Hydrocephalus Shunts Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

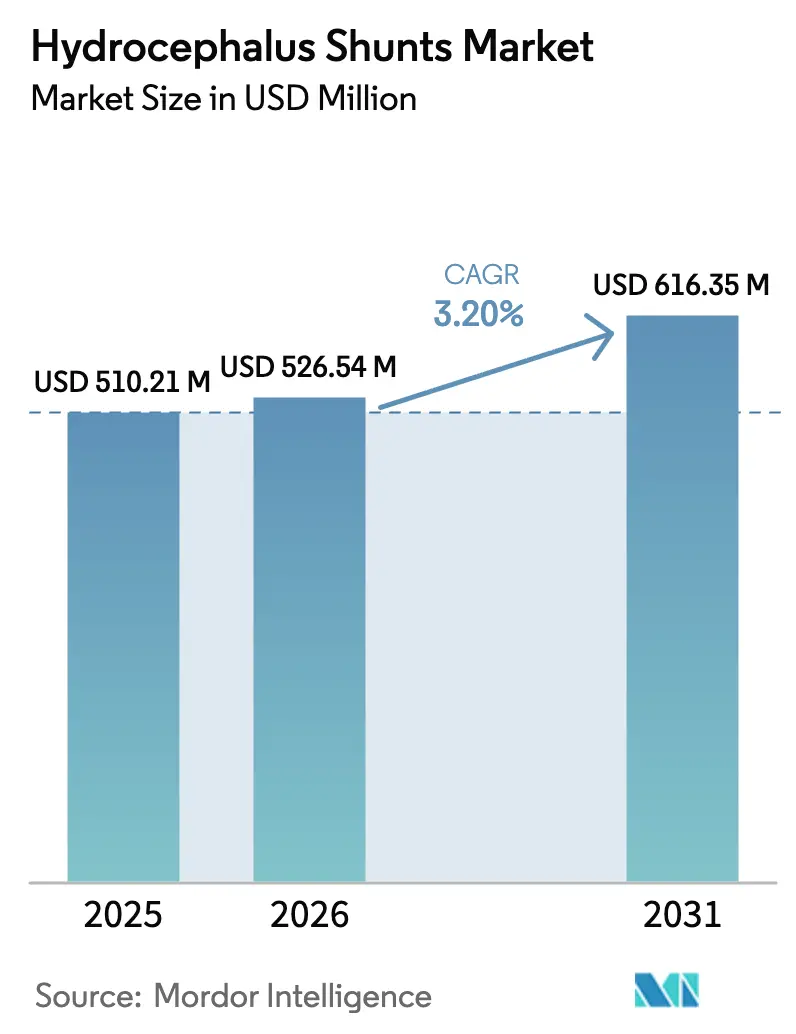

| Market Size (2026) | USD 526.54 Million |

| Market Size (2031) | USD 616.35 Million |

| Growth Rate (2026 - 2031) | 3.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrocephalus Shunts Market Analysis by Mordor Intelligence

The hydrocephalus shunts market size was valued at USD 510.21 million in 2025 and is estimated to grow from USD 526.54 million in 2026 to reach USD 616.35 million by 2031, at a CAGR of 3.20% during the forecast period (2026-2031). Demand tilts toward pediatric congenital cases, yet normal-pressure hydrocephalus (NPH) in adults over 65 is rising faster as aging populations and better diagnostics convert dementia misdiagnoses into shunt candidates. Reimbursement caps slow mature-market volumes, while public-private capacity-build programs in India, Indonesia, and Nigeria unlock latent demand. Product differentiation centers on programmable valves that lower revision risk, though magnetic-field interference prompts regulator scrutiny. Hospitals remain the dominant setting, yet payer push for cost control is steering suitable adult cases into ambulatory surgical centers (ASCs).

Key Report Takeaways

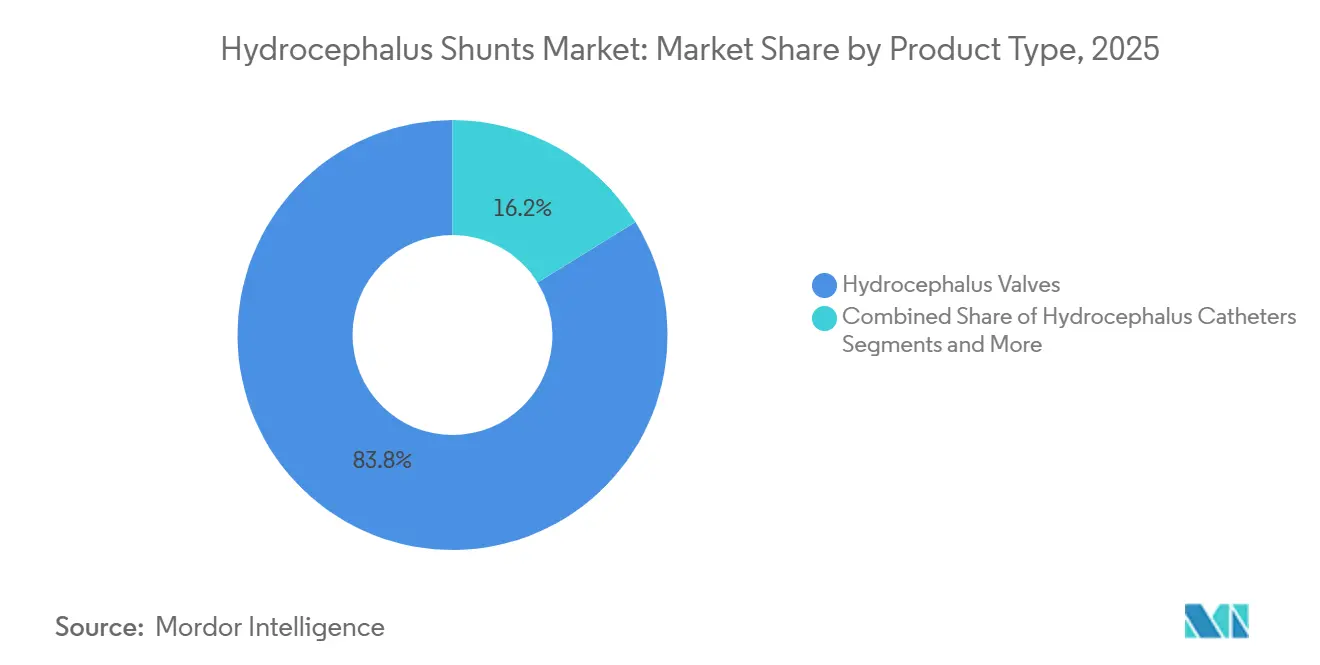

- By product type, hydrocephalus valves captured 83.81% of revenue in 2025, and programmable variants are forecast to grow at a 4.12% CAGR to 2031.

- By age group, pediatric procedures represented 70.23% of volume in 2025, while the adult segment is set to expand at a 4.21% CAGR through 2031.

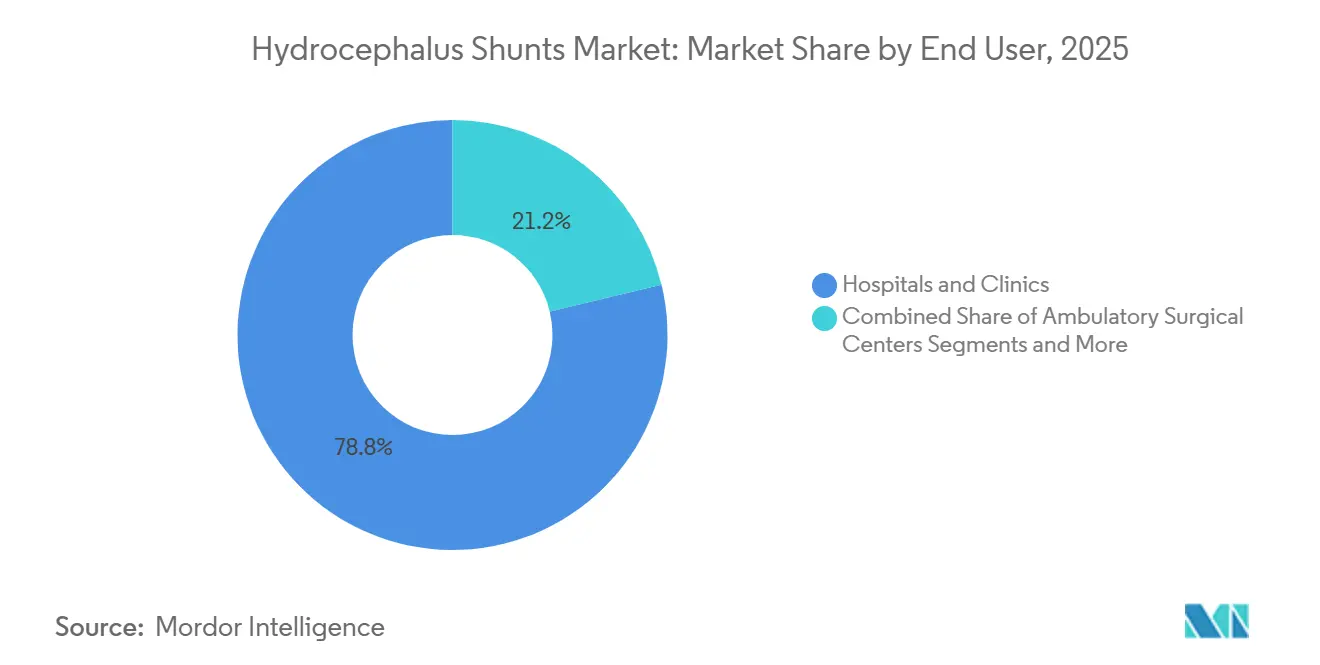

- By end user, hospitals and clinics held 78.76% share in 2025, whereas ASCs post the fastest growth at a 4.32% CAGR to 2031.

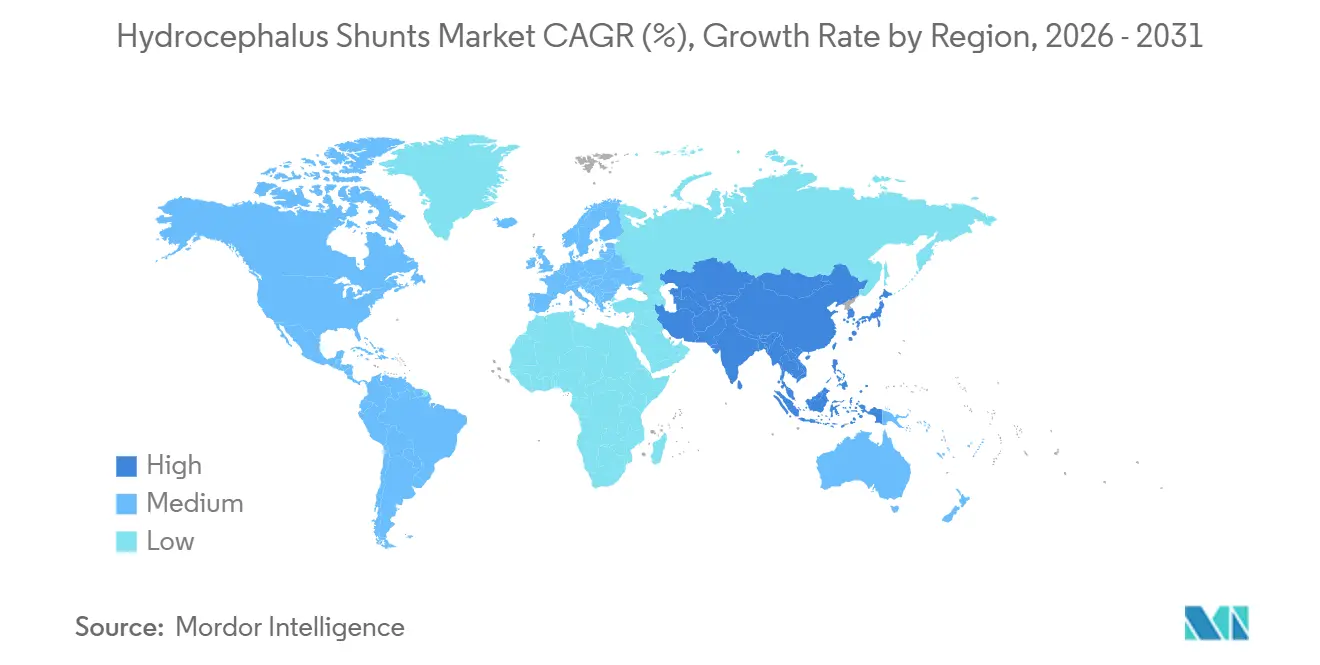

- By Geography, North America led with 42.23% of 2025 revenue; Asia-Pacific is projected to rise at a 4.52% CAGR, the quickest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hydrocephalus Shunts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of hydrocephalus & related neurological disorders | +0.8% | Global, with acute incidence growth in aging OECD nations and congenital case detection in APAC | Medium term (2-4 years) |

| Rapid growth of the geriatric population | +0.7% | North America, Europe, Japan, South Korea; emerging in China | Long term (≥4 years) |

| Accelerating adoption of programmable/adjustable-pressure valves | +0.6% | North America & EU core markets; gradual uptake in APAC urban centers | Short term (≤2 years) |

| Emergence of telemetric, sensor-enabled "smart" shunts | +0.5% | North America pilot sites; EU regulatory pathways under review; limited APAC penetration | Medium term (2-4 years) |

| PPP-funded neurosurgical capacity build-out in emerging markets | +0.4% | India, Indonesia, Nigeria, Kenya; selective Middle East initiatives | Long term (≥4 years) |

| Regulatory fast-track paths for novel shunts | +0.2% | North America, Europe, Japan, South Korea; emerging in India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hydrocephalus and Related Neurological Disorders

Congenital detection is climbing as prenatal ultrasound becomes routine in middle-income countries, while NPH prevalence grows among adults over 65, a cohort expected to reach 1.6 billion by 2050. Revised American Academy of Neurology guidelines now recommend lumbar puncture when gait disturbance and cognitive decline coexist, redirecting previously misdiagnosed dementia patients toward shunt therapy. Post-hemorrhagic and post-infectious cases also expand where neonatal intensive-care capacity outpaces infection-control infrastructure. This dual epidemiological pressure sustains procedure volumes beyond baseline population growth. Device makers view these trends as reliable demand drivers because each new implant anchors a multiyear revision-replacement revenue stream. Health-system planners, however, weigh the long-term follow-up burden when allocating neurosurgery budgets.

Rapid Growth of the Geriatric Population

Individuals aged 65 and older will nearly double to 1.6 billion by 2050, with East Asia and Southern Europe leading the surge.[1]United Nations, “World Population Prospects 2024,” un.org NPH prevalence in this cohort ranges from 0.2% to 2.9%, translating into millions of potential recipients. Japan already recorded a 23% jump in NPH admissions from 2020 to 2024. In the United States, Medicare raised ASC payments for shunt placement by 4.2% in 2025, signaling payer intent to shift uncomplicated adult cases away from higher-cost inpatient wards. As longevity extends in emerging economies, similar volume waves are anticipated, although surgeon shortages risk lengthening wait times. Manufacturers are therefore adapting product mixes, offering fixed-pressure valves for stable adult cases and reserving premium programmable models for pediatric growth-related pressure changes.

Accelerating Adoption of Programmable Valves

Programmable valves allow non-invasive pressure setting adjustments that cut two-year revision rates from 38% to 24% versus fixed-pressure designs. Medtronic’s Strata and Integra’s CERTAS Plus jointly hold roughly 60% of the North American programmable segment.[2]Medtronic, “Investor Presentation Q4 FY2025,” medtronic.com Uptake lags in resource-constrained markets because these valves cost two to three times more and require magnetic tools for post-operative tuning. Safety concerns surfaced when 37 unintended reprogramming incidents were linked to MRI scans, prompting a 2024 recall and new pre-imaging protocols. Despite the setback, payers still favor programmability for its lower lifetime episode cost, and device makers are redesigning magnetic shielding to meet an upcoming ISO standard for implantable device immunity.[3]U.S. Food and Drug Administration, “Safety Communication: Programmable Shunt Valve Reprogramming Risks 2024,” fda.gov

Emergence of Telemetric “Smart” Shunts

CereVasc’s eShunt received FDA Investigational Device Exemption in May 2024, embedding a wireless sensor that streams intracranial pressure data to clinicians. A 30-patient pilot showed occlusions were detected 11 days earlier than symptom-based methods. If pivotal trials extend these findings, revenue could shift toward subscription-based monitoring services that complement the implant. Medtronic disclosed a competing telemetry-enabled valve under development, confirming incumbent recognition of connectivity as a new competitive axis. Regulators require cybersecurity risk assessments under EU Medical Device Regulation, raising development costs but creating a moat around compliant products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High rates of shunt malfunction, revision & infection | -0.6% | Global, with higher revision burdens in resource-limited settings lacking sterile technique infrastructure | Short term (≤2 years) |

| Growing uptake of shunt-free alternatives | -0.4% | North America & EU where ETV expertise is concentrated; limited penetration in APAC and Africa | Medium term (2-4 years) |

| Magnetic-field–induced valve reprogramming risk | -0.2% | Primarily North America & EU with high MRI utilization; emerging concern in urban APAC centers | Short term (≤2 years) |

| EU circular-economy rules raising compliance costs for polymer shunts | -0.2% | European Union member states; indirect cost pass-through to global supply chains | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Rates of Shunt Malfunction, Revision and Infection

Roughly 40% of pediatric shunts fail within two years, and infection rates reach 15% in facilities with suboptimal sterile technique. Each revision costs up to 50% more than the initial implantation when emergency imaging and intensive care are included. Mechanical obstruction drives 60% of failures, while valve defects and tubing disconnections account for the rest. Antibiotic-impregnated catheters cut infection risk by about 30% but add USD 200–400 per device, limiting adoption in public systems. The reliability gap strengthens the case for outcome-based reimbursement contracts that penalize high revision rates and reward devices demonstrating sustained patency.

Growing Uptake of Shunt-Free Alternatives

Endoscopic third ventriculostomy (ETV) now achieves success rates above 70% in aqueductal stenosis patients older than one year. North American and European payers have begun tiered reimbursement that steers eligible patients to ETV-capable centers. While ETV avoids hardware complications, it suits only 20–30% of total hydrocephalus cases and relies on advanced endoscopic skill sets absent in many emerging regions. Nonetheless, its existence pressures shunt pricing and compels manufacturers to differentiate on durability and remote monitoring rather than commodity components. Hospitals lacking ETV capability face competitive disadvantage when payers favor centers of excellence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Valves Anchor Revenue, Systems Trail

Hydrocephalus valves held 83.81% of the hydrocephalus shunts market share in 2025 and are forecast to compound at 4.12% through 2031. Programmable versions gain momentum in North America and Europe due to reduced revision rates, whereas fixed-pressure models dominate cost-sensitive tenders in emerging markets. Standalone catheter sales grow where surgeons custom-build configurations for complex anatomies, yet bundled shunt systems remain attractive for inventory simplicity. The hydrocephalus shunts market size for valves is set to expand as telemetry layers new value propositions onto existing hardware. Sensor-enabled models under clinical evaluation could redirect profit pools toward data services, but extended regulatory pathways afford incumbents time to defend share.

Catheters and complete systems split the remaining revenue. Antibiotic-impregnated tubing gains traction in high-acuity pediatric centers, yet price premiums slow uptake in public hospitals. Fixed-package shunt kits appeal to ASCs that prioritize speed over customization. FDA 510(k) clearance timelines of under nine months enable quick iterative improvements, whereas sensor-integrated platforms must navigate the lengthier Premarket Approval route. Makers balancing both paths can hedge timelines and sustain portfolio breadth.

By Age Group: Pediatric Volume Meets Adult Growth

Pediatric patients accounted for 70.23% of 2025 implantations, reflecting a congenital incidence of 1–2 per 1,000 live births. These lifelong recipients generate recurring revision revenue, anchoring volume predictability even when birthrates plateau. Premature-infant survival improvements lift post-hemorrhagic demand in Asia and Africa, though infection risk complicates outcomes. The hydrocephalus shunts market size serving pediatric cohorts therefore remains resilient despite procurement budget pressures.

Adults over 65 represent the fastest-growing cohort with a projected 4.21% CAGR to 2031. Updated diagnostic protocols turn gait disturbance and cognitive decline into shunt referrals, particularly in Japan, South Korea, and the United States. ASCs capture many of these lower-complexity cases, aligning with payer incentives for outpatient care. Fixed-pressure valves often suffice for adult NPH physiology, creating a distinct product-mix compared with programmable pediatric demand. Manufacturers that segment offerings by age-specific clinical needs can optimize margin and market penetration.

By End User: ASCs Gain Momentum

Hospitals and clinics commanded 78.76% of revenue in 2025 because complex pediatric and revision surgeries necessitate inpatient resources. However, ASCs are projected to record a 4.32% CAGR through 2031, the quickest among end users, after CMS removed shunt procedures from its inpatient-only list. National insurers followed, using differential cost-sharing to nudge uncomplicated NPH cases toward outpatient venues. The hydrocephalus shunts market size attributable to ASCs therefore expands even as average selling prices trend lower. Device makers now supply turnkey shunt kits optimized for ASC workflows, which favor rapid turnover and minimal intraoperative customization.

Regional ASC penetration varies. In the United States about 15% of shunt placements already occur in ASCs, yet hospital-centric payment models slow similar shifts in Europe. Regulatory compliance remains stringent: Joint Commission standards for infection control apply equally to ASCs, raising per-case overhead for smaller facilities. Still, payers continue to expand eligible procedure lists, suggesting outpatient settings will claim incremental share over the forecast horizon.

Geography Analysis

North America generated 42.23% of 2025 revenue, driven by high reimbursement and rapid adoption of programmable and telemetric valves. Medicare’s 2025 outpatient payment uplift and FDA breakthrough designations ensure the region remains the launchpad for novel devices. Canada funds programmable implants through provincial systems, though cost-containment pilots tie payment to two-year revision outcomes. Mexico’s dual-track market sees private institutions adopt premium imports while public hospitals rely on lower-cost fixed-pressure valves.

Asia-Pacific is the fastest-growing geography at a 4.52% CAGR through 2031 as China and India expand reimbursement catalogs and hospital infrastructure. Domestic assembly by multinational device makers sidesteps tariffs, cutting retail prices and accelerating uptake. Japan and South Korea face aging-driven volume growth yet grapple with neurosurgeon shortages that lengthen wait times; capacity pilots now train general surgeons in basic shunt placement. Southeast Asian growth concentrates in urban medical hubs, while rural areas remain underserved.

Europe shows steady but slower expansion. Programmable valves enjoy reimbursement in Germany, whereas the United Kingdom’s National Health Service favors fixed-pressure models to curb device budgets. The region’s Circular Economy directive forces manufacturers to redesign polymer components for recyclability by 2028, raising compliance costs that likely translate into higher device prices. Southern Europe regains procurement momentum post-pandemic, though tenders remain intensely price-competitive.

The Middle East and Africa record uneven performance. Gulf Cooperation Council nations allocate oil revenues to tertiary neurosurgery centers that specify premium programmable valves, while sub-Saharan growth depends on donor-funded PPPs that can stall when fiscal priorities shift. South America is anchored by Brazil, where reimbursement delays pressure hospital cash flows, and Argentina, where currency volatility curtails imports, prompting surgeons to adopt locally sourced alternatives.

Competitive Landscape

Global leadership is moderately consolidated. Medtronic leverages its Strata family and worldwide distribution spanning 150 countries; the firm also disclosed development of a telemetry-enabled valve slated for 2026 trials. Integra bundles shunts with dural grafts and cranial fixation products, exchanging volume discounts for multi-year supply-chain lock-ins. Niche competitors such as Sophysa, B. Braun, and Kaneka Medix win tenders in emerging markets through price or specialized features like dual-pressure posture control.

White-space competition centers on data connectivity and hardware-free procedures. CereVasc’s eShunt could shift competitive dynamics toward subscription monitoring if pivotal trials succeed. Incumbents answer with in-house telemetry projects or acquisitions targeting software analytics capabilities. Meanwhile, ETV adoption in obstructive cases introduces a procedural substitute that erodes implant demand in advanced markets. Manufacturers that demonstrate lower revision rates through real-world evidence may sustain premium pricing despite rising cost pressures.

Hydrocephalus Shunts Industry Leaders

Medtronic

Spiegelberg GmbH & Co. KG

Tokibo Co., Ltd. (Sophysa)

Natus Medical Incorporated

B. Braun SE (Christoph Miethke)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kaneka Medix announced a 40% capacity expansion in Osaka focused on antibiotic-impregnated catheters

- December 2024: Phoenix Biomedical gained FDA 510(k) clearance for its low-cost Ascent fixed-pressure valve targeting emerging-market tenders.

- May 2024: CereVasc secured FDA IDE for the eShunt, enabling pivotal U.S. trials with 150 patients.

- April 2024: CereVasc pilot data showed sensor-equipped shunts detected occlusions 11 days sooner than symptom-based approaches.

Global Hydrocephalus Shunts Market Report Scope

As per the scope of the report, a hydrocephalus shunt is a medical device that helps treat a condition in the brain in which excessive accumulation of cerebrospinal fluid occurs, resulting in increased intracranial pressure within the skull. These devices relieve pressure on the brain caused by fluid accumulation.

The hydrocephalus shunts market is segmented by product type, age group, end user, and geography. By product type, the market is segmented into hydrocephalus valves and hydrocephalus catheters (shunt systems). By age group, the market is segmented into pediatric and adult. By end user, the market is segmented into hospitals and clinics, ambulatory surgical centers, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market size is provided in terms of value (USD).

| Hydrocephalus Valves | Adjustable-Pressure Valves |

| Fixed-Pressure Valves | |

| Hydrocephalus Catheters | |

| Shunt Systems |

| Pediatric |

| Adult |

| Hospitals and Clinics |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hydrocephalus Valves | Adjustable-Pressure Valves |

| Fixed-Pressure Valves | ||

| Hydrocephalus Catheters | ||

| Shunt Systems | ||

| By Age Group | Pediatric | |

| Adult | ||

| By End User | Hospitals and Clinics | |

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hydrocephalus shunts market?

The hydrocephalus shunts market is valued at USD 526.54 million in 2026 and is forecast to reach USD 616.35 million by 2031.

How fast is the market expected to grow?

The market is projected to expand at a 3.2% CAGR between 2026 and 2031.

Which product category holds the largest market share?

Hydrocephalus valves accounted for 83.81% of 2025 revenue and remain the leading product type.

Why are programmable valves gaining adoption?

They allow non-invasive pressure adjustments that reduce two-year revision rates from 38% to 24%, lowering lifetime treatment costs.

Which region is growing the fastest?

Asia-Pacific posts the highest forecast CAGR at 4.52%, propelled by expanded reimbursement and hospital capacity in China and India.

How will telemetric “smart” shunts affect the market?

If pivotal trials succeed, telemetric shunts could shift revenue toward subscription-based remote monitoring, challenging traditional hardware-only models.

Page last updated on: