Houston Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

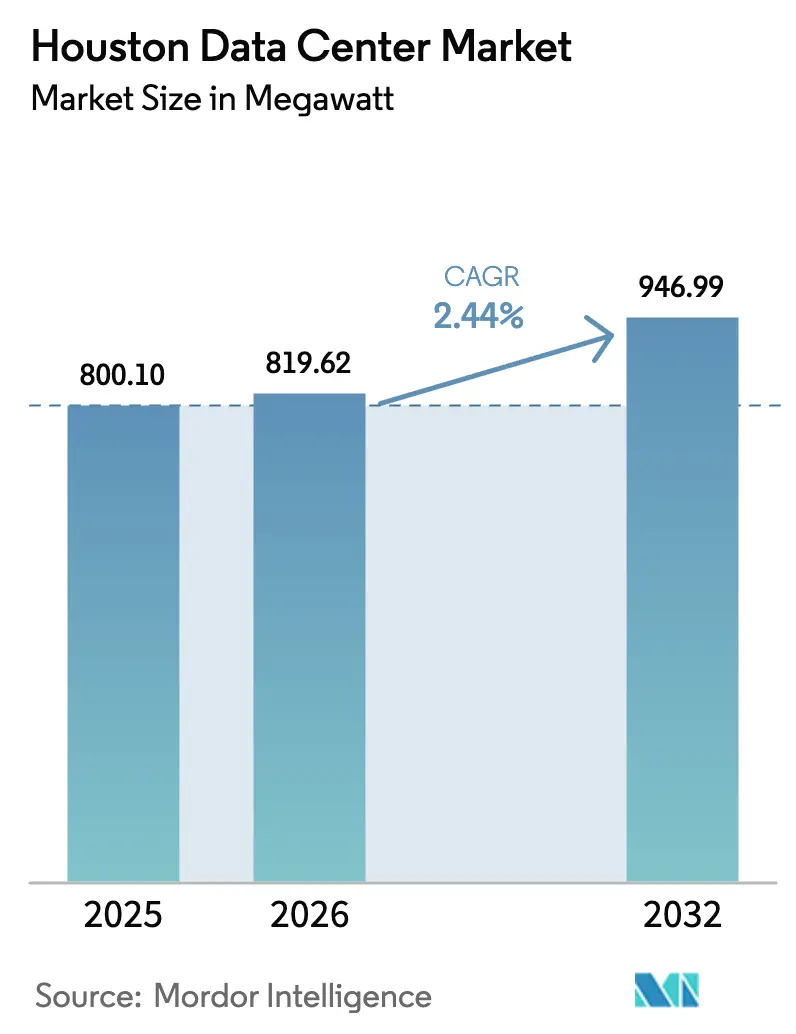

| Base Year Market Size (2025) | 800.10 megawatt |

| Market Volume (2026) | 819.62 megawatt |

| Market Volume (2032) | 946.99 megawatt |

| Growth Rate (2026 - 2032) | 2.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Houston Data Center Market Analysis by Mordor Intelligence

The Houston data center market size was valued at 800.10 MW in 2025 and estimated to grow from 819.62 MW in 2026 to reach 946.99 MW by 2032, at a CAGR of 2.44% during the forecast period (2026-2032). CenterPoint Energy’s interconnection queue jumped from 1 GW to 8 GW in less than one year, signaling demand that already dwarfs installed capacity and pointing to a potential 50% rise in electric load across Houston by 2031.

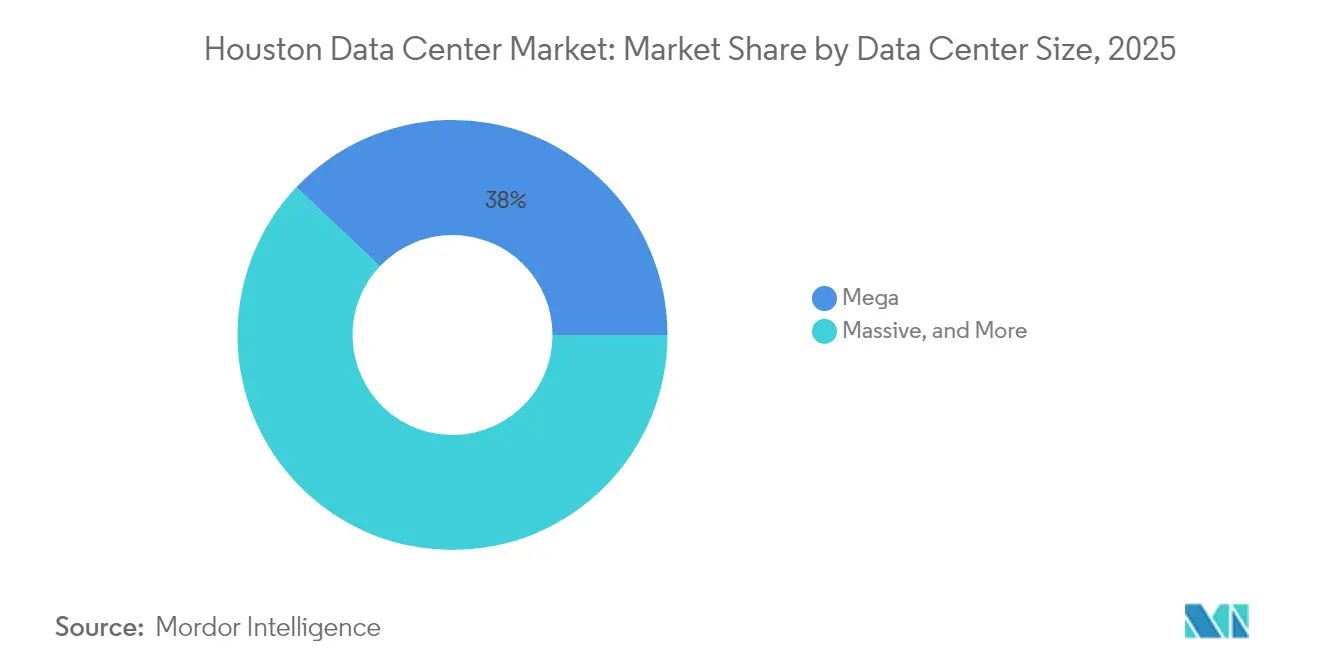

Mega facilities held the dominant 38.4% share of the Houston data center market in 2024, yet Massive facilities are advancing fastest at 10.2% CAGR as both hyperscale and energy-sector HPC projects consolidate into fewer, larger campuses. Market differentiation stems from the city’s 3,600-plus energy organizations that require edge sites for digital-twin analytics, specialized cooling, and elevated power density, all of which separate Houston from traditional hyperscale-centric metros. Competitive intensity is heightening: hyperscale newcomers such as Google invested more than USD 1 billion statewide in 2024 alone, even as established energy-focused operators race to lock in land and power, particularly in West Houston, where land costs jumped 20-25% since 2024.

Key Report Takeaways

- By data center size, Mega campuses captured 37.95% of the Houston data center market share in 2025, while Massive campuses are projected to post the highest growth at 9.65% CAGR through 2032.

- By tier standard, Tier III infrastructure led with 56.60% share of the Houston data center market size in 2025; Tier IV is on track for a 6.42% CAGR to 2032.

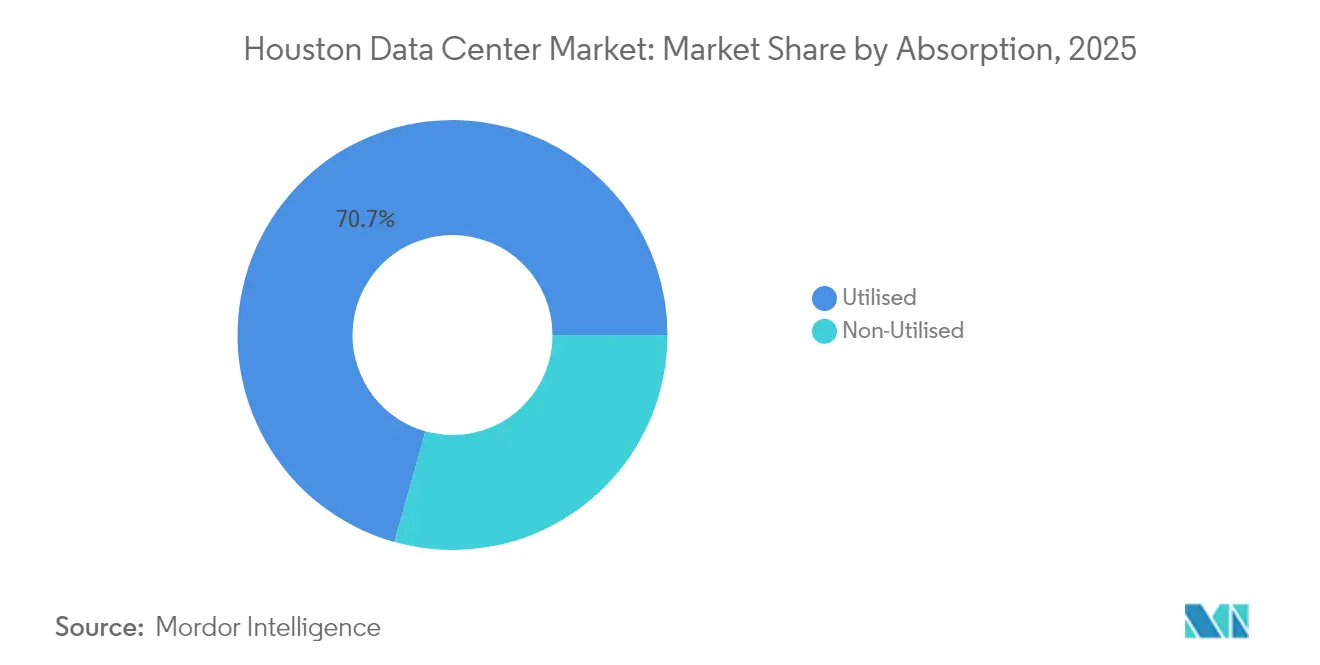

- By absorption, Utilised capacity represented 70.65% of the Houston data center market in 2025, but Non-Utilised inventory is expanding at 8.68% CAGR.

- By hotspot, Downtown CBD retained 45.90% share of the Houston data center market size in 2025, yet West Houston (Katy) is the fastest-growing sub-market at 11.02% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Houston Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast-growing edge-compute demand from Oil and Gas digital twins | +1.20% | Houston Energy Corridor, Gulf Coast refineries | Medium term (2-4 years) |

| Influx of hyperscale cloud campuses (AWS, Google, Microsoft) | +0.90% | Greater Houston metropolitan area | Short term (≤ 2 years) |

| 5G private-network roll-outs at Port Houston and airports | +0.40% | Houston Ship Channel, IAH/HOU airports | Medium term (2-4 years) |

| ERCOT renewable PPAs unlocking green-powered capacity | +0.70% | ERCOT grid region, West Texas wind corridor | Long term (≥ 4 years) |

| Tax incentives under Texas Chapter 313 replacement programs | +0.50% | Texas statewide, Houston enterprise zones | Short term (≤ 2 years) |

| Low-latency financial-trading corridors to Mexico and LATAM | +0.30% | Houston-Mexico border, Eagle Pass fiber crossing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fast-growing Edge-Compute Demand from Oil and Gas Digital Twins

Energy operators are redesigning field architecture around real-time digital-twin analytics that require placing compute nodes close to wells, refineries, and pipelines. Texmark Chemicals’ IoT deployment demonstrated that relocating analytics to the edge lets technicians pre-empt equipment failure and save tens of millions annually through optimized maintenance. ExxonMobil and Halliburton are pursuing subsea fiber and edge-HPC builds to stream sensor data back to Houston with sub-10 ms latency, reinforcing the city’s role as an industrial analytics nerve center [1]TechnipFMC, “Subsea Fiber Optic Solution Selected by ExxonMobil,” technipfmc.com. High-density GPU clusters needed for reservoir modeling raised hardware outlays by roughly 15-20% since 2024, yet operators still prioritize these deployments because each avoided hour of downtime can exceed USD 100,000. The clustering effect of 3,600-plus energy entities allows vendors to pool edge resources, further accelerating Houston data center market growth.

Influx of Hyperscale Cloud Campuses (AWS, Google, Microsoft)

Google’s USD 1 billion Texas build combined with a 375 MW solar PPA from Houston-based Engie paved the way for similar moves by Microsoft and AWS, confirming that hyperscale capital is now firmly aimed at the Houston data center market. Long equipment lead times—electrical switchgear can take up to 24 months—are forcing providers to pre-order gear, inflating cost baselines by USD 200–300 per kW. CyrusOne answered with a USD 12 billion sustainability-linked debt program earmarked for large-scale Texas sites. Hyperscale builders now pay premiums for plots that guarantee immediate power and future substation expansion, a trend expected to keep West Houston land prices climbing.

ERCOT Renewable PPAs Unlocking Green-Powered Capacity

ERCOT’s unique nodal market lets data center owners contract directly with wind or solar farms. Element Critical inked a PPA with NextEra to supply its Houston campus entirely from renewable generation, shaving long-term electricity costs by up to 25% against conventional tariffs. Digital Realty lifted its renewable mix to 70% via 160,000 MWh of new solar in Dallas[2],Wylie Wong, “Digital Realty Boosts Renewable Energy Supply,” datacenterknowledge.com while Ørsted’s PPA with Google showcased another 300 MW of wind capacity dedicated to data center loads. These deals lower cost of power to USD 25–35 per MWh, helping attract sustainability-focused tenants and intensifying competition among developers who can guarantee carbon-free energy.

Tax Incentives Under Texas JETI Act

Texas replaced the expiring Chapter 313 regime with the Jobs, Energy, Technology and Innovation (JETI) Act, offering 50% property-tax relief—escalating to 75% within Opportunity Zones—for projects above 100,000 sq ft that create at least 20 high-wage jobs. Added sales-tax exemptions on servers and electricity can strip USD 15–25 million from a 50 MW build’s lifetime cost [3]Texas Comptroller, “Qualifying Data Centers FAQ,” comptroller.texas.gov. Clearer rules and a shorter approval cycle minimize regulatory risk, prompting operators to commit earlier and at larger scale, directly bolstering the Houston data center market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising power-grid congestion in West Houston | -0.80% | West Houston (Katy), Energy Corridor | Short term (≤ 2 years) |

| Hurricane and flood-zone insurance cost premiums | -0.60% | Harris County, Gulf Coast floodplains | Medium term (2-4 years) |

| Talent scarcity for high-density liquid-cooling operations | -0.40% | Greater Houston metropolitan area | Medium term (2-4 years) |

| Water-use restrictions during Gulf-Coast drought periods | -0.70% | Texas Gulf Coast, ERCOT region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Power-Grid Congestion in West Houston

ERCOT congestion charges ballooned five-fold between 2016 and 2022, reflecting transmission bottlenecks that add USD 10–15 per MWh to spot prices in West Houston [4].ERCOT, “Congestion Cost Savings Test,” ercot.com CenterPoint invested USD 285 million on the Brazos Valley Connection line, but its own forecast shows a 50% load surge by 2031, indicating that line additions will trail demand. Prefabricated substation packages now cost 30% more than in 2024 due to commodity inflation, limiting rapid power roll-outs. These dynamics make power the gating factor on campus scale rather than land or fiber, constraining near-term Houston data center market growth in the west.

Hurricane and Flood-Zone Insurance Cost Premiums

Commercial-property insurance in Texas climbed 24% above the national norm and is on pace to double by 2030 because of intensifying Gulf storms. FEMA’s Risk Rating 2.0 could lift Harris County flood-premiums by 75%, which for a 50 MW campus adds USD 2–4 million in annual OPEX. Operators responded by elevating floors and installing submersible pumps, measures that add USD 500–800 per kW in capex but remain cheaper than prolonged downtime. While Tier III and Tier IV facilities historically weathered hurricanes without outage, higher insurance and construction premiums dampen ROI for new entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Consolidation Around Massive Campuses

Mega campuses commanded 37.95% of 2025 installed power, underscoring a pivot toward large contiguous footprints that accommodate multi-tenant hyperscale halls and energy-sector HPC cages. Massive campuses, however, surface as the volume story, advancing at 9.65% CAGR thanks to efficiencies that cut unitary OPEX by roughly 15% compared with standalone Mega builds. The Houston data center market size for Massive facilities is projected to surpass 42.3 MW by 2032, and Data Foundry’s 60 MW Houston 2 campus illustrates how high-density racks (≥50 kW) coupled with 185 mph wind-rated envelopes entice petrochemical users seeking flood resilience. Land scarcity downtown pushes operators to suburban mega-sites where lower real-estate cost offsets higher transmission-upgrade spend. Medium and Small footprints serve edge hubs near refineries, but their Houston data center market share is expected to decline as digital-twin workloads consolidate into central locations that offer advanced liquid cooling.

Second-tier campuses function as testbeds for new vendors gauging Houston demand before leveling up to Massive investments. Skybox Houston I, a Large-class campus on a 20-acre private tract with 300 MVA potential, typifies the step-up model favored by energy clients anxious for bespoke security. Construction-material inflation lifted chilled-water plant costs by USD 300–400 per kW since 2024, yet operators still green-light these builds because each new 10 MW hall can absorb a single cloud anchor. Over the forecast period, Massive facilities are likely to secure the highest Houston data center market share gains as hyperscalers co-locate AI training clusters with energy-industry partners.

By Tier Standard: Reliability Arms Race

Tier III remained the workhorse at 56.60% share of 2025 installed load, balancing redundancy with cost for enterprise ERP, seismic-data archives, and retail colocation suites. The Houston data center market size contribution from Tier IV, however, is rising as AI inference and high-frequency trading require zero unplanned downtime. The Houston data center market share for Tier IV builds will expand beyond 15.40% by 2032 if current 6.42% CAGR holds. CyrusOne’s climate-neutral DFW10 campus, though sited in Dallas, demonstrates tactics being mirrored in Houston: on-site generation and dual utility feeds buttress uptime while satisfying green-energy mandates. Capital premium for Tier IV currently sits 40–50% above Tier III, yet GPU farm operators accept the surcharge given hourly downtime costs.

Meanwhile, Netrality’s 1301 Fannin site typifies Tier III excellence by layering flood-plain avoidance, multi-carrier meet-me rooms, and Energy Star certification into a downtown skyscraper retro-fit. Customers upgrading from Tier II previously valued low cost but now re-evaluate after calculating out-age risk. As liquid-cooling spreads across floors, personnel certified for high-density operations will command wage premiums, potentially tightening the local labor pool. Over time, a two-tier ecosystem should persist: Tier III for broad workload diversity and Tier IV for latency-sensitive AI workloads critical to both energy trading and industrial automation.

By Absorption: Speculative Shells Signal Confidence

Utilised capacity represented 70.65% of Houston’s total power draw in 2025, evidence of robust back-fill of newly launched halls. The Houston data center market size for Non-Utilised space is growing 8.68% CAGR as developers lock in steel, generators, and switchgear early to shorten ramp-to-revenue. Stream Data Centers’ pre-built shells in The Woodlands illustrate how speculative frameworks secure hyperscale anchors that demand ready-for-fitout halls on day one. Carrying costs rise during lease-up, but Houston’s energy-centric growth profile emboldens developers to maintain inventories larger than those seen in Chicago or Silicon Valley.

Within active halls, hyperscale colocation soaks up the bulk of MWs; wholesale suites follow, with retail cages catering to smaller oilfield-services firms seeking 50–200 kW footprints. Digital Realty’s 50,000 sq ft wholesale blocks offer cross-connect economies to pipeline-monitoring SaaS providers. Construction inputs such as rebar and cement rose USD 100–150 per sq ft after 2024, nudging break-even occupancy to the 30–35% range, yet most Houston developers report leasing velocity that reaches that mark within 18 months—an indicator of sustained Houston data center market momentum

Geography Analysis

Downtown CBD possessed 45.90% of active power in 2025, anchored by interconnection density and proximity to finance trading floors. However, West Houston (Katy) leads on growth at 11.02% CAGR because it offers 100-acre parcels next to energy-corridor HQs where GIS seismic teams demand proximity. The Houston data center market size allocated to Katy is forecast to rival downtown by 2032 despite grid constraints that currently cap hall size. CenterPoint’s grid upgrades may lag the demand curve, pushing developers to supplement utility feeds with gas turbines or fuel-cell farms until ERCOT adds new transmission.

Rest-of-Houston sites host edge nodes at refineries or near Port Houston; EdgeConneX employs a tri-fiber topology for sub-5 ms latency to process-control PLCs along the Ship Channel. Land cost differentials—USD 15–20 per sq ft suburban versus USD 25–30 downtown—create strategic arbitrage for operators building hybrid footprints. Over the outlook, West Houston is expected to double its Houston data center market share even as downtown maintains critical mass for carrier hotels and meet-me rooms.

Competitive Landscape

Houston’s provider mix blends global REITs—CyrusOne, Digital Realty, and Equinix—with energy-specialized independents such as Data Foundry, Skybox, Stream, and Element Critical. The top five operators accounted for roughly 50 % of 2024 installed power, indicating a moderately concentrated scene that still offers room for upstarts. CyrusOne’s USD 12 billion debt round and 190 MW DFW10 blueprint illustrate the scale at which incumbents now compete. Digital Realty advanced its green credentials to secure enterprise renewals, while Equinix leverages Platform Equinix inter-metro backbones to sell high-performance routes for seismic interpretation.

Specialists vie on high-density liquid cooling, modular power pods, and hardened envelopes rated for 500-year flood plains. Stream Data Centers markets 300 MVA ready-for-operation Katy land, and Skybox’s military-grade campus courts LNG exporters seeking near-plant HPC. Cross-border routes emerged as a differentiator: MDC Data Centers’ Eagle Pass fiber crossing slices latency to Querétaro, vital for energy hedging desks. Rising equipment costs reward companies with bulk-buy leverage; players under 20 MW pipelines may struggle to obtain transformers amid an 18-month backlog, accelerating M and A chatter as smaller groups search for scale efficiencies. Sustainability commitments also shape competition: Element Critical’s 100% renewable power pledge and Calpine-CyrusOne on-site generation models position them favorably with ESG-minded customers.

Houston Data Center Industry Leaders

Digital Realty Trust, Inc.

DataBank

Equinix Inc.

Cogent

Netrality Data Centers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: CyrusOne revealed a 190 MW climate-neutral data center (DFW10) slated for Q4 2026 commissioning.

- July 2025: CyrusOne secured USD 12 billion in sustainability-linked debt, earmarking USD 7.9 billion for U.S. builds.

- June 2025: ENGIE and Meta executed a 200 MW renewable-energy deal to supply future Texas campuses.

- May 2025: RWE signed two 15-year PPAs with Microsoft for 446 MW of Texas wind generation.

- April 2025: CyrusOne began construction on the 70 MW DFW7 campus in Fort Worth.

Houston Data Center Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The Houston data center market is segmented by DC size (small, medium, large, massive, mega), by tier type (tier 1&2, tier 3, tier 4), by absorption (utilized [colocation type [retail, wholesale, hyperscale], end user [cloud & IT, telecom, media & entertainment, government, BFSI, manufacturing, e-commerce]], Non-Utilized). The market sizes and forecasts are provided in terms of value (MW) for all the above segments.

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User Industry | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End Users | ||

| Downtown CBD |

| West Houston (Katy) |

| Rest of Houston |

| By Data Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilised | ||

| Utilised | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User Industry | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End Users | |||

| By Hotspot | Downtown CBD | ||

| West Houston (Katy) | |||

| Rest of Houston | |||

Key Questions Answered in the Report

How large is current installed capacity in the Houston data center market?

Total installed IT load reached 819.62 MW in 2026 and is forecast to climb to 946.99 MW by 2032.

Which sub-market is expanding fastest within greater Houston?

West Houston (Katy) is advancing at an 11.02% CAGR through 2032 due to abundant land and proximity to energy-sector HQs.

What incentives does Texas offer new data-center builds?

The JETI Act grants 50–75% property-tax abatements plus sales-tax exemptions on equipment and electricity for qualifying projects.

How are operators addressing Houston’s grid-congestion challenge?

Developers deploy onsite generation, secure long-lead switchgear early, and collaborate with CenterPoint on new substations.

Why is Tier IV adoption rising in Houston?

AI, high-frequency trading, and industrial digital-twin workloads require near-zero downtime, boosting demand for Tier IV redundancy.

What share of capacity is currently utilized versus pre-built shell?

Utilised halls account for 70.65% of installed power, while Non-Utilised inventory grows 8.68% CAGR to capture future hyperscale demand.

Page last updated on: