In-Memory Database Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.05 Billion |

| Market Size (2031) | USD 15.31 Billion |

| Growth Rate (2026 - 2031) | 13.72% CAGR |

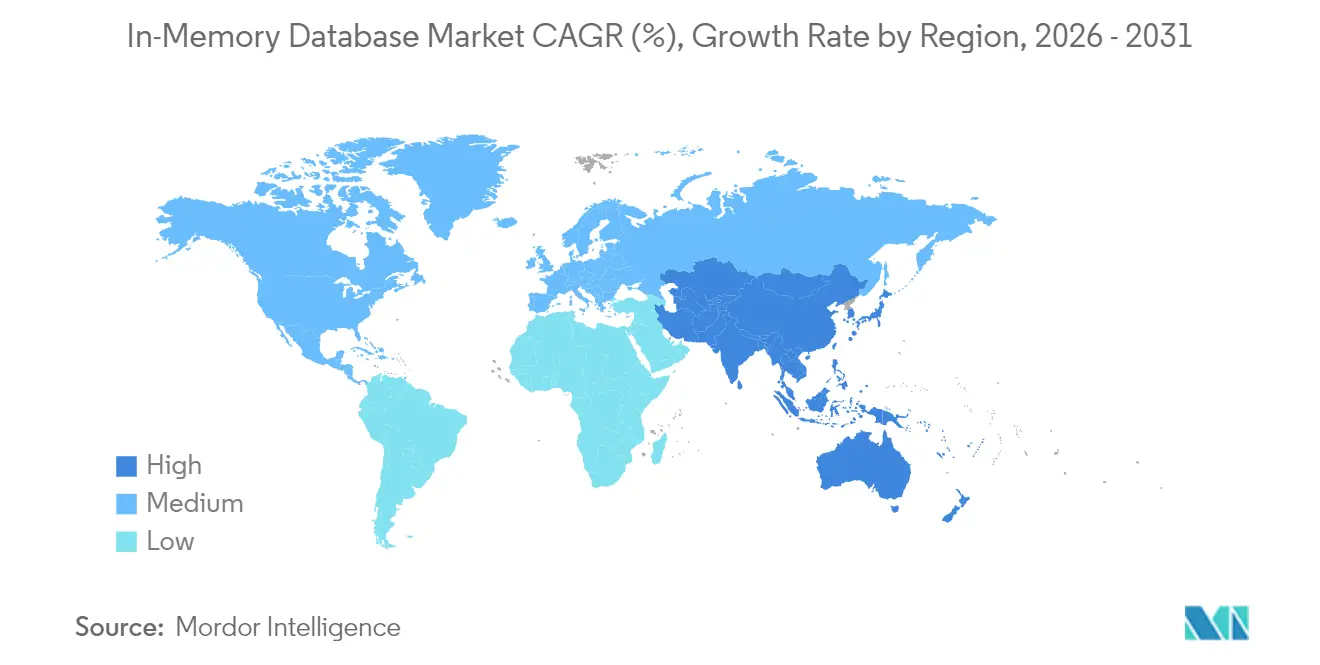

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

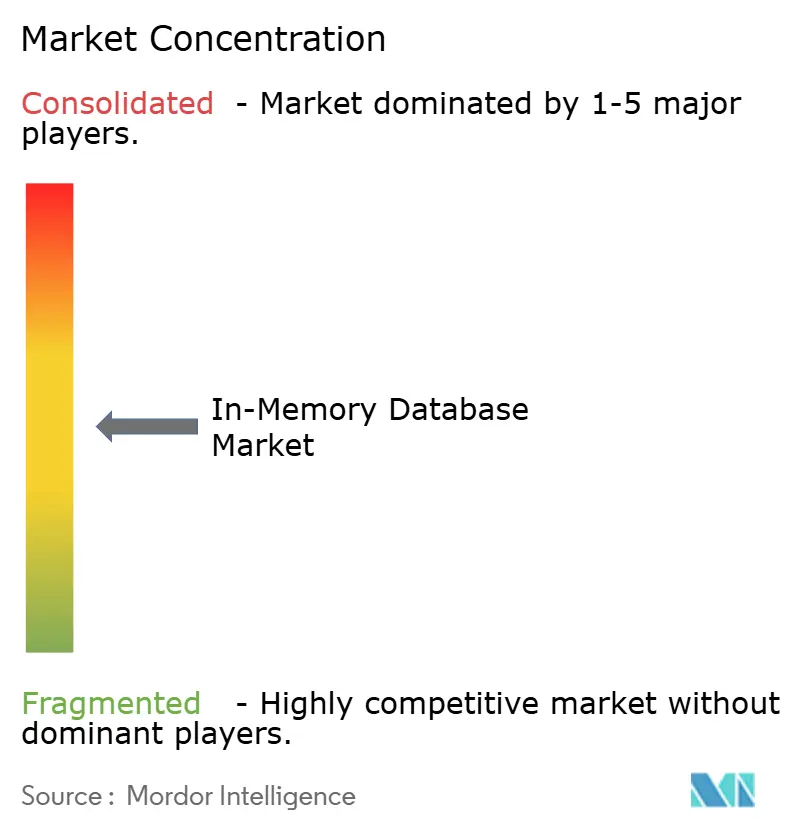

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In-Memory Database Market Analysis by Mordor Intelligence

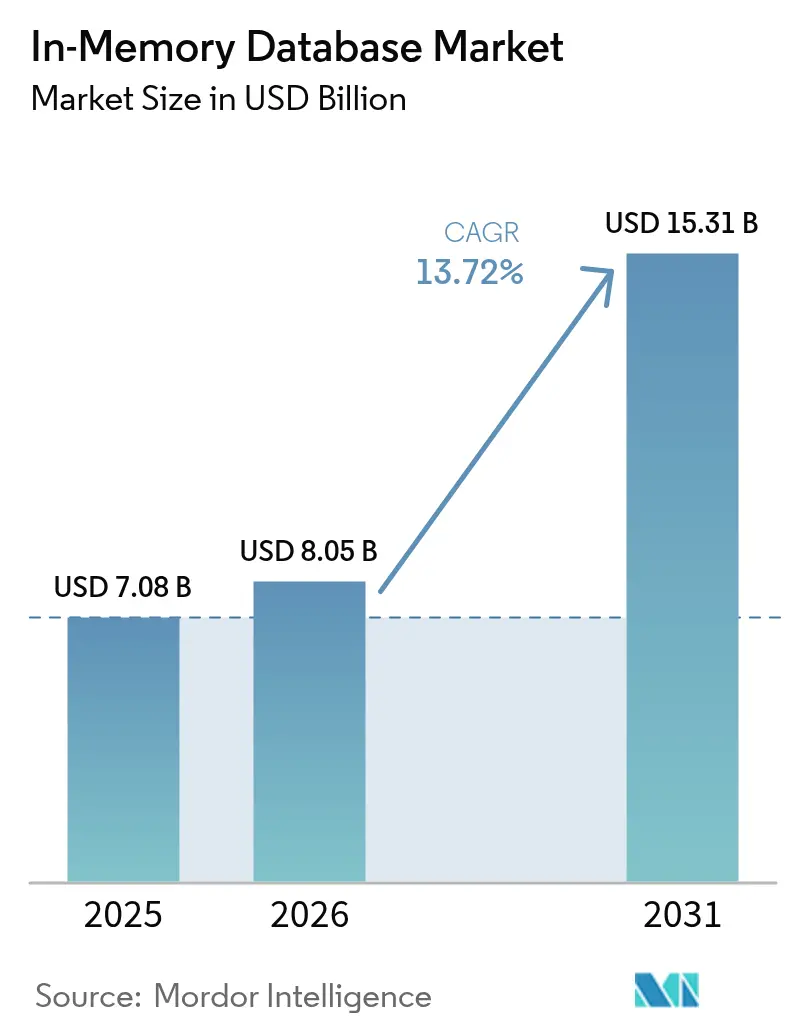

The In-Memory Database market size is expected to grow from USD 7.08 billion in 2025 to USD 8.05 billion in 2026 and is forecast to reach USD 15.31 billion by 2031 at 13.72% CAGR over 2026-2031. Sub-millisecond performance requirements from cloud-native microservices, AI inference engines, and streaming analytics platforms continued to push enterprises toward memory-centric architectures. Lower DRAM prices and the arrival of CXL-based persistent memory modules have reduced the total cost of ownership, encouraging more workloads to migrate from disk-backed systems. Edge deployments in connected vehicles and Industrial IoT plants further expanded demand because local processing avoids network latency penalties. Competitive dynamics remained fluid as traditional vendors deepened integrations with hyperscale clouds while open-source forks gained momentum, giving buyers new paths to avoid vendor lock-in.

Key Report Takeaways

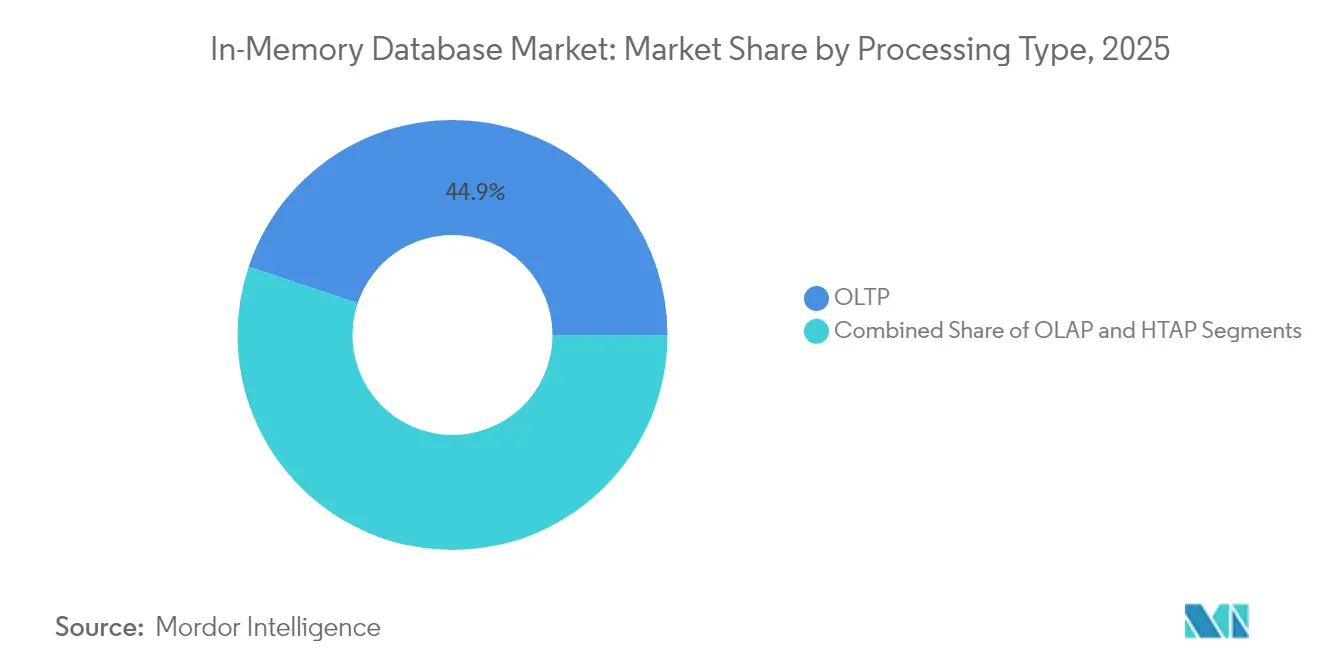

- By processing type, Online Transaction Processing (OLTP) led with 44.85% of the In-Memory Database market share in 2025, while Hybrid Transactional/Analytical Processing (HTAP) is projected to grow at a 20.68% CAGR to 2031.

- By deployment mode, on-premise installations retained 55.15% revenue share in 2025; edge and embedded deployments are forecast to expand at a 22.55% CAGR through 2031.

- By data model, relational SQL captured a 59.95% share in 2025, whereas multi-model platforms are set to post a 19.6% CAGR between 2026 and 2031.

- By organization size, large enterprises held 70.15% share of the In-Memory Database market size in 2025; small and medium enterprises will register the fastest 17.7% CAGR to 2031.

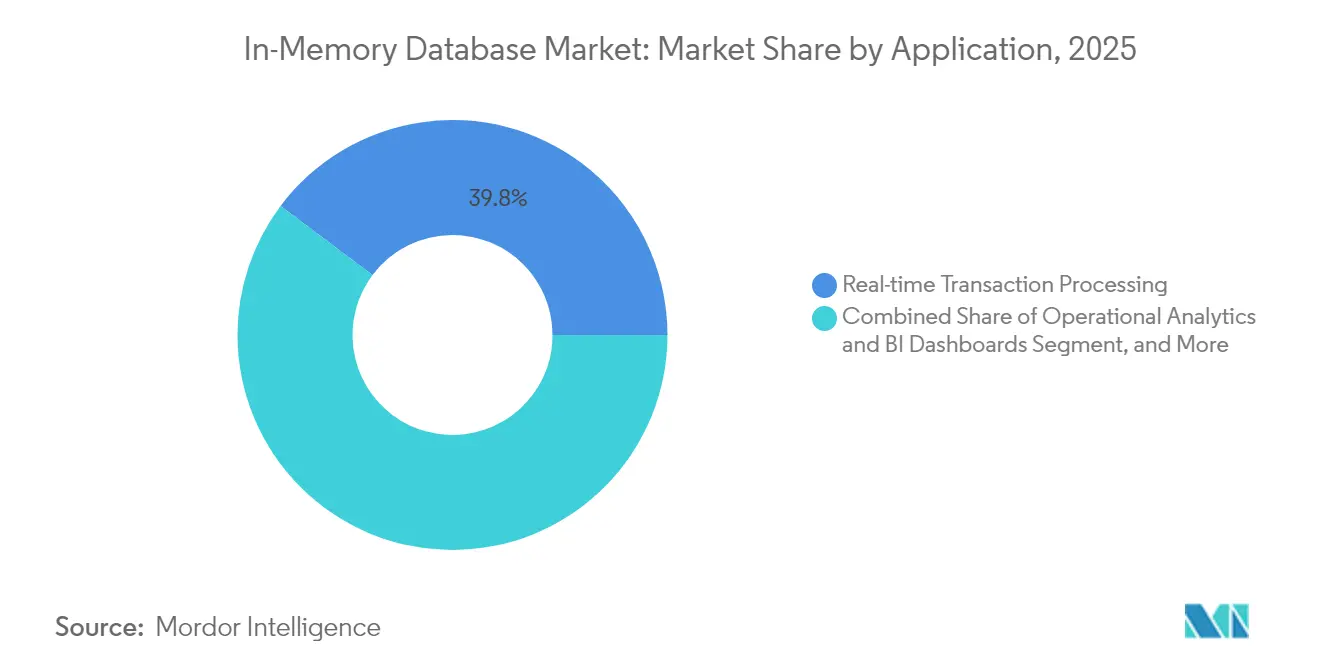

- By application, real-time transaction processing accounted for 39.75% of the In-Memory Database market size in 2025, while AI/ML model serving is forecast to expand at a 23.1% CAGR through 2031.

- By end-user industry, BFSI dominated with 27.95% revenue share in 2025; healthcare and life sciences are poised for an 17.4% CAGR through 2031.

- By geography, Asia-Pacific commanded 31.95% of global revenue in 2025 and remains the fastest-growing region at 16.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global In-Memory Database Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native micro-services demanding sub-millisecond latency | +3.2% | Global, with a concentration in North America and EU | Short term (≤ 2 years) |

| Falling DRAM and persistent-memory USD/GB widening TCO gap vs. disk | +2.8% | Global, early adoption in APAC manufacturing hubs | Medium term (2-4 years) |

| Streaming analytics adoption in BFSI and telecom for fraud and network QoS | +2.1% | North America and EU financial centers, APAC telecom infrastructure | Short term (≤ 2 years) |

| HTAP architectures accelerating AI/ML model-serving in healthcare | +1.9% | Global, with regulatory-driven adoption in EU and North America | Medium term (2-4 years) |

| Edge-compute use-cases (connected vehicles, IIoT) requiring embedded IMDB | +2.4% | APAC manufacturing, North America automotive corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Microservices Demanding Sub-Millisecond Latency

Cloud-native adoption reshaped performance baselines as containerized microservices needed data access in microseconds. Session stores, personalization engines, and high-frequency trading platforms shifted from disk-backed databases to memory-centric stores because every millisecond of delay reduced conversion rates or trading profit. Dragonfly demonstrated 6.43 million operations per second on AWS Graviton3E silicon, highlighting the ceiling now expected from database tiers.[1]DragonflyDB, “2024 New Year, New Number,” dragonflydb.io Financial institutions and digital commerce operators that migrated monoliths to distributed systems saw response-time improvements translate into tangible revenue gains, reinforcing the driver’s near-term importance.

Falling DRAM and Persistent Memory Costs Widening TCO Gap

Global spot pricing of DDR4 and DDR5 modules continued to slide, while Samsung’s CXL Memory Module Hybrid prototype showed DRAM-class latency with persistence, creating a compelling cost profile. Hyperscale operators pooled memory across racks, reducing stranded capacity and backup cycles. Enterprises pivoted roadmaps toward in-memory deployment because the premium over SSD arrays narrowed, especially for analytics workloads with tight SLA windows. The effect is visible in Asia-Pacific manufacturing hubs where large historian datasets are moved into memory for real-time digital-twin analytics.

Streaming Analytics Adoption in BFSI and Telecom

Banks deployed streaming fraud-detection systems that processed millions of card authorizations per second using Aerospike’s in-memory engine. Telecom operators rolling out 5G monitored radio-access-network logs in real-time to maintain quality of service, leveraging vector searches on MongoDB to flag anomalies. Regulation in North America and Europe required real-time suspicious-activity reporting, pushing the driver’s adoption curve steeply upward.

HTAP Architectures Accelerating AI/ML Model Serving

Hybrid Transactional/Analytical Processing removed ETL delays by unifying writes and analytics in the same memory pool. Oracle embedded large language models inside HeatWave GenAI so patient records could be queried and scored for clinical decisions without data movement. Healthcare providers adopted HTAP stores to serve predictions during consultations, improving outcomes and lowering infrastructure overhead, which underpinned sustained medium-term growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vendor lock-in concerns around proprietary in-memory formats | -1.8% | Global, particularly affecting multi-cloud enterprises | Short term (≤ 2 years) |

| High-availability design complexity for >40 TB clusters | -1.2% | Enterprise deployments in North America & EU | Medium term (2-4 years) |

| Data-sovereignty laws (e.g., China CSL, EU GDPR) limiting global replication | -0.9% | EU, China, with spillover to multinational deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vendor Lock-in Concerns Around Proprietary Formats

Redis’s license change in 2024 heightened buyer wariness of proprietary formats, spurring AWS, Google, and Oracle to back the Valkey fork under the Linux Foundation. Enterprises budgeting multi-year database projects factored in exit costs, slowing purchase cycles. To mitigate risk, some adopted multi-database orchestration layers, but those abstractions introduced latency penalties that partially offset memory-speed gains.

High-Availability Design Complexity for Large Clusters

Clusters larger than 40 TB encountered protocol overhead that degraded replica-sync times. Redis Cluster’s gossip approach scaled quadratically, whereas Dragonfly’s alternative orchestration improved but still required intricate monitoring scripts. Financial-services workloads demanding five-nines uptime hesitated to migrate the biggest datasets fully into memory, opting for hybrid tiers that diluted peak performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Processing Type: HTAP Emerges as Unified Architecture

The OLTP segment held 44.85% of the In-Memory Database market share in 2025, underscoring continued reliance on high-integrity transactional workloads across banking, e-commerce, and ERP systems. Demand persisted because mission-critical records still required ACID compliance, with enterprises paying a performance premium for sub-millisecond commits. OLAP deployments addressed established business-intelligence front ends but grew slowly as analytics shifted toward more flexible engines.

HTAP climbed with a 20.68% CAGR forecast from 2026 to 2031 as firms sought single-platform simplicity. GridGain’s platform showed up to 1,000× speed-ups over disk-based systems while retaining ANSI SQL-99 support. Real-time risk calculations and supply-chain twins needed simultaneous read-write access, making HTAP the preferred architecture. The convergence unlocked incremental budget from departments earlier siloed between operations and analytics, pushing the In-Memory Database market toward unified designs.

By Deployment Mode: Edge Computing Drives Embedded Growth

On-premise installations captured 55.15% of 2025 revenue because regulated sectors required full control over data residency and tailored HA architectures. Legacy enterprise software stacks tightly integrated with on-premise databases, anchoring spending even as public clouds mature. Cloud deployments, nonetheless, have advanced as digital-native firms adopted managed services to avoid infrastructure administration.

Edge and embedded deployments displayed a 22.55% CAGR outlook, fueled by connected cars and IIoT gateways. Modern vehicles generate around 300 TB annually, which demands in-vehicle processing for autonomous features. TDengine achieved 10× compression over Elasticsearch in smart-vehicle telemetry, cutting bandwidth for upstream transfers. Manufacturers applied similar strategies on production lines to detect defects instantly. The shift signaled that performance gains once reserved for data centers were now indispensable at the edge, expanding the In-Memory Database market footprint.

By Data Model: Multi-Model Architectures Gain Traction

Relational SQL engines retained 59.95% revenue in 2025 because decades of application code and developer skills remained tied to the model. Corporations hesitated to rewrite core systems, preserving relational primacy even as new use cases emerged. NoSQL categories—key-value, document, graph—addressed flexible schemas but served narrower workloads.

Multi-model platforms forecast a 19.6% CAGR as AI workloads demand unified storage for structured records, vectors, and unstructured text. Hazelcast added vector search alongside traditional key-value APIs. Consolidating varied data types into a single memory pool lowered operational complexity and latency, enabling conversational AI, fraud graphs, and recommendation pipelines. This momentum is expected to expand the In-Memory Database market across heterogeneous data landscapes.

By Organization Size: SMEs Accelerate Cloud Adoption

Large enterprises accounted for 70.15% revenue in 2025 due to the capital intensity of petabyte-scale deployments and stringent SLA demands. Global banks, telecom carriers, and aerospace firms invested in redundant clusters with terabytes of DRAM to uphold business continuity. Their budgetary capacity shielded them from high per-gigabyte costs.

Small and medium enterprises are projected to rise at an 17.7% CAGR through managed services. AWS introduced Aurora DSQL to combine distributed SQL semantics with in-memory-style performance. By offloading scaling and patching to cloud vendors, startups accessed enterprise-grade latency for micro-SaaS products without headcount overhead. ElastiCache’s Valkey support lowered licensing expenses, accelerating the democratization of the In-Memory Database market among budget-constrained firms.

By Application: AI/ML Model Serving Drives Innovation

Real-time transaction processing kept the largest slice at 39.75% in 2025, with stock trading, payment gateways, and inventory systems reliant on instant commits. Operational analytics delivered dashboards for manufacturing and IT observability, but decelerated as newer AI use cases captured spending.

AI/ML model serving is forecast to expand at 23.1% CAGR as enterprises embed vector indexes and embeddings directly into databases for inference. Microsoft proposed Managed Retention Memory to reduce latency in large language model execution. The pattern integrates inference within the transactional layer, eliminating WAN hops between model servers and source data. Hybrid workloads that combine ACID updates with vector similarity searches are set to dominate the incremental In-Memory Database market revenue.

By End-User Industry: Healthcare Leads Digital Transformation

BFSI commanded 27.95% revenue in 2025, reflecting early adoption for high-frequency trading and fraud prevention. Regulatory mandates for real-time reporting and strict RTO requirements secured continued investment. Telecommunications applies in-memory analytics for network orchestration and customer-experience insights, sustaining a steady share.

Healthcare and life sciences show an 17.4% CAGR outlook. Corti released specialized AI infrastructure requiring immediate access to patient data for diagnostic support. Electronic health-record vendors integrated HTAP databases to feed clinical decision algorithms, improving care quality and operational efficiency. Manufacturing invested in predictive maintenance, and retail leveraged personalization engines, keeping the overall In-Memory Database industry diversified.

Geography Analysis

Asia-Pacific recorded the largest regional revenue at 31.95% in 2025 and maintained a 16.65% CAGR outlook. National Industry 4.0 programs in China, Japan, and India spurred factory automation that required in-memory historian databases for sub-second MES feedback loops. General Motors linked more than 100,000 operational technology connections in its MES 4.0 rollout, illustrating the scale of edge deployments. Local vendors such as Nautilus Technologies' advanced indigenous relational engines, reducing reliance on foreign IP.

North America formed a mature but innovation-rich market centered on financial services, hyperscale clouds, and autonomous-vehicle R&D. Oracle and Google deepened their partnership to run Oracle Database services natively on Google Cloud, marrying enterprise SQL capabilities with AI accelerators. The region’s venture funding supported emerging players such as Dragonfly, intensifying competitive churn.

Europe prioritized data-sovereignty compliance under GDPR, driving hybrid cloud adoption and favoring on-premise clusters combined with managed services in local data centers. Oracle expanded Database@Azure coverage to additional EU regions to satisfy residency rules. The continent also saw healthcare deployments of HTAP databases to power AI diagnostics under strict privacy frameworks.

The Middle East and Africa invested in smart-city fiber and 5G backbones, leading to pilot IIoT deployments that require real-time analytics. South America gained traction in mining operations and digital banking, where low-latency fraud detection justified premium memory-centric systems. Though absolute spend in these two regions remained modest, double-digit growth expanded the In-Memory Database market’s global diversity.

Regulatory Landscape

In-memory database adoption and deployment choices are shaped by cross-border semiconductor trade controls and AI governance rules that affect access to high-end compute and memory infrastructure used to run latency-sensitive database clusters. In January 2026, the US Department of Commerce, Bureau of Industry and Security (BIS) revised license review policy for advanced computing commodities exported to China, tightening compliance requirements for leading accelerators used in data center builds that commonly pair with memory-centric database tiers.

In Europe, regulation is increasingly tied to AI-driven workloads that use in-database vector search and HTAP to support model serving and real-time decisions. The EU Artificial Intelligence Act (Regulation (EU) 2024/1689), adopted in June 2024, established a harmonized framework for AI systems, reinforcing the need for strong data governance, auditability, and privacy controls in database architectures supporting regulated use cases, particularly in healthcare, BFSI, and public sector deployments.

Value Chain Analysis

The in-memory database value chain spans hardware and infrastructure inputs (DRAM, persistent memory, CPUs, networking such as RDMA-capable fabrics, and server platforms), platform software (proprietary and open-source in-memory engines, clustering, replication, and HTAP components), cloud and edge delivery models (managed database services, embedded runtimes, and orchestration layers), and application integration across BFSI, telecom, manufacturing/IIoT, retail, and healthcare. On-premise deployments remain anchored in regulated industries that require control over data residency and high-availability design, while hyperscalers and enterprise software vendors differentiate through managed offerings, native integrations with AI toolchains, and ecosystem connectors.

Upstream semiconductor constraints influence the economics of scaling memory-centric architectures, as supply tightness in high-end memory and advanced packaging affects server availability and cost per GB at the infrastructure layer. Industry commentary around late 2024 to 2025 flagged advanced packaging (for example, CoWoS-class capacity) and tightening HBM supply as bottlenecks for AI hardware, which in turn shapes enterprise refresh cycles for memory-dense systems that host in-memory databases. Downstream, implementation partners and systems integrators package reference architectures for SAP, Oracle, and cloud-native stacks, and buyers increasingly evaluate governance and licensing models (including Valkey fork momentum after Redis licensing changes) as part of long-term sourcing decisions.

Competitive Landscape

The In-Memory Database market remained moderately fragmented, with SAP, Oracle, Microsoft, and IBM leveraging broad enterprise suites to retain incumbency. Their roadmaps integrate in-database vector stores and ML accelerators, aligning with customer demands for unified platforms. Redis’s license shift prompted hyperscalers to endorse Valkey, illustrating how governance models can reshape competitive lines.

Specialist vendors such as Aerospike and Hazelcast competed on predictable, low-latency at scale and lower total cost per gigabyte. Aerospike’s success at PayPal proved the capacity to process real-time fraud signals on commodity hardware. Hazelcast released Platform 5.5 with extended connectors that simplified AI pipeline integrations.[4]Hazelcast, “Announcing Hazelcast Platform 5.5 Release,” hazelcast.com Dragonfly positioned itself as a drop-in replacement for Redis with superior single-core efficiency, challenging incumbents in the developer community.

Strategic alliances accelerated. Oracle’s April 2025 agreement with Google Cloud enabled enterprises to consolidate databases and AI toolchains without cross-cloud egress penalties. AWS formed an agentic AI group to tie model development more tightly to in-memory data services. Market entry barriers rose around ecosystem depth and integrated AI features, consolidating share among vendors that can field both transactional excellence and vector search natively.

In-Memory Database Industry Leaders

IBM Corporation

Microsoft Corporation

Oracle Corporation

SAP SE

TIBCO Software Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A whitespace is emerging at the intersection of AI-optimized infrastructure upgrades and database architectures that keep operational data, vectors, and streaming features close to compute. Recent infrastructure moves show how vendors are targeting larger memory footprints and lower contention for write-heavy workloads: in May 2026, HPE announced the HPE Compute Scale-up Server 3250 for in-memory database use cases, supporting up to 48 TB of memory, and in July 2026 Oracle introduced In-Memory Transaction Table and Commit Cache capabilities in Oracle AI Database 26ai on Exadata to accelerate transaction lookups and commit processing. These product updates align with enterprise patterns where model serving, fraud scoring, and real-time personalization run closer to the transactional system of record.

Supply-side investment in advanced memory and packaging also supports more cost-effective scaling of memory-centric stacks, particularly for HTAP and AI/ML model serving. In July 2026, SK Hynix disclosed a 100 trillion KRW investment plan in the Chungcheong region that includes advanced packaging (P&T7) and a new NAND facility (M17), and Samsung Electronics and SK Hynix communicated a broader, government-supported plan around a large-scale chipmaking hub in South Korea. For in-memory database vendors and cloud providers, these investments strengthen the case for deploying denser, memory-rich instance types and appliances across regions, while data-sovereignty constraints keep demand for hybrid deployments and local in-region managed services active in Europe and parts of Asia-Pacific.

Recent Industry Developments

- July 2026: Oracle introduced In-Memory Transaction Table and Commit Cache capabilities within Oracle AI Database 26ai on Exadata, targeting faster transaction lookups and commit processing using high-performance interconnects. The update reinforces Oracle’s push toward AI-optimized database infrastructure where in-memory acceleration features are packaged alongside Exadata to serve mixed OLTP and AI workloads.

- May 2026: HPE announced the HPE Compute Scale-up Server 3250, positioned for in-memory database deployments and built on Intel Xeon 6 processors with support for up to 48 TB of memory. By expanding the addressable ceiling for memory-dense configurations, the launch supports larger in-memory clusters and consolidation of latency-sensitive enterprise workloads.

- May 2025: AWS announced the general availability of Amazon Aurora DSQL to provide distributed SQL scalability with in-memory-style performance characteristics. The release expands managed-service options for teams that want low-latency semantics without running and tuning large on-premise memory footprints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The in-memory database market covers software and related services where the primary working dataset is kept in RAM to deliver very low latency for transactions, analytics, caching, and mixed workloads across enterprise and cloud environments.

Scope exclusions: We exclude general-purpose storage hardware and unrelated database tooling that does not materially rely on in-memory processing as the core value driver.

Segmentation Overview

- By Processing Type

- OLTP

- OLAP

- Hybrid Transactional/Analytical Processing (HTAP)

- By Deployment Mode

- On-premise

- Cloud

- Edge/Embedded

- By Data Model

- Relational (SQL)

- NoSQL (Key-Value, Document, Graph)

- Multi-model

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Application

- Real-time Transaction Processing

- Operational Analytics and BI Dashboards

- AI/ML Model Serving

- Caching and Session Stores

- By End-user Industry

- BFSI

- Telecommunications and IT

- Retail and E-commerce

- Healthcare and Life Sciences

- Manufacturing and Industrial IoT

- Media and Entertainment

- Government and Defense

- Others (Energy, Education, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- Taiwan

- South Korea

- Japan

- India

- Rest of Asia-Pacific

- South America

- Brazil

- Mexico

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the fact base around database adoption and IT spend patterns, and then narrowing it to solutions where in-memory processing is a defining feature. We referenced public sources such as US SEC filings, annual reports, and investor presentations, along with cloud provider documentation and pricing pages that help validate deployment patterns and common workload mixes.

To keep inputs grounded, we also used non-paywalled indicators from the US Bureau of Economic Analysis for digital investment context, World Bank and OECD macro series for cross-country normalization, and ITU connectivity statistics for infrastructure readiness. We used peer-reviewed systems and database journals to sanity check technical adoption claims. Patent databases and a news and financials subscription were used selectively to track product releases, M&A, and feature shifts that affect what gets counted as an in-memory database versus adjacent caching or analytics layers. These sources are not exhaustive, and we used many other public references for data collection, validation, and clarification as the model was built.

Primary Interviews and Surveys

Primary work focused on checking what buyers actually deploy for latency-sensitive workloads, and how license, subscription, and managed-service pricing is packaged in real deals. We spoke with a mix of software providers, cloud and channel partners, and enterprise users across major regions so gaps from desk inputs could be closed, and then assumptions on adoption, pricing, and upgrade cycles could be triangulated.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 19% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 25% | EMEA: 29% |

| Smaller Players: 20% | Managers: 56% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic, where the top-down view reconstructs the addressable spend by mapping enterprise database and data-platform budgets into in-memory use cases, and then applying region and vertical level adoption signals. When the demand pool is formed, it is corrected using bottom-up approximations from sampled pricing and volume checks, partner feedback on deployment counts, and selective supplier revenue splits to keep totals realistic.

Key model inputs include cloud versus on-premise deployment mix, average contract values by organization size, the share of workloads that are transactional versus analytic (including HTAP), renewal and upgrade timing, and the rate at which RAM-heavy architectures are adopted for real-time use cases. Where direct volume indicators are missing, gaps are handled through proxy variables that can be defended on calls, such as application penetration in BFSI and telecom, and the shift toward managed database services.

Forecasts are produced using scenario analysis supported by trend smoothing on adoption and pricing paths, and then reviewed against what interviewees expect for cloud migration pace, AI and streaming workload growth, and cost sensitivity. The final series is kept repeatable by tying each step to a small set of measurable inputs and clearly stated assumptions.

Data Validation & Update Cycle

Validation is done in multiple passes, starting with unit checks on pricing, adoption, and regional splits, followed by variance checks against independent signals such as cloud consumption direction, enterprise software spend trends, and reported performance-driven upgrade cycles. If an input creates an unusual jump in one region or industry, it is flagged, reviewed by another analyst, and then rechecked with a fresh secondary source or a re-contact with a relevant respondent.

The model and narrative are reviewed before sign-off so the final numbers align with the stated scope and definitions. Reports are refreshed annually, and interim updates are made when material events occur, such as major product changes or shifts in deployment models. Before delivery, we do a final pass so the market numbers reflect the latest available information.

Mordor Intelligence's In Memory Database Market Sizing Compared With Other Published Estimates

Published market values for in-memory databases can differ because each publisher makes its own choices on what to count, which year is treated as the base, and how cloud-managed database revenue is handled. Differences also show up when one model leans more on vendor-side revenue reporting, while another leans on buyer adoption signals.

The main gap comes from whether adjacent layers like in-memory data grids, caching services, and broader in-memory computing stacks are folded into the total, where Mordor Intelligence counts only in-memory database revenues tied to database deployments and related services within the defined scope, and then forecasts from a 2026 base year using adoption and pricing checks by region.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.05 B (2026) | |

| Global Consultancy A | USD 6.66 B (2025) | Uses a different base year and a broader packaging of related services in the category definition, which can shift what is counted as database revenue versus platform add-ons, and then changes the starting point for the forecast path. |

| Industry Publisher B | USD 3.90 B (2024) | Starts from an earlier year with a smaller adoption pool and often applies slower growth assumptions for cloud-managed deployments, which can understate the share of spend moving into subscription and consumption-led pricing. |

Taken together, the spread is mainly explained by scope choices and year selection, followed by how cloud revenue is translated into market value. By keeping inclusions explicit and tying the forecast to adoption, deployment mix, and pricing movement, the final number stays traceable to clear steps that can be repeated and reviewed.

Key Questions Answered in the Report

What is the current value of the In-Memory Database market?

The In-Memory Database market was valued at USD 8.05 billion in 2026 and is projected to reach USD 15.31 billion by 2031.

Which region leads the In-Memory Database market growth?

Asia-Pacific led with 31.95% revenue in 2025 and is expected to post a 16.65% CAGR through 2031.

Why are HTAP architectures important for AI workloads?

HTAP unifies transactional and analytical processing, enabling real-time inference without ETL delays, as shown by Oracle HeatWave GenAI.

How are falling DRAM prices affecting adoption?

Lower USD/GB pricing and new persistent memory options reduce the total cost of ownership, making in-memory deployments economically viable.

What challenges limit very large in-memory clusters?

High-availability architecture becomes complex beyond 40 TB, with clustering protocols incurring performance overhead.

Page last updated on: