Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

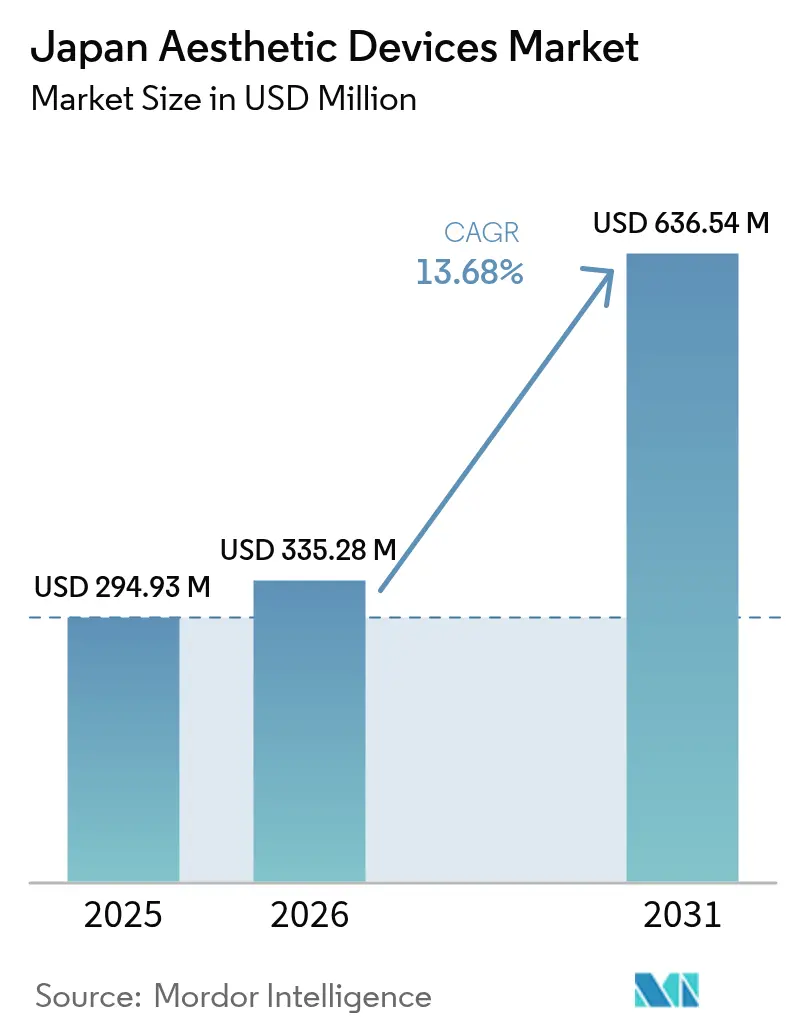

| Base Year Market Size (2025) | USD 294.93 Million |

| Market Size (2026) | USD 335.28 Million |

| Market Size (2031) | USD 636.54 Million |

| Growth Rate (2026 - 2031) | 13.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Aesthetic Devices Market Analysis by Mordor Intelligence

The Japan Aesthetic Devices market size is expected to grow from USD 294.93 million in 2025 to USD 335.28 million in 2026 and is forecast to reach USD 636.54 million by 2031 at 13.68% CAGR over 2026-2031.

Rising discretionary spending among older consumers, faster regulatory approvals for artificial-intelligence (AI) enabled hardware, and a clear shift toward minimally invasive energy-based platforms underpin this trajectory. The Japan aesthetic devices market also benefits from domestic loyalty: 65% of consumers who once traveled overseas now choose local providers for safety and convenience. Tight PFAS regulations that take effect in 2025 raise material compliance costs, yet companies that align early gain a competitive edge. Continuous technology convergence particularly radiofrequency (RF) systems that pair with LED and electrical-muscle-stimulation (EMS) modules expands treatment versatility and clinic revenue per device.

Key Report Takeaways

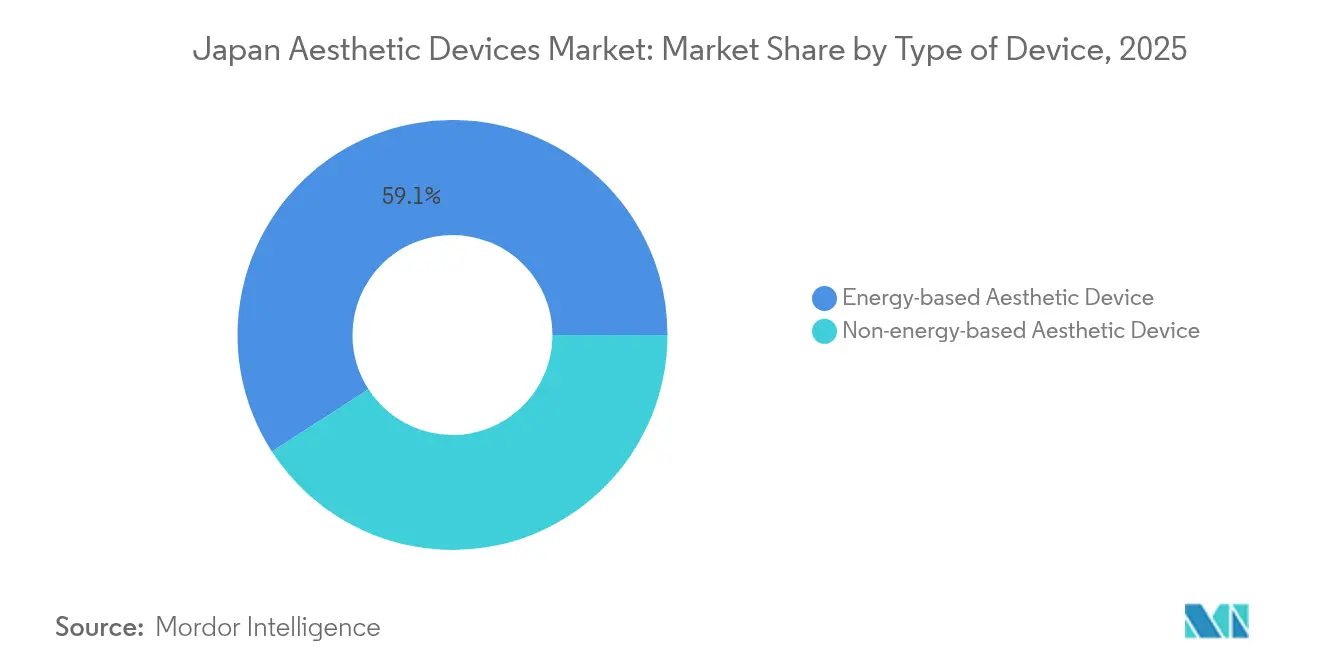

- By type of device, energy-based platforms led with 59.12% of Japan aesthetic devices market share in 2025, while RF-based systems posted the fastest 17.85% CAGR through 2031.

- By application, skin resurfacing and tightening accounted for 31.74% of the Japan aesthetic devices market size in 2025; body-contouring procedures are projected to accelerate at a 16.27% CAGR between 2026 and 2031.

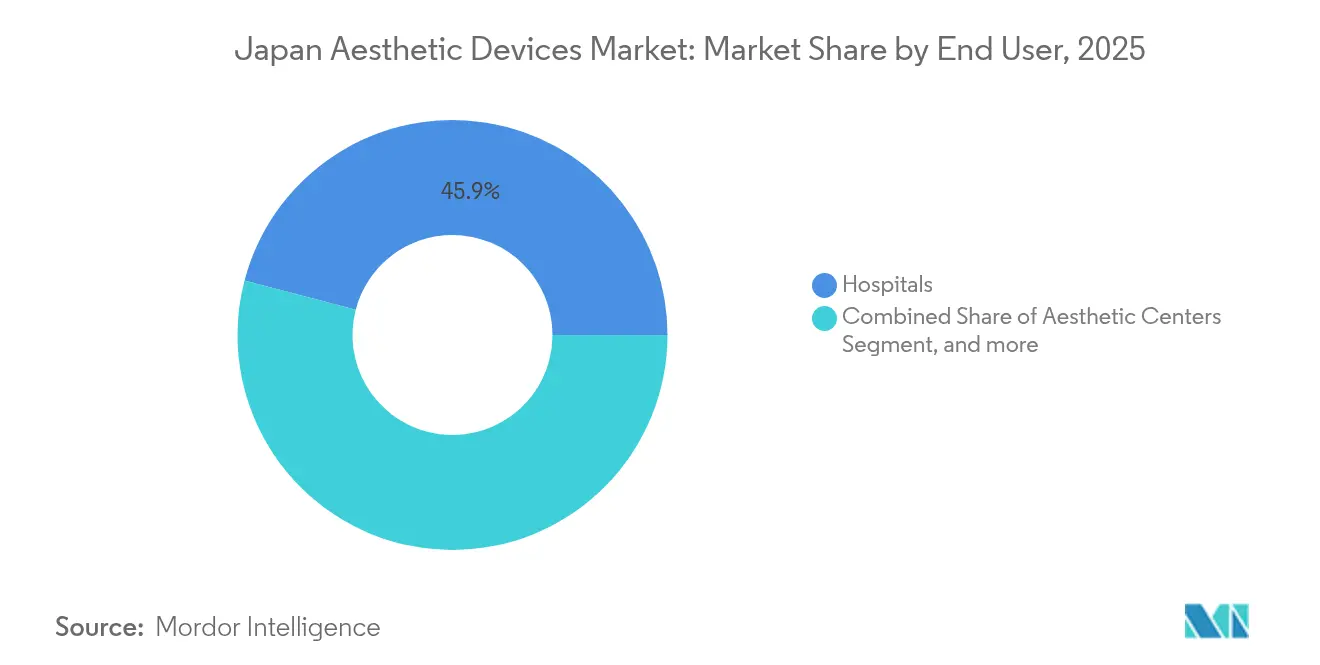

- By end user, hospitals commanded 45.92% revenue share in 2025, whereas aesthetic centers are set to expand at a 18.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population Driving Anti-Aging Demand | +3.2% | National, with concentration in Tokyo, Osaka, Nagoya metropolitan areas | Long term (≥ 4 years) |

| Rising Adoption of Minimally & Non-Invasive Devices | +2.8% | National, with higher penetration in urban centers | Medium term (2-4 years) |

| Technological Breakthroughs in Energy-Based Platforms | +2.1% | Global influence with Japan-specific adaptations | Medium term (2-4 years) |

| Tele-Aesthetic Platforms & Home-Use Device Ecosystem | +1.9% | National, with rural area emphasis | Short term (≤ 2 years) |

| PMDA Fast-Track for AI-Assisted Aesthetic Devices | +1.4% | National regulatory framework | Medium term (2-4 years) |

| Medical-Stay Visa Spurring Inbound Aesthetic Tourism | +1.1% | Major cities with international airports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population Driving Anti-Aging Demand

Japan’s super-aged demographic structure intensifies demand for rejuvenation treatments, and anti-aging spending is projected to exceed USD 3 billion annually by 2028.[1]“Japan Becomes Super-Aged Society,” Nature, nature.com The worker-to-senior ratio falls to 2.4:1 by 2025, concentrating purchasing power among older adults who readily pay for premium procedures. Companies funnel R&D budgets into senolytic-based equipment that targets cellular senescence, positioning the Japan aesthetic devices market as a proving ground for longevity-oriented devices. Male participation rises: men in their 40s represent 31% of aesthetic patients seeking laser hair removal and skin maintenance. As research pivots from appearance to health-span extension, device makers partner with pharmaceutical firms to co-develop platforms that marry cosmetic and preventive benefits.

Rising Adoption of Minimally & Non-Invasive Devices

More than 80% of potential patients now prioritize safety and downtime over cost when choosing procedures, and home-use gadgets already reside in 16% of households. The best-selling domestic brands combine RF, EMS, and LED in palm-sized tools that mirror clinic-grade efficacy. Clinical evidence backs the shift: monopolar RF boosts dermal elasticity with no adverse events in controlled trials.[2]S. Lee et al., “Monopolar RF Improves Skin Elasticity,” MDPI, mdpi.com Updated PMDA quality-management-system guidelines that harmonize with ISO 13485:2016 reduce red-tape hurdles for incremental device upgrades, allowing manufacturers to refresh popular models annually without re-inventing the approval wheel.

Technological Breakthroughs in Energy-Based Platforms

Next-generation RF applicators deploy AI algorithms to modulate thermal output in milliseconds, improving predictability across diverse skin phototypes. Lumenis’s OptiLIFT platform realized a 75% reduction in lid laxity during peer-reviewed trials. Academic engineers now prototype metamaterial waveguide antennas that elevate tissue temperature 35.4°C at 80 W, expanding noninvasive body-sculpting options.[3]L. Wang et al., “Metamaterial RF Antenna for Skin Tightening,” Frontiers in Bioengineering and Biotechnology, frontiersin.orgInMode Japan secured class-II certification for its Optimus Lumecca xenon-light system, signaling regulator confidence in multi-modal chassis. Such advances sustain the premium that energy-based hardware commands in the Japan aesthetic devices market.

Tele-Aesthetic Platforms & Home-Use Device Ecosystem

Physician shortages outside major metros motivate providers to embed video-consult modules and remote-parameter-locking software directly inside device firmware. V-Cube targets 500 tele-consultation booths nationwide by 2026, creating a physical anchor for follow-up visits in shopping malls and rail stations. Subscription-model e-commerce portals ship treatment-specific consumables on auto-replenishment cycles, improving compliance and post-procedure outcomes. Celebrity endorsements push LED masks priced at JPY 55,000 (USD 371) into mainstream retail. These digital bridges widen the Tamagotchi-like “care loop” that bonds user, clinician, and device, helping the Japan aesthetic devices market reach rural and time-poor demographics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Safety Rules & Limited Reimbursement | -2.1% | National regulatory framework | Long term (≥ 4 years) |

| High Capex / Opex for Smaller Clinics | -1.8% | Regional, affecting rural and suburban markets | Medium term (2-4 years) |

| Dermatologist Shortages Outside Metro Areas | -1.4% | Rural and suburban regions, excluding Tokyo-Osaka corridor | Medium term (2-4 years) |

| Sustainability Scrutiny on Single-Use Consumables | -1.1% | National, with stricter enforcement in metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Safety Rules & Limited Reimbursement

Mandatory PFAS tracking from January 2025 forces manufacturers to audit supply chains and re-engineer coatings, elevating bill-of-materials cost. Reimbursement schedules exclude elective aesthetics, so patients self-finance, dampening uptake among price-sensitive groups. PMDA reviews, though faster than a decade ago, still lag the United States, extending lead times for global releases. Every five years, companies must renew quality-system approval, adding paperwork heft.

High Capex / Opex for Smaller Clinics

Top-tier lasers list between JPY 10–50 million (USD 67,000–333,000), not counting disposables or annual service contracts. Staffing costs climb as aesthetic nurses job-hop to metropolitan chains offering better pay, leaving rural facilities understaffed and unprofitable. A record 126 dental clinics declared bankruptcy in 2024, illustrating the structural fragility of small, procedure-based practices. Without financing support, independent operators defer upgrades, widening the technology gap that ultimately limits the Japan aesthetic devices market’s geographic penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Device: Energy-Based Dominance Drives Innovation

Energy-based equipment owns 59.12% of Japan aesthetic devices market share in 2025, and RF-centric units deliver an 17.85% CAGR through 2031. Shiseido’s Quick Facial Trainer exemplifies next-step integration, layering EMS over interference-waveforms to stimulate deep musculature while minimizing epidermal irritation. Laser arrays still command premium prices; Shirono Clinic installed the Stella M22 platform with six swappable filters for dermatologist-tailored pigmentation sessions. Ultrasound-RF hybrids reduced average waist circumference by 3.83 cm in randomized trials.

Non-energy devices, syringe-based fillers, and neurotoxins retain physician loyalty for wrinkle relaxation, yet lack the cross-selling potential of smart console systems. PMDA’s flexible quality-management updates accelerate roll-outs of firmware-driven feature sets, giving energy-device makers an innovation flywheel. As AI analytics gain traction, console dashboards will push outcome data to cloud portals, allowing vendors to upsell algorithm subscriptions, reinforcing long-term revenue capture inside the Japanese aesthetic devices market.

By Application: Body Contouring Emerges as Growth Leader

Skin resurfacing and tightening contributed 31.74% to Japan aesthetic devices market size in 2025, but body-contouring procedures capitalizing on non-invasive RF and ultrasound are rising at 16.27% CAGR to 2031. Controlled studies confirm combined-energy treatments melt adipose layers while sparing dermal structures, meeting patient demand for subtle silhouette refinement without downtime. Facial rejuvenation remains steady; clinics now tout painless, needle-free plasma delivery that penetrates 6.5 mm, deepening collagen remodeling.

Consumer curiosity widens to intimate wellness, where vaginal-laser platforms like Timewalker II Intima address functional and aesthetic outcomes. Hair-removal units migrate from clinic to living room, riding the 16% household penetration of home IPL devices, and feeding a pre-procedure “try-before-clinic” funnel that ultimately lifts professional bookings. Overall, multi-application workstations that toggle between face, body, and specialty probes dominate purchasing decisions in the Japan aesthetic devices market.

By End User: Aesthetic Centers Accelerate Market Transformation

Hospitals held a 45.92% slice of revenue in 2025, leveraging surgical-backup credibility. Yet specialized aesthetic centers, scaling at 18.92% CAGR, outpace broader medical facilities by offering concierge-style experience and rapid device turnover. Chains such as SBC Medical Group extended footprints to Hiratsuka and Kobe, adapting Korean hybrid protocols for Japanese skin phenotypes.

Home settings register outsized buzz thanks to LED masks and microcurrent rollers that mimick clinic outputs. Subscription models for consumables cement recurring revenue, letting manufacturers harvest data on usage patterns that inform next-gen design. Workforce-training alliances, like the Japan Aesthetic Medical Society summer school, funnel new graduates into boutique centers, reinforcing a staffing ecosystem that propels the Japan aesthetic devices market into decentralized care modalities.

Geography Analysis

Tokyo, Osaka, and Nagoya anchor spend, fueled by dense clinic networks and affluent, beauty-savvy clients. Ginza alone houses dozens of flagship laser suites that cater to inbound Chinese visitors seeking stem-cell facelifts. Secondary cities gain traction through chain expansion; SBC’s Hiratsuka branch, Kanagawa’s first, captures suburban commuters who once traveled to Shonan or Yokohama. Teleconsult booths roll out across rail hubs, letting rural residents receive pre-screening, then travel for single-day treatments, smoothing regional demand curves.

Demographic reality older populations in countryside prefectures boosts the utility of at-home solutions where clinics shutter from physician retirements. V-Cube’s tele-clinic pods bridge gaps by enabling virtual follow-ups tied to mail-order consumables. Local governments court growth via tax incentives for clinic startups; Osaka leverages the 2025 Expo as a showcase for AI skincare kiosks developed by Momotani Juntenkan and university researchers.

Uniform PMDA oversight means product labeling and adverse-event reporting remain consistent nationwide, though prefectural reimbursement pilot schemes for postoperative pain relief devices create patchwork adoption speeds. Ultimately, hub-and-spoke provider models, plus robust e-commerce fulfilment, ensure the Japan aesthetic devices market reaches both cosmopolitan and remote populations across its archipelago.

Competitive Landscape

Consolidation accelerates: Hahn & Company merged Cynosure and Lutronic in April 2024, forming Cynosure Lutronic Inc. and instantly commanding a broad laser portfolio. Incumbents respond by bundling hardware sales with cloud analytics that optimize pulse-width presets per clinic. InMode, armed with Optimus Lumecca’s thermal-therapy certification, leverages cross-selling into vascular-lesion practices. Domestic conglomerates such as Shiseido incubate device lines that complement topical skincare, fostering closed-loop ecosystems that multiply customer lifetime value.

Start-ups compete via direct-to-consumer LED and microcurrent hardware, with some surpassing 350,000 unit sales in under two years. These entrants often partner with pop culture icons, bypassing clinical channels to seed brand equity. However, PMDA class-II pathways impose manufacturing-site audits, filtering out under-capitalized newcomers. Strategic R&D alliances proliferate: optical-component makers team with AI software firms to co-develop predictive-maintenance dashboards, slashing device downtime for high-volume centers.

Japan Aesthetic Devices Industry Leaders

Bausch Health Companies Inc. (Solta Medical, Inc.)

Cutera Inc.

Venus Concept

Lumenis Ltd.

AbbVie (Allergan)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Gunze Medical debuted CAREVEAM, an ultraviolet platform cleared for psoriasis and vitiligo, combining South Korean optics with Japanese distribution channels.

- June 2025: InMode Japan received class-II certification for Optimus Lumecca xenon-light therapy, validated for increasing local blood flow and mitigating pain.

- February 2024: Rohto Pharmaceutical formed an equity partnership with Ireland’s EMMA Aesthetics to accelerate Europe-focused product innovation, signaling globalization of Japanese expertise

Japan Aesthetic Devices Market Report Scope

The scope of the aesthetic devices market refers to all medical devices used for various cosmetic procedures, including plastic surgery, unwanted hair removal, excess fat removal, anti-aging, and skin tightening, which are used for beautification correction and improvement of the body. Aesthetic procedures include both surgical and non-surgical procedures. The Japanese aesthetic devices market is segmented by type, application, and end user.

By Type of Device

| Energy-based Aesthetic Device | Laser-based Aesthetic Device |

| Radiofrequency-based Aesthetic Device | |

| Light-based Aesthetic Device | |

| Ultrasound Aesthetic Device | |

| Other Energy-based Aesthetic Devices | |

| Non-energy-based Aesthetic Device | Botulinum Toxin |

| Dermal Fillers & Threads | |

| Microdermabrasion | |

| Implants | |

| Other Non-energy-based Aesthetic Devices |

By Application

| Skin Resurfacing & Tightening |

| Body Contouring & Cellulite Reduction |

| Facial Aesthetic Procedures |

| Hair Removal |

| Breast Augmentation |

| Other Applications |

By End User

| Hospitals |

| Aesthetic Centers |

| Home Settings |

| By Type of Device | Energy-based Aesthetic Device | Laser-based Aesthetic Device |

| Radiofrequency-based Aesthetic Device | ||

| Light-based Aesthetic Device | ||

| Ultrasound Aesthetic Device | ||

| Other Energy-based Aesthetic Devices | ||

| Non-energy-based Aesthetic Device | Botulinum Toxin | |

| Dermal Fillers & Threads | ||

| Microdermabrasion | ||

| Implants | ||

| Other Non-energy-based Aesthetic Devices | ||

| By Application | Skin Resurfacing & Tightening | |

| Body Contouring & Cellulite Reduction | ||

| Facial Aesthetic Procedures | ||

| Hair Removal | ||

| Breast Augmentation | ||

| Other Applications | ||

| By End User | Hospitals | |

| Aesthetic Centers | ||

| Home Settings | ||

Key Questions Answered in the Report

How large is the Japan aesthetic devices market in 2026?

The Japan aesthetic devices market size is USD 335.28 million in 2026 and is forecast to grow at 13.68% CAGR through 2031.

Which device category holds the largest share?

Energy-based platforms dominate with 59.12% Japan aesthetic devices market share in 2025, led by RF-centric systems.

What is the fastest-growing application segment?

Body-contouring procedures, powered by combined ultrasound-RF technology, advance at a 16.27% CAGR from 2026 to 2031.

Where is demand the strongest geographically?

Tokyo, Osaka, and Nagoya metropolitan areas lead spending, though suburban and rural growth rises via tele-aesthetic platforms.

How do new PFAS regulations affect manufacturers?

Starting January 2025, device makers must audit and limit PFAS usage, increasing material costs but encouraging safer formulations.

What recent merger reshaped the competitive landscape?

Hahn & Company’s merger of Cynosure and Lutronic in 2024 created Cynosure Lutronic Inc., strengthening its laser technology portfolio.

Page last updated on: