Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

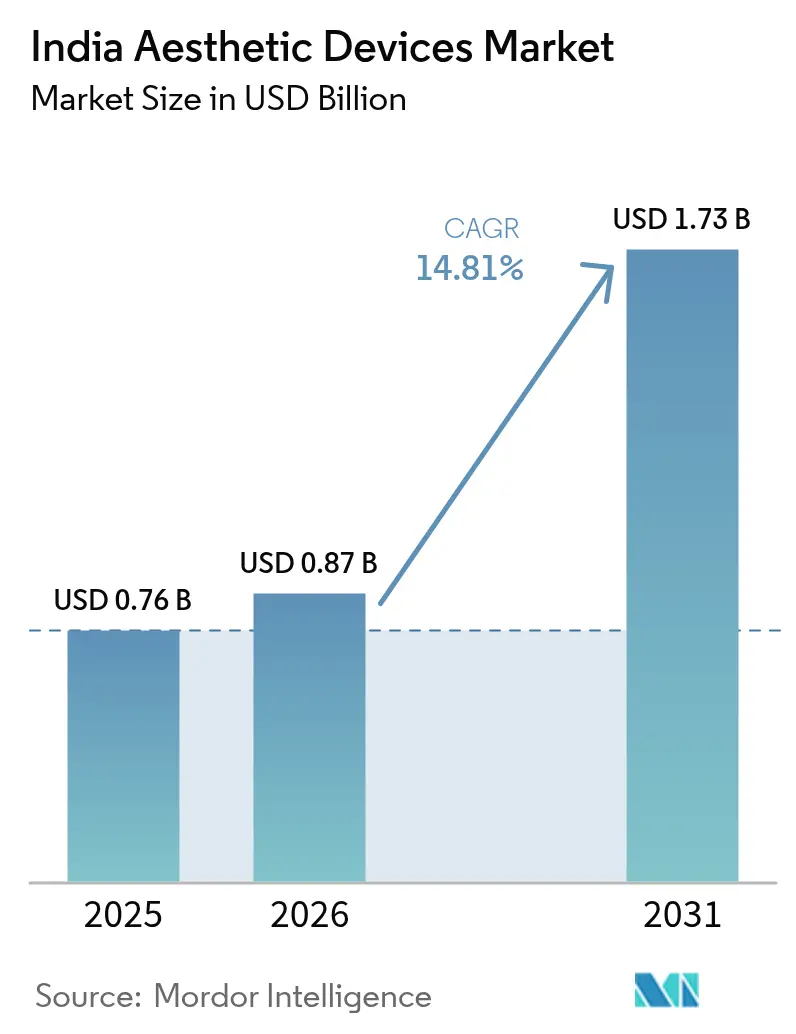

| Base Year Market Size (2025) | USD 0.76 Billion |

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 14.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Aesthetic Devices Market Analysis by Mordor Intelligence

The India Aesthetic Devices Market size is projected to be USD 0.76 billion in 2025, USD 0.87 billion in 2026, and reach USD 1.73 billion by 2031, growing at a CAGR of 14.81% from 2026 to 2031.

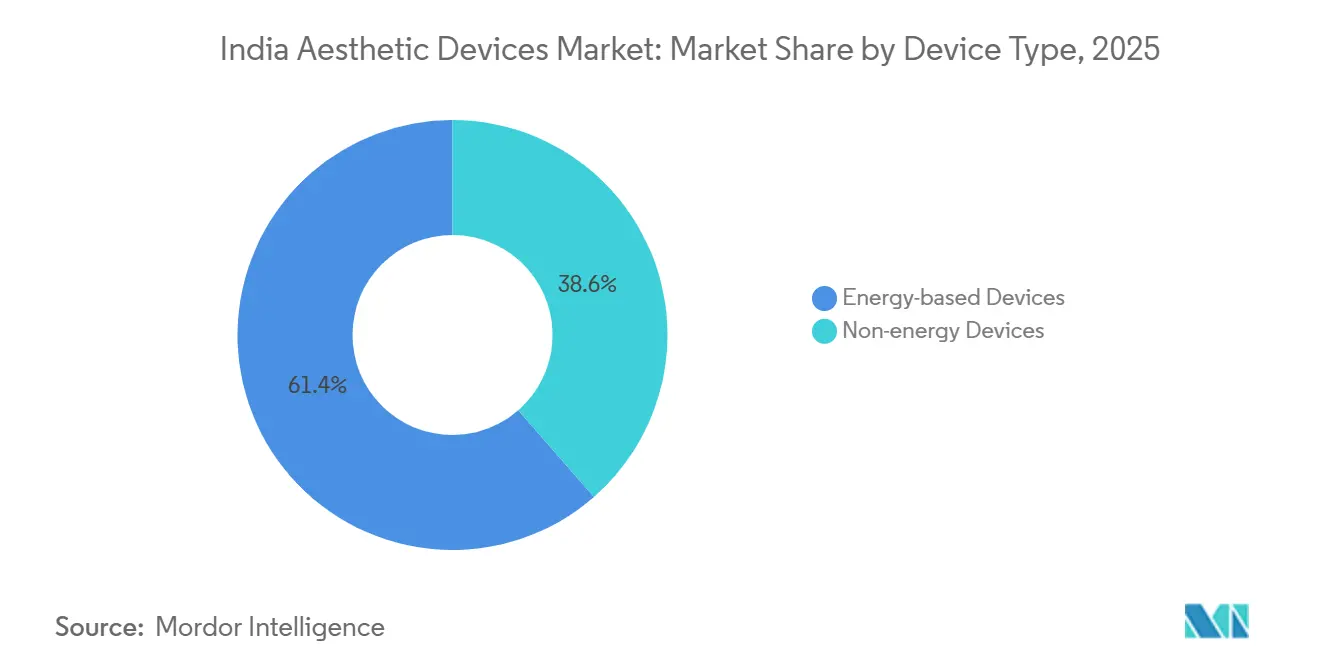

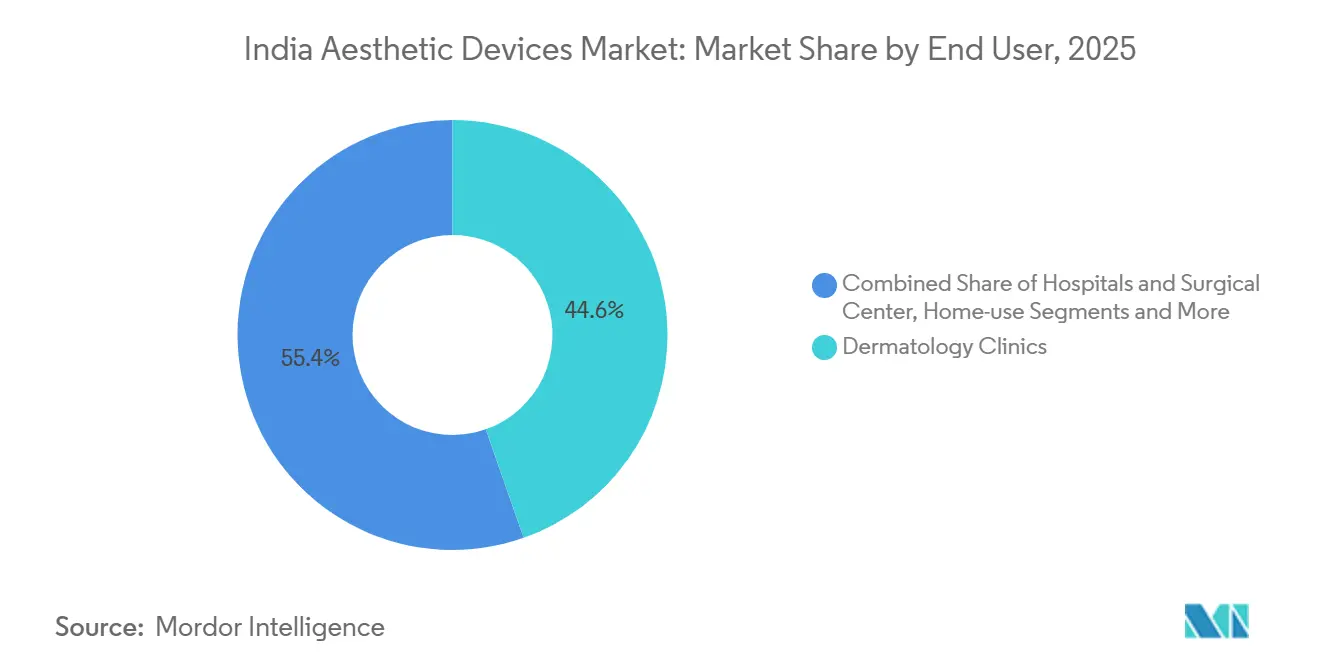

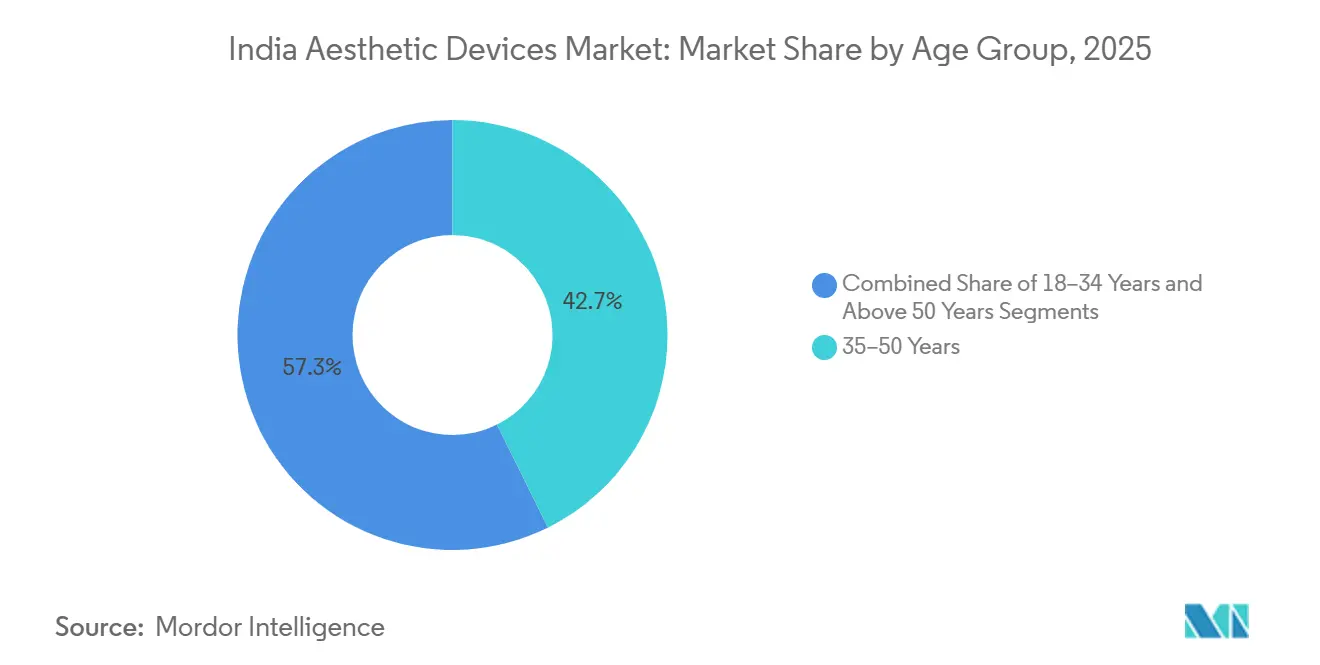

A favorable demographic profile, rising disposable incomes and the government’s Production-Linked Incentive (PLI) program, which approved 22 new med-tech plants by 2025, are accelerating local manufacturing capacity.[1]CDSCO, “Medical Device Rules 2017 and Classification Guidelines,” cdsco.gov.in Energy-based systems held 61.43% share in 2025, yet non-energy platforms such as dermal fillers and injectables are projected to expand 16.67% annually thanks to shorter procedures and minimal downtime, making them attractive for time-pressed professionals. Hair-removal applications generated 23.75% of 2025 revenue, while body-contouring and cellulite-reduction devices are on track for 17.01% CAGR, supported by radiofrequency (RF) and high-intensity focused ultrasound (HIFU) technologies that reduce fat without surgery. Dermatology clinics dominated end-user revenue with 44.62% share, but home-use gadgets are climbing at 18.89% CAGR as e-commerce widens access. Male procedures, although only 16.86% of volume, are gaining 15.85% a year as workplace appearance expectations grow, and the 18-34 age group is rising 16.83% annually on the back of “tweakment” culture fueled by social media.

Key Report Takeaways

- By device type, energy-based systems led with 61.43% of the India aesthetic devices market share in 2025, while non-energy platforms are projected to expand at a 16.67% CAGR through 2031.

- By application, body contouring and cellulite reduction is forecast to advance at a 17.01% CAGR through 2031, overtaking legacy hair-removal growth rates.

- By end user, dermatology clinics held 44.62% of revenue in 2025, whereas home-use devices post the highest projected CAGR at 18.89% to 2031.

- By gender, female patients accounted for 83.14% share in 2025, yet male demand is expanding at a 15.85% CAGR over 2026-2031.

- By age group, the 35-50 years cohort captured 42.68% of the India aesthetic devices market size in 2025, while the 18-34 years segment is projected to log the fastest growth at a 16.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes & beauty focus | +2.5% | Metros and tier-1 cities such as Delhi NCR, Mumbai, Bengaluru, Hyderabad, Chennai, Pune | Medium term (2-4 years) |

| Medical tourism & premium wellness boom | +2.0% | Delhi NCR, Mumbai, Bengaluru, Chennai; spillover in Goa, Kerala, Rajasthan | Long term (≥4 years) |

| Tech advances in energy-based & AI devices | +2.8% | National; earliest uptake in metro clinics with tier-1 spillover | Short term (≤2 years) |

| Government PLI scheme for med-tech | +1.8% | Manufacturing hubs in Gujarat, Tamil Nadu, Karnataka, Maharashtra | Long term (≥4 years) |

| Shift to non-invasive, home-use devices | +2.3% | Metros and tier-1 cities; nationwide via e-commerce | Medium term (2-4 years) |

| Localization to cut import dependence | +1.5% | Device parks in Gujarat, Tamil Nadu, Karnataka; national supply-chain benefits | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Awareness Regarding Aesthetic Procedures

Urban consumers view cosmetic enhancement as routine wellness rather than vanity, a perception shift amplified by celebrity endorsements and social-media narratives. India now ranks second in rhinoplasty volume and third in liposuction counts worldwide, giving clinics deeper case experience that feeds further acceptance. Male demand grows for gynecomastia correction and hair restoration, broadening the gender mix once skewed toward female clientele. Consultation numbers surge in tier-2 cities yet infrastructure gaps still limit procedural throughput outside metros. Training institutes respond by running short intensive programs, which in turn seed new clinics in smaller urban clusters.

Rising Disposable Incomes & Beauty-Conscious Consumers

India’s per-capita disposable income is growing 14.6% annually through 2027, widening the pool of consumers who can afford elective aesthetic treatments. Dual-income households in metros now direct 3-5% of discretionary spend to personal grooming, and the broader beauty-and-personal-care sector is on track to double to USD 30 billion by 2027. Elevated workplace grooming norms in IT services, banking and hospitality are prompting earlier intervention, with the typical first procedure age slipping from the mid-40s to the early-30s. Clinics bundle entry-level services with installment plans, lowering the trial barrier and sustaining demand for consumables.

Growing Medical Tourism & Premium Wellness Segment Expansion

India drew 7.3 million inbound medical travelers in 2024 and the segment could generate USD 16.21 billion by 2030, buoyed by cost advantages of 60-70% versus Western markets and streamlined e-visas under the “Heal in India” initiative. High-value visitors book facelifts, body contouring and laser resurfacing alongside wellness packages in Goa, Kerala and Rajasthan, allowing clinics to invest in flagship lasers such as PicoWay and Morpheus8 without fearing price push-back. Global patient expectations drive technology upgrades that later disseminate to domestic clientele.

Technological Advances in Energy-Based and AI-Integrated Devices

Artificial-intelligence modules embedded in devices now guide treatment parameters and predict outcomes, cutting operator dependency and elevating satisfaction. InMode’s Morpheus8 blends microneedling with bipolar RF for deep collagen remodeling, while BTL’s Emsculpt NEO couples RF heating with high-intensity focused electromagnetic fields to produce simultaneous fat reduction and muscle gains validated at 30% and 25%, respectively.[2] Picosecond-class lasers like PicoWay fragment pigment with less thermal damage, reducing sessions from eight to roughly five, thereby boosting clinic throughput.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device and treatment costs in tier-2/3 cities | -1.2% | Tier-2, tier-3 cities and rural pockets | Medium term (2-4 years) |

| Fragmented CDSCO pathways and long approval cycles | -0.9% | Nationwide | Short term (≤2 years) |

| Shortage of skilled practitioners outside metros | -0.7% | Tier-2, tier-3 cities and rural areas | Long term (≥4 years) |

| Proliferation of low-quality or grey-market devices | -0.8% | Nationwide, but acute in price-sensitive smaller cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device and Treatment Costs Limiting Tier-2/3 Penetration

Capital equipment prices range from INR 15 lakh to INR 1.5 crore (USD 18,000-180,000), a hurdle for single-doctor clinics beyond major metros. May 2025 pricing data showed skin-rejuvenation sessions averaging INR 27,000-55,000 (USD 325-660), far above the spending power of most households. Banks treat aesthetic platforms as non-essential assets, so loans carry 12-15% interest with five-year ceilings, pushing up practice overhead. The National Pharmaceutical Pricing Authority does not cap these procedures, leaving prices to market forces. Consequently, the India aesthetic devices market still skews toward the top income decile, slowing rural penetration.

Fragmented Regulatory Pathways and CDSCO Approval Delays

Energy-based platforms fall into Class C or D under the Medical Device Rules 2017, demanding clinical data and ISO 10993 biocompatibility tests that stretch approval to 9-15 months.[3]BTL Aesthetics, “Emsculpt NEO Clinical Data and Technology Overview,” btlaesthetics.com Devices from non-GHTF nations undergo extra local trials, costing up to INR 1 crore (USD 120,000) and a further year in lead time. The January 2025 ban on refurbished imports erased an INR 1,500 crore (USD 180 million) gray channel but also removed a lower-cost option for budget clinics. While an expert panel is drafting rules, implementation is unlikely before 2027. These frictions delay innovation and allow established players to entrench share in the India aesthetic devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Non-Energy Platforms Gain Share

Energy-based systems captured 61.43% of the India aesthetic devices market share in 2025. Non-energy options—fillers, injectables and microdermabrasion kits—are projected to grow 16.67% a year because sessions last just 15-30 minutes and have little downtime. A microdermabrasion unit costs INR 1-3 lakh (USD 1,200-3,600), versus INR 25-50 lakh (USD 30,000-60,000) for a fractional CO₂ laser, so new clinics find entry barriers lower. Dermal-filler demand rises as certified injectors multiply in tier-1 cities, while hyaluronic-acid brands from Galderma and AbbVie lead supply.

Radiofrequency devices are expanding fastest within the energy cohort, favored for treating Fitzpatrick IV-V skin without risking post-inflammatory hyperpigmentation. InMode’s Morpheus8 marries RF with microneedling, and BTL’s Exilis Ultra combines RF and ultrasound in a single handpiece. High-intensity focused ultrasound (HIFU) gains ground for non-surgical facelifts, whereas intense pulsed light (IPL) fills a lower-price niche at INR 8-15 lakh (USD 10,000-18,000). All energy units must clear CDSCO Class C rules, prolonging market-entry lead times by up to a year, yet technology upgrades continue to refresh the India aesthetic devices market.

By Application: Body Contouring Outpaces Legacy Segments

Hair removal delivered 23.75% of 2025 application revenue and remains a core entry point for many clinics. Even so, body-contouring and cellulite-reduction procedures are set to expand at a 17.01% CAGR, the fastest among all uses. BTL’s Emsculpt NEO produced 30% fat reduction and 25% muscle gain in trials, reinforcing a non-surgical alternative narrative. Cryolipolysis brands such as CoolSculpting price a single area at INR 80,000-150,000 (USD 960-1,800) but still undercut surgical liposuction by roughly half.

Skin resurfacing with fractional CO₂ or erbium lasers forms the second-largest slice, treating acne scars and photoaging in the 40-60 age group. Picosecond lasers like Candela’s PicoWay shorten treatment cycles to three or four sessions. Facial injectables grow fastest in metros, while pigmented- and vascular-lesion therapies benefit from improved selectivity at 755 nm and 1,064 nm wavelengths. Together these shifts broaden procedure menus and enlarge the India aesthetic devices market.

By End User: Home-Use Devices Disrupt Clinic Dominance

Dermatology clinics generated 44.62% of end-user revenue in 2025, leveraging multi-device portfolios and medical credibility. Hospitals and surgical centers follow with roughly one-quarter share, bundling aesthetic add-ons with reconstructive or bariatric surgery for medical tourists. Medical spas differentiate through hospitality-style ambience but face patchy licensing, which could tighten under proposed IADVL oversight rules.

Home-use gadgets—LED masks, microcurrent rollers, low-energy RF wands—are gaining at an 18.89% CAGR. Amazon India, Nykaa and Flipkart expanded listings 40-plus percent in 2025, pairing EMI plans with influencer marketing to draw first-time buyers. Draft CDSCO guidance slots most at-home tools into Class A or B, allowing approval in 3-6 months. Although clinical power remains modest, convenience is helping this channel widen the India aesthetic devices market among tier-2 households.

By Gender: Male Aesthetic Adoption Accelerates

Female patients still represented 83.14% of demand in 2025. Nonetheless, male volume is climbing 15.85% annually as grooming culture spreads in IT, banking and media workplaces. India’s men’s-care retail segment is marching toward INR 35,000 crore (USD 4.2 billion) by 2028, and procedures such as beard-line laser sculpting, back-hair removal and abdominal contouring are part of the basket.

Device makers now market settings optimized for coarse male hair and thicker collagen. RF energy for muscle definition and higher fluence alexandrite lasers (18-22 J/cm²) headline campaigns on sports and business social networks. Higher consumable usage per session keeps male ticket sizes 10-15% above female equivalents, expanding clinic margins and enlarging the India aesthetic devices market.

By Age Group: Youth Cohort Embraces Preventative Aesthetics

The 35-50 bracket generated 42.68% of 2025 revenue, reflecting accumulated photoaging that drives corrective treatments. Yet the 18-34 cohort is forecast to rise 16.83% a year as social platforms normalize low-dose “baby Botox,” skin boosters and LED phototherapy. Millennials demand downtime under 48 hours and favor non-ablative fractional lasers over aggressive CO₂ peels.

Disposable income is lower for this group, so clinics push subscription bundles and EMI plans spreading costs across 12 months. Express sessions priced at INR 3,000-5,000 (USD 36-60) widen the funnel, while loyalty programs retain customers through quarterly maintenance visits. Older consumers (>50 years) remain fewer but spend more per visit on multi-modal plans, adding depth to the India aesthetic devices market.

Geography Analysis

Delhi NCR, Mumbai, Bengaluru, Hyderabad, Chennai and Pune collectively generated about 65-70 % of 2025 revenue, underscoring the metro-centric nature of the India aesthetic devices market. In Delhi NCR, Practo data put an average skin-rejuvenation ticket at INR 44,000 (USD 530), roughly 20 % above Pune or Chennai, mirroring higher real-estate and practitioner costs. Southern states also benefit from 46.4 % of postgraduate dermatology seats, helping them adopt picosecond lasers and HIFU earlier than northern peers.

Tier-2 cities such as Ahmedabad, Jaipur, Lucknow, Chandigarh, Kochi and Indore represent the next frontier for the India aesthetic devices market, powered by rising disposable income and chain-clinic rollouts from operators like Kaya and Oliva. Yet penetration remains hamstrung by INR 15-50 lakh (USD 18,000-60,000) device costs, limited specialist density and lower consumer awareness. Home-use gadgets sold on Amazon India and Flipkart are filling part of the gap, although lower clinical power caps repeat purchase rates because outcomes trail clinic systems by about 50 %.

Medical tourism funnels high-value patients into Delhi, Mumbai, Bengaluru and Chennai, reinforcing their dominance in the India aesthetic devices market. The “Heal in India” campaign drove 7.3 million inbound patients in 2024 and promises expedited e-visas plus Joint Commission International-accredited facilities. Simultaneously, the PLI program is dispersing manufacturing to Tamil Nadu, Gujarat, Karnataka and Maharashtra, shrinking device lead times from 90-120 days to 30-45 days. By 2031, local assembly could furnish 30-40 % of domestic energy-based demand, cutting landed costs and improving after-sales service for clinics in emerging cities—an inflection point for wider India aesthetic devices market adoption.

Competitive Landscape

Global OEMs include Candela, Lumenis, InMode, BTL, Alma Lasers, Cutera, Fotona and Sciton, shaping a moderately concentrated India aesthetic devices market. Their edge stems from direct sales, key-opinion-leader endorsements and multi-year service contracts that lock in consumable revenue. Indian pharmaceutical majors Galderma India, AbbVie, Merz Pharma and Piramal Enterprises dominate injectables, leveraging dermatology networks to cross-sell energy devices.

Competitive differentiation now pivots on multimodality. InMode’s Morpheus8 pairs bipolar RF with microneedling, while BTL’s Emsculpt NEO unites RF heating with high-intensity electromagnetic fields, producing simultaneous muscle gain and fat loss validated at 25 % and 30 %, respectively. Candela’s PicoWay picosecond laser disrupts pigment in trillionths of a second, cutting downtime and allowing clinics to charge 20-30 % premiums, a factor that lifts revenue density across the India aesthetic devices market.

Quality control remains a flashpoint. The Delhi High Court awarded Johnson & Johnson INR 3.34 crore (USD 400,000) for counterfeit losses, and Telangana regulators seized INR 4 lakh (USD 4,800) of unlicensed gear in February 2026. Industry groups are lobbying for mandatory QR-code traceability. Until then, sporadic enforcement means grey-market operators continue to undercut legitimate players, tempering price realization within the India aesthetic devices market but also opening whitespace for mid-tier, locally built platforms that meet CDSCO norms.

India Aesthetic Devices Industry Leaders

Alma Lasers

AbbVie

BTL India Pvt Ltd

Cutera Healthcare Pvt Ltd

Lumenis Be India Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: AIIMS New Delhi announced India’s first face-transplantation program, establishing a patient registry for severe facial deformity cases

- January 2026: VCare opened a Bangalore Center of Excellence offering “Single-Day Facial Architecture,” with expansion plans for Hyderabad and more Bengaluru sites.

- August 2025: Aerolase introduced its Neo Elite laser, the first US FDA-cleared 650-microsecond Nd:YAG platform to enter the India aesthetic devices market.

- April 2025: Skinwood Luxury Aesthetic Centre launched SkinPen Precision, the first US FDA-cleared microneedling device in India, signaling stricter evidence requirements for premium clinics.

India Aesthetic Devices Market Report Scope

As per the scope of the report, aesthetic devices are tools used for non-surgical or minimally invasive cosmetic procedures to improve appearance through technologies like lasers, radiofrequency, ultrasound, and light.

The India aesthetic devices market report is segmented by Device Type, Application, End User, Gender, and Age Group. By Device Type, the market is segmented into Energy-based Devices (Laser-based, Radiofrequency, IPL & Light‑based, Ultrasound/HIFU) and Non-energy Devices (Dermal Fillers & Injectables, Implants, Microdermabrasion & Dermarollers). By Application, the market is segmented into Skin Resurfacing & Tightening, Hair Removal, Body Contouring & Cellulite Reduction, Facial Aesthetic Procedures, Pigmented & Vascular Lesion Treatment, and Others. By End User, the market is segmented into Dermatology Clinics, Hospitals & Surgical Centers, Medical Spas & Wellness Centers, and Home‑use. By Gender, the market is segmented into Female and Male. By Age Group, the market is segmented into 18–34 Years, 35–50 Years, and Above 50 Years. Market Forecasts are Provided in Terms of Value (USD).

By Device Type

| Energy-based Devices | Laser-based |

| Radiofrequency | |

| IPL & Light-based | |

| Ultrasound / HIFU | |

| Non-energy Devices | Dermal Fillers & Injectables |

| Implants | |

| Microdermabrasion & Dermarollers |

By Application

| Skin Resurfacing & Tightening |

| Hair Removal |

| Body Contouring & Cellulite Reduction |

| Facial Aesthetic Procedures |

| Pigmented & Vascular Lesion Treatment |

| Others |

By End User

| Dermatology Clinics |

| Hospitals & Surgical Centers |

| Medical Spas & Wellness Centers |

| Home-use |

By Gender

| Female |

| Male |

By Age Group

| 18–34 Years |

| 35–50 Years |

| Above 50 Years |

| By Device Type | Energy-based Devices | Laser-based |

| Radiofrequency | ||

| IPL & Light-based | ||

| Ultrasound / HIFU | ||

| Non-energy Devices | Dermal Fillers & Injectables | |

| Implants | ||

| Microdermabrasion & Dermarollers | ||

| By Application | Skin Resurfacing & Tightening | |

| Hair Removal | ||

| Body Contouring & Cellulite Reduction | ||

| Facial Aesthetic Procedures | ||

| Pigmented & Vascular Lesion Treatment | ||

| Others | ||

| By End User | Dermatology Clinics | |

| Hospitals & Surgical Centers | ||

| Medical Spas & Wellness Centers | ||

| Home-use | ||

| By Gender | Female | |

| Male | ||

| By Age Group | 18–34 Years | |

| 35–50 Years | ||

| Above 50 Years | ||

Key Questions Answered in the Report

What is the current size of the India aesthetic devices market and its expected 2031 value?

The market is valued at USD 0.868 billion in 2026 and is forecast to reach USD 1.73 billion by 2031.

Which device category is growing fastest?

Non-energy platforms, led by dermal fillers and injectables, are projected to grow at 16.67 % CAGR.

Which application shows the highest future growth?

Body contouring and cellulite reduction devices are forecast to expand at a 17.01 % CAGR through 2031.

How quickly are home-use aesthetic devices expanding?

Home-use gadgets are advancing at an 18.89 % CAGR as e-commerce channels broaden access.

What role does the PLI scheme play in market dynamics?

The PLI program funds new med-tech plants and could lift local assembly to 30-40 % of domestic energy-based sales by 2031, easing import reliance.

Page last updated on: