Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

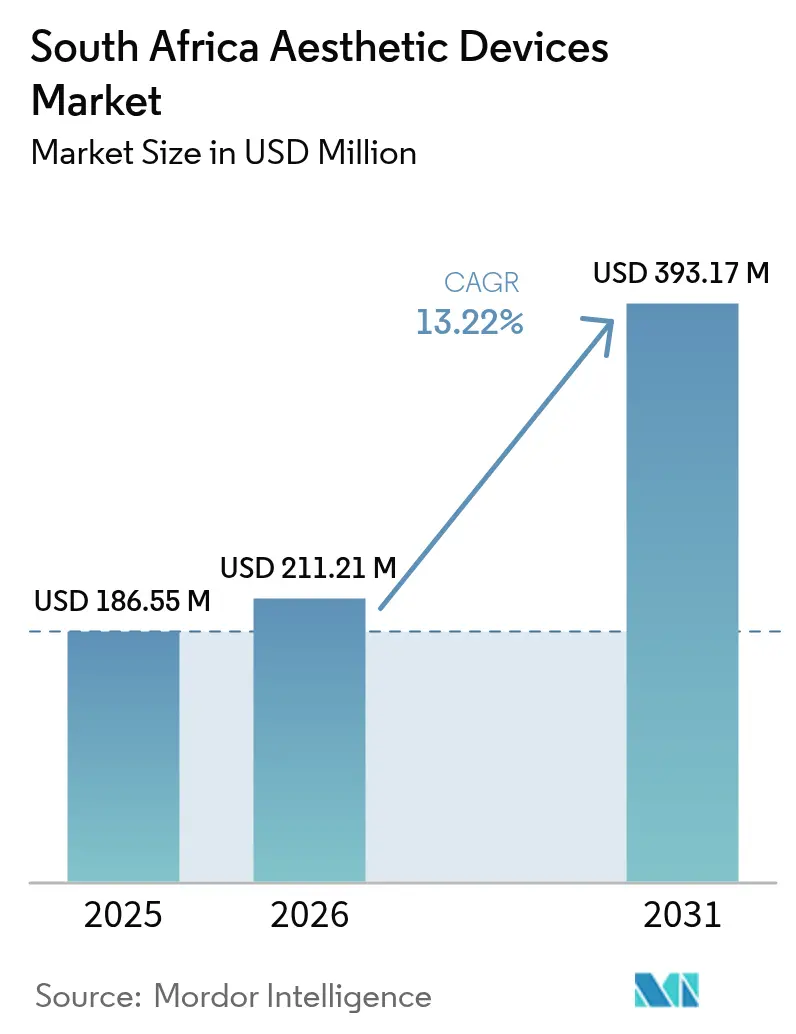

| Base Year Market Size (2025) | USD 186.55 Million |

| Market Size (2026) | USD 211.21 Million |

| Market Size (2031) | USD 393.17 Million |

| Growth Rate (2026 - 2031) | 13.22% CAGR |

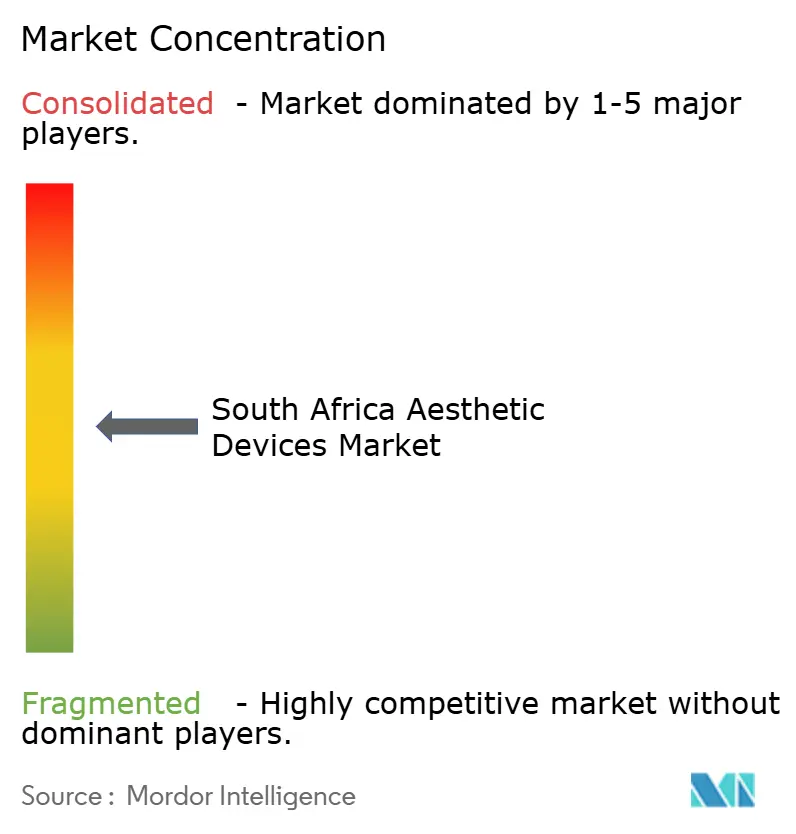

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Aesthetic Devices Market Analysis by Mordor Intelligence

The South Africa Aesthetic Devices Market size is expected to grow from USD 186.55 million in 2025 to USD 211.21 million in 2026 and is forecast to reach USD 393.17 million by 2031 at 13.22% CAGR over 2026-2031.

Sustained demand for minimally-invasive procedures, a growing pool of qualified specialists, and South Africa’s role as a regional medical-tourism hub provide strong tailwinds. Energy-efficient device innovations help facilities mitigate chronic power-supply risks, while the International Society of Aesthetic Plastic Surgery (ISAPS) records show that non-surgical treatments already outnumber surgical interventions, underscoring the market’s device-centric growth path. Increasing male participation, especially among black professionals, further broadens the addressable patient base. At the same time, the South Africa aesthetic devices market faces structural hurdles ranging from out-of-pocket payment norms to intermittent load-shedding that raises operating costs for energy-based systems.

Key Report Takeaways

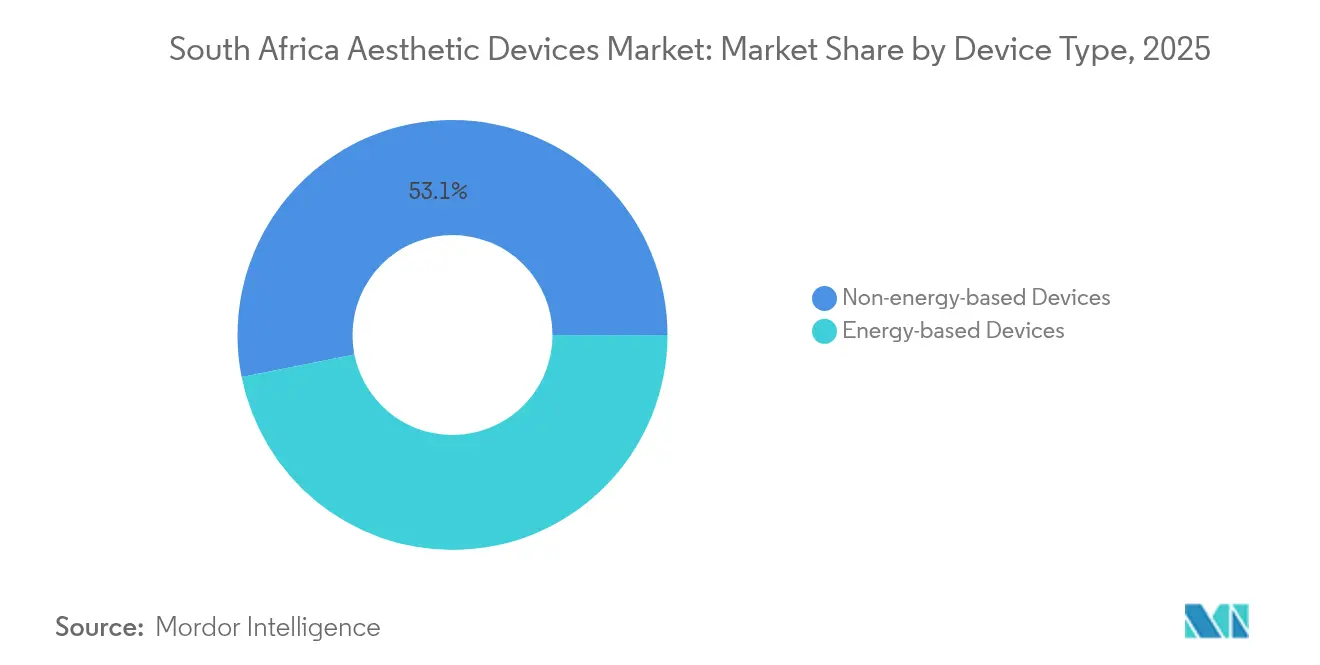

- By device type, non-energy-based devices held 53.12% revenue share in 2025; radio-frequency-based devices are forecast to expand at a 16.58% CAGR through 2031.

- By application, hair removal led with a 31.20% share of the South Africa aesthetic devices market size in 2025, while body contouring and cellulite reduction is set to grow at a 14.92% CAGR to 2031.

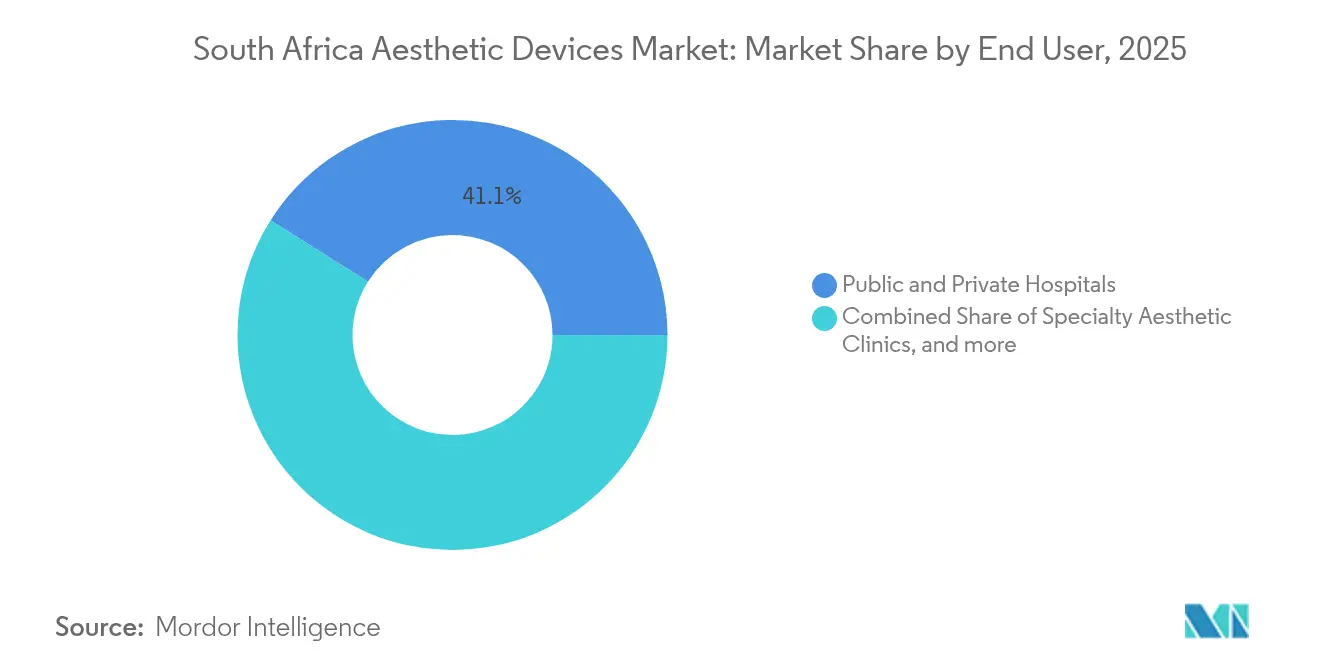

- By end user, public and private hospitals accounted for 41.05% of the South Africa aesthetic devices market share in 2025, whereas specialty aesthetic clinics are poised for the fastest 13.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased awareness of minimally-invasive procedures | +2.8% | Major metros including Johannesburg, Cape Town, Durban | Medium term (2–4 years) |

| Rising prevalence of skin disorders & obesity | +1.9% | National, skewed toward emerging middle-income cohorts | Long term (≥ 4 years) |

| Medical-tourism inflow | +1.2% | Regional hub drawing patients from sub-Saharan Africa | Medium term (2–4 years) |

| Expanding disposable income & aspirational spend | +0.9% | Urban middle class | Short term (≤ 2 years) |

| Post-pandemic surge in male demand | +0.8% | Urban, especially black professionals | Short term (≤ 2 years) |

| Social-media-enabled tele-consult platforms | +0.6% | Rural and semi-urban districts with mobile access | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Awareness of Minimally-Invasive Cosmetic Procedures

Social media normalizes aesthetic enhancements and rapidly diffuses treatment knowledge. ISAPS data show that non-surgical procedures represented 56.5% of all South African aesthetic interventions in 2023, led by 29,643 botulinum-toxin injections and 12,641 hyaluronic-acid filler sessions.[1]International Society of Aesthetic Plastic Surgery, “Global Survey 2023,” isaps.org Celebrity endorsements reinforce safety perceptions, and tele-consultation apps widen specialist access for rural residents. Artificial-intelligence-guided treatment planning raises outcome predictability, addressing safety concerns. SAHPRA’s device-registration system ensures that only approved technologies reach clinics, further boosting patient confidence.[2]South African Health Products Regulatory Authority, “Medical Device Regulatory Framework,” sahpra.org.za

Rise in Skin Disorders & Obesity Prevalence

Environmental stressors and genetic predispositions heighten incidences of hyperpigmentation, keloids, and post-inflammatory scars among black South Africans, sharpening demand for pigment-safe lasers and intense-pulsed-light systems. Simultaneously, national obesity rates spur interest in non-invasive fat-reduction and skin-tightening devices. Emerging male-grooming brands tailored to black-male skin, such as locally developed lines targeting razor-bump complications, illustrate untapped product-adjacency opportunities. Medical-aid schemes increasingly recognize functional benefits of scar-revision therapies, supporting partial reimbursement for select devices.

Growth in Medical Tourism Inflow

Competitive procedure pricing and English-language care attract patients from Namibia, Botswana, and beyond. Some Johannesburg plastic surgeons report that regional clients make up more than 80% of their caseloads. Dedicated recovery villas, safari-linked wellness packages, and internationally accredited clinics amplify South Africa’s value proposition. The multiplier effect lifts local hospitality sectors, justifying investments in advanced energy-based systems that command premium prices.

Expanding Disposable Income & Aspirational Spending

Despite broad macro-economic headwinds, the emerging middle class continues to channel discretionary funds into appearance-enhancing services as a marker of professional success. Academic research on conspicuous consumption among black professionals confirms status-signaling motivations behind elective healthcare purchases. Flexible payment plans and buy-now-pay-later options make high-ticket body-contouring packages more accessible, smoothing clinic cash flows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of reimbursement; out-of-pocket model | -1.7% | National, hardest on lower-income groups | Long term (≥ 4 years) |

| High capital & maintenance cost of devices | -1.2% | National, severe for small practices | Medium term (2–4 years) |

| Electricity load-shedding disruptions | -0.8% | National, acute in public hospitals | Short term (≤ 2 years) |

| Counterfeit injectables eroding trust | -0.6% | Informal markets in metropolitan areas | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Lack of Reimbursement; Out-of-Pocket Model

Full cash payment narrows access to advanced treatments, concentrating demand among affluent urbanites. Multi-session therapies such as cryolipolysis face higher patient-dropout risk due to cumulative cost. Although third-party financing products exist, high interest rates still deter middle-income consumers. Insurers seldom cover procedures even when functional benefits—for example, hyperhidrosis management—are clinically documented.

High Capital & Maintenance Cost of Advanced Devices

Cutting-edge lasers and energy-based platforms often exceed USD 100,000, and quarterly maintenance contracts add recurring overhead. Currency volatility inflates import costs, while limited rural technical support prolongs downtime. Backup-power investment has become non-negotiable: hospital chains estimate that generator-fuel spending rose 35% in 2025 alone.[3]Bonitas Medical Fund, “Load-Shedding and Healthcare Equipment,” bonitas.co.za As a result, smaller practices gravitate to lower-cost non-energy modalities or refurbished systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Non-Energy Dominance Faces Technology Disruption

Non-energy-based products, led by botulinum toxin and dermal fillers, contributed 53.12% of the South Africa aesthetic devices market size in 2025 and remain the entry point for cost-conscious patients. Rapid-growing radio-frequency (RF) systems, however, are forecast to post a 16.58% CAGR as monopolar and bipolar platforms deliver visible tightening without incisions. AI-assisted ultrasound imaging is improving RF probe placement, elevating safety profiles. Portable diode lasers maintain popularity in mid-tier clinics because of versatile hair-removal and vascular-lesion settings. Top-end practices adopt hybrid RF-microneedling units that integrate depth-controlled needle cartridges, enhancing collagen remodeling while minimizing downtime. Emerging cryolipolysis and plasma-based resurfacing solutions find traction among patients seeking single-session body-sculpting or scar-revision options. SAHPRA’s impending device-registration regime could accelerate market consolidation by excluding substandard imports.

Energy-efficiency considerations shape capital-expenditure decisions; devices featuring sleep-mode and low-heat handpieces gain favor in load-shedding zones. Leasing models lower upfront cost barriers, allowing smaller clinics to trial premium lasers before full purchase. As competitive intensity rises, manufacturers bundle accreditation training and predictive-maintenance software, cementing brand loyalty. Secondary markets for refurbished lasers are expanding, offering entry-level providers a pathway into the South Africa aesthetic devices market without prohibitive capex.

By Application: Hair Removal Leadership Challenged by Body Contouring Innovation

Hair removal remained the highest-volume application, holding a 31.20% share of the South Africa aesthetic devices market in 2025, with diode and alexandrite lasers serving mixed-Fitzpatrick skin types effectively. Body contouring and cellulite-reduction technologies, nonetheless, are poised to deliver the fastest 14.92% CAGR, propelled by non-invasive fat-free and RF-based skin-tightening platforms that suit patients reluctant to undergo liposuction. Combination protocols using cryolipolysis followed by vibration-plate therapy shorten recovery and improve lymphatic drainage.

Skin-resurfacing demand rides on an aging yet professionally active population seeking subtle rejuvenation. Fractional CO₂ lasers and plasma-pen devices address post-inflammatory hyperpigmentation prevalent in darker skin tones, while pigment-safe 1064 nm lasers minimize risk of hypopigmentation. Acne-scar management deploys a multi-modality approach microneedling RF plus platelet-rich plasma to maximize collagen induction. Tattoo-removal volumes rise as workplace-appearance standards tighten, supporting investment in pico-second lasers with lower aberration risk.

By End User: Hospital Infrastructure Advantage Versus Clinic Specialization

Public and private hospitals retained 41.05% of the South Africa aesthetic devices market share in 2025 thanks to extensive infrastructure, higher bed capacity, and better emergency-support capabilities. Their embedded generator systems mitigate load-shedding downtime, safeguarding device longevity. Nevertheless, specialty aesthetic clinics are projected to surge at a 13.85% CAGR as physician-entrepreneurs capitalize on focused branding and premium service models. Clinics emphasize same-day protocols, private recovery pods, and membership-based loyalty schemes.

Other end users, including dermatology practices and medical spas, carve out niches through personalized skin-health programs that combine aesthetic and therapeutic interventions. Public-private joint ventures under the National Health Insurance roadmap open new geographic pockets by equipping regional hospitals with mid-tier laser equipment. Workforce-development grants subsidize nurse-aesthetician upskilling, improving device-utilization rates in semi-urban settings.

Geography Analysis

Johannesburg, Cape Town, and Durban anchor the South Africa aesthetic devices market, accounting for a combined majority of installed laser and RF capital due to higher disposable incomes and dense private-clinic networks. Gauteng province alone houses more than half of the country’s board-certified plastic surgeons, creating a robust referral pipeline. Cape Town attracts a disproportionate share of international “surgery-safari” patients seeking post-operative recuperation in coastal resorts, reinforcing local demand for high-end energy-based systems. Durban’s multicultural demographic accelerates adoption of pigment-safe lasers tailored for Fitzpatrick IV–VI skin.

Rural provinces such as Limpopo and the Eastern Cape witness growing but latent demand. Distance-decay studies confirm that patient utilization declines sharply beyond 15 km from specialist centers, underscoring tele-consultation’s role in bridging access gaps. Infrastructure-upgrade grants under National Health Insurance target secondary hospitals for refurbishment, including stable power and high-speed broadband—prerequisites for device uptime and remote-calibration services. Nonetheless, persistent poverty levels and limited credit access constrain uptake of multi-session treatments.

Power-supply reliability remains the key geographical differentiator. Clinics in Eskom’s high-risk load-shedding zones report 20% higher maintenance expenditure to protect sensitive optics. By contrast, facilities in the Western Cape leverage municipal energy-resilience plans, enabling longer operating hours and higher procedural throughput. SAHPRA maintains uniform regulatory standards across provinces, yet enforcement resources vary, leaving rural clinics more vulnerable to counterfeit consumables.

Regional medical-tourism flows further tilt market gravity toward urban hubs. Direct international flights into OR Tambo and Cape Town International Airports shorten patient itineraries, while accredited recuperation villas cluster around Table Mountain and Sandton. Provincial marketing agencies now position aesthetic wellness packages alongside wine-route tours, adding non-clinical revenue streams that subsidize advanced equipment purchases.

Competitive Landscape

International manufacturers dominate premium energy-based segments, while local distributors compete on service responsiveness and flexible financing. Brands such as Allergan, Galderma, and Candela maintain top-of-mind status through continuous-education workshops, yet emerging Korean and Israeli vendors chip away with price-competitive RF-microneedling and pico-second platforms. Mid-tier clinics prize total cost of ownership above sticker price, scrutinizing consumable pricing and warranty length.

Service ecosystems differentiate winners in the South Africa aesthetic devices market. Vendors offering 24-hour technical hotlines, remote diagnostics, and loaner units minimize revenue-loss risk during downtime. Device-agnostic maintenance companies are also gaining ground, offering multi-brand service packages attractive to mixed-fleet facilities. Consolidation appears imminent: SAHPRA’s stricter registration regime raises compliance costs, likely nudging smaller importers toward mergers or exit.

Localized innovation centers around energy-efficiency. One Cape Town distributor retrofits RF platforms with smart-power modules that cut consumption by 18%. Several Johannesburg clinics pilot AI-driven predictive-maintenance dashboards that trigger spare-part orders before breakdowns. The competitive arena is not solely device focused; patient-experience enhancements digital appointment scheduling, virtual reality pain distraction become decisive tie-breakers.

South Africa Aesthetic Devices Industry Leaders

Alma Lasers

Galderma

Venus Concept

Abbvie (Allergan Inc.)

Sciton Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: LG Chem divested its aesthetics unit to VIG Partners for USD 144 million, reshaping hyaluronic-acid filler supply dynamics and opening share-gain avenues for remaining vendors.

- April 2024: SAHPRA launched a feasibility study on mandatory aesthetic-device registration, signposting stricter market-entry standards.

South Africa Aesthetic Devices Market Report Scope

As per the scope of the report, aesthetic devices refer to all medical devices used for various cosmetic procedures, including plastic surgery, unwanted hair removal, excess fat removal, anti-aging, aesthetic implants, and skin tightening. The Aesthetic Medicine South Africa Market Report is Segmented by Type of Devices (Energy-based Aesthetic Devices and Non-energy-based Aesthetic Devices), Application (Skin Resurfacing and Tightening, Hair Removal and Tattoo Removal, Facial Aesthetic Procedures, and Other Applications), and End User (Hospitals, Clinics, and Home Settings). The report offers the value (in USD million) for the above segments.

By Device Type

| Energy-based Devices | Laser-based |

| Light-based (IPL) | |

| Radio-frequency-based | |

| Ultrasound-based | |

| Cryolipolysis & Plasma-based | |

| Non-energy-based Devices | Botulinum Toxin |

| Dermal Fillers & Threads | |

| Chemical Peels | |

| Microdermabrasion | |

| Implants | |

| Mesotherapy & Others |

By Application

| Skin Resurfacing & Tightening |

| Body Contouring & Cellulite Reduction |

| Hair Removal |

| Tattoo & Pigmentation Removal |

| Breast Augmentation |

| Acne & Scar Treatment |

| Other Applications |

By End User

| Public & Private Hospitals |

| Specialty Aesthetic Clinics |

| Other End Users |

| By Device Type | Energy-based Devices | Laser-based |

| Light-based (IPL) | ||

| Radio-frequency-based | ||

| Ultrasound-based | ||

| Cryolipolysis & Plasma-based | ||

| Non-energy-based Devices | Botulinum Toxin | |

| Dermal Fillers & Threads | ||

| Chemical Peels | ||

| Microdermabrasion | ||

| Implants | ||

| Mesotherapy & Others | ||

| By Application | Skin Resurfacing & Tightening | |

| Body Contouring & Cellulite Reduction | ||

| Hair Removal | ||

| Tattoo & Pigmentation Removal | ||

| Breast Augmentation | ||

| Acne & Scar Treatment | ||

| Other Applications | ||

| By End User | Public & Private Hospitals | |

| Specialty Aesthetic Clinics | ||

| Other End Users | ||

Key Questions Answered in the Report

How fast is the South Africa aesthetic devices market expected to grow to 2031?

It is projected to advance at a 13.22% CAGR, moving from USD 211.21 million in 2026 to USD 393.17 million in 2031.

Which device category leads current sales?

Non-energy-based injectables and fillers hold 53.12% of 2025 revenue.

What is the fastest-growing application?

Body contouring and cellulite reduction is forecast to grow at a 14.92% CAGR through 2031.

Why are specialty clinics expanding faster than hospitals?

Focused branding, premium patient experiences, and lower fixed-asset intensity drive a forecast 13.85% CAGR for clinics.

Page last updated on: