Rhizobium-Based Biofertilizer Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 1.65 Billion |

| Growth Rate (2026 - 2031) | 10.62% CAGR |

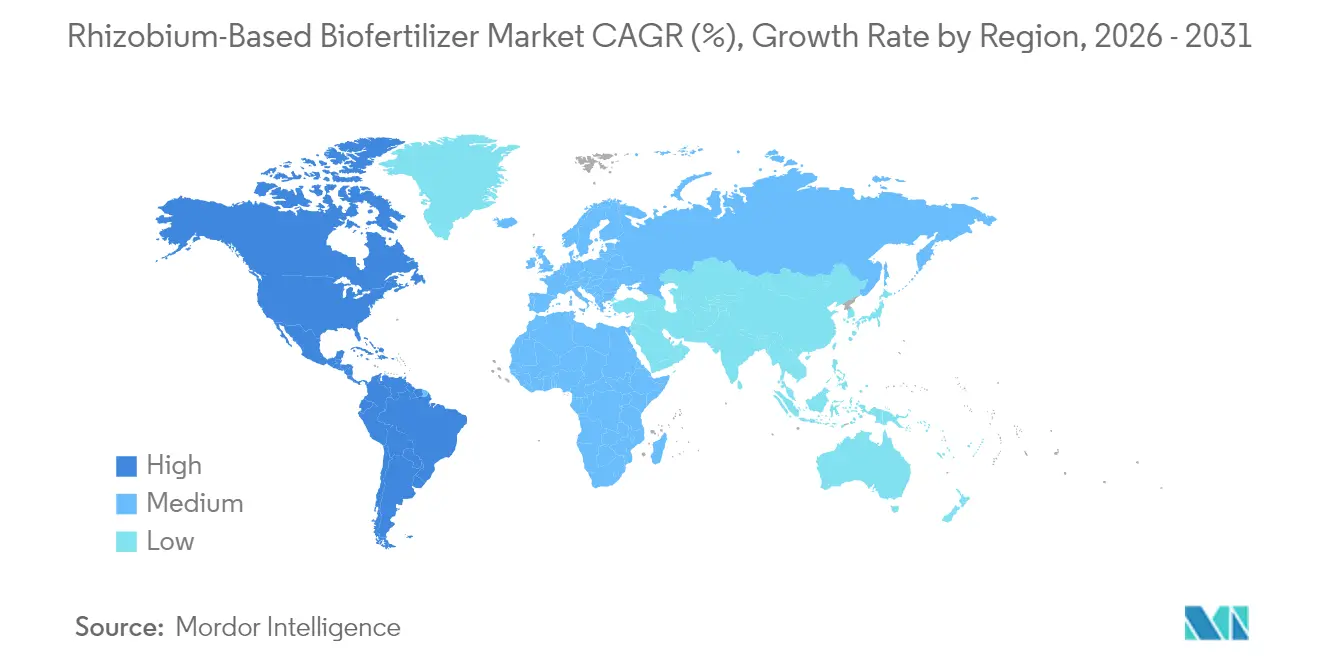

| Fastest Growing Market | South America |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rhizobium-Based Biofertilizer Market Analysis by Mordor Intelligence

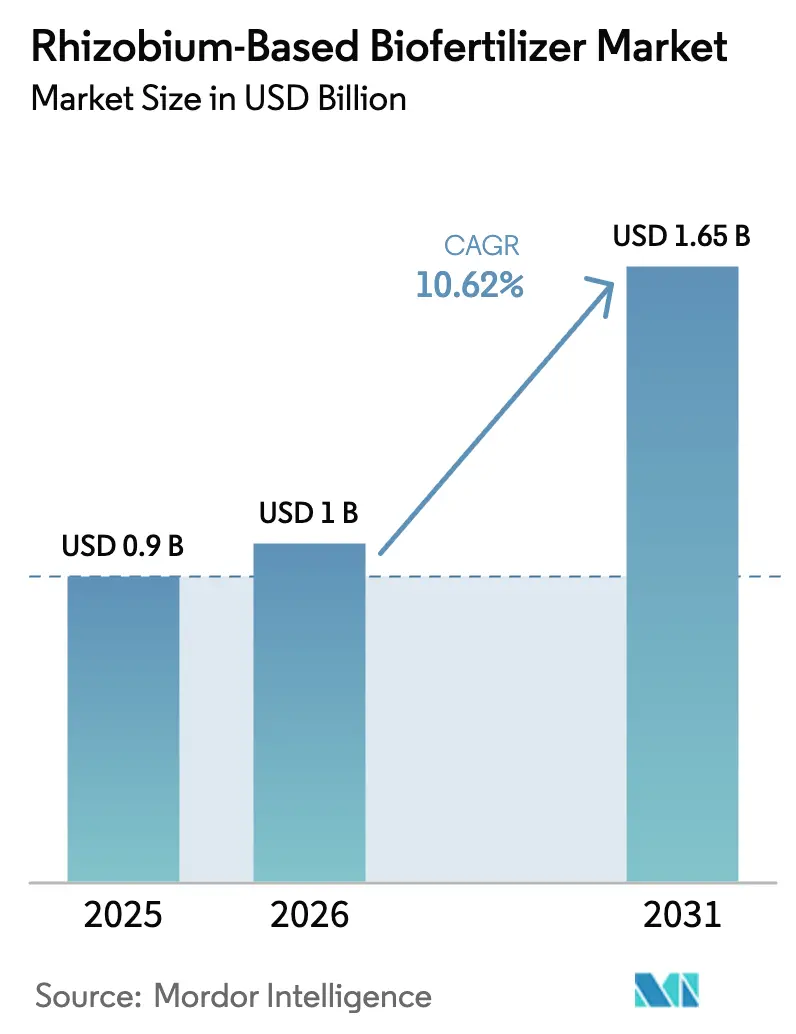

The rhizobium-based biofertilizer market size was valued at USD 0.90 billion in 2025 and estimated to grow from USD 1 billion in 2026 to reach USD 1.65 billion by 2031, at a CAGR of 10.62% during the forecast period (2026-2031). Heightened demand for sustainable nitrogen management, supportive regulations for biological inputs, and rapid technology improvements in microbial strain engineering converge to spur this expansion. Large row-crop farming systems view rhizobium inoculants as a direct route to higher yields and lower synthetic fertilizer costs, especially as commodity prices and environmental compliance expenses rise. Government subsidy programs, increased organic acreage, and precision application tools are now reducing historic barriers to adoption, helping the rhizobium-based biofertilizer market penetrate regions once limited by shelf-life and cold-chain constraints. Competitive intensity remains high because stringent strain-to-soil specificity limits standardization, while local distributors capitalize on geographic knowledge to serve fragmented grower segments.

Key Report Takeaways

- By crop type, the row crops accounted for 69.30% of the rhizobium-based biofertilizer market share in 2025, and are forecast to expand at a 10.74% CAGR through 2031.

- By geography, North America held 52.30% of the rhizobium-based biofertilizer market size in 2025, while South America is projected to record the fastest CAGR at 11.42% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rhizobium-Based Biofertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of certified organic farmland | +2.10% | Europe and North America | Medium term (2-4 years) |

| Government subsidies for microbial inoculants | +1.80% | Asia-Pacific spill-over to South America and Africa | Short term (≤ 2 years) |

| Yield boosts in soybeans and other legumes | +1.60% | North America, South America, Asia-Pacific | Medium term (2-4 years) |

| Seed-coating polymer technology extends inoculant shelf-life | +1.30% | North America and Europe | Long term (≥ 4 years) |

| Precision agricultural applicators enable on-seed dosing | +1.10% | North America and Europe | Long term (≥ 4 years) |

| CRISPR-enhanced strains tolerant to abiotic stress | +0.90% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Certified Organic Farmland

Organic standards prohibit the use of synthetic nitrogen, so certified operations rely on biological nitrogen fixation to preserve soil fertility. European Union organic farmland reached 16.9 million hectares in 2024, an 8.1% rise, while U.S. organic acreage climbed to 5.4 million acres with 5.3% annual growth[1]Source: European Commission, “Organic Farming Statistics,” agriculture.ec.europa.eu. These figures create a structural demand for rhizobium inoculants because legumes form a core part of organic rotations. The premium price realization for organic soybeans further incentivizes farmers to ensure reliable nodulation, driving bulk purchases of high-cell-count formulations. Regional cooperatives in Germany and France now bundle rhizobium into organic transition packages, thereby improving the reach of extension services among smallholders. As consumer preference shifts toward chemical-free food, growth in organic acreage is likely to sustain a multi-year pull effect on the rhizobium-based biofertilizer market.

Government Subsidies for Microbial Inoculants

Directed incentive schemes lower the initial cost for smallholders and accelerate the adoption of new technologies. India’s National Mission for Sustainable Agriculture has earmarked USD 2.4 billion for biofertilizers in 2024, funding up to 75% of rhizobium purchase prices for growers with less than 2 hectares of land[2]Source: Ministry of Agriculture and Farmers Welfare, “National Mission for Sustainable Agriculture,” agricoop.nic.in. Brazil’s PRONAF program now offers low-interest seasonal loans for biological inputs, while Germany allocates approximately USD 163 million annually through its Common Agricultural Policy to subsidize the use of microorganisms. These initiatives have created artificial demand elasticity, resulting in rhizobium-based biofertilizer market penetration exceeding 60% in select Indian pulse belts. Administrative alignment with broader soil-health goals ensures continuity, making subsidies an enduring catalyst over the next two to three seasons.

Yield Boosts in Soybeans and Other Legumes

Extensive field trials underscore the economic value proposition. University of Illinois researchers measured soybean yield gains of 8-12% under optimized inoculation in low-nitrogen fields during 2024. In Brazil, grower cooperatives covering 2.1 million hectares achieved a 180 kg/ha yield improvement, resulting in USD 108 in additional revenue per hectare. Such quantifiable benefits resonate with commercial farmers focused on return on investment. Legume acreage expansion magnifies aggregate demand for inoculants, and documented success stories aid word-of-mouth diffusion. Because commodity soybeans and pulses trade in tight margin bands, even modest productivity gains support rapid growth in the rhizobium-based biofertilizer market.

Seed-Coating Polymer Technology Extends Inoculant Shelf-Life

Polymer matrices now protect rhizobium cells from desiccation and thermal stress during storage and transport. Corteva’s Vault HP, launched in 2024, lengthens shelf-life from six to twenty-four months while maintaining viable counts above 1 × 10^9 per g. Removing strict refrigeration lowers distribution costs in tropical supply chains by USD 0.15-USD 0.25 per hectare. Retailers gain inventory flexibility, and farmers can store product through extended planting windows. Improved viability also increases nodulation reliability, boosting repeat purchase rates. As polymer technologies become license-ready, more manufacturers are projected to retrofit existing strains, reinforcing the rhizobium-based biofertilizer market's technological edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Field-level performance variability by soil pH | -1.40% | Acidic regions worldwide | Medium term (2-4 years) |

| Cold-chain and short shelf-life logistics cost | -1.10% | Africa and rural Asia | Short term (≤ 2 years) |

| Nitrogen-efficient genetically modified crops reduce demand | -0.80% | North America and South America | Long term (≥ 4 years) |

| Regulatory uncertainty for gene-edited microbes | -0.60% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Field-Level Performance Variability by Soil pH

Approximately 30% of global farmland has a pH level below 5.5, where rhizobium survival drops by 40-60% according to IRRI soil health trials. Poor bacterial survivability leads to inconsistent nodulation and discourages repeat purchases. While lime amendments mitigate acidity, smallholders seldom afford corrective inputs, particularly across Sub-Saharan Africa. Manufacturers attempt to engineer acid-tolerant strains, yet commercial offerings still fail to meet agronomic needs. Until adaptation advances outpace pH variability, this restraint will weigh on the rhizobium-based biofertilizer market trajectory in key growth zones.

Cold-Chain and Short Shelf-Life Logistics Cost

Conventional inoculants require 2-8 °C storage, adding USD 0.15-0.25 per hectare in logistics fees in regions with weak infrastructure. Transport distances exceeding 200 km erode dealer margins, leading to stockouts during peak planting periods. Farmers often face outdated inventory with reduced viable counts, undermining confidence in product efficacy. Although polymer coatings extend shelf life, most emerging-market distributors have yet to upgrade. Without near-term investments in cold-chain technology or its diffusion, distribution friction will continue to limit rhizobium-based biofertilizer market reach across remote territories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Row Crops Anchor Market Dominance

Row crops command a 69.30% market share of the rhizobium-based biofertilizer market in 2025, with soybeans alone accounting for two-thirds of the segment's revenue. This positioning aligns naturally with legume biology, where biological nitrogen fixation delivers tangible fertilizer savings of up to 150 kg/ha and yields measured increases of 8-12%. North and South American growers, operating in large contiguous acreage blocks, can deploy seed-applied inoculants at scale. Over the forecast horizon, the segment anticipates a 10.74% CAGR on the back of acreage additions in Brazil’s Cerrado and Argentina’s Pampas. Precision-seeding retrofits and polymer-coated shelf-stable products reduce application risk, driving sustained uptake among large commercial operations. Competitive pricing pressure, however, keeps margins tight, motivating manufacturers to add value through co-formulation with growth-promoting consortia and micronutrient coatings.

Cash crops and horticultural crops collectively absorb the remaining 30.70% share but present higher per-unit pricing. Cotton producers pursue co-inoculation strategies leveraging rhizobium to enhance early-season nitrogen availability, while pulse growers favor strain-specific inoculants for chickpeas and lentils cultivated in lower-nitrogen soils. Specialty horticulture relies on Rhizobium to comply with organic certification standards that prohibit the use of synthetic fertilizers. European greenhouses report improvements in yield stability, and premium pricing offsets the increased costs of inoculants. Although smaller in absolute size, these crop classes offer margin diversity and create entry points for niche providers specializing in strain selection and value-added advisory services. Strategically, rising consumer demand for plant-based proteins and organic produce secures long-term expansion prospects in these sub-segments.

Geography Analysis

North America accounted for 52.30% of the rhizobium-based biofertilizer market size in 2025, anchored by expansive soybean areas and established precision agriculture infrastructure. The United States deploys inoculants on over 65% of its 34.6 million ha soybean acreage, leveraging bin-integrated dosing systems and strong extension services. Canada contributes incremental volume through pulse crop growth in Saskatchewan and Manitoba, where rhizobium products adapt to cooler soil temperatures. Regional cold-chain maturity ensures product viability, supporting high farmer confidence and repeat purchase rates.

South America exhibits the fastest trajectory, with a 11.42% CAGR through 2031, driven by Brazil’s soybean footprint, which reached 45.2 million hectares in 2024. Rhizobium adoption approaches 85% among Brazilian growers, driven by demonstrated yield gains and cost parity with urea. Argentina’s macroeconomic constraints heighten sensitivity to imported fertilizer costs, prompting growers to favor domestic biological alternatives. Government credit facilities subsidize microbial purchases under sustainable agriculture mandates, further boosting demand. Logistics limitations persist in remote Cerrado frontier zones, but polymer-enhanced stability mitigates product loss and broadens reach.

The Asia-Pacific region holds untapped opportunities, with India spearheading regional demand through a government-supported biofertilizer push that has raised national production capacity to 1.2 million metric tons in 2024. Rhizobium accounts for roughly 35% of that output, which is channeled toward pulse belts in Madhya Pradesh and Maharashtra. China focuses on ecological agriculture to curb soil degradation, with a particular emphasis on fostering pilot rhizobium subsidy programs in Henan and Shaanxi. Fragmented farm structures, variable soil pH, and limited cold-chain capacity remain obstacles, but mobile advisory applications and community storage centers improve extension efficacy. Long-term potential rests on rising protein demand and increasing awareness of soil health benefits, setting the stage for progressive rhizobium-based biofertilizer market penetration.

Competitive Landscape

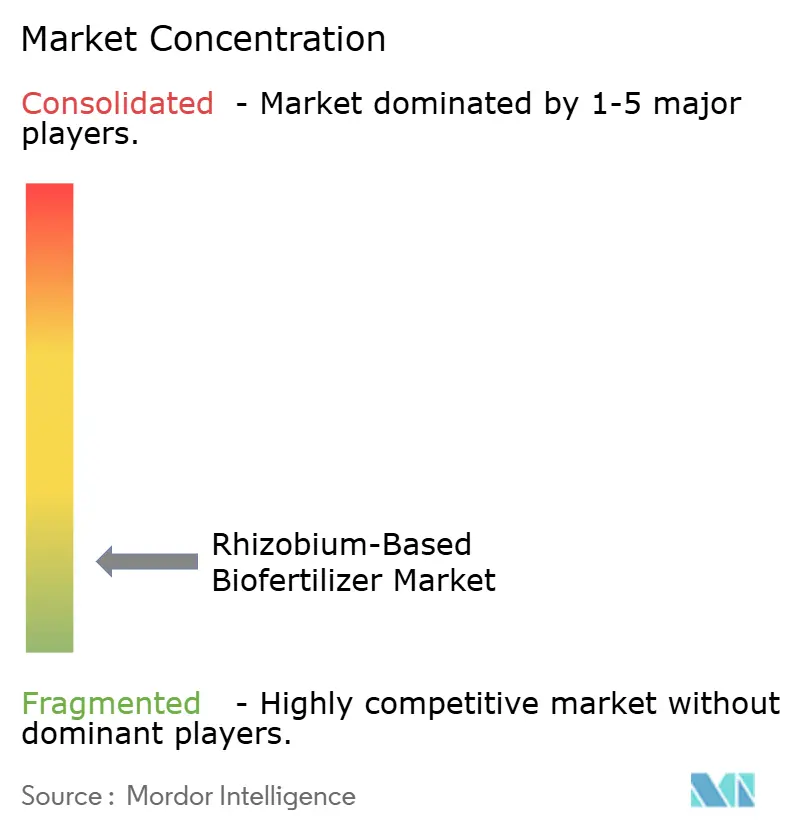

The rhizobium-based biofertilizer market remains highly fragmented, as the top five players control a significant share of global revenue[3]Source: USPTO, “Patent Search,” uspto.gov. Novozymes, holding a significant share, commands the widest strain library and cross-regional distribution capabilities. Regional champions, such as Rizobacter in Argentina and Vittia in Brazil, leverage local agronomy expertise and proximity to growers. Biological specificity hampers scale economies; strains optimized for one soil-crop combination seldom perform optimally elsewhere, encouraging a mosaic of local players.

Competitive strategy centers on technology differentiation rather than capacity expansion. Firms allocate R&D toward multi-strain consortia, stress-tolerant gene-edited variants, and polymer protective coatings. Patent activity rose 34% in 2024, underscoring innovation’s critical role in defending margins. Strategic partnerships, such as Corteva and BioConsortia’s consortium development deal, exemplify collaboration to expedite time-to-market for next-generation products. Distribution alliances with precision-ag hardware providers integrate inoculant delivery into seeding workflows, strengthening market presence at the point of input decision.

Pricing remains competitively tight due to lower production barriers compared with synthetic fertilizers. Manufacturers, therefore, differentiate via bundled advisory services, warranty programs, and compatibility assurances with seed treatments. As efficacy data accumulate and regulatory acceptance widens, leading suppliers may pursue targeted acquisitions to integrate region-specific strains and consolidate distribution, gradually increasing market concentration without materially disrupting local adaptation requirements.

Rhizobium-Based Biofertilizer Industry Leaders

Indian Farmers Fertiliser Cooperative Limited

Madras Fertilizers Limited

National Fertilizers Limited

Novozymes A/S

Rizobacter Argentina S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Syngenta Canada has launched the Atuva brand, marking its entry into the inoculant market. The Atuva inoculants, renowned for their reliability, deliver seed- and soil-applied rhizobia bacteria. These bacteria enhance nodulation in pulse and soybean crops, ensuring efficient biological nitrogen fixation.

- July 2024: Rovensa Next has unveiled Wiibio, a biofertilizer designed to regenerate soil and enhance its biostimulant properties. Wiibio harnesses the power of Bacillus subtilis, a strain from the Bacillus genus, renowned for its role as a plant-growth-promoting rhizobacteria.

- January 2023: Odisha University of Agriculture and Technology has begun producing biofertilizers, notably those based on rhizobium bacteria. This initiative aims to offer the state's farmers cost-effective biofertilizer solutions. In contrast to chemical fertilizers, these biofertilizers boast no adverse effects and come with a shelf life of one year.

Global Rhizobium-Based Biofertilizer Market Report Scope

Cash Crops, Horticultural Crops, Row Crops are covered as segments by Crop Type. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.| Cash Crops |

| Horticultural Crops |

| Row Crops |

| Africa | By Country |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Africa | |

| Asia-Pacific | By Country |

| Australia | |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Europe | By Country |

| France | |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Turkey | |

| United Kingdom | |

| Rest of Europe | |

| Middle East | By Country |

| Iran | |

| Saudi Arabia | |

| Rest of Middle East | |

| North America | By Country |

| Canada | |

| Mexico | |

| United States | |

| Rest of North America | |

| South America | By Country |

| Argentina | |

| Brazil | |

| Rest of South America |

| Crop Type | Cash Crops | |

| Horticultural Crops | ||

| Row Crops | ||

| Geography | Africa | By Country |

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Africa | ||

| Asia-Pacific | By Country | |

| Australia | ||

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Philippines | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | By Country | |

| France | ||

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | By Country | |

| Iran | ||

| Saudi Arabia | ||

| Rest of Middle East | ||

| North America | By Country | |

| Canada | ||

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | By Country | |

| Argentina | ||

| Brazil | ||

| Rest of South America | ||

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of Rhizobium applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The crop nutrition function of agricultural biological consists of various products that provide essential plant nutrients and enhance soil quality.

- TYPE - Rhizobium are beneficial microorganisms that form an endosymbiotic relationship with crops and help in nitrogen fixation.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.