Nitrile Butadiene Rubber (NBR) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

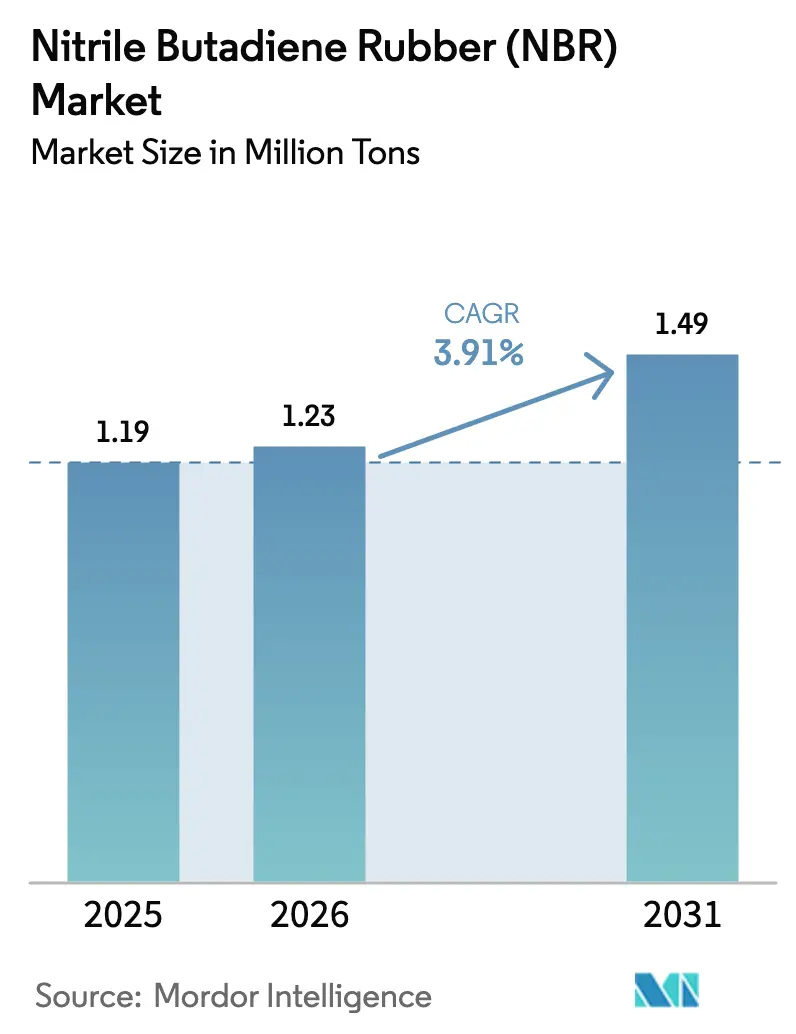

| Market Volume (2026) | 1.23 Million tons |

| Market Volume (2031) | 1.49 Million tons |

| Growth Rate (2026 - 2031) | 3.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nitrile Butadiene Rubber (NBR) Market Analysis by Mordor Intelligence

The Nitrile Butadiene Rubber Market size is expected to grow from 1.19 million tons in 2025 to 1.23 million tons in 2026 and is forecast to reach 1.49 million tons by 2031 at a 3.91% CAGR over 2026-2031. Cost swings in butadiene feedstock, steady reshoring of glove capacity, and dual ICE-EV seal demand shape the growth profile. Latex grades advance faster than bale grades as medical and cleanroom users lock in long-term offtake. Automotive and MRO users continue to anchor volume because NBR balances oil resistance and price. Rising solution-polymerized supply adds a purity-driven premium tier that cushions overall margins.

Key Report Takeaways

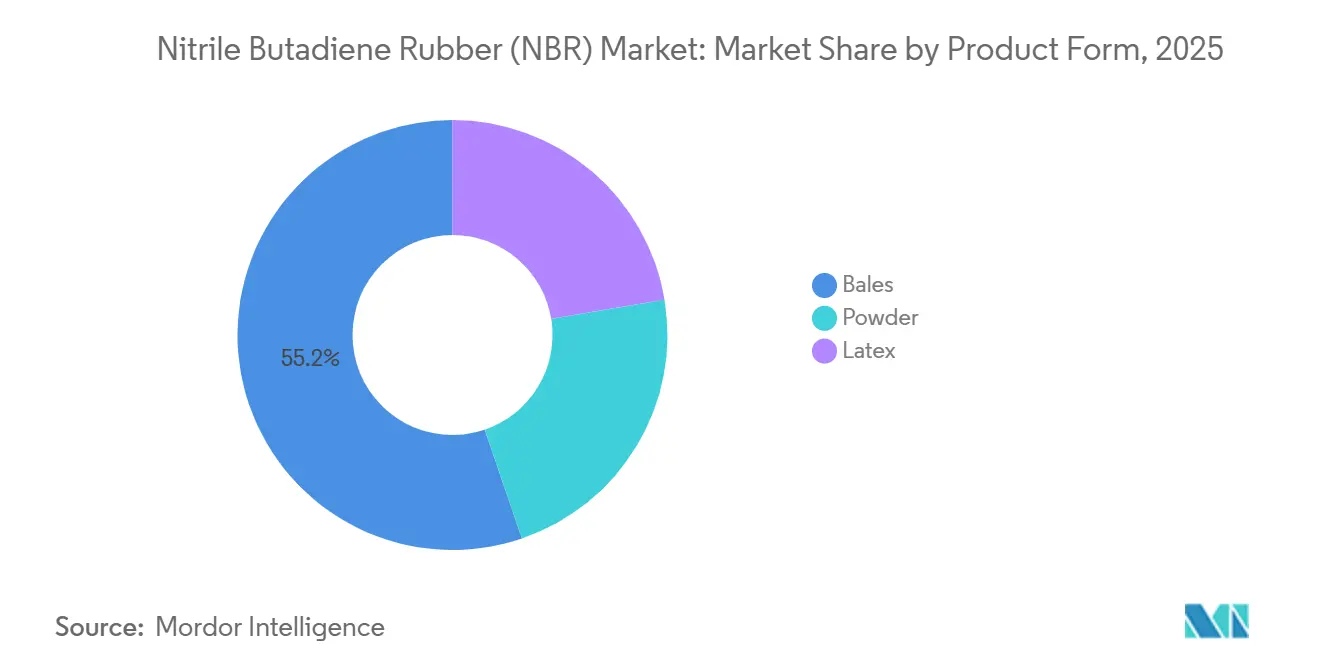

- By product form, bales accounted for 55.23% of the market share in 2025, and the latex product form is expected to grow at a CAGR of 4.59% during the forecast period (2026-2031).

- By manufacturing process, emulsion polymerization led with 62.56% volume share in 2025, while solution polymerization is set to accelerate at a 4.81% CAGR.

- By application, gaskets and O-rings commanded 32.29% of the Nitrile Butadiene Rubber (NBR) market share in 2025; the segment is on track for a 4.44% CAGR to 2031.

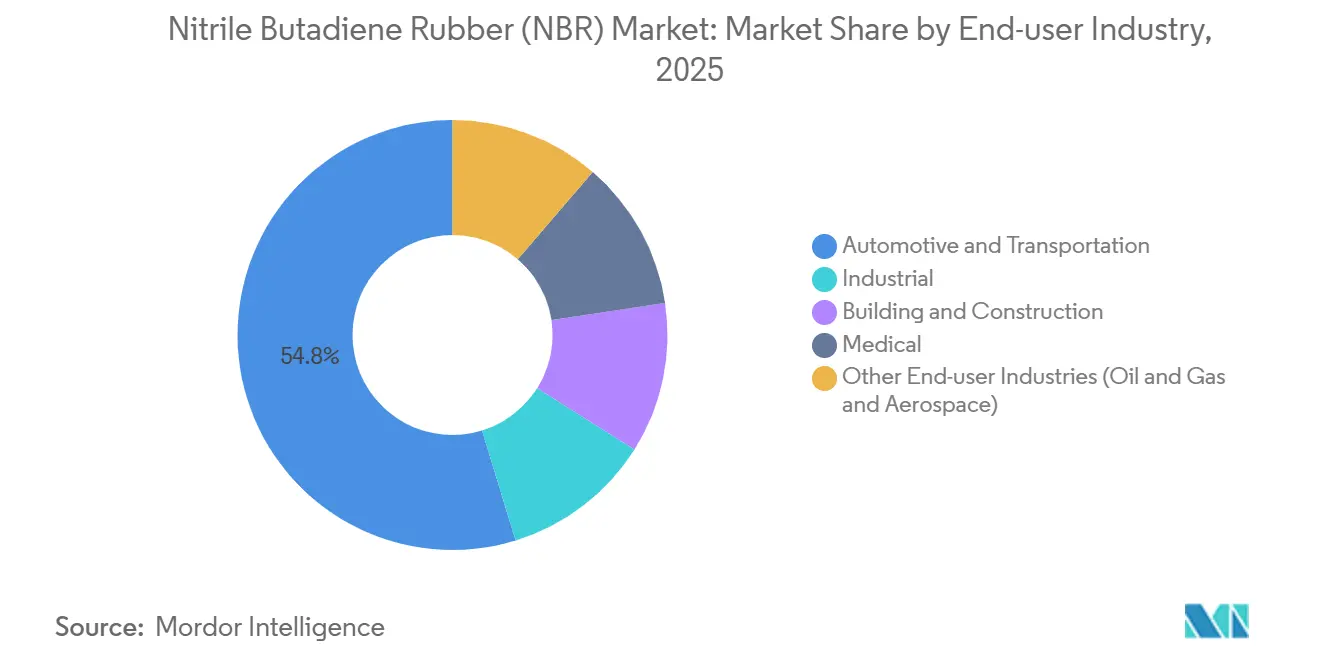

- By end-user industry, the automotive and transportation segment accounted for 54.76% in 2025, whereas the medical segment is poised for a 4.89% CAGR during the forecast period (2026-2031).

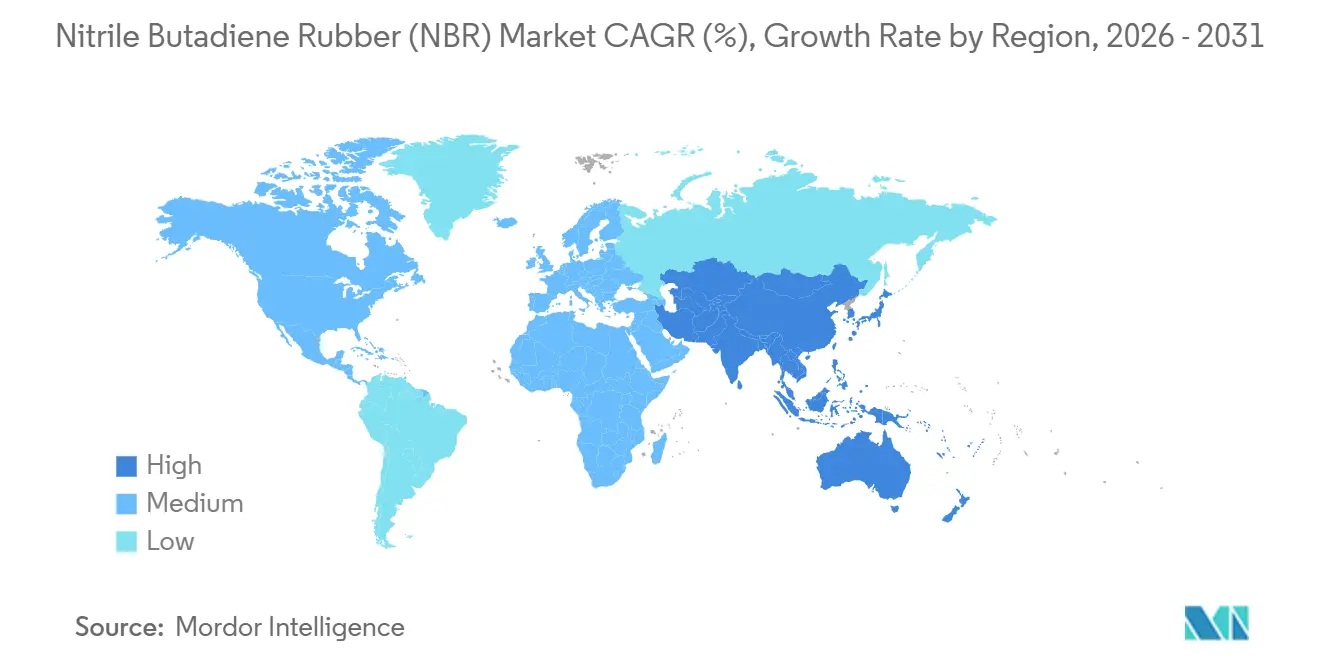

- By region, Asia Pacific captured 57.81% of the Nitrile Butadiene Rubber (NBR) market size in 2025 and is forecast to grow at a 4.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nitrile Butadiene Rubber (NBR) Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in disposable nitrile glove capacity | +0.8% | North America, Southeast Asia (Malaysia, Vietnam), Japan | Medium term (2-4 years) |

| Growing OEM demand for oil-resistant seals and hoses in ICE and EV powertrains | +0.7% | Global, with concentration in Asia-Pacific, North America, Europe | Long term (≥ 4 years) |

| Expansion of industrial machinery MRO in Asia's light-manufacturing hubs | +0.6% | Asia-Pacific (China, India, Indonesia, Thailand, Vietnam) | Medium term (2-4 years) |

| Surge in NBR seals for hydrogen fuel-cell vehicles | +0.3% | Japan, South Korea, Europe (Germany, France), California | Long term (≥ 4 years) |

| Growth of oil-resistant gloves for semiconductor cleanrooms | +0.2% | Asia-Pacific (Taiwan, South Korea, China), United States (Arizona, Texas) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise In Disposable Nitrile Glove Capacity

United States investments of USD 1.5 billion since 2024 secured new glove lines in Virginia, Baltimore, and Ohio[1]U.S. Department of Commerce, “Domestic Glove Manufacturing Investments 2024–2025,” commerce.gov. Japan’s Showa Glove added JPY 15 billion for domestic expansion, and Malaysia’s Hong Seng earmarked RM 3 billion for fresh latex output. Multiyear offtake deals with health systems underpin regional suppliers. The strategic pivot from low-cost imports to resilience elevates local NBR latex sales. Producers that guarantee consistent copolymer purity win the early contracts.

Growing OEM Demand For Oil-Resistant Seals And Hoses In ICE And EV Powertrains

NBR covers around 60% of automotive O-ring needs because it withstands petroleum fluids at moderate heat[2]Freudenberg Sealing Technologies, “Powertrain Seal Materials Presentation 2024,” freudenberg.com. Electric vehicles still use gearboxes and cooling circuits that specify NBR. HNBR only displaces NBR where temperatures exceed 120°C, so dual-platform production preserves base demand. OEMs now maintain mixed seal portfolios rather than full material swaps. This strategy supports steady nitrile butadiene rubber market growth above the broader elastomer average.

Expansion Of Industrial Machinery MRO In Asia’s Light-Manufacturing Hubs

China’s synthetic-rubber output climbed 4.7% year on year in 2024 to 7.02 million t. Aging factories in India, Indonesia, and Vietnam shorten maintenance cycles, driving hoses, belts, and gasket consumption. MRO now represents about 55% of Asia’s industrial-rubber volume (IRSG.ORG). Local compounders choose Bale NBR because mills and internal mixers are already installed. The MRO surge is structural, not cyclical, sustaining the nitrile butadiene rubber market beyond new-equipment slumps.

Surge In NBR Seals For Hydrogen Fuel-Cell Vehicles

Studies show silica-filled NBR lowers hydrogen swelling to near 37% compression-set increase, broadening its use in secondary FCEV seals. Japanese and Korean automakers forecast cumulative FCEV sales above 50,000 units by 2028. While HNBR secures high-pressure stack seals, NBR remains in coolant pumps and low-pressure lines. Incremental volumes add diversity to the nitrile butadiene rubber market without heavy price premiums.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight butadiene supply volatility and price spikes | -0.5% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Stringent VOC limits on solvent-borne NBR adhesives | -0.3% | Europe, North America, Japan | Medium term (2-4 years) |

| Rising substitution by HNBR in high-temperature sealing | -0.4% | Global, concentrated in automotive and oil & gas sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tight Butadiene Supply Volatility And Price Spikes

Spot butadiene ranged from USD 956 per t in the US Gulf to USD 1,380 per t in China during May 2025, a 44% gap. Producers lacking a captive monomer risk margin compression when outages occur. Asia will add 4.91 million t per year of new cracker capacity by 2030, yet near-term tightness persists. Petrochemical majors leverage integration to undercut merchant NBR sellers, which fuels consolidation and reshapes the nitrile butadiene rubber market.

Stringent VOC Limits On Solvent-Borne NBR Adhesives

The European Industrial Emissions Directive tightens VOC thresholds below 50 g/L for many adhesive lines. California’s South Coast AQMD mirrors these limits. Formulators shift toward carboxylated latex and reactive hot melts. This transition requires capex for new emulsion reactors and pushes commodity bale NBR toward lower-margin outlets. Waterborne innovation thus becomes a competitive necessity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Bales Remain Core While Latex Leads Growth

Bales accounted for 55.23% of volume in 2025, underscoring their status as the flexible workhorse for compounders. Latex grades, however, post a 4.59% CAGR on the back of glove expansion and waterborne adhesive uptake. Powder NBR stays niche but profitable, with the top five vendors holding 65% of the sub-segment.

Carboxylated latex addresses VOC rules in automotive interiors and footwear. Bale demand rides Asia’s mixing-mill infrastructure despite feedstock volatility. Powder commands premiums in PVC modification and wire coatings where solvent-free handling is vital. The interplay of these formats supports balanced growth for the nitrile butadiene rubber market.

By Manufacturing Process: Emulsion Dominates, Solution Adds Premium Tier

Emulsion polymerization supplied 62.56% of the 2025 output owing to cost and scale advantages. Solution routes grow 4.81% per year as medical and electronics buyers specify low residual monomer. FDA guidance for pharmaceutical stoppers favors solution-grade purity.

JSR and ARLANXEO invest in solution capacity at Yokkaichi and Leverkusen to serve this premium. Emulsion remains the cost leader for automotive hoses and gaskets. The two processes thus segment the nitrile butadiene rubber market into commodity and specialty lanes without direct cannibalization.

By Application: Seals Anchor Volume, Gloves Sustain Momentum

Gaskets and O-rings delivered 32.29% of 2025 consumption and grew at a 4.44% CAGR as ICE and EV platforms both need oil-resistant seals. Industrial MRO adds a steady pull from hydraulic presses and CNC machines. Gloves represent the headline growth story as global nitrile revenue climbs toward USD 19.3 billion by 2032.

Hoses and belts see softer uptake because EPDM and HNBR win ozone and heat resistance niches. Adhesives migrate to waterborne systems that favor latex over solvent NBR. Flooring and consumer goods provide a base load but limited upside, keeping the nitrile butadiene rubber market tied to core sealing and glove demand.

By End-user Industry: Automotive Tops, Medical Fastest

Automotive and transportation absorbed 54.76% of the 2025 volume thanks to entrenched engine and drivetrain uses. BEVs still deploy NBR in gearboxes and steering racks, preserving relevance. Medical products, led by examination gloves, log the highest 4.89% CAGR.

Industrial machinery benefits from Asia’s deep manufacturing base and older plant fleets. Building and construction rely on latex sealants that meet stricter indoor-air rules. Niche oil-and-gas and aerospace users pay premiums for certified grades, boosting margins in the nitrile butadiene rubber market.

Geography Analysis

Asia-Pacific held 57.81% of the 2025 volume and is forecast to grow at a 4.38% CAGR to 2031 as China increases its synthetic-rubber output. Sinopec, PetroChina, and CNPC lead the way in operating the largest local NBR facilities. In Southeast Asia, the glove clusters in Malaysia, Thailand, and Vietnam are set to absorb an increasing tonnage of latex, bolstered by Hong Seng's RM 3 billion plant, which is slated to come online in 2026.

North America is ramping up its capacity for medical gloves, fueled by significant investment in U.S. projects scheduled between 2024 and 2025. In Montreal, Canada’s Medicom has poured in substantial funding, while Mexico's auto supply chain is turning to Gulf Coast crackers for their bale NBR imports. However, feedstock fluctuations pose a challenge.

Europe is on track to consume significant volumes by 2032, growing at a steady CAGR, primarily driven by demand in automotive sealing and VOC-compliant adhesives. While ARLANXEO is supplying specialty grades from its Leverkusen facility, SIBUR's plants in Russia are catering to Eastern Europe, navigating through trade frictions. Both South America and the Middle East find themselves importing the majority of their requirements, but Brazil's aftermarket and South Africa's mining hose demand are providing a modest yet consistent boost to the nitrile butadiene rubber market.

Competitive Landscape

The Nitrile Butadiene Rubber (NBR) market is moderately consolidated. Backward integration shields costs for majors, whereas Zeon and JSR differentiate through solution and HNBR lines. Synthomer’s ISCC-certified bio-based latex pilot slated for 2026 introduces a sustainability premium. Commodity bale NBR suffers the fiercest price pressure as spot butadiene volatility cascades downstream. Specialty niches such as powder, carboxylated latex, and solution grades earn 20–40% premiums due to formulation lock-in.

Nitrile Butadiene Rubber (NBR) Industry Leaders

LG Chem

ARLANXEO

KUMHO PETROCHEMICAL

LANXESS

China Petrochemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: At an inauguration ceremony in Nantong, China, ARLANXEO and TSRC unveiled their newly relocated and expanded joint venture NBR (nitrile-butadiene rubber) plant. The revamped facility boasts an enhanced capacity of 40,000 tons per annum, enabling it to produce a wider array of high-quality NBR products.

- February 2025: Synthomer, in collaboration with Neste and PCS, set up a pioneering value chain certified by the International Sustainability and Carbon Certification (ISCC). This initiative focuses on producing bio-based nitrile latexes for the glove industry, utilizing responsibly sourced bio-based feedstock.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the nitrile butadiene rubber (NBR) market as all virgin, solid, and latex copolymers of acrylonitrile and butadiene that are polymerized by emulsion or solution routes and then sold for value-adding into end-products such as hoses, belts, seals, gaskets, cables, adhesives, and industrial or medical gloves.

Scope exclusion: reground or recycled NBR streams and downstream finished goods revenues lie outside the baseline.

Segmentation Overview

- By Product Form

- Bales

- Powder

- Latex

- By Manufacturing Process

- Emulsion Polymerisation

- Solution Polymerisation

- By Application

- Hoses

- Belts and Cables

- Gloves

- Adhesives and Sealants

- Gaskets and O-Rings

- Other Applications (Consumer Goods)

- By End-user Industry

- Automotive and Transportation

- Industrial

- Building and Construction

- Medical

- Other End-user Industries (Oil and Gas and Aerospace)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Thailand

- Malaysia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC

- Turkey

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- South Africa

- Nigeria

- Egypt

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Interviews and pulse surveys with polymer scientists, automotive hose converters, glove exporters, chemical distributors, and procurement heads across Asia-Pacific, North America, Europe, and the Gulf validated desk findings, clarified latent demand in EV thermal loops, and fine-tuned ASP progression assumptions. Follow-up calls with raw-material suppliers flagged expected acrylonitrile turnarounds that we wove into the near-term scenario book.

Desk Research

Analysts began with trade-flow reconstruction from sources such as UN Comtrade, Eurostat COMEXT, and China Customs before pairing output with capacity disclosures in company 10-Ks and investor decks.

Government portals, including the U.S. Energy Information Administration for feedstock price curves and UNIDO's industrial production index for demand proxies, helped us normalize long-run volume swings.

We then sampled technical papers from Rubber Chemistry & Technology and regional trade associations (e.g., IRSG, JSRPMA) to benchmark application density per vehicle or glove.

Subscription resources like D&B Hoovers and Dow Jones Factiva supplied revenue splits that refine regional average-selling-price (ASP) ladders.

This list is indicative; many other open and paid references informed data validation.

Market-Sizing & Forecasting

The core model starts with a top-down "production + net trade" build that yields apparent NBR consumption by region, which is then pressure-tested through selective bottom-up checks such as sampled maker revenue roll-ups and channel ASP × volume probes.

Key variables include global light-vehicle assemblies, nitrile glove export tonnage, butadiene and ACN cost indices, refinery operating rates, and infrastructure capex pipelines.

A multivariate regression links these drivers to historical demand and produces the base projection, while scenario analysis captures feedstock price shocks and accelerated glove capacity additions.

Where bottom-up estimates stray beyond a five-percent band, analyst judgment aligns them with the reconciled total.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, peer analyst cross-checks, and senior review sign-off.

Reports refresh each year, and interim updates trigger when material events, such as plant closures, force-majeure, and regulatory bans, shift modeled supply or demand.

Why Our Nitrile Butadiene Rubber Baseline Commands Reliability

Published figures often differ because firms choose distinct scope boundaries, price bases, and refresh cadences.

Key gap drivers include whether latex glove revenues are counted, how unreported merchant sales are imputed, the currency year used for ASP deflation, and how quickly modelers bake in new capacity ramps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.67 billion (2025) | Mordor Intelligence | - |

| USD 2.33 billion (2024) | Global Consultancy A | Excludes medical-grade latex; applies 2019 ASPs without inflation uplift |

| USD 2.84 billion (2025) | Trade Journal B | Uses announced capacity rather than operational output; limited primary checks outside Asia |

The comparison shows that, by grounding volumes in verified production and trade data and refreshing prices yearly, Mordor Intelligence delivers a balanced, decision-ready baseline clients can track and replicate with confidence.

Key Questions Answered in the Report

What is the 2026 size outlook for nitrile butadiene rubber?

What is the 2026 size outlook for nitrile butadiene rubber?

Which product form grows fastest in the next five years?

Latex grades expand at a 4.59% CAGR through 2031, outpacing bale and powder formats due to glove and adhesive demand.

Why does automotive remain the largest consuming sector?

ICE and EV powertrains both need oil-resistant seals and hoses, keeping automotive at 54.76% of 2025 volume.

Which region drives future volume gains?

Asia-Pacific leads with 57.81% of 2025 demand and a 4.38% CAGR thanks to China’s synthetic-rubber expansion and Southeast Asian glove output.

How are VOC rules affecting NBR adhesives?

Stricter European and Californian limits force a switch from solvent-borne to waterborne systems, lifting demand for carboxylated NBR latex.

Page last updated on: