northern plants once operational. Meanwhile, differing state-level plastic-waste rules create compliance variability; Gujarat and Maharashtra impose advanced recycling certificates while Uttar Pradesh offers landfill-tax rebates, affecting effective cost to serve. Such regional nuances explain why the India BOPP films market continues to display a dual concentration: production in coastal petro hubs, consumption across dispersed metropolitan centers.

Competitive Landscape

The India BOPP films market exhibits moderate concentration: four integrated players SRF, UFlex, Jindal Poly Films, and Polyplex, collectively command an estimated mid-50s share of installed capacity. Their economies of scale, captive metallizers, and backward integration into PET chips or polypropylene resin underpin cost advantages. Recent strategic moves show a tilt toward specialty value pools: SRF is commissioning a 60,000 MTPA BOPP/BOPE complex in Indore, earmarked largely for high-barrier films aimed at premium snack and pharma customers. UFlex has started an in-house PET chips facility in Panipat to secure resin supply and enhance margin capture along the chain.

Mid-tier contenders such as Garware Hi-Tech are diversifying into solar-control and paint-protection films, tapping higher ASP niches insulated from commodity swings. Emerging players with single-line setups struggle against volatile PP feedstock and pricing wars, but some are finding lifelines in toll-coating partnerships with brand owners seeking smaller batches of functional films. Technology adoption, AI-driven process monitoring, high-speed sequential orientation, and extrusion-coating hybrids is becoming a decisive battleground as buyers demand narrower gauge tolerances and faster roll changeovers. Sustainability credentials, particularly the ability to supply high-PCR-content films without compromising barrier, now influence RFP awards across the India BOPP films industry.

India BOPP Films Industry Leaders

Jindal Poly Films Limited

Cosmo First Limited

UFlex Limited

SRF Limited

Polyplex Corporation Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Hitachi Energy India Limited reported 838.8% year-over-year growth in orders for Q3 FY25, signaling robust industrial demand that indirectly supports packaging film consumption across capital-goods supply chains.

- October 2024: SRF Limited announced a 60,000 MTPA BOPP/BOPE greenfield plant in Indore with a INR 445 crore (USD 53.1 million) investment, targeting completion in 25 months to reinforce specialty-film capabilities.

- August 2024: UFlex Limited achieved record quarterly production and commissioned a PET-chips line in Panipat, strengthening backward integration for future India BOPP films market expansion.

- August 2024: Garware Hi-Tech Films Limited posted all-time-high quarterly revenue of INR 474.5 crore (USD 56.7 million) and confirmed a new paint-protection-film line expected online in FY 26.

India BOPP Films Market Report Scope

Biaxially oriented polypropylene films (BOPP films) are manufactured by stretching the polypropylene films. These films are widely used in packaging, labeling, and lamination applications. BOPP films are considered to be the barrier film substrate for food packaging, offering inherent moisture barrier properties, sealability, high clarity, and graphic reproduction and shelf appearance. The market study has considered the wide range of applications of BOPP films in flexible packaging and industrial usage. The market is segmented by end-user vertical and and is divided into flexible packaging, industrial, and other end-user verticals. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By End-user Vertical

| Flexible Packaging |

| Industrial (Lamination, Adhesive, Capacitor) |

| Tapes and Labels |

| Other End-user Verticals |

By Film Type

| Transparent/Plain |

| Metallized |

| White/Opaque/Matt |

| Specialty (Barrier, Anti-fog, Heat-seal, Pearlised) |

By Application

| Food Packaging |

| Non-Food Consumer Goods |

| Industrial Packaging |

| Labelling and Wrap-around |

| By End-user Vertical | Flexible Packaging |

| Industrial (Lamination, Adhesive, Capacitor) | |

| Tapes and Labels | |

| Other End-user Verticals | |

| By Film Type | Transparent/Plain |

| Metallized | |

| White/Opaque/Matt | |

| Specialty (Barrier, Anti-fog, Heat-seal, Pearlised) | |

| By Application | Food Packaging |

| Non-Food Consumer Goods | |

| Industrial Packaging | |

| Labelling and Wrap-around |

Key Questions Answered in the Report

How large is the India BOPP films market in 2026?

The India BOPP films market size is USD 6.05 billion in 2026.

What is the expected growth rate for BOPP films in India through 2031?

The market is projected to post a 4.72% CAGR, reaching USD 7.62 billion by 2031.

Which end-user segment drives the highest volume?

Flexible packaging dominates with 67.90% market share in 2025, led by food and FMCG applications.

Why are metallized BOPP films gaining traction?

Metallized grades deliver superior oxygen and moisture barriers, supporting premium snack and beverage packs and are expanding at a 6.12% CAGR.

How are policy incentives shaping supply?

The PLI scheme and petrochemical investment corridors are spurring capacity additions, improving feedstock access and lowering costs for domestic producers.

What regulatory factor most affects producers today?

Tightening EPR mandates require up to 70% recycling by FY 2028, inflating compliance costs and prompting investments in collection and recycling infrastructure.

Page last updated on: