HVAC Motor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

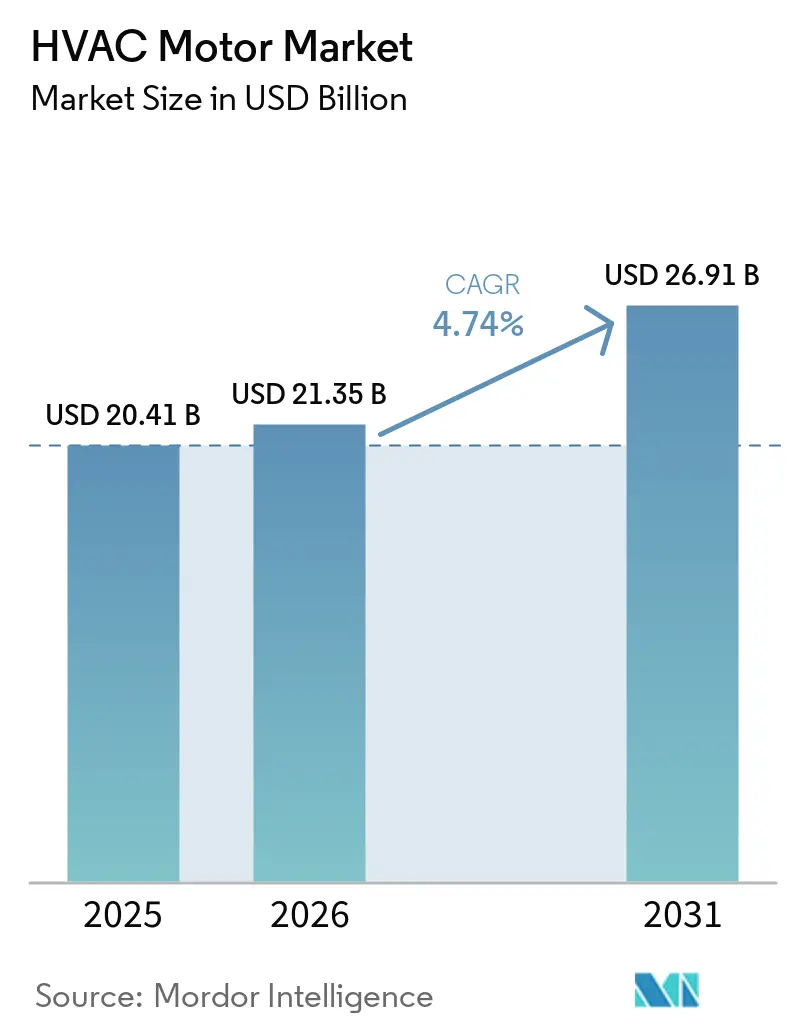

| Market Size (2026) | USD 21.35 Billion |

| Market Size (2031) | USD 26.91 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HVAC Motor Market Analysis by Mordor Intelligence

The HVAC motor market size is expected to grow from USD 20.41 billion in 2025 to USD 21.35 billion in 2026 and is forecast to reach USD 26.91 billion by 2031 at 4.74% CAGR over 2026-2031. In 2026, binding motor efficiency rules, faster electrification of space heating, and AI-led data center construction are raising motor specification requirements across the HVAC motor market at the same time. This overlap is supporting both replacement demand and new installations, which gives the HVAC motor market a steadier base than earlier housing-led cycles usually delivered. Compliance timelines through 2029 are turning many upgrades from optional spending into required procurement, which supports demand even when parts of the building cycle soften. The same shift is lifting the value of motors with variable-speed capability, embedded controls, and tighter power quality performance, which is changing product mix and pricing across OEM channels. Semiconductor tightness and longer redesign cycles tied to low-GWP refrigerants are still slowing some premium products, but they are not strong enough to alter the broader growth path of the HVAC motor market.

Key Report Takeaways

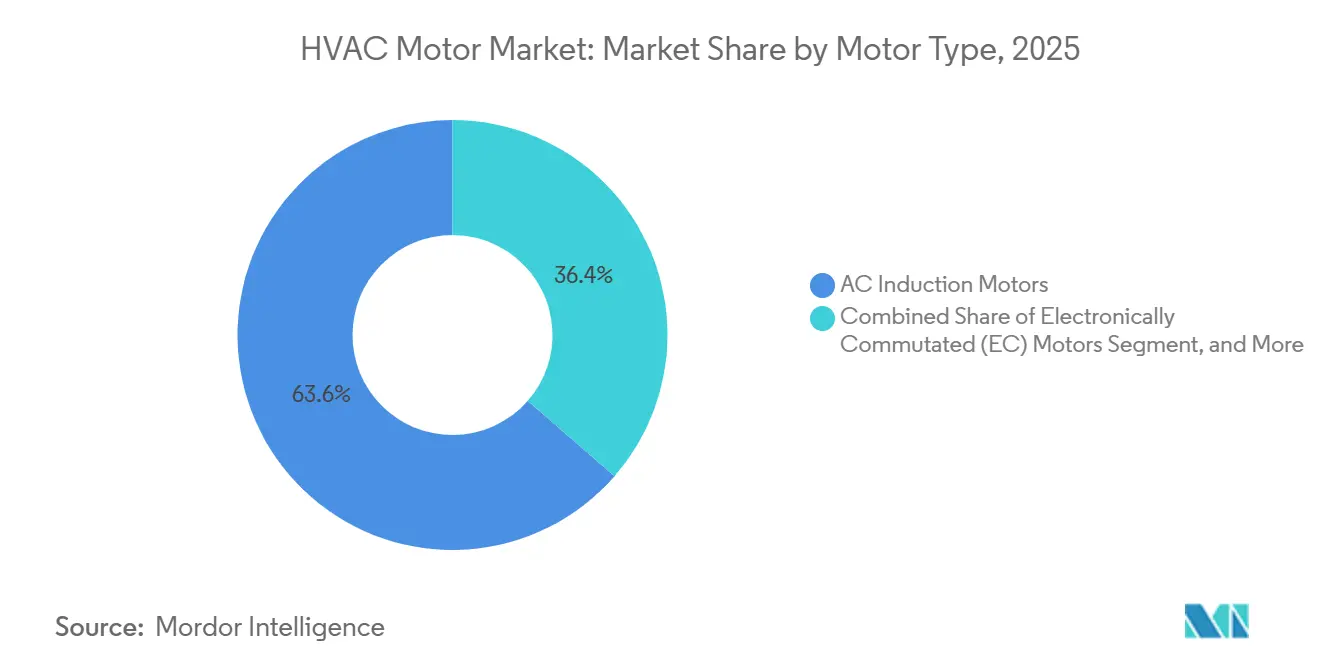

- By motor type, AC induction motors held 63.55% of the HVAC motor market revenue in 2025, while EC motors are projected to expand at a 5.54% CAGR through 2031.

- By power rating, less than 1 HP motors accounted for 58.89% of HVAC motor market revenue in 2025, and are expected to grow at a 5.26% CAGR during the forecast period.

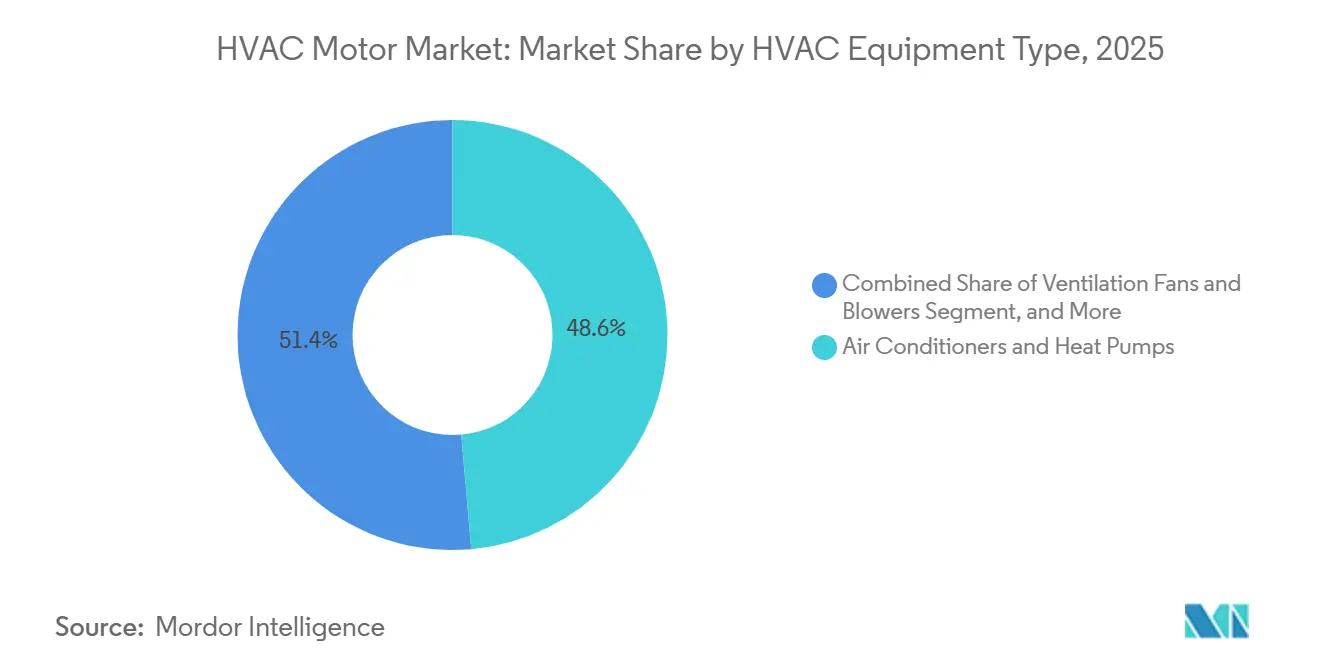

- By HVAC equipment type, air conditioners and heat pumps accounted for 48.61% of the HVAC motor market size in 2025, while chillers and cooling towers are forecast to grow at a 5.41% CAGR through 2031.

- By end-use sector, the commercial segment held 42.78% of market revenue in 2025, while the residential segment is forecast to expand at a 5.32% CAGR through 2031.

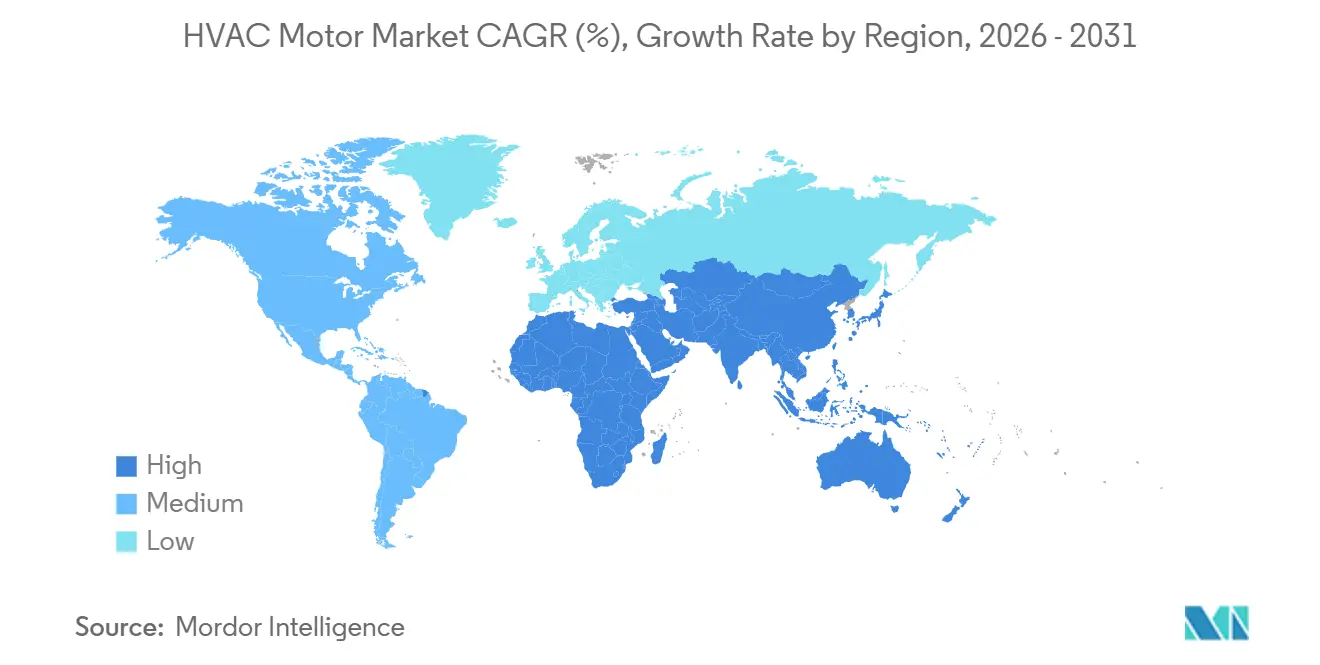

- By geography, Asia-Pacific held 45.54% of global HVAC motor market revenue in 2025, while the Middle East and Africa are projected to grow at a 4.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HVAC Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Motor and Fan Efficiency Standards | +1.5% | Global, with early gains in North America and EU | Short term (≤ 2 years) |

| Heat Pump and Inverter HVAC Adoption | +1.2% | APAC core, spill-over to North America and EU | Medium term (2-4 years) |

| Commercial Retrofit Payback Compression | +0.9% | North America and EU | Short term (≤ 2 years) |

| Data Center Precision Cooling and Fan-Wall Retrofits | +0.8% | Global, with early gains in North America and APAC | Short term (≤ 2 years) |

| Indoor Air Quality and Ventilation Upgrades | +0.5% | North America, EU, APAC | Medium term (2-4 years) |

| Low-GWP Refrigerant Transition Re-Engineering | +0.3% | Global, with early gains in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Motor and Fan Efficiency Standards Drive Compliance-Mandated Upgrades

The US DOE final rule issued in 2025 expanded minimum efficiency standards to expanded scope electric motors in the 0.25-3 HP range, which directly affects the residential and light commercial motor categories widely used across the HVAC motor market, with compliance required from January 1, 2029.[1]U.S. Department of Energy, “Energy Conservation Standards for Expanded Scope Electric Motors - Final Rule,” U.S. Department of Energy, energy.gov DOE said the rule will deliver 8.8 quads of full-fuel-cycle energy savings and USD 21.1-47.5 billion in consumer net present value benefits through 2058, while total manufacturer conversion costs are estimated at USD 360 million. A separate direct final rule already set a June 1, 2027, compliance date for general electric motors in the 1-200 HP range, which closes a major gap that had allowed many larger commercial HVAC motors to remain under weaker standards.[2]U.S. Department of Energy, “Energy Conservation Program, Energy Conservation Standards for Electric Motors - Direct Final Rule,” Federal Register, federalregister.gov These overlapping deadlines matter because the HVAC motor market serves both small residential fan systems and large commercial air-moving equipment, so the compliance burden is reaching a very broad installed base at once. The practical effect is faster retirement of PSC and shaded-pole designs, even in applications where buyers had historically favored low first cost over efficiency improvement. This rule-led reset is giving the HVAC motor market a clearer path toward EC, PMSM, and other variable-speed platforms that already align better with tighter efficiency expectations.

Heat Pump and Inverter HVAC Adoption Expand Variable-Speed Motor Content Per System

Global heat pump sales weakened in 2024 and 2025, but the United States still recorded growth in 2024, and heat pumps continued to outsell natural gas furnaces, which shows that electrified heating remains a durable demand driver for the HVAC motor market in major economies.[3]International Energy Agency, “Global Energy Review 2025,” International Energy Agency, iea.org The IEA also reported that global heat pump sales in 2024 were 27% above 2020 levels, which points to a much larger installed base of inverter-led equipment than the market had just a few years ago. The same outlook indicates that heat pumps will meet 40% of space heating demand in Japan and the United States by 2035, which keeps the medium-term direction intact even after short-term volatility. Each modern inverter-driven heat pump uses a variable-speed compressor motor and several additional brushless or permanent magnet motors for air movement, valve control, and auxiliary pumping, which raises motor content value per system versus older single-speed units. The US EPA Technology Transitions program applied GWP limits to residential air conditioners and heat pumps from January 1, 2025, forcing OEMs to redesign products around A2L refrigerants such as R-32 and R-454B. That redesign work is expanding the role of variable-speed and torque-matched motor platforms across the HVAC motor market, even where near-term equipment shipments have been uneven.

Commercial Retrofit Payback Compression Speeds Forced Upgrade Cycles

The HVAC motor market is also benefiting from shorter retrofit decision cycles in commercial buildings, where higher electricity costs and tighter building performance requirements are making older fixed-speed motors harder to justify. This effect is strongest in offices, healthcare facilities, and other long-hour buildings, where air handlers, VAV systems, and rooftop units can magnify the savings from variable-speed operation over time. ASHRAE Standard 62.1-2025 added mandatory humidity control sequences and updated demand-controlled ventilation logic, which raises the value of motors that can modulate speed more precisely in compliant systems.[4]American Society of Heating, Refrigerating and Air-Conditioning Engineers, “ANSI/ASHRAE Standard 62.1-2025, Ventilation and Acceptable Indoor Air Quality,” ASHRAE, ashrae.org Once ventilation and humidity control become harder requirements, motor replacement becomes part of compliance work rather than a simple maintenance choice. That matters for the HVAC motor market because commercial owners often replace multiple motors in a single project, which supports higher order values than one-for-one residential swaps. The result is a steadier stream of retrofit demand in North America and Europe, even when broader construction conditions remain mixed.

Data Center Precision Cooling Creates Specification-Led Demand

The AI-led data center buildout is creating a part of the HVAC motor market that is less tied to normal commercial construction cycles and far more demanding on performance. Operators are specifying low harmonic distortion, embedded telemetry, long service life, and fan-wall redundancy, which pushes motor requirements upward across precision cooling systems. Regal Rexnord reported USD 735 million in data center E-Pod air-moving system orders in Q4 2025, with initial shipments expected in early 2027, which shows the scale of thermal management demand now moving into contracted backlog. Johnson Controls published a 2026 air-cooled reference design guide for gigawatt-scale AI factories that projected a 32% improvement in annual energy consumption and 50 MW of thermal management gains per campus installation through intelligent use of redundant chillers. Munters commissioned a 10 MW water-cooled EC fan wall system for a Sydney data center in Q1 2026, using 20 units with custom group airflow controls built for continuous 24/7 operation. As these requirements spread, the HVAC motor market is seeing data center buyers set design expectations that then move into wider commercial cooling applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Premium-Efficiency Motors | -0.8% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Control Electronics and Semiconductor Bottlenecks | -0.6% | Global | Short term (≤ 2 years) |

| Installer and Commissioning Gaps for Advanced Retrofits | -0.4% | APAC, Middle East and Africa, South America | Medium term (2-4 years) |

| Refrigerant Transition Timing and Enforcement Uncertainty | -0.3% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Premium-Efficiency Motors Limits Adoption

High first cost remains a real barrier in the HVAC motor market because EC, PMSM, and switched reluctance units still carry a clear premium over standard AC induction motors at similar power ratings. This issue is most visible in new residential construction and other price-sensitive channels where the developer or OEM selects the motor, but the building owner or occupant pays the power bill later. That split weakens the case for lifecycle savings, especially in emerging markets where rebate programs and energy performance contracts are less common. The restraint is especially important because the fastest unit growth is still concentrated in the same high-volume segments that are most exposed to upfront cost pressure. The correction path is more regulatory than economic, since the US DOE expanded-scope motor standards will require covered products to meet tighter efficiency levels from 2029. Until scale, regulation, and procurement learning lower the premium, the HVAC motor market will continue to see slower penetration of top-end designs in cost-led applications.

Control Electronics and Semiconductor Bottlenecks Slow Premium Motor Shipments

Control electronics bottlenecks are constraining the fastest-moving part of the HVAC motor market rather than the whole product mix. EC motors with integrated electronics, inverter-driven compressor motors, and VFD-linked PMSM systems all depend on power semiconductors and control chips that remain harder to source than basic electromechanical parts. This imbalance favors standard AC induction products in the short run because they can still ship with simpler contactor-based architectures and much lower electronics content. The result is selective pressure on the categories that regulators and OEMs are pushing hardest for efficiency gains, which slows transition timing even when underlying demand remains firm. Manufacturers that control drive production internally or secure semiconductor supply earlier are in a better position to protect premium product shipments and customer relationships. For the HVAC motor market, this restraint is manageable, but it still creates uneven availability and longer qualification cycles in the most electronics-heavy applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Regulatory Timelines Speed the Move Beyond Induction

AC induction motors held 63.55% of the HVAC motor market revenue in 2025, keeping the largest position in the HVAC motor market because OEM sourcing habits, installed-base compatibility, and very low unit manufacturing costs still favor them. This scale came more from the legacy installed base than from stronger future positioning, since many buyers still prioritize wiring compatibility and simple field replacement. EC motors are the fastest-growing motor type at a 5.54% CAGR through 2031, as building automation systems increasingly treat motor electronics as operating data points rather than passive components. In the HVAC motor industry, that shift is changing the value of telemetry, modulation accuracy, and integrated controls alongside pure efficiency.

PMSM and brushless DC motors continue to hold the highest-performance positions in VRF compressor drives and precision air handling, where torque density, acoustics, and part-load control support higher prices. ABB launched the world’s first magnet-free IE6 motor certified to ATEX and IECEx for hazardous areas in May 2026, which showed how suppliers are using rare-earth-free high-efficiency platforms to defend premium niches. Switched reluctance motors still face acoustic concerns at partial load, which is limiting broader use even as development work continues.

By Power Rating: Small Motors Stay Central as System Design Changes

Less than 1 HP motors accounted for 58.89% of the HVAC motor market size in 2025 and are anticipated to expand at 5.26% CAGR, reflecting the heavy use of small motors in fan coils, energy recovery ventilators, mini-split indoor units, and plenum fans. Demand in this class is also rising because multi-zone VRF and ductless systems use dedicated motors in each conditioned zone rather than a single large central blower. That architecture multiplies motor count per installed project and keeps the smallest power band central to both replacement and new installations. Within the HVAC motor industry, the more important change is the mix shift inside this band from PSC products toward EC and PMSM designs, which lifts average selling prices even when unit growth is moderate.

The 1-5 HP range is gaining from light commercial air handlers and data center in-row cooling units, where fan arrays replace one larger motor with several smaller ones for redundancy and part-load control. The 5-20 HP band remains important in rooftop units, cooling towers, and larger air handling systems, where efficiency-upgrade payback is easier to justify under long operating hours. ABB reported 9% comparable order growth in its Motion business in Q1 2026, reflecting continued demand from HVAC and buildings end markets, including large-motor applications above 20 HP. The power-rating mix, therefore, shows that the HVAC motor market is growing not only through more equipment sales but also through a redesign of how airflow and cooling loads are distributed across systems.

By HVAC Equipment Type: Cooling Applications Hold Scale While Chillers Gain Speed

Air conditioners and heat pumps held 48.61% of the HVAC motor market size in 2025, making them the largest application pool because they span everything from small residential fan motors to commercial inverter-driven compressor motors. Their position is supported by the move toward heat pump electrification, which adds more variable-speed motor content than legacy single-speed equipment. The IEA outlook indicates that heat pumps will meet 40% of space heating demand in Japan and the United States by 2035, which supports medium-term redesign activity across this installed base. The US EPA refrigerant transition rules also pushed residential air conditioners and heat pumps toward A2L-compatible redesigns from January 1, 2025, which reinforced the need for updated torque profiles and motor controls.

Chillers and cooling towers are the fastest-growing equipment category at a 5.41% CAGR through 2031, and this part of the HVAC motor market is now being shaped as much by data centers as by traditional commercial buildings. Infinitum launched integrated EC fan systems at AHR Expo 2026 that were designed to deliver up to 25% energy savings and keep total demand distortion below 5% across the load range, which shows how precision cooling requirements are influencing motor design. Ventilation fans and blowers are also benefiting from ASHRAE Standard 62.1-2025, which added humidity control and demand-controlled ventilation requirements that favor variable-speed capability. Furnaces and boilers remain a durable but slower-moving base, especially as electrification policy in North America and Europe continues to redirect investment toward heat pump systems.

By End-Use Sector: Commercial Leads in Scale While Residential Gains Mix Value

The commercial sector led with 42.78% of market revenue in 2025, and that HVAC motor market share reflects the high motor count inside air handlers, VAV systems, rooftop units, chiller plants, and precision cooling equipment. Large buildings also create more visible energy savings, which makes old fixed-speed motor populations easier to identify in audits and modernization programs. Regal Rexnord said its Q1 2026 commercial HVAC revenue kept growing mainly because of data center demand in North America and Asia-Pacific, even as residential conditions were softer. The commercial segment, therefore, remains the scale anchor for the HVAC motor market, especially where uptime, monitoring, and system integration matter as much as motor efficiency.

The residential segment is the fastest-growing end-use category at a 5.32% CAGR through 2031, supported by heat pump incentives, rising air conditioning adoption across South and Southeast Asia, and refrigerant-led product redesign. EPA rules under the AIM Act required new residential air conditioning and heat pump equipment to shift toward lower-GWP refrigerants from January 1, 2025, which forced fresh motor matching and control changes at the OEM level. That requirement matters because manufacturers often standardize residential platforms across regions so that a US regulatory change can influence procurement and product architecture well beyond North America. Industrial and institutional users continue to provide stable demand for long-life motors with strict EMC and reliability needs, but residential is where the strongest mix upgrade is now occurring in the HVAC motor market.

Geography Analysis

Asia-Pacific held 45.54% of the HVAC motor market share in 2025, making it the largest regional base for both production and demand. China remains central because its HVAC supply chains connect motors, compressors, electronics, and final equipment assembly at scale, which keeps the region cost-competitive and highly responsive. The regional story is also moving from pure volume toward better product mix, as higher-efficiency inverter systems replace older single-speed equipment across a large installed base. India is adding to this momentum through rising residential air conditioning penetration and a broader expansion of local manufacturing capacity. ABB said India is now tied as its fourth-largest market and outlined planned 2026 manufacturing investment of USD 75 million across its businesses, which underscores the strategic weight of South Asian demand and production.

North America is moving through a rule-led upgrade cycle, with DOE compliance dates in 2027 and 2029 already shaping specification decisions in commercial and residential equipment. The IEA reported that US heat pump sales rose 15% in 2024 and that heat pumps continued to outsell gas furnaces in 2025, even though overall sales volumes weakened during the refrigerant transition. Europe is following a parallel path, where tighter ecodesign expectations and building performance targets are pushing buyers toward premium-efficiency motors and integrated drives. WEG launched its W80 AXgen axial flux motor in October 2025 with IE5+ efficiency and a smaller form factor, showing how suppliers are positioning advanced platforms for efficiency-led applications such as air handlers and blowers.

The Middle East and Africa are the fastest-growing regional segments at a 4.96% CAGR through 2031, supported by GCC megaprojects, high cooling intensity, and rising demand for commercial-grade systems. Extreme ambient temperatures, rapid urban development, and tighter building rules in Gulf markets are sustaining demand for motors built for long operating hours and heavy cooling loads. South America remains a more measured growth market, but Brazil still matters because domestic manufacturing depth supports supply availability and replacement demand across commercial and industrial installations. Overall, the regional mix shows that the HVAC motor market is being supported by a combination of rule-driven upgrades in developed markets and structural cooling demand in faster-growing climates.

Competitive Landscape

The global HVAC motor market is moderately consolidated with a visible global top tier. ABB Ltd., Nidec Corporation, Regal Rexnord Corporation, WEG S.A., and Danfoss A/S form the main competitive pole because they combine motors, drives, and application engineering in a way that fits OEM procurement needs. That breadth matters because buyers increasingly want system performance, digital connectivity, and compliance support, not only a standalone motor. The competitive center of gravity is therefore shifting from basic volume supply toward integrated motion platforms that can improve efficiency, airflow control, and serviceability across the HVAC motor market. This keeps pressure on smaller vendors that lack testing scale, certification depth, or secure access to advanced electronics.

ABB launched the first magnet-free IE6 motor certified to ATEX and IECEx for hazardous areas in May 2026, showing how top suppliers are defending premium segments through specialized efficiency leadership. Danfoss introduced its iC7-HVACR drive portfolio in May 2026 with ultra-low harmonic performance, embedded cybersecurity, and a package that is 20% smaller than earlier generations, which highlights the move toward integrated motor-drive value capture. Nidec said its Maharashtra facility is advancing toward first sample production in Q4 2026 and will target an annual capacity of 6 million compressor and motor units, which shows how capacity expansion in India is supporting both cost efficiency and regional demand capture. These moves show that scale players are competing on technology, manufacturing footprint, and platform integration at the same time.

Venture-backed challengers are also adding pressure, especially firms using PCB-stator or air-core designs that cut weight and pursue strong part-load efficiency in fan systems. Infinitum said its 2026 EC fan systems can deliver up to 25% energy savings and maintain distortion below 5%, while its July 2024 funding extension lifted total Series E funding to USD 220 million, giving it more room to challenge incumbents in air-moving applications. White-space demand remains strongest in commercial retrofits, prefabricated data center cooling modules, and price-sensitive residential channels in Africa and South Asia, where current offers still do not fully cover the range of cost and installation needs. The HVAC motor market, therefore, remains competitive in structure, with strong leaders at the top and a long tail of suppliers underneath them.

HVAC Motor Industry Leaders

Regal Rexnord Corporation

Nidec Corporation

WEG S.A.

ABB Ltd.

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ABB Ltd. launched the world's first magnet-free IE6 Hyper-Efficiency motor certified to ATEX and IECEx for hazardous area use (Zones 1 and 2). Based on synchronous reluctance (SynRM) technology, the motor offers up to 60% lower energy losses versus IE3 equivalents

- May 2026: Danfoss A/S unveiled the iC7-HVACR variable frequency drive portfolio globally, featuring ultra-low harmonic technology, a cybersecure-by-design hardware cryptochip, and a compact form factor 20% smaller than prior-generation drives. The platform targets data center PUE reduction, smart building HVAC, and clean room reliability applications.

- May 2026: Nidec Global Appliance confirmed rapid construction progress at its Aurangabad (Chhatrapati Sambhaji Nagar), Maharashtra, India facility, representing an investment of over USD 120 million and targeting first sample production in Q4 2026 at an eventual annual capacity of 6 million compressor and motor units. The plant is fully verticalized, covering stamping, machining, assembly, motor manufacturing, and electronics.

- February 2026: Infinitum launched its integrated EC fan systems, fan, motor, and variable frequency drive in a single package, at AHR Expo 2026 in Las Vegas. The platform delivers up to 25% energy savings versus traditional fan solutions and maintains TDD below 5% across the full load range without external harmonic filters.

Global HVAC Motor Market Report Scope

The HVAC Motor Market Report is Segmented by Motor Type (AC Induction Motors, Electronically Commutated (EC) Motors, Brushless DC Motors, Permanent Magnet Synchronous Motors, and Switched Reluctance Motors), Power Rating (Less Than 1 HP, 1 HP to 5 HP, 5 HP to 20 HP, and Above 20 HP), HVAC Equipment Type (Air Conditioners and Heat Pumps, Ventilation Fans and Blowers, Furnaces and Boilers, and Chillers and Cooling Towers), End-Use Sector (Residential, Commercial, and Industrial and Institutional), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| AC Induction Motors |

| Electronically Commutated (EC) Motors |

| Brushless DC Motors |

| Permanent Magnet Synchronous Motors |

| Switched Reluctance Motors |

| Less than 1 HP |

| 1 HP to 5 HP |

| 5 HP to 20 HP |

| Above 20 HP |

| Air Conditioners and Heat Pumps |

| Ventilation Fans and Blowers |

| Furnaces and Boilers |

| Chillers and Cooling Towers |

| Residential |

| Commercial |

| Industrial and Institutional |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Motor Type | AC Induction Motors | ||

| Electronically Commutated (EC) Motors | |||

| Brushless DC Motors | |||

| Permanent Magnet Synchronous Motors | |||

| Switched Reluctance Motors | |||

| By Power Rating | Less than 1 HP | ||

| 1 HP to 5 HP | |||

| 5 HP to 20 HP | |||

| Above 20 HP | |||

| By HVAC Equipment Type | Air Conditioners and Heat Pumps | ||

| Ventilation Fans and Blowers | |||

| Furnaces and Boilers | |||

| Chillers and Cooling Towers | |||

| By End-Use Sector | Residential | ||

| Commercial | |||

| Industrial and Institutional | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the HVAC motor market?

The HVAC motor market stands at USD 21.35 billion in 2026 and is forecast to reach USD 26.91 billion by 2031, growing at a CAGR of 4.74% over 2026-2031.

Which motor type leads global revenue in HVAC applications?

AC induction motors led with 63.55% of revenue in 2025 because of legacy OEM sourcing, installed-base compatibility, and lower manufacturing cost.

Which motor technology is growing fastest in HVAC systems?

EC motors are the fastest-growing motor type, with a projected 5.54% CAGR through 2031, supported by efficiency rules and rising BAS integration.

Which equipment category creates the largest pool of motor demand?

Air conditioners and heat pumps held 48.61% of revenue in 2025, making them the largest application group for HVAC motors worldwide.

Why are data centers becoming important for HVAC motor suppliers?

AI-led data center construction is raising demand for precision cooling, fan-wall systems, low distortion performance, and embedded telemetry, which supports higher-value motor platforms.

Which region leads revenue and which region is growing fastest?

Asia-Pacific held 45.54% of global revenue in 2025, while the Middle East and Africa are the fastest-growing region with a projected 4.96% CAGR through 2031.

Page last updated on: