Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

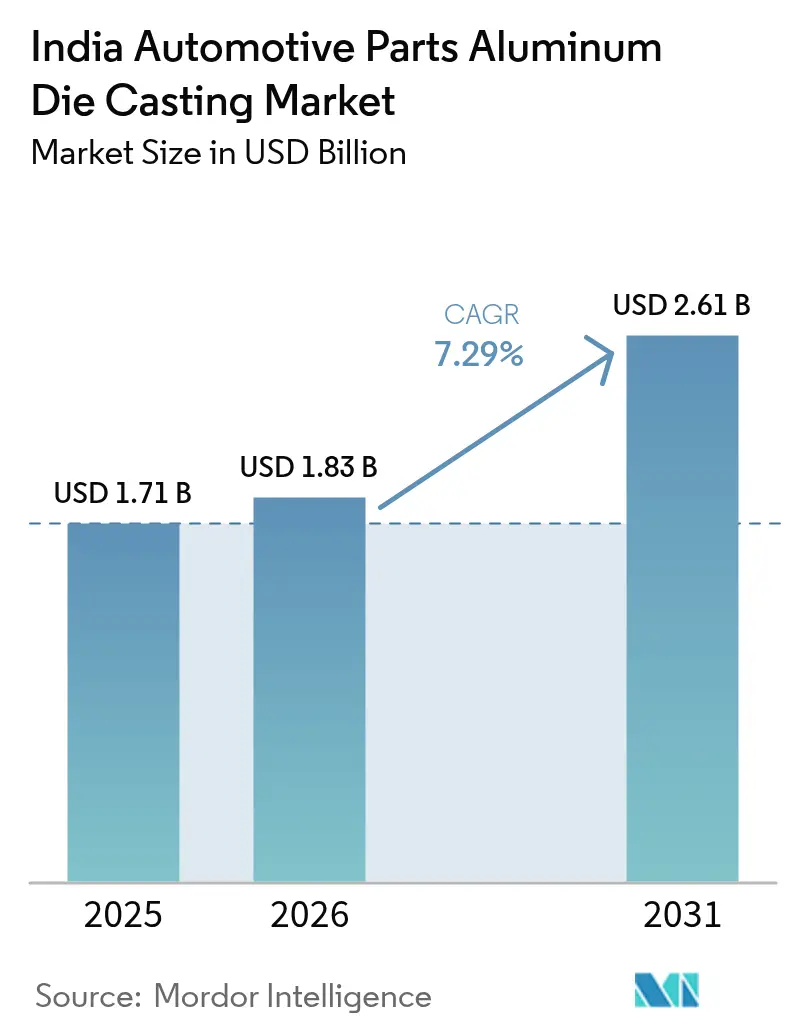

| Base Year Market Size (2025) | USD 1.71 Billion |

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.61 Billion |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive Parts Aluminum Die Casting Market Analysis by Mordor Intelligence

The India automotive parts aluminum die casting market size was valued at USD 1.71 billion in 2025 and estimated to grow from USD 1.83 billion in 2026 to reach USD 2.61 billion by 2031, at a CAGR of 7.29% during the forecast period (2026-2031). Current momentum stems from a confluence of passenger-vehicle production growth, rising electrification, and the rapid shift toward integrated giga-casting platforms that cut part counts and bolster structural integrity. Pressure die casting remains the core production route thanks to its dimensional accuracy and speed, while semi-solid rheocasting gains favor for premium EV battery housings. Raw-material supply security is improving after the End-of-Life Vehicle Rules 2025 enhanced scrap flows, yet capital spending requirements for 6,000-9,000 tonne presses constrain new entrants. OEMs deepen localization to hedge against global supply disruptions, and coastal clusters leverage port proximity to serve ASEAN customers seeking non-China sourcing options.

Key Report Takeaways

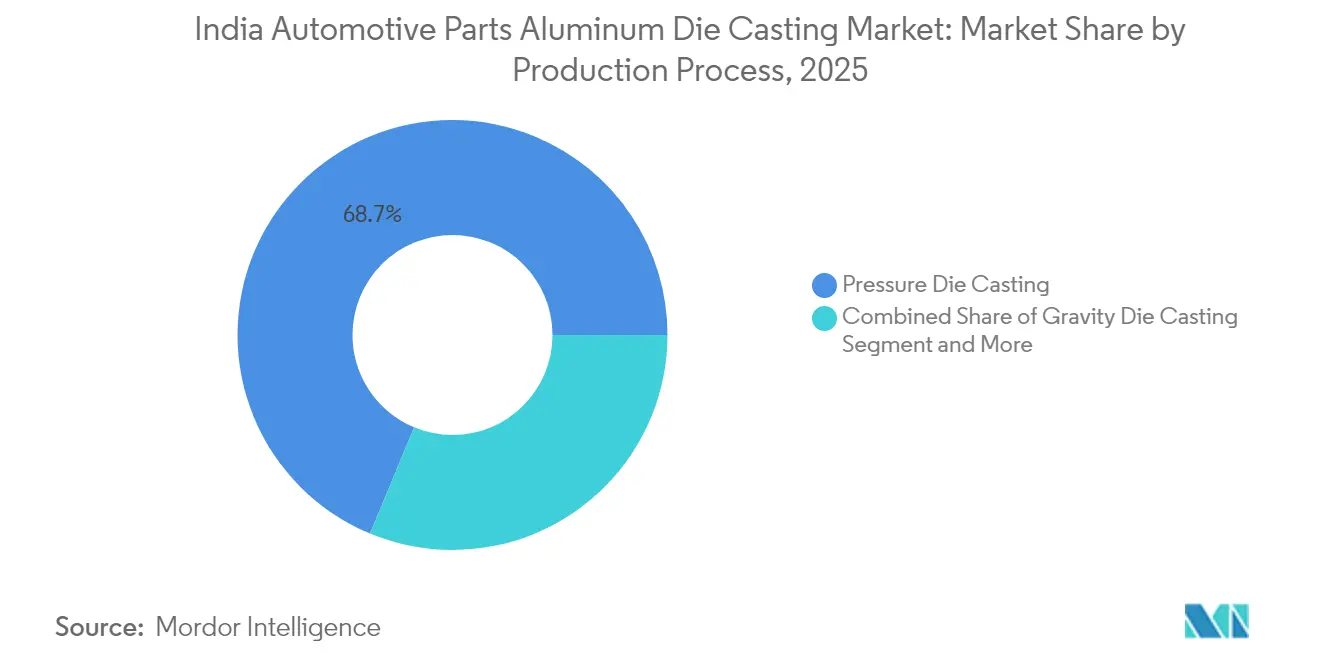

- By production process, pressure die casting held 68.74% of the India automotive parts aluminum die casting market share in 2025; semi-solid/rheocasting is projected to expand at a 9.32% CAGR through 2031.

- By application, engine parts commanded a 45.98% share of the India automotive parts aluminum die casting market size in 2025, while body and structural parts are advancing at an 8.61% CAGR to 2031.

- By vehicle type, passenger cars accounted for 54.80% of the India automotive parts aluminum die casting market share in 2025 and are growing at a 7.70% CAGR through 2031.

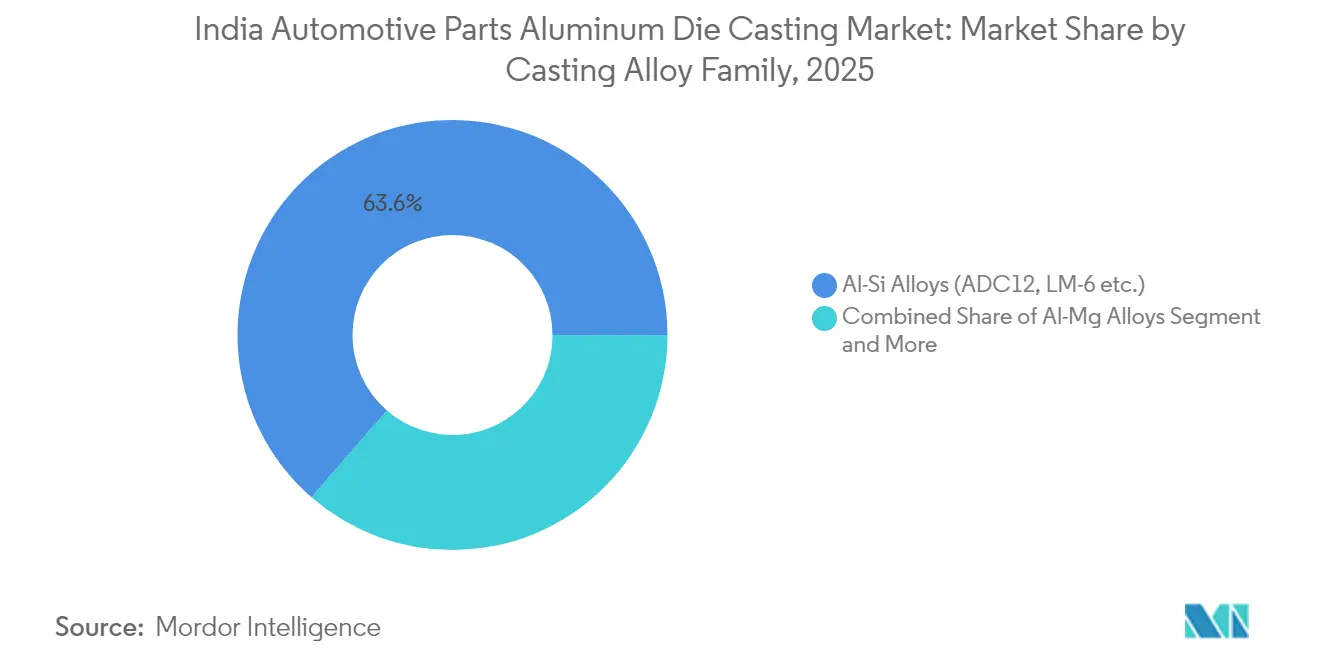

- By casting alloy family, Al-Si alloys accounted for 63.62% of the India automotive parts aluminum die casting market share in 2025, while Al-Mg alloys are advancing at an 8.02% CAGR to 2031.

- By end-user, OEM/Tier-1 suppliers controlled 74.88% of the India automotive parts aluminum die casting market share in 2025 and are expanding at a 9.01% CAGR through 2031.

- By region, West India led with a 39.40% of the India automotive parts aluminum die casting market share in 2025; South India records the highest projected CAGR at 8.39% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Automotive Parts Aluminum Die Casting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Production and Battery Demand | +2.1% | National; Tamil Nadu–Karnataka corridor | Long term (≥ 4 years) |

| Vehicle Lightweighting and Efficiency | +1.8% | Early adoption in West and South India | Medium term (2-4 years) |

| Domestic Passenger Vehicle Growth | +1.5% | West and South India | Short term (≤ 2 years) |

| ASEAN Export Demand Surge | +1.3% | National; coastal clusters | Medium term (2-4 years) |

| China-De-Risking and Giga-Casting | +1.2% | Pilots in Gujarat and Tamil Nadu | Long term (≥ 4 years) |

| ELV Rules Boost Aluminum Scrap | +0.8% | National; industrial recycling hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising EV Production and Demand for Battery Housings

Electric-vehicle output surged at a 76% CAGR between 2020-2024, lifting EV components to 6% of total automotive part value. Battery enclosures demand Al-Mg alloys that provide electromagnetic shielding and crash energy absorption, spurring alloy innovation. A USD 2 billion annual sourcing agreement between Tesla and Tata Group suppliers underscores export potential[1]“Tesla to Source Components Worth USD 2 Billion from Tata Group,” Correspondent, timesofindia.com. Thermal-management castings with intricate cooling channels emerge via low-pressure sand casting. ASK Automotive recorded 133% EV revenue growth after capacity expansion in Rajasthan and Karnataka plants. Production-Linked Incentives under FAME-II channel USD 1.1 billion toward advanced component facilities.

Vehicle Lightweighting and Fuel-Efficiency Norms

Corporate Average Fuel Economy rules and Bharat Stage VI standards accelerated aluminum substitution, pushing average content from 29 kg in 2024 toward 160 kg per vehicle by 2030. The shift cascades across casting supply chains, replacing ferrous parts with aluminum alternatives that trim mass by 40% without compromising stiffness. ICRA projects 9% annual domestic aluminum demand growth through 2025, with automotive uses dominant [2]“Indian Aluminium Demand Outlook,” ICRA Analyst Team, autocarpro.in. High-pressure die casting now produces single-piece transmission housings, lowering manufacturing costs by up to 30%. Bureau of Indian Standards specifications harmonize alloy quality, ensuring mechanical properties remain within safety thresholds. Simulation-led design shortens development cycles and lowers defect rates as OEMs seek faster homologation.

Growth in Domestic Passenger-Vehicle Production

Maruti Suzuki’s Gujarat site targets 1 million units, and Tata Motors boosts Sanand output for domestic and export customers. Modern passenger vehicles integrate 150-200 aluminum parts versus 100 earlier, driven by premiumization. SUV popularity heightens aluminum content across roof rails, door frames, and chassis reinforcements. State-level duty structures favor value-added castings, encouraging deeper localization. Cluster-based supply chains in Maharashtra-Gujarat and Tamil Nadu-Karnataka reduce logistics cost and enhance just-in-time deliveries. Platform strategies allow OEMs to amortize tooling over multiple models, improving supplier order visibility.

Export Demand Surge from ASEAN “China-De-Risking”

Automotive assemblers in Thailand, Indonesia, and Vietnam accelerated supplier diversification programs in 2024, shifting aluminum die-cast component orders toward Indian vendors to mitigate over-reliance on Chinese sources. India’s coastal clusters now offer 14- to 18-day lead times to major ASEAN ports, a three-day improvement over inland Chinese factories once customs and inland haulage are included, giving buyers a tangible logistics advantage. Preferential duties under the ASEAN–India Free Trade Agreement reduce most auto-component tariffs to 0%–5%, enhancing landed-cost competitiveness for high-pressure die castings such as transmission cases and suspension knuckles. Chennai, Ennore, and Mundra ports reported a 21% year-on-year rise in aluminum auto-part exports during 2024, with nearly two-thirds destined for ASEAN markets. Tier-1 suppliers are responding by dedicating up to 30% of new giga-press capacity to export-qualified parts, while simultaneously obtaining IATF 16949 recertification to satisfy Japanese and Korean OEM audit requirements.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Swings | -1.4% | National; energy-intensive zones | Short term (≤ 2 years) |

| High-Tonnage Machine Capex | -0.9% | National | Medium term (2-4 years) |

| Skilled Workforce Shortage | -0.7% | Emerging hubs | Long term (≥ 4 years) |

| Alternative Forming Competition | -0.5% | Application-specific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility and Power-Coal Shortages

Primary aluminum cash prices oscillated between USD 2,160 and USD 2,480 per tonne in 2024, while the Central Electricity Authority reported a 6% year-on-year rise in India’s average industrial power tariff, squeezing die casters’ operating margins. Coal supply issues forced smelters to import power-grade coal, raising costs. Hindalco committed USD 10 billion to expand capacity and transition toward renewables, hoping to stabilize input costs. Quarterly price-adjustment clauses now dominate OEM contracts, complicating forecast planning. Currency swings add risk for imported alloys and tool steel. To buffer volatility, leading die casters install scrap-melting lines, pushing recycled content toward 80% and lowering virgin-metal exposure.

High Capex for High-Tonnage HPDC Machines

Giga-presses costing above USD 20 million deter small firms and stretch payback to 5-7 years. Facility upgrades span deep foundations, crane capacity, and dedicated substations. Supplier options remain limited to a handful of European and Asian OEMs, elongating lead times. Smaller companies pivot to niche gravity-casting jobs or subcontract finishing work. Leasing models and state-backed credit lines emerge but adoption is slow. Consolidation accelerates as Tier-1 suppliers acquire capacity-constrained rivals, raising the India automotive parts aluminum die casting market’s entry barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process: Pressure Die Casting Maintains Primacy amid Precision Needs

Pressure die casting captured 68.74% of the India automotive parts aluminum die casting market in 2025. Stronghold applications include engine blocks, gear housings, and integrated suspension arms, where tolerance windows below 50 microns are mandatory. Industry 4.0 dashboards track injection pressure, melt temperature, and cycle time, trimming rejection rates below 5%. The India automotive parts aluminum die casting market size generated by semi-solid rheocasting is small today, yet shows the highest 9.32% CAGR, thanks to lower porosity, making it ideal for EV battery cases exposed to thermal cycling. Gravity die casting persists in truck components with lower surface-finish needs, though share erodes as cost per part falls for high-pressure equipment.

Advanced simulation packs such as ProCAST and MAGMASOFT enable virtual gating trials, saving USD 0.5 million per tool set and accelerating PPAP sign-off. Automated die-spray robots and vacuum-assisted filling strengthen mechanical properties, crucial for safety-critical chassis parts. ISO 9001 and IATF 16949 certification levels now exceed 85% of installed capacity nationwide, raising baseline quality and attracting export orders from ASEAN assemblers seeking predictable dimensional profiles.

By Application Type: Engine Parts Lead as Structural Castings Accelerate

Engine parts held a 45.98% share in 2025, benefiting from aluminum’s superior heat transfer that cools down-sized turbocharged engines more efficiently. The India automotive parts aluminum die casting market share for engine components will taper as EV penetration rises, yet absolute volume remains resilient due to hybrid powertrain complexity. Body and structural components grow fastest at 8.61% CAGR thanks to giga-casting adoption that consolidates rear under-bodies into single 60-kg castings. The India automotive parts aluminum die casting market size generated by battery housing castings may surpass engine blocks by the late 2020s as OEMs reorient platforms around skateboard architectures.

OEM validation protocols for structural castings now mirror BIW steel weld audits, demanding CT-scan inspections to verify internal integrity. End-users pay 15-20% price premiums for the elimination of 100-plus stamped parts and weld fixtures. Transmission and driveline castings remain steady as hybrids add planetary gearboxes. HVAC, steering, and brake parts embrace aluminum for corrosion resistance, especially in coastal cities where salt exposure accelerates oxidation on conventional ferrous alloys.

By Vehicle Type: Passenger Cars Dominate while Commercial Vehicles Modernize

Passenger cars produced 54.80% of 2025 revenue and will register a 7.70% CAGR through 2031. SUV models, which now account for 48% of domestic sales, consume larger structural castings and thick-wall suspension links. Two-wheeler OEMs pivot to aluminum clutch housings and alloy wheels, but unit value per vehicle remains low. Commercial fleets upgrade to aluminum cross-members and gearbox cases to boost payload efficiency. Scrappage incentives tied to weight reductions encourage fleet renewal. In last-mile delivery, three-wheelers employ aluminum swing arms to offset battery mass, improving ride comfort.

Regulations capping CO₂ per ton-kilometer spur heavy-truck makers to trial aluminum space frames, though adoption is early-stage. The India automotive parts aluminum die casting market benefits as bus OEMs test lightweight seat frames that cut curb weight by 150 kg, enabling extra ticketing capacity without breaching axle load limits.

By Casting Alloy Family: Al-Si Grades Dominate, yet Al-Mg Alloys Gain Momentum

Al-Si alloys such as ADC12 comprise 63.62% of 2025 output, prized for fluidity that fills thin-wall die cavities in under 1 second. Foundries optimize Sr-based modifiers to enhance elongation for safety-critical parts. Al-Mg alloys expanded at 8.02% CAGR owing to EV battery housing demand for corrosion resistance and electromagnetic compatibility. Recycled content now averages 45% across all alloy families and is poised to reach 60% under End-of-Life Vehicle mandates. Specialty Al-Cu grades serve turbocharger housings subjected to 600 °C exhaust gas, while proprietary low-shrink alloys enter giga-casting lines to curb distortion on 1.5 m long floor sections.

Spectrographic checks every batch ensure Si content stays within ±0.2 %, safeguarding tensile limits. Mechanical test coupons cast alongside production parts validate yield strength thresholds above 200 MPa. Foundries implementing closed-loop melt-quality feedback reduce inclusions below 80 ppm, improving fatigue life on suspension knuckles exposed to Indian road shock loads.

By End-User: OEM/Tier-1 Integration Tightens Supply Chains

OEM and Tier-1 players controlled 74.88% of 2025 turnover and expanded at 9.01% CAGR as automakers crave vertically integrated partners for platform modularity. Long-term agreements stretch five-plus years, ensuring amortization of USD 1 million multi-cavity dies across volume cycles. Independent aftermarket demand lags due to longer replacement intervals on aluminum parts with superior corrosion resistance.

The India automotive parts aluminum die casting industry sees consolidation: Samvardhana Motherson’s recent QIP raised USD 771 million to fund EV-oriented casting expansions. Quality systems aligned to IATF 16949 and ISO 14001 grant incumbents preferred-supplier status for export contracts to ASEAN and Japan.

Geography Analysis

West India generated 39.40% of 2025 revenue, anchored by Maharashtra-Gujarat’s mature ecosystem and port connectivity through JNPT and Kandla. Gujarat hosts 2.2 million-unit installed passenger-car capacity, driving stable die-casting pull via Maruti Suzuki and Tata Motors. Pune’s supplier belt focuses on precision gravity-casting and post-machining, while Aurangabad adds raw-material recycling capacity that lifts scrap utilization above 50%. State incentives, including tax holidays and subsidized power, cut landed cost against inland rivals.

South India is the fastest-growing cluster at 8.39% CAGR, spearheaded by Tamil Nadu’s Chennai-Oragadam corridor nicknamed “Detroit of Asia.” Hyundai, Renault-Nissan, and BYD anchor die-casting demand for engine blocks and EV platforms. State policies offering 35% capital-subsidy ceilings for EV parts spur new greenfield foundries along the Hosur-Attibele stretch. Port access at Ennore and Krishnapatnam expedites outbound ASEAN shipments.

North India’s Delhi-NCR caters mainly to aftermarket and Tier-2 machining hubs that supply clutch housings and steering components, benefiting from proximity to India’s largest vehicle park. However, growth lags at mid-single digits due to limited OEM production bases. East and North-East India leverage alumina and coal reserves yet remain nascent casting centers; infrastructure upgrades on the Digha-Petrapole corridor may unlock coastal export opportunities by late decade.

Regulatory Landscape

India’s regulatory regime for automotive aluminum die-cast parts is shaped by MoRTH notifications under the Central Motor Vehicles Rules (CMVR), supported by the Automotive Industry Standards Committee (AISC) and Automotive Industry Standards (AIS) published through ARAI, alongside product and material standardization by the Bureau of Indian Standards (BIS). In practice, these frameworks affect casting validation, documentation, and the test evidence OEMs request for safety and homologation, particularly for structural components.

A key compliance anchor for foundries and their upstream suppliers is BIS material standard IS 617:2024 for aluminium and aluminium alloy ingots and castings (applicable across casting processes including pressure die casting), which sets chemical composition and mechanical test parameters. In addition, DPIIT’s Aluminium and Aluminium Alloy Products (Quality Control) Order, 2026 (S.O. 1319(E), dated 11 March 2026) mandates BIS certification for specified aluminium and aluminium alloy products under the BIS Act, 2016, with BIS as the enforcing authority. Implementation is staged, with requirements becoming effective from 1 December 2026 for covered product groups, which increases the need for lot-level traceability and formal compliance documentation across the supply chain.

Value Chain Analysis

The value chain starts with primary aluminum and secondary scrap sourcing, followed by alloying and melt preparation, die and tooling design (often involving simulation-led gating and solidification engineering), and core manufacturing through high-pressure die casting (and, where relevant, low-pressure and gravity routes). Downstream steps include trimming, heat treatment (where specified), CNC machining, surface finishing, dimensional and metallurgical inspection, and then delivery to OEM/Tier-1 assembly lines under just-in-sequence schedules, with exports routed through coastal logistics corridors.

Industry participants include integrated automotive component suppliers and specialist casters. Named players with aluminum die-casting footprints include Endurance Technologies, Rockman Industries, Jaya Hind Industries, Sipra Engineers, Sandhar Group, Spark Minda Group, and Rico Auto Industries, supported by multi-location manufacturing networks serving regional automotive clusters. Trade bodies such as the Aluminium Casters’ Association (ALUCAST) and the Automotive Component Manufacturers Association of India (ACMA) back capability building through knowledge exchange and collaboration. Bottlenecks typically center on capital intensity for higher-tonnage cells, tooling lead times, and the need to secure consistent scrap quality and certification-ready test records to meet OEM and export audit requirements.

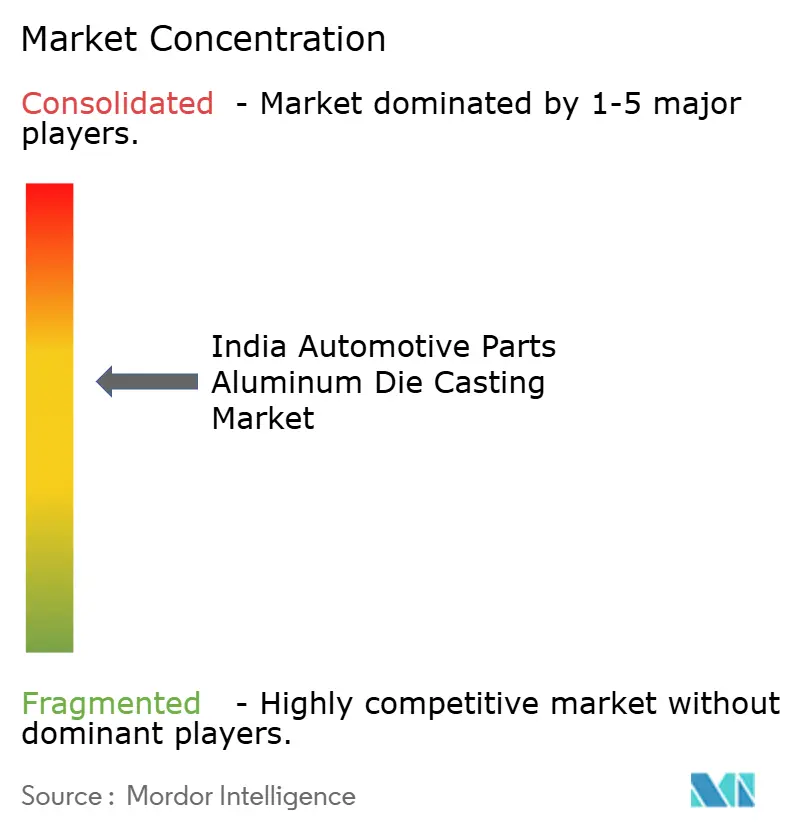

Competitive Landscape

The India automotive parts aluminum die casting market exhibits moderate fragmentation. The top five players control a significant share, reflecting sizable yet not dominant positions. Capital-intensive giga-casting lines tilt the field toward well-funded Tier-1s, while niche grav-casting shops survive on aftermarket orders. The technology race centers on real-time shot monitoring, vacuum-assisted filling, and AI-driven defect prediction.

Samvardhana Motherson expanded structural casting output after its AURANGABAD plant commissioned a 5,500-tonne press in 2025. Uno Minda broke ground on a Sambhaji Nagar die-casting unit focused on EV driveline parts in June 2025, targeting SOP within 18 months [3]“Uno Minda to Set Up New Aluminium Die Casting Facility,” Press Release, unominda.com. Sandhar Ascast doubled capacity by acquiring Sundaram-Clayton’s Hosur plant, ensuring captive supply to Japanese OEMs.

Export competitiveness improves as coastal foundries quote 15-day lead times to ASEAN OEMs pursuing China-plus-one strategies. Domestic rivals experiment with closed-loop recycling to lower carbon footprint, which appeals to global customers tracking Scope 3 emissions. New entrants face high die-steel prices and scarce simulation talent, nudging the industry toward collaborative R&D hubs in Pune and Bengaluru.

India Automotive Parts Aluminum Die Casting Industry Leaders

Endurance Technologies

Samvardhana Motherson Group

Rockman Industries

Sandhar Technologies

Spark Minda (Minda Corp)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity area is the shift in investment toward higher-tonnage high-pressure die casting capacity and integrated machining to supply EV and lightweighting-driven parts that require tighter metallurgy, repeatability, and traceability. Capacity announcements and corporate actions already signal where suppliers are placing resources: Jaya Hind Industries initiated a Chennai expansion program backed by a stated INR 200 crore plan with HPDC machines ranging from 1,400 to 4,400 tonnes, and Uno Minda approved a greenfield aluminium die-casting facility at Sambhaji Nagar (Aurangabad) with an announced INR 210 crore outlay to support EV-oriented demand.

Operational consolidation and digital process control also open room for suppliers that can shorten PPAP cycles and respond to audit intensity for safety-critical castings. In April 2026, CIE Automotive India’s board approved the merger of its wholly owned subsidiary CIE Aluminium Casting India Limited to drive production synergies and efficiencies, reflecting a move toward more integrated operating models. Alongside this, ALUCAST’s 2026 messaging around digital simulation and energy-efficient casting points to near-term buyer preference for suppliers that can document process capability and reduce defect risk while meeting increasingly formalized product quality expectations under BIS-led standardization and phased Quality Control Order enforcement.

Recent Industry Developments

- May 2026: Samvardhana Motherson highlighted its FY26 capex orientation and continued investment focus across businesses, reinforcing the ability of well-capitalized Tier-1 groups to fund casting, machining, and automation upgrades. This reinforces competitive pressure on smaller die casters facing high machine and infrastructure capex, accelerating the tilt toward scale players for complex programs.

- October 2025: Endurance Technologies commenced production at its AURIC, Bidkin facility following prior approvals for capacity addition, expanding its localized footprint in an industrial hub relevant to automotive aluminum components. The added manufacturing base supports shorter lead times for OEM programs and strengthens supply continuity for high-volume parts.

- December 2024: Jaya Hind Industries installed a 4,400-tonne high-pressure die-casting machine at its Urse, Pune plant to increase capability for large and intricate structural castings. The commissioning lifts domestic capacity for higher-complexity parts and aligns supplier capability with OEM moves toward more integrated cast components.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks the value of aluminum die cast automotive parts produced and supplied for use in vehicles in India, across common die casting routes used for automotive-grade components.

Scope exclusions: It excludes non-automotive end uses of aluminum die castings and non-die-casting processes such as forging, machining-only parts, and plastic molding.

Segmentation Overview

- By Production Process

- Pressure Die Casting

- Gravity Die Casting

- Semi-solid/Rheocasting

- By Application Type

- Engine Parts

- Body and Structural Parts

- Transmission and Driveline Parts

- E-mobility Battery Housings and Thermal Systems

- Other Applications (HVAC, Steering, Braking)

- By Vehicle Type

- Passenger Cars

- Two-Wheelers

- Three-Wheelers

- Light Commercial Vehicles

- Heavy Commercial Vehicles and Buses

- By Casting Alloy Family

- Al-Si Alloys (ADC12, LM-6 etc.)

- Al-Mg Alloys

- Al-Cu and Others

- By End-User

- OEM/Tier-1 Suppliers

- Independent Aftermarket

- By Region (India)

- West India

- South India

- North India

- East and North-East India

Data Sources, Market Sizing, and Validation

Desk Research

To build the first cut of the model, we start with public production and trade signals that explain how fast vehicle output and component demand are moving in India. Inputs such as the Society of Indian Automobile Manufacturers (SIAM), Ministry of Road Transport and Highways (vehicle registrations), Directorate General of Commercial Intelligence and Statistics (trade), and the India Brand Equity Foundation (sector snapshots) help us set realistic demand boundaries.

We also use company annual reports, investor presentations, and press releases to track capacity additions, program wins, and how alloy and energy costs are discussed, since these factors feed into component pricing. For grounding and cross-checks, we refer to peer-reviewed journals and patent databases for die casting process shifts and lightweighting adoption, and we selectively use paid subscriptions for company financials, news and financials, and shipment-level import export checks where disclosure is limited. These desk sources are illustrative only, and many other public references were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work was used to test assumptions that are usually not visible in public data, especially the share of parts actually made by aluminum die casting and the way OEM sourcing is shifting for new platforms. We spoke with a mix of die casters, tooling and process specialists, and automotive procurement and engineering stakeholders across India to confirm utilization patterns, typical part migration (for example, from iron or steel to aluminum), and near-term price movement expectations.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 18% | |

| Mid tier: 51% | Functional/Unit leaders: 25% | |

| Smaller Players: 19% | Managers: 57% |

Market-Sizing & Forecasting

The sizing starts from a top-down demand pool, where vehicle production and registration trends are translated into a likely build rate for die cast aluminum parts, followed by an adjustment for local sourcing versus imports. Once this total is built, it is checked against selective bottom-up approximations using a sample of supplier revenues, installed press capacity with typical utilization, and an ASP per kg applied to implied tonnage so the final number stays practical.

Key inputs used in the model include passenger vehicle and commercial vehicle output, aluminum share of powertrain and body parts, average casting weight per vehicle (and how it changes with electrification), observed utilization and scrap rates, and the pass-through timing of aluminum and energy costs into component pricing. For forecasting, scenario analysis is used with a base case anchored to OEM production outlooks and supplier expansion plans that were validated during interviews, and then the short-term trend is smoothed so year-to-year jumps are explained by capacity changes rather than assumption alone. When supplier disclosures are incomplete, gaps are handled by using process-level benchmarks and then tightening them through follow-up calls and consistency checks across applications like engine, transmission, and body parts.

Data Validation & Update Cycle

Outputs are validated through triangulation across at least three angles, which typically include implied tonnage, price per kg ranges, and vehicle-output-linked demand. If a metric looks off, such as a sudden rise in value without a matching production trigger, the drivers are rechecked and the assumptions are revisited with additional expert inputs before sign-off.

Each report is refreshed annually, and interim updates are done when material events occur, such as major capacity announcements, sharp metal price swings, or policy changes affecting vehicles. Before delivery, a final pass is completed so the published view reflects the latest available data and interview feedback.

Mordor Intelligence's India Automotive Parts Aluminium Die Casting Market Size Measured Against Other Published Estimates

It is normal to see different market sizes for the same space because publishers do not always count the same boundary, the same pricing basis, or the same timing for conversion into USD. Differences also show up when one study uses tonnage-led logic while another relies more on company revenue snapshots, which can shift the final number even if the growth story looks similar.

By tracking vehicle production-linked casting intensity and refreshing currency timing assumptions, Mordor Intelligence keeps the estimate tied to automotive-only die cast parts in India rather than mixing in broader industrial die cast revenue or older price points. The biggest gaps usually come from whether non-automotive die castings are included, whether the scope is total aluminum die casting versus automotive parts only, and whether the base year reflects recent changes in press utilization and alloy pass-through.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.71 B (2025) | |

| Industry Research Marketplace A | USD 1.09 B (2020) | Uses an older base year with a shorter window, and the price and mix assumptions can sit at pre-recent capacity shifts, which pulls the value down versus a 2025-priced view. |

| Market Outlook Publisher B | USD 1.27 B (2024) | Covers India aluminum die casting across end uses, so non-automotive demand can be blended in, and automotive-only application weights are not always isolated cleanly. |

The spread is mainly explained by scope and timing, since an automotive-only model priced in 2025 will not match a broader die casting total or an older year snapshot. With clear boundary rules and repeatable checks using production, tonnage, and price signals, the final result stays easier to audit and to update when demand or input costs move.

Key Questions Answered in the Report

What is the projected value of the India automotive parts aluminum die casting market in 2031?

The market is forecast to reach USD 2.61 billion by 2031.

Which region holds the largest share of aluminum die casting demand in India?

West India, led by the Maharashtra-Gujarat corridor, accounted for 39.40% of revenue in 2025.

Which production process dominates aluminum die casting for automotive parts in India?

Pressure die casting leads with 68.74% share owing to its precision and high throughput.

How fast is the body and structural casting segment growing?

This segment is expanding at an 8.61% CAGR through 2031, the quickest among applications.

Page last updated on: