India Biofertilizer Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

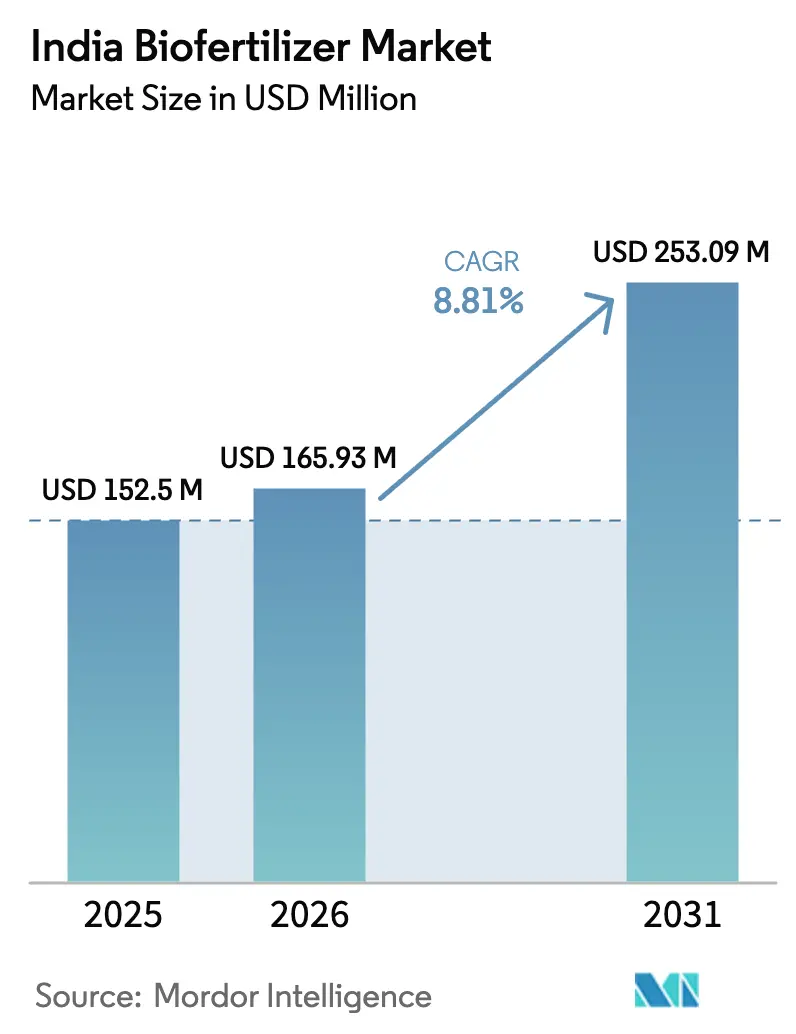

| Base Year Market Size (2025) | USD 152.5 Million |

| Market Size (2026) | USD 165.93 Million |

| Market Size (2031) | USD 253.09 Million |

| Growth Rate (2026 - 2031) | 8.81% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Biofertilizer Market Analysis by Mordor Intelligence

The India Biofertilizer market size was valued at USD 152.5 million in 2025 and estimated to grow from USD 165.93 million in 2026 to reach USD 253.09 million by 2031, at a CAGR of 8.81% during the forecast period (2026-2031). Rapid policy backing, escalating chemical-fertilizer costs, and the strategic push for residue-free exports collectively expand the demand base. Technology investments ranging from AI-enabled soil-microbiome mapping to encapsulated formulations lengthen product shelf life and improve field efficacy, encouraging repeat purchases. The greater penetration of controlled-environment agriculture and liquid fertigation systems creates premium micro-segments, while stricter Schedule VI microbial specifications favor manufacturers with robust quality assurance infrastructure.[1]Source: Department of Fertilizers, “Schedule-VI Microbial Specifications,” fert.nic.in Continued fragmentation, with more than 94% of sales dispersed among small regional firms, keeps pricing competitive yet signals consolidation opportunities as compliance costs rise.

Key Report Takeaways

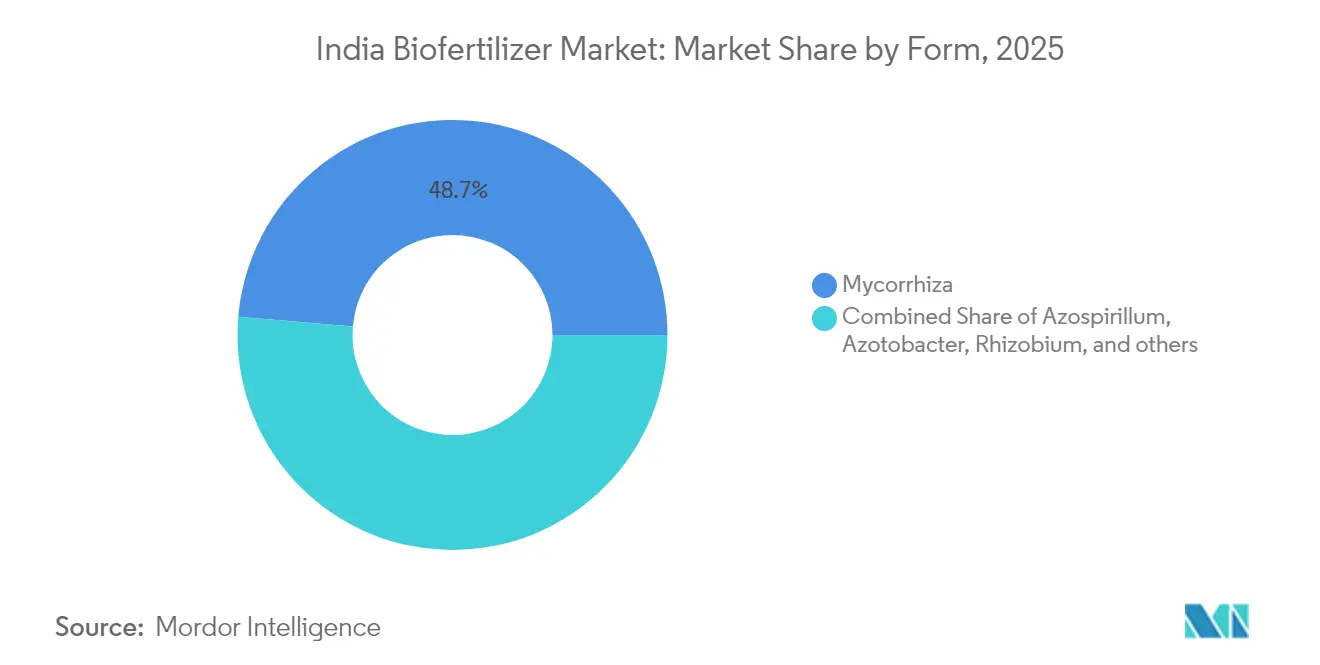

- By Form, Mycorrhiza accounts for 48.65% of the India Biofertilizer Market in 2025, while Rhizobium exhibits the fastest growing CAGR of 9.02% through 2031.

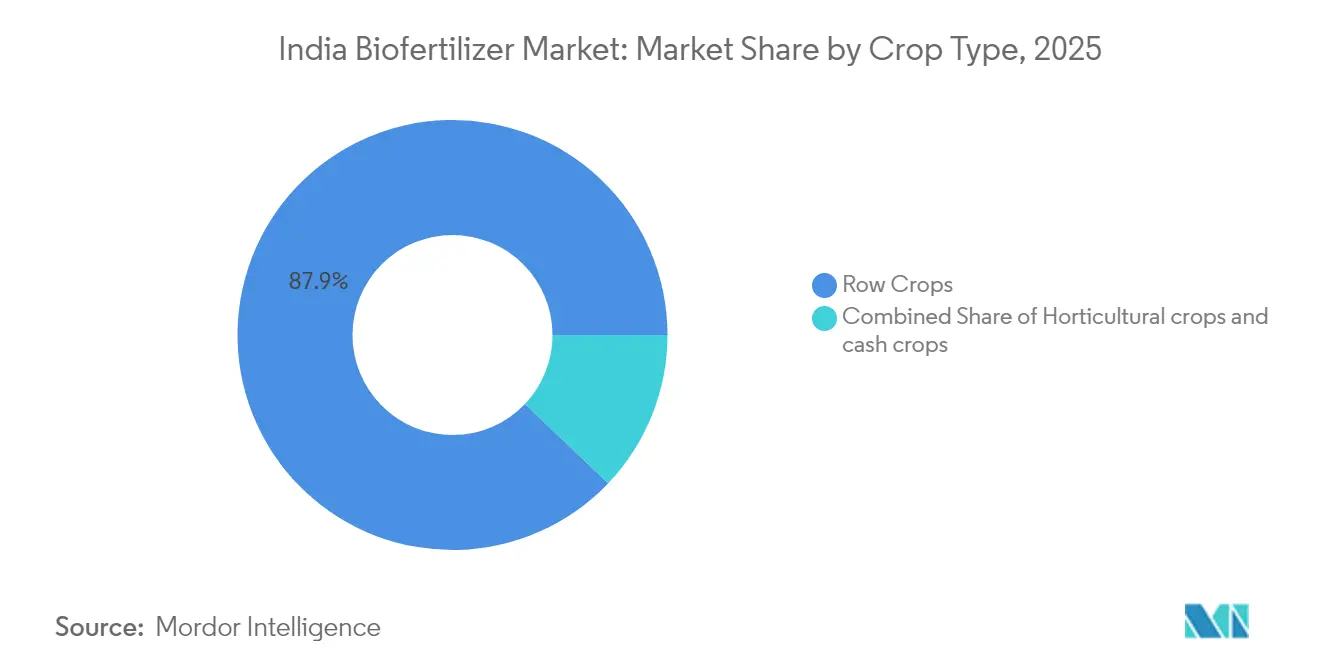

- By Crop Type, Row Crops account for 87.90% of the India Biofertilizer Market in 2025 and are projected to grow at a CAGR of 7.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Biofertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies and organic-farming schemes | +2.10% | Nationwide, stronger in Maharashtra, Punjab, Uttar Pradesh | Medium term (2-4 years) |

| Rising consumer demand for organic produce | +1.80% | Urban markets in Delhi NCR, Mumbai, Bangalore | Short term (≤2 years) |

| Cost advantage versus volatile chemical-fertilizer prices | +1.50% | Input-cost-sensitive districts countrywide | Short term (≤2 years) |

| CEA fertigation demand for liquid biofertilizers | +1.20% | Haryana, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| AI-enabled soil-microbiome customized blends | +0.90% | Gujarat, Maharashtra, Punjab | Long term (≥4 years) |

| Gulf export push for residue-free produce | +0.70% | Gujarat, Maharashtra, Rajasthan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government subsidies and organic-farming schemes

Central programs, such as Paramparagat Krishi Vikas Yojana, disbursed INR 1,197 crore (USD 144 million) in 2024, covering up to 50% of verified biofertilizer costs for farmers.[2]Source: Ministry of Agriculture and Farmers Welfare, “Paramparagat Krishi Vikas Yojana Guidelines,” agricoop.nic.in Linked initiatives fund 10,000 Farmer-Producer Organizations and 1,000 bio-input centers, shrinking last-mile logistics expenses. The PM-PRANAM incentive share subsidy incentivizes states that curb mineral-fertilizer usage, turning fiscal rewards into adoption accelerators.[3]Source: Department of Fertilizers, “Schedule-VI Microbial Specifications,” fert.nic.in Twenty-five regional organic farming hubs provide testing and extension services, ensuring product authenticity and maintaining sustained farmer confidence. Collectively, these schemes form a multi-layered safety net that shields growers from early-stage switching costs and locks in the demand momentum of the India Biofertilizers market.

Rising consumer demand for organic produce

Urban household expenditure on certified organic food climbed 25% annually between 2022 and 2024 to hit USD 1.8 billion, boosting farm-gate premiums by 20-40%[4]Source: Agricultural and Processed Food Products Export Development Authority, “Organic Products Export Statistics 2024,” apeda.gov.in . Residue-testing mandates by the Food Safety and Standards Authority of India link organic labeling directly to documented biofertilizer usage, turning certification from an option into a prerequisite. Metropolitan clusters spearhead distribution efficiencies, enabling manufacturers to pilot value-added liquids and customized blends near consumption centers. Exports mirror domestic patterns in 2024, organic shipments rose 18% to USD 1.2 billion, and the adoption of zero-tolerance residue policies in Europe reinforced reliance on biological inputs. [5]Source: Directorate General of Foreign Trade, “Agricultural Exports Data 2024,” dgft.gov.in The synergy between premium retail channels and export protocols expands order volumes for the India Biofertilizers market.

Cost advantage versus volatile chemical-fertilizer prices

Throughout 2024, urea prices oscillated between INR 266 and INR 310 per kilogram (approximately USD 3.2-3.7), whereas standard biofertilizer regimens cost INR 150-200 per hectare (approximately USD 1.8-2.4)[6]Source: Department of Fertilizers, “Schedule-VI Microbial Specifications,” fert.nic.in . Freight surcharges push mineral-fertilizer landed costs up another 8-12% in remote zones, yet locally produced bio-inputs bypass such mark-ups. During peak volatility, farmers can secure a two-season payback by shifting 20-30% of their nutrient requirements to biological sources, thereby lifting gross margins for pulse, sugarcane, and cotton fields. Government price-stabilization ceilings on synthetic fertilizers simultaneously compress supplier margins, nudging distributors toward higher-return bio-lines. The economic calculus strengthens substitution trends and expands the India Biofertilizers market customer base.

CEA fertigation demand for liquid biofertilizers

Protected-cultivation acreage reached 47,000 hectares in 2024, growing at a rate of 15% per year as growers pursue high-density yields under shade nets and greenhouses.[7]Source: National Horticulture Board, “Protected Cultivation Statistics 2024,” nhb.gov.in Fertigation-compatible liquids carry 40-60% price premiums over carrier-based powders, offset by higher uptake efficiency. Urban-periphery states install cold-storage nodes, allowing distributors to guarantee six-month viability on strained transport lanes. Government horticulture funds worth INR 2,250 crore (USD 270 million) underwrite infrastructure for drip and mist systems that pair natively with biofertilizer injections, particularly for tomatoes, cucumbers, and leafy greens. These dynamics position liquid lines as the fastest-growing revenue pool within the India Biofertilizer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low farmer awareness and training gaps | −1.4% | Rural belts nationwide, heavier in Eastern states | Short term (≤2 years) |

| Short shelf life and cold-chain limits | −1.1% | Rajasthan, Andhra Pradesh, Tamil Nadu | Medium term (2-4 years) |

| Tightened biostimulant deregistration post-June 2025 | −0.8% | National, small producers at higher risk | Short term (≤2 years) |

| High compliance cost of Schedule-VI microbial specs | −0.6% | Nationwide, intense for micro-scale units | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low farmer awareness and training gaps

Extension programs reach only 35% of the country’s 146 million holdings, while formal biofertilizer modules reach fewer than 5% of growers each year.[8]Source: Ministry of Agriculture and Farmers Welfare, “Paramparagat Krishi Vikas Yojana Guidelines,” agricoop.nic.in Missteps such as mismatched strains or premature application can slash efficacy by half, discouraging repeat uptake. Eastern states suffer from both lower literacy levels and fragmented landholdings, magnifying outreach challenges. Digital tutorials remain underpenetrated due to patchy network coverage, especially during the monsoon season when usage peaks. Until technical knowledge dissemination scales, hesitancy will clip the otherwise aggressive growth profile of the India Biofertilizer market.

Short shelf life and cold-chain limits

Liquid formulations typically guarantee six to 12 months of viability under refrigeration, compared to indefinite stability for mineral inputs.[9]Source: Central Insecticides Board, “Biofertilizer Registration Guidelines,” cibrc.nic.in Only 4% of India’s produce travels through temperature-controlled corridors, and the overlap with biofertilizer routes is even smaller. Logistical setbacks expose vials to 45°C summer highs, cutting microbial counts by up to 50% before farm-gate arrival. Though bead-encapsulated lines extend shelf life to 18-24 months, their higher production costs limit price competitiveness in lower-income districts. These bottlenecks constrain the depth of reach for the India Biofertilizer market in heat-prone regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Mycorrhiza commands lead while rhizobium accelerates

Mycorrhiza held a dominant 48.65% share of the Indian Biofertilizers market in 2025, underpinned by its compatibility with cereals, pulses, and vegetables across diverse soil textures. Farmers value the synergistic phosphorus uptake, which helps counter the escalating costs of mono-phosphate. Carrier-based powders remain volume mainstays because eight-month shelf lives align with local storage realities. However, liquid and bead-encapsulated lines grow swiftly in greenhouse clusters, where fertigation or drip systems favor higher microbial counts at planting.

Rhizobium, propelled by national pulse-cultivation drives, is set to record a 9.02% CAGR, the fastest among forms. States with bold protein self-sufficiency targets, such as Madhya Pradesh and Maharashtra, subsidize rhizobium packets at 30-50% of the retail value. Granular variants cater to mechanized seeders in high-acreage farms, particularly in Haryana and Punjab, where machinery penetration exceeds 80%. Product innovations, such as polymer-coated granules, extend microbial viability beyond two cropping seasons, reducing waste and increasing dealer confidence in the Indian Biofertilizer market.

Row crops dominate yet horticulture shows latent lift

Row crops accounted for 87.90% of the Indian Biofertilizers market size in 2025, primarily due to cereals occupying 60% of the cultivated land. Direct seeding and broadcast methods facilitate the easy integration of carrier-based inoculants, while government minimum-support-price regimes mitigate price risk and preserve farmers’ cash flow for biological experiments. Cash crops, such as cotton and sugarcane, follow, leveraging export premiums tied to organic certification.

Row crops are forecast to retain top growth, yet horticultural lines could surprise on the upside. Protected-cultivation plots consume higher-priced liquid inoculants per square foot, and urban shoppers reward pesticide-free vegetables with 30% markups. Pulses and oilseeds in rain-fed belts adopt Rhizobium more quickly, encouraged by demonstrations showing 15-20% yield increases. As diversified cropping gains policy attention, varied agronomic windows will widen demand peaks for the India Biofertilizer market.

Geography Analysis

Biofertilizer adoption in India is concentrated in high-input agrarian regions, particularly where intensive cereal and horticulture production intersects with soil fatigue and sustainability initiatives. Key states driving adoption include Maharashtra, Karnataka, Tamil Nadu, Andhra Pradesh, Telangana, Gujarat, Madhya Pradesh, Uttar Pradesh, Punjab, and Haryana. These regions benefit from active support by state agriculture departments, Krishi Vigyan Kendras (KVKs), PM-PRANAM incentives, and subsidies under the National Mission for Sustainable Agriculture (NMSA). Southern and western India lead in biofertilizer consumption due to well-established biopesticide–biofertilizer ecosystems, large agricultural cooperatives, and widespread availability of products like Rhizobium, Azotobacter, Azospirillum, phosphate-solubilizing bacteria (PSB), and mycorrhiza through government and private ag-retail networks.

Biofertilizer usage is highest in crops such as rice, wheat, pulses (tur, urad, moong), soybean, sugarcane, cotton, groundnut, and maize. These crops benefit from nitrogen-fixing and phosphate-solubilizing strains, which enhance nutrient efficiency and reduce reliance on urea and diammonium phosphate (DAP). Regionally, Rhizobium is predominantly used in pulse and soybean-growing areas like Madhya Pradesh, Maharashtra, and Rajasthan. Azotobacter and Azospirillum are widely adopted in cereal-based systems in Punjab, Haryana, Uttar Pradesh, and Tamil Nadu. PSB and mycorrhiza see significant uptake in horticultural crops, such as grapes and vegetables in Maharashtra, fruits and plantation crops in Karnataka, and spices in Gujarat. Sugarcane-growing regions in Maharashtra and Uttar Pradesh have integrated consortia biofertilizers through mill-linked schemes.

Eastern and northeastern states, including Bihar, Jharkhand, West Bengal, Odisha, and Assam, represent emerging markets for biofertilizer adoption. Growth in these regions is driven by government-led organic farming clusters, Farmer-Producer Organizations (FPOs), and integrated nutrient management projects. However, adoption volumes in these areas remain smaller compared to southern and western India. Adoption is increasing most rapidly in organic and residue-free horticulture export clusters, protected cultivation zones, plantation crops (tea and coffee), and rainfed pulse and oilseed belts. Farmers in these areas are increasingly turning to biological inputs to stabilize yields and enhance soil carbon levels. India's biofertilizer market is transitioning from subsidy-driven distribution models to value-driven adoption. This shift is linked to improving input efficiency, promoting soil regeneration, and catering to premium produce markets. Adoption patterns remain geographically differentiated, influenced by crop economics and state-level policy support.

Competitive Landscape

The competitive landscape of India’s biofertilizer market is marked by fragmentation and multi-tier competition, involving large fertilizer incumbents, mid-sized specialty biological companies, and numerous regional manufacturers. Established fertilizer companies leverage their extensive dealer networks, procurement scale, and government connections to maintain broad market penetration. In contrast, regional manufacturers focus on localized production, competitive pricing, and partnerships with state agriculture departments and Farmer-Producer Organizations (FPOs). While policy support for sustainable agriculture encourages new entrants, long-term success increasingly depends on consistent product performance across diverse climates and cropping systems.

Competition is evolving from the sale of single microbial strains to the provision of differentiated biological solutions. This shift has created a clear divide between companies with strong research and development (R&D) capabilities and those offering commodity-grade formulations. Today, player positioning is increasingly defined by portfolio sophistication, including products such as liquid seed coating biofertilizers, microbial consortia, phosphate-solubilizing blends, mycorrhiza-based products, and integrated solutions combining biofertilizers, biostimulants, and soil amendments. Beyond product offerings, strategic advantages now hinge on distribution strategies and trust-building measures, such as demonstration plots, agronomic advisory services, soil-testing partnerships, digital dosage tools, and integration with organic certification and traceability systems for premium horticulture clusters.

Looking ahead, the market is expected to consolidate around players who combine technological innovation, effective distribution, and credible agronomic outcomes, rather than those competing solely on price. Key drivers of future competitiveness include proven shelf stability under high-temperature and high-humidity supply chains, robust lab validation and field trial documentation, integration with FPO and government programs, and the ability to target premium user segments such as protected cultivation growers, export-oriented horticulture, and regenerative farming clusters. As the industry evolves, companies that link biological inputs to tangible improvements in soil health, nutrient-use efficiency, and farm economics are likely to emerge as category leaders. This shift reflects a transition in farmer purchasing behavior from subsidy-driven trials to value-driven, repeat adoption.

India Biofertilizer Industry Leaders

Biostadt India Limited

Gujarat State Fertilizers & Chemicals Ltd

Indian Farmers Fertiliser Cooperative Limited

National Fertilizers Limited

IPL Biologicals Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: KRIBHCO partnered with Novonesis to launch Rhizosuper biofertilizer for pulse and oilseed farmers across 15 states, to improve crop yields and soil health.

- August 2024: Gujarat State Fertilizers and Chemicals Limited expanded biofertilizer output by 40% at its Vadodara site, emphasizing fertigation liquids.

India Biofertilizer Market Report Scope

The India Biofertilizer Market is segmented by Form (Azospirillum, Azotobacter, Mycorrhiza, Phosphate Solubilizing Bacteria, and Rhizobium) and by Crop Type (Cash Crops, Horticultural Crops, and Row Crops). The Report Offers Market Size in Both Market Value in USD and Market Volume in Metric Tons.

| Azospirillum |

| Azotobacter |

| Mycorrhiza |

| Phosphate Solubilizing Bacteria |

| Rhizobium |

| Other Biofertilizers |

| Row Crops |

| Cash Crops |

| Horticultural Crops |

| By Form | Azospirillum |

| Azotobacter | |

| Mycorrhiza | |

| Phosphate Solubilizing Bacteria | |

| Rhizobium | |

| Other Biofertilizers | |

| By Crop Type | Row Crops |

| Cash Crops | |

| Horticultural Crops |

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of biofertilizers applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The crop nutrition function of agricultural biological consists of various products that provide essential plant nutrients and enhance soil quality.

- TYPE - Biofertilizers enhance soil quality by increasing the population of beneficial microorganisms. They help crops absorb nutrients from the environment.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.