Advanced Therapy Medicinal Products (ATMP) CDMO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

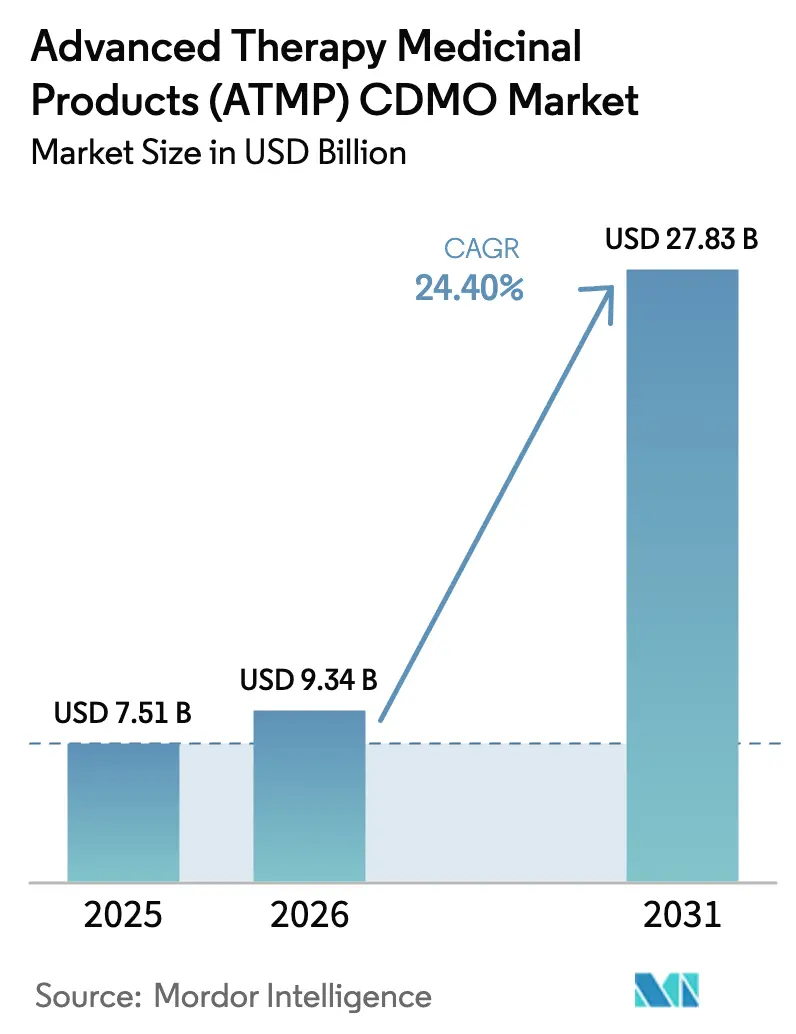

| Market Size (2026) | USD 9.34 Billion |

| Market Size (2031) | USD 27.83 Billion |

| Growth Rate (2026 - 2031) | 24.40% CAGR |

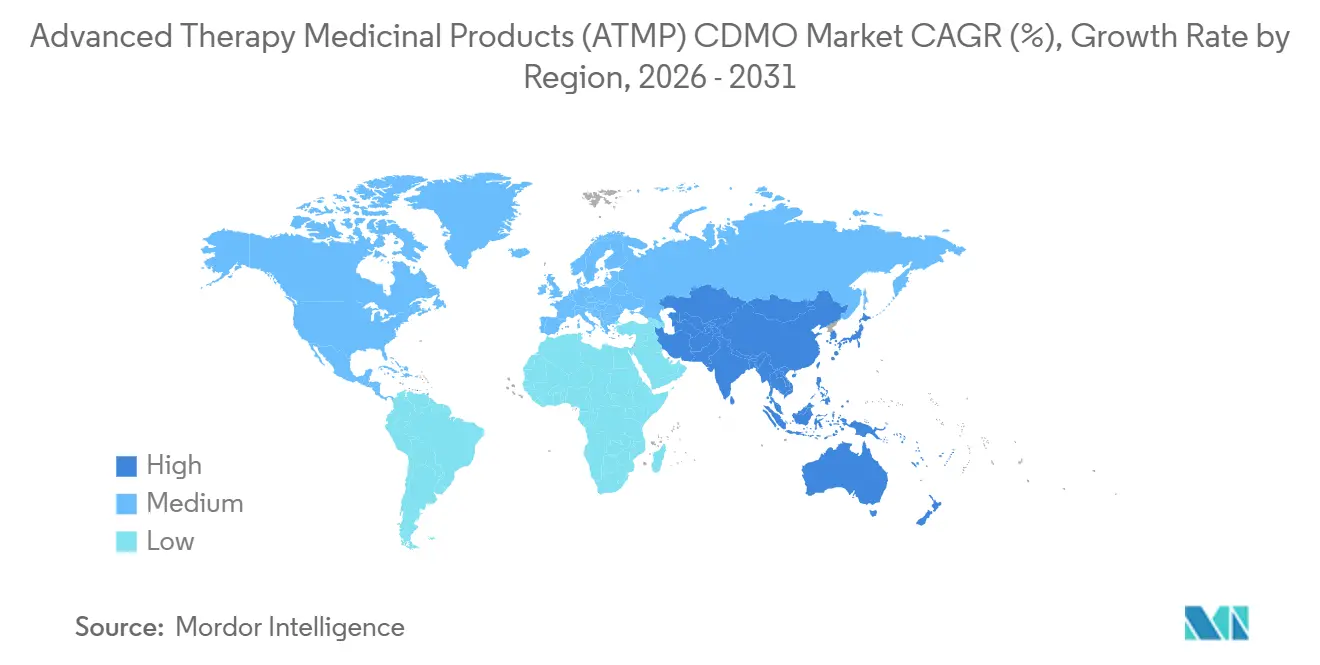

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Therapy Medicinal Products (ATMP) CDMO Market Analysis by Mordor Intelligence

The Advanced Therapy Medicinal Products CDMO Market size is expected to grow from USD 7.51 billion in 2025 to USD 9.34 billion in 2026 and is forecast to reach USD 27.83 billion by 2031 at 24.40% CAGR over 2026-2031.

Momentum stems from a steady flow of new U.S. Food and Drug Administration (FDA) and European Medicines Agency (EMA) approvals, tighter clinical timelines, and the escalating complexity of autologous and allogeneic manufacturing platforms. Sponsors are locking in multi-year contracts earlier in development, transforming CDMOs into strategic partners that supply process know-how, regulatory guidance, and capital-intensive capacity. Viral-vector projects dominate capital spending, yet rapid uptake of closed, automated cell-processing suites is compressing production lead times and lowering contamination risk. Simultaneously, digital-twin software allows engineers to model critical process parameters, cutting engineering runs in half while satisfying emerging real-time release expectations at the FDA’s Center for Biologics Evaluation and Research.

Key Report Takeaways

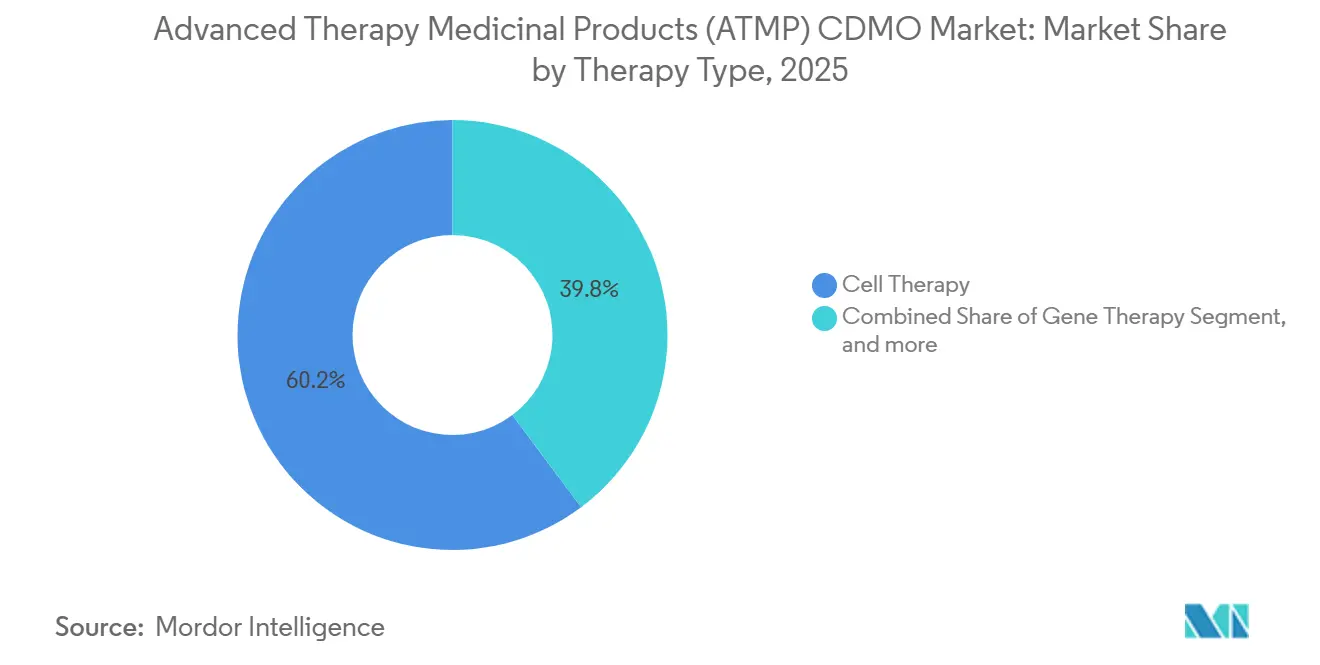

- By therapy type, cell therapy held 60.21% of revenue in 2025, whereas gene therapy is pacing for a 26.43% CAGR to 2031.

- By service type, cGMP manufacturing contributed 45.78% in 2025, while regulatory and quality-assurance support is advancing at a 26.87% CAGR through 2031.

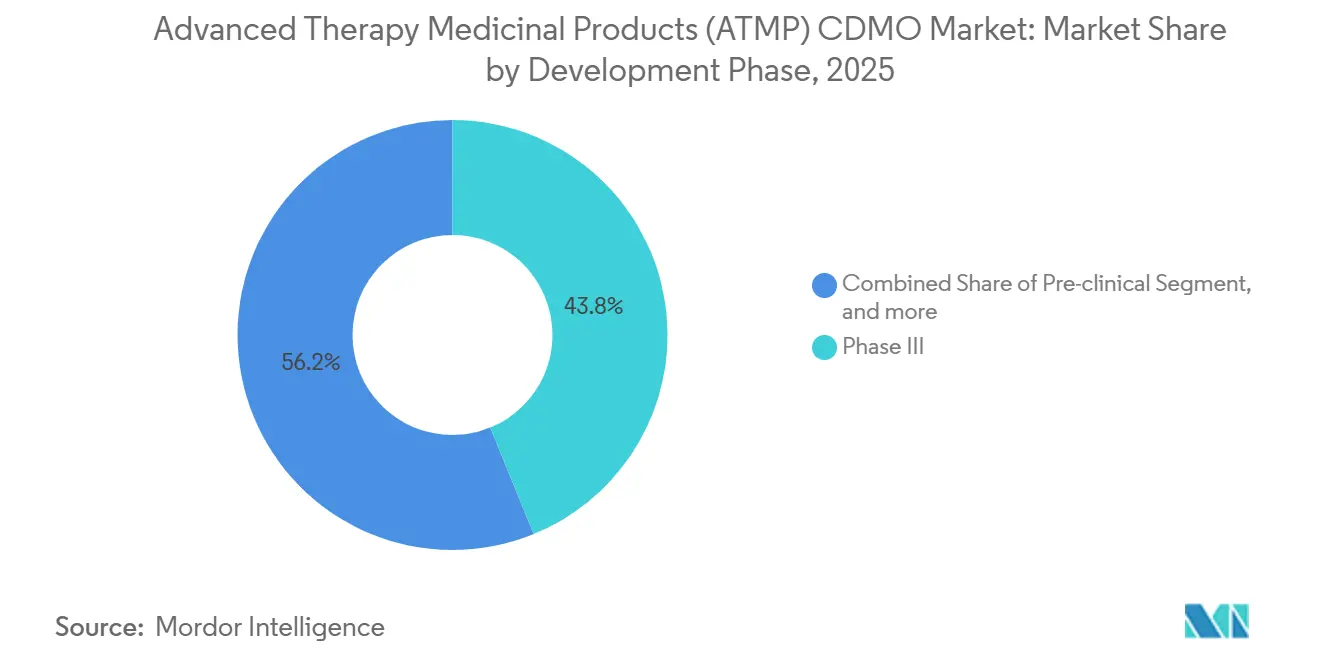

- By development phase, Phase III accounted for 43.83% of demand in 2025, yet pre-clinical work is set for a 27.11% CAGR over the forecast window.

- By vector type, adeno-associated virus (AAV) captured 36.76% in 2025, whereas lentiviral vectors are expanding at 26.66% to 2031.

- By cell source, autologous formats led with 55.76% in 2025 and allogeneic approaches are growing at 27.43% through 2031.

- By geography, North America commanded 42.76% of 2025 revenue; Asia-Pacific is registering the fastest 25.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Advanced Therapy Medicinal Products (ATMP) CDMO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of approved cell and gene therapies | +6.2% | Global, led by North America & Europe | Medium term (2–4 years) |

| Outsourcing trend among small and mid biotech sponsors | +5.8% | Global, concentrated in North America & APAC | Short term (≤ 2 years) |

| Scaling investments in viral vector manufacturing capacity | +4.9% | North America, Europe, emerging APAC | Long term (≥ 4 years) |

| Adoption of closed modular manufacturing suites | +3.7% | North America & Europe, spill-over to APAC | Medium term (2–4 years) |

| Digital twin platforms for bioprocess optimization | +2.1% | Global, early adoption in North America & EU | Long term (≥ 4 years) |

| Regionalization of supply chains to reduce vein-to-vein time | +1.7% | APAC core, spill-over to MEA & South America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Approved Cell and Gene Therapies

The FDA and EMA cleared 27 advanced-therapy products across 2024-2025, broadening indications from ultra-rare to high-prevalence diseases. Each approval demands discrete manufacturing footprints, forcing CDMOs to run parallel vector and cell platforms. EMA’s PRIME pathway shortened development timelines by roughly 18 months, prompting sponsors to reserve commercial slots during Phase I, years earlier than historical norms[1]European Medicines Agency, “PRIME Annual Update 2025,” ema.europa.eu . Modalities now span CRISPR-edited hematopoietic stem cells, oncolytic viruses, and in vivo base editors, elevating fixed costs yet positioning full-service CDMOs as one-stop solutions. The pipeline mix is diversifying facility layouts; suites optimized for ex vivo lentiviral work do not readily pivot to suspension AAV, driving capital outlays for multi-purpose cleanrooms. Competitive advantage is shifting toward providers that master multiple GMP technologies under one roof.

Outsourcing Trend Among Small and Mid-Size Biotech Sponsors

Cash-constrained biotechs increasingly view internal plants as capital traps; nearly 9 in 10 early-stage developers now outsource at least one GMP task, a figure up 30 percentage points from 2023. Risk-sharing contracts, in which CDMOs co-fund process development in exchange for future volume, are becoming the norm. European firms frequently tap Asian partners for Phase I material, then shift to Western facilities for pivotal batches to satisfy proximity preferences from inspectors. Modular service bundles covering analytics, regulatory filings, and process validation reduce hiring needs, making CDMOs de facto extensions of sponsor CMC teams. As more pivotal trials run on externally produced drug substance, investors reward outsourcing-heavy business models, reinforcing the cycle.

Scaling Investments in Viral-Vector Manufacturing Capacity

Fujifilm committed USD 1.2 billion to expand its Holly Springs, North Carolina, gene-therapy campus in 2024, adding 200,000 L of suspension bioreactor capacity. AGC Biologics allocated USD 350 million to a Yokohama lentiviral suite in 2025, in response to Asia’s growing demand. Capital intensity and regulatory scrutiny create high entry barriers, concentrating capacity among deep-pocketed conglomerates. Smaller CDMOs specialize in non-viral and lipid nanoparticle delivery to avoid USD 150 million viral-suite price tags. Licensing deals that import mRNA expertise into vector manufacturing, such as the Lonza-Moderna deal, allow players to amortize learning curves across modalities.

Adoption of Closed Modular Manufacturing Suites

Cellares’ fully automated Cell Shuttle demonstrated clinical-grade CAR-T production in seven days, prompting a USD 380 million partnership with Bristol Myers Squibb in 2024. Lonza’s Cocoon and Miltenyi’s CliniMACS Prodigy similarly eliminate open handling, easing global tech-transfer and reducing contamination. Identical closed modules can be deployed in Boston, Basel, and Beijing, ensuring process comparability without replicating entire cleanrooms. Academic hospitals are leveraging these systems to run investigator-initiated trials, fragmenting early-stage demand yet expanding consumable sales. Vendor lock-in risk rises once a module is validated, driving stickier client relationships.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic shortage of skilled advanced therapy workforce | -3.4% | Global, acute in North America & Europe | Medium term (2–4 years) |

| High capital expenditure for GMP-compliant facilities | -2.9% | Global, barrier in emerging APAC & South America | Long term (≥ 4 years) |

| Limited supply of GMP-grade plasmid starting materials | -1.8% | Global, bottleneck in North America & Europe | Short term (≤ 2 years) |

| Heightened geopolitical scrutiny of cross-border vector supply | -1.2% | North America, Europe, China | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Chronic Shortage of Skilled Advanced-Therapy Workforce

The Alliance for Regenerative Medicine projects a 20,000-person global shortfall by 2028 across manufacturing, QC, and regulatory roles[2]Alliance for Regenerative Medicine, “2025 Annual Report,” alliancerm.org. CDMOs report onboarding lead times for new AAV teams lengthened from six to 12 months between 2022 and 2025. Universities offer few targeted curricula, forcing companies to run in-house academies that inflate labor budgets. QC analysts with orthogonal assay expertise command 25-35% salary premiums, pressuring margins. Regional talent imbalances persist; Boston and San Francisco remain deep pools, while Singapore and Research Triangle Park struggle to recruit without relocation incentives.

High Capital Expenditure for GMP-Compliant Facilities

Building a 500-L viral-vector suite costs upward of USD 150 million, including redundant utilities and ISO 7 cleanrooms, deterring mid-tier entrants. Fixed assets depreciate over 15-20 years, yet technology cycles evolve faster, risking stranded costs. Modular single-use systems cut initial spend to USD 30-50 million but still pose financing hurdles in emerging markets where importing specialized equipment lengthens timelines. Sale-leaseback deals convert CapEx into OpEx but raise per-batch charges. Rapid capsid evolution (AAV9 to engineered variants) threatens facility relevance before payback.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Cell Therapy Dominates, Gene Therapy Accelerates

Cell therapy generated 60.21% of the Advanced Therapy Medicinal Products CDMO market share in 2025, a lead driven by commercial CAR-T programs. Gene therapy is advancing at a 26.43% CAGR through 2031, propelled by in vivo AAV platforms for hemophilia and Duchenne muscular dystrophy. Cell therapies command premium pricing because each patient requires a bespoke batch, which inflates per-dose costs. Gene therapies benefit from pooled manufacturing runs that amortize fixed costs across larger patient cohorts, improving margin scalability. Tissue-engineered products remain niche but are gaining traction in orthopedics as payers finalize reimbursement codes. Combined ATMPs, integrating cells and scaffolds, are at an early adoption stage; the FDA draft guidance published in 2025 should catalyze clinical momentum[3]U.S. Food and Drug Administration, “Combination ATMP Draft Guidance 2025,” fda.gov.

The advanced clinical pipeline for gene therapy is expanding pediatric indications, doubling addressable volumes and straining existing vector capacity. Autologous cell therapy growth, while slower in percentage terms, remains robust in absolute dollars, given per-patient manufacturing expense that can exceed USD 200,000. Tissue-engineered grafts face hurdles in generating evidence, slowing uptake despite technical advances. Combined ATMPs struggle with divergent device-versus-biologic classifications across jurisdictions, complicating compliance for CDMOs. Overall, gene therapy’s scalable economics position it as the long-term growth engine for the Advanced Therapy Medicinal Products CDMO market.

By Service Type: Manufacturing Leads, Regulatory Support Surges

cGMP manufacturing accounted for 45.78% of 2025 revenue, underscoring high per-batch fees tied to viral-vector runs and complex cell-processing workflows. Regulatory and quality support is forecast to grow at a 26.87% CAGR, reflecting divergent expectations for FDA, EMA, and National Medical Products Administration dossier submissions. Process development captured roughly one-fifth of revenue but is increasingly priced as a commodity in fixed-fee packages. Fill-finish services remain a smaller slice, yet integrated cold-chain logistics set full-service providers apart. Analytical testing commands premium rates when next-generation sequencing or flow cytometry potency assays are required.

Regulatory divergence forces sponsors to maintain parallel strategies, elevating demand for CDMOs with ex-agency reviewers on staff. The analytical scope is expanding from ELISA to genomic integrity metrics, requiring capital-intensive instrumentation and advanced bioinformatics skills. Fill-finish commoditization squeezes margins, but providers integrating shipping, depot management, and just-in-time delivery win share. Overall, manufacturing retains the lion’s share of the Advanced Therapy Medicinal Products CDMO market size, while regulatory consulting delivers the fastest revenue growth.

By Development Phase: Late-Stage Trials Dominate, Pre-Clinical Expands

Phase III programs accounted for 43.83% of 2025 spending, as numerous pivotal trials launched between 2022-2024. Pre-clinical engagements are set to grow at a 27.11% CAGR, fueled by venture-backed biotechs using CDMOs to de-risk CMC before building internal plants. Phase II demand outpaces Phase I demand thanks to accelerated approval rules, pushing GMP scale-up forward earlier in development. Commercial manufacturing involves fewer batches but higher revenue per lot due to exhaustive validation, stability, and pharmacopeial testing.

Platform technologies like base editing enable early-stage firms to run multiple candidates, each requiring unique process development. Large CDMOs with inspection histories secure most Phase III and commercial contracts as sponsors prioritize compliance track records. Decentralized production models, endorsed in an FDA 2025 draft, may fragment commercial manufacturing over the next decade, creating regional opportunities for mid-size providers.

By Vector Type: AAV Dominates, Lentiviral Surges

AAV accounted for 36.76% of 2025 revenue, cementing its lead in in-vivo gene transfer. Lentiviral vectors are on a 26.66% CAGR trajectory as allogeneic CAR-T and NK pipelines grow. Retroviral systems retain niche usage in stem-cell ex-vivo settings, while non-viral lipid nanoparticles serve mRNA therapeutics and ex-vivo editing. AAV production remains capital-intensive; a single batch can cost USD 5-10 million, driven by high-titer requirements and empty-capsid removal steps. Lentiviral containment adds 10-15% to facility spend due to replication-competent virus precautions.

Engineered AAV capsids with enhanced tropism are pushing demand for custom vector development, a capability offered by few CDMOs. Non-viral vectors sidestep immunogenicity but face efficacy constraints for systemic delivery. Collectively, vector diversification keeps multi-platform expertise a core competitive differentiator and underpins sustained growth in the Advanced Therapy Medicinal Products CDMO market.

By Cell Source: Autologous Leads, Allogeneic Accelerates

Autologous products delivered 55.76% of 2025 revenue, powered by approved CAR-T brands. Allogeneic formats offer a projected 27.43% CAGR by eliminating patient-specific batch records and slashing per-dose costs to nearly one-quarter of autologous levels. Master cell banks enable industrial-scale runs, though immunogenicity management requires CRISPR edits and adds regulatory complexity. CDMOs are building closed, automated bioreactor lines tailored to allogeneic manufacturing, betting on future volume.

Autologous processes remain sticky; switching to allogeneic approaches would force new clinical trials and regulatory filings. Nevertheless, demand for rapid treatment in acute indications positions allogeneic platforms as a disruptive force. The FDA’s 2024 donor-eligibility guidance and EMA’s 2025 risk-assessment draft reduce uncertainty, encouraging sponsors to scale allogeneic trials and cementing long-term growth for the Advanced Therapy Medicinal Products CDMO market.

Geography Analysis

North America generated 42.76% of 2025 revenue thanks to a dense clinical pipeline, FDA regulatory clarity, and proximity of Boston-Cambridge and San Francisco CDMO clusters. Capacity bottlenecks and rising labor costs temper regional CAGR, nudging sponsors toward European and Asian alternatives. Europe delivered roughly 30% of revenue in 2025, leveraging Germany’s viral-vector hubs, the United Kingdom’s Oxford-Cambridge corridor, and EMA’s centralized ATMP approvals that grant access to 27 markets via one license.

Asia-Pacific is poised for a 25.76% CAGR to 2031, buoyed by China’s national cell-therapy roadmap, Japan’s conditional approval system, and South Korea’s GMP investments. BioNTech’s Singapore plant and WuXi’s Suzhou expansion underline the shift toward localized production to meet vein-to-vein targets. Australia’s Therapeutic Goods Administration alignment with the EMA positions the country as a regional entry point.

The Middle East and Africa accounted for less than 5% of 2025 demand, though Dubai’s 2025 cell-therapy hub signals early growth. South America stood near 3%, constrained by reimbursement limits and scarce viral-vector suites, yet Argentina’s streamlined ATMP rules are improving the outlook. Overall, geographic diversification is central as sponsors hedge geopolitical risk, reinforcing multi-continent footprints across the Advanced Therapy Medicinal Products CDMO market.

Competitive Landscape

Five leading players—Lonza, Catalent (Novo Holdings), Thermo Fisher Scientific, Samsung Biologics, and WuXi Advanced Therapies—control roughly 35-40% of installed capacity, giving the Advanced Therapy Medicinal Products CDMO market a moderate-concentration profile. Novo Holdings’ USD 16.5 billion acquisition of Catalent in February 2024 exemplifies vertical integration, granting Novo Nordisk priority access to viral vector and cell suites. Smaller firms differentiate via specialization: Oxford Biomedica in lentivirus, Vibalogics in select AAV serotypes, and Resilience through modular campuses.

Automation and data analytics shape competition; CDMOs adopting digital twins and closed systems command premium pricing by reducing tech-transfer timelines. Regulatory pedigree remains a deal-winning lever—facilities with zero FDA Form 483 observations enjoy higher bid conversion. Emerging disruptors, including Cellares’ automated cell-therapy shuttle, push incumbents toward efficiency gains. Consolidation is expected to accelerate as private equity funds and large pharma chase scarce GMP capacity.

Advanced Therapy Medicinal Products (ATMP) CDMO Industry Leaders

Catalent, Inc.

Lonza

WuXi Advanced Therapies

AGC Biologics

CELONIC Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Porton Advanced, one of the leading contract development and manufacturing organizations (CDMO) specializing in advanced therapy medicinal products (ATMPs), partnered with Eureka Therapeutics, Inc., a clinical-stage biotechnology company dedicated to developing novel T‑cell therapies for both solid tumors and hematologic malignancies.

- September 2024: Rentschler Biopharma SE, one of the leading global contract development and manufacturing organization (CDMO) for biopharmaceuticals, including advanced therapy medicinal products (ATMPs) launched an expanded service offering at its dedicated advanced therapies site in Stevenage, United Kingdom. This enhancement introduces a new lentiviral vector manufacturing (LVV) toolbox that complements the company’s existing adeno-associated viral (AAV) vector services.

Global Advanced Therapy Medicinal Products (ATMP) CDMO Market Report Scope

As per the scope of the report, advanced therapy medicinal products (ATMPs) are innovative medicines based on gene therapy, somatic-cell therapy, or tissue-engineered products. They are designed to treat or cure rare and complex diseases by modifying or replacing faulty cells or genes. ATMPs are highly specialized and require advanced manufacturing processes and regulatory oversight.

The Advanced Therapy Medicinal Products CDMO Market is Segmented by Therapy Type (Gene Therapy, Cell Therapy, Tissue-Engineered Products, and Combined ATMPs), Service Type (Process Development, CGMP Manufacturing, Fill-Finish & Packaging, Analytical & QC Testing, and Regulatory & QA Support), Development Phase (Pre-Clinical, Phase I, Phase II, Phase III, and Commercial), Vector Type (AAV, Lentiviral, Retroviral & Γ-Retroviral, and Non-Viral/Plasmid), Cell Source (Autologous and Allogeneic), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD for the above segments.

| Gene Therapy |

| Cell Therapy |

| Tissue-Engineered Products |

| Combined ATMPs |

| Process Development |

| CGMP Manufacturing |

| Fill-Finish & Packaging |

| Analytical & QC Testing |

| Regulatory & QA Support |

| Pre-Clinical |

| Phase I |

| Phase II |

| Phase III |

| Commercial |

| Adeno-Associated Virus (AAV) |

| Lentiviral |

| Retroviral & Γ-Retroviral |

| Non-Viral / Plasmid |

| Autologous |

| Allogeneic |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Gene Therapy | |

| Cell Therapy | ||

| Tissue-Engineered Products | ||

| Combined ATMPs | ||

| By Service Type | Process Development | |

| CGMP Manufacturing | ||

| Fill-Finish & Packaging | ||

| Analytical & QC Testing | ||

| Regulatory & QA Support | ||

| By Development Phase | Pre-Clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Commercial | ||

| By Vector Type | Adeno-Associated Virus (AAV) | |

| Lentiviral | ||

| Retroviral & Γ-Retroviral | ||

| Non-Viral / Plasmid | ||

| By Cell Source | Autologous | |

| Allogeneic | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving double-digit growth in the Advanced Therapy Medicinal Products CDMO market?

A broader pipeline of FDA- and EMA-approved cell and gene therapies plus early outsourcing of CMC tasks propels a 24.4% CAGR through 2031.

Which service line is expanding fastest for CDMOs?

Regulatory and quality-assurance support is pacing at a 26.87% CAGR as sponsors juggle diverging global dossier requirements.

How large will Asia-Pacific's share become by 2031?

Asia-Pacific is projected to outpace all regions at a 25.76% CAGR, closing much of the gap with North America by the end of the forecast period.

Why are closed modular suites gaining traction?

Fully automated, closed systems trim vein-to-vein time to under one week and cut contamination risk, making them attractive for autologous CAR-T production.

What technology bottleneck most threatens supply continuity?

GMP-grade plasmid DNA remains constrained, with lead times stretching to 9-12 months due to the limited number of kilogram-scale suppliers worldwide.

Page last updated on: